Household Beauty Appliances Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

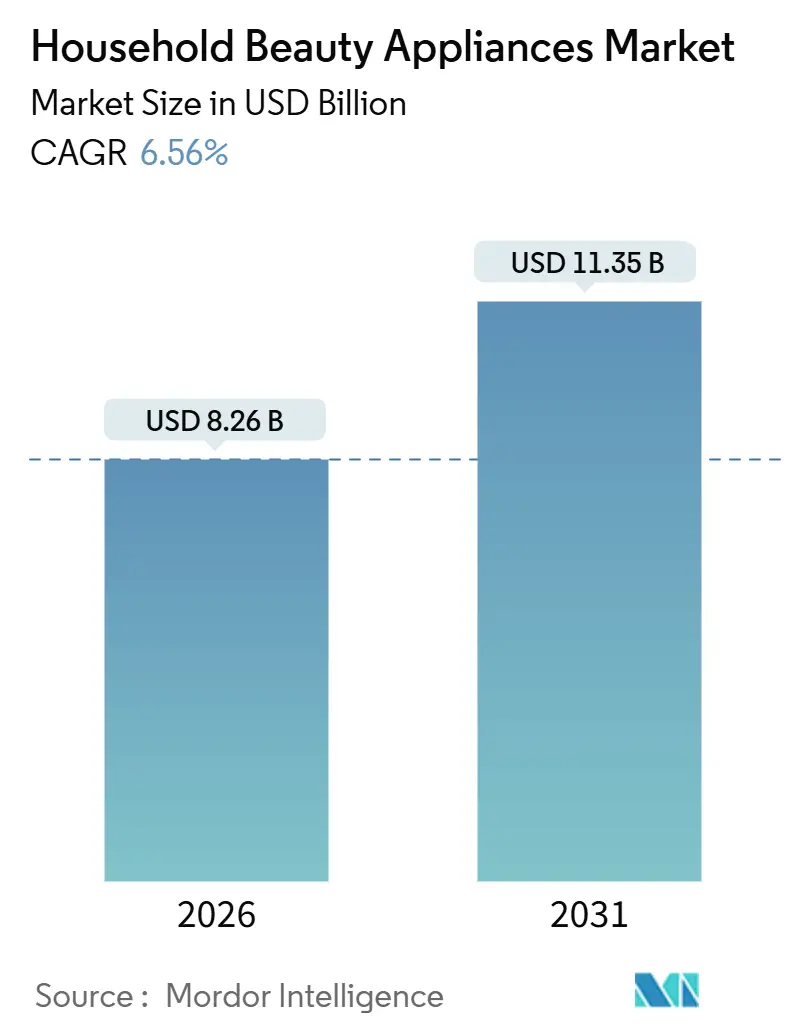

| Market Size (2026) | USD 8.26 Billion |

| Market Size (2031) | USD 11.35 Billion |

| Growth Rate (2026 - 2031) | 6.56% CAGR |

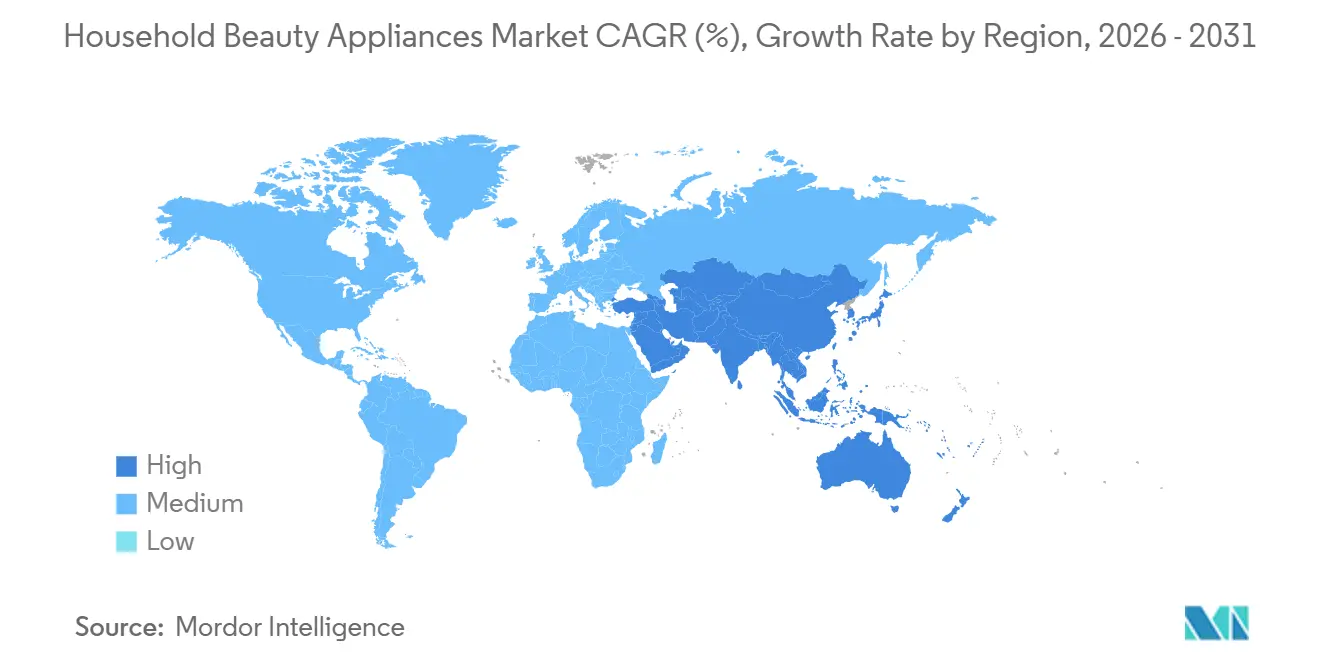

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Household Beauty Appliances Market Analysis by Mordor Intelligence

The household beauty appliances market size is USD 8.26 billion in 2026 and is projected to reach USD 11.35 billion by 2031 at a 6.56% CAGR. The household beauty appliances market is experiencing strong growth as consumer demand shifts from traditional hair tools to advanced, skin-focused technologies. Devices that use LED wavelengths, microcurrents, and other professional-grade techniques for at-home results are increasingly popular, offering efficacy comparable to salon treatments. Regulatory alignment in key markets enhances consumer confidence, with updated safety standards for lasers and intense light devices ensuring trustworthy and reliable use. Innovation in product design featuring precision light, cooling systems, and adaptive sensors expands functionality and boosts perceived effectiveness for anti-aging and hair-care applications. Geographic trends further support growth, with established markets providing steady demand while emerging regions benefit from manufacturing advantages, digital adoption, and omnichannel retail strategies that increase accessibility and conversion.

Key Report Takeaways

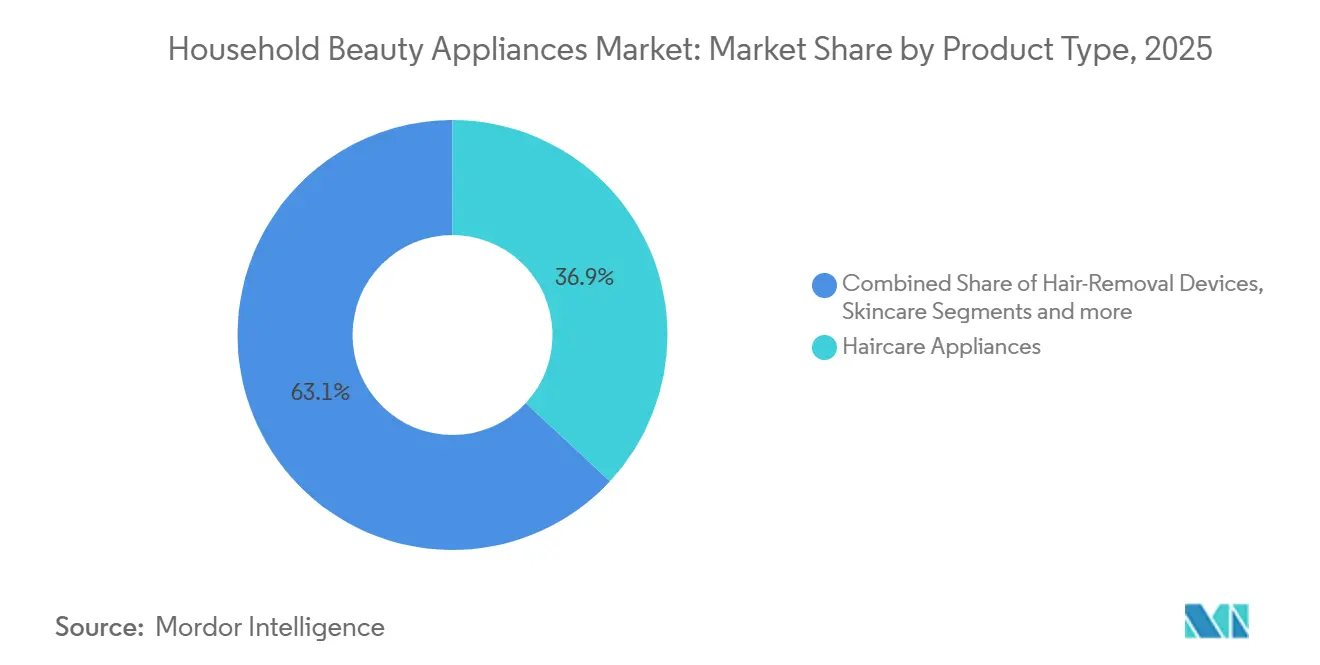

- By product type, Haircare Appliances led with 36.91% of the household beauty appliances market share in 2025, while Skincare and Facial Devices recorded the highest projected growth at a 6.83% CAGR through 2031.

- By distribution channel, Supermarkets and Hypermarkets held 41.62% of the household beauty appliances market share in 2025, and Online Retail posted the fastest projected growth at a 7.35% CAGR through 2031.

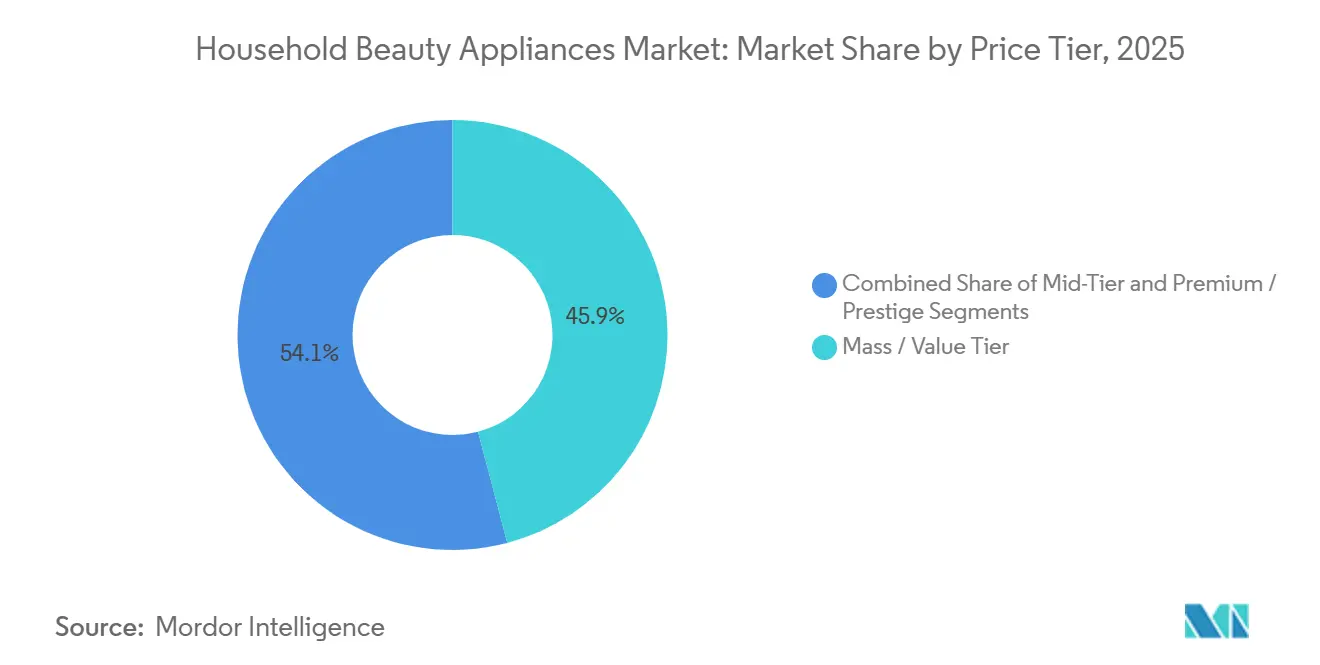

- By price tier, the Mass and Value Tier accounted for 45.91% of the household beauty appliances market share in 2025, while the Premium and Prestige Tier is set to expand at a 6.91% CAGR through 2031.

- By geography, North America held 32.82% of the household beauty appliances market share in 2025, and Asia Pacific is forecast to be the fastest-growing region at a 7.25% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Household Beauty Appliances Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising preference for convenient at-home treatments | +1.8% | Global, early gains in North America, Western Europe, and urban Asia-Pacific | Medium term (2-4 years) |

| Technological advances in LED/IPL/AI personalization | +1.5% | Global core, spill-over to Middle East and Africa and Latin America as price points decline | Long term (≥ 4 years) |

| E-commerce and influencer-led visibility boom | +1.3% | North America and Europe lead, Asia-Pacific accelerating | Short term (≤ 2 years) |

| Subscription-based device ecosystems | +0.7% | North America, Western Europe | Medium term (2-4 years) |

| Asian export incentives lowering price points | +0.9% | Asia-Pacific manufacturing hubs exporting globally | Short term (≤ 2 years) |

| Growing male-grooming demand | +0.4% | North America, Middle East and Africa, Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Preference For Convenient At-Home Treatments Accelerates Device Adoption

Home-based beauty routines have become a lasting habit, with many consumers seeking near-professional results without visiting clinics or salons. Leading brands continue to expand their at-home product lines, introducing new grooming, oral-care, and hair-removal devices that reinforce the appeal and convenience of in-home solutions. The rollout of popular IPL and similar platforms in major markets has broadened the addressable consumer base and extended strong regional franchises into more regulated retail environments. Cost-effectiveness encourages adoption, as a single device can replace repeated in-office treatments, reducing ongoing expenses over time. Regulatory clarity further boosts consumer confidence, with updated guidance such as the U.S. Modernization of Cosmetics Regulation Act (MoCRA) enhancing FDA oversight of cosmetics and personal care products through improved safety substantiation, facility registration, product listing, and adverse event reporting[1]U.S. Food and Drug Administration, Cosmetics & U.S. Law, FDA.gov/cosmetics/cosmetics-laws-regulations/cosmetics-us-law. These factors collectively support steady growth in the household beauty appliances market, as consumers increasingly invest in multifunctional devices for regular use.

Technological Advances In LED/IPL/AI Personalization Unlock New Efficacy Benchmarks

Advances in light delivery, thermal control, and sensor feedback are moving outcomes closer to clinical benchmarks while retaining safe use at home. L’Oréal introduced the Light Straight + Multi-styler with near-infrared capabilities that reshape hydrogen bonds at temperatures capped at 320°F, and also previewed a flexible LED Face Mask that delivers 630 nm red and 830 nm near-infrared in 10-minute sessions for firming and smoothing[2]L’Oréal Groupe, “L’Oréal Advances Leadership in Beauty Tech at CES 2026,” L’Oréal Groupe, loreal.com. Cooling and comfort features have also matured, with new LED face masks integrating targeted thermal management to reduce heat discomfort while maintaining consistent irradiance across treatment zones. AI-linked experiences are now embedded into apps and connected devices to guide protocols, track adherence, and tailor intensity, which helps new users build confidence with precise routines. Microcurrent platforms now include adaptive sensors and boost features for brows, cheek contours, and jawline toning, and app-based coaching to increase consistency and deliver visible results. These product improvements increase perceived value and raise willingness to trade up, which sustains premium-tier momentum within the household beauty appliances market.

E-Commerce And Influencer-Led Visibility Boom Reshapes Discovery And Conversion

Digital channels compress the journey from discovery to purchase, which favors devices that benefit from demonstrations, before-after content, and tutorial-led education. Marketplace storefronts and brand-owned shops allow efficient assortment expansion and rapid iteration on creative and copy, while affiliate and influencer content provides social proof for fit, feel, and visible results. Brands that localized livestreams and festival promotions in Asia saw high-intensity bursts of volume. A larger share of direct-to-consumer sales also allows manufacturers to gather usage and satisfaction feedback and test run subscription programs for gels, attachments, or content. As discovery fragments across social platforms and retail sites, omnichannel presence still matters for large launches, but the core growth engine continues to be digital storytelling that decodes new technologies for mass audiences. This channel mix supports broader reach for the household beauty appliances market while enabling precise performance messaging and rapid response to consumer questions.

Subscription-Based Device Ecosystems Create Recurring Revenue Streams

Leading manufacturers are redesigning offerings as platforms with attachments, consumables, and app content that extend the product life and raise lifetime value. Dyson’s multi-year investment in beauty emphasizes attachment-based ecosystems, turning high-velocity launches into ongoing attachment sales and service revenue. Conair’s Style Chemistry system illustrates a modular design for mass audiences, with a core handle and multiple styling heads to build personalized kits over time[3]Conair Corporation, “Style Chemistry,” Conair, conair.com. Panasonic funded partnerships with skincare data and diagnostic platforms to connect appliances with online treatment services, which lay the groundwork for companion experiences and recurring digital services. App-enabled subscriptions for guided routines and advanced protocols further embed devices into weekly habits and create predictable revenue for brands that invest in content and support. These models help offset component cost volatility, enhance retention, and support premium positioning in the household beauty appliances market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront device cost | -1.2% | Global, most acute in Latin America, Southeast Asia, and Africa | Short term (≤ 2 years) |

| Tightening safety and laser regulations | -0.8% | North America, Europe, Japan | Medium term (2-4 years) |

| Chip and specialty-LED supply bottlenecks | -0.6% | Global supply chains with concentration in East Asia | Short term (≤ 2 years) |

| Counterfeit and grey-market devices eroding trust | -0.5% | Asia-Pacific, Middle East, Latin America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Upfront Device Cost Limits Penetration In Price-Sensitive Segments

Premium devices compete for discretionary budgets, which narrows immediate reach in lower-income regions and within younger cohorts with limited spending power. Flagship tools in hair and skin categories often carry prices that match or exceed monthly income in emerging markets, creating friction without installment or wallet support. The mass and value tier helps bridge this gap with sub-USD 150 devices, although reduced LED counts, shorter flash lifespans, and lower power can affect outcomes and repeat intent. BNPL and similar financing help some consumers distribute payments, while warranty support and clear replacement-part pricing reduce perceived risk. Regulatory compliance and testing add development costs that brands must amortize across units, which can sustain higher price points for features like safety interlocks and medical-grade components. These realities temper the speed of adoption, even as ecosystem models, content guidance, and entry SKUs encourage trial in the household beauty appliances market.

Tightening Safety And Laser Regulations Increase Compliance Burden

Regulatory updates in the United States shifted laser product certifications to align with IEC 60825-1 Edition 3, and this change affects device design, labeling, and safety validation[4]U.S. Food and Drug Administration, “Overview of Device Regulation,” U.S. Food and Drug Administration, fda.gov. Additional standards related to surface temperature limits and optical radiation assessments further reinforce safe use for home devices that employ lasers or intense light. Compliance requires detailed documentation, updated testing, and structured reporting, which adds time and cost to new product development cycles. In parallel, European requirements for marking and conformity documentation continue to raise the bar on technical files and clinical or performance evidence for claims. Heightened enforcement also increases the risk profile for non-compliant imports, online sellers, or improperly labeled devices. The net effect is a steeper curve for new entrants and a stronger moat for compliant brands in the household beauty appliances market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Skincare/Facial Devices lead efficacy-driven premiumization

Haircare Appliances hold the largest share at 36.91% in 2025, reflecting deep household penetration for dryers, straighteners, and curlers across income bands. Skincare and facial devices post the fastest projected expansion at a 6.83% CAGR through 2031 as consumers prioritize anti-aging outcomes and routine consolidation. The household beauty appliances market benefits as flexible LED designs, near-infrared wavelengths, and smart intensity control produce visible results at safer temperatures. Flagship launches now emphasize protective heat management with sensor-driven precision in hair tools and clinically aligned wavelengths in facial masks. As home-use efficacy improves, consumers increasingly treat premium devices as long-term care investments rather than single-function gadgets.

The household beauty appliances market is also shaped by advanced cooling and comfort integrations that address earlier-generation heat discomfort. LED masks that combine red and near-infrared light with targeted thermal control increase session tolerance while maintaining uniform light delivery. Hair tools using near-infrared to reshape bonds at lower temperatures now offer faster results and smoother finishes without the high heat that causes damage over time. Multi-mode devices that blend microcurrent, LED, and RF in streamlined routines expand perceived value at higher price points as they replace multiple single-function purchases. Regulatory alignment for lasers and light-based consumer products under IEC 60335-2-113, combined with FDA device and labeling requirements, guides safer designs and improves user instructions, which supports category trust within the household beauty appliances industry.

By Distribution Channel: Online Retail’s ascent reshapes competitive moats

Supermarkets and hypermarkets held a 41.62% share in 2025, supported by in-aisle visibility and the convenience of bundling appliances with adjacent beauty purchases. Online Retail is the fastest-growing channel at a 7.35% projected CAGR as video demos, before-and-after content, and creator partnerships increase conversion. The household beauty appliances market share for large-format stores remains durable, where shoppers prefer in-person trials before committing to a USD 300 or higher device. Digital storefronts offer brand-controlled storytelling and rapid assortment expansion, while omnichannel strategies pair retail displays with online bundles and accessories. This blend of tactile trial and rich content improves overall category engagement and shortens the learning curve for complex devices.

E-commerce also amplifies promotion windows, search-driven discovery, and app-based education that improve adherence and outcomes. Leading brands used seasonal festivals and livestreams to bring new lines to broader audiences, and events in China elevated brand rankings for grooming and oral-care categories in 2025. Attachments, replacement heads, gels, and content subscriptions sell efficiently online, which increases lifetime value for connected devices. Specialty stores keep relevance through curated assortments, trained staff, and loyalty programs that accommodate replenishment and premium upgrades. This channel interplay supports the household beauty appliances market as consumers compare features, verify safety credentials, and choose their preferred path to purchase.

By Price Tier: Premium segment captures value as consumers trade up

The Mass and Value Tier captured 45.91% of 2025 volume as shoppers balanced price and performance in haircare and entry-level facial devices. The Premium and Prestige tier is projected to grow at a 6.91% CAGR as willingness to pay rises for devices that combine safety credentials, clinical alignment, and robust warranties. Mid-tier devices compete with multi-mode functionality and smart guidance that elevate outcomes without reaching luxury price points. Premium leaders invest in motor, airflow, and heat-control breakthroughs in hair as well as wavelength precision and comfort engineering in skin devices. These investments differentiate performance with repeatable results and strengthen upgrade paths across ownership cycles in the household beauty appliances market.

Attachment ecosystems and content subscriptions reinforce value, since buyers can personalize routines and extend product lifespans with mix-and-match components. Dyson’s multi-year commitment to beauty expands the pipeline for high-performance hair tools and modular attachments that deepen engagement beyond the initial purchase. Conair’s modular handle-and-head system brings customization to mass audiences, creating a budget-friendly pathway into more techniques. Panasonic’s investments in diagnostic partners set the stage for companion services that bundle devices with intelligent recommendations and recurring care. This premiumization and ecosystem strategy supports a health-and-results narrative that resonates in the household beauty appliances industry as consumers seek practical, at-home maintenance with credible safety and outcomes.

Geography Analysis

North America held 32.82% of global revenues in 2025, as high disposable incomes, established specialty retail, and regulatory clarity underpin demand for certified devices. Consumers prioritize safety, efficacy, and reliable warranties, which favors brands with FDA device experience and mature service networks. The household beauty appliances market benefits from strong digital retail adoption that brings LED, IPL, and microcurrent education to a broad audience. Tariff volatility continues to influence component sourcing and bill-of-materials choices for hair and skin devices. Enforcement actions against unapproved imports and misbranded online listings create a safer environment for compliant offerings and strengthen trust across channels.

Asia-Pacific is the fastest-growing region with a 7.25% projected CAGR to 2031, propelled by middle-class expansion, e-commerce-led discovery, and robust manufacturing infrastructure. China, India, Japan, and South Korea anchor scale, while Vietnam and other Southeast Asian nations support assembly and packaging to navigate tariffs and shorten lead times. Japanese innovators broadened device portfolios and IP positions while expanding into new geographies, tapping luxury retail and premium malls that emphasize experiential education. Foreo’s expansion in the region supports nearshoring and flexible production that serve broad price tiers and multiple markets. These development patterns support rising adoption and a strong funnel of device trial among a growing base of digital-first consumers in the household beauty appliances market size trajectory for Asia-Pacific.

Europe accounts for a sizable share with balanced growth and a strong specialty retail footprint in key countries. Regulatory frameworks embed rigorous safety, labeling, and documentation requirements that influence product design, claims, and user instructions across LEDs, IPLs, and microcurrent devices. The publication of IEC 60335-2-113 in 2025 created a harmonized reference for beauty care appliances with lasers and intense light sources, supporting consistent safety guardrails for home use. CE marking requirements further formalize device conformity and documentation standards for distribution across the bloc. This environment supports steady adoption of advanced devices and aligns incentives for compliant innovation in the household beauty appliances market.

Competitive Landscape

The household beauty appliances market remains moderately fragmented, with leading players leveraging brand recognition, safety credentials, and global service networks to maintain their positions. Companies are increasingly pursuing strategies such as vertical integration and partnerships to enhance product categories and create connected ecosystems. These ecosystems often link devices with attachments, gels, and digital content, improving user engagement and loyalty. Brands are also focusing on local regulatory expertise, which helps streamline approvals and ensures high-quality labeling and instructions across markets. This combination of capabilities supports a steady pace of innovation and facilitates scalable growth across geographies and retail channels.

Portfolio renewal continues to be a key strategy for market leaders. Some brands are expanding distribution in new regions to build on existing strengths and broaden reach through trusted retail networks. Others are investing in technology platforms that connect devices with companion services, enabling ongoing engagement beyond the hardware itself. Device innovation, ecosystem development, and service integration are central to maintaining leadership positions and driving consumer interest. These efforts demonstrate a comprehensive approach that blends product performance with long-term brand value.

Consolidation and strategic partnerships are creating additional momentum in the market. Companies are acquiring specialized technology to enhance their offerings and expand their product catalogs. Large-scale alliances between major brands signal continued investment in premium positioning and global strategies. Innovation in device design, precision, and user guidance remains critical, with a focus on safety and measurable results. By emphasizing adaptive control and guided routines, brands are making home beauty treatments more effective and easier for consumers to adopt over time.

Household Beauty Appliances Industry Leaders

Koninklijke Philips N.V.

Panasonic Corporation

Conair Corporation

L’Oréal S.A.

Home Skinovations Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: L'Oréal Groupe unveiled two breakthrough beauty tech innovations at CES 2026 in Las Vegas, the Light Straight + Multi-styler, featuring patented near-infrared light technology capping temperatures at 320°F to reshape hydrogen bonds and deliver results three times faster and twice smoother than premium competitors, and a flexible LED Face Mask prototype developed with iSmart, delivering 630 nm red and 830 nm near-infrared wavelengths in 10-minute sessions.

- October 2025: Panasonic Corporation invested in SISI Co., Ltd., a functional skincare products provider, through the Panasonic Kurashi Visionary Fund, and signed a memorandum of understanding to collaborate on developing new beauty products by combining SISI's cosmetics expertise and SISI LAB skin-analysis data with Panasonic's beauty appliance manufacturing and R&D capabilities.

- October 2025: Kering and L’Oréal announced a long term strategic partnership in luxury beauty and wellness that includes L’Oréal acquiring the House of Creed and obtaining exclusive long term licenses to develop and distribute fragrance and beauty products for several iconic Kering brands.

- August 2025: ReFa launched the EPI CX IPL hair removal device exclusively in China, extending its rapid device-launch cadence across premium Asia-Pacific segments.

Global Household Beauty Appliances Market Report Scope

A complete background analysis of the Household Beauty Appliances Market, which includes an assessment of the parental market, emerging trends by segments and regional markets, Significant changes in market dynamics and market overview is covered in the report. The report also features the qualitative and quantitative assessment by analyzing data gathered from industry analysts and market participants across key points in the industry’s value chain.

| Haircare Appliances |

| Hair-Removal Devices |

| Skincare / Facial Devices |

| Multi-functional Beauty Devices |

| Others (Nail, Massage, Body Care) |

| Supermarkets / Hypermarkets |

| Specialty Stores |

| Online Retail |

| Convenience Stores |

| Others |

| Mass / Value Tier |

| Mid-Tier |

| Premium / Prestige |

| North America | Canada |

| United States | |

| Mexico | |

| South America | Brazil |

| Peru | |

| Chile | |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX (Belgium, Netherlands, and Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| Australia | |

| South Korea | |

| South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines) | |

| Rest of Asia-Pacific | |

| Middle East And Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East And Africa |

| By Product Type | Haircare Appliances | |

| Hair-Removal Devices | ||

| Skincare / Facial Devices | ||

| Multi-functional Beauty Devices | ||

| Others (Nail, Massage, Body Care) | ||

| By Distribution Channel (Value) | Supermarkets / Hypermarkets | |

| Specialty Stores | ||

| Online Retail | ||

| Convenience Stores | ||

| Others | ||

| By Price Tier | Mass / Value Tier | |

| Mid-Tier | ||

| Premium / Prestige | ||

| By Geography (Value) | North America | Canada |

| United States | ||

| Mexico | ||

| South America | Brazil | |

| Peru | ||

| Chile | ||

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| BENELUX (Belgium, Netherlands, and Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines) | ||

| Rest of Asia-Pacific | ||

| Middle East And Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East And Africa | ||

Key Questions Answered in the Report

What is the current size and growth outlook for the household beauty appliances market?

The household beauty appliances market size is USD 8.26 billion in 2026 and is projected to reach USD 11.35 billion by 2031 at a 6.56% CAGR, reflecting ongoing premiumization and broader at-home adoption.

Which product categories are gaining the most momentum within household devices?

Haircare remains the largest, while skincare and facial devices post the fastest growth as LED, microcurrent, and temperature-control advances deliver more reliable at-home results.

How are online channels changing category performance for home-use beauty devices?

E-commerce raises visibility through tutorials and before-after content, while brand-owned stores and marketplaces improve conversion and attachment sales that extend device lifecycles.

Which region has the biggest share in Household Beauty Appliances Market?

In 2025, North America accounted for the largest market share in the Household Beauty Appliances Market.

What regulatory themes matter most for at-home lasers, IPL, and LED devices?

Safety standards for lasers and intense light, labeling requirements, and CE or FDA conformity frameworks guide design, claims, and instructions and support user confidence.

Page last updated on: