Dual Chamber Prefilled Syringes Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

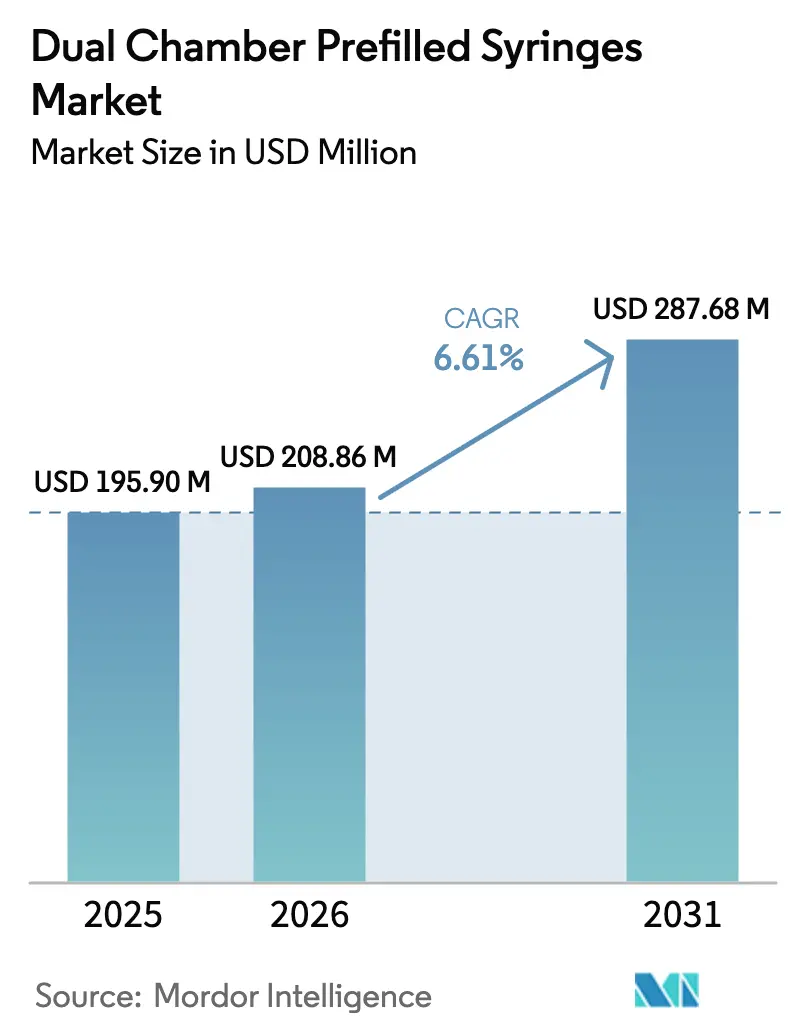

| Market Size (2026) | USD 208.86 Million |

| Market Size (2031) | USD 287.68 Million |

| Growth Rate (2026 - 2031) | 6.61% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Dual Chamber Prefilled Syringes Market Analysis by Mordor Intelligence

Dual chamber prefilled syringes market size in 2026 is estimated at USD 208.86 million, growing from 2025 value of USD 195.90 million with 2031 projections showing USD 287.68 million, growing at 6.61% CAGR over 2026-2031. Continued migration of high-value biologics into self-administration formats, growing use of lyophilized combination therapies, and tighter container-closure integrity rules are moving the dual chamber prefilled syringes market from a convenience option to a compliance requirement, especially for therapies that degrade rapidly after reconstitution [1]U.S. Food and Drug Administration, “Guidance for Industry: Essential Drug Delivery Outputs,” fda.gov . Manufacturers are prioritizing barrier-isolator lines and ready-to-use platforms that speed up fill-finish while satisfying the latest deterministic leak-testing guidance. Investments exceeding USD 4 billion in North America and Europe demonstrate that capacity expansion remains a core strategy for incumbents, while material science breakthroughs in cyclic olefin polymers (COP) open fresh opportunities in segments historically dominated by glass. Demand also benefits from the spread of home-care models, where dual chamber autoinjectors simplify chronic disease management and support digital adherence tracking. Collectively, these forces position the dual chamber prefilled syringes market for durable mid-single-digit growth over the next five years.

Key Report Takeaways

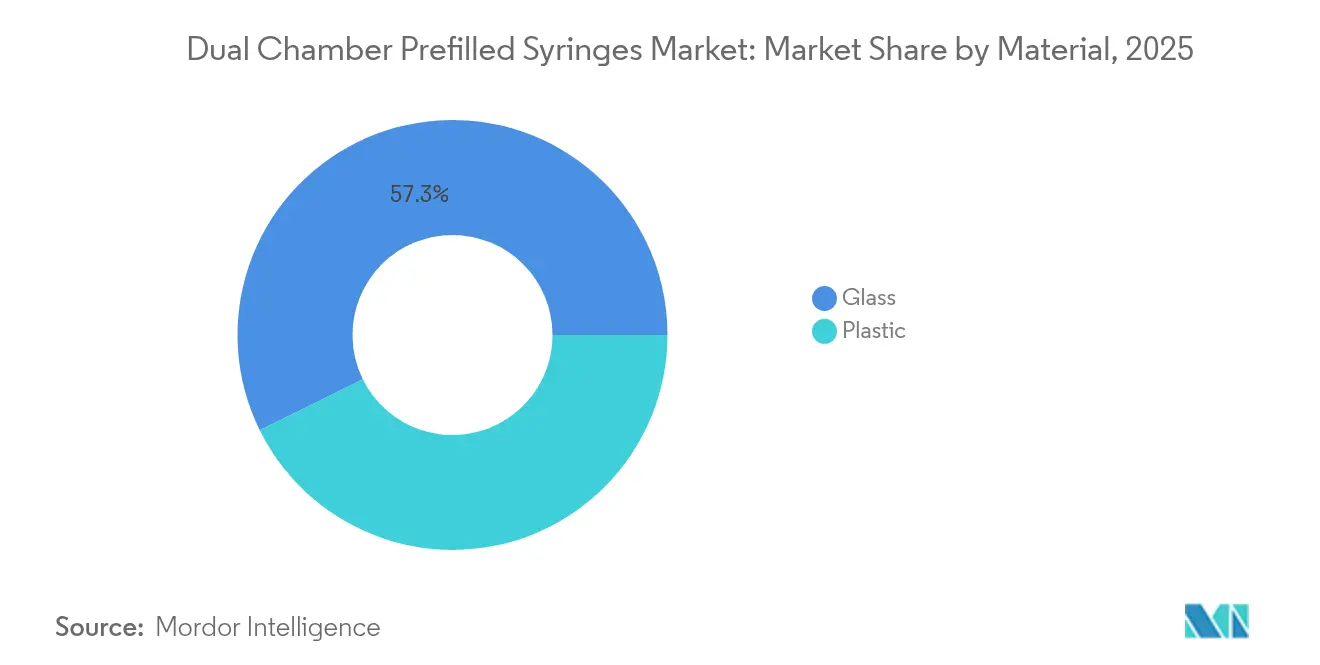

- By material, glass retained 57.30% of dual chamber prefilled syringes market share in 2025, while plastics led by advanced COP grades are projected to grow at a 7.12% CAGR to 2031.

- By application, diabetes therapies led with 37.80% revenue share in 2025, whereas oncology is set to expand at a 7.28% CAGR through 2031.

- By capacity, the 1-2.5 ml segment accounted for 37.05% of the dual chamber prefilled syringes market size in 2025; sub-1 ml formats are poised for a 7.19% CAGR to 2031.

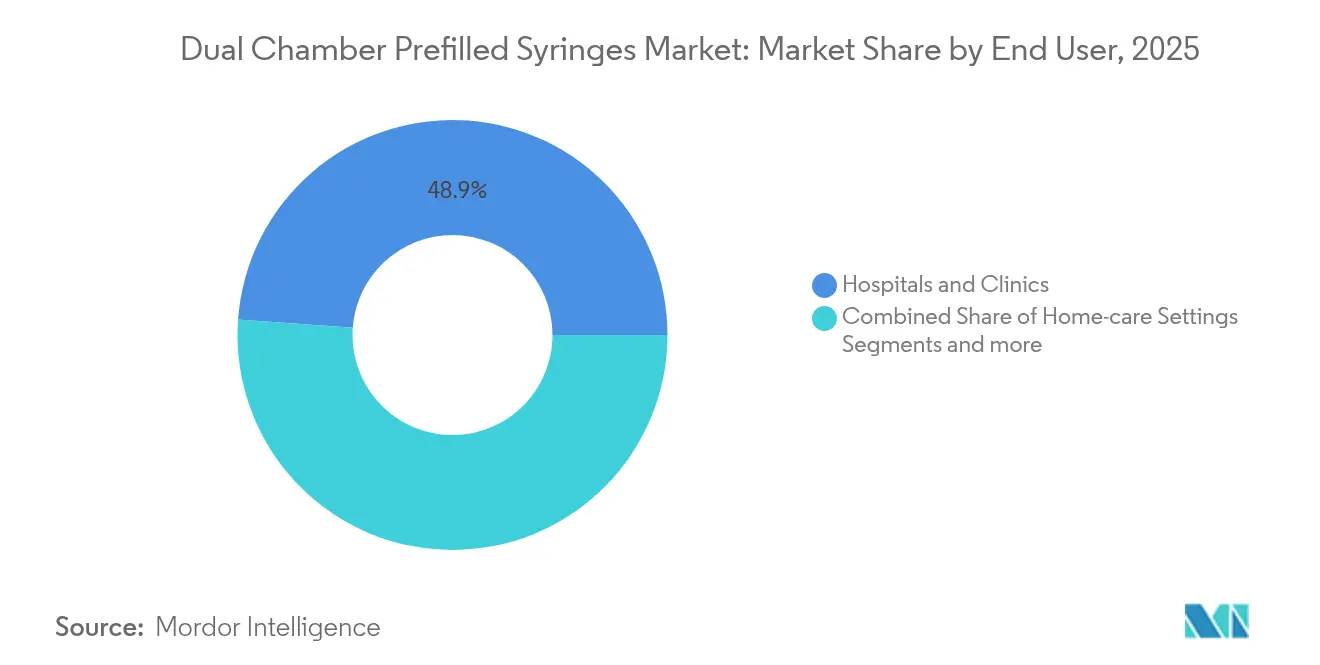

- By end user, hospitals and clinics held 48.85% of demand in 2025, yet home-care settings record the fastest growth at 7.22% CAGR.

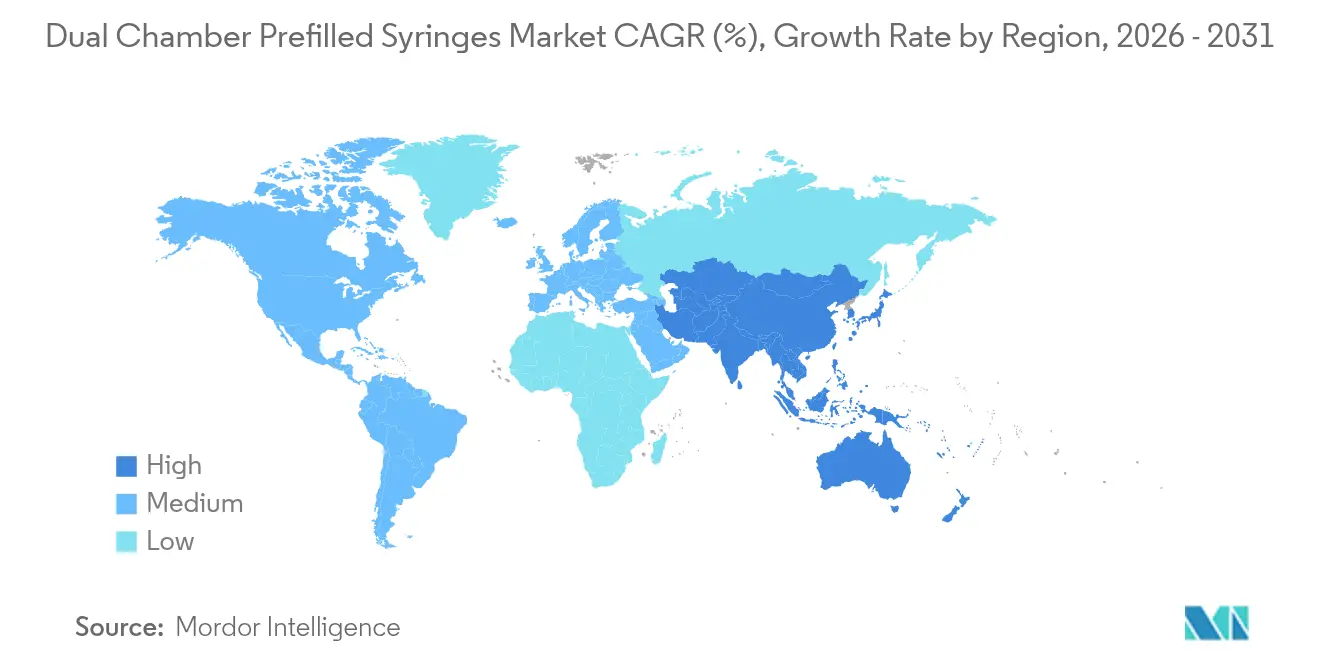

- By geography, North America commanded 40.90% of revenue in 2025, while Asia-Pacific is expected to post a 7.42% CAGR during the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Dual Chamber Prefilled Syringes Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Biologics pipeline shift toward freeze-dried formulations | +1.8% | Global, concentrated in North America & EU | Medium term (2-4 years) |

| Home-care self-injection demand surge | +1.5% | North America & EU primary, APAC emerging | Short term (≤ 2 years) |

| Container-closure integrity regulations tighten | +1.2% | Global, FDA and EMA leadership | Long term (≥ 4 years) |

| Workflow savings for fill-finish CDMOs | +0.9% | Global, manufacturing hub concentration | Medium term (2-4 years) |

| Lyophilized combination therapies entering trials | +0.7% | North America & EU clinical centers | Long term (≥ 4 years) |

| RTU nested dual-chamber tubs enabling micro-batching | +0.6% | Global, advanced manufacturing regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Biologics pipeline shift toward freeze-dried formulations

Pharmaceutical developers increasingly position dual chamber systems as the default container for new freeze-dried biologics because their sealed architecture prevents aggregation that occurs when proteins dwell in liquid form for extended periods. The latest vacuum-assisted lyophilization processes shorten drying cycles by 40%, yielding energy and time savings that strengthen the value proposition for contract development and manufacturing organizations. Several late-stage trials—including Phesgo for HER2-positive breast cancer—validated clinical advantages such as reduced infusion times, prompting more sponsors to lock in dual chamber compatibility at phase I rather than retrofitting formulations later [2]European Medicines Agency, “Phesgo EPAR Summary,” ema.europa.eu . Regulatory acceptance accelerates adoption because dossier reviewers now regard dual chamber integrity data as a mature, low-risk component of combination product submissions. As freeze-dried biologics outpace liquid biologics in pipeline counts, the dual chamber prefilled syringes market secures a long runway of demand tied to the next generation of high-value therapies.

Home-care self-injection demand surge

Patient surveys show 92.9% adherence with dual chamber autoinjectors compared with markedly lower rates for vial-and-syringe regimens, driving payers to favor home administration that cuts clinic visits. The pandemic highlighted the safety and cost benefits of shifting routine injections out of hospitals, and the FDA’s 2024 Essential Drug Delivery Outputs guidance codified performance metrics that streamline home-use claims. Device makers now embed Bluetooth modules that transmit dose confirmation to electronic health records, improving provider oversight without in-person appointments. These developments expand the addressable population of patients willing to self-inject, particularly in chronic conditions like diabetes and autoimmune disorders.

Container-closure integrity regulations tighten

Revised FDA and EMA guidances require deterministic helium leak testing and holistic risk assessments that are easier to satisfy with pre-sterilized, nested dual chamber tubs than with traditional washed glass vials. Regulators also view dual chamber plungers and stoppers as inherently less prone to particulate contamination because they are handled in closed isolators. Manufacturers able to show early compliance enjoy faster review timelines, making container-closure integrity not just a quality imperative but a schedule advantage, thereby deepening customer preference for dual chamber formats.

Workflow savings for fill-finish CDMOs

High-speed robotic cells such as Cytiva’s SA25 workcell maintain EU Annex 1 compliance while enabling bubble-free filling of dual chamber barrels at 15,000 units per hour. Eliminating glass washing stages cuts water for injection consumption and reduces footprint requirements. CDMOs report improved yields and fewer line stoppages, allowing them to offer competitive pricing that further nudges clients toward dual chamber configurations.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital outlay for barrier-isolator lines | -1.4% | Global, concentrated in emerging markets | Short term (≤ 2 years) |

| Complex global E&L compliance burden | -1.1% | Global, regulatory-intensive markets | Long term (≥ 4 years) |

| Silicone-oil interaction knowledge gaps | -0.8% | Global, biologics-focused applications | Medium term (2-4 years) |

| COP barrel feedstock shortages | -0.6% | Global, plastic segment concentration | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High capital outlay for barrier-isolator lines

Complete dual chamber isolator suites routinely surpass USD 50 million, a figure that deters small biologics developers in Latin America, Africa, and parts of Southeast Asia from internalizing production. Depreciation and validation costs stretch project payback well beyond a typical five-year horizon, forcing many firms to outsource or abandon dual chamber plans. Although financing schemes and government incentives reduce upfront burdens, accessibility remains limited, slowing near-term adoption in resource-constrained markets.

Complex global E&L compliance burden

Regulators demand extractables and leachables data covering 200 plus compounds across barrel, stopper, and activation components, driving testing costs of USD 2–5 million per program. Divergent regional limits for specific organic acids and heavy metals complicate dossier preparation and lengthen approval agendas. Suppliers offering certified material libraries gain leverage, but smaller players face delays that can erode competitive timelines.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Glass Dominance Faces Polymer Innovation Challenge

Glass held 57.30% of dual chamber prefilled syringes market share in 2025, underpinned by decades of validated performance, while plastics are projected to register a 7.12% CAGR through 2031 as advanced COP, COC, and multilayer hybrids overcome historical permeability limitations . The dual chamber prefilled syringes market hinges on predictability; glass offers unmatched chemical resistance for alkaline or highly ionic formulations. Yet brittle breakpoints, delamination risks, and heavier logistics footprints spur interest in polymer alternatives.

Polymer suppliers have responded with materials such as OXYCAPT, which delivers 14-fold superior oxygen barrier properties compared with conventional COP and withstands dry-heat sterilization without yellowing. Nested RTU polymer tubs eliminate glass washing, reduce particle loads, and enable 25% faster line changeovers. Consequently, the dual chamber prefilled syringes market increasingly views material choice as therapy-specific rather than one-size-fits-all. Over the forecast period, glass sustains a majority of installed capacity, but polymer lines capture new greenfield investments, preserving balanced competition across substrates.

By Application: Diabetes Leadership Challenged by Oncology Acceleration

Diabetes accounted for 37.80% of the dual chamber prefilled syringes market size in 2025, buoyed by GLP-1 combinations that benefit from automatic reconstitution for weekly dosing. Insulin plus incretin co-formulations demonstrate improved glycated hemoglobin control and lower hypoglycemia risk, helping the dual chamber prefilled syringes market cement its presence in routine endocrinology practice.

Oncology, however, exhibits the fastest expansion at a 7.28% CAGR, as large-volume subcutaneous monoclonal antibodies migrate away from infusion centers into outpatient clinics. Phesgo’s fixed-dose combination illustrates the operational gains achieved when infusion times fall from 150 minutes to 8 minutes, freeing chair capacity and boosting patient satisfaction. Pipeline reviews identify more than 180 biologics requiring injection volumes above 2 ml, signalling sustained oncology demand for dual chamber designs capable of segregating co-factors or lyophilized payloads until the final moment of delivery.

By End User: Hospital Dominance Shifts Toward Home Care

Hospitals and clinics consumed 48.85% of total units in 2025, reflecting entrenched procurement contracts and in-house compounding practices that favor centralized control. Many oncology regimens still demand professional oversight to manage adverse-event monitoring, supporting hospital retention in the dual chamber prefilled syringes market.

Home-care channels, nonetheless, are forecast to grow at 7.22% CAGR, driven by payer pressure to reduce administration costs and technological advances that embed passive safety needles, audible dose-completion cues, and smartphone-enabled adherence logging. FDA guidance now clarifies human-factor study expectations for self-administration claims, shortening approval cycles and giving manufacturers confidence to design autoinjector variants into early product planning. These developments widen consumer access and reposition the dual chamber prefilled syringes industry for retail pharmacy distribution models.

By Capacity: Mid-Range Volumes Lead as Precision Dosing Grows

The 1-2.5 ml bracket delivered 37.05% of 2025 revenue thanks to its compatibility with prevalent protein concentrations and moderate injection forces. Sponsors prefer this sweet spot because it balances ergonomic grip, plunger travel, and activation torque, simplifying device development.

Sub-1 ml formats, advancing at 7.19% CAGR, respond to pediatric indications and ultra-potent antibodies where dose accuracy within ±2% is critical. New autoinjector engines regulate spring force to accommodate dual chamber barrels as small as 0.5 ml while maintaining activation forces below 25 N, which enhances usability for elderly and adolescent populations. At the opposite end, 5 ml plus volumes remain niche until ergonomic and dwell-time challenges can be fully resolved, though early prototypes target long-acting oncology injectables and depot hormones.

Geography Analysis

North America captured 40.90% of global spending in 2025, supported by FDA leadership, deep biologics pipelines, and investments exceeding USD 2.8 billion in glass and polymer syringe capacity expansions by BD and SCHOTT Pharma. The dual chamber prefilled syringes market benefits from clear regulatory pathways that align device and drug reviews under combination product centers, accelerating approvals. Canada and Mexico further fortify regional volumes through joint manufacturing clusters enabled by favorable USMCA trade provisions and shared quality systems audits.

Europe ranked second in revenue, underpinned by EMA guidance that harmonizes dossier expectations across 30 authorities and fosters cross-border supply chains. Capital projects such as Gerresheimer’s USD 180 million Georgia, EU, expansion and Nipro’s German upgrades increase regional RTU availability and shorten lead times for mid-size biotech firms. Healthcare systems emphasize time-saving subcutaneous injections to reduce bed occupancy, aiding diffusion of dual chamber formats. Sustainability priorities also influence procurement, with polymer barrels offering reduced weight and related transport emissions, an advantage cited in multiple tender documents.

Asia-Pacific is the fastest growing territory at a 7.42% CAGR, propelled by harmonization initiatives under the Asia Partnership Conference of Pharmaceutical Associations that pilot joint review programs in Singapore, Japan, and South Korea. China upgrades its National Medical Products Administration review framework to accept electronic Common Technical Documents, trimming average review times from 22 to 15 months for combination products. Local contract manufacturers co-license technology from European partners, accelerating domestic supply while mitigating freight risk. India, Thailand, and Vietnam invest in cold-chain networks to handle temperature-sensitive biologics, expanding the potential patient base. The Middle East, Africa, and South America show nascent adoption tied to oncology rollouts and donor-funded diabetes programs, but reimbursement constraints and variable regulatory capacity temper immediate scale.

Competitive Landscape

The dual chamber prefilled syringes market exhibits moderate concentration, with the top five suppliers estimated to command about 60% of global volume. BD produces more than 3 billion prefillable units annually and allocates USD 1.2 billion through 2026 to expand RTU glass and polymer lines, preserving economies of scale that deter new entrants. SCHOTT Pharma, Gerresheimer, and Stevanato Group formed an “Alliance for RTU” to standardize nested tub footprints and sterilization cycles, enabling interchangeable filling solutions that lower switching costs for drug sponsors.

Material science differentiation intensifies as Stevanato’s EZ-fill® platform posts double-digit growth by combining baked-on silicone with low-tungsten glass to safeguard sensitive antibodies. Polymer innovators secure premium contracts in high-oxygen-sensitive biologics, while newcomers focus on freeze-drying innovations that enhance protein integrity and allow micro-batching for orphan indications. Patent filings concentrate on automatic mixing pistons, anti-backflow valves, and silicone-free glide coatings; the USPTO lists more than 200 new claims filed between 2023 and 2024 alone, underscoring the technology arms race.

Strategic moves include Lifecore Biomedical’s commissioning of a GMP-ready five-head isolator filler that doubles customer capacity, signaling CDMO enthusiasm for integrated drug-device offerings. Meanwhile, Asian contract fillers license European RTU technology stacks to sidestep multi-year learning curves. Competitive intensity is expected to sharpen as container-closure integrity mandates raise performance bars and as device-centric digital health platforms open ancillary revenue streams.

Dual Chamber Prefilled Syringes Industry Leaders

-

Gerresheimer AG

-

West Pharmaceutical Services, Inc.

-

Credence MedSystems, Inc.

-

Vetter Pharma International GmbH

-

MAEDA INDUSTRY Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: BD invested USD 10 million to add syringe and needle lines in Connecticut and Nebraska, lifting U.S. capacity for safety-engineered devices.

- September 2024: Lifecore Biomedical announced the operational readiness of its high-speed 5-head isolator filler, doubling fill-finish capacity for prefilled formats.

- May 2024: Gerresheimer committed USD 180 million to expand its Peachtree City, Georgia plant, adding 18,000 m² of cleanroom space dedicated to dual chamber syringe production.

- March 2024: SCHOTT Pharma allocated USD 371 million to construct a polymer syringe facility in Wilson, North Carolina, aiming to triple U.S. supply by 2030.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

We define the dual-chamber prefilled syringes market as all factory-built, two-compartment syringe systems that keep an active ingredient (often a lyophilized biologic) physically separate from its diluent or activator until reconstitution immediately before injection. This study covers disposable glass and polymer formats ranging from sub-1 mL to 5 mL that are supplied to drug-makers on a contract or captive basis and sold through hospital, clinic, and home-care channels.

Exclusion: Reusable autoinjectors, single-chamber prefilled syringes, and bulk cartridge barrels are outside scope.

Segmentation Overview

-

By Material

- Glass

- Plastic

-

By Application

- Diabetes

- Oncology

- Autoimmune Diseases

- Hormonal Disorders

- Others

-

By End User

- Hospitals and Clinics

- Home-care Settings

- Ambulatory Surgical Centers

- Others

-

By Capacity

- <1 ml

- 1-2.5 ml

- 2.5-5 ml

- >5 ml

-

By Geography

-

North America

- United States

- Canada

- Mexico

-

Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

-

Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

-

Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

-

South America

- Brazil

- Argentina

- Rest of South America

-

North America

Detailed Research Methodology and Data Validation

Primary Research

Structured interviews with contract fill-finish engineers, sterile packaging experts, hospital pharmacists, and regulatory reviewers across North America, Europe, and key Asian hubs help us verify usage rates, average selling prices, and upcoming molecule launches. Surveys of diabetes and oncology clinicians further calibrate patient-side adoption assumptions that secondary data cannot reveal.

Desk Research

Our analysts first map the demand pool using freely available tier-one sources such as US FDA Biologics License Application archives, EMA's EudraGMDP batch recall notices, UN Comtrade HS 901831 shipment data, and International Diabetes Federation prevalence tables, which signal therapy volumes. Company 10-Ks, investor decks, and scientific papers in the Journal of Pharmaceutical Sciences clarify fill-finish capacities and failure modes. To cross-check competitive footprints, we draw limited metrics from D&B Hoovers and Dow Jones Factiva. These sources are illustrative, not exhaustive; many additional public databases enrich the evidence base.

Market-Sizing & Forecasting

We begin with a top-down reconstruction. Global production of sterile dual-chamber blanks is aligned with trade volumes and regional fill-finish utilization, then adjusted for average reject rates before deriving revenue. Select bottom-up checks, such as supplier roll-ups, sampled ASP × unit volumes, and hospital purchasing audits, validate and fine-tune totals. Key variables guiding the model include (i) annual count of lyophilized biologic approvals, (ii) GLP-1 treated patient pool, (iii) average glass barrel conversion yield, and (iv) regional tender pricing trends. A multivariate regression that links these drivers to historical revenue underpins the forecast, while scenario analysis captures shifts in self-injection adoption and polymer uptake. Where bottom-up evidence is thin, gap factors are transparently disclosed and sensitivity tested.

Data Validation & Update Cycle

Outputs pass variance and anomaly screens, after which senior reviewers compare them with independent capacity expansions and import trends. Reports refresh each year, and triggered re-checks occur when material events, such as regulatory recalls, major line closures, or >10% price moves, surface, ensuring clients always receive an updated baseline.

Why Mordor's Dual Chamber Prefilled Syringes Market Baseline Commands Reliability

Published estimates differ because firms choose varying design scopes, approval cut-off dates, and price assumptions. Our disciplined selection of lyophilized-ready formats, 2025 currency averaging, and annual refresh cadence minimizes such noise.

Key gap drivers include: some publishers bundle single-chamber units, others apply uniform ASPs across regions, and a few project capacity plans without validating financing or regulatory lead times.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 195.9 M (2025) | Mordor Intelligence | - |

| USD 176.2 M (2024) | Global Consultancy A | Excludes polymer formats; older currency rates |

| USD 182 M (2025) | Trade Journal B | Uses forecast ASP, not actual contract prices |

| USD 177.7 M (2024) | Research Boutique C | Bundles certain cartridge barrels as syringes |

In sum, by anchoring our model to verifiable production data and real-world prices and by openly flagging assumptions that remain uncertain, Mordor Intelligence delivers a balanced, repeatable baseline that decision-makers can trust.

Key Questions Answered in the Report

What is the current size of the dual chamber prefilled syringes market?

The dual chamber prefilled syringes market size reached USD 208.86 million in 2026 and is projected to grow to USD 287.68 million by 2031 at a 6.61% CAGR.

Which material dominates dual chamber prefilled syringes?

Glass barrels hold 57.30% of market share, but advanced polymers are the fastest climbers, expanding at a 7.12% CAGR through 2031.

Why are dual chamber formats gaining popularity in oncology?

They shorten infusion times, enable fixed-dose combinations like Phesgo, and accommodate high-volume subcutaneous biologics that shrink chair time in clinics.

How does home-care adoption affect market growth?

Home-care channels grow at 7.22% CAGR because autoinjectors raise adherence to 92.9%, cut hospital visits, and now meet streamlined FDA human-factor expectations.

Which region is expanding the fastest?

Asia-Pacific leads in growth, forecast at a 7.42% CAGR, supported by regulatory harmonization and fresh local manufacturing capacity.

What is the key hurdle for new entrants?

Capital expenditure exceeding USD 50 million for barrier-isolator lines and stringent global extractables and leachables requirements create high entry barriers for smaller firms.

Page last updated on: