Los Angeles Data Center Market Size and Share

Market Overview

| Study Period | 2021 - 2032 |

|---|---|

| Forecast Data Period | 2026 - 2032 |

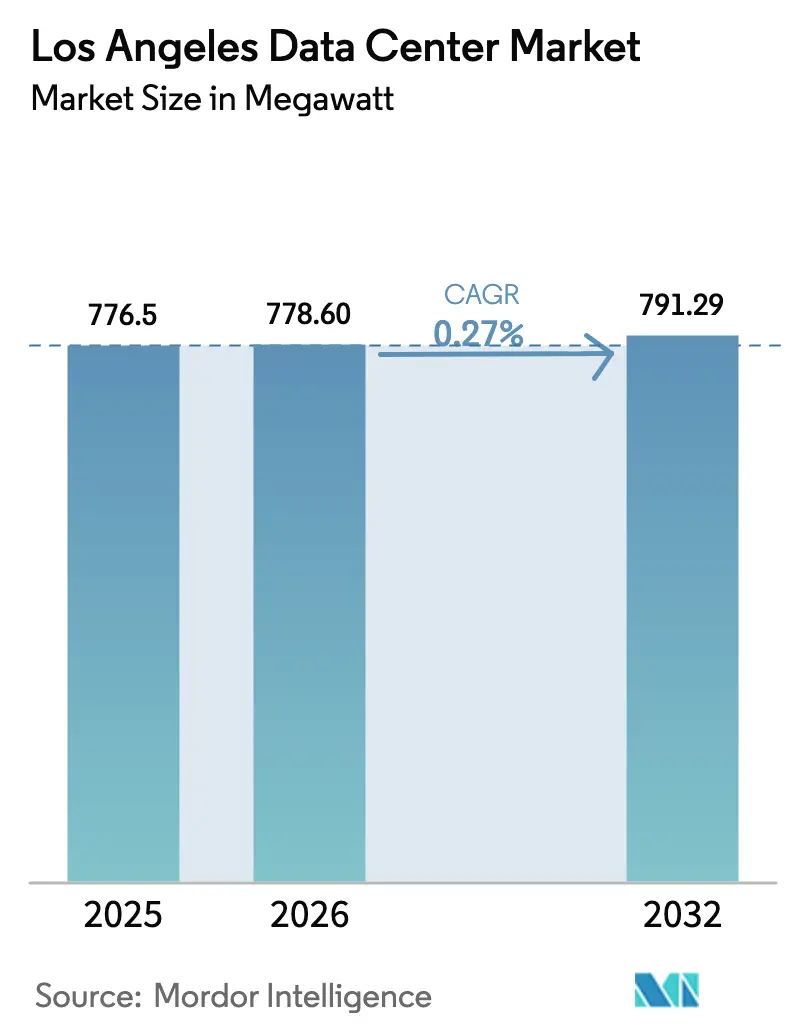

| Base Year Market Size (2025) | 776.5 megawatt |

| Market Volume (2026) | 778.60 megawatt |

| Market Volume (2032) | 791.29 megawatt |

| Growth Rate (2026 - 2032) | 0.27% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Los Angeles Data Center Market Analysis by Mordor Intelligence

The Los Angeles data center market size was valued at 776.5 MW in 2025 and estimated to grow from 778.6 MW in 2026 to reach 791.29 MW by 2032, at a CAGR of 0.27% during the forecast period (2026-2032). This tepid headline growth contrasts sharply with the city’s strategic role as a trans-Pacific interconnection hub and as North America’s entertainment capital, two factors that continue to anchor demand even when capacity additions remain modest. AI-centric hyperscale requirements, entertainment rendering workloads, and West-Coast subsea cable landings are driving incremental power purchases, while scarce 230 kV transmission interconnects, seismic-design premiums, and lengthy power-delivery queues restrain large new builds. Operators with legacy downtown footprints leverage existing utility allocations and dense carrier ecosystems to out-compete greenfield entrants in emerging suburban clusters. Together, these countervailing forces underpin a market that grows slowly in aggregate capacity yet remains critical for latency-sensitive workloads traversing both domestic and Asia-Pacific routes.

Key Report Takeaways

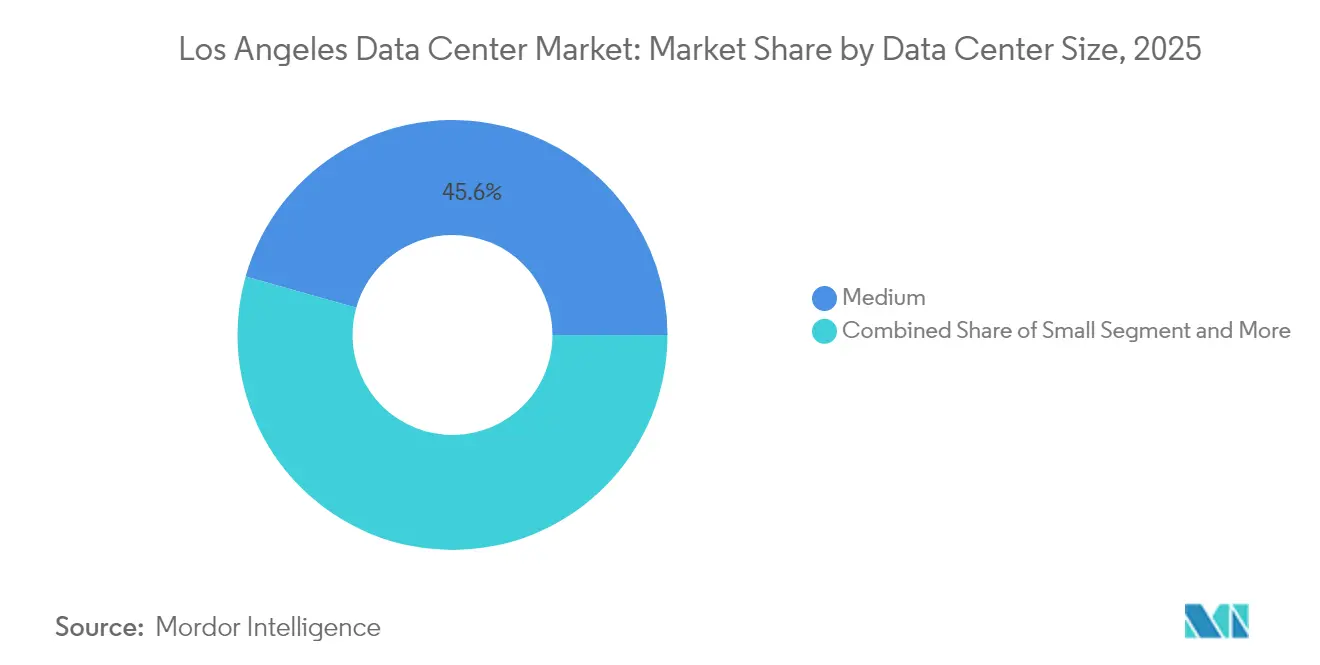

- By data center size, 20–50 MW facilities led with 45.62% of Los Angeles data center market share in 2025, whereas mega-scale deployments above 50 MW are forecast to expand at a 0.96% CAGR through 2032.

- By tier standard, Tier III infrastructure dominated with 63.25% share of the Los Angeles data center market size in 2025, while Tier IV facilities are projected to advance at a 2.08% CAGR to 2032.

- By absorption, retail colocation accounted for 57.65% of the Los Angeles data center market size in 2025; hyperscale utilization is rising at a 2.37% CAGR through 2032.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Los Angeles Data Center Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| AI-centric hyperscale tranche demand | +0.8% | Global, concentrated in LA metro | Medium term (2–4 years) |

| Surging film-render and streaming workloads | +0.4% | Los Angeles Basin, Hollywood corridor | Short term (≤ 2 years) |

| West-Coast subsea cable landings (Hawaiki Nui, CAP-1) | +0.3% | Pacific-Rim connectivity, LA landing points | Long term (≥ 4 years) |

| 400 MW Southern CA utility-scale solar + BESS PPAs | +0.2% | Southern California Edison territory | Medium term (2–4 years) |

| Revitalization of under-utilized Hollywood sound stages into edge DCs | +0.1% | Hollywood, Burbank, Culver City | Short term (≤ 2 years) |

| State “L.A. Clean Grid 2045” incentives for on-site micro-nuclear SMRs | +0.1% | LADWP service territory | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

AI-centric hyperscale tranche demand

Liquid-cooled racks exceeding 50 kW are now standard in new builds as GPU training clusters reshape facility design parameters. Digital Realty introduced direct liquid cooling across its Los Angeles footprint in May 2024, eliminating the thermal limitations of legacy CRAC systems.[1]Swinhoe Dan, “Digital Realty Launches Direct Liquid Cooling Offering,” Data Center Dynamics, datacenterdynamics.com Equinix followed with a USD 15 billion joint venture that allocates more than 1.5 GW of hyperscale power to key U.S. metros, including Los Angeles. Procurement lead times reinforce first-mover advantages: Cooling Distribution Units now average 25 weeks, constraining late entrants from scaling at the pace demanded by AI tenants. Combined, these factors elevate the Los Angeles data center market as an AI infrastructure linchpin for workloads bridging North America and Asia-Pacific.

Surging film-render and streaming workloads

Netflix’s cloud-native Media Production Suite handles up to 700 TB per title, eliminating physical media and requiring edge nodes close to Hollywood studios.[2]Netflix Technology Blog, “Globalizing Productions with Netflix’s Media Production Suite,” netflixtechblog.com Warner Bros. committed USD 500 million to expand 16 soundstages—proof that studio operators view local compute as indispensable. Gaming adds parallel demand; Riot Games’ esports platform moves 3.2 PB in under 30 minutes during tournament play, reinforcing latency-sensitive traffic patterns. These workflows translate into sustained power draws for edge nodes within the Los Angeles Basin.

West-Coast subsea cable landings (Hawaiki Nui, CAP-1)

The JUNO cable will deliver 350 Tbps from Japan to Los Angeles, while Southern Cross NEXT links the city directly to Sydney at 72 Tbps, both raising the metro’s value as a Pacific gateway. The municipal Trans-Pacific Telecommunications Cable Hub authorizes four additional landings at Dockweiler State Beach, ensuring long-term path diversity. Elevated east-west traffic cements the Los Angeles data center market as the principal U.S. interconnection site for Asia-bound traffic.

400 MW Southern CA utility-scale solar + BESS PPAs

The Compass Battery Energy Storage Project provides 250 MW/1,000 MWh of four-hour storage, enabling dispatchable capacity that data center operators can contract under resource-adequacy agreements. LADWP’s LA100 Plan adds 400 MW of PV and 1,200 MWh of batteries, positioning renewable PPAs as a hedge against escalating spot power costs. State microgrid incentives totaling USD 200 million further sweeten on-site generation economics, especially for suburban campuses with excess land.

Restraints Impact Analysis*

| RESTRAINTS | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Scarce 230 kV transmission interconnects within LA Basin | −0.6% | Los Angeles Basin, downtown core | Medium term (2–4 years) |

| Rising seismic-design CAPEX premiums (Zone 4b) | −0.4% | Seismic Zone 4b areas, LA County | Long term (≥ 4 years) |

| Lengthy LADWP and SCE power-delivery queue (48-60 months) | −0.3% | LADWP and SCE service territories | Short term (≤ 2 years) |

| Shortage of Tier IV-certified technicians and electricians | −0.2% | Regional, affecting all major metros | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Scarce 230 kV transmission interconnects within LA Basin

California ISO lists 28.4 GW of renewable projects already delayed by transmission constraints, a backlog mirrored in data-center queue positions.[3]California ISO, “2024 Transmission Plan Deliverability Allocation Report,” caiso.com LADWP’s McCullough-Victorville upgrades add only 475 MW by 2029, insufficient for the sub-gigawatt requests lodged by hyperscale aspirants. As a result, downtown expansions depend increasingly on networked diesel or gas-turbine generators for standby megawatts, inflating capital intensity and complicating air-quality permitting.

Rising seismic-design CAPEX premiums (Zone 4b)

California Building Code Zone 4b compels base-isolation systems, viscous dampers, and heavier steel weights. Data Center Knowledge estimates seismic provisions can add 15% to downtown project budgets. Operators scale up floor plates to dilute fixed-cost premiums, which helps explain why many new bids exceed 50 MW even though the Los Angeles data center market grows slowly in net capacity.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Data Center Size: Mega-scale Drives Future Capacity

Facilities exceeding 50 MW account for the fastest-growing slice of the Los Angeles data center market, expanding at a 0.96% CAGR to 2032, although mid-range Medium deployments still led with 45.62% of 2025 installed capacity. The Los Angeles data center market size for mega-scale builds registered an incremental 60 MW in 2024 after Prime Data Centers energized its 33 MW Vernon campus, the single-largest addition of the year. Edge nodes below 5 MW persist for specialized rendering, but their aggregate footprint remains less than 5% of capacity, underscoring a bifurcated demand curve favoring either hyperscale or highly targeted micro-edge projects.

Economies of scale drive this gravitation toward larger blocks because seismic-design premiums and protracted utility queues dilute unit costs when amortized over higher IT loads. Hyperscale operators also prefer campus-style layouts that support future expansions under a single permit umbrella, mitigating the risk of interconnect moratoria. Santa Clarita Valley, once a secondary location, now attracts master-planned campuses upwards of 80 MW as land and water availability exceed what downtown parcels can provide. Consequently, the Los Angeles data center market continues to consolidate incremental megawatts into fewer, but markedly larger, footprints.

By Tier Standard: Tier IV Gains Mission-Critical Traction

Tier III remained the workhorse in 2025, holding 63.25% of Los Angeles data center market share, yet Tier IV footprints are forecast to record a 2.08% CAGR to 2032. The Los Angeles data center market size for Tier IV builds rose by 8 MW in 2024 as CoreSite brought LA2 Phase 3 online, incorporating 2N utility feeds and N+1 chilled-water plants. Sector-specific compliance—FINRA, FedRAMP, and PCI-DSS—pushes financial and healthcare tenants toward Tier IV environments where concurrent maintainability is guaranteed.

Operational headwinds remain: a regional shortage of Tier-IV-certified technicians threatens uptime SLAs, fueling premium wage inflation that outpaces national averages. Training partnerships with IBEW and the County of Los Angeles aim to alleviate the gap, but those programs will not materially boost capacity until late-2027. Despite staffing constraints, demand outstrips supply, and operators able to demonstrate 99.995% availability continue to command double-digit price premiums over Tier III equivalents.

By Absorption: Hyperscale Momentum Accelerates

Retail colocation still captured 57.65% of 2025 utilized capacity, yet hyperscale tenants are adding square footage faster, growing at 2.37% CAGR through 2032. Hyperscale demand consumed 20 MW of fresh power in 2024 alone, largely within Digital Realty and Equinix campuses that can hand over 2–5 MW suites under single-tenant models. Because Los Angeles data center market vacancy sits below 3%, pre-leasing commitments often precede construction by 18 months, reinforcing first-mover advantages for incumbents with shovel-ready expansions.

Wholesale blocks serve enterprises bridging on-premises kit with public cloud platforms, a middle-ground absorption path expected to plateau as hybrid-cloud maturity increases. Non-utilized space, meanwhile, remains minimal; speculative builds rarely remain idle longer than two quarters due to acute absorption from media rendering bursts and AI experimentation labs. Overall, hyperscale demand sets the cadence, dictating both construction schedules and power-procurement strategies across the Los Angeles data center industry.

Geography Analysis

Downtown Los Angeles continues to house 42.55% of installed capacity, a consequence of One Wilshire’s 295-network meet-me room that underpins the region’s carrier-hotel status. Yet seismic premiums, land scarcity, and 230 kV congestion are pushing new-build activity toward northern suburbs. Santa Clarita Valley leads with a projected 2.03% CAGR, underpinned by greenfield parcels conducive to multi-building campuses and adjacency to renewable corridors capable of delivering 100 MW blocks under long-term PPAs.

Urban densification persists in limited downtown parcels. Digital Realty’s planned 13-story tower at 727 S. Grand Avenue will add 480,000 sq ft of server space and leverage dual LADWP substations in a stacked-data-hall design. Such vertical builds illustrate how operators reconcile core-metro latency requirements with land constraints, albeit at elevated per-MW costs relative to single-story suburban variants.

Southern nodes like Vernon capitalize on industrial zoning and easier access to 66 kV feeders, evidenced by Prime Data Centers’ 33 MW go-live in November 2024. Meanwhile, coastal sites near Dockweiler State Beach prepare for new cable landings, adding beach-manhole real estate that could spawn micro-edge facilities tailored to subsea backhaul termination. Collectively, these geographies form a hub-and-spoke topology in which downtown remains the network core while suburban spokes absorb the bulk of incremental megawatts.

Competitive Landscape

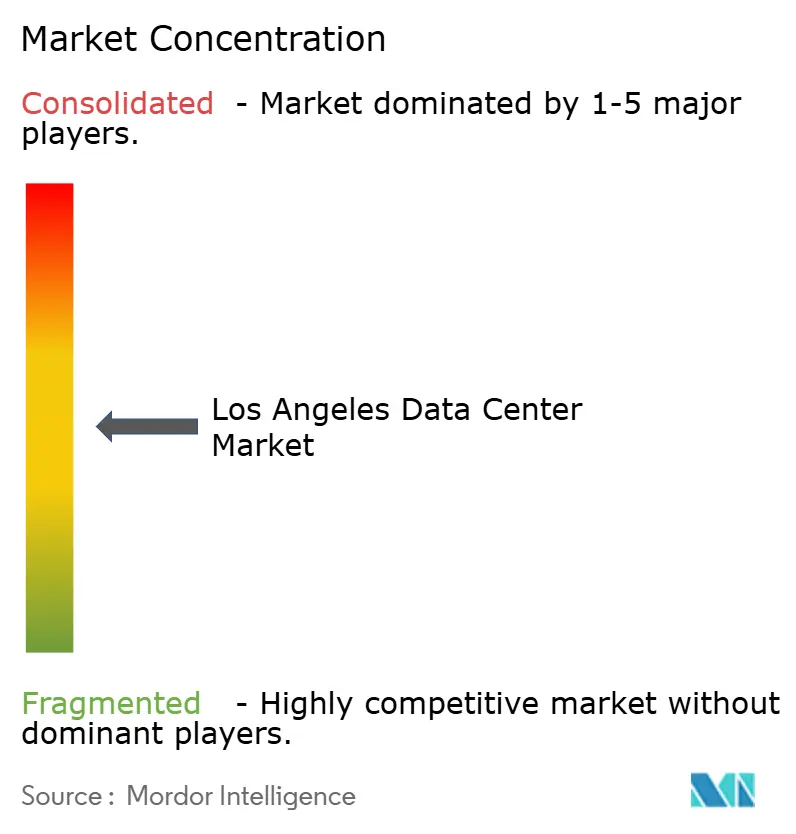

Los Angeles displays moderate consolidation; the top five operators control roughly 68% of commissioned power, placing the market at a concentration score of 6. Incumbents Equinix, Digital Realty, and CoreSite exploit legacy interconnect ecosystems and entrenched power contracts, enabling rapid sell-outs of new phases. Equinix’s xScale rollout earmarks additional Los Angeles acreage for build-to-suit hyperscale pods, while Digital Realty leverages its global 3,000 MW portfolio to cross-sell hybrid deployments.

New entrants pursue suburban parcels; Prime Data Centers’ Vernon campus and Edge Centres’ acquisition of QuadraNet exemplify this outer-ring strategy. Competitive levers pivot on securing megawatt-class renewable PPAs, deploying liquid cooling, and obtaining Tier IV certifications faster than peers constrained by labor shortages. Technology upgrades are equally decisive: operators investing in 400G-ready DWDM backbones and campus microgrids differentiate themselves when courting AI tenants.

M&A remains active. Vantage Data Centers raised USD 13 billion in January 2025 for U.S. expansion, while DataBank secured USD 2 billion to proliferate edge campuses. Private-equity appetite suggests further roll-ups, although strict earthquake codes and utility bottlenecks temper speculative over-builds, sustaining pricing discipline across the Los Angeles data center market.

Los Angeles Data Center Industry Leaders

Digital Realty Trust, Inc.

DataBank

Equinix Inc.

CoreSite

Cogent

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Vantage Data Centers secured record USD 13 billion in incremental funding driven by AI and cloud adoption, positioning the company for aggressive expansion across key markets including Los Angeles.

- January 2025: DataBank completed a USD 2 billion equity round led by DigitalBridge, with proceeds targeted for new campuses across 27 markets, including edge facilities in metropolitan Los Angeles.

- November 2024: Prime Data Centers opened its hyperscale facility in Vernon, California, the largest single capacity addition to the metro.

- October 2024: Equinix announced a USD 15 billion joint venture with GIC and CPP Investments to add 1.5 GW of hyperscale power across U.S. markets, Los Angeles included.

Los Angeles Data Center Market Report Scope

A data center is a physical room, building, or facility that holds IT infrastructure used to construct, run, and provide applications and services and store and manage the data connected with those applications and services.

The Los Angeles Data Center Market is segmented by DC Size (Small, Medium, Large, Massive, Mega), Tier Type (Tier 1&2, Tier 3, Tier 4), Absorption (Utilized (Colocation Type (Retail, Wholesale, Hyperscale), End User ( Cloud & IT, Telecom, Media & Entertainment, Government, BFSI, Manufacturing, E-Commerce)), and Non-Utilized).

The market sizes and forecasts are provided in terms of value (MW) for all the above segments.

| Small |

| Medium |

| Large |

| Hyperscale |

| Tier I and II |

| Tier III |

| Tier IV |

| Non-Utilised | ||

| Utilised | By Colocation Type | Retail |

| Wholesale | ||

| By End-User Industry | Cloud Service Providers | |

| Media and Entertainment | ||

| Manufacturing | ||

| Telecom | ||

| BFSI | ||

| E-commerce | ||

| Government | ||

| Other End User | ||

| By Data Center Size | Small | ||

| Medium | |||

| Large | |||

| Hyperscale | |||

| By Tier Standard | Tier I and II | ||

| Tier III | |||

| Tier IV | |||

| By Absorption | Non-Utilised | ||

| Utilised | By Colocation Type | Retail | |

| Wholesale | |||

| By End-User Industry | Cloud Service Providers | ||

| Media and Entertainment | |||

| Manufacturing | |||

| Telecom | |||

| BFSI | |||

| E-commerce | |||

| Government | |||

| Other End User | |||

Key Questions Answered in the Report

How large is the Los Angeles data center market in 2026?

Installed capacity is 778.6 MW, edging toward 791.29 MW by 2032 at a 0.27% CAGR.

Which sub-market is growing fastest in Los Angeles?

Santa Clarita Valley leads with a projected 2.03% CAGR through 2032, thanks to land availability and renewable-energy proximity.

What segment commands the largest share of capacity?

2050 MW facilities hold 45.62% of installed capacity, making mid-range deployments the dominant footprint.

Why are Tier IV facilities gaining traction?

AI, BFSI, and healthcare workloads demand 99.995% uptime, pushing Tier IV capacity to a forecast 2.08% CAGR through 2032.

How does AI affect new data-center builds in Los Angeles?

AI workloads require liquid cooling and > 50 kW rack densities, accelerating hyperscale demand and lengthening equipment lead times.

What regulatory factors most constrain expansion?

Scarcity of 230 kV interconnects and LADWP power-delivery queues of up to 60 months delay greenfield projects inside the Los Angeles Basin.

Page last updated on: