Market Overview

| Study Period | 2020 - 2031 |

|---|---|

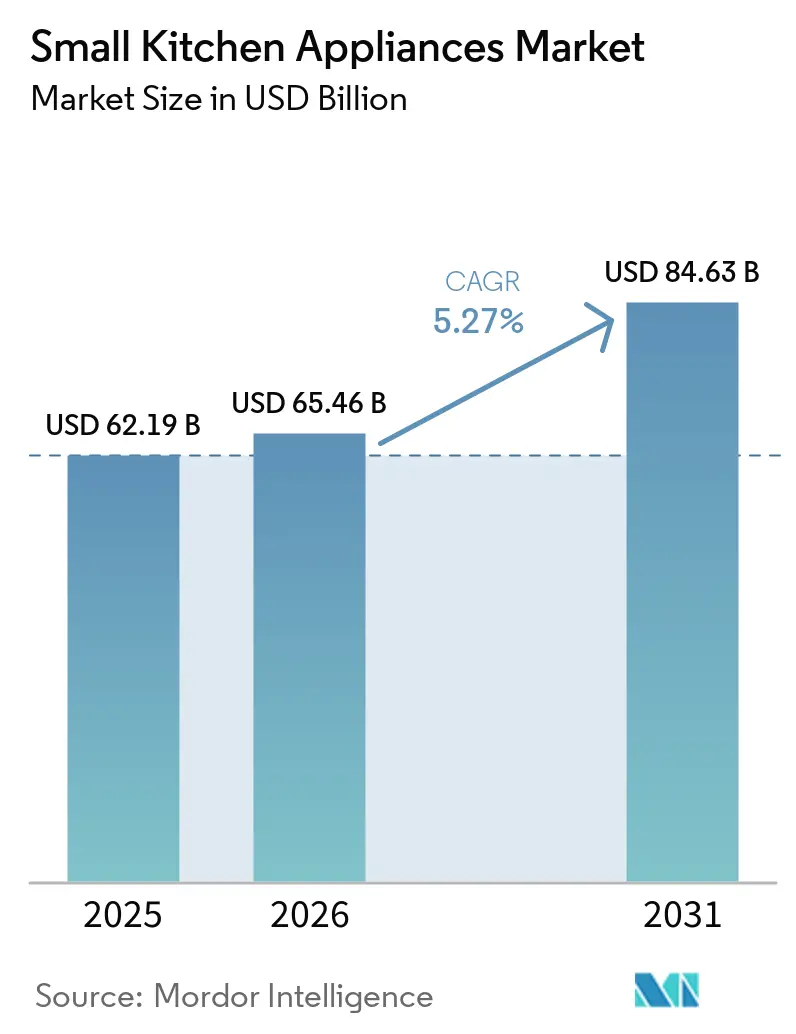

| Market Size (2026) | USD 65.46 Billion |

| Market Size (2031) | USD 84.63 Billion |

| Growth Rate (2026 - 2031) | 5.27% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Small Kitchen Appliances Market Analysis by Mordor Intelligence

The small kitchen appliances market size is expected to grow from USD 62.19 billion in 2025 to USD 65.46 billion in 2026 and is forecast to reach USD 84.63 billion by 2031 at 5.27% CAGR over 2026-2031. The growth links directly to rapid urbanization, rising demand for convenient cooking solutions, and ongoing integration of connected-home technologies. Consumers now expect appliances that save time, fit limited counter space, and connect seamlessly to mobile apps. Manufacturers respond by bundling multiple cooking modes—air-fry, convection bake, pressure cook, and induction heat—into one compact unit. Supply-side challenges, such as tariffs and raw-material price swings, raise production costs yet simultaneously encourage design innovation that reduces material intensity. Competitive activity focuses on AI-driven features, energy-efficiency upgrades, and premium finishes that transform once-utilitarian devices into lifestyle statements.

Key Report Takeaways

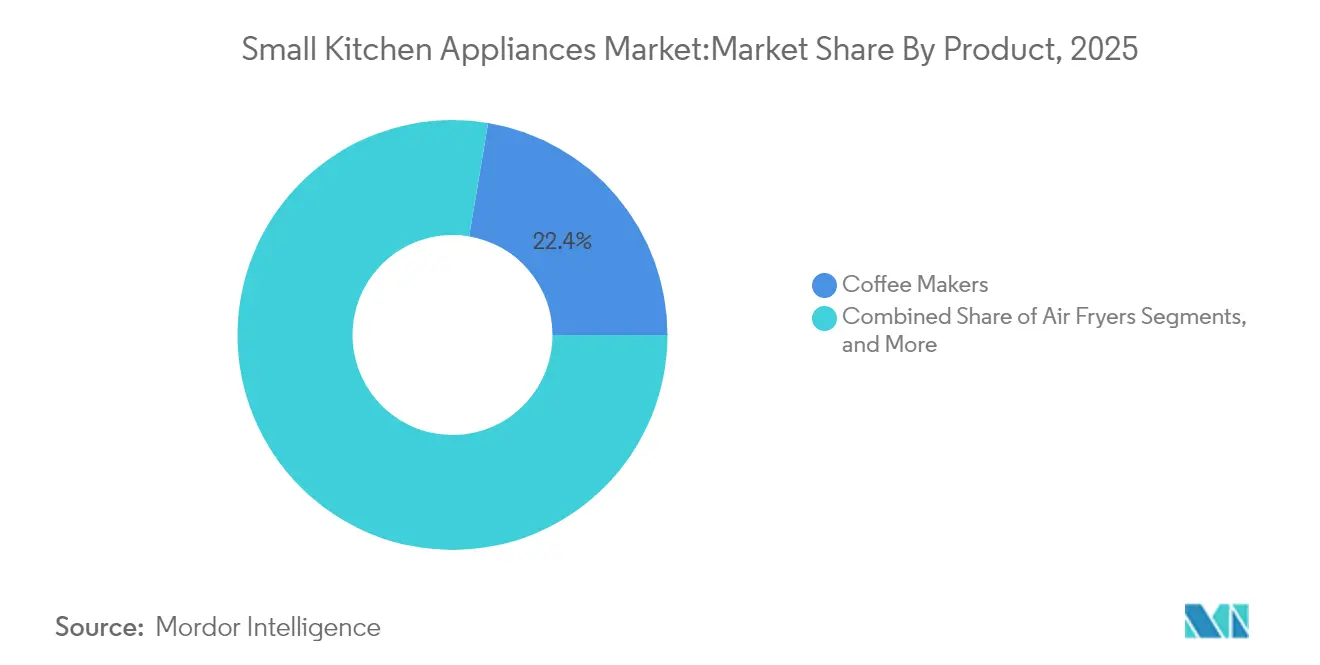

- By product category, coffee makers led with 22.35% revenue share in 2025; air fryers are forecast to expand at a 6.42% CAGR through 2031.

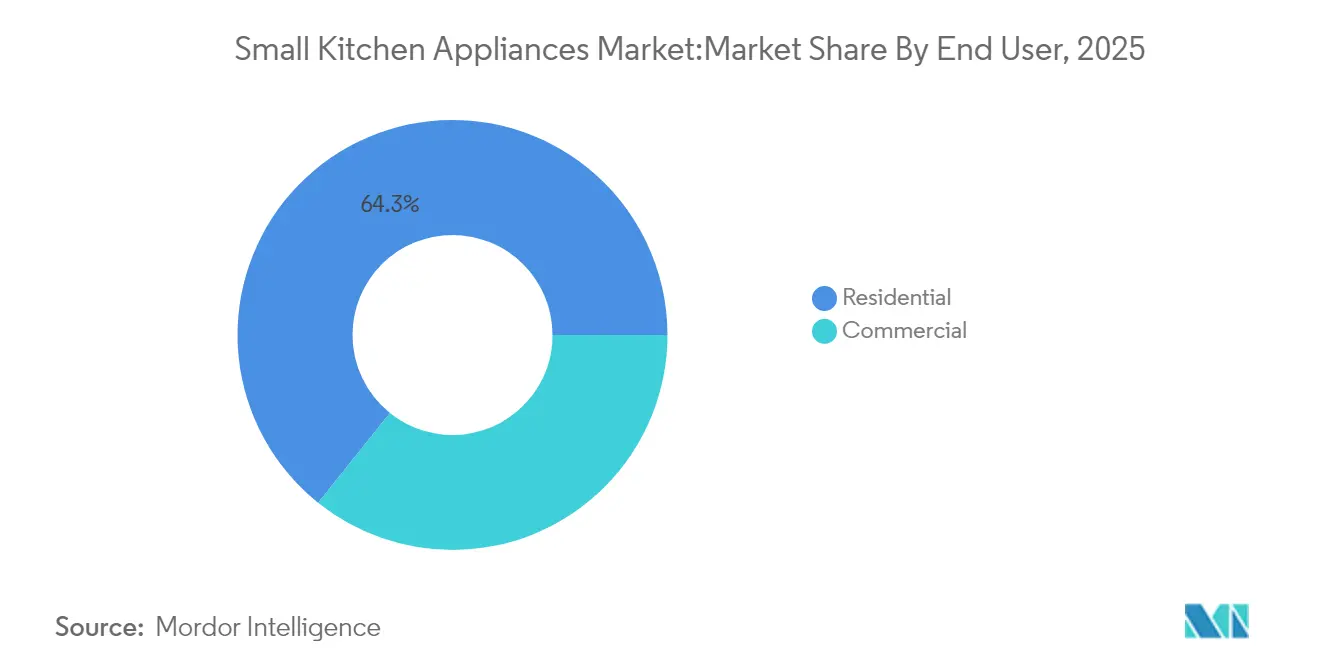

- By end user, the residential segment held 64.25% of the small kitchen appliances market share in 2025 and is advancing at a 5.61% CAGR to 2031.

- By distribution channel, B2C retail captured 73.10% share of the small kitchen appliances market size in 2025, while online retail is growing at a 6.01% CAGR to 2031.

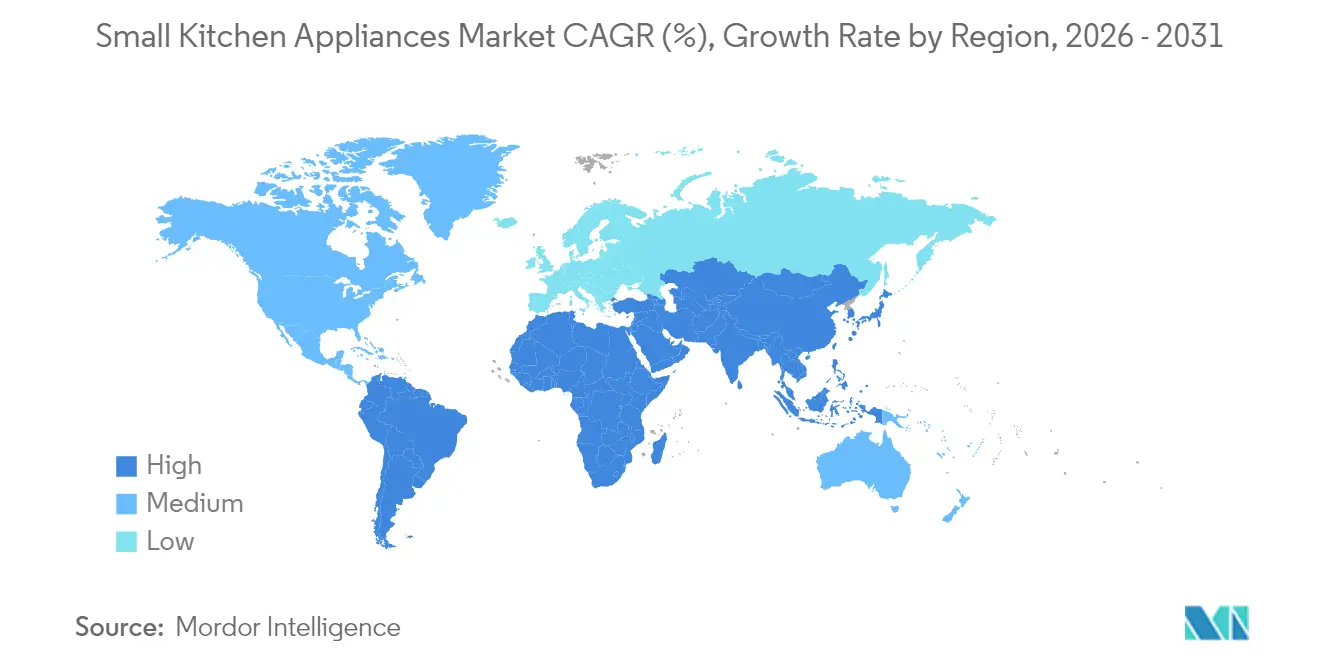

- By geography, North America commanded 32.55% share of the small kitchen appliances market in 2025; Asia-Pacific is projected to record the fastest 6.15% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Small Kitchen Appliances Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising urban living & space constraints | +1.2% | Global, concentrated in Asia-Pacific megacities | Medium term (2-4 years) |

| Growing demand for convenient & time-saving appliances | +0.9% | North America & EU primary, expanding to Asia-Pacific | Short term (≤ 2 years) |

| Increasing disposable income in emerging economies | +0.8% | Asia-Pacific core, spill-over to MEA | Long term (≥ 4 years) |

| Rapid e-commerce expansion boosting product accessibility | +0.7% | Global, accelerated in Southeast Asia | Short term (≤ 2 years) |

| Integration of compact IH & pressure tech in multi-cookers | +0.5% | North America & EU, emerging in Asia-Pacific | Medium term (2-4 years) |

| Micro-form-factor inverter compressors enabling countertop refrigeration | +0.3% | Global, early adoption in urban centers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Urban Living & Space Constraints

Urban density pushes designers toward smaller, multi-functional devices that add minimal footprint yet deliver restaurant-grade results. Smart compact dishwashers, stackable espresso stations, and wall-mounted ovens exemplify how the small kitchen appliances market solves space shortages. Demand concentrates in APAC megacities where housing supply trails population growth, creating durable opportunities for manufacturers that master modularity. Brand differentiation increasingly hinges on fold-flat handles, hidden ventilation, and cabinetry integration that converts living rooms into pop-up kitchens. Vendors able to certify performance without enlarging form factors win loyalty among renters and condo owners concerned with every square inch.

Growing Demand for Convenient & Time-Saving Appliances

Consumers in the global kitchen appliances market increasingly equate convenience with automation, motivating brands to embed AI that adjusts temperature, monitors doneness, and proposes recipes. Panasonic’s HomeCHEF platform demonstrates how voice commands and cloud recipes transform an oven into a meal planner. SharkNinja’s 89% sales jump in food-prep devices underscores willingness to pay for speed and cognitive ease [1]Source: SharkNinja Investor Relations, “Q1 2025 Results,” investors.sharkninja.com. Dual-income households now view countertop appliances as everyday productivity tools, not holiday luxuries. As AI modules become standard, convenience transitions from premium extra to base expectation, pushing laggards aside.

Increasing Disposable Income in Emerging Economies

Higher wages in India, Indonesia, and Vietnam enable households to swap entry-level rice cookers for feature-rich multi-cookers with premium branding. This income lift fuels a “first upgrade” cycle that benefits mid-tier firms combining global design with local price points. Consumers treat appliance choice as a status signal, accelerating premiumization within the small kitchen appliances market. Brand messaging highlights stainless finishes, app linkage, and nutritional cooking modes that align with aspirational lifestyles. The rising middle class, therefore, extends growth well beyond replacement cycles that dominate mature regions.

Integration of Compact IH & Pressure Tech in Multi-Cookers

Induction coils paired with sealed pressure chambers cut cooking times by 70% and energy use by 40%, turning one appliance into every-day steamer, sauté pan, and slow cooker [2]Source: Groupe SEB Japan, “Lacra Cooker Pro Product Sheet,” groupeseb.jp. Groupe SEB’s Lacra Cooker Pro stirs automatically, freeing users from manual tasks. Combining technologies allows the small kitchen appliances market to satisfy health goals and regulatory efficiency mandates simultaneously. For families in studio apartments, a single multi-cooker replaces five devices, aligning with both cost and space savings. This upgrade path keeps average selling prices resilient amid raw-material volatility.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront cost of premium smart appliances | -0.8% | Global, pronounced in price-sensitive markets | Short term (≤ 2 years) |

| Volatility in raw-material prices | -0.6% | Global, manufacturing hubs most affected | Medium term (2-4 years) |

| Fire-safety rules limiting wattage in multi-unit dwellings | -0.4% | North America & EU regulatory zones | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Upfront Cost of Premium Smart Appliances

AI modules, multiple sensors, and secure connectivity add 30–50% to base prices, slowing adoption among value-focused households. In developing regions, buyers favor essential features over cloud analytics, creating market bifurcation between luxury and mass. Brands attempt to soften the blow with financing plans and entry-level smart lines, yet sticker shock remains a barrier. Competitors introducing basic connectivity at lower margins squeeze incumbents’ premium tiers. The small kitchen appliances market, therefore, balances innovation with affordability or risks stalling volume growth.

Volatility in Raw-Material Prices

Steel swinging between USD 800 and 1,000 per ton and aluminum hovering at USD 2,500 – 3,000 complicate the cost. A 50% tariff on imported steel injected 19.4–31% onto appliance price tags during 2024 [3]Source: NPR, “Tariffs May Raise Appliance Prices,” npr.org. Copper above USD 10,000 per metric ton lifted circuit and coil costs by up to 4.2%. Manufacturers hedge with multi-sourcing and design adjustments that reduce metal content, yet margin pressure endures. Persistent volatility may prompt further consolidation as scale advantages offset procurement risk within the small kitchen appliances market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Health-Centric Air Fryers Reshape Demand

Air fryers lead unit growth with a 6.42% CAGR through 2031 as consumers seek up to 90% oil reduction without flavor loss, hindustantimes.com. Their surge catalyzes frozen-food makers to label packaging with air-fry instructions, shown by a 90% increase in SKUs during 2024 conagrabrands.com. Coffee makers still hold the largest 22.35% slice, underpinning stable repeat-purchase behavior anchored in morning rituals. The small kitchen appliances market size for coffee makers remains resilient even while share flattens due to air-fryer momentum. Emerging niches, such as automated bread makers and sous-vide sticks, gain traction as social media spotlights specialty cooking. Multi-functional electric cookers blend pressure, induction, and robotic stirring to attract upgrade shoppers who aim to clear counter clutter. Routine categories like toasters and kettles log steady replacement demand but now incorporate connectivity and style updates to keep relevance. Overall, product competition shifts toward versatility and wellness alignment.Compact ovens with convection, steam, and air-fry modes in one chassis illustrate how the small kitchen appliances market presses suppliers to consolidate functions.

Grills, blenders, and juicers ride the wellness trend, particularly in APAC cities where smoothie culture accelerates. Countertop refrigeration, enabled by inverter tech, births a fresh subcategory that addresses beverage storage in micro-apartments. Product bundling, such as blender-cup packages and fryer-rack accessories, supports margin retention. Small-batch manufacturing and color variants satisfy consumers who view appliances as visible décor.

By End User: Residential Preference Signals Lifestyle Shift

The residential domain controlled 64.25% of the small kitchen appliances market in 2025 and posts the quickest 5.61% CAGR as home cooking transforms into entertainment and self-expression, pressroom.geappliances.com. Remote work elevates meal preparation frequency, spurring demand for quiet motors, app-based timers, and safe-to-touch exteriors. Social platforms trigger purchase spikes each time viral recipes appear, pushing brands to release limited-edition colors to capitalize on trend loops. Commercial kitchens, although smaller in share, deploy robotics to offset labor gaps, illustrating potential long-run convergence between residential and professional specifications. Quick-service restaurants install AI-driven fry stations for portion control and consistency, foreshadowing technologies that later diffuse into home appliances. Within households, premiumization reigns as consumers allocate discretionary income toward stainless finishes, customizable handles, and subscription-based recipe services.

Average order values rise when buyers bundle food processors, juicers, and beverage fridges in a single cart. In apartments, residents favor modular systems that stack a microwave oven and dishwasher into a column to optimize space. In the commercial realm, chain restaurants negotiate volume contracts that stabilize vendor pipelines, yet cost pressures persist due to metal volatility. These distinct needs drive segmented marketing yet encourage shared R&D for durability and hygiene standards.

By Distribution Channel: Online Growth Redefines Retail Playbook

B2C outlets still generated 73.10% of 2025 revenue, but web storefronts expand at a 6.01% CAGR, reshaping purchase journeys. Consumer trust in freight, installation, and returns now matches in-store experiences, even for heavy induction ranges. The small kitchen appliances market size within pure-play online platforms widens as influencers demonstrate product outcomes in real time retailtoday.com. Live-stream selling on Southeast Asian apps further accelerates adoption, letting viewers buy during cooking demos.Physical multi-brand stores answer with experiential zones where visitors test steam-oven humidity or compare blender decibel levels.

Exclusive brand boutiques provide warranty registration, recipe classes, and same-day repairs to build loyalty beyond price. Meanwhile, manufacturers adopt direct-to-consumer microsites to harvest user data, deliver firmware updates, and cross-sell accessories. The omnichannel arms race compels tight inventory orchestration so that online flash-sale promises align with warehouse reality. For the foreseeable future, a hybrid approach that links QR codes on store shelves to online video tutorials will dominate.

Geography Analysis

North America held 32.55% of 2025 revenue, anchored by high replacement cycles and early smart-home adoption, packagingdigest.com. U.S. households boosted air-fryer ownership so rapidly that the category became the fourth most common kitchen device. Canada’s updated energy standards push manufacturers to rate products above Tier II, favoring inverter motors that slash standby draw canadagazette.gc.ca. Mexico benefits from proximity to U.S. retail chains, fostering near-shoring of assembly to hedge tariff risk and speed delivery. Despite maturity, upsell potential remains via voice-enabled cooktops and countertop wine dispensers.

Asia-Pacific shows the fastest 6.15% CAGR through 2031, propelled by urbanization, rising incomes, and e-commerce. China exported 4.48 billion household appliances in 2024, up 20.8%, underlining the region’s scale and domestic appetite. India, with projected consumer-durables expansion this year, fuels premium small kitchen appliances market demand for air-fryers and multi-cookers ibef.org. Southeast Asia’s supermarket boom and logistical upgrades open last-mile delivery to peri-urban areas previously underserved. Local brands experiment with rice cooker-air-fryer hybrids tailored to staple diets, reinforcing regional customization as a growth lever.

Europe registers stable growth driven by eco-design rules that nudge buyers toward A-class efficiency labels and recyclable packaging. Germany and France favor induction and steam functions that align with low-fat cooking, while Italy’s design heritage boosts demand for colored finishes and retro handles. South America advances steadily yet faces exchange-rate swings that influence affordability. The Middle East and Africa region witnesses rising demand in metropolitan hubs such as Dubai and Lagos, but fragmented regulations necessitate country-specific certification strategies. As connectivity spreads, data-localization laws could shape cloud services that power smart ovens, adding complexity to multinational rollouts.

Competitive Landscape

The small kitchen appliances market remains moderately concentrated, with Whirlpool, Haier Inc. (incl. GE Appliances), LG Electronics among the leaders. GE Appliances secured “Smart Appliance Company of the Year” for embedding generative AI into connected ranges. Whirlpool’s portfolio restructuring with Arçelik formed Beko Europe, sharpening strategic focus on profit pools. Midea’s acquisition of Küppersbusch’s parent company widens its European premium.

Emerging challengers like Posha raise venture funding for robotic kitchen arms that promise consistent sautéing at home. Direct-to-consumer newcomers exploit social media to bypass retail fees, offering subscription meal kits that integrate with proprietary air fryers. Incumbents counter through in-house innovation hubs such as GE’s FirstBuild, which co-creates niche products like a sourdough fermentation station with King Arthur Baking.

Strategic themes center on software-hardware fusion, energy-saving engineering, and form-factor miniaturization. Consolidation continues as scale becomes critical to amortize R&D and raw-material volatility. Still, white-space opportunities remain in health-centric countertop refrigeration, countertop fermentation, and child-safe induction hotplates. Competitive advantage will follow firms that pair sensor-rich hardware with recipe clouds, turning transactional sales into recurring service revenue.

Small Kitchen Appliances Industry Leaders

Whirlpool Corporation

Haier Inc. (incl. GE Appliances)

AB Electrolux

LG Electronics

BSH Hausgeräte GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: GE Appliances completed a USD 180 million expansion of its Georgia plant, adding 600 jobs and advanced robotics to boost range production capacity.

- April 2025: Midea acquired Küppersbusch’s parent company, deepening its European premium segment presence.

- March 2025: GE Appliances’ FirstBuild and King Arthur Baking launched the Sourdough Sidekick for automated starter care.

- April 2024: Whirlpool and Arçelik formed Beko Europe B.V., combining EUR 5.5 billion in revenue while retaining KitchenAid small appliances.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the small kitchen appliances market as all plug-in countertop devices used for food or beverage preparation, heating, cooking, or beverage service, including coffee makers, air fryers, food processors, juicers, grills, electric cookers, kettles, toasters, and compact ovens. Devices sold loose or bundled through retail, B2B, and online channels across residential and light-commercial kitchens are counted in value terms.

Scope exclusion: built-in "major" appliances such as ranges, dishwashers, refrigerators, and extractor hoods sit outside this analysis.

Segmentation Overview

- By Product

- Food Processors

- Juicers and Blenders

- Grills and Roasters

- Air Fryers

- Coffee Makers

- Electric Cookers

- Toasters

- Electric Kettles

- Countertop Ovens

- Other Small Kitchen Appliances (bread makers, waffle makers, egg cookers, etc.)

- By End User

- Residential

- Commercial

- By Distribution Channel

- B2C / Retail

- Multi-brand Stores

- Exclusive Brand Outlets

- Online Retail

- Other Distribution Channels

- B2B (directly from the manufacturers)

- B2C / Retail

- By Geography

- North America

- Canada

- United States

- Mexico

- South America

- Brazil

- Peru

- Chile

- Argentina

- Rest of South America

- Europe

- United Kingdom

- Germany

- France

- Spain

- Italy

- BENELUX

- NORDICS

- Rest of Europe

- Asia-Pacific

- India

- China

- Japan

- Australia

- South Korea

- South-East Asia

- Rest of Asia-Pacific

- Middle East & Africa

- United Arab Emirates

- Saudi Arabia

- Turkey

- South Africa

- Nigeria

- Rest of Middle East & Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed appliance product managers, regional distributors, and large e-commerce merchants across North America, Europe, and Asia Pacific. These discussions validated channel mix shifts, average selling prices, and emerging demand pockets that were only partially evident in documents.

Desk Research

We began with public trade data from UN Comtrade, Eurostat, and the US International Trade Commission, which helped us trace cross-border shipment values. Household appliance penetration ratios came from the International Housewares Association and AHAM, while consumer-price and income series were sourced from the World Bank and OECD. Company filings, retailer investor decks, and news archived on Dow Jones Factiva rounded out brand-level benchmarks. Proprietary spend estimates on leading OEMs from D&B Hoovers supplied extra financial checks. This list is illustrative; many other references informed our desk work.

Market-Sizing & Forecasting

We built a top-down model that reconstructs global demand from production and trade data, then aligns it with household formation, disposable income per capita, e-commerce share of appliance sales, energy-efficiency label adoption, and average replacement cycles. Select bottom-up tests, supplier roll-ups and sampled ASP × unit estimates, helped fine-tune totals. An ARIMA-based forecast, fed by the five variables above, generates the 2025-2030 outlook; coefficient choices were vetted with our primary respondents. Gaps in bottom-up coverage were bridged using regional price proxies adjusted by PPP factors.

Data Validation & Update Cycle

Outputs undergo variance checks versus historical spend trends, and outlier flags trigger re-contacts. A senior reviewer signs off before release. Reports refresh annually, and our team issues interim updates when material events surface.

Why Mordor's Small Kitchen Appliances Baseline Earns Trust

Published figures often diverge because firms choose different product baskets, price bases, and update cadences. According to Mordor Intelligence, consistency begins with a clear scope that groups every countertop device consumers actually buy, values them in real 2024 dollars, and revisits assumptions each year.

Key gap drivers versus other publishers include rivals limiting coverage to select SKUs, using list rather than transacted prices, or rolling forward pre-pandemic models without fresh channel inputs.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 62.19 B (2025) | Mordor Intelligence | - |

| USD 29.09 B (2024) | Global Consultancy A | Omits countertop ovens and Asia's long-tail brands; relies on list prices |

| USD 19.54 B (2025) | Industry Journal B | Counts retail sales only, excludes B2B demand and emerging online-first labels |

In short, our disciplined variable selection, annual refresh, and dual validation steps give decision-makers a balanced, reproducible baseline they can confidently plug into strategy models.

Key Questions Answered in the Report

What is the current size of the small kitchen appliances market?

The market stands at USD 65.46 billion in 2026 and is projected to reach USD 84.63 billion by 2031 at a 5.27% CAGR.

Which product category is growing the fastest?

Air fryers lead growth with a 6.42% CAGR through 2031 due to demand for healthier oil-free cooking.

Which region will see the highest growth?

Asia-Pacific is forecast to register a 6.15% CAGR, fueled by urbanization, rising incomes, and e-commerce expansion.

How are online channels influencing sales?

Online retail grows at a 6.01% CAGR, enabling niche brands to reach wider audiences and letting consumers compare features and prices easily.

What are the main challenges facing manufacturers?

Key challenges include high upfront costs for smart features, raw-material price volatility, and wattage limits imposed by fire-safety regulations.

Who are the leading companies in the market?

Whirlpool, Haier Inc., Electrolux, Electronics and several emerging direct-to-consumer players dominate through innovation, acquisitions, and AI integration.

Page last updated on: