Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

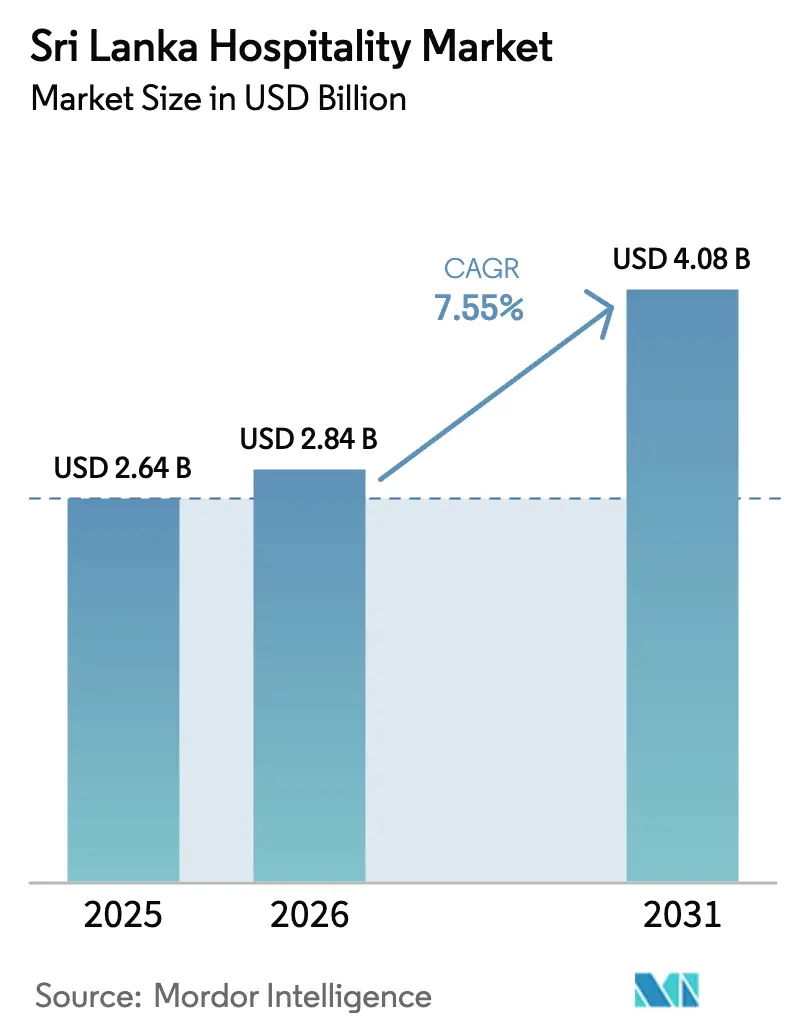

| Base Year Market Size (2025) | USD 2.64 Billion |

| Market Size (2026) | USD 2.84 Billion |

| Market Size (2031) | USD 4.08 Billion |

| Growth Rate (2026 - 2031) | 7.55% CAGR |

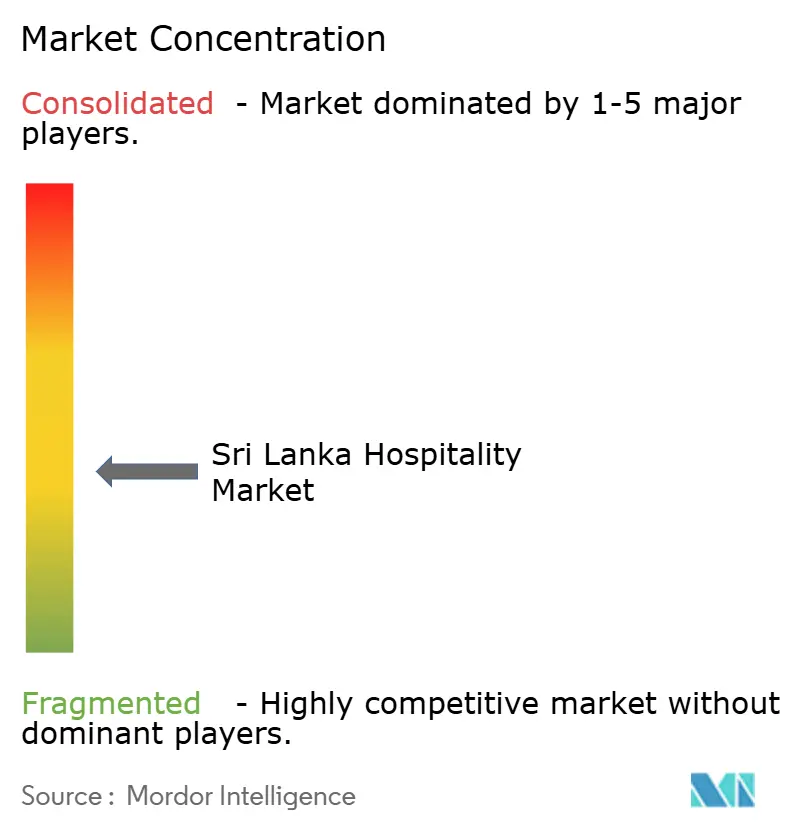

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Sri Lanka Hospitality Market Analysis by Mordor Intelligence

The Sri Lanka Hospitality Market size is projected to expand from USD 2.64 billion in 2025 and USD 2.84 billion in 2026 to USD 4.08 billion by 2031, registering a CAGR of 7.55% between 2026 to 2031.

The sector’s recovery gained significant momentum in 2024, as international tourist arrivals increased to approximately 2.05 million, representing a 38% year-on-year growth. This resurgence generated an estimated USD 3.17 billion in foreign-exchange earnings, the highest level recorded since the pre-pandemic period, underscoring the sector’s renewed economic contribution. [1]Sri Lanka Tourism Development Authority, “Monthly Tourist Arrivals Reports 2024,” SLTDA Publications, sltda.gov.lk. A broad-based recovery across leisure, MICE, and wellness tourism segments is driving growth. Macroeconomic stabilization under the IMF Extended Fund Facility has strengthened policy credibility, improved fiscal discipline, and restored investor confidence following the country’s recent economic crisis. The sustained rebound in international arrivals during 2024 has translated into stronger occupancy levels and increased demand across accommodation categories.

Ongoing investments in branded and integrated developments, including projects such as City of Dreams Colombo, are expanding the appeal of Sri Lanka to high-spending travelers while supporting premium average daily rates (ADRs). Hotel operators are also increasingly adopting AI-driven revenue-management and dynamic pricing systems to optimize short booking windows, protect revenue per available room (RevPAR), and reduce dependency on high-commission distribution channels. Policy support through designated Tourism Corridors and Port City Colombo continues to stimulate investment in both upscale and midscale segments. Nevertheless, the market faces ongoing challenges, including cautious credit underwriting by financial institutions and exposure to foreign-exchange volatility, which may constrain capital expenditure planning. Overall, improving macroeconomic fundamentals, rising tourist inflows, and strategic investments position Sri Lanka’s hospitality sector for sustained medium-term growth, despite lingering financial and currency-related risks.

Key Report Takeaways

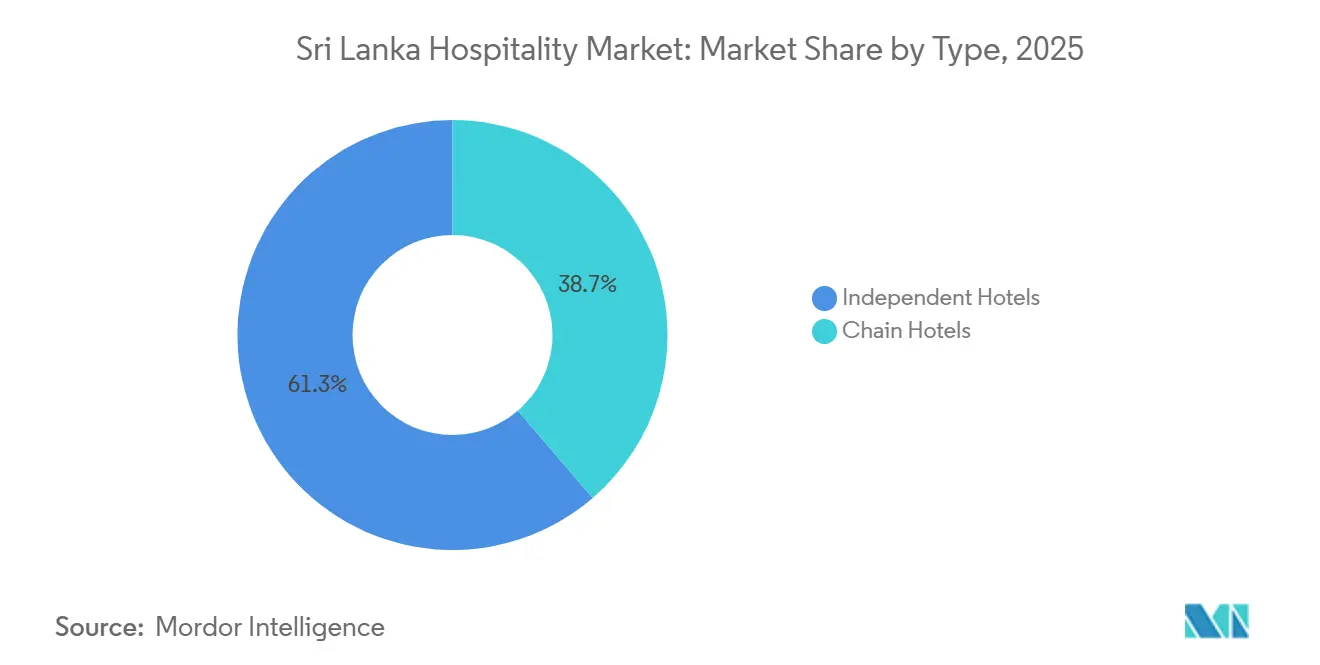

- By type, independent hotels held 61.25% of Sri Lanka hospitality market share in 2025, while chain operators are forecast to expand at a 7.81% CAGR through 2031.

- By accommodation class, mid and upper-mid-scale properties accounted for 42.25% of Sri Lanka hospitality market share in 2025, while the luxury tier is projected to grow at 8.11% annually to 2031.

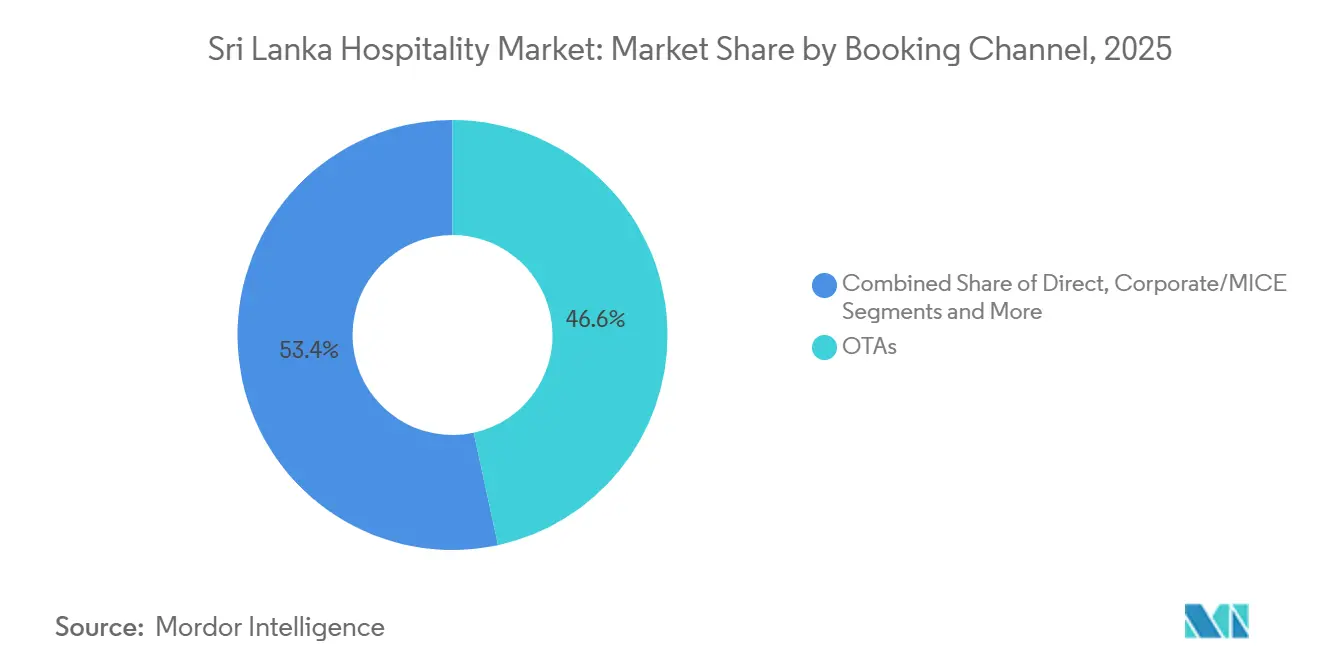

- By booking channel, online travel agencies captured 46.61% of Sri Lanka hospitality market share in 2025, while direct-digital channels are set to expand at an 8.35% CAGR through 2031.

- By geography, Colombo and the Western Province accounted for 53.48% of Sri Lanka hospitality market share in 2025, while the Eastern Province is the fastest-growing region with a projected 9.56% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Sri Lanka Hospitality Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Island Circuit Tourism Increasing Multi-Destination Travel | 0.90% | Multi-Destination Tourism Corridors | Short term (≤ 2 years) |

| Ayurveda Heritage Creating Specialized Wellness Hospitality | 0.70% | Wellness Retreat Destinations | Medium term (2–4 years) |

| Wildlife Tourism Supporting Nature-Based Accommodation | 0.60% | Safari & Eco-Lodge Zones | Medium term (2–4 years) |

| Boutique Colonial Property Conversion Expanding Unique Stays | 0.50% | Heritage Hospitality Conversions | Long term (≥ 4 years) |

| Beach Resort Development Supporting Coastal Tourism Growth | 0.80% | Coastal Resort Development | Medium term (2–4 years) |

| Indian Ocean Position Supporting Regional Leisure Travel | 0.60% | International Gateway Tourism Hub | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Island Circuit Tourism Increasing Multi-Destination Travel

Sri Lanka’s compact geography makes it well suited for multi-stop circuit travel, with nine UNESCO World Heritage Sites, eight national parks, more than 1,000 kilometers of coastline, and highland tea country concentrated on an island the size of Ireland. Based on current tourism targets and projections, the island expects to welcome more than 223,000 international visitors in January 2026, close 2025 with a record 2.36 million total arrivals, and reach the government’s target of 3 million arrivals by the end of 2026. The classic Colombo–Kandy–Galle–South Coast loop remains relevant, but it is no longer the only major circuit. Travelers in 2025–2026 are expected to extend into new circuits that include Kalpitiya (lagoons, dolphin migrations, and kitesurfing), the Jaffna Peninsula and its offshore islands such as Delft (Tamil heritage, rawness, and northern culture), Gal Oya (boat safaris), Madulsima, and Belihuloya (hiking and misty valleys). The expansion of Jaffna International Airport is expected to open the northern territories to international tourism for the first time in decades, helping distribute visitor flows beyond established southern routes. Purpose-driven journeys, slower travel, and destination layering—moving from the Cultural Triangle to a wildlife zone, then to the coast and a wellness retreat within a single trip—are increasingly defining the travel product. This multi-destination demand structure is prompting hospitality operators across the island to invest in quality accommodation, directly supporting room inventory growth, increased occupancy potential, and higher ADRs in previously underserved circuits.

Ayurveda Heritage Creating Specialized Wellness Hospitality

Sri Lanka’s more than 2,500-year-old indigenous Hela-Ayurveda and Hela Wedakama healing traditions have catalyzed a distinct, fast-growing segment within its hospitality sector. In 2026, BookRetreats.com, a global retreat-booking platform, ranked Sri Lanka as the world’s top trending wellness destination, citing a 100% year-on-year increase in visitor interest and placing the country ahead of Australia, Morocco, England, and Spain[2]Travel and Tour World, “XRC4PKRO6M41” (use the article's actual title if available), Travel and Tour World, travelandtourworld.com. Sri Lanka hosts more than 100 registered Ayurveda resorts, as well as licensed Ayurveda hospitals, certified spa clinics, and multi-specialty wellness institutions in Colombo and across the island. Core hospitality offerings include Panchakarma detoxification programs, gut-health protocols using native ingredients, yoga, meditation, and forest therapy. The Sri Lanka Tourism Promotion Bureau and the Sri Lanka Export Development Board have positioned wellness as a strategic pillar, supported by THASL-affiliated operators that participate in global travel fairs, digital campaigns, and international exhibitions. Visitor data from 2024–2025 indicates that wellness or Ayurvedic interests primarily motivated 0.6%–1.1% of international arrivals, and this share continues to increase as awareness grows. Since May 2026, Sri Lanka has waived tourist visa fees for travelers from 40 countries, further lowering entry barriers for wellness-motivated long-stay travelers. This high-value demographic typically spends more per day and books longer stays, directly supporting the growth of specialized wellness hospitality properties.

Wildlife Tourism Supporting Nature-Based Accommodation

Wildlife tourism remains one of Sri Lanka's most structurally important hospitality demand drivers, with more than 50% of foreign tourists visiting at least one national park, up from approximately 30% a decade ago. For the first half of 2025, projections indicate that Yala National Park will attract more than 380,000 visitors and generate over LKR 1.6 billion (USD 5 million) in revenue, making it the highest-income generator among individual parks[3]Mongabay, “In Sri Lanka, Animals Pay the Price for Overcrowding and Speeding Jeeps,” Mongabay, news.mongabay.com. In 2024, Sri Lanka's wildlife parks attracted an estimated 44% of total tourist arrivals, while foreign ticket revenue accounted for 94.7% of total park earnings. The Department of Wildlife Conservation reported total tourism revenue of LKR 8.815 billion (USD 0.03 billion) in 2024.

The country’s high density of national parks, with 22 open to tourists, including Yala, Udawalawe, Wilpattu, Minneriya, and Horton Plains, spans geographically distinct regions and supports strong demand for nearby accommodation. This demand has directly catalyzed a sub-sector of eco-lodges, luxury glamping camps, boutique safari retreats, and jungle villas located along park peripheries. Properties such as VerdEra Wild (Wilpattu), Wilds Wilpattu, Yakaduru Yala, Sigiri Vananthara, and Wild Elephant Reach are expected to open or expand in 2025–2026 to serve this demand. The government's proposed 2026 park management plans, including limiting jeep numbers at Yala Block I to 250–300 and opening less-trafficked blocks, aim to distribute wildlife tourism demand more evenly across the island and create new accommodation investment opportunities beyond the established Yala corridor.

Boutique Colonial Property Conversion Expanding Unique Stays

The adaptive reuse of Sri Lanka's colonial-era architectural stock, including British planter bungalows, Dutch walauwa mansions, tea factory buildings, and heritage residences, is creating a growing pipeline of distinctive boutique hospitality assets that command significant RevPAR premiums over standard hotel inventory. Several high-profile conversions are scheduled to enter the market or have been announced for 2025–2026. Newburgh Ella – The Tea Factory Resort by Browns Hotels & Resorts, a century-old estate originally established in 1903 by Scottish planter George Thomson, is scheduled to open on January 30, 2026, bringing an industrial-heritage narrative to the Ella highlands[4]The Sunday Times Sri Lanka, “Newburgh Ella Tea Factory Resort: Browns Hotels Bring a Century of Tea Heritage to Life,” The Sunday Times Sri Lanka, sundaytimes.lk. Uga Ghiri, a restored early-1900s colonial manor overlooking the Nine Arch Bridge in Ella, is scheduled to open in July 2026 with 15 private villas and jacuzzis. Jetwing Wahawa Walauwa in Rambukkana, an 1870s aristocratic mansion featuring intricate woodwork and antique-inspired furnishings, operates as a fully converted luxury all-suite boutique villa. Jetwing Ratnam Residence in Colombo, a Geoffrey Bawa-designed private home from 1979, is expected to open as a four-room boutique property in late 2025. Uga Halloowella, a British-era bungalow on a 252-acre tea estate near Castlereagh Reservoir, serves as the group's sixth heritage property. International demand for place-specific hospitality is driving these conversions, as travelers increasingly seek architectural authenticity and curated local narratives that new-build properties cannot replicate. Sri Lanka's tea country, coastal corridors, and cultural triangle continue to offer a significant pipeline of eligible colonial properties.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Economic Volatility and Currency Fluctuations Affect Hospitality Investment Confidence | −0.8% | Hospitality Investment Risk Areas | Short term (≤ 2 years) |

| Limited Large-Scale Tourism Infrastructure Restricts Expansion Beyond Established Destinations | −0.6% | Tourism Infrastructure Deficit Regions | Long term (≥ 4 years) |

| Dependence on Seasonal International Tourism Causes Revenue Fluctuations | −0.7% | Seasonal Demand Volatility | Medium term (2–4 years) |

| Limited Premium Accommodation Inventory Outside Main Tourist Zones | −0.5% | Accommodation Supply Gap Regions | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Economic Volatility and Currency Fluctuations Affect Hospitality Investment Confidence

Sri Lanka’s post-2022 economic recovery remains notable but structurally fragile, creating meaningful uncertainty for hospitality investment decisions. The Sri Lankan rupee is expected to depreciate from LKR 292/USD at end-2024 to LKR 308/USD by November 2025, increasing the local-currency cost of imported furniture, fixtures, HVAC systems, and construction materials used in hotel refurbishments and new builds. Properties that rely on European stone, imported fittings, or international FF&E suppliers are likely to face materially higher foreign-exchange exposure, prompting a strategic shift toward localized sourcing and phased capex. Currency volatility further increases the sensitivity of multi-year investment return calculations. IRR models for hotel developments remain highly exposed to exchange rate assumptions, making long-horizon commitments riskier for both domestic and foreign developers. At the macroeconomic level, tourism earnings, expected to total USD 3.22 billion in 2025 and to account for an estimated 12% of GDP, including multiplier effects, remain a critical pillar of foreign exchange reserves. When tourism revenues contract, as projected in H1 2026 with an 11.8% year-on-year decline, current account pressure is likely to increase, the rupee may weaken, import costs may rise, and the broader investment climate may tighten. The 2026 Middle East conflict-related airspace disruptions are expected to cause nearly 2,000 flight cancellations, directly reducing arrivals and showing how external geopolitical shocks can quickly translate into domestic macroeconomic imbalances. These risks may further deter the long-term capital commitments required for large-scale hospitality development.

Limited Large-Scale Tourism Infrastructure Restricts Expansion Beyond Established Destinations

Despite projected arrivals of 2.36 million in 2025 and an ambitious target of 3 million arrivals by 2026, Sri Lanka’s tourism infrastructure remains structurally inadequate to support the expansion of hospitality investment into secondary and tertiary destinations. Bandaranaike International Airport (BIA), which handles most international passenger traffic, is expected to operate at or beyond efficient capacity during peak periods, with congestion, extended immigration queues, and processing bottlenecks reported as key concerns. The planned Phase II expansion, which aims to reach 24.2 million annual passengers by 2055, is unlikely to provide near-term relief, according to infrastructure experts. A complementary Terminal II expansion supported by Japan is still in the planning stage, while the original BIA development has faced years of delays following the 2022 debt restructuring. Domestically, rail disruptions in key tourist corridors, such as Kandy–Nuwara Eliya and Ella, following Cyclone Ditwah in late 2025, could isolate highland destinations for extended periods, with Nuwara Eliya’s tourism industry still not fully recovered seven months after the cyclone. Road and utility infrastructure outside the Colombo–Galle–Kandy–Ella circuit remains insufficient to support high-volume hospitality investment. Cultural sites, including Sigiriya, which generates approximately 25% of cultural tourist traffic, lack adequate lighting, safety infrastructure, and emergency protocols. Hospitality developers targeting secondary destinations face higher infrastructure costs, unreliable last-mile connectivity, and greater project risk, which restrict the expansion of quality accommodation beyond the established tourist belt.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Independents Retain Share as Chains Deploy Loyalty Platforms

Independent hotels held 61.25% of inventory in 2025, the largest slice of the Sri Lanka hospitality market share, as owners leverage proximity to local attractions and personalized itineraries that resonate with value-seeking travelers. Chain operators are projected to grow at a 7.81% CAGR through 2031, supported by loyalty ecosystems and revenue tools that lift direct bookings while deepening engagement with repeat guests. Cinnamon’s entry into Global Hotel Alliance’s DISCOVERY platform positions its Sri Lanka and Maldives properties to harvest cross-brand demand and promote member-only offers that compete with OTA discounts. New flags introduced by Minor Hotels, including NH Collection Colombo and NH Bentota Ceysands, signal confidence in the Sri Lanka hospitality market and add corporate-focused and leisure-focused inventory that meets distinct traveler archetypes. BOI’s 2025 recalibration, which lowered thresholds and extended tax holidays in Tourism Corridors, gives both independents and chains optionality to develop secondary destinations where returns hinge on product-market fit rather than pure footfall.

Independents increasingly pivot to direct digital marketing to capture margin from travelers seeking immersive experiences, while chains deploy enterprise-grade CMS and marketing automation to optimize conversion and lifetime value across segments. Renewable energy retrofits by listed operators such as Jetwing Symphony show how capex can de-risk utility exposure and enhance sustainability credentials with European tour operators that value verified standards. Chain groups scale AI-enabled revenue management that recalibrates rates intraday, which helps protect RevPAR during event-driven surges and soft patches that are common in coastal submarkets. Certification uptake remains a differentiator as national schemes align with global criteria, giving certified properties a procurement edge for B2B contracting. The Sri Lanka hospitality industry therefore shows a two-speed structure where digital sophistication, energy management, and loyalty capabilities separate performance leaders from peers across both urban and resort footprints.

By Accommodation Class: Luxury Tier Expands Fastest Despite Mid-Scale Dominance

Mid and upper-mid-scale properties accounted for 42.25% in 2025, anchoring the value segment of the Sri Lanka hospitality market as regional brands and corporate-focused hotels balance price and amenities for business and leisure stays. The luxury segment expands at 8.11% annually on rising wellness and MICE demand, supported by new large-format inventory and a pipeline that targets high-yield travelers who prioritize spa, design, and culinary depth. Shangri-La’s 2024 disclosures show a marked RevPAR rebound in Colombo tied to occupancy and rate gains, reinforcing the recovery trajectory of top-tier city assets in line with broader destination momentum. Refurbishment programs at mid-scale resorts, including work disclosed by Aitken Spence, aim to capture wellness-adjacent demand through spa and F&B upgrades that narrow the experiential gap with five-star competitors. The Sri Lanka hospitality market, therefore, sustains a barbell profile where midscale remains the volume anchor while luxury delivers the fastest value creation through rate leadership and lift in ancillary revenue.

Budget and economy properties retain relevance through domestic leisure and backpack segments, yet face rising operating costs that emphasize the need for efficiency in housekeeping and front-office deployment. Service apartments in Colombo attract extended stays from digital nomads and relocating executives, which smooths seasonality and complements short-stay hotel demand around the CBD and embassy districts. Luxury city and resort properties absorb MICE and wellness spill-over as Port City Colombo’s events calendar scales, putting pressure on five-star supply during peak periods and creating opportunities for premium ADRs. Midscale and upper-midscale operators continue to enhance product through room renovations and food and beverage concepts that target rising European and regional travelers seeking value-plus propositions. The Sri Lanka hospitality industry maintains a layered structure where each class plays a distinct role in both recovery and expansion cycles into 2031.

By Booking Channel: Direct Digital Surges as Chains Reclaim Margin from OTAs

Online travel agencies held 46.61% of bookings in 2025, the largest share of distribution, while direct-digital channels are set to expand at an 8.35% CAGR on the back of loyalty, content personalization, and owned-media investments. Chains deploy AI-powered pricing and segmented offers across web, app, and email to convert OTA browsers into members who unlock lower net rates and on-property benefits. MICE and corporate bookings command premium ADRs relative to leisure OTA flows, which motivates operators to allocate inventory to wholesale and direct corporate contracts with bundled F&B and transport. Even so, traditional agents retain relevance for long-stay visas and complex group itineraries, while consumer discovery continues to originate on OTA and metasearch platforms. The Sri Lanka hospitality market responds by refining content and merchandising on owned channels to protect margin while maintaining visibility within high-traffic marketplaces.

Technology providers expand their footprint across PMS, channel management, and dynamic pricing, which compresses the gap between supplier capabilities when deployed at scale. Within Sri Lanka, chains capture early advantages from integrated stacks that connect rate, inventory, and marketing automation, while independents adopt modular solutions as budgets allow. The digital-nomad visa also reshapes direct booking behavior because guests negotiating monthly stays often bypass OTAs and book directly with property managers to secure inclusive rates. Operators report higher conversion on refreshed websites that emphasize long-stay offers and work-friendly amenities, which supports the growth trajectory for direct channels. Over the forecast period, the Sri Lanka hospitality market maintains a hybrid distribution model, with owned channels expanding net yield while OTAs reach anchors, discovery, and shoulder-season demand.

Geography Analysis

Colombo and the Western Province account for 53.48% of Sri Lanka’s hotel inventory, driven by the concentration of five-star, upper-midscale, and serviced-apartment stock. This concentration supports MICE demand and leisure spill-over, anchored by Port City Colombo’s convention infrastructure. Seasonal booking patterns in coastal Colombo suburbs and Negombo influence allocation strategies across OTAs, wholesale, and direct corporate channels. Multi-year urban projects increasingly integrate mixed-use elements, feeding restaurants, retail, and entertainment during shoulder periods. Overall, Colombo functions as the capacity and brand anchor while enabling expansion into underserved zones with lower land and utility costs.

The Southern Coast contributes significant resort capacity, including heritage, surf, and wellness nodes that attract longer-stay European travelers. Operators manage monsoon-driven volatility using rate ladders and promotions, protecting occupancy without compromising brand positioning. Hill-country circuits around Kandy, Ella, and Nuwara Eliya provide cultural, wellness, and hiking experiences that extend lengths of stay. Infrastructure investments in utilities, water management, and renewable energy at flagship properties support ESG objectives and cost control. These inland and coastal offerings balance beach-driven seasonality, creating year-round experiences for domestic and international visitors.

The Eastern Province is projected to grow at a 9.56% CAGR, supported by surf lodges, eco-resorts, and upscale developments along the underdeveloped coastline. Improved connectivity and spill-over from Colombo enhance weekend and week-long itineraries, appealing to both experiential and value travelers. Northern districts remain nascent and require further investment in access and utilities before larger sponsors commit capital. Regional certification programs and community integration are expected to influence procurement and European tour-operator contracting. Collectively, the geographic strategy pairs a mature Western core with a rapidly developing Eastern corridor, raising national ADR and diversifying the visitor mix.

Competitive Landscape

The Sri Lanka hospitality market exhibits moderate concentration, with leading operators holding a significant share of classified rooms across city and resort portfolios. Domestic brands leverage balance-sheet strength and brand equity to expand through management agreements, select leases, and asset-light growth models. International entrants rely on capital-light management contracts to enter Colombo and resort districts, where scale economics depend on occupancy stability and food and beverage capture. ESG credentials have become a key differentiator with European partners, as published certifications and renewable energy initiatives improve access to distribution networks and corporate RFPs. Overall, the market rewards operators that combine loyalty, technology, and sustainability in strategies aligned with destination strengths.

Technology adoption remains a core driver of competitive advantage, with chains upgrading revenue management systems, content management platforms, and customer relationship tools to improve conversion and yield. Lagging responsiveness leaves revenue unrealized, reinforcing the need for automated workflows in rate-setting and channel management. Corporate and MICE demand concentrates around properties with event capacity, while resort-based MICE benefits from coastal locations where package economics justify transport and F&B minimums. Energy-management investments help stabilize operating costs while meeting sustainability certification standards in key source markets. Property teams also test direct-channel offers and dynamic ancillaries to protect net ADR during periods of intense competition.

Innovation manifests in both product and process, with portfolio owners exploring proprietary energy solutions and sustainability-linked refurbishments to enhance operational efficiency and rate flexibility. LEED, ISO, and GSTC-aligned practices strengthen reputational capital and improve access to procurement lists that require verified ESG impact. Partnerships with global loyalty networks extend market reach and create cross-selling opportunities across city and resort properties. Operators balance OTA visibility with growth in owned channels, refining parity strategies in the absence of explicit local enforcement on rate clauses. As the market evolves, competitive advantage favors brands that integrate technology, sustainability, and disciplined distribution to deliver consistent performance across seasonal cycles.

Sri Lanka Hospitality Industry Leaders

Jetwing Hotels PLC

Cinnamon Hotels & Resorts

Aitken Spence Hotels

Hilton & DoubleTree Sri Lanka

Minor Hotels (Anantara/Avani)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Marriott International signed a seven-hotel portfolio agreement with Ventive Hospitality covering 1,548 keys across multiple brands, including a Ritz-Carlton Reserve in Pottuvil targeted to ultra-luxury wellness travelers.

- January 2025: Cinnamon Hotels & Resorts joined Global Hotel Alliance’s DISCOVERY program, opening access to a 30-million-member ecosystem that supports direct bookings and member-rate strategies at properties including the City of Dreams flagship.

- March 2025: Jetwing Symphony completed solar PV installations totaling 1,075 kW across select properties, with surplus energy exported under net-metering agreements disclosed in filings.

- December 2024: TAL Lanka Hotels disclosed investments in building, plant, and furnishings upgrades at Taj Samudra Colombo to strengthen competitive positioning within the five-star set.

Sri Lanka Hospitality Market Report Scope

The hospitality industry encompasses businesses offering accommodation, food and beverages, travel, and leisure services to both domestic and international tourists. This sector is pivotal for generating employment, boosting tourism, and bolstering the nation's service-driven economy.

The Sri Lanka Hospitality Market is Segmented by Type (Chain Hotels, Independent Hotels), Accommodation Class (Luxury, Mid & Upper-Mid-scale, Budget & Economy, Service Apartments), Booking Channel (Direct Digital, OTAs, Corporate/MICE, Wholesale & Traditional Agents), and Geography (Colombo & Western Province, Southern Coast, Central & Hill Country, Eastern Province, Northern Province, Other Regions).

By Type

| Chain Hotels |

| Independent Hotels |

By Accommodation Class

| Luxury |

| Mid & Upper-Mid-scale |

| Budget & Economy |

| Service Apartments |

By Booking Channel

| Direct Digital |

| OTAs |

| Corporate / MICE |

| Wholesale & Traditional Agents |

By Geographic Region

| Colombo & Western Province |

| Southern Coast |

| Central & Hill Country |

| Eastern Province |

| Northern Province |

| Other Regions |

| By Type | Chain Hotels |

| Independent Hotels | |

| By Accommodation Class | Luxury |

| Mid & Upper-Mid-scale | |

| Budget & Economy | |

| Service Apartments | |

| By Booking Channel | Direct Digital |

| OTAs | |

| Corporate / MICE | |

| Wholesale & Traditional Agents | |

| By Geographic Region | Colombo & Western Province |

| Southern Coast | |

| Central & Hill Country | |

| Eastern Province | |

| Northern Province | |

| Other Regions |

Key Questions Answered in the Report

What is the size and growth outlook for the Sri Lanka hospitality market through 2031?

The Sri Lanka hospitality market size is USD 2.84 billion in 2026 and is projected to reach USD 4.08 billion by 2031 at a 7.55% CAGR, supported by a broad-based recovery in leisure, wellness, and MICE demand.

Which segments are growing fastest within the Sri Lanka hospitality market and why?

The luxury tier grows at 8.11% annually on rising European wellness and Indian MICE demand, while direct-digital booking channels expand at an 8.35% CAGR as chains use loyalty and AI to reduce OTA commissions.

How concentrated is competition, and who leads the Sri Lanka hospitality market?

The top five operators control 40.7% of classified rooms, led by Jetwing, Cinnamon, Aitken Spence, Hilton, and Minor Hotels, while independents still dominate with 61.25% of inventory in 2025.

Which regions should investors prioritize in the Sri Lanka hospitality market over the next five years?

Colombo and the Western Province hold 53.48% of the inventory and anchor MICE-led growth, while the Eastern Province leads expansion at a 9.56% CAGR on surf, eco-tourism, and improving connectivity.

How are distribution channels shifting, and what is the margin impact in the Sri Lanka hospitality market?

OTAs hold 46.61% of bookings in 2025, but direct-digital is the fastest growing channel at 8.35% CAGR, helping operators cut 15–18% commissions and lift net ADR through member-only rates and personalization.

Page last updated on: