Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

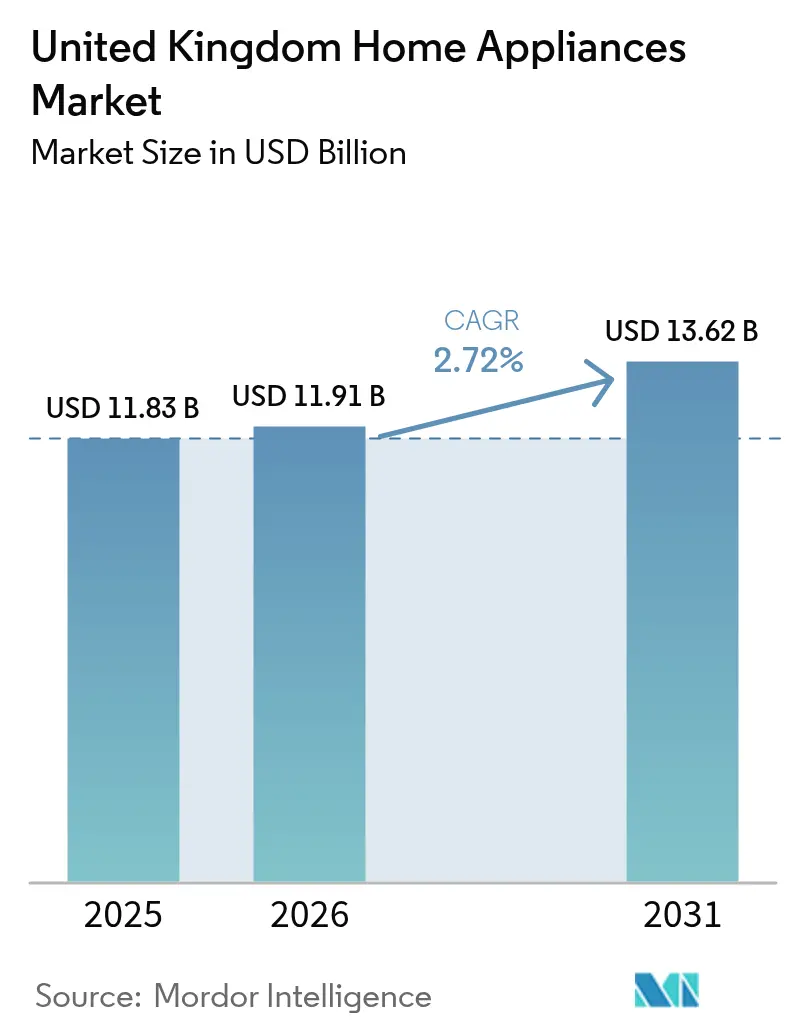

| Base Year Market Size (2025) | USD 11.83 Billion |

| Market Size (2026) | USD 11.91 Billion |

| Market Size (2031) | USD 13.62 Billion |

| Growth Rate (2026 - 2031) | 2.72% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United Kingdom Home Appliances Market Analysis by Mordor Intelligence

The United Kingdom home appliances market size is expected to grow from USD 11.83 billion in 2025 to USD 11.91 billion in 2026 and is forecast to reach USD 13.62 billion by 2031 at a 2.72% CAGR over 2026-2031. The growth path reflects long appliance lifecycles, a steady push toward net-zero by 2050, and clearer efficiency signals from the 2021 A to G energy label rescaling that simplify consumer choice and sharpen product differentiation. The Clean Heat Market Mechanism, Boiler Upgrade Scheme grants, and consultations to raise standards for tumble dryers align efficiency with policy objectives, while right-to-repair measures and expanded spare parts access may extend replacement intervals and temper volumes at the margin. Channel dynamics remain in transition, with multi-brand stores holding a sizable share today, while online channels post the fastest gains on the back of better tools, logistics options, and greater convenience for younger cohorts.

Key Report Takeaways

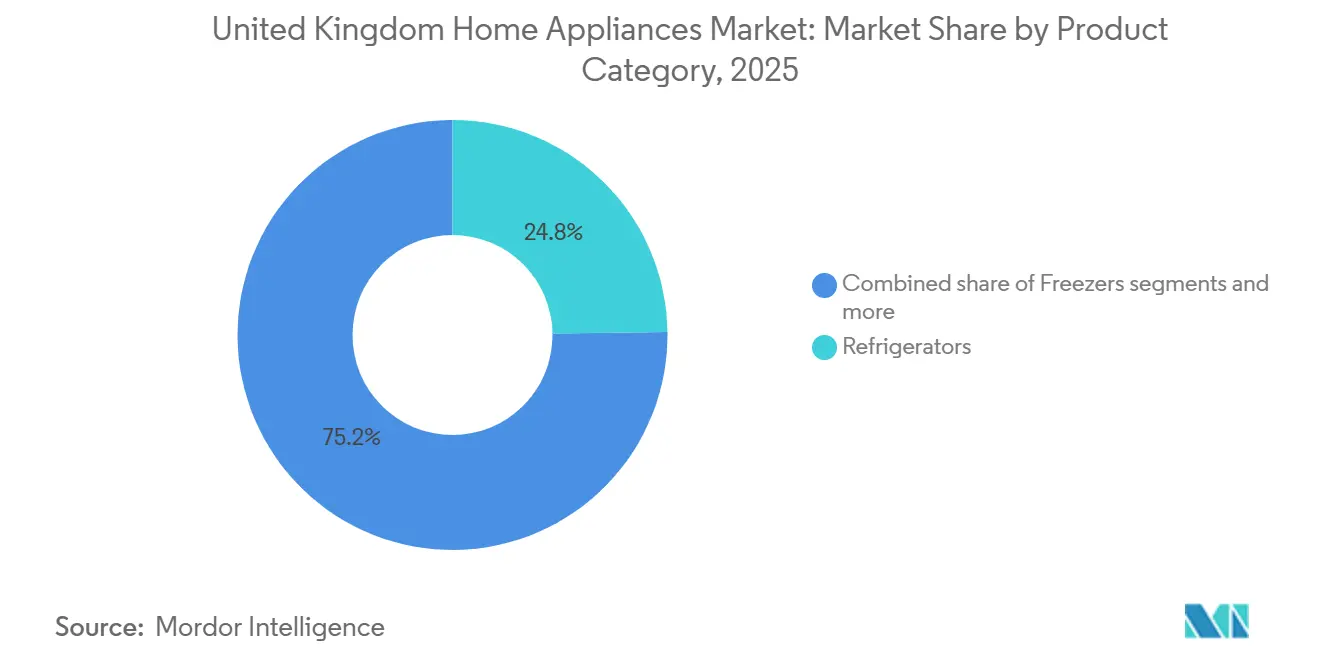

- By product type, refrigerators led with 24.78% of the United Kingdom home appliances market share in 2025, while air fryers are forecast to expand at a 3.51% CAGR through 2031.

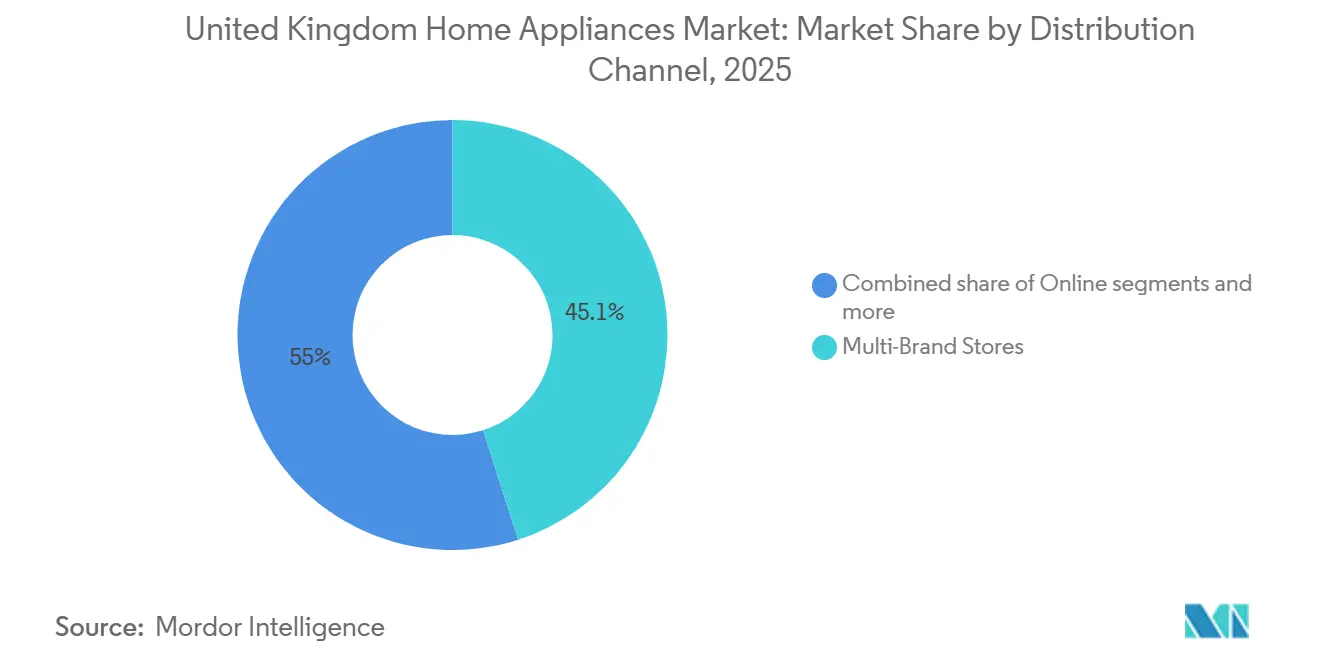

- By distribution channel, multi-brand stores held 45.05% of the United Kingdom home appliances market size in 2025, whereas online is projected to grow at a 4.06% CAGR through 2031.

- By geography, England commanded 39.18% of the United Kingdom's home appliances market share in 2025, but Northern Ireland is set to record the fastest 4.28% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United Kingdom Home Appliances Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Energy label rescaling and UK ecodesign standards | +0.8% | Global, strongest in England and Scotland, with high-consumption stock | Medium term (2-4 years) |

| Smart and connected appliances adoption | +0.4% | Urban centers such as London, Manchester, and Birmingham, with spillover to the suburbs | Medium term (2-4 years) |

| Electrification of heating and kitchen retrofits | +0.3% | Scotland, England heat-pump clusters, Wales social housing | Long term (≥ 4 years) |

| Premiumisation with design-led and feature-rich models | +0.3% | South East and London, 25-44 age cohort nationwide | Medium term (2-4 years) |

| Demand flexibility and time-of-use tariffs | +0.2% | Great Britain core with early gains among EV and tech-forward households | Medium term (2-4 years) |

| Private-label expansion at the entry-tier | +0.2% | National, strongest in discount and online-only retail | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Energy Label Rescaling and UK Ecodesign Standards Accelerate A-Rated Replacements From 2026

Across Europe, consumers are highly aware of energy labels and often use them as a key factor in purchasing decisions. This trend has supported the popularity of A-rated refrigerators and washing machines, especially after price caps highlighted significant lifetime savings in 2025 and 2026. With Ofgem setting its dual-fuel price cap at GBP 1758 (USD 2,371.7), retailers are increasingly emphasizing kilowatt-hour consumption, both in-store and online, to present a clearer picture of the total cost of ownership relative to the upfront price. Northern Ireland's regulatory alignment through the Windsor Framework enables manufacturers to adopt dual-compliance strategies that cater seamlessly to both Great Britain and Northern Ireland. This alignment simplifies product planning and labeling processes. In July 2025, the United Kingdom proposed new requirements for tumble dryers, aiming to phase out inefficient models, introduce repairability indices, and tighten standards for condensation efficiency and low-power modes. These measures establish a compliance baseline that benefits heat-pump dryers. In response, brands are expanding heat-pump dryer offerings and providing extended warranties, emphasizing the link between efficiency and post-sale support. This strategy reduces payback periods for consumers willing to invest more upfront. NIQ GfK data show smart A-rated washing machines up 38% in unit sales (August 2023-July 2024), accounting for over 50% of all machines sold, while Beko's Which? Best Value Appliance Brand award for 2024 and 2025 underscores competitive intensity at the efficiency frontier[1]NIQ, “Ownership of smart home products doubles in the UK in five years,” NIQ, nielseniq.com.

Smart/Connected Appliances Adoption And Interoperability Ecosystems Mature In UK Homes

Broadband upgrades and smart meter rollout underpin a wave of connected appliances that can automate energy use and coordinate with time-of-use tariffs. National Grid ESO’s Demand Flexibility Service became a year-round program and demonstrated that households will shift appliance usage during peak events when compensated, which validates the value proposition for scheduleable devices. Partnerships between appliance makers and energy suppliers, such as Haier with Octopus Energy, show how low off-peak prices can help recover device premiums through optimized cycles and smart scheduling. September 2025, refrigerators, washers, dryers, air conditioners with seven years of software updates, Knox Matrix security, and enhanced AI Vision Inside, elevate interoperability expectations beyond single-brand ecosystems, while LG's AI Core-Tech in MoodUP™ fridge-freezers and Bespoke AI Jet Ultra vacuums showcase machine-learning optimization of cooling curves and suction profiles[2]Samsung Newsroom UK, “Bespoke AI and One UI updates for appliances,” Samsung, samsung.com.

Electrification Of Heating And Kitchen Retrofits Boosts Demand For Energy-Efficient White Goods

Net-zero targets for 2050 and the Sixth Carbon Budget put decarbonizing homes at the center of energy policy, supporting the electrification of heating and cooking and triggering related appliance upgrades. The Clean Heat Market Mechanism requires suppliers to move a share of boiler sales to heat pumps, and the Boiler Upgrade Scheme grants of up to USD 10,000 to reduce upfront costs for homeowners making larger retrofit decisions[3]UK Government Cabinet Office, “Energy Labelling and Ecodesign Requirements,” GOV.UK, gov.uk. Scotland’s grant and loan packages add a further incentive to align heat pump adoption with energy-efficient laundry and refrigeration purchases, which can bundle installation and enable whole-home savings. As households switch from gas hobs to induction, buyers pair high-efficiency cooking with energy-smart ovens and extractor systems that improve both control and operating costs. Induction cooking pairs well with low-carbon electricity during off-peak windows, which supports time-of-use alignment across dishwashers and washers to better utilize smart meter capabilities. As the installer base scales and training pipelines deepen, heat-related retrofits can open cross-selling opportunities for connected white goods that offer remote diagnostics and proactive maintenance.

Premiumisation Trend Lifts Average Selling Prices Through Design-Led And Feature-Rich Models

Premium growth aligns with buyers who want efficient products with smart features, attractive designs, and reliable software support, which together justify higher average selling prices. Liebherr’s Energy Class A integrated refrigeration, LG’s MoodUP and ThinQ features, and Samsung’s Bespoke AI Family Hub with vision-based food management signal a sustained innovation cycle at the top end. Manufacturers are combining machine learning, internal cameras, and app-driven controls to fine-tune cycles, reduce energy consumption, and extend product life, which strengthens the total cost of ownership case. Built-in products benefit from renovations and new-builds, where design coherence and integration drive package sales across multiple categories and price points. Extended warranties and remote diagnostics improve retention and satisfaction, nudging customers to pay premiums for longevity, reliability, and software updates that keep features current. Even as affordability pressures persist for some cohorts, premium demand remains resilient in affluent regions and among buyers who value design and convenience.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cost-of-living squeeze on discretionary upgrades | -0.7% | National, sharper in the North East, West Midlands, Wales | Medium term (2-4 years) |

| Housing slowdown and fewer new completions | -0.5% | South East and London, Scotland | Short term (≤ 2 years) |

| Rising repair, logistics, and compliance costs | -0.4% | National, with added pressures in Scotland and Northern Ireland | Medium term (2-4 years) |

| New import controls and border checks | -0.3% | National, heavier impact on EU-sourced goods via key ports and inland BCPs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Cost-of-Living Squeeze Defers Discretionary Upgrades And Compresses Volumes

Inflation remained above the Bank of England’s target into late 2025, and real wage gains were modest into early 2026, which kept budgets tight for many households. Ofgem’s energy price cap at GBP 1,758 (USD 2,371.7) in early 2026 reinforced household sensitivity to energy bills, and many buyers continued to delay non-essential upgrades until failure rather than replacing a still-functional unit. Retail pricing in some categories softened in 2025 as retailers absorbed deflation and used promotions to stimulate demand, which compressed gross margins in the process. Entry-tier volumes held better as consumers prioritized essential items and lower upfront prices, while premium buyers in affluent areas remained active on value, longevity, and design integration. Financing options and subscriptions helped lower barriers to higher-efficiency dryers and connected washers, though energy bill pressures still limited uptake among price-sensitive cohorts. This environment narrows the near-term growth runway for the United Kingdom home appliances market, yet it also elevates the pitch for efficient and smart products that can clearly document bill savings over time.

Housing Slowdown And Fewer New Completions Weigh On Built-In Installations

Slower housing transactions and the reset of stamp duty thresholds in 2025 dampened new-build momentum and delayed some renovation decisions, which matters for built-in appliance packages that rely on project pipelines. Mortgage-rate sensitivity through 2024 and into 2025 curtailed larger kitchen refits for many households and developers, which lowered near-term volumes for integrated ovens, hobs, dishwashers, and refrigeration. The Future Homes Standard 2026 pushes new homes to be zero-carbon-ready, effectively favoring all-electric solutions such as induction hobs and efficient integrated appliances. This sets a regulatory floor that helps the premium-built-in category even if overall housing transaction volumes are slower than in past cycles. As financing costs ease and clarity improves on compliance pathways, developers and renovators can resume projects that bundle multiple categories, which benefits multi-brand appliance sets. Savills forecasts +4% national growth in 2025, but -4% in prime central London, while Knight Frank and Zoopla converge on ~+2.5% in moderated growth, as rising supply and elevated stamp-duty costs feed into asking-price realism[4]The Week UK, “Is the UK about to see a house price crash?” The Week, theweek.com. In the interim, the United Kingdom home appliances market sees more stable replacement-led demand than project-driven volumes in built-in channels.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Refrigerators anchor value, air fryers lead innovation velocity

Refrigerators accounted for 24.78% of the United Kingdom home appliances market in 2025, driven by mandatory placement, long service lives, and energy visibility, which sustained high replacement intent, supporting premium models that meet stricter efficiency standards. Flagship launches include Liebherr’s Energy Class A integrated models, LG’s InstaView configurations with app controls and precise temperature stability, and Samsung’s Family Hub with vision-based food recognition, which sustain average selling prices through a clear feature and efficiency case. A-rated refrigeration and laundry now stand out under the rescaled A to G label, and retailers emphasize kilowatt-hours and total cost of ownership in-store and online. Tumble dryers are shifting to heat-pump architectures to meet proposed standards and repairability requirements, which link energy savings with longer warranties and better diagnostics. The United Kingdom home appliances market benefits when brands position warranties, service networks, and software updates as part of the overall value proposition across refrigeration, laundry, and cooking.

Air fryers are forecast to expand at a 3.51% CAGR through 2031 as healthier cooking, smaller footprints, and efficient operation align with hybrid work patterns and price-sensitive meal preparation. Multifunctional devices from Ninja, Instant Brands, and Tefal combine multiple cooking modes into single countertop appliances, which increases appeal among urban households with limited kitchen space and busy routines. In major appliances, washing machines and dishwashers integrate auto-dosing, soil sensing, and cycle optimization, which reduce resource use without sacrificing performance. Beko’s platform highlights algorithms to reduce energy use and enhance garment care across programs beyond eco modes, pointing to iterative efficiency gains in mainstream price bands. Ovens and hobs are adding AI-assisted presets and induction for better control, speed, and safety, which pairs well with time-of-use tariffs and smart meter participation in flexibility events. Robotic and cordless vacuums continue to split the cleaning category as automation and higher suction at lighter weights show up in premium launches.

By Distribution Channel: Multi-brand stores defend tactile advantage, online gains via AI tools

Multi-brand stores accounted for 45.05% of transaction value in 2025, supported by in-person demos, same-day installation options, and the reassurance of expert advice for high-involvement purchases in the United Kingdom home appliances market. Physical formats continue to bundle services such as extended warranties, trade-in credits, and flexible payments, and staff content guides buyers through features that now span energy labels, smart integrations, and durability. For built-in packages, in-store planning and installation coordination remain sticky, which helps multi-brand stores defend share against pure online price competition. As part of their proposition, select stores and showrooms offer live kitchens and hands-on experiences that help buyers assess noise, seals, and controls before a higher-ticket purchase. This tactile advantage is hard to replace and remains relevant for complex installations that involve carpentry and electrical changes.

Online is projected to grow at a 4.06% CAGR through 2031, narrowing the gap through virtual configuration tools, AR previews, customer reviews, and reliable delivery and haul-away services. E-commerce leaders amplify convenience with transparent delivery slots, packaging removal, and disposal of old units, which now match many of the practical benefits once reserved for specialist stores. Discount grocers and online-only platforms are deepening their private-label strategies in small appliances, presenting attractive value without sacrificing basic energy performance. Exclusive brand outlets and direct-to-consumer channels, including manufacturer stores and experience centers, capture margin by bundling subscriptions, upgrades, and extended warranties. Investment in last-mile logistics and post-purchase support remains a must-have for pure-play online retailers, given expectations set by specialist chains and brand-owned channels.

Geography Analysis

England accounted for a 39.18% share in 2025, led by population density, higher disposable incomes in the South East and London, and deeper retailer coverage for same-day and next-day delivery options. London serves as an early adopter hub for connected refrigeration, robotic vacuums, and boiling-water taps, with buyers valuing design integration and long software support windows alongside efficiency. The South East continues to sustain demand for premium built-in packages as part of kitchen renovations and extensions, even as housing activity moderated in 2025. Regions such as the North West and West Midlands show stable mid-tier activity, driven by strong value brands and competitive promotions. As financing and subscription models broaden, more buyers in commuter belts and urban centers can adopt high-efficiency washers and dryers that align with time-of-use optimization.

Scotland contributes a smaller share by value but has outsized policy relevance because its 2045 net-zero target amplifies the economics of efficient electric appliances, especially in areas with higher winter heating loads. Combined grants and loans improve the payback period for heat pumps and support complementary upgrades in laundry and refrigeration. Premium refrigeration with longevity and precise temperature management resonates with owner-occupiers who prefer to reduce replacement frequency and invest in quality. Wales benefits from targeted efficiency programs for rental and owner-occupied stock, with activity clustered around Cardiff and Swansea, and budget constraints shaping product mixes. In these devolved nations, installer capacity and support networks influence the speed and type of appliance upgrades that accompany heating and fabric retrofits.

Northern Ireland leads growth at a 4.28% CAGR through 2031, as the Windsor Framework enables dual-market access and simpler compliance for products that meet EU-aligned labelling requirements in that jurisdiction. This reduces friction for retailers serving both NI and GB customers and can lower working capital tied up in duplicate stock. Public funding programs continue to back rural household efficiency, encouraging replacement of pre-2010 units across refrigeration and laundry. In Belfast and Derry/Londonderry, smart-appliance adoption aligns with fiber and 5G availability, while cross-border pricing dynamics around the Euro and Sterling influence shopping in border counties. The United Kingdom home appliances market benefits when these regional pockets of policy support and connectivity translate into broader adoption of efficient, connected products.

Competitive Landscape

Competition is moderately fragmented, with BSH Hausgeräte, Beko Europe, Haier, Samsung, and LG as leading groups that span value to premium positions in the United Kingdom home appliances market. Beko Europe integrated Whirlpool EMEA brands Hotpoint and Indesit into its portfolio, consolidating share and broadening its price ladder under a single operating structure. Premium differentiation rests on AI features, design customization, and robust software roadmaps that extend device lifecycles through updates and remote diagnostics. Connected ecosystems are becoming a core part of brand identity as platforms expand interoperability and security features to support smart tariffs and grid services.

Recent product cycles highlight larger bets on embedded intelligence. Samsung’s CES line-up introduced conversational AI on Family Hub refrigerators and updated robotic cleaning platforms, matched by longevity commitments for software updates and Knox Matrix security. LG widened its AI Core-Tech footprint in refrigeration and cooking, including camera-assisted cooking and Ingredient recognition that connects with ThinQ Food. Dyson’s 2025 Berlin event introduced multiple cordless and robotic cleaning devices, including a wet-dry robot for stain detection and a slim cordless vacuum designed for ease of use. Beko’s IFA presentation highlighted AI-enabled laundry efficiencies and quieter heat-pump dryers as part of its HomeWhiz platform, reinforcing the brand’s value-to-tech narrative. As right-to-repair rules mature and extended parts availability becomes standard, support costs and service design are becoming points of competition alongside upfront pricing.

Ecosystem partnerships connect appliances with the energy system. Haier’s collaboration with Octopus Energy uses time-of-use windows to lower washing costs for customers who schedule overnight washes, reinforcing off-peak arbitrage and flexibility value. National Grid ESO’s Demand Flexibility Service provides a template for recurring incentives to shift scheduleable loads during peak times, creating an option for appliance makers to layer energy services subscriptions on top of hardware. Security and privacy have become system requirements rather than optional extras, and manufacturers are positioning hardware-level safeguards to build trust and encourage wider consumer participation. As these capabilities spread through product lines, the United Kingdom home appliances market can see more durable differentiation based on software support, grid-ready features, and service reliability.

United Kingdom Home Appliances Industry Leaders

Beko (Arçelik)

Bosch

Haier

Samsung Electronics UK

Electrolux Group (AEG)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Dyson launched the pencilwash in the United Kingdom, a wet-and-dry floor cleaner that mirrors the ultra-slim 38 mm diameter design of the pencilvac series. It is designed for modern, compact homes in the United Kingdom, offering 30 minutes of runtime and the ability to lie flat to clean under furniture as low as 15 cm.

- January 2026: At CES 2026, Samsung introduced the bespoke AI refrigerator family hub and AI wine cellar, marking the first integration of Google Gemini into home appliances. The Gemini-powered AI vision inside now identifies a broader range of food items, including processed foods and user-labeled containers, without manual registration. It also features a brief now, which provides personalized daily schedules and nutritional insights directly on the refrigerator screen.

- July 2025: The Department for Energy Security and Net Zero launched a consultation to raise ecodesign and energy labeling standards for household tumble dryers. The proposal seeks to phase out inefficient vented and condenser models in favor of heat pump technology, moving to a new a-g energy scale. It also proposes a mandatory repairability index, effective from 2027, to ensure spare parts remain available for 10 years.

United Kingdom Home Appliances Market Report Scope

A home appliance refers to a domestic electrical or mechanical device designed to assist with routine household tasks such as cooking, cleaning, food preservation, and climate control, thereby improving convenience and efficiency in daily life. The United Kingdom home appliances market encompasses both large household equipment used for core home operations and smaller countertop or portable devices used for food preparation, beverage making, and cleaning.

The United Kingdom Home Appliances Market is segmented by Product, Distribution Channel, and Geography. By product, the market is divided into Major Home Appliances and Small Home Appliances. Major appliances include refrigerators, freezers, washing machines, dishwashers, ovens (including combi and microwave ovens), air conditioners, and other major appliances. Small appliances include coffee makers, food processors, grills and roasters, electric kettles, juicers and blenders, air fryers, vacuum cleaners, electric rice cookers, toasters, countertop ovens, and other small appliances. By distribution channel, the market is segmented into multi-brand stores, exclusive brand outlets, online channels, and other distribution channels. Geographically, the market analysis covers England, Scotland, Wales, and Northern Ireland. The report provides market size and forecasts for the United Kingdom home appliances market in value (USD million) across all the above segments.

By Product

| Major Home Appliances | Refrigerators |

| Freezers | |

| Washing Machines | |

| Dishwashers | |

| Ovens (Incl. Combi & Microwave) | |

| Air Conditioners | |

| Other Major Home Appliances | |

| Small Home Appliances | Coffee Makers |

| Food Processors | |

| Grills & Roasters | |

| Electric Kettles | |

| Juicers & Blenders | |

| Air Fryers | |

| Vacuum Cleaners | |

| Electric Rice Cookers | |

| Toasters | |

| Counter-top Ovens | |

| Other Small Home Appliances |

By Distribution Channel

| Multi-Brand Stores |

| Exclusive Brand Outlets |

| Online |

| Other Distribution Channels |

By Geography

| England |

| Scotland |

| Wales |

| Northern Ireland |

| By Product | Major Home Appliances | Refrigerators |

| Freezers | ||

| Washing Machines | ||

| Dishwashers | ||

| Ovens (Incl. Combi & Microwave) | ||

| Air Conditioners | ||

| Other Major Home Appliances | ||

| Small Home Appliances | Coffee Makers | |

| Food Processors | ||

| Grills & Roasters | ||

| Electric Kettles | ||

| Juicers & Blenders | ||

| Air Fryers | ||

| Vacuum Cleaners | ||

| Electric Rice Cookers | ||

| Toasters | ||

| Counter-top Ovens | ||

| Other Small Home Appliances | ||

| By Distribution Channel | Multi-Brand Stores | |

| Exclusive Brand Outlets | ||

| Online | ||

| Other Distribution Channels | ||

| By Geography | England | |

| Scotland | ||

| Wales | ||

| Northern Ireland | ||

Key Questions Answered in the Report

What is the size and growth outlook for the United Kingdom home appliances market in 2026?

The United Kingdom home appliances market size is USD 11.91 billion in 2026 and is projected to reach USD 13.62 billion by 2031, with a 2.72% CAGR over 2026-2031.

Which product category holds the largest share in the United Kingdom home appliances market?

Refrigerators led with a 24.78% revenue share in 2025, driven by mandatory placement and visible energy savings.

Which channel is growing fastest in the United Kingdom home appliances market?

Online is projected to grow at a 4.06% CAGR through 2031 as better tools, delivery, and returns enhance convenience.

Which region is expanding fastest within the United Kingdom home appliances market?

Northern Ireland is the fastest growing, with a 4.28% CAGR projected through 2031, supported by dual-market access under the Windsor Framework.

What policies are most shaping demand in the United Kingdom home appliances market today?

Energy label rescaling, repairability and ecodesign consultations, the Clean Heat Market Mechanism, and smart appliance standards are key, supported by time-of-use tariffs and National Grid ESO flexibility programs.

Page last updated on: