Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

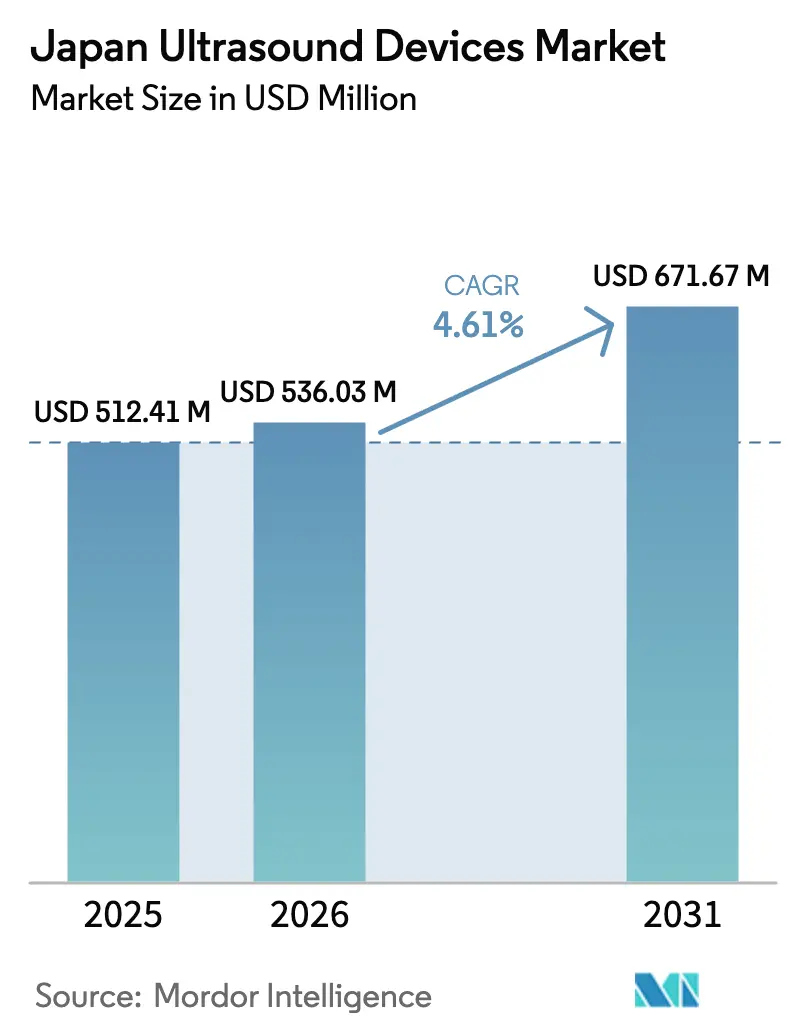

| Base Year Market Size (2025) | USD 512.41 Million |

| Market Size (2026) | USD 536.03 Million |

| Market Size (2031) | USD 671.67 Million |

| Growth Rate (2026 - 2031) | 4.61% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Japan Ultrasound Devices Market Analysis by Mordor Intelligence

Japan Ultrasound Devices Market size in 2026 is estimated at USD 536.03 million, growing from 2025 value of USD 512.41 million with 2031 projections showing USD 671.67 million, growing at 4.61% CAGR over 2026-2031.

Demographic aging, chronic-disease prevalence, and systematic replacement of analog scanners underpin steady demand, while AI-enabled 3D/4D platforms and handheld devices create new revenue pools in emergency, primary-care, and home-care settings. Hospitals are renewing infrastructure that is more than four decades old, driving near-term procurement despite capital-budget constraints under bundled DRG payments. At the same time, a limited pool of certified sonographers pushes providers toward automated imaging solutions. Competitive intensity is shaped by alliances such as Canon-Olympus in endoscopic ultrasound, and by the emergence of focused ultrasound for therapeutic oncology, both of which reinforce the strategic importance of domestic R&D investment.

Key Report Takeaways

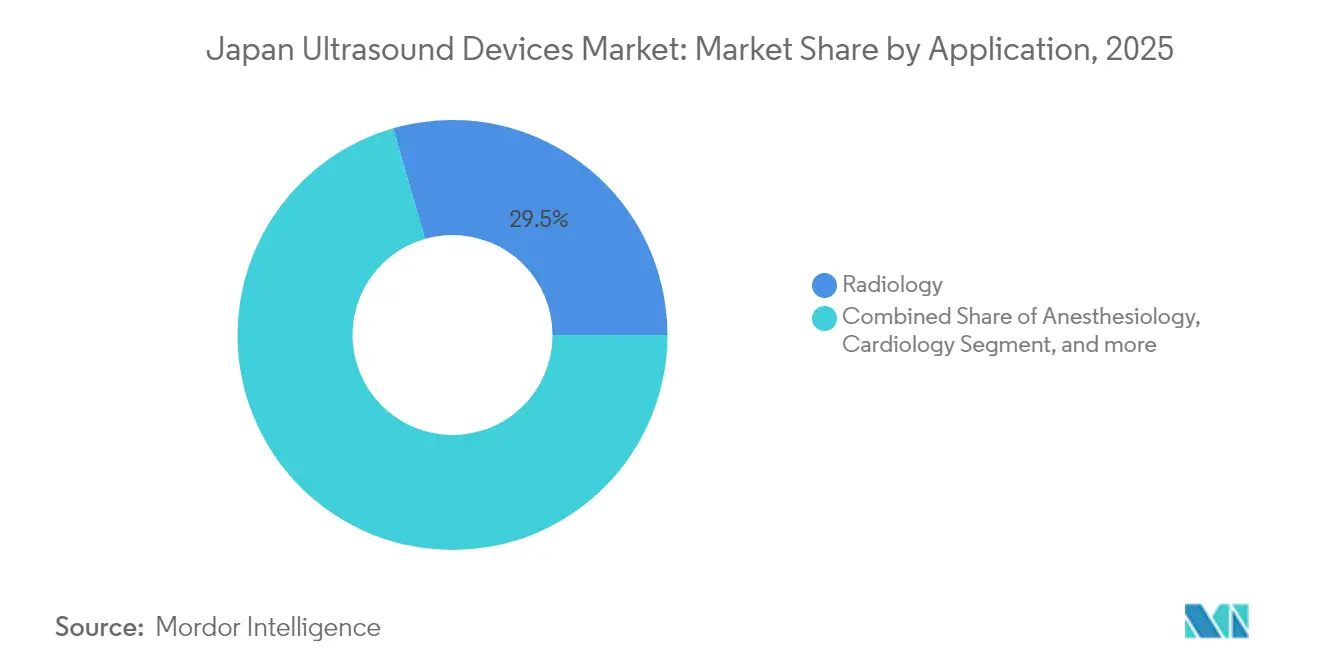

- By application, radiology held 29.45% of Japan ultrasound market share in 2025, while critical care is advancing at a 6.38% CAGR through 2031.

- By technology, 3D/4D systems commanded 44.12% share of Japan ultrasound market size in 2025; high-intensity focused ultrasound is projected to expand at 5.79% CAGR between 2026-2031.

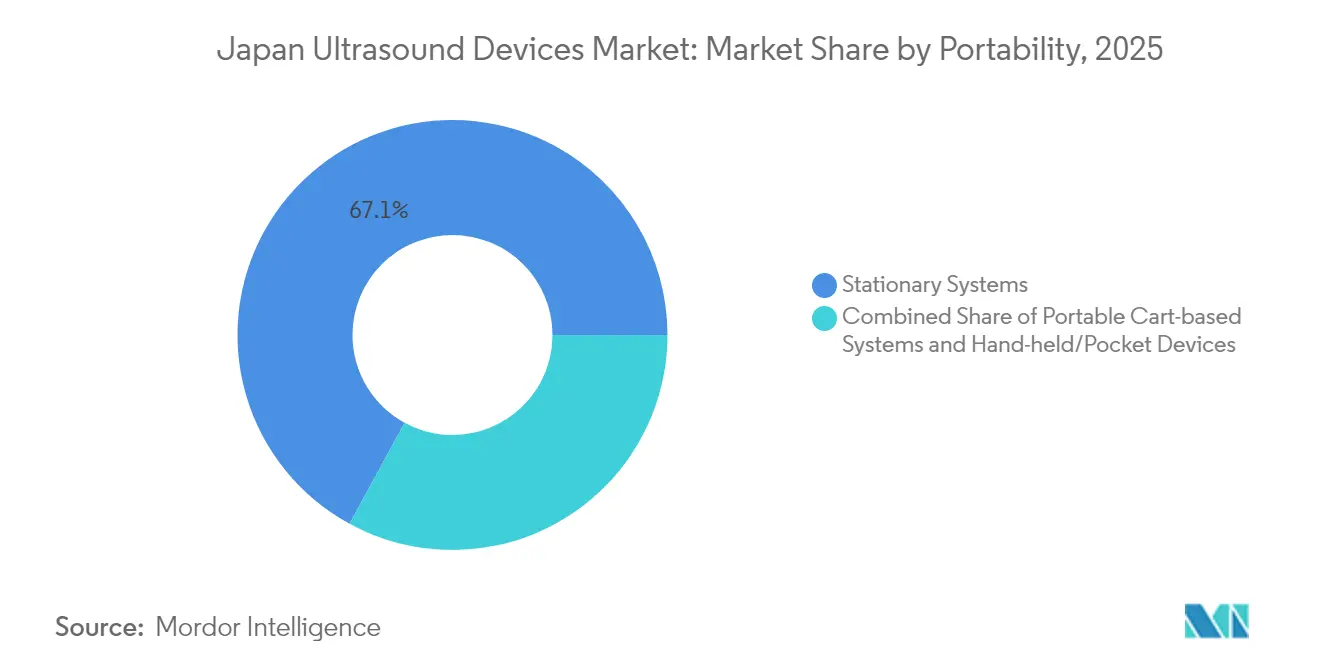

- By portability, stationary consoles accounted for 67.05% of Japan ultrasound market size in 2025, whereas handheld devices are growing at 7.74% CAGR through 2031.

- By end user, hospitals and academic medical centers represented 56.72% of Japan ultrasound market share in 2025, but private hospitals record the fastest 7.12% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Japan Ultrasound Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising burden of chronic diseases & aging population | +1.2% | Nationwide, strongest in rural prefectures | Long term (≥ 4 years) |

| Accelerated adoption of AI-enabled 3D/4D & handheld ultrasound | +0.9% | Urban hubs, extending to regional hospitals | Medium term (2-4 years) |

| Government-funded point-of-care ultrasound training initiatives | +0.7% | Nationwide, priority for underserved areas | Short term (≤ 2 years) |

| Replacement of aging analog systems | +0.8% | Nationwide, acute in 40-year-old hospitals | Medium term (2-4 years) |

| Breast-density screening programs | +0.6% | Urban screening centers | Medium term (2-4 years) |

| Technological innovation & domestic R&D | +0.5% | Tokyo and Osaka technology clusters | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Burden of Chronic Diseases & Aging Population

Japan’s over-65 demographic now exceeds 30% of the population, creating sustained demand for cardiovascular and musculoskeletal imaging where ultrasound offers non-invasive, radiation-free diagnostics. Elderly patients’ preference for outpatient care bolsters portable scanner uptake, especially for home-health and rehabilitation services.[1]Ministry of Health, Labour and Welfare, “Digital Health Strategy 2025,” mhlw.go.jp GE Healthcare’s Voluson Performance 18 was positioned to mitigate obstetrician shortages while supporting perinatal networks. Policy goals that extend healthy life expectancy depend on early detection programs reliant on ultrasound, anchoring long-term growth for the Japan ultrasound market.

Accelerated Adoption of AI-Enabled 3D/4D & Handheld Ultrasound

AI-driven software such as RN-Descartes and METIS Eye demonstrates sensitivity rates that outstrip manual interpretation in breast-cancer detection, directly addressing Japan’s sonographer shortfall. Multicenter trials of the KOSMOS handheld platform reported 91.5% clinical applicability, validating bedside use in emergency and rural clinics. The fusion of 3D/4D imaging with real-time AI analytics expands clinical value in cardiology and obstetrics, although PMDA has cleared only two AI SaMD applications to date, creating a window of advantage for early license holders.[2]Fujioka T. et al., “AI-Based Breast Ultrasound CADx Validation,” fujooka-lab.org

Government-Funded Point-of-Care Ultrasound Training Initiatives

The Ministry of Health subsidizes POCUS programs delivered through the Japan Society of Ultrasonics in Medicine, whose certification exams in November 2024 attracted a record cohort of multidisciplinary practitioners. Studies show structured curricula raise operator accuracy and cut scan time, reinforcing adoption in emergency departments, primary-care clinics, and neonatal ICUs. Formation of the National Neonatal POCUS Collaborative expands standardized protocols, ensuring quality outcomes while accelerating device turnover.

Replacement of Aging Analog Systems

More than 1,600 Japanese hospitals operate wards, and analog scanners within these facilities fail to meet updated echocardiography maintenance guidelines. Digital transformation initiatives require DICOM-compliant connectivity and cybersecurity features absent in legacy hardware, pushing replacement cycles forward despite CAPEX limits. COVID-19 heightened infection-control standards, favoring sealed transducers and touchless interfaces available only in newer models, thereby supporting short-to-medium-term demand.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lengthy PMDA approval timelines & post-market costs | -0.6% | Nationwide, all device categories | Long term (≥ 4 years) |

| Constrained hospital CAPEX under bundled DRG payments | -0.8% | Nationwide, heaviest in public sector | Medium term (2-4 years) |

| Shortage of certified sonographers & uneven skills | -0.4% | Rural prefectures and small cities | Medium term (2-4 years) |

| Price competition from low-cost Chinese imports | -0.3% | Nationwide, mid-tier segments | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Lengthy PMDA Approval Timelines & Post-Market Surveillance Costs

Ultrasound vendors allocate 9-16 months to navigate PMDA pathways, prolonging cash-flow breakeven and advantaging incumbents with legacy approvals. Compliance with Ordinance 169 and ISO 13485 mandates exhaustive validation, while ongoing vigilance reports pile additional costs. Only two of 27 AI SaMD filings have been cleared, illustrating systemic hurdles that temper innovation velocity in the Japan ultrasound market.[3]Pharmaceuticals and Medical Devices Agency, “Medical Device Review Statistics 2024,” pmda.go.jp

Constrained Hospital CAPEX Under Bundled DRG Payments

Episode-based reimbursements cap revenue regardless of diagnostic sophistication, restricting equipment budgets particularly in the public segment that commands the majority of scan volumes. Facilities juggling structural renovations and device upgrades often favor mid-range models or defer replacements, lengthening sales cycles for premium consoles. Private providers, less tethered to DRG constraints, post higher scanner-acquisition growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Critical Care Expands Amid Radiology Leadership

Radiology generated 29.45% of Japan ultrasound market size in 2025 and remains the backbone of imaging services because every hospital relies on general-purpose consoles for abdominal, vascular, and soft-tissue diagnostics. Growth, however, pivots toward critical-care usage where bedside sonography guides fluid resuscitation, detects pneumothorax, and monitors cardiac function in hemodynamically unstable patients. Certification modules by the Japan Society of Ultrasonics in Medicine reinforce proficiency, ensuring uniform quality nationwide.

Critical-care volumes are predicted to rise at 6.38% CAGR to 2031, propelled by intensivist adoption of portable probes and handhelds that connect wirelessly to hospital PACS. Rapid decision-making reduces ICU length of stay, appealing to administrators operating under DRG cost ceilings. As a result, critical care’s share of Japan ultrasound market size is likely to climb beyond its current 11.05% threshold, gradually diluting radiology’s dominance while catalyzing software-as-a-service revenues through AI-based hemodynamic analysis modules.

By Technology: HIFU Innovation Challenges 3D/4D Supremacy

3D/4D imaging occupied 44.12% of Japan ultrasound market share in 2025 thanks to entrenched obstetrics and cardiology workflows. Volumetric datasets improve anomaly detection, a quality metric prized by insurers and clinicians alike. Yet high-intensity focused ultrasound is charting the fastest 5.79% CAGR, propelled by oncology trials evaluating non-invasive ablation for liver, prostate, and pancreatic tumors. Domestic startups translate photonics and robotics know-how into precise beam steering, seeking to commercialize hybrid diagnostic-therapeutic suites.

2D and Doppler modalities continue across routine abdominal scans and vascular studies, especially where hospital budgets remain tight. Even so, vendors embed AI noise suppression and auto-measure algorithms into baseline 2D systems, raising clinical value without inflating price tags. This staircase innovation approach keeps adoption broad while protecting the Japan ultrasound market from abrupt technology obsolescence risk.

By Portability: Handheld Wave Redefines Point-of-Care

Consoles anchored to imaging suites still generate 67.05% of 2025 revenue, but handheld probes lighter than 400 g and tethered to tablets are capturing physician mindshare at an 7.74% CAGR. Pandemic-era infection-control lessons persuaded clinicians to triage patients at the bedside, a workflow handhelds facilitate. Comparative bench tests ranked SonoEye and Vscan Air highest for B-mode clarity and ergonomic software, demonstrating capability parity with mid-range carts.

Cart-based portables deliver a middle path by preserving Doppler and elastography features while rolling easily between wards. Nevertheless, reimbursement parity for handheld examinations, combined with the government’s free-loan program for rural clinics, accelerates volume migration toward pocket devices.

By End User: Private Hospitals Outpace Public Counterparts

Public hospitals and university clinics held 56.72% of Japan ultrasound market share in 2025, reflecting their role as tertiary centers and teaching hubs. They face the heaviest architectural depreciation and DRG-linked capital rationing, limiting rapid fleet renewal. Conversely, private hospitals expand imaging suites to secure competitive differentiation, delivering a forecast 7.12% CAGR through 2031.

Diagnostic imaging centers maintain specialized ABUS and vascular services, chiefly in metropolitan areas where population density yields economies of scale. Ambulatory surgery centers and specialty clinics form a tertiary customer tier, leveraging handhelds for pre-operative assessments. Emerging home-health organizations pilot remote ultrasound guided by tele-mentoring, opening a nascent consumer-facing channel for the Japan ultrasound market.

Geography Analysis

Metropolitan corridors encompassing Tokyo, Osaka, and Nagoya account for major share of ultrasound equipment installed base, undergirded by high patient throughput and abundant specialist availability. These cities spearhead AI pilots where cloud connectivity and 5G support real-time data off-loading, reinforcing continuous imaging workflow upgrades. Rural prefectures, by contrast, struggle with physician shortfalls and transportation barriers; handheld scanners, shipped via government grant programs, bridge access gaps by enabling community nurses and general practitioners to perform basic echography under remote supervision.

Regional replacement cycles track aging infrastructure: hospitals older than 40 years cluster disproportionately in northern Tohoku and parts of Kyushu, generating concentrated demand for console swaps. However, budgetary latitude is narrower; thus vendors often propose trade-in packages and deferred-payment schedules to clinch deals. Island communities such as Okinawa leverage tele-ultrasound to channel images to mainland radiologists, demonstrating how connectivity mitigates geographic isolation.

Medical-device manufacturing itself is geospatially clustered; Canon’s Tochigi plant and Fujifilm’s Saitama R&D hub anchor an innovation belt that collaborates closely with university hospitals. Policy makers encourage such clusters through tax incentives and expedited land-use approvals, ensuring Japan ultrasound market resiliency against global supply-chain headwinds. Standardized PMDA regulations apply nationwide, maintaining product-quality parity irrespective of facility locale.

Competitive Landscape

The field is moderately concentrated: the top five suppliers collectively control significant sales, balancing domestic incumbency and global scale. Canon Medical leverages its diagnostic pedigree while Olympus contributes optical leadership to their joint endoscopic-ultrasound venture launched in 2024. Fujifilm’s outpatient-focused cart systems integrate AI triage through a partnership with Us2.ai, exemplifying ecosystem strategies that marry imaging hardware with cloud analytics.

GE Healthcare and Philips adapt flagship platforms to Japan-specific ergonomics, for instance by downsizing console footprints and localizing interface language nuances. Meanwhile, Shenzhen-based entrants price aggressively 20-25% below median but still require PMDA clearance, tempering immediate share wins. Focused-ultrasound startups pursue oncology niches, a pathway potentially insulated from price wars due to therapeutic value differentiation.

Service offerings broaden from warranty-linked maintenances to subscription-based AI upgrades and remote uptime monitoring, mirroring hospital demand for predictable OPEX within DRG confines. Consequently, the basis of competition shifts from pure hardware specs to lifecycle economics and workflow integration a trend likely to reinforce strategic partnerships and consolidation over the forecast horizon of the Japan ultrasound market.

Japan Ultrasound Devices Industry Leaders

Fujifilm Holdings Corporation

GE Healthcare

Siemens Healthineers AG

Canon Medical Systems Corporation

Koninklijke Philips N.V.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Furuno demonstrated its commitment to medical innovation by exhibiting at the JETRO Pavilion during Japan Health 2025, held at INTEX Osaka from June 25 to 27, 2025. This strategic presence highlighted Furuno’s expanding portfolio in diagnostic imaging and clinical analysis. This exhibition underscores Furuno’s ongoing efforts to deliver innovative, reliable, and user-friendly medical solutions that meet the needs of healthcare professionals across diverse clinical settings.

- February 2025: Canon Medical Systems Corporation officially introduced Aplio Beyond, a cutting-edge multi-purpose ultrasound system designed to meet the evolving demands of modern imaging environments in Japan. The launch reinforces Canon Medical’s leadership in delivering clinically advanced, operationally efficient, and ergonomically optimized imaging solutions.

- November 2024: Mindray, a prominent player in healthcare technologies spanning ultrasound, patient monitoring, and anesthesia, has announced the launch of its Consona-Series Ultrasound Machines, marking a significant expansion of its private office imaging portfolio.Powered by Mindray’s proprietary Zone Sonography Technology+ (ZST+), a software-based beamformer, the Consona-Series sets a new standard in shared service ultrasound environments, with tailored solutions for women’s health, radiology, and cardiovascular care.

Japan Ultrasound Devices Market Report Scope

As per the scope of the report, ultrasonography is an imaging method that creates images of various body structures using high-frequency sound waves. They are used to evaluate a variety of disorders relating to the liver, kidneys, and other abdominal conditions, including usage in pregnancy. As a result, these devices have a variety of uses in the medical area, including diagnostic imaging and therapeutic modality.

Japan ultrasound device market is segmented by application, technology, and type. Based on application the market is segmented as anesthesiology, cardiology, gynecology/obstetrics, musculoskeletal, radiology, critical care, and other applications). Based on technology the market is segmented into 2D ultrasound imaging, 3D and 4D ultrasound imaging, doppler imaging, and high-intensity focused ultrasound. Based on type the market is segmented as stationary ultrasound and portable ultrasound. The report offers the value (in USD) for the above segments.

By Application

| Anesthesiology |

| Cardiology |

| Gynecology / Obstetrics |

| Musculoskeletal |

| Radiology |

| Critical Care |

| Urology |

| Vascular |

| Other Applications |

By Technology

| 2D Ultrasound Imaging |

| 3D & 4D Ultrasound Imaging |

| Doppler Imaging |

| High-Intensity Focused Ultrasound |

| Other Technologies |

By Portability

| Stationary Systems |

| Portable Cart-based Systems |

| Hand-held / Pocket Devices |

By End User

| Hospitals & Academic Medical Centers |

| Diagnostic Imaging Centers |

| Ambulatory & Specialty Clinics |

| Home-care Settings |

| By Application | Anesthesiology |

| Cardiology | |

| Gynecology / Obstetrics | |

| Musculoskeletal | |

| Radiology | |

| Critical Care | |

| Urology | |

| Vascular | |

| Other Applications | |

| By Technology | 2D Ultrasound Imaging |

| 3D & 4D Ultrasound Imaging | |

| Doppler Imaging | |

| High-Intensity Focused Ultrasound | |

| Other Technologies | |

| By Portability | Stationary Systems |

| Portable Cart-based Systems | |

| Hand-held / Pocket Devices | |

| By End User | Hospitals & Academic Medical Centers |

| Diagnostic Imaging Centers | |

| Ambulatory & Specialty Clinics | |

| Home-care Settings |

Key Questions Answered in the Report

What is the projected value of the Japan ultrasound market in 2031?

It is expected to reach USD 671.67 million, reflecting a 4.61% CAGR.

Which application area is expanding fastest in Japanese ultrasound use?

Critical-care imaging is advancing at 6.38% CAGR through 2031.

How large is the handheld segment expected to become by 2031?

Handheld devices are projected to grow at 7.74% between 2026-2031

Why do PMDA approval timelines matter to device vendors?

They stretch 9-16 months, which delays revenue realization and elevates compliance costs.

What strategic alliance shapes Japan’s endoscopic ultrasound niche?

Canon Medical and Olympus collaborate to co-develop next-generation endoscopic ultrasound systems.

Page last updated on: