Holographic Display Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

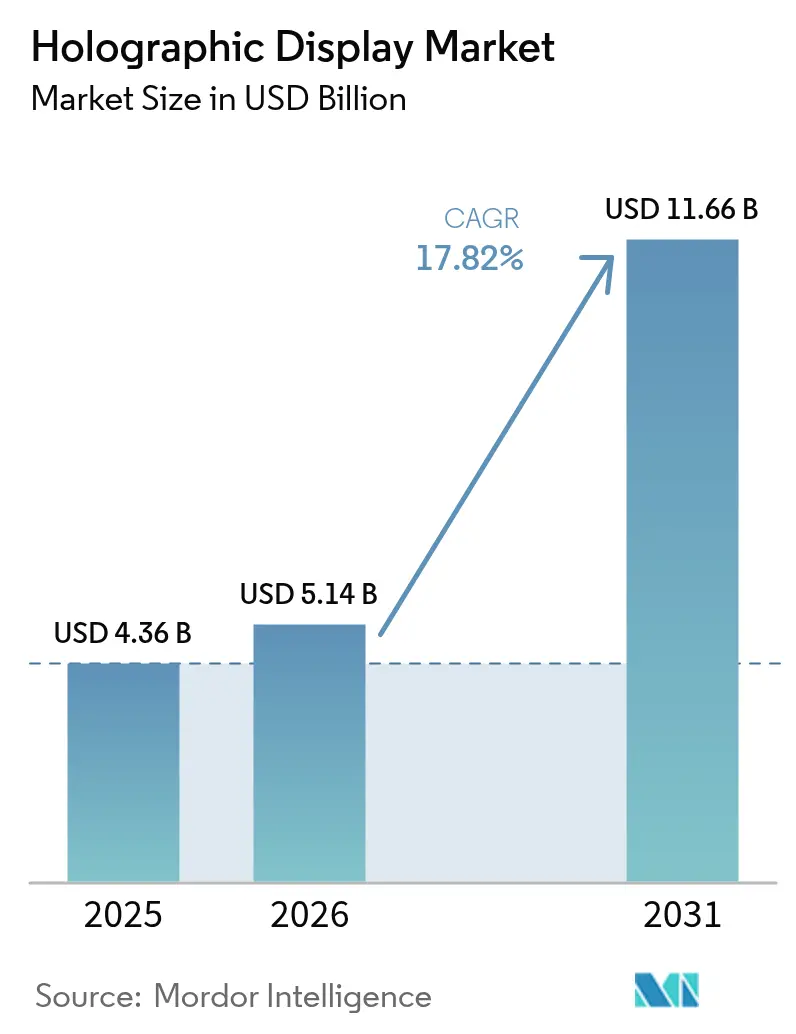

| Market Size (2026) | USD 5.14 Billion |

| Market Size (2031) | USD 11.66 Billion |

| Growth Rate (2026 - 2031) | 17.82% CAGR |

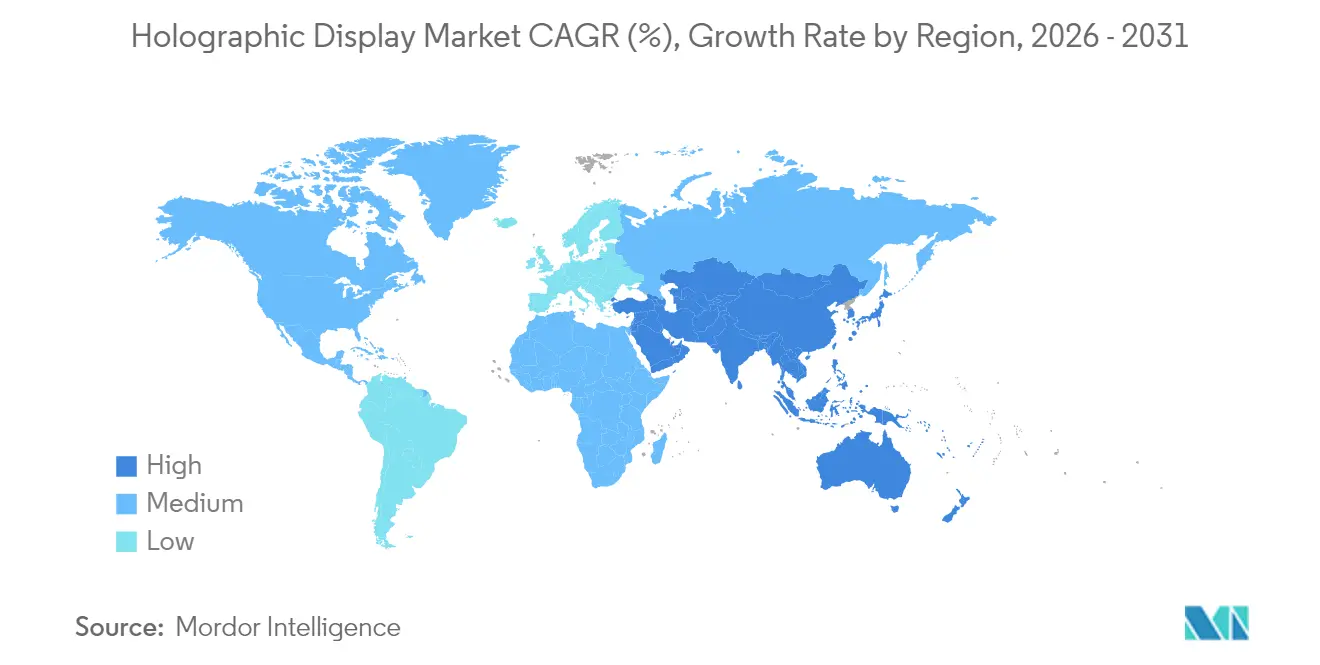

| Fastest Growing Market | Middle East |

| Largest Market | Asia |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Holographic Display Market Analysis by Mordor Intelligence

holographic display market size in 2026 is estimated at USD 5.14 billion, growing from 2025 value of USD 4.36 billion with 2031 projections showing USD 11.66 billion, growing at 17.82% CAGR over 2026-2031. Robust demand stems from automotive premium brands rolling out augmented-reality head-up displays, tier-1 U.S. hospitals installing volumetric surgical suites, and luxury retailers adopting 360-degree signage. These use-cases signal a decisive move from research pilots to production roll-outs as micro-LED waveguide yields improve and AI-driven content engines cut creation costs. German and Chinese automakers account for the bulk of windshield deployments, while U.S. health providers accelerate 3D imaging purchases that shorten operating-room planning cycles. Asia continues to lead production scale and content innovation, whereas the Middle East’s retail sector delivers the fastest regional expansion. The convergence of optics, computing, and content creation underpins an ecosystem where enterprises can monetize immersive experiences and create durable competitive advantage.

Key Report Takeaways

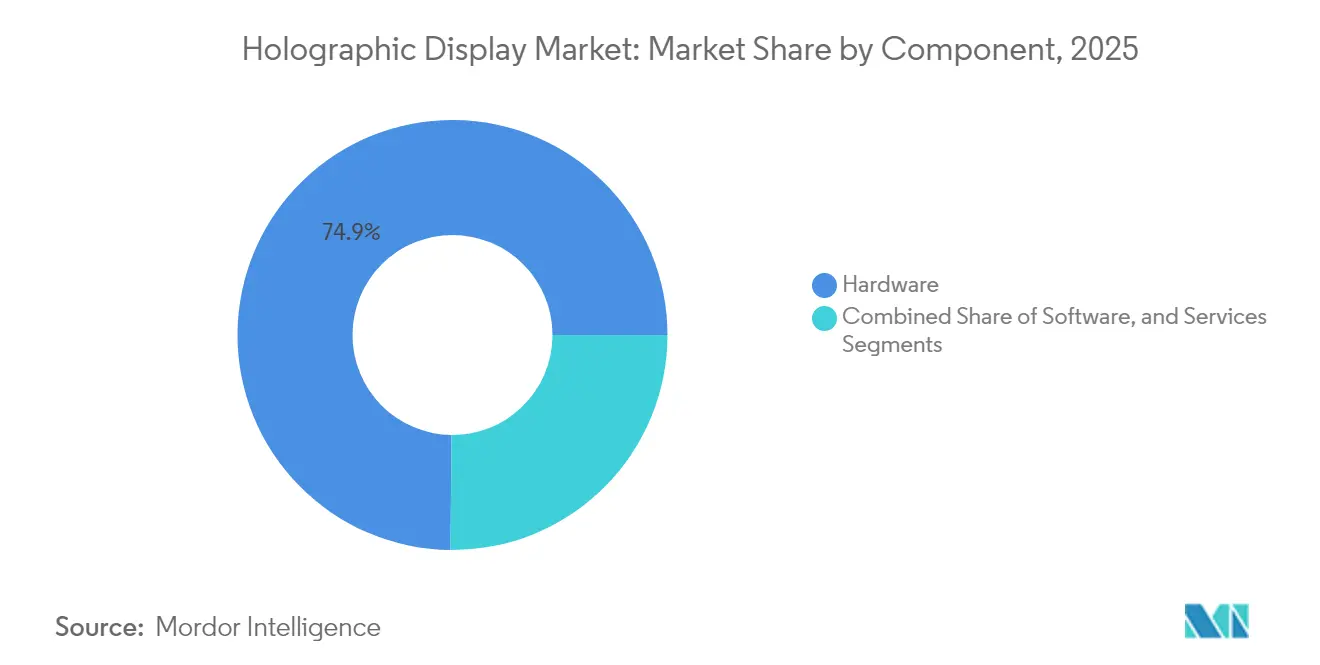

- By component, hardware held 74.85% of holographic display market share in 2025; services are forecast to grow at a 22.32% CAGR to 2031.

- By technology, electro-holographic solutions led with 40.25% revenue share in 2025, while touchable/mid-air haptic systems are projected to expand at a 24.05% CAGR.

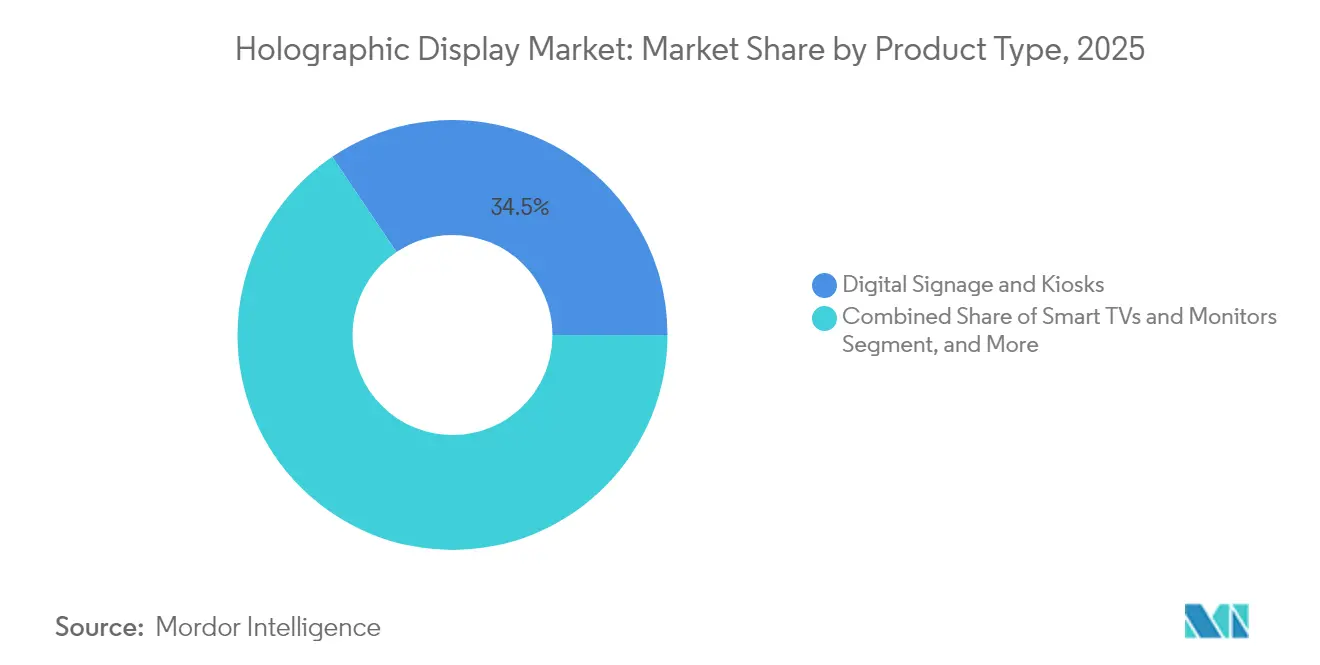

- By product type, digital signage and kiosks captured 34.45% of the holographic display market size in 2025; medical scanners and microscopes are advancing at a 24.62% CAGR through 2031.

- By end-user, retail and exhibition applications accounted for 28.75% revenue share in 2025; healthcare and medical education are set to grow at a 22.85% CAGR.

- By geography, Asia Pacific controlled 36.55% revenue in 2025; the Middle East is forecast to register the fastest regional CAGR at 21.18% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Holographic Display Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Automotive OEM adoption of augmented-reality holographic HUDs | +3.20% | Germany, China, North America spillover | Medium term (2-4 years) |

| Deployment of volumetric 3D surgical-planning suites in U.S. tier-1 hospitals | +2.80% | North America, Europe, APAC | Short term (≤ 2 years) |

| Luxury retail chains in Middle-East malls pivoting to 360° holographic signage | +2.10% | Middle East, Asia Pacific | Medium term (2-4 years) |

| Live-event and streaming platforms monetizing hologram concerts | +1.90% | Japan, South Korea, global expansion | Long term (≥ 4 years) |

| Defense battlefield-visualization programs adopting holographic sand tables | +1.70% | United States, Israel, NATO | Long term (≥ 4 years) |

| AI-generated content engines lowering 3D hologram production costs | +2.40% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Automotive OEM adoption of augmented-reality holographic HUDs

German luxury marques and Chinese electric-vehicle brands are integrating full-windshield holographic head-up displays to differentiate premium trims and enhance driver situational awareness. Hyundai Mobis’ concept shown at CES 2025 projects navigation cues, alerts, and entertainment content across three viewing zones, and joint development with Zeiss targets mass production by 2027. Market forecasts suggest 7 million automotive units will ship by 2030, converting dashboard real estate into immersive AR canvases. [1]SPIE Europe, “Zeiss, Hyundai Mobis hook up on holographic windshield displays,” optics.org

Deployment of volumetric 3D surgical-planning suites in U.S. tier-1 hospitals

Hospitals are turning to true-depth holograms for oncology, cardiology, and orthopedics. RealView Imaging’s HOLOSCOPE-i enables surgeons to manipulate 3D anatomy in real time, trimming planning hours and reducing operating-room errors. Clinical studies show 61% preference for holographic plans over 2D methods, especially for non-coplanar radiotherapy beams.

Luxury retail chains in Middle-East malls pivoting to 360° holographic signage

Flagship boutiques deploy freestanding volumetric displays that rotate handbags, jewelry, and haute couture without physical handling. The region’s high disposable income, emphasis on in-store theatrics, and competitive leasing rates accelerate adoption, inspiring Asian malls to follow suit.

Live-event and streaming platforms monetizing hologram concerts

Japanese and Korean studios capture performers volumetrically and broadcast them into clubs or VR spaces. A field-programmable-gate-array hologram processor built by Korean researchers renders 4K holograms at 30 ms latency, letting ticket buyers experience lifelike shows without travel.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Scarcity of mass-production micro-LED waveguides elevating BOM costs | -2.90% | Global, Asia manufacturing hubs | Short term (≤ 2 years) |

| Eye-safety and photobiological regulations limiting laser/plasma projection power | -1.80% | Europe, spillover to regulated markets | Medium term (2-4 years) |

| Geographic reliance on Japanese and Korean waveguide suppliers constrains scaling | -1.30% | Asia, North America OEMs | Short term (≤ 2 years) |

| Extended EU certification cycles delay product launches | -1.00% | Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Scarcity of mass-production micro-LED waveguides elevating BOM costs

Few fabs can achieve the nanoscale tolerances required for efficient waveguides, keeping prices 40-60% above LCD or OLED alternatives. Sample quotes for Sony’s 0.44-type Full HD OLED microdisplay exceed USD 260 (JPY 40,000), restricting consumer-device economics. [2]Sony Semiconductor Solutions, “0.44-Type Full HD OLED Microdisplay with Industry’s Smallest Pixels,” sony-semicon.com

Eye-safety and photobiological regulations limiting projection power

EU standards cap permissible laser energy, forcing automotive suppliers to add optical diffusers or reduce field-of-view, which raises cost and compromises brightness. Compliance testing extends development cycles, placing European vendors behind counterparts in less-restricted markets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Hardware Dominance Drives Service-Led Value

Hardware accounted for 74.85% of 2025 revenue, underscoring the capital intensity of spatial-light modulators, laser engines, and precision optics that underpin the holographic display market. Projectors, optical waveguides, and microdisplay engines remain cost drivers, yet falling component prices will push the hardware share of the holographic display market size down modestly by the decade’s close. Services already command the fastest 22.32% CAGR as enterprises look for turnkey deployment, calibration, and lifecycle support agreements. Integration specialists bundle on-premises installation, cloud rendering, and training, converting one-off device sales into multi-year contracts. Healthcare networks specify service-level agreements that guarantee uptime for surgical planning suites, while automakers outsource optical system alignment to tier-1 suppliers. The holographic display market is therefore shifting from hardware margin dependency to attached-service annuities.

In parallel, software stacks add real-time rendering, AI-assisted content creation, and analytics, layering subscription revenue atop physical equipment. The trend mimics earlier transitions in the projection and signage industries, where content-management platforms became indispensable. As volumetric streaming proliferates, bandwidth optimization and security patches will further enlarge the services opportunity. Hardware vendors now incubate internal professional-services groups or ally with systems integrators, ensuring tight coupling between optics, firmware, and managed content—an approach that strengthens ecosystem lock-in across the holographic display industry.

By Technology: Electro-Holographic Leads, Haptics Accelerate

Electro-holographic architectures captured 40.25% revenue in 2025 thanks to mature liquid-crystal-on-silicon and reflective spatial-light-modulator supply chains. Stable yields and established design toolsets make the format the safe choice for automotive HUDs and medical scanners, sustaining its lead in the holographic display market. Meanwhile, haptic mid-air systems clock a 24.05% CAGR as developers combine phased-array ultrasounds with volumetric visuals to let users “touch” floating interfaces. Retail podiums that permit gesture-based product rotation and hospital displays allowing sterile interaction exemplify commercial traction.

Laser/plasma projection solutions target extreme-brightness scenarios such as open-air stage shows and dashboard sunlit conditions, while semi-transparent waveguides serve AR smart-glasses. Metasurface optics unveiled by POSTECH help correct chromatic aberration, simplifying color management and slimming device profiles. Acoustic and photon-trap research lines could redefine efficiency, yet commercialization sits beyond the current forecast horizon. Overall, incumbent electro-holographic vendors must innovate on power, resolution, and interaction to fend off fast-rising haptic challengers in the holographic display market.

By Product Type: Medical Scanners Outpace Signage

Digital signage and kiosks contributed 34.45% of 2025 revenue as malls, airports, and exhibitions sought immersive visuals to boost footfall. Yet hospital scanners and microscopes register the highest 24.62% CAGR, reflecting clinical validation and reimbursement momentum. The holographic display market size for medical scanners is forecast to climb alongside surgical hub modernization budgets through 2031. Automotive HUDs form the second-fastest pool as windshield-wide overlays shift navigation data into the driver’s natural sightline. Full-color, full-FOV prototypes demonstrated at CES 2025 confirm optical readiness for fleet roll-outs.

Smart TVs, monitors, and smart-phones remain nascent because battery drain and content scarcity cool consumer adoption. Cameras and smart-glasses are farther along: Qualcomm’s Snapdragon AR1 enables tethered glasses that render low-latency holograms by off-loading compute to smartphones. As manufacturing scale improves, home entertainment may later eclipse signage. For now, high-value medical and automotive implementations steer product-mix expansion within the holographic display market.

By End-User: Healthcare Gains on Retail Leadership

Retail and exhibition venues held 28.75% revenue in 2025, banking on holographic storefronts to distinguish in-person shopping from e-commerce. Engagement analytics show dwell-time lifts of up to 40%, reinforcing ROI for flagship chains in Asia and the Middle East. Healthcare, however, is growing faster at 22.85% because surgeons value true-depth visualization that cuts operating-room time, and administrators appreciate remote consultation boxes that improve specialist access.

Media and entertainment continue to expand via hologram concerts that livestream deceased or virtual artists into multiple venues simultaneously. Automotive deployment quickens as ADAS stacks migrate to AR dashboards, while defense users invest in volumetric sand tables for mission rehearsal. Industrial, education, and consumer electronics segments trail but are positioned to benefit once component costs normalize. Collectively, these patterns show healthcare closing the gap with retail to become a co-anchor end-market for the holographic display market.

Geography Analysis

Asia Pacific generated 36.55% of 2025 revenue, leveraging China’s electric-vehicle boom, Japan’s entertainment tech, and South Korea’s semiconductor ecosystem. Public-private programs funnel incentives into micro-LED backplanes and metasurface optics, fortifying regional supply dominance. The holographic display market size attributed to Asia Pacific also benefits from dense retail deployments in Tokyo, Seoul, and Shanghai. Europe follows with automotive design wins but faces brightness restrictions that temper growth, although collaborations such as Zeiss-Hyundai sustain innovation pipelines.

North America exhibits steady momentum anchored by U.S. tier-1 hospitals that upgrade surgical visualization suites and defense agencies procuring volumetric mission-planning tables. Canada’s live-event promoters experiment with hologram festivals, extending market reach. The Middle East posts the highest 21.18% CAGR through 2031 as luxury malls in Dubai, Riyadh, and Doha invest heavily in 360-degree holographic showcases that elevate brand storytelling. Government smart-city initiatives in Abu Dhabi and Neom foster further experimentation.

Latin America and Africa remain early-stage, constrained by import duties and bandwidth limitations, yet pilot projects in São Paulo retail and South African mining visualization hint at downstream expansion. Global supply chains nonetheless route critical waveguide fabrication through Japan and South Korea, exposing all regions to potential bottlenecks, a factor that stakeholders across the holographic display market monitor closely for risk mitigation.

Regulatory Landscape

Regulation for holographic displays is shaped by product safety, photobiological and laser safety, and market-entry conformity schemes that vary by end use (consumer/XR, automotive, medical). In India, the Bureau of Indian Standards (BIS) issued implementation guidance tied to IS/IEC 62368-1:2023 for extended reality and wearable devices, with a compliance deadline of May 1, 2026, creating a clear recertification trigger for vendors shipping holographic-capable XR hardware into the country.

Across Europe, CE marking requirements anchor go-to-market, typically pulling holographic display hardware under electrical safety, electromagnetic compatibility, radio equipment, and RoHS obligations (via the European Commission framework). On the safety side, laser-based and projection-oriented holographic systems are constrained by laser display safety guidance (IEC TR 60825-3:2022) and related national adoptions (for example, KS C IEC 60825-3 updates in Korea), while AR/VR safety guidance continues to formalize at the standards level (ISO/IEC 5927:2024). This is increasing documentation and testing burden for global product lines.

Value Chain Analysis

The holographic display value chain spans raw and specialty materials (photopolymers, optical films), optical component fabrication (HOEs, waveguides, lenses, microdisplays/SLMs, laser engines), module and system integration (optical engines, enclosures, calibration), and downstream packaging into product categories such as automotive windshield displays, medical visualization systems, and retail signage. Recent supply-chain structuring is visible in automotive, where ZEISS, tesa, Saint-Gobain Sekurit, and Hyundai Mobis formed the QuadAlliance (February 2026) to align optical design, materials and adhesives, windshield lamination, and tier-1 integration into a one-stop chain for holographic windshield displays. The structure reflects the growing need to industrialize processes beyond lab-scale optics.

Manufacturing scale-up and yield remain critical constraints and differentiators. Capacity additions for key optical elements and waveguides are emerging across regions, including Luminit expanding US-based roll-to-roll production for holographic optical elements (July 2025), SCHOTT reaching serial production capability for geometric reflective waveguides with expanded processing infrastructure in Malaysia (October 2025), and Nika Optics unveiling an automated holographic waveguide production line in Tianjin with 1 million units annual capacity (June 2026). Distribution and delivery increasingly bundle software rendering pipelines and field services, particularly in healthcare and automotive programs where calibration, uptime, and compliance documentation are embedded in procurement.

Competitive Landscape

Roughly two dozen active vendors participate, yielding moderate fragmentation. Electronics giants such as Samsung, Sony, LG, and Sharp leverage display know-how and manufacturing muscle, whereas pure-plays like Looking Glass Factory, RealFiction, and RealView Imaging pursue niche breakthroughs. Competitive advantage accrues to firms that marry optics fabrication with software rendering pipelines, as Samsung’s metasurface collaboration with POSTECH demonstrates. Qualcomm’s tie-up with Google and Samsung for Snapdragon-based smart-glasses showcases cross-value-chain alliances aimed at shortening time-to-market.

Patent filings cluster around waveguide designs, foveated rendering, and mid-air haptics. Sony’s recent disclosures promise higher diffraction efficiency and environmental durability—critical for eyewear form factors. Start-ups exploit white spaces: RealView’s medical focus secures hospital budgets, while the Public University of Navarra’s elastic diffuser prototype opens new interaction paradigms. Industry watchers anticipate M&A as incumbent display makers acquire specialized optics houses to secure IP and scale.

Government R&D grants and university spin-offs add another competitive layer, funneling breakthroughs into the commercial arena. The resulting ecosystem complexity makes platform openness, standards compliance, and channel partnerships decisive. Stakeholders that lock in automotive or medical design slots early gain recurring revenue and data network effects, shaping future winner-take-most trajectories within the holographic display industry.

Holographic Display Industry Leaders

MDH Hologram Ltd

Looking Glass Factory Inc.

Provision Holding Inc.

Realview Imaging Ltd

RealFiction Holding AB

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Industrialization in automotive and XR optics is creating whitespace for suppliers that can deliver waveguides, HOEs, and photopolymer materials at volume with automotive-grade quality control. The QuadAlliance formation (ZEISS, tesa, Saint-Gobain Sekurit, and Hyundai Mobis, February 2026) points to buyer demand for integrated, auditable supply chains that cover mastering, replication, and lamination for holographic windshield displays, rather than fragmented sourcing. Complementing this, ZEISS and LG Chem announced a strategic alliance to strengthen photopolymer supply for advanced optics (October 2025), indicating a near-term opportunity for materials vendors and process specialists able to lock in multi-year qualification cycles.

A second opportunity track is scaling manufacturing capacity and reducing bottlenecks in waveguide production, which supports expansion in smart glasses, automotive HUDs, and other semi-transparent architectures. This includes Nika Optics launching an automated holographic waveguide production line in Tianjin with annual capacity of 1 million units (June 2026), and Luminit adding a fourth facility in the United States for high-volume holographic optical film production (July 2025). On the technology roadmap, research progress in high-refresh-rate, chip-integrated holography (for example, a VCSEL-based chip array demonstrated with 1.93 GHz refresh capability, June 2026) and programmable metasurfaces projecting dozens of images (62 images reported, July 2026) expands the design space for lower-latency, more compact systems. This strengthens the case for software and services providers that productize content pipelines, calibration, and runtime optimization around these hardware capabilities.

Recent Industry Developments

- April 2026: Realfiction Holding AB announced progress on its Spatial Light Modulator, describing a more direct and scalable route toward mass production of large-format Directional Pixel Technology (DPT) displays. The update underscores a push to de-risk manufacturability, a key barrier for scaling glasses-free multi-user 3D systems into higher-volume deployments.

- March 2026: Looking Glass Factory unveiled musubi, positioned as a consumer holographic photo and video frame, and communicated an initial shipment timeline starting in June 2026. The move broadens holographic displays beyond enterprise pilots toward consumer hardware, expanding the addressable ecosystem for content tooling and creator workflows.

- October 2024: ZEISS and Hyundai Mobis formalized a partnership to co-develop panoramic automotive holographic displays, targeting future windshield-scale deployments. The collaboration ties a leading optics supplier to a tier-1 automotive integrator, supporting longer-cycle automotive qualification programs and supply-chain readiness.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this report, the holographic display market is defined as revenues generated from holographic display products and solutions that project or reconstruct 2D or 3D images for visualization and interaction across commercial and institutional use cases.

Scope exclusions: Excluded are general 2D/3D flat displays that do not create a holographic effect, and standalone content creation without a holographic display output.

Segmentation Overview

- By Component

- Hardware

- Spatial Light Modulators (SLM)

- Projectors and Laser Engines

- Optical/Lens Modules

- Sensors and Cameras

- Others

- Software

- Services

- Integration and Consulting

- Support and Maintenance

- Hardware

- By Technology

- Electro-Holographic

- Touchable/Mid-Air Haptic

- Laser/Plasma

- Semi-Transparent

- Other Emerging (Acoustic, Photon-Trap)

- By Product Type

- Digital Signage and Kiosks

- Smart TVs and Monitors

- Cameras and Smart Glasses

- Medical Scanners and Microscopes

- HUDs and Windshield Displays

- Smartphones and Tablets

- Others

- By End-User

- Consumer Electronics

- Retail and Exhibition

- Media, Entertainment and Live Events

- Healthcare and Medical Education

- Automotive and Transportation

- Military, Defense and Aerospace

- Industrial and Manufacturing

- Education and Training

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Nordics

- Rest of Europe

- South America

- Brazil

- Rest of South America

- Asia-Pacific

- China

- Japan

- India

- South-East Asia

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Gulf Cooperation Council Countries

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to build the starting structure of the model and to keep assumptions anchored to measurable signals. We reviewed public technical and adoption indicators, such as IEEE and other peer reviewed publications, along with patent libraries, to map where performance and cost curves are moving.

For market inputs, we relied on public or official references such as ITU releases on telecom readiness, the World Bank for macro indicators that influence electronics demand, UN Comtrade for trade flows of relevant electronics and optics categories, and customs and tariff schedules that help separate device classes where possible. We also used sources like company annual reports, investor presentations, association websites, and reputed press coverage to cross-check shipment narratives and announced rollouts. Where needed, we used paid subscriptions for company financials, news and financials, and patent databases to support triangulation. These examples are not exhaustive, and many other public sources were also referred to for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on converting the desk assumptions into realistic adoption, pricing, and procurement patterns. We spoke with a balanced mix of display ecosystem participants, including component suppliers, product integrators, channel partners, and end user buyers across Americas, EMEA, and APAC. The inputs were then used to validate demand timing and remove over-counting across use cases.

Feedback from these discussions helped tighten ranges for adoption by vertical, identify typical pricing bands for holographic display deployments, and assess the pace of design wins moving from pilots to scaled deployment.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 34% | CXOs: 15% | APAC: 47% |

| Mid tier: 48% | Functional/Unit leaders: 37% | EMEA: 32% |

| Smaller Players: 18% | Managers: 48% | Americas: 21% |

Market-Sizing & Forecasting

Sizing started from a top-down demand pool reconstruction, where electronics shipment and deployment signals were translated into holographic display attach rates across major end uses, and then converted to value using realistic price bands. This was then corroborated through selective bottom-up checks, such as sampled ASP times unit volumes for key form factors and a limited roll-up of supplier and integrator revenues, which helped adjust for double counting.

A few practical variables used as inputs (illustrative) included: announced deployments in retail and live events, vehicle and mobility display adoption signals for HUD style use, hospital and medical education digitization activity for imaging visualization, import and export movement of relevant optical and display equipment categories, and the direction of average selling price changes as production scales. Where unit visibility was weak, gaps were handled using conservative penetration ranges agreed in interviews, and then tested against what channel participants said was actually shipping.

For forecasting, we used scenario analysis supported by short time series smoothing on the base signals, since adoption can move in steps when new product releases or procurement cycles hit. The final outlook reflects the midpoint scenario, and the upside and downside were checked with experts to confirm that timelines and price erosion assumptions were not overly aggressive.

Data Validation & Update Cycle

To validate the totals, outputs were compared against independent signals like shipment direction, pricing movement, and adoption pacing by end use, and then checked again at regional level so outliers could be explained. When a variance could not be tied back to a clear driver, assumptions were revisited, and follow-up calls were triggered to confirm whether the change was real or just timing noise.

Before sign-off, the model goes through multi-step analyst review, including math checks, scope checks, and consistency checks between historical and forecast years. Reports are refreshed annually, with interim updates when material events occur, and a final pre-delivery pass is completed so clients receive the most current view available.

Mordor Intelligence's Holographic Display Market Sizing Compared With Other Published Estimates

Published market values for holographic displays often do not match because the category can be stretched in different directions, and because the year chosen for the starting point is not always the same. Differences in what gets counted as a holographic display, how services are treated, and how fast pricing is assumed to fall can all move the final number.

Some estimates fold in factory-gate service revenues like event experiences, demonstrations, and training packages bundled around holographic experiences, which tends to inflate the market for earlier years. In Mordor Intelligence, the count is limited to holographic display hardware, software, and related services directly tied to the display deployment, and then validated using adoption by vertical and realistic ASP bands before projecting forward.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 5.14 B (2026) | |

| Industry Research Publisher A | USD 2.99 B (2026) | Uses factory-gate accounting that bundles broader experience and training service revenues, and it can also apply a narrower device definition, which depresses the 2026 total versus a deployment-led view. |

| Regional Consultancy B | USD 5.20 B (2024) | Uses an earlier base year and a slower growth track, and the scope appears to emphasize selected application buckets, which can understate newer end-use adoption that shows up after 2024. |

Looking at the three figures together, the spread is mainly explained by scope treatment and the choice of starting year, and not by a simple math issue. By keeping the model tied to observable deployment signals and cross-checking price and penetration assumptions with interview feedback, we produce a value that can be traced back to clear inputs and repeated when new data arrives.

Key Questions Answered in the Report

What is the current size of the holographic display market?

The market stands at USD 5.14 billion in 2026 and is projected to reach USD 11.66 billion by 2031, reflecting an 17.82% CAGR.

Which region grows the fastest?

The Middle East posts the highest 21.18% CAGR through 2031, driven by luxury retail investments in 360-degree holographic signage.

Which component segment expands the quickest?

Services grow at a 22.32% CAGR because enterprises seek turnkey integration, maintenance, and content-management support.

Why are hospitals adopting holographic displays?

Volumetric imaging improves surgical planning accuracy and enables life-size remote consultations, leading to measurable clinical outcomes and broader specialist access.

What hampers wider consumer adoption?

High bill-of-materials costs for micro-LED waveguides and stringent laser-safety regulations in some regions keep retail prices elevated for mass-market devices.

How fragmented is the competitive landscape?

With more than 20 active players and no single firm exceeding 20% revenue, the market exhibits moderate fragmentation but shows signs of partnership-driven consolidation.

Page last updated on: