Healthcare Training And Education Services Outsourcing Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

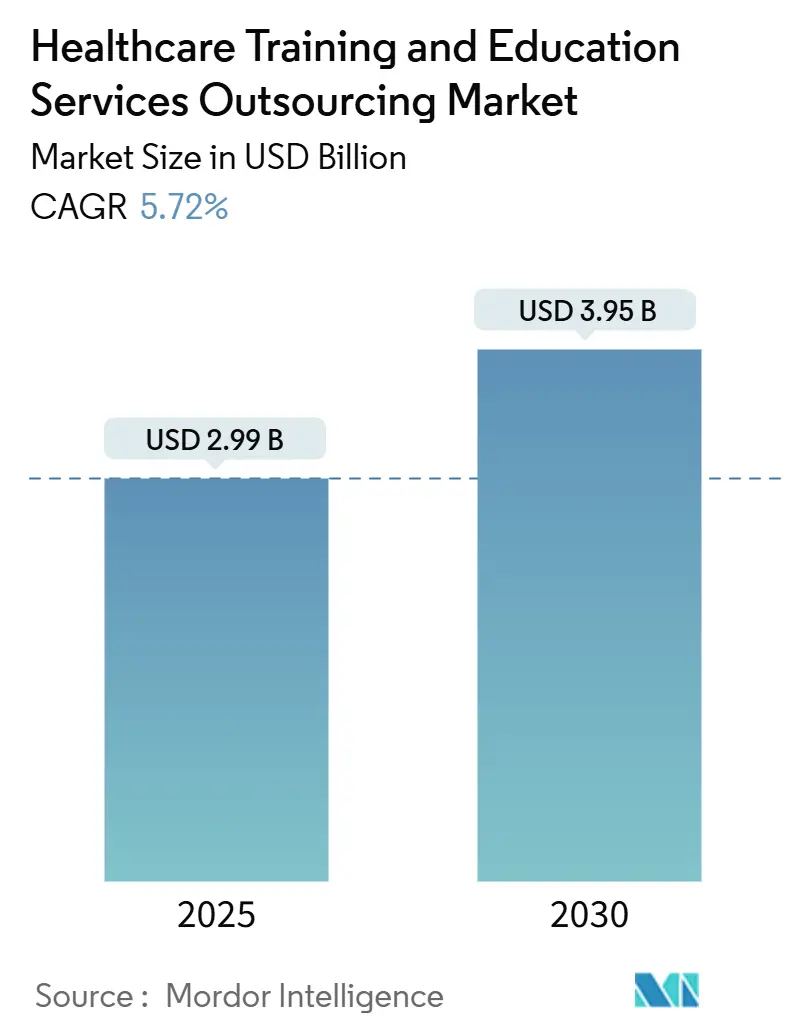

| Market Size (2025) | USD 2.99 Billion |

| Market Size (2030) | USD 3.95 Billion |

| Growth Rate (2025 - 2030) | 5.72% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Healthcare Training And Education Services Outsourcing Market Analysis by Mordor Intelligence

The Healthcare Training And Education Services Outsourcing market size stood at USD 2.99 billion in 2025 and is forecast to advance to USD 3.95 billion by 2030, expanding at a 5.72% CAGR. The growth reflects providers’ pivot toward external experts who can manage rising instructional complexity while containing costs.[1]OpusVi, “A Lookback on 2024: What Will Be Crucial in 2025's Healthcare Industry to Address Workforce Challenges?,” OpusVi, opusvi.com Demand is bolstered by fresh regulatory mandates such as the U.S. MATE Act’s 8-hour opioid‐prescribing coursework requirement, which pushes organizations toward turnkey compliance programs. Rapid virtual‐reality simulation uptake, strong investment in AI-driven personalization tools, and escalating device sophistication all reinforce market momentum. North American health systems keep spending to meet strict CME standards, yet Southeast Asian hospitals are the fastest adopters of immersive platforms as they modernize workforces and attract foreign trainees. Cost pressures are equally pivotal because hospitals measure residency-program ROI in avoided turnover, with one U.S. network reporting USD 16.3 million savings after outsourcing nursing‐residency training.

Key Report Takeaways

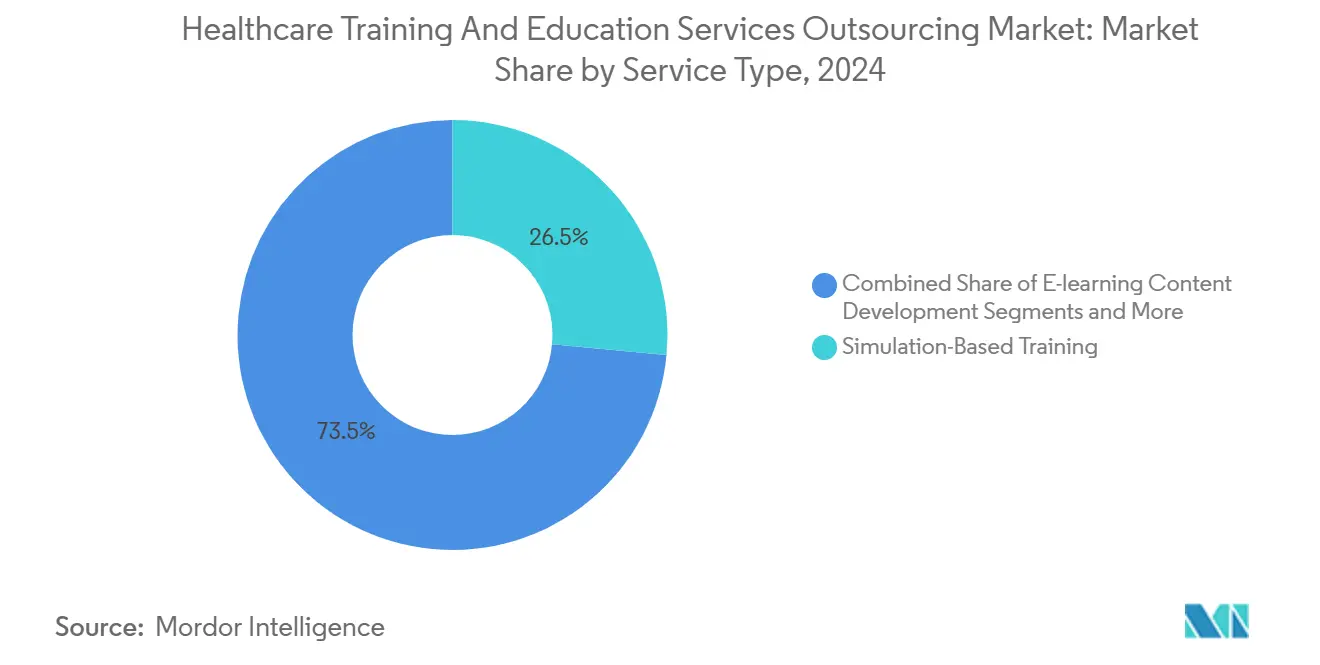

- By service type, simulation-based training led with 26.48% revenue share in 2024 and is advancing at an 8.89% CAGR through 2030.

- By delivery mode, on-site instructor-led programs held 34.38% of the Healthcare Training And Education Services Outsourcing market share in 2024, while virtual and augmented-reality modules record the quickest rise at an 8.47% CAGR.

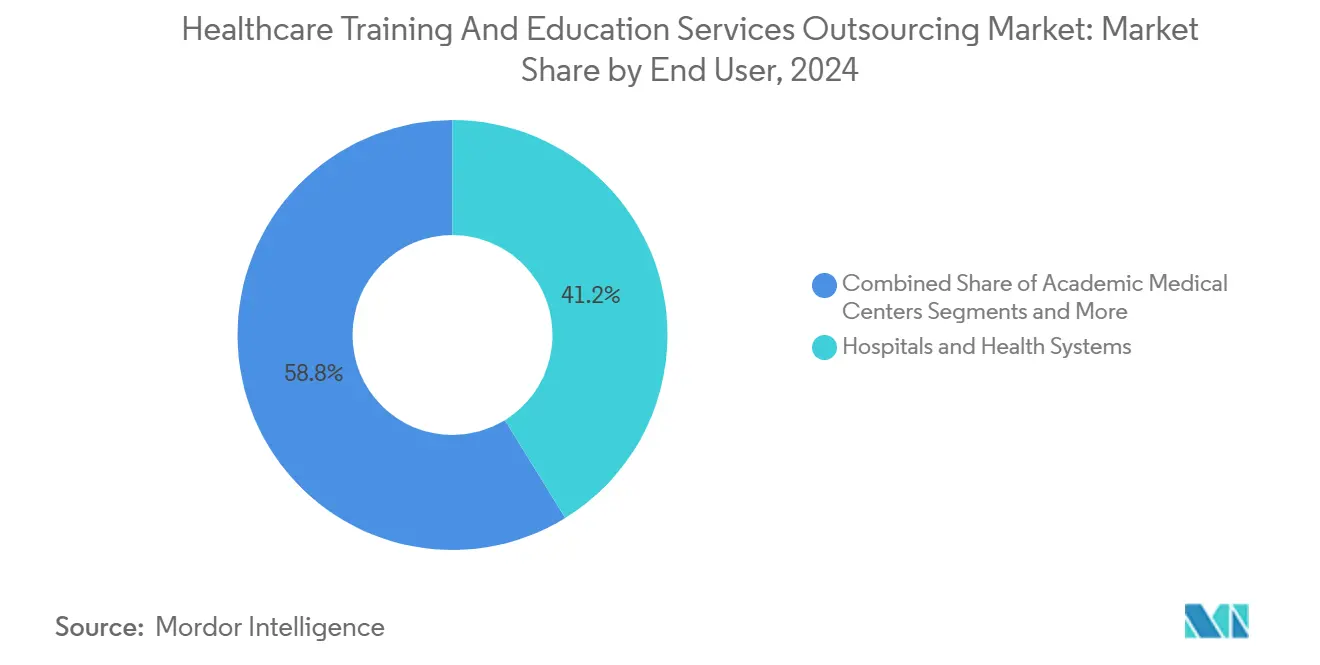

- By end-user, hospitals and health systems accounted for 41.22% of the Healthcare Training And Education Services Outsourcing market size in 2024; home healthcare and long-term care facilities post the fastest 9.88% CAGR.

- By provider type, specialist outsourcing firms captured 29.48% share in 2024, whereas IT and BPO providers show the steepest 9.37% CAGR.

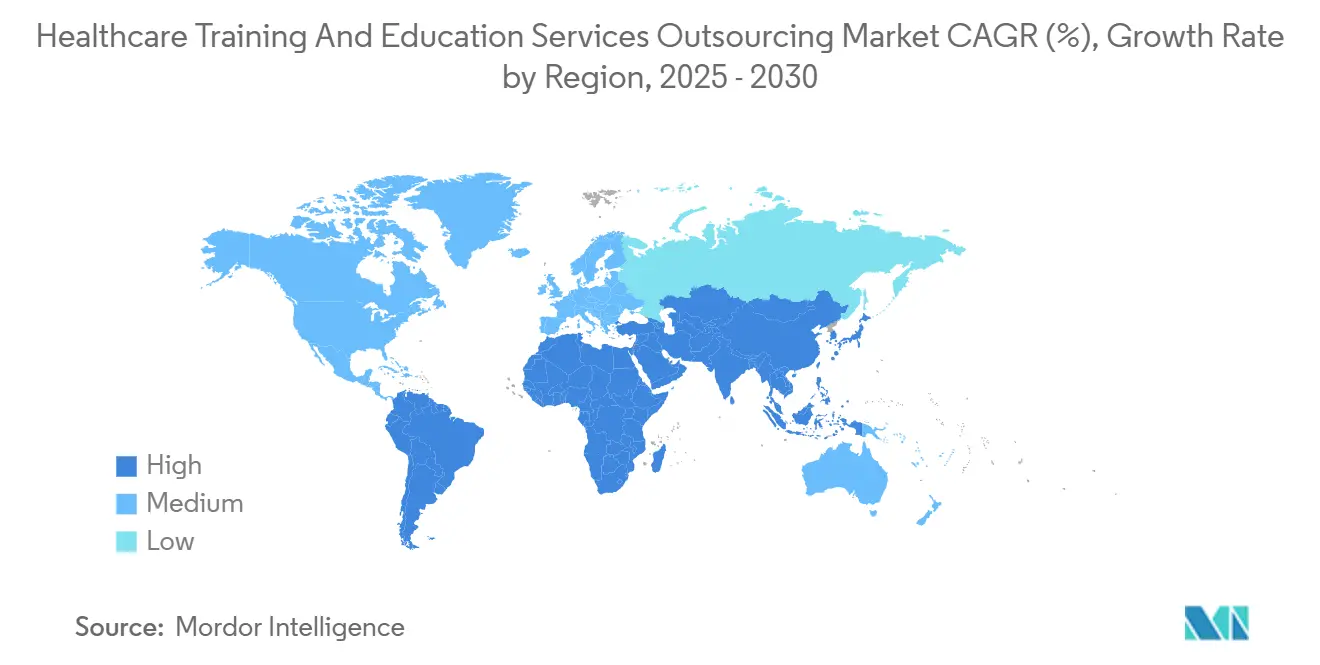

- By geography, North America retained 36.67% share in 2024, while Asia-Pacific is projected to climb at a 7.48% CAGR through 2030.

Global Healthcare Training And Education Services Outsourcing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growth of e-learning and digital simulations | +1.2% | Global, early gains in North America and Europe | Medium term (2–4 years) |

| Rising complexity of medical devices | +1.0% | Global, concentrated in developed markets | Long term (≥ 4 years) |

| Regulatory mandates for CME | +0.9% | North America and EU, expanding to Asia-Pacific | Short term (≤ 2 years) |

| Cost pressures and outsourcing | +0.8% | Global, strongest in cost-sensitive markets | Short term (≤ 2 years) |

| AI-driven personalized learning | +0.7% | North America, EU, select Asia-Pacific economies | Medium term (2–4 years) |

| Bundled training within value-based BPO | +0.6% | North America, emerging in EU | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Growth of E-Learning & Digital Simulation Platforms

Health systems now deploy immersive virtual reality suites that deliver repeatable skill practice without access to expensive cadaver labs. A multicenter study using the RetinaVR simulator for eye surgery showed strong proficiency gains among residents, illustrating how simulation expands access to rare procedures.[2]Fares Antaki et al., “RetinaVR: Democratizing Vitreoretinal Surgery Training with a Portable Simulator,” arXiv, arxiv.org AI-linked dashboards such as Stanford’s Data Ocean curate adaptive lessons that kept 92% of enrollees on track, a completion level rarely achieved by static modules. Multisensory manikins now include tactile cues so learners feel pulses and tissue resistance, sharpening diagnostic accuracy. Nursing programs that embed virtual clinical rotations report problem-solving effect sizes up to 0.9, underscoring the pedagogic payback.[3]Abdalkarem Alsharari et al., “Effectiveness of Virtual Clinical Learning in Nursing Education,” BMC Nursing, bmc.comBecause these cloud platforms scale across sites, large health systems standardize curricula while smaller providers bypass costly bricks-and-mortar skills labs.

Rising Complexity of Medical Devices & Procedures

The EU Medical Device Regulation 2017/745 now obliges manufacturers to certify end-user competence, prompting many to hand content creation to niche vendors who understand regulatory language, risk-management files, and clinical-evaluation updates. In surgical robotics, iterative firmware releases outpace hospital educators, so outsourcing ensures teams receive just-in-time refreshers that align with software changes. Contract development and manufacturing firms expand portfolios to encompass design-for-training services, embedding instructional videos within device documentation. Multimodal programs include virtual walkthroughs of unique device identifiers and post-market surveillance dashboards, a depth impractical for in-house teams. The result is a steady revenue stream for external educators who bundle regulatory insight with technical mastery.

Regulatory Mandates for Continuous Medical Education (CME)

U.S. prescribers of controlled substances must now complete 8 hours on substance-use disorders, catalyzing turnkey compliance classes with standardized transcripts for credentialing audits. Podiatrists confront 20–50 annual credit-hour quotas that vary by state yet allow fully online fulfillment, pushing demand for scalable e-modules. Long-term-care nurses face 13 contact-hour updates to master the Minimum Data Set 3.0, an area many facilities outsource for consistency. International medical graduates must study at schools accredited by a World Federation for Medical Education–recognized agency to qualify for U.S. certification, creating cross-border training partnerships. Vendors that navigate multistate or multinational rules gain a clear competitive edge.

Cost Pressures Driving Outsourcing of Non-Core Training

Hospital CFOs increasingly treat training as an operating expense best delivered through service-level agreements, freeing internal staff for direct patient care. A U.S. hospital group’s nurse-residency outsourcing produced 92% retention and saved USD 16.3 million in avoided turnover, validating the financial logic. Nursing-home chains confront thin margins and high churn, so BPO vendors now package payroll, billing, and staff-education services in unified contracts, lowering per-learner costs through shared platforms. Outsourcing also sidesteps the need to license courseware engines, maintain servers, or track credential expirations. As apprenticeship-style upskilling gains favor, external providers supply structured roadmaps that internal HR teams would struggle to design and audit.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data security and patient-privacy compliance | -0.8% | Global, strictest in HIPAA and GDPR regions | Short term (≤ 2 years) |

| High initial platform-integration costs | -0.6% | Global, hardest for small providers | Medium term (2–4 years) |

| Cultural and language localization gaps | -0.5% | Global, acute in multilingual markets | Long term (≥ 4 years) |

| Cross-border accreditation recognition limits | -0.4% | International education hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Data Security & Patient-Privacy Compliance Challenges

Any outsourcer that touches protected health information must execute business-associate agreements and run HIPAA-grade audit trails, adding legal overhead and vendor-risk assessments that slow procurement. European clients layer GDPR consent-management requirements on top, creating dual compliance maps that complicate cloud hosting decisions. Non-compliance fines can exceed USD 1 million per incident, so hospitals insist on encryption and immutable log architectures. Emerging technologies such as homomorphic encryption promise secure computation but demand continuous staff re-training to stay current. The compliance burden creates procurement friction, especially for cross-border partnerships.

High Initial Platform Integration Costs

Electronic health record integrations require API development, sandbox testing, and clinician change-management sessions that can cost mid-size practices over USD 500,000 in the first year. Organizations working on tight margins may limit feature scope, downgrading analytics or simulation fidelity. Over time, deferred upgrades create workflow pain points and erode learning quality, forcing eventual reinvestment. Studies on corporate training budgets show that underfunded programs rarely deliver expected behavior changes, making CFOs skeptical of new requests. The barrier is particularly steep for community hospitals that lack grant support.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Simulation-Based Training Drives Innovation

Simulation-based programs represented 26.48% of the Healthcare Training And Education Services Outsourcing market size in 2024 and are forecast to expand at an 8.89% CAGR, the fastest among all service lines. Widespread VR echocardiography simulators now feature multi-user connectivity so geographically dispersed cardiology fellows practice collaboratively while sharing outcomes analytics. Clinical skills training still commands a substantial share because bedside competency remains foundational for licensure. Compliance and regulatory modules enjoy steady volume as device and pharmaceutical rules evolve, ensuring recurring revenue for outsourcers.

Simulation’s rise stems from its ability to replicate high-risk procedures without patient exposure. RetinaVR kits lower the cost-of-entry for ophthalmology departments that previously relied on costly wet labs. Adaptive e-learning built on AI curates personalized pathways that boost completion rates, shifting budgets away from lecture-heavy CME. Leadership and management instruction gains importance as health systems pivot to value-based reimbursement models that require agile decision-making. Across these offerings, vendors that blend tactile interfaces with analytics gain competitive traction because hospitals prioritize measurable competence gains.

By Delivery Mode: Virtual Reality Transforms Learning Experiences

On-site instructor-led sessions held 34.38% share of the Healthcare Training And Education Services Outsourcing market in 2024 thanks to direct mentoring in operating theaters. However, AR/VR modules will post an 8.47% CAGR through 2030, reflecting their growing role as institutions diversify learning portfolios. Self-paced e-learning retains popularity among clinicians juggling unpredictable schedules, while blended programs pair virtual classrooms with brief in-person labs to reinforce muscle memory.

Immersive headsets now project anatomically correct holograms that learners can palpate using haptic gloves, shortening the learning curve for invasive techniques. Mobile microlearning pushes five-minute case vignettes to phones during shift breaks, nudging continuous engagement. Pandemic-era adoption of virtual instructor-led training persists because travel budgets remain thin. Vendors differentiate by embedding AI tutors that analyze gaze patterns and response latencies, then recommend remedial clips in real time, a capability difficult to match in traditional classrooms.

By End-User: Home Healthcare Facilities Drive Rapid Adoption

Hospitals and health systems accounted for 41.22% of the Healthcare Training And Education Services Outsourcing market in 2024, reflecting their immense staffing bases and complex credential matrices. Academic medical centers supplement this demand as they test novel curricula before cascading them to affiliated sites. Life-sciences manufacturers outsource product-specific education to accelerate launches and satisfy post-market surveillance obligations.

Home healthcare and long-term care facilities will grow at a 9.88% CAGR, spurred by aging populations and staffing shortages that heighten training needs. Many operate on slim margins so they outsource to secure turnkey programs covering wound care, infusion therapy, and telehealth protocols. Nursing and allied-health schools partner with external providers to enrich simulation resources without capital expenditure. Payors bundle upskilling for care navigators within value-based contracts, while government agencies commission standardized courses to raise baseline competencies across rural clinics.

By Provider Type: IT Companies Reshape Training Delivery

Specialist educators commanded 29.48% of the 2024 Healthcare Training And Education Services Outsourcing market share due to domain depth and longstanding hospital ties. Yet IT and BPO providers will log a 9.37% CAGR because they pair cloud engineering with content design. OEMs continue running device-specific academies to safeguard brand reputation. Professional societies maintain certification grids, but their growth lags as digital natives gravitate to micro-credential platforms.

AI-first ecosystems like HealthStream HLX blend LMS functions with adaptive-recommendation engines so hospitals mine performance data while clinicians earn digital badges. MedCerts trains 15,000 learners annually using mixed-reality labs delivered entirely online, proving technology firms can scale healthcare curricula effectively. As IT vendors acquire niche educators, the competitive field blurs, giving hospitals integrated stacks that marry scheduling, credential tracking, and immersive content under single contracts.

Geography Analysis

North America captured 36.67% of 2024 revenue, anchored by stringent CME statutes and sophisticated provider IT ecosystems. U.S. systems leverage bundled contracts to streamline licensure tracking across multistate operations, while Canadian provinces fund simulation centers to offset rural clinical-placement shortages. The region also serves as an AI-curriculum test bed because vendors access rich EHR datasets that train recommendation models.

Europe follows as regulatory complexity around EU MDR and cross-border patient flows sparks demand for standardized multilingual training. German and French systems co-invest in joint e-learning repositories that satisfy both national and EU directives, reducing duplication. In the United Kingdom, integrated care boards fund virtual placements for community nurses to relieve clinical-site bottlenecks, a model that outsourcing firms replicate in Ireland and the Nordics.

Asia-Pacific will post a 7.48% CAGR through 2030, the swiftest worldwide. Hospitals in Singapore, Thailand, and Malaysia race to install VR labs to differentiate medical-tourism offerings. The Philippines positions itself as a medical-education hub where tuition ranging USD 2,000–6,000 attracts foreign students while aligning curricula with U.S. standards. Emerging Middle East and African markets invest in foundational CME to support expanding primary-care footprints. South American nations capitalize on tele-education networks that carry Spanish and Portuguese modules into remote Amazonian clinics, creating incremental demand for localization services.

Competitive Landscape

The Healthcare Training And Education Services Outsourcing industry is moderately fragmented, with tech-driven entrants raising stakes for traditional vendors. HealthStream spent USD 2.25 million acquiring Total Clinical Placement System and The Clinical Hub, stitching them into myClinicalExchange to orchestrate 285,000 rotations yearly. This network effect builds switching costs because universities embed roster management deeper into curricula.

OpusVi rebranded from Dignity Health Global Education and linked with ShiftMed to serve 350,000 frontline professionals, illustrating the potency of channel alliances that marry curriculum depth with workforce marketplaces. Adtalem and Hippocratic AI co-develop an ethics and workflow curriculum that folds into Chamberlain University degree tracks, signaling convergence between degree providers and AI startups. Pearson pairs with Microsoft to embed AI learning paths across its publishing catalog, expanding reach to non-traditional learners.

Competitive intensity centers on analytics, localization depth, and platform interoperability. Vendors that offer plug-and-play APIs plus pre-mapped CME credit registries occupy stronger negotiating positions. White-space remains in cultural-competence training; systematic reviews expose persistent skill gaps, especially in multilingual primary care. Companies that codify case libraries reflecting diverse social determinants of health can carve defensible niches even as platform commoditization grows.

Healthcare Training And Education Services Outsourcing Industry Leaders

HealthStream

Relias

Elsevier Clinical Solutions

GE HealthCare Education

Philips Healthcare Education

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Simplify Healthcare partnered with Atento to pilot a CX program powered by Xperience1, letting U.S. payers improve member and provider experience without upfront capital outlays.

- June 2025: The College of Health Care Professions launched its Intelligent Workforce Solutions group to deliver employer-centered training nationwide, appointing AJ Thomas as Chief Business Development Officer.

- January 2025: HealthStream released its AI-first HealthStream Learning Experience application to enhance personalized, self-directed learning and workforce retention across healthcare organizations.

Global Healthcare Training And Education Services Outsourcing Market Report Scope

| Clinical Skills Training |

| Compliance & Regulatory Training |

| Continuing Medical Education (CME) Courses |

| Simulation-Based Training |

| E-learning Content Development |

| Leadership & Management Training |

| On-site Instructor-led |

| Virtual Instructor-led (VILT) |

| Self-paced E-learning Modules |

| Blended Learning Programs |

| Mobile Microlearning |

| Virtual/AR Modules |

| Hospitals & Health Systems |

| Academic Medical Centers |

| Life Sciences & Medtech Companies |

| Nursing & Allied Health Schools |

| Payors & Insurance Companies |

| Government & Public Health Agencies |

| Home Healthcare & Long-term Care Facilities |

| Specialist Healthcare Training Outsourcing Firms |

| IT & BPO Service Providers |

| Medical Device & Pharma OEMs as Providers |

| Professional Associations & Societies |

| Universities & Academic Institutions |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Service Type | Clinical Skills Training | |

| Compliance & Regulatory Training | ||

| Continuing Medical Education (CME) Courses | ||

| Simulation-Based Training | ||

| E-learning Content Development | ||

| Leadership & Management Training | ||

| By Delivery Mode | On-site Instructor-led | |

| Virtual Instructor-led (VILT) | ||

| Self-paced E-learning Modules | ||

| Blended Learning Programs | ||

| Mobile Microlearning | ||

| Virtual/AR Modules | ||

| By End-user | Hospitals & Health Systems | |

| Academic Medical Centers | ||

| Life Sciences & Medtech Companies | ||

| Nursing & Allied Health Schools | ||

| Payors & Insurance Companies | ||

| Government & Public Health Agencies | ||

| Home Healthcare & Long-term Care Facilities | ||

| By Provider Type | Specialist Healthcare Training Outsourcing Firms | |

| IT & BPO Service Providers | ||

| Medical Device & Pharma OEMs as Providers | ||

| Professional Associations & Societies | ||

| Universities & Academic Institutions | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the Healthcare Training And Education Services Outsourcing market in 2025?

The market is valued at USD 2.99 billion in 2025 with a projected 5.72% CAGR to 2030.

Which service type generates the most revenue?

Simulation-based training leads with 26.48% share, reflecting strong demand for immersive learning.

What region shows the fastest growth?

Asia-Pacific is forecast to advance at a 7.48% CAGR through 2030 due to digital transformation and medical-education tourism.

Why are providers outsourcing training functions?

Outsourcing cuts development costs, accelerates compliance, and helped one U.S. network save USD 16.3 million by improving nurse retention.

How is AI influencing healthcare training?

AI engines personalize content, reduce time-to-competency, and power platforms like HealthStream HLX that recommend micro-lessons based on learner data.

Page last updated on: