Highly Reactive Polyisobutylene Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 2.40 Billion |

| Market Size (2031) | USD 3.33 Billion |

| Growth Rate (2026 - 2031) | 6.75% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Highly Reactive Polyisobutylene Market Analysis by Mordor Intelligence

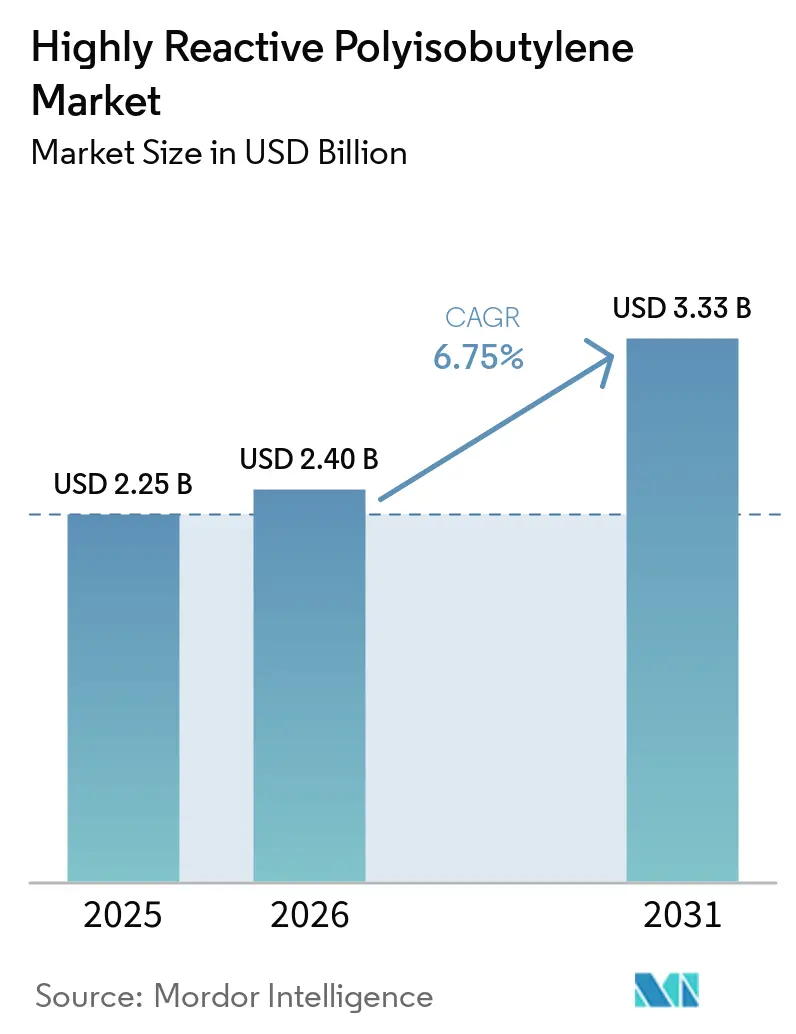

The Highly Reactive Polyisobutylene Market size is projected to be USD 2.25 billion in 2025, USD 2.40 billion in 2026, and reach USD 3.33 billion by 2031, growing at a CAGR of 6.75% from 2026 to 2031. Market participants are transitioning from traditional commodity butyl-rubber applications to specialized uses, including lubricant dispersants, fuel detergents, and sealing compounds for data centers, which benefit from controlled vinylidene reactivity. This shift is driven by four key factors: the growth of electric vehicles (EVs), which increasingly use polyisobutylene (PIB)-rich battery gaskets, stricter emission regulations such as Euro-7 and China VI, requiring ash-free detergent chemistries, the expansion of hyperscale data centers, which prioritize PIB’s dielectric strength, and a constrained supply of isobutylene feedstock, enabling integrated producers to capitalize on high-margin niches. While competitive dynamics remain moderate, regional self-sufficiency is increasing due to capacity expansions in China and South Korea. Simultaneously, formulators in North America and Europe are securing multiyear agreements for medium-molecular-weight grades.

Key Report Takeaways

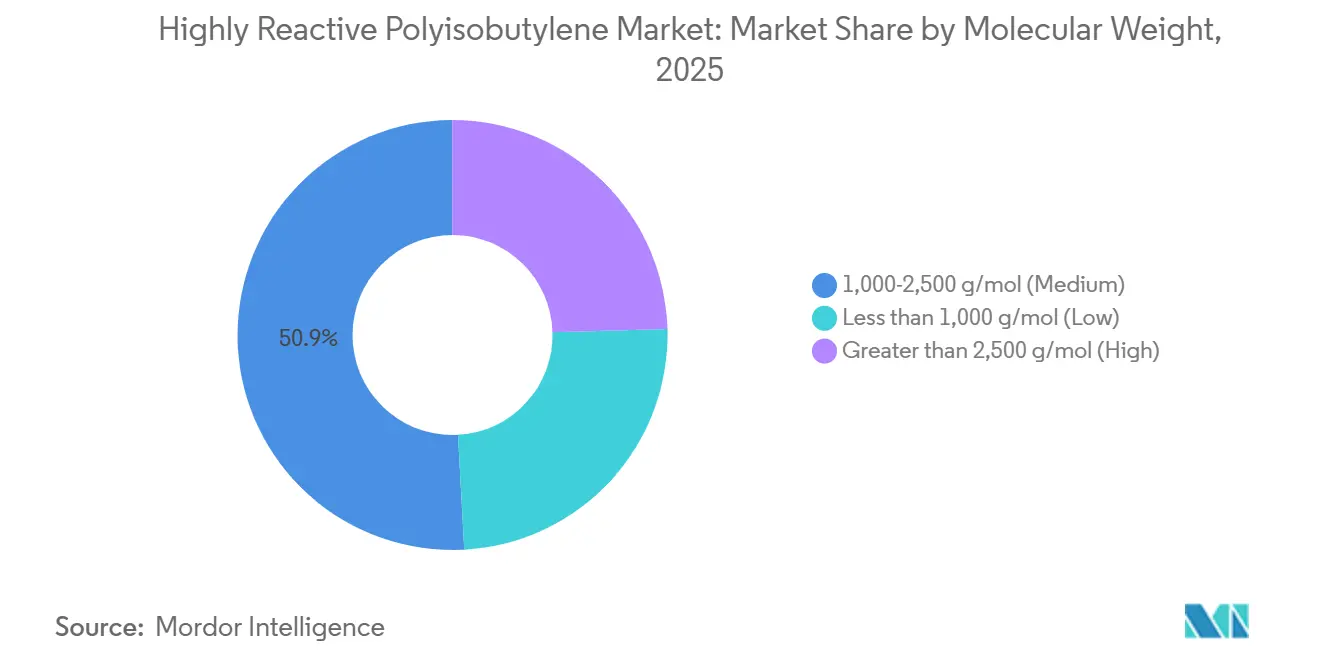

- By molecular weight, 1,000-2,500 g/mol (Medium) captured 50.87% of the highly reactive polyisobutylene market share in 2025, while Greater than 2,500 g/mol (High) are projected to expand at a 6.63% CAGR through 2031.

- By application, adhesives delivered 37.02% of the highly reactive polyisobutylene market size in 2025; fuel detergents are forecast to advance at a 6.89% CAGR to 2031.

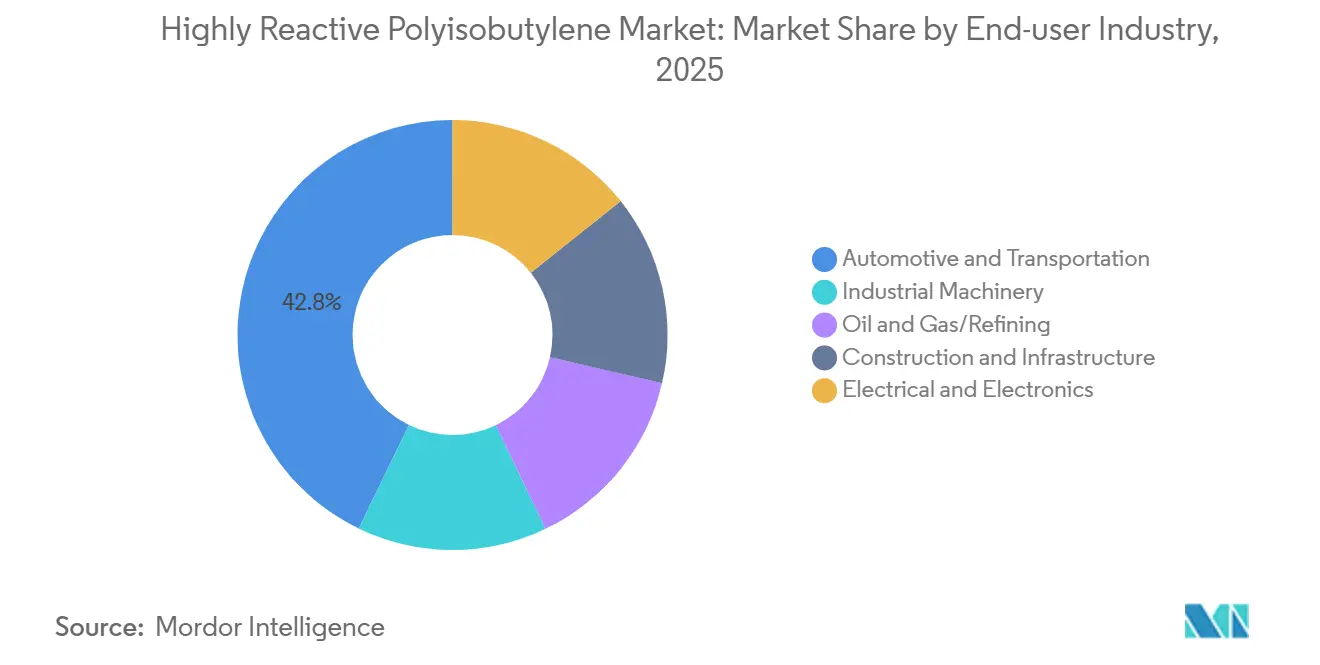

- By end-user industry, automotive and transportation held 42.82% revenue share in 2025, whereas electrical and electronics is expected to post the fastest 7.07% CAGR through 2031.

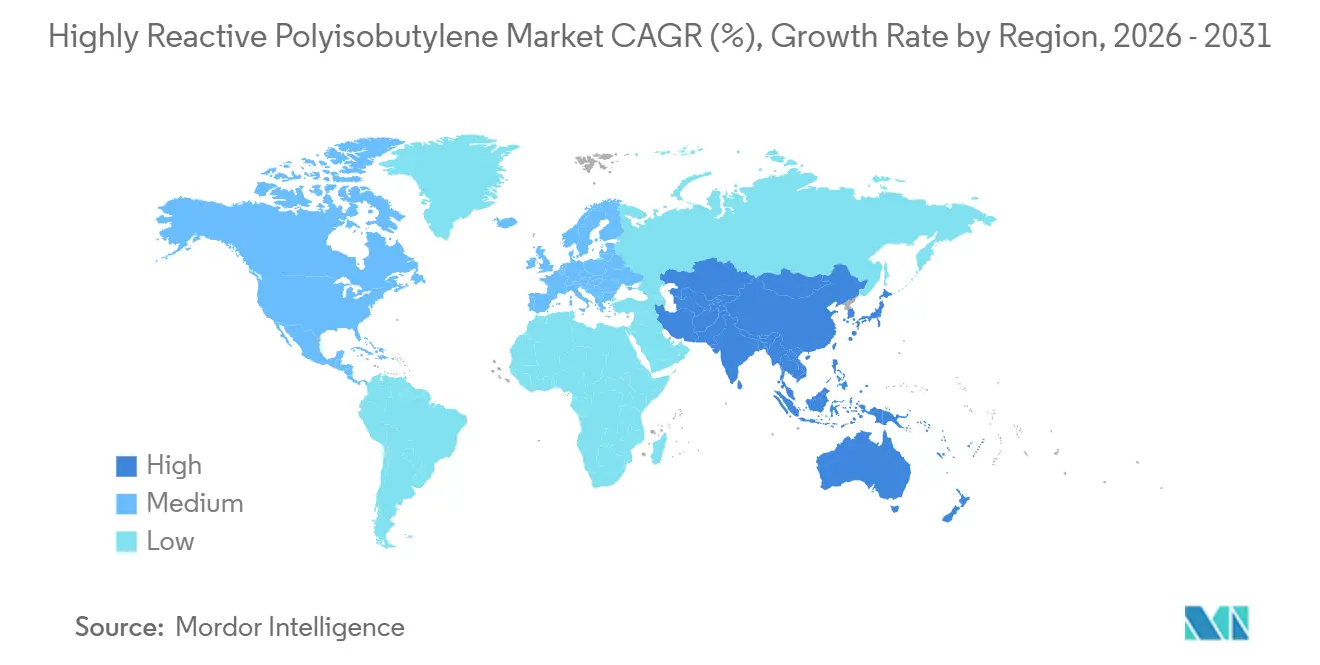

- By geography, Asia-Pacific accounted for 47.03% of the highly reactive polyisobutylene market share in 2024 and is set to grow at a 7.32% CAGR over the forecast window.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Highly Reactive Polyisobutylene Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for fuel and lubricant additives | +1.8% | Global, with a concentration in Asia-Pacific and North America | Medium term (2–4 years) |

| Surge in adhesive and sealant consumption in EV assembly | +1.5% | Asia-Pacific core, spill-over to Europe and North America | Short term (≤ 2 years) |

| Accelerated capacity additions in Asia-Pacific | +1.2% | China, South Korea, ASEAN; export flows to the EU and MEA | Medium term (2–4 years) |

| Regulatory push for low-SAPS and Euro-7-compliant engine oils | +1.0% | Europe, North America, China | Medium term (2–4 years) |

| Emerging role of HR-PIB as binder in solid-state batteries | +0.6% | Japan, South Korea, United States (R&D hubs); early commercial in Asia-Pacific | Long term (≥ 4 years) |

| Commercialization of bio-based isobutylene feedstock | +0.4% | Europe (France, Germany), North America, pilot projects | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Fuel and Lubricant Additives

According to a 2025 peer-reviewed study that combined density-functional theory with engine testing, polyisobutenyl succinimide (PIBSI) dispersants, containing 3.5-4.0% nitrogen, achieved a 98% suppression of low-speed pre-ignition and a 90% reduction in turbocharger deposits compared to metallic detergents. In Mack T-11 trials, the amine centers of the dispersants anchored to soot, while the hydrophobic PIB tails prevented agglomeration, ensuring viscosity rise remained below 20%. China and India bolstered this trend by imposing caps on sulfated ash at 0.5% and phosphorus at 0.08%, effectively sidelining the use of zinc dialkyldithiophosphate.

Surge in Adhesive and Sealant Consumption in EV Assembly

To prevent moisture ingress and contain thermal-runaway gases, electric-vehicle battery packs utilize 8-12 m of PIB-based butyl cord and 200-400 g of hot-melt sealant per unit. Henkel’s LOCTITE RB EV 9740 cord and H.B. Fuller’s EV SEAL 500 grade boast helium permeability below 10⁻¹⁰ cm³·cm/cm²·s·Pa and can withstand temperatures up to 150°C, surpassing acrylic counterparts in 1,000-hour cycling tests[1]Henkel AG, “LOCTITE RB EV 9740 Technical Data Sheet,” Henkel, henkel.com. With global EV assembly projected to exceed 20 million units by 2030, this translates to an additional PIB demand of up to 20,000 t/y.

Accelerated Capacity Additions in Asia-Pacific

Daelim’s HR-PIB complex in Yeosu, boasting a capacity of 185,000 t/y, stands as the world’s largest single site. In 2025, BASF increased output in Ludwigshafen by 10,000 t/y to cater to the rising demand for data-center sealants in Europe. Between 2024 and 2025, three Chinese producers collectively added around 30,000 t/y of high-reactivity capacity, targeting cost-competitive PIBSA intermediates for lubricant blenders in India and Vietnam.

Emerging Role of HR-PIB as Binder in Solid-State Batteries

Research from Oak Ridge National Laboratory revealed that a PIB binder with a molecular weight of 1,270 kg/mol enhanced the NMC811 cathode capacity by 44% and ensured a 90% retention over 90 cycles. This performance eclipsed that of PVDF, which is prone to cracking during volume fluctuations[2]Oak Ridge National Laboratory, “Polyisobutylene Binder for Solid-State Batteries,” ORNL, ornl.gov. Japanese and Korean cell manufacturers are testing PIB binders in sulfide-electrolyte systems, with commercial release anticipated post-2029. If solid-state cells capture a 15% share of the EV market, this could lead to a PIB uptake of 8,000 t/y.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile isobutylene prices | -0.9% | Global, acute in non-integrated producers (North America, Europe, China) | Short term (≤ 2 years) |

| Stringent VOC and carbon-footprint regulations | -0.7% | North America (SCAQMD, CARB), Europe (REACH, national VOC limits) | Medium term (2–4 years) |

| Growing preference for silicone-free sealants in construction | -0.3% | Europe, North America, green-building segments | Medium term (2–4 years) |

| High CAPEX for ultra-low-temperature BF₃ polymerization lines | -0.5% | Global, barrier to entry for new capacity | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile Isobutylene Prices

In Q4 2025, isobutylene prices averaged USD 1,038 per ton in China, compared to USD 1,187 per ton in the United States, driven by differences in refinery run rates. Exxon Mobil Corporation and INEOS AG utilized their captive Fluid Catalytic Cracking (FCC) streams to sustain profit margins, while non-integrated Polyisobutylene (PIB) producers, dependent on merchant isobutylene purchases, reduced new plant investments due to margin pressures.

Stringent VOC and Carbon-Footprint Regulations

The South Coast Air Quality Management District (SCAQMD) Rule 1168 limits VOC content in sealants to 50-250 grams per liter (g/L). Additionally, the European Union (EU) Registration, Evaluation, Authorization, and Restriction of Chemicals (REACH) Annex XVII is phasing out high-aromatic solvents, such as toluene and xylene. Shifting to 100%-solids PIB systems increases raw material costs by up to 25% and impacts adoption rates in cost-sensitive Do-It-Yourself (DIY) markets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Molecular Weight: Medium Grades Anchor Dual-Use Versatility

Medium-molecular-weight grades accounted for 50.87% of the 2025 revenue, establishing them as key contributors in the reactive polyisobutylene market. Their application in pressure-sensitive adhesives and polyisobutylene succinic anhydride (PIBSA) dispersants ensures consistent demand from both packaging and lubricant sectors. High-molecular-weight grades (exceeding 2,500 g/mol) recorded a 6.63% compound annual growth rate (CAGR), gaining adoption in battery binders and cable flooding compounds that require viscosities above 300,000 centistokes (cSt) at 100 °C.

Southeast Asian cable manufacturers identify dielectric strength exceeding 20 kilovolts per millimeter (kV/mm) as a critical factor in transitioning from petroleum jelly to PIB-enriched flooding pastes, indicating a stable demand outlook. In contrast, low-molecular-weight PIB (below 1,000 g/mol) shows slower growth due to refinery alkylate economics, which diverts isobutylene into gasoline blending when octane spreads widen, limiting the availability of this specialty polymer.

By Application: Fuel Detergents Outpace Adhesives on Emission Mandates

Adhesives held a significant 37.02% revenue share in 2025, while stricter injector deposit regulations have positioned fuel detergents as the fastest-growing sub-segment with a 6.89% CAGR. Treat rates in Tier 3 gasoline have increased to 300-500 parts per million (ppm), driving PIB demand even as gasoline volumes stabilize. Medium-molecular-weight PIB, essential for PIBSA packages meeting Euro-7 ash caps, supports the 28% volume share absorbed by lubricant dispersants. Sealant tapes and cable compounds, which together account for approximately 20% of consumption, benefit from growth tied to infrastructure investments.

By End-User Industry: Electrical Surges on Data-Center Insulation

The automotive and transportation sectors held a 42.82% share of 2025 sales, while the electrical and electronics industry is projected to grow at 7.07% through 2031, surpassing other segments. Data-center developers increasingly prefer PIB-based breathable membranes, which manage vapor effectively while ensuring fire retardancy. With the expansion of hyperscale campuses, an additional 3,000-5,000 tons per year (t/y) of PIB demand is expected by 2028. Industrial machinery and oil-and-gas refining sectors maintain a steady 12-15% share, aligning with global Purchasing Managers' Index (PMI) trends and capital expenditure (CAPEX) cycles. The construction industry, holding close to a 10% share, faces challenges from silicone-free design standards.

Geography Analysis

Asia-Pacific, accounting for 47.03% of 2025's revenue, is growing at a 7.32% compound annual growth rate (CAGR). This growth is supported by China's efforts toward self-reliance in synthetic lubricants and the cost efficiencies achieved at Daelim's Yeosu site in South Korea. By 2031, the region's share in the highly reactive polyisobutylene market is expected to exceed 50%. This increase is driven by regional blenders raising polyisobutylene succinimide (PIBSI) inclusion rates in passenger-car oils to comply with China VI-B emission standards.

North America accounted for a significant portion of global consumption, supported by integrated value chains. Companies such as TPC Group, ExxonMobil, and INEOS direct fluid catalytic cracking (FCC)-sourced isobutylene into their proprietary polyisobutylene (PIB), polyisobutylene succinic anhydride (PIBSA), and detergent production facilities. In 2024, TPC Group expanded its diisobutylene capacity by 27%, positioning itself to supply low-global warming potential (GWP) refrigerant lubricants in compliance with the Kigali Amendment.

Europe contributed through key industry players. BASF's facilities in Ludwigshafen and Antwerp focus on medium-molecular-weight grades, which are used in low-sulfated ash, phosphorus, and sulfur (low-SAPS) engine-oil packages for Euro-7 test fleets. Although strict volatile organic compound (VOC) limits have reduced construction sealant volumes, demand for breathable membranes in net-zero buildings has supported specialty polyisobutylene (PIB) consumption. South America and the Middle East-Africa, together accounting for less than 5%, may see growth following the 2027 start-up of Saudi Arabia's USD 11 billion Amiral petrochemical complex, which integrates isobutylene extraction with specialty polymer production.

Competitive Landscape

The highly reactive polyisobutylene market is moderately concentrated. The top five players include BASF, INEOS AG, TPC Group, Daelim Co., Ltd., and Lubrizol. Daelim has the highest single-site production capacity, while BASF, with a strategic presence across multiple continents, reduces logistics risks. These companies are managing feedstock fluctuations by utilizing captive Fluid Catalytic Cracking (FCC) isobutylene. The cost savings from this approach are being directed toward research and development (R&D) initiatives, such as BASF’s work on low-volatility cable compounds and ExxonMobil’s advancements in detergent modeling for improved performance.

Specialty formulators in the U.S. and China, including Shandong Orient Hongye, KZJ New Materials, RB Products, and Janex, are establishing specific niches. Their focus is on customized molecular-weight cuts and faster lead times. Intellectual property is a key competitive factor: Chevron Oronite’s patented post-treated Polyisobutylene Succinimide (PIBSI) technology limits soot-thickening viscosity increases to under 20%, outperforming standard dispersants. Lubrizol plans to enhance additive design with its 2025 introduction of digital twin modeling and machine-learning techniques for amine center geometry, which will streamline cycles and improve product differentiation. Suppliers targeting the European market are strengthening their credentials by obtaining Registration, Evaluation, Authorization, and Restriction of Chemicals (REACH) registration, ISO 9001 certification, and compliance with South Coast Air Quality Management District (SCAQMD) Rule 1168 to access premium markets restricted by Volatile Organic Compound (VOC) regulations.

Highly Reactive Polyisobutylene Industry Leaders

TPC Group

BASF

Lubrizol

INEOS AG

Daelim Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Lubrizol published multiscale modeling research that explains polyisobutylene succinimide (PIBSI) soot-dispersancy mechanisms, highlighting its role in the development of Euro-7-compliant additives. The study connects these mechanisms to highly reactive polyisobutylene, which is critical for enhancing additive performance in managing soot levels effectively.

- October 2024: TPC Group expanded its diisobutylene (DIB) production capacity by 27% in Texas to support the growing demand for low-global warming potential (GWP) refrigerant lubricants under the Kigali phasedown. This expansion is expected to enhance the supply of highly reactive polyisobutylene (HR-PIB), a key component in the production of these refrigerant lubricants.

Global Highly Reactive Polyisobutylene Market Report Scope

Highly reactive polyisobutylene is a specialized polymer containing over 80% of terminal double bonds (exo-olefin end groups), unlike conventional Polyisobutylene (PIB), which has internal double bonds. This structure enhances its reactivity, enabling the efficient production of fuel and lubricant additives, such as Polyisobutylene Succinic Anhydride (PIBSA), and sealants.

The highly reactive polyisobutylene market is segmented by molecular weight, application, end-user Industry, and geography. By molecular weight, the market is segmented into less than 1,000 g/mol (Low), 1,000-2,500 g/mol (Medium), and greater than 2,500 g/mol (High). By application, the market is segmented into adhesives, lubricant dispersants, fuel detergents, sealant tapes, cable compounds, and others. By end-user Industry, the market is segmented into automotive and transportation, industrial machinery, oil and gas/refining, construction and infrastructure, and electrical and electronics. The report also covers the market size and forecasts for highly reactive polyisobutylene in 17 countries across major regions. The market sizes and forecasts are provided in terms of value (USD).

| Less than 1,000 g/mol (Low) |

| 1,000-2,500 g/mol (Medium) |

| Greater than 2,500 g/mol (High) |

| Adhesives |

| Lubricant Dispersants |

| Fuel Detergents |

| Sealant Tapes |

| Cable Compounds and Others |

| Automotive and Transportation |

| Industrial Machinery |

| Oil and Gas/Refining |

| Construction and Infrastructure |

| Electrical and Electronics |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Molecular Weight | Less than 1,000 g/mol (Low) | |

| 1,000-2,500 g/mol (Medium) | ||

| Greater than 2,500 g/mol (High) | ||

| By Application | Adhesives | |

| Lubricant Dispersants | ||

| Fuel Detergents | ||

| Sealant Tapes | ||

| Cable Compounds and Others | ||

| By End-user Industry | Automotive and Transportation | |

| Industrial Machinery | ||

| Oil and Gas/Refining | ||

| Construction and Infrastructure | ||

| Electrical and Electronics | ||

| By Geography | Asia-Pacific | China |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large will the highly reactive polyisobutylene market be by 2031?

The Highly Reactive Polyisobutylene Market size is projected to be USD 2.25 billion in 2025, USD 2.40 billion in 2026, and reach USD 3.33 billion by 2031, growing at a CAGR of 6.75% from 2026 to 2031.

Which region is growing fastest for highly reactive polyisobutylene demand?

Asia-Pacific is advancing at a 7.32% CAGR through 2031, driven by new Chinese and Korean capacity and higher PIBSI treat rates in lubricants.

What application segment is expanding most rapidly?

Fuel detergents are projected to post a 6.89% CAGR to 2031 as Euro-7 and China VI rules tighten injector-deposit limits.

Why are medium-molecular-weight grades so dominant?

Grades between 1,000-2,500 g/mol serve both PIBSA dispersants and pressure-sensitive adhesives, capturing more than 50% of 2025 revenue.

Page last updated on: