High Integrity Pressure Protection System Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

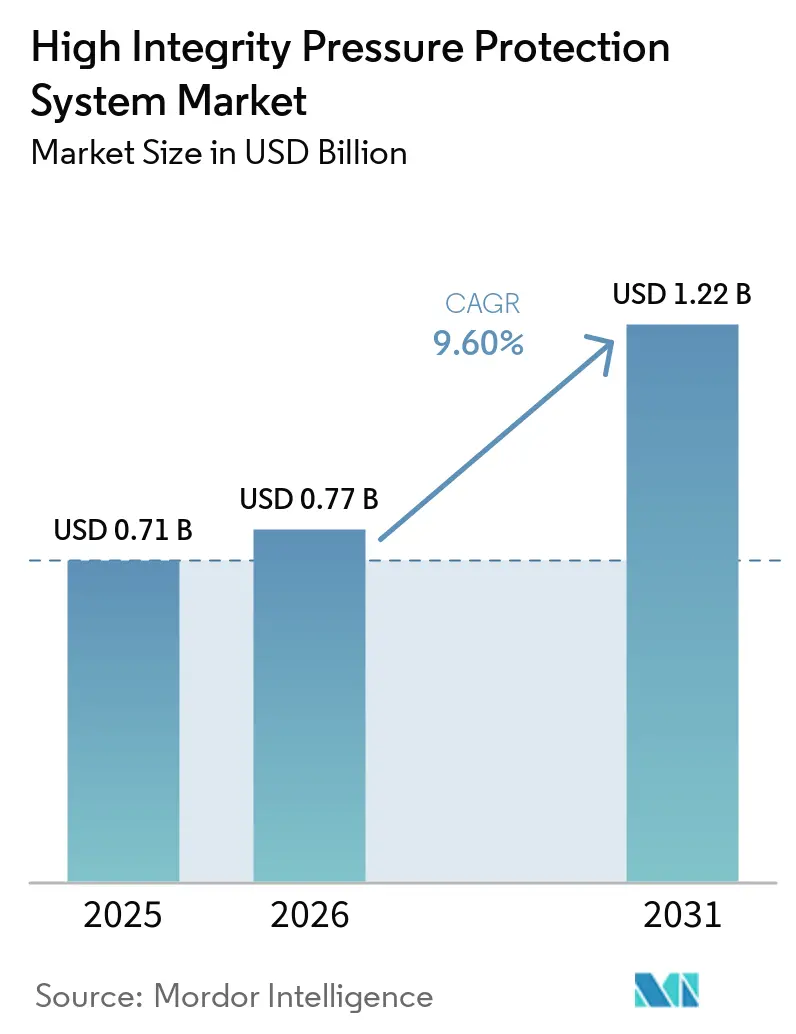

| Market Size (2026) | USD 0.77 Billion |

| Market Size (2031) | USD 1.22 Billion |

| Growth Rate (2026 - 2031) | 9.60% CAGR |

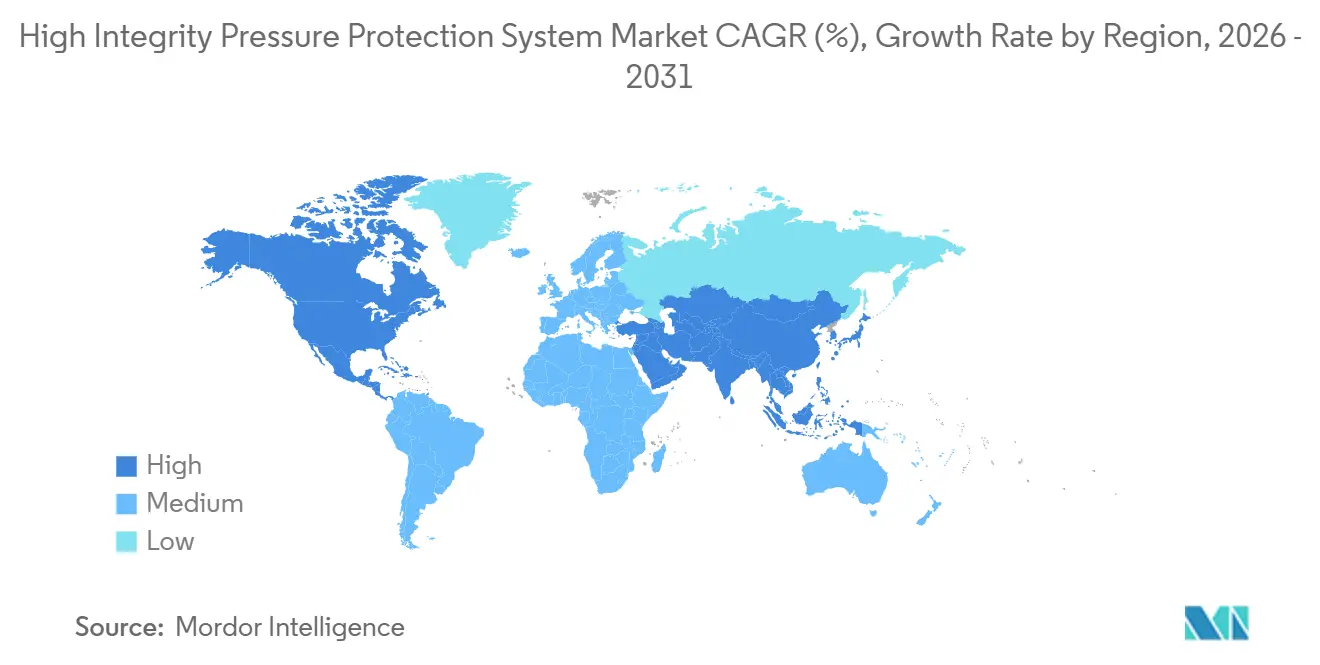

| Fastest Growing Market | Middle East |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

High Integrity Pressure Protection System Market Analysis by Mordor Intelligence

The High Integrity Pressure Protection System market size is expected to increase from USD 0.71 billion in 2025 to USD 0.77 billion in 2026 and reach USD 1.22 billion by 2031, growing at a CAGR of 9.60% over 2026-2031. Escalating functional-safety mandates, headline mega-projects in offshore oil and gas, and rapid build-out of hydrogen and carbon-capture assets are widening the installed base. Offshore deployments are moving to subsea depths where wellhead pressures exceed 10,000 psi, driving demand for titanium-bodied valves and high-speed logic solvers that meet SIL3 targets. Onshore, modular skid-mounted packages are shrinking engineering schedules for LNG trains and blue-hydrogen plants, while lifecycle services built around digital twins are displacing reactive maintenance. Competitive intensity is rising as automation majors fold HIPPS modules into distributed-control-system suites and valve specialists consolidate around ultra-high-pressure niches.

Key Report Takeaways

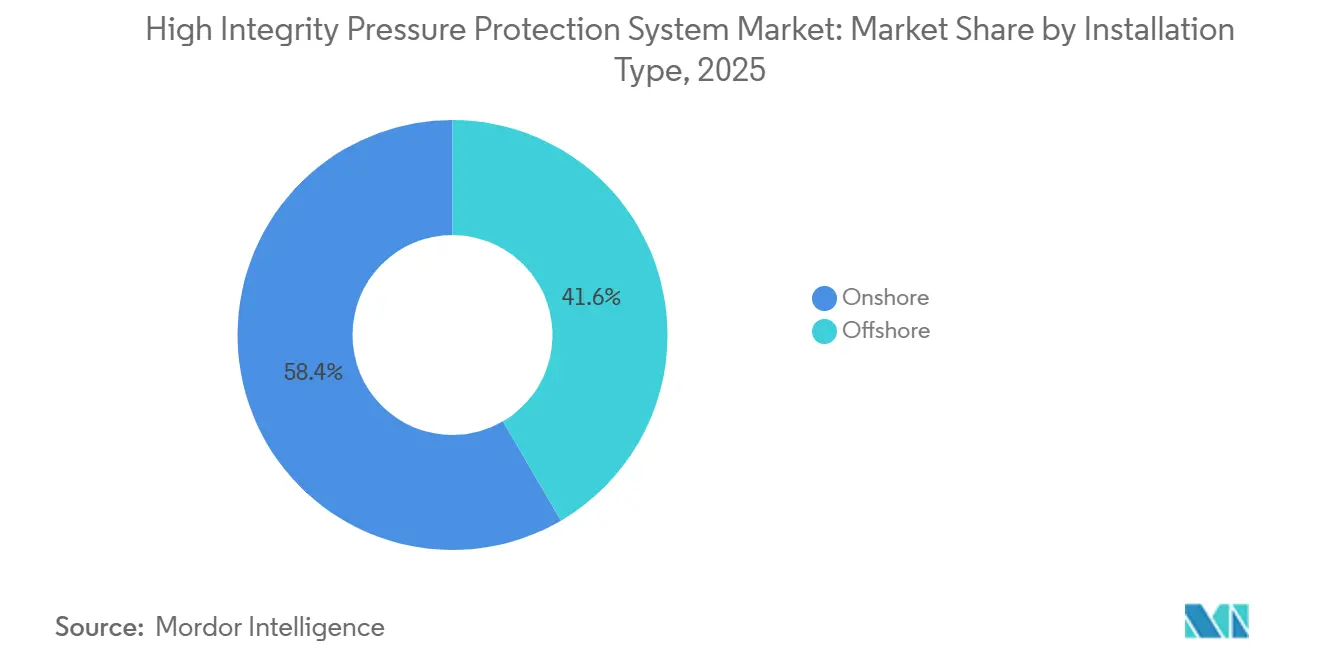

- By installation type, offshore captured 41.59% of the High Integrity Pressure Protection System market share in 2025, while offshore is forecast to expand at a 10.15% CAGR through 2031.

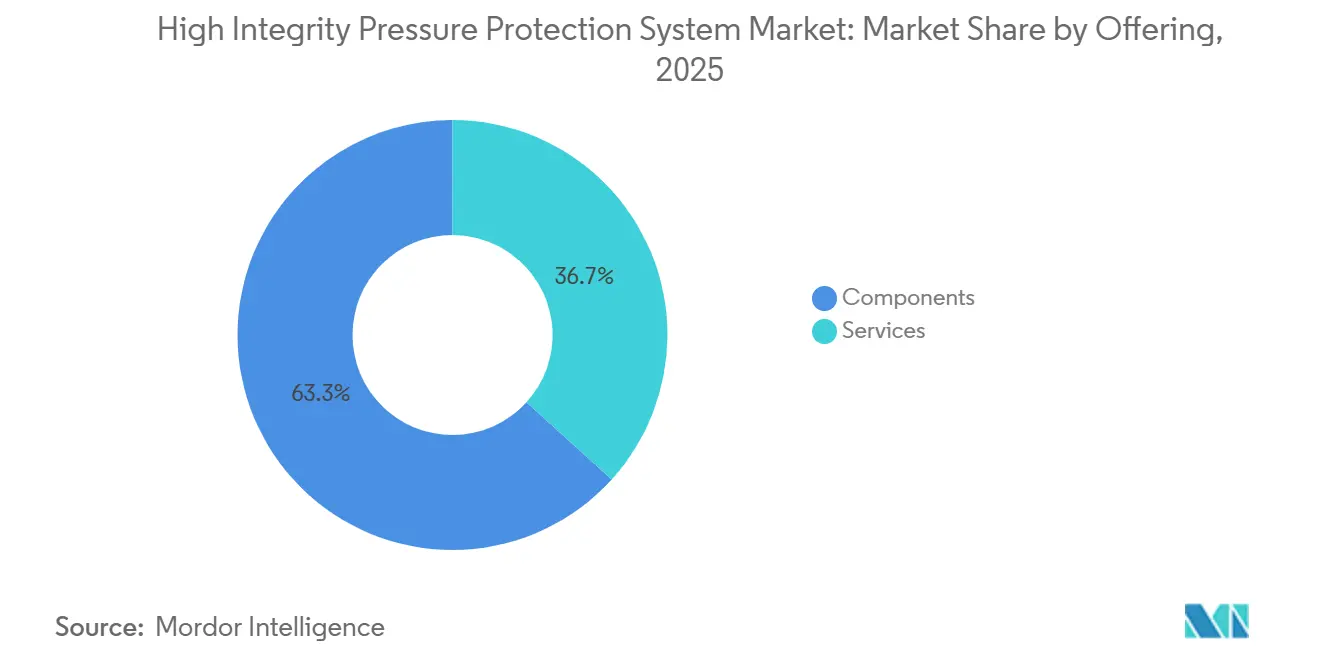

- By offering, components held a 63.28% share of the High Integrity Pressure Protection System market in 2025, whereas services are projected to record the fastest growth at a 10.05% CAGR between 2026 and 2031.

- By end-user industry, oil and gas led with 46.27% revenue share in 2025, but hydrogen and carbon-capture use cases are advancing at a 10.22% CAGR through 2031.

- By pressure rating, the 3000-6000 psi band accounted for 41.15% of the High Integrity Pressure Protection System market in 2025, while systems above 6000 psi are poised for the fastest growth at a 9.98% CAGR.

- By geography, North America retained 34.73% share in 2025, and the Middle East is expected to be the fastest-growing region at 9.91% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global High Integrity Pressure Protection System Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stricter Global Functional-Safety Directives in Oil and Gas | +2.1% | Global, with concentrated enforcement in North America, Europe, Middle East | Medium term (2-4 years) |

| Rapid Growth of Deep-Water Offshore Projects | +1.8% | Americas (Brazil, Gulf of Mexico), Europe (North Sea), Africa (West Africa) | Medium term (2-4 years) |

| Expansion of Hydrogen and Carbon-Capture Infrastructure | +1.6% | Europe (Germany, Netherlands), Asia-Pacific (China, Japan), North America | Long term (≥ 4 years) |

| Increasing Adoption of Modular, Skid-Mounted HIPPS Packages | +1.3% | Global, early gains in Middle East LNG terminals, Asia-Pacific import facilities | Short term (≤ 2 years) |

| Integration With Digital Twins for Predictive Maintenance | +1.0% | North America, Europe, Middle East mega-projects | Medium term (2-4 years) |

| Surge in LNG Import Terminals Across Emerging Markets | +1.5% | Asia-Pacific (India, Southeast Asia), Middle East, South America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stricter Global Functional-Safety Directives in Oil and Gas

The publication of IEC 61511:2026 SER and EEMUA 222 Edition 2 introduced stricter requirements for proof-test intervals, software tool qualification, and management-of-change procedures. Additionally, the updated United Kingdom guidance in 2025 now mandates oversight by a competent person to ensure proper alignment between HAZOP (Hazard and Operability Study) and SIL (Safety Integrity Level) assessments. This regulatory shift has driven increased demand for third-party verification services and integrated lifecycle software solutions that streamline compliance processes and reduce audit preparation time by up to 40%.[1]IEC, “IEC 61511:2026 SER,” IEC webstore, iec.ch These updates have compelled brownfield operators to transition from pneumatic HIPPS to electronic architectures, which provide enhanced diagnostic coverage and improved reliability.

Rapid Growth of Deep-Water Offshore Projects

Ultra-high-pressure reservoirs in Brazil’s pre-salt and Norway’s North Sea routinely exceed 10,000 psi, necessitating the use of subsea High-Integrity Pressure Protection Systems (HIPPS) designed for millisecond closure to prevent overpressure incidents. These systems must also incorporate corrosion-resistant alloys to withstand the harsh subsea environment and ensure long-term reliability. Recent contract awards for compression upgrades and mega Floating Production Storage and Offloading (FPSO) units highlight the critical need for pressure protection systems that seamlessly integrate with electrical fault-limiter schemes and subsea compression trains.[2]SLB, “SLB OneSubsea Awarded Subsea Compression Upgrade For Gullfaks Field,” SLB newsroom, slb.comThis integration is essential to mitigate the risk of catastrophic pipe ruptures, ensuring operational safety and efficiency in these challenging ultra-deepwater conditions.

Expansion of Hydrogen and Carbon-Capture Infrastructure

Germany’s EUR 18.9 billion (USD 20.3 billion) hydrogen pipeline grid and China’s 1,000-kilometer Kangbao-Caofeidian corridor operate at pressures of up to 1,000 bar, which significantly increases the risk of hydrogen embrittlement in sensor diaphragms. To address these challenges, next-generation High-Integrity Pressure Protection Systems are designed with advanced features such as exotic seat materials and high-frequency pressure transmitters. These innovations ensure the systems maintain Safety Integrity Level 3 compliance, even under extreme operating conditions with wide temperature fluctuations and high pressure.

Increasing Adoption of Modular, Skid-Mounted HIPPS Packages

Factory-acceptance-tested skids integrate sensors, logic solvers, and actuated valves into a single, pre-assembled unit, significantly reducing on-site commissioning time by 30% and lowering lifecycle costs by 15%. These skids are designed to streamline installation and ensure operational efficiency. Qatar’s North Field Expansion project is leveraging this technology by deploying identical HIPPS skids across eight LNG trains. This approach highlights the scalability and cost-effectiveness of plug-and-play modules, which simplify deployment while maintaining high safety and performance standards.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevenace | Impact Tiimeline |

|---|---|---|---|

| High Up-Front Engineering and Certification Costs | -1.4% | Global, particularly acute in cost-sensitive segments (food and beverages, metals and mining) | Short term (≤ 2 years) |

| Scarcity of SIL-Certified Professionals | -1.1% | Global, with pronounced shortages in Asia-Pacific and Africa | Medium term (2-4 years) |

| Complex Retrofit Challenges in Brownfield Plants | -0.8% | North America, Europe, Middle East legacy facilities | Medium term (2-4 years) |

| Cyber-Security Vulnerabilities in Connected Safety Systems | -0.7% | Global, heightened risk in digitally integrated facilities | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Up-Front Engineering and Certification Costs

Engineering a SIL3 High-Integrity Pressure Protection System for a mid-size petrochemical train can cost USD 1 million. These expenses typically cover extensive studies, third-party verification, and the preparation of detailed documentation, all of which are necessary before the hardware is even procured. For smaller operators, the financial burden increases further, as they often allocate an additional 10-15% of the project value to hire consultants. These consultants are essential for navigating the complex requirements outlined in IEC 61511 clauses, which govern the safety lifecycle of such systems. This additional expenditure significantly extends the payback periods for these projects, making the adoption of SIL3 HIPPS less appealing, particularly in industries outside high-hazard sectors where such systems are neither mandated nor critical.

Scarcity of SIL-Certified Professionals

Only one in three process-safety engineers carries recognized SIL credentials, and retirements are outpacing new certifications. This shortage has created a significant gap in the availability of skilled professionals, leading to increased reliance on external consultants. As a result, consulting fees have risen by more than 20% annually, further straining project budgets. Additionally, this shortage has introduced schedule risks, particularly for hydrogen and CCUS megaprojects, where each HIPPS loop must undergo independent validation to meet the stringent requirements of lenders and insurers. These challenges are compounding the complexity of implementing safety systems in high-stakes industries, emphasizing the need for strategic workforce planning and training initiatives.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Lifecycle Services Outpace Hardware Growth

The High Integrity Pressure Protection System market size for components retained a commanding share in 2025 with 63.28%, yet services are advancing at a faster pace. The revenue generated from components is primarily driven by sensor retrofits designed to resist hydrogen embrittlement and by logic-solver upgrades that comply with IEC 62443 cybersecurity standards. Large-scale LNG and deep-water projects are increasingly specifying triple-modular-redundant solvers rated SIL3, capable of maintaining 2-year proof-test intervals. This ensures the overall High Integrity Pressure Protection System market remains robust and resilient, even as technological advancements continue to evolve.

Lifecycle services, which include proof testing, SIL verification, and predictive-maintenance analytics, are projected to grow at a compound annual growth rate (CAGR) of 10.05%. The adoption of digital twins has become a key enabler, as these models simulate transient pressure scenarios, allowing operators to defer proof tests without compromising risk reduction. Additionally, third-party verification houses are stepping in to address competency gaps, particularly in the Asia-Pacific region, where demand for such expertise is rising. The rapid growth of services highlights a significant shift from capital expenditure to operating expenditure, as asset owners prioritize uptime, operational efficiency, and schedule reliability to meet the increasing demands of the market.

By End-User Industry: Hydrogen and CCUS Emerge as Fastest-Growing Niche

Oil and gas accounted for nearly half of 2025 revenue, at 46.27%, driven by reliance on SIL3 subsea HIPPS loops in deep-water tiebacks. These systems are critical for ensuring safety and operational efficiency in high-pressure environments. However, hydrogen pipelines and post-combustion capture units are projected to grow the fastest, contributing to a gradual shift in the overall High Integrity Pressure Protection System market share toward cleaner-energy verticals. This shift aligns with the global push for decarbonization and the adoption of sustainable energy solutions.

The chemicals sector continues to be a consistent adopter of HIPPS with 9.98% CAGR, supported by the expansion of polyolefin and aromatics projects in regions such as India and the Middle East. In the power generation sector, HIPPS are increasingly specified for combined-cycle drum protection, ensuring compliance with stringent safety standards. Meanwhile, industries such as metals, mining, food, and beverages remain slower adopters due to limited regulatory requirements and lower perceived risks. The diversification of industrial applications is driving vendors to enhance their product offerings by optimizing metallurgy and sealing compounds to handle hydrogen and supercritical CO₂.

By Installation Type: Offshore Accelerates on Subsea Complexity

Onshore facilities continue to dominate the High Integrity Pressure Protection System market, accounting for 58.41% of revenue, as refineries, petrochemical plants, and LNG trains require multiple HIPPS loops per unit to ensure operational safety and compliance. These systems are critical in managing pressure surges and preventing catastrophic failures in high-risk environments. However, offshore applications are growing faster, with a 10.15% CAGR as deep-water exploration and production increase. Subsea HIPPS systems are particularly advantageous in these settings, as they eliminate the need for topside relief valves, significantly reducing platform weight and minimizing greenhouse gas emissions during blowdown events.

Regions such as the ultra-deep Santos Basin, the North Sea, and West Africa are driving demand for advanced subsea HIPPS solutions. These regions require titanium-clad valves capable of withstanding pressures exceeding 10,000 psi while maintaining fail-safe operations in challenging seabed conditions, where temperatures can drop to approximately 4 °C. To meet these stringent requirements, suppliers are incorporating redundant electric-hydraulic actuators and black-channel data paths designed to remain operational even in the event of cable damage. These innovations enhance the reliability and safety of offshore systems, further solidifying their value proposition in the market.

By Pressure Rating: Demand Shifts Toward Ultra-High-Pressure Classes

The 3000-6000 psi tier accounted for 41.15% of 2025 revenue, driven by its widespread application in conventional refining processes and in intermediate-depth wells, which are critical components of the oil and gas industry. This pressure range is particularly favored for its compatibility with standard refining operations and its ability to handle moderate well depths effectively. However, installations exceeding 6000 psi are expected to experience the fastest compound annual growth rate (CAGR) with 9.98% as the industry shifts toward hydrogen transmission systems designed for 100 bar service and as offshore wells continue to push pressure limits to new extremes. These challenging conditions are driving significant investments in advanced materials, such as duplex and nickel alloys, which offer enhanced durability and resistance to high-pressure environments.[3]Global CCS Institute, “CCS Technologies 2025,” globalccsinstitute.com Additionally, these conditions are fostering research and development of fast-response piezoelectric sensors that withstand hydrogen permeation, ensuring reliable performance in demanding applications.

In contrast, lower-pressure classes below 3000 psi are projected to grow more slowly. This is primarily because industries such as food processing and utility gas grids face fewer stringent compliance requirements and tend to allocate budgets for incremental upgrades rather than undertaking complete system replacements. These sectors prioritize cost-effective solutions that meet their operational needs without necessitating significant capital expenditures, resulting in a more gradual adoption of new technologies within this pressure range.

Geography Analysis

North America captured the largest regional slice of the High Integrity Pressure Protection System market in 2025, supported by Gulf of Mexico ultra-deepwater drilling, a prolific LNG export build-out, and mature functional-safety enforcement. Operators rely on services to extend turnaround intervals, so proof-test and partial-stroke contracts are rising faster than hardware sales. The Middle East is projected to be the fastest riser, with a 9.91% CAGR, as Qatar’s North Field Expansion replicates modular LNG trains, Saudi downstream projects pursue petrochemical integration, and Abu Dhabi embarks on blue-ammonia complexes.

Factory-tested skids, bundled with integrated cyber-secure logic solvers, align with the region’s preference for compressed schedules and high-capacity modules. Europe maintains steady demand because IEC 61511 harmonization and EEMUA 222 guidelines have unified brownfield retrofit expectations across the North Sea, Germany, and the Mediterranean. Hydrogen backbone investments in Germany and the Netherlands, coupled with North Sea CCS clusters, ensure long-run momentum.

Asia-Pacific is highly fragmented: Japan and South Korea enforce strict SIL verification, India’s refineries are in mid-upgrade, and Southeast Asian LNG import terminals are driving near-term skid demand. China alone commands multiple hydrogen and CCUS pipelines that will each require hundreds of HIPPS loops. South America’s share hinges on Brazil’s pre-salt surge, while Africa is nascent but gathering attention as Nigeria and Angola consider new FPSOs.

Competitive Landscape

Five automation majors, ABB, Emerson, Siemens, Schneider Electric, and Yokogawa, bundle High Integrity Pressure Protection Systems Market into distributed-control-system suites, leveraging their extensive engineering toolchains and global service networks. These companies dominate the market by offering integrated solutions that streamline operations and enhance efficiency. However, their dominance is challenged by high-pressure valve specialists such as Mokveld, Severn, and HIMA, which have carved out niches in subsea and hydrogen applications due to their expertise in handling extreme conditions. Valmet’s USD 480 million acquisition of Severn in 2026 highlights the ongoing trend of market consolidation, aimed at combining advanced choke-valve metallurgy with cutting-edge flow-control analytics to deliver superior solutions.

Technology differentiation in the HIPPS market now focuses on several key areas. These include cyber-secure logic solvers certified to IEC 62443 standards, which ensure robust protection against cyber threats; digital-twin analytics that enable predictive maintenance by identifying trip set-point drift; and modular skids that are factory-tested to reduce installation and commissioning time. Emerson’s PACSystems RX3i CPS400 controller serves as a prime example of innovation in this space, as its pre-certified safety function blocks significantly reduce field engineering time.[4]Emerson, “New Emerson Safety Controller Streamlines Integration,” emerson.com This feature is particularly attractive to emerging-market LNG import terminals, where efficiency and reliability are critical.

The growing hydrogen and Carbon Capture, Utilization, and Storage (CCUS) markets are attracting new entrants specializing in advanced materials and ultra-high-pressure seal technologies. Smaller firms like ATV HIPPS and Mogas are gaining traction by offering rapid customization and establishing regional service hubs to meet localized demands. As the High Integrity Pressure Protection System market continues to expand into new energy sectors, vendors capable of certifying 1,000-bar valve assemblies and developing virtual-commissioning models are expected to gain a competitive edge over their rivals, positioning themselves as leaders in this evolving market.

High Integrity Pressure Protection System Industry Leaders

Emerson Electric Co.

Yokogawa Electric Corporation

Siemens AG

Schneider Electric SE

ABB Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Equinor awarded an EPC contract to SLB OneSubsea, tasking them with upgrading the Gullfaks subsea compression system using advanced modules designed to prolong the field's operational life.

- January 2026: Valmet finalized the USD 480 million acquisition of Severn, adding subsea choke-and-control-valve expertise.

- January 2026: Bharat Petroleum contracted Technip Energies for polypropylene, butene-1, and fluidized catalytic cracker projects in India valued at up to USD 536 million.

- January 2026: Utonomy secured its first deal with Delgaz Grid to retrofit intelligent pressure-control systems on Romanian gas networks.

Global High Integrity Pressure Protection System Market Report Scope

The High Integrity Pressure Protection System Market is the global industry focused on the development, deployment, and maintenance of safety instrumented systems designed to prevent overpressurization in industrial processes. HIPPS are critical safety solutions that automatically isolate pressure sources to protect equipment, personnel, and the environment, while reducing reliance on conventional relief systems such as flaring.

The High Integrity Pressure Protection System Market Report is Segmented by Offering (Components including Sensors, Logic Solvers, Valves and Actuators, and Services), End-User Industry (Oil and Gas, Chemicals, Power, Metal and Mining, Food and Beverages, and More), Installation Type (Onshore, and Offshore), Pressure Rating (Up to 3000 psi, 3000-6000 psi, and Above 6000 psi), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Components | Sensors |

| Logic Solvers | |

| Valves and Actuators | |

| Services |

| Oil and Gas |

| Chemicals |

| Power |

| Metal and Mining |

| Food and Beverages |

| Other Process Industries |

| Onshore |

| Offshore |

| Up to 3000 psi |

| 3000 – 6000 psi |

| Above 6000 psi |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia and New Zealand | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| Turkey | |

| Rest of Middle East | |

| Africa | Nigeria |

| South Africa | |

| Rest of Africa |

| By Offering | Components | Sensors |

| Logic Solvers | ||

| Valves and Actuators | ||

| Services | ||

| By End-User Industry | Oil and Gas | |

| Chemicals | ||

| Power | ||

| Metal and Mining | ||

| Food and Beverages | ||

| Other Process Industries | ||

| By Installation Type | Onshore | |

| Offshore | ||

| By Pressure Rating | Up to 3000 psi | |

| 3000 – 6000 psi | ||

| Above 6000 psi | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Qatar | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | Nigeria | |

| South Africa | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the forecast value of the High Integrity Pressure Protection System market by 2031?

The market is projected to reach USD 1.22 billion by 2031.

Which region is expected to grow the fastest over 2026-2031?

The Middle East is forecast to record a 9.91% CAGR due to LNG and petrochemical megaprojects.

Why are services outpacing component sales?

Operators favor proof-testing and predictive-maintenance contracts that extend uptime and defer capital expenditure, driving a 10.05% CAGR for services.

How are hydrogen projects influencing technology requirements?

Hydrogen pipelines operating up to 1000 bar require embrittlement-resistant valves and high-frequency sensors, expanding demand for ultra-high-pressure HIPPS designs.

What are the key challenges limiting wider adoption?

High engineering costs and a global shortage of SIL-certified professionals are restraining uptake, especially in cost-sensitive industries.

Which pressure class is expanding the fastest?

Systems rated above 6000 psi are expected to grow at 9.98% CAGR, propelled by deep-water and hydrogen applications.

Page last updated on: