Textile Composites Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

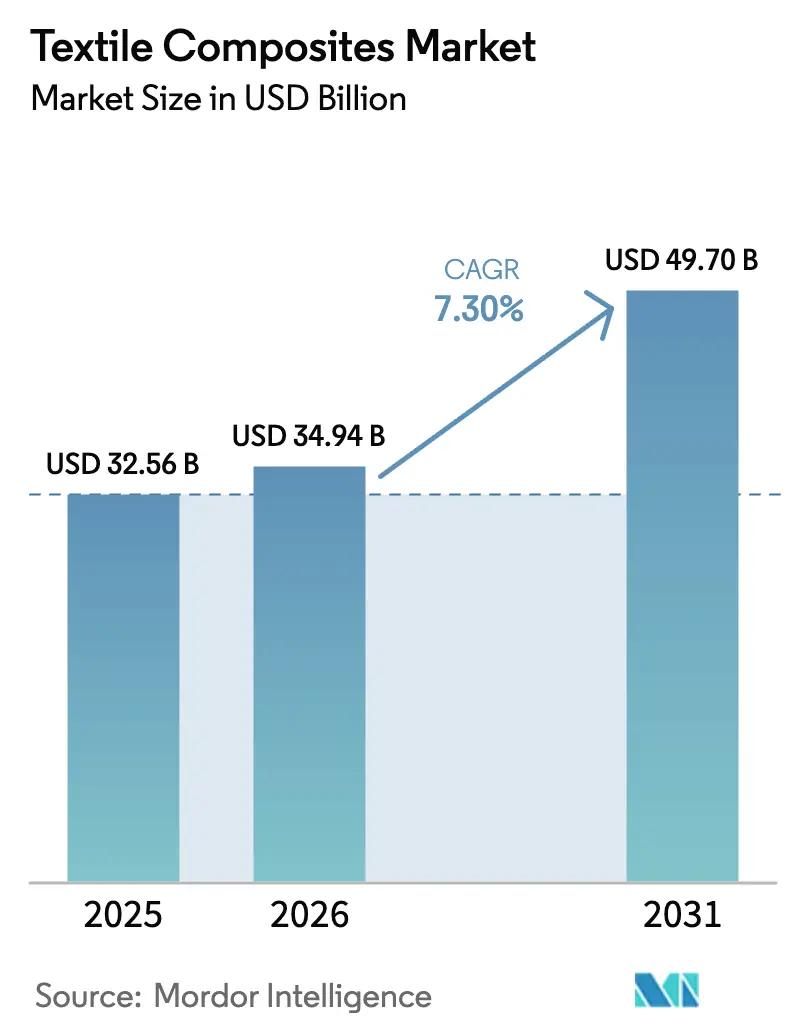

| Market Size (2026) | USD 34.94 Billion |

| Market Size (2031) | USD 49.70 Billion |

| Growth Rate (2026 - 2031) | 7.30% CAGR |

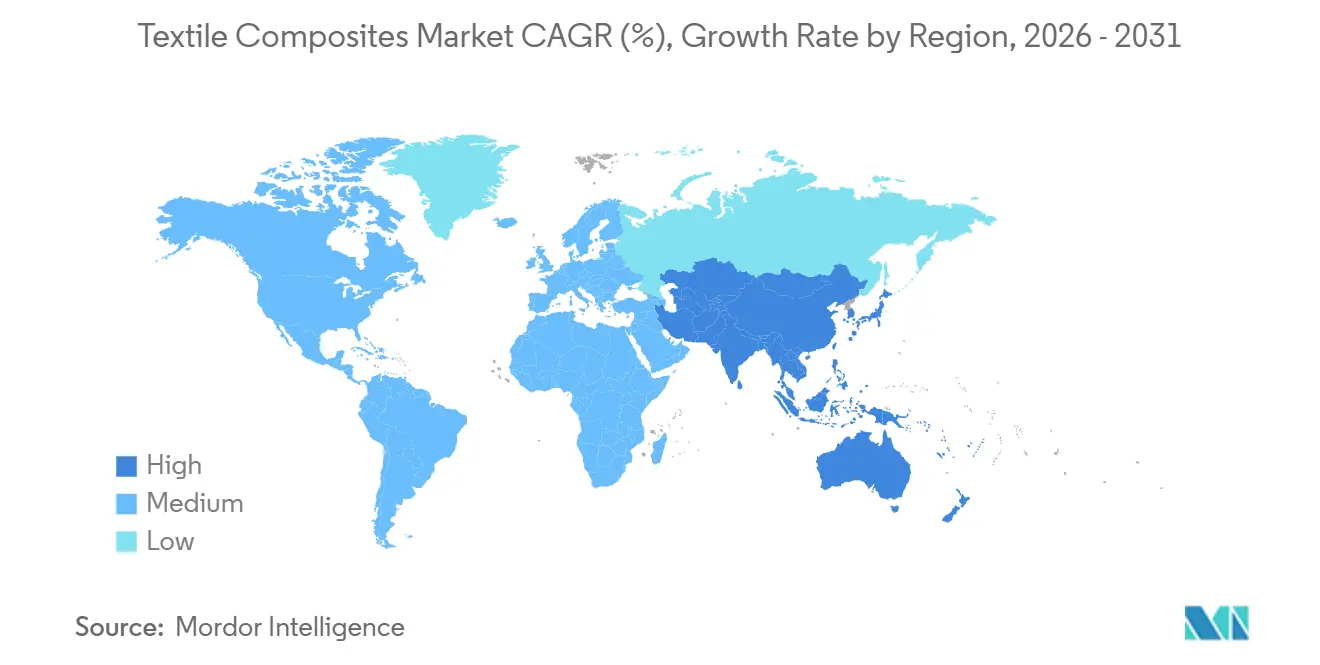

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

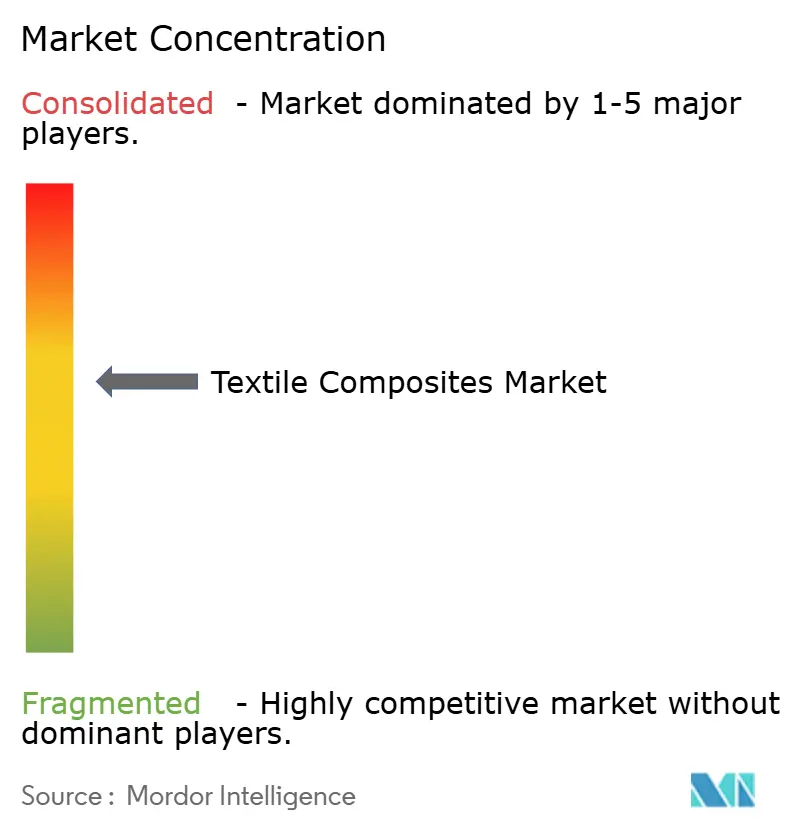

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Textile Composites Market Analysis by Mordor Intelligence

The Textile Composites Market size was valued at USD 32.56 billion in 2025 and is estimated to grow from USD 34.94 billion in 2026 to reach USD 49.70 billion by 2031, at a CAGR of 7.30% during the forecast period (2026-2031). Robust aircraft backlogs, offshore-wind turbine scale-ups, and policy-driven vehicle lightweighting continue to expand the addressable base for high-performance fabrics while commodity glass reinforcements protect cost-sensitive domains. Carbon fiber maintains pricing power despite USD 30–100 per kilogram tags because automated fiber placement now trims ply counts and labor hours in wide-body wings. Glass fiber retains dominance in marine and industrial tanks thanks to below-USD 3 per kilogram economics, though styrene emission rules in Europe are nudging builders toward epoxies. Aramid commands niche but irreplaceable roles in ballistic shielding and thermal barriers, with DuPont and Kolon preserving dual-source resiliency. Regionally, Asia-Pacific captures more than half of revenue as Chinese producers scale 12,000-ton carbon lines, but North American defense programs and European premium autos sustain pricing discipline.

Key Report Takeaways

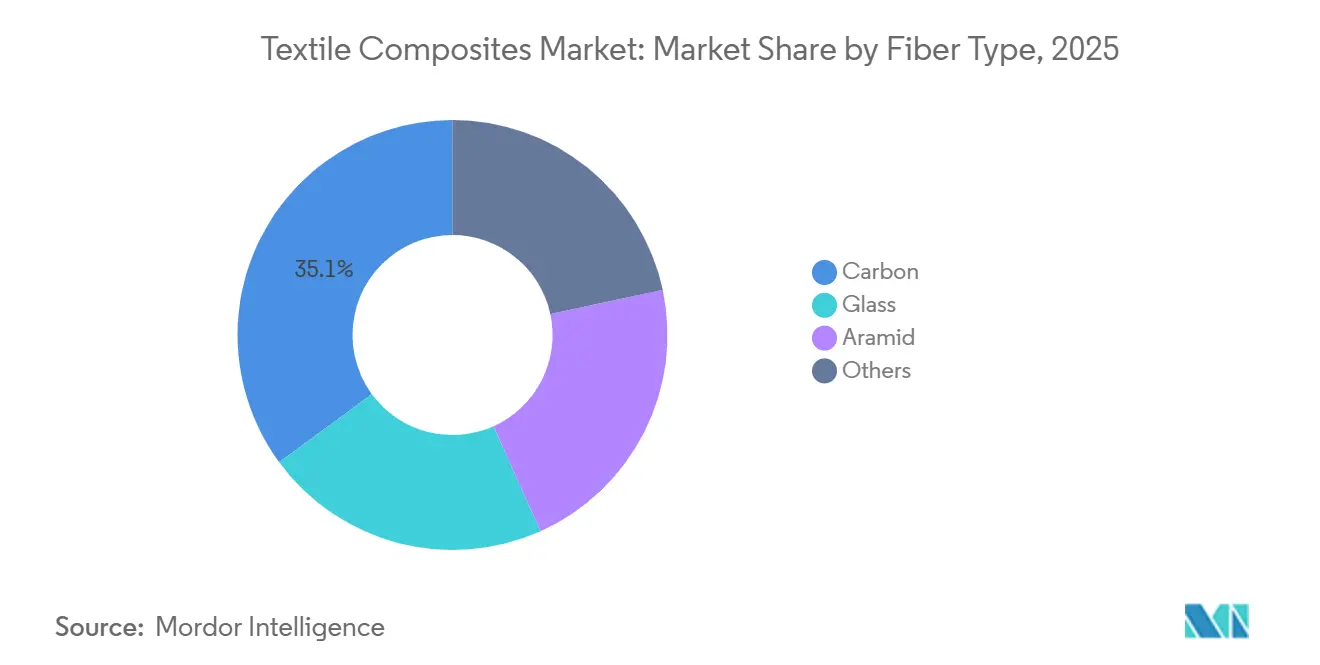

- By fiber type, carbon captured 35.07% of textile composites market share in 2025 while glass led volume but trailed value growth at a 4.6% CAGR to 2031.

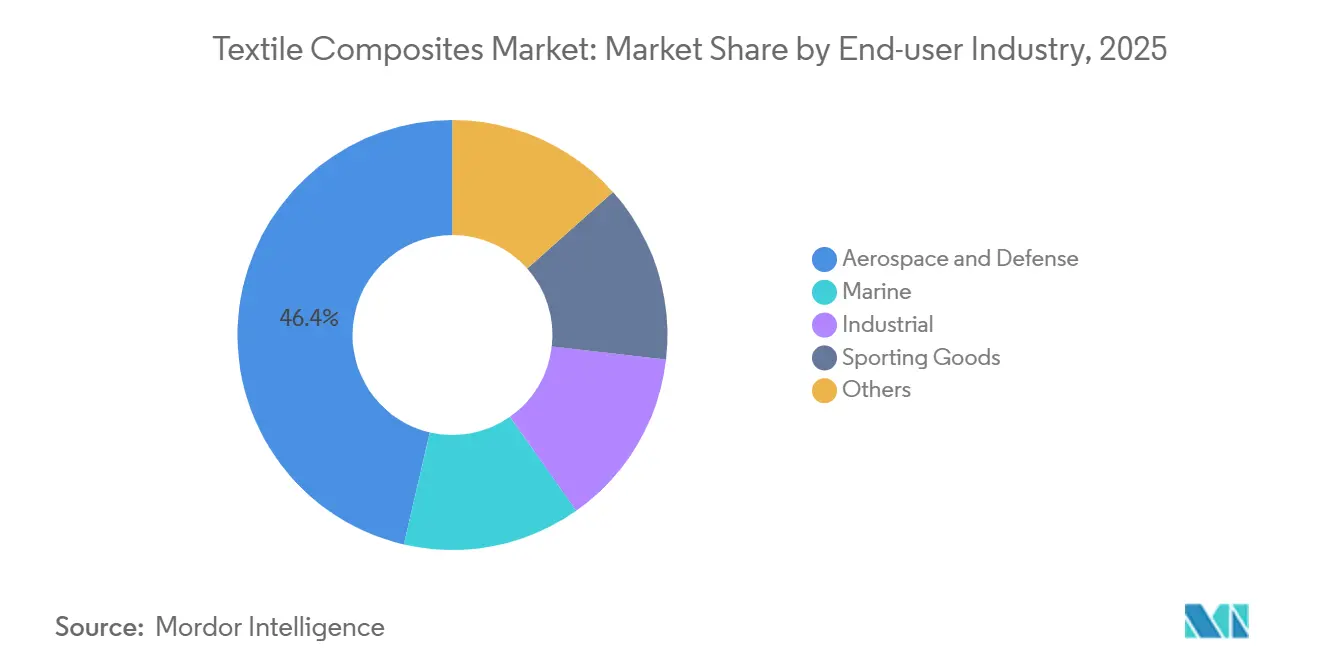

- By end-user industry, aerospace and defense held 46.35% of 2025 revenue whereas industrial pressure-vessel demand is projected to post the fastest 9.8% CAGR through 2031 on hydrogen-tank roll-outs.

- By geography, Asia-Pacific commanded 54.45% of 2025 sales and is set to expand at 8.34% annually to 2031, outpacing North America’s 5.9% trajectory.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Textile Composites Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand in commercial and military aerospace programs | +2.1% | Global, with concentration in North America, Europe, and APAC defense hubs | Long term (≥ 4 years) |

| Light-weighting push in automotive and high-performance EV platforms | +1.8% | North America, Europe, China EV corridors | Medium term (2-4 years) |

| Capacity additions in global wind-blade production | +1.5% | APAC offshore zones, North Sea, US Gulf Coast | Medium term (2-4 years) |

| Urban air-mobility (eVTOL) structures adoption | +0.9% | North America and EU certification zones, early APAC trials | Short term (≤ 2 years) |

| 3D-woven, fully recyclable preforms gaining OEM validation | +0.7% | EU circular-economy mandates, North America sustainability-linked finance | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand in Commercial and Military Aerospace Programs

Composite content in next-generation airframes accelerates as automated fiber placement cuts wing assembly hours by 30% on Boeing’s 777-8F while retaining 90,000-cycle fatigue life [1]Boeing Engineering Group, “777-8F Composite Wing Automation,” boeing.com. Airbus targets thermoplastic stringers for its future single-aisle jet, shifting from rivets to welds and shortening final-assembly flow. Defense jets entrench the pull-through; the F-35 program validates radar-transparent laminates that sustain 9-G loads and carrier-deck shocks, cementing multi-decade demand stability. Long certification cycles mean every design freeze locks in tonnage for 20 years, granting fiber suppliers forecast visibility. As passenger travel normalizes, the backlog shields composite consumption even when macro cycles soften aluminum demand.

Light-Weighting Push in Automotive and High-Performance EV Platforms

EV range sensitivity converts each kilogram saved into direct battery cost relief. BMW’s 2024 iX Carbon Cage trimmed 150 kilograms and delivered a 15-kilometer WLTP range gain while meeting side-impact standards. Yet mass-market programs temper adoption because carbon still costs 5 times stamped steel. Mercedes-Benz selectively reinforces roof rails and rear bulkheads but keeps primary crash zones metallic to exploit controlled deformation. Ultra-luxury sports cars emphasize stiffness over sheer mass; Porsche’s 911 GT3 RS leveraged carbon fenders principally for aerodynamic stability. Break-even shifts closer as battery density approaches 300 Wh/kg, making material premium bearable versus a fourth module.

Capacity Additions in Global Wind-Blade Production

Offshore turbines above 15 MW depend on carbon spar caps to survive 107-meter blade loads on GE’s Haliade-X platform. TPI Composites built 601 blade sets in Q3 2024 yet suffered margin squeeze from protracted resin-infusion cycles. Exel’s pultrusion line in India offers 40% cost relief, pressuring European factories to automate or relocate. Research into thermoplastic roots enabling bolted joints could slash field repair time, further enhancing carbon’s value proposition as maintenance OPEX outweighs CAPEX.

Urban Air-Mobility (eVTOL) Structures Adoption

Joby Aviation’s all-composite eVTOL gained FAA Part 135 authority in 2025, showing Toray’s T1100G can meet damage tolerance without hand lay-up. XTI employs resin-transfer molding to hold 0.3 millimeter tolerances on ducted-fan nacelles, a precision once exclusive to Formula 1. Because hover endurance scales 1.5 minutes per kilogram, OEMs willingly pay USD 80 per kilogram for prepreg, double wide-body spending norms. Regulators now accept 70% residual strength after impact rather than “no-damage-visible,” collapsing test timelines, and de-risking entry-into-service by two years.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Brittle failure and low impact resistance versus metals | -1.2% | Global, acute in North America and EU automotive crash-test regimes | Medium term (2-4 years) |

| High material and processing costs for medium-volume applications | -1.0% | North America and Europe mid-tier automotive, regional aerospace | Short term (≤ 2 years) |

| Emerging shortage of high-modulus PAN precursor grade carbon fiber | -0.8% | Global, concentrated in aerospace and wind-blade supply chains | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Brittle Failure and Low Impact Resistance Versus Metals

Small-overlap crash tests demand controlled buckling, a mechanism composites cannot match without 20-30% mass penalties. Invisible delaminations cut residual strength by up to 40% and force costly ultrasonic inspections that sheet metal ignores. Repair economics also hinder uptake; a damaged carbon door typically requires USD 2,500 replacement versus USD 400 steel panel dent-out, inflating fleet insurance premiums. Aerospace tolerates the trade-off because loads trend tensile, but ground vehicles face omnidirectional impacts that expose composite brittleness.

High Material and Processing Costs for Medium-Volume Applications

Resin-transfer molding lands near EUR 40 per kilogram landed cost, fivefold aluminum die-casting. Tool life favors metals: a carbon hood tool wears after 50,000 shots compared with 2 million for stamping dies, resulting in USD 3.00 versus USD 0.15 per-unit amortization. Even next-generation presses eject parts in 90 seconds, well behind 6-second steel strokes, requiring fifteen composite cells to match one metal press. Until cycle times halve, composites will focus on aerospace, racing, and ultra-premium trim where price elasticity is minimal.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Fiber Type: Carbon Extends Lead, Glass Guards Cost-Critical Niches

Carbon fiber contributed 35.07% of 2025 revenue and is projected to advance at 9.35% annually to 2031, adding almost 8 percentage points of textile composites market share through expanded aerospace wings and offshore blades. Toray’s 700 GPa T1100G lets designers cut wing-skin ply counts 15% without sacrificing bird-strike resilience, paring recurring material cost by USD 120,000 per twin-aisle jet. Glass fiber still accounts for the bulk tonnage in wind, marine, and tanks because sub-USD 3 per kilogram pricing overwhelms stiffness deficits; however, epoxy shifts prompted by styrene restrictions are eroding its cost moat in boats and recreational vehicles. Aramid holds a considerable value due to unrivaled heat resistance in ballistic and re-entry shields, with a U.S. critical-material designation spurring domestic capacity incentives[2]U.S. Department of Defense, “Critical Materials List 2024,” defense.gov. Natural flax and basalt inch toward the EU interior.

Aerospace shift to carbon standard-modulus variants has concentrated supply risk; Toray, Teijin, and Mitsubishi Chemical provide 65% of aerospace-grade volume, prompting Boeing and Airbus to qualify Chinese producer Weihai Guangwei by 2026 to hedge geopolitical disruption. Glass fiber’s marine demand faces the International Maritime Organization’s looming 2028 styrene cap, likely propelling epoxy substitution and nudging prices upward. Natural-fiber recyclability aligns with EU End-of-Life rules, yet moisture-ingress testing protocols still marginalize their structural ambitions.

By End-User Industry: Aerospace Dominates, Industrial Hydrogen Tanks Accelerate

Aerospace and defense commanded 46.35% of textile composites revenue in 2025 and will expand at an 8.17% CAGR, maintaining primacy in the textile composites market. The textile composites market size for aerospace alone is projected to reach USD 23 billion by 2031. Wide-body fuselages, stealth bombers, and growing drone fleets secure multi-decade contracts insulated from consumer cycles. Marine yachts exploit corrosion immunity; carbon superstructures on premium yachts sliced topside weight 1,200 kilograms, enhancing roll stability in 3-meter seas.

Sporting goods pay the steepest premiums; a USD 12,000 Specialized SL8 frame uses ultra-high-modulus plies to cut frame mass to 700 grams, showing discretionary buyers will pay USD 1,700 per saved kilogram. Industrial wind blades stay cost-anchored, but impending 120-meter designs require carbon caps, nudging glass out of spar segments by 2027. Collectively, end-user diversification reduces cyclicality; when airliner rates dip, wind and hydrogen projects prop up throughput, smoothing the revenue curve for converters.

Geography Analysis

Asia-Pacific captured 54.45% of 2025 sales and is forecast to compound at 8.34% to 2031, retaining the largest regional node of the textile composites market. Chinese producers like Jiangsu Hengshen add 12 000-ton lines, positioning the country to supply 40% of aerospace-grade fiber by 2028, albeit amid intellectual-property and export-control frictions. Japan’s incumbents still wield 48% of high-modulus capacity through long-term Boeing and Airbus contracts, but discounted Chinese standard-modulus threatens low-end share. South Korea pivots toward aramid and UHMWPE for defense contracts in Southeast Asia. India’s government-backed incentives subsidize 25% of capex for advanced-material plants, spurring Exel’s pultrusion exports to regional turbine OEMs.

Robust defense budgets and offshore wind blade factories along the Gulf Coast drive North America market growth. Hexcel’s USD 417 million Q3 2024 turnover hinged on F-35 and 787 builds but flagged potential 2025 softness if Boeing cuts rates. TPI’s U.S. blade sites ran at 68% utilization due to permitting delays, yet the Inflation Reduction Act’s domestic content bonuses could revive orders post-2026. Canada’s Montreal cluster battles labor costs as composite technicians earn CAD 45 per hour, prompting shift of low-critical parts to Mexico.

Europe accounts for a considerable market size owing to the established automotive industry. German automakers use selective carbon reinforcements where 3-times material premiums still yield return on range. Airbus’s thermoplastic stringer pivot strains local PEEK resin supply, and failure to scale beyond 500 tons could push program entry into service beyond 2030. Siemens Gamesa blades in Denmark and Spain will migrate to carbon for 120-meter rotor designs, adding EUR 200 million annual fiber demand. South America and the Middle East-Africa are witnessing growing demand for textile composites, with Brazil’s Embraer composite empennages and Saudi Arabia’s NEOM ordering GFRP rebar; yet both hinge on policy follow-through and supply-chain build-out.

Value Chain Analysis

The textile composites value chain starts upstream with polymer and fiber precursors (for example, PAN for carbon fiber and glass raw materials), then moves into fiber production for carbon, glass, aramid, and other reinforcement types, followed by sizing and finishing before conversion into technical textiles such as woven, knitted, braided, and multiaxial non-crimp fabrics (NCF) that serve as preforms. Midstream players include resin and prepreg compounders and composite part fabricators using resin transfer molding, compression molding, pultrusion, and filament winding, with downstream steps such as machining, joining, coating, and NDT/quality assurance that are particularly important for aerospace-qualified laminates.

Downstream demand comes from OEMs and Tier suppliers serving aerospace and defense, automotive, wind energy, marine, industrial tanks and pressure vessels, and sporting goods. Distribution is often routed through converter networks and qualified material lists for regulated programs. Bottlenecks concentrate around manufacturing rate and consistency, including tooling longevity for repeated cure cycles, balancing infusion quality with cycle time, and material standardization across programs. At the same time, circular-economy requirements are pushing adoption of recycled fiber streams and lower-fossil or bio-based matrix options, including EU-focused work such as CIRCUTEX that documents practices for circularity in fibrous composites.

Competitive Landscape

The textile composites market is moderately consolidated. Fiber precursor remains the strategic choke point, with Toray, Teijin, and Mitsubishi Chemical owning 65% of aerospace-grade capacity and locking OEMs into take-or-pay contracts. The leading players compete on faster out-of-autoclave cure cycles but face Chinese entrants offering room-temperature systems at 60% of Western prices. Vertical integration defines recent moves: Toray bought a U.S. prepreg line to satisfy Buy American mandates, and Owens Corning diversified glass output to India and Mexico to hedge tariff risk. Thermoplastic composites and recycling emerge as white-space arenas. Regulation filters entrants: FAA Part 25 certification spans 18-24 months and favors incumbents with design databases, whereas evolving IIHS and Euro-NCAP tests create room for hybrid composites balancing impact energy and stiffness.

Textile Composites Industry Leaders

TORAY INDUSTRIES, INC.

Owens Corning

Teijin Limited

Hexcel Corporation

Hyosung

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Near-term whitespace centers on higher-performance reinforcement architectures and qualification pathways that reduce the penalty of switching materials in regulated end uses. A specific example is the April 2026 AGY and SAERTEX joint development work on S-2 Glass multiaxial NCF architectures for structural composite applications across aerospace, defense, and mobility, which aims to improve specific properties while preserving glass-fiber cost advantages in weight-sensitive designs.

A second opportunity is the industrialization of lower-footprint composite systems and natural-fiber composites beyond interior trim, supported by visible OEM demonstrations and supplier portfolio moves. In June 2026, Bcomp delivered ampliTex biocomposite roof components for the BMW M Concept Neue Klasse, extending qualification activity toward exterior parts where surface, durability, and repeatability constraints are typically tighter than for cabin components. On the matrix side, suppliers are bringing recycled or reduced-fossil feedstock resin systems to market (for example, Syensqo adding MTM 58 ReGen and SolvaLite 714 ReGen grades showcased around JEC World 2026), creating procurement-friendly options for converters that need to document circularity without abandoning established high-rate composite processes.

Recent Industry Developments

- May 2026: Toray Advanced Composites expanded NCAMP qualifications for its Toray Cetex TC1225 LMPAEK thermoplastic composite material system, including additional T700 unidirectional tape prepreg formats. The added qualification scope supports broader adoption in aerospace and defense programs that rely on standardized, auditable material allowables for primary and secondary structures.

- April 2026: Owens Corning completed the sale of its global glass reinforcements business to Praana Group, closing on April 30, 2026, at a final enterprise value of USD 645 million. The ownership change reshapes competitive dynamics in glass-fiber reinforcements by moving capacity and customer relationships to a reinforcement-focused industrial group, while Owens Corning reallocates capital toward its core building-products portfolio.

- December 2024: Hexcel signed a five-year supply agreement with Airbus for A350 wing and fuselage prepregs. The multi-year commitment reinforces long-cycle aerospace demand visibility for qualified textile-based composite intermediates and strengthens the position of incumbent prepreg suppliers in certified commercial airframe programs.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the textile composites market covers composite materials that use textile-form fiber reinforcements (woven, knitted, braided, or nonwoven) combined with a resin matrix, and sold into end-use manufacturing where the composite part carries load.

Scope exclusions: We exclude conventional technical textiles that are not impregnated and cured into a composite structure, as well as purely metallic composites and raw fiber yarn trade that is not converted into composite materials.

Segmentation Overview

- By Fiber Type

- Carbon

- Glass

- Aramid

- Others

- By End-user Industry

- Aerospace and Defense

- Marine

- Industrial

- Sporting Goods

- Others

- By Geography

- Asia-Pacific

- China

- Japan

- India

- South Korea

- ASEAN Countries

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle-East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle-East and Africa

- Asia-Pacific

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts with defining what gets counted as textile composites and what does not, and then collecting the best public signals that can be tied to volumes and pricing. We rely on sources such as UN Comtrade trade statistics, the US International Trade Commission data releases, Eurostat industrial and trade tables, and national statistical offices that publish manufacturing output and producer price indicators.

To keep the model practical, we also use standards and technical references from groups such as ASTM and ISO, along with peer-reviewed materials journals that discuss adoption by process and end use. Company annual reports, investor presentations, and reputable industry news are used to confirm capacity additions, plant utilization commentary, and demand timing. Where needed, our analysts use paid subscriptions for company financials and intelligence, patent databases, and shipment-level import and export datasets to cross-check directional trends. These examples are not exhaustive, and many other public sources were also reviewed for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work is used to pressure-test the demand pool and pricing logic, especially where public datasets do not cleanly separate textile composites from adjacent composite materials. We speak with a mix of material suppliers, converters, distributors, and end-use manufacturing teams across APAC, EMEA, and the Americas so assumptions on application mix, resin selection, and typical selling prices can be confirmed, and then aligned to the final model.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 31% | CXOs: 17% | APAC: 46% |

| Mid tier: 52% | Functional/Unit leaders: 32% | EMEA: 34% |

| Smaller Players: 17% | Managers: 51% | Americas: 20% |

Market-Sizing & Forecasting

Sizing is built using a top-down approach where end-use composite demand pools are reconstructed and then filtered down to the share that is realistically served by textile-form reinforcements. We start from end-use output indicators and composite penetration signals, and then map them to textile composite usage in applications such as structural and semi-structural parts.

In the working model, a few inputs do most of the heavy lifting, such as aerospace build and delivery cadence, automotive lightweighting adoption by component, marine production cycles, industrial equipment output, and typical resin and fiber mix shifts that influence average selling prices. Pricing is handled through a blended ASP path by fiber type and process, and then converted consistently into USD using the same timing for exchange rates. Results are corroborated with selective bottom-up approximations, including sampled supplier revenue checks, channel feedback on volumes, and sanity checks using typical kg per part ranges, which are then used to adjust totals when gaps show up.

For forecasting, scenario analysis is used to reflect how fast penetration and pricing can move under different demand conditions, and the forward view is validated with what interviewees expect for order books and capacity utilization. Where company disclosures or public statistics leave holes, we fill gaps using conservative interpolation anchored to nearby years and then re-check the effect on the total market path.

Data Validation & Update Cycle

Outputs are validated by comparing implied volumes, prices, and growth rates against independent signals like trade movement, end-use production trends, and public commentary on composite substitution. When large variances appear by region or end use, the assumptions are revisited. If needed, respondents are re-contacted to confirm whether the change is real or caused by a definition mismatch.

Before sign-off, the model is reviewed in multiple steps, including peer checks on formulas, unit consistency, and the logic behind key drivers. The report is refreshed annually, and interim updates are made when material events occur, such as major capacity additions, sharp raw material price changes, or demand shocks in aerospace and automotive. Right before delivery, analysts perform a fresh scan so clients receive the latest updated view.

Mordor Intelligence's Textile Composites Market Size Measured Against Other Published Estimates

Published market sizes for textile composites can look far apart because the counted scope is not always the same, and because pricing and end-use coverage are handled differently across studies. Differences often show up when one estimate treats the market as a niche material category, while another rolls it into broader composites or counts only a few high-value end uses.

Key gaps usually come from whether figures include only textile reinforcement based composites or also add chopped-fiber composites, how resin systems are treated, and whether aerospace and defense demand is modeled using build cycles or simple growth assumptions. Currency conversion timing, the base year chosen, and how quickly average selling prices are assumed to rise can also move the final USD value by a lot.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 32.56 B (2025) | |

| Global Consultancy A | USD 7.70 B (2025) | Appears to size a narrower product universe where only selected textile composite forms and end uses are counted, which can exclude sizable industrial and multi-industry composite consumption that uses textile reinforcements. |

| Industry Publisher B | USD 5.69 B (2024) | Uses an earlier base year and a lower-growth framing, and the scope may emphasize specific fiber types and listed applications, which can undercount other end uses and regions where textile composites are adopted. |

The table shows a wide spread, and in Mordor Intelligence's model the value is built from a broader end-use demand pool where textile-form reinforcements are counted across multiple industries when they are converted into cured composite structures. Once scope is aligned and the same year, currency timing, and ASP path are applied, the remaining differences usually narrow to a few practical inputs that can be re-checked and updated over time.

Key Questions Answered in the Report

How large will the textile composites market be in 2031?

It is projected to reach USD 49.70 billion by 2031, up from USD 34.94 billion in 2026 at a 7.30% CAGR.

Which region accounts for the highest share of textile composites sales?

Asia-Pacific held 54.45% of 2025 revenue and is expected to remain the largest regional contributor through 2031.

Which fiber type is expanding fastest inside the textile composites space?

Carbon fiber leads with a 9.35% CAGR to 2031, driven by aerospace wings and offshore wind spar-cap demand.

What is the main restraint limiting automotive uptake of textile composites?

Brittle failure under crash loads and high repair costs continue to curb large-volume adoption in mainstream vehicle platforms.

Who are the key suppliers of aerospace-grade carbon fiber?

Toray, Teijin, and Mitsubishi Chemical jointly provide about 65% of global aerospace-grade capacity, anchoring the upstream supply chain.

Page last updated on: