Pressure Washer Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 5.74 Billion |

| Market Size (2031) | USD 7.37 Billion |

| Growth Rate (2026 - 2031) | 5.12% CAGR |

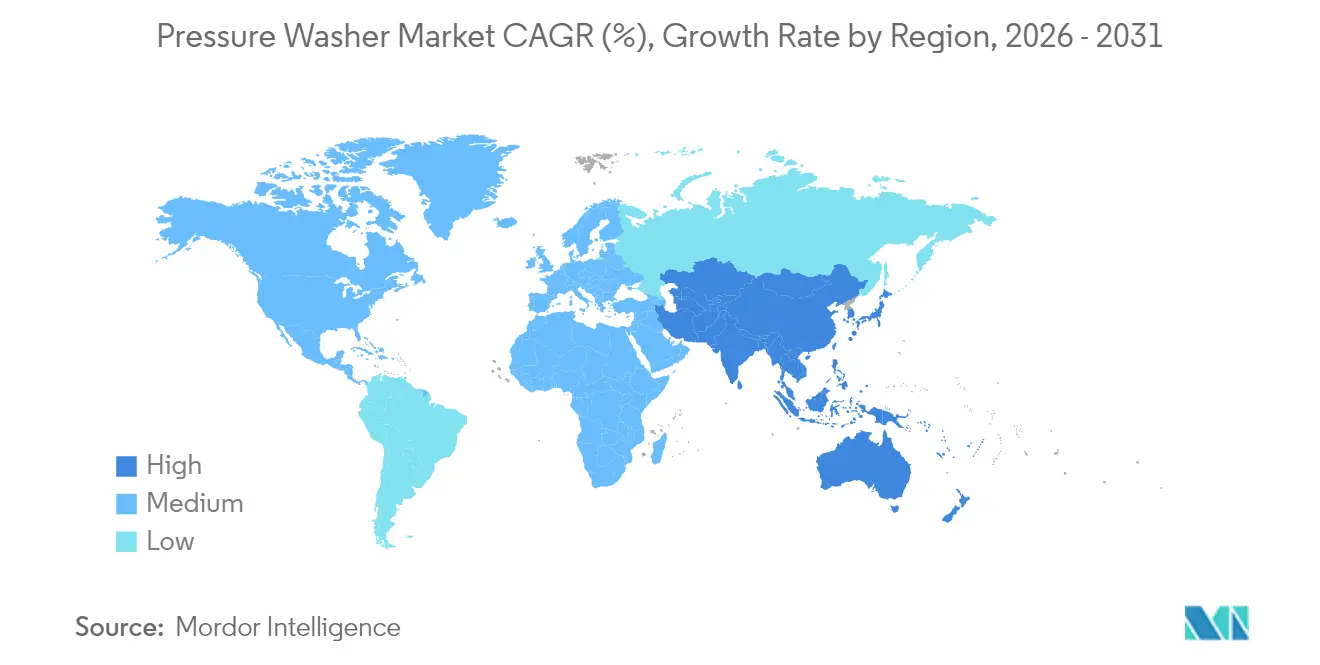

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

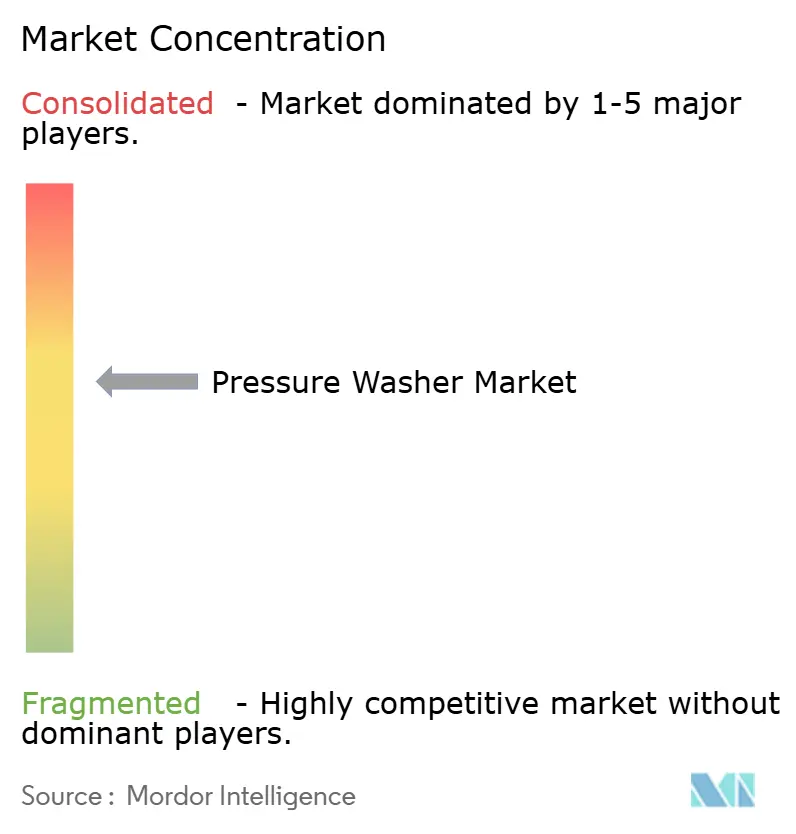

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Pressure Washer Market Analysis by Mordor Intelligence

The pressure washer market size was valued at USD 5.46 billion in 2025 and estimated to grow from USD 5.74 billion in 2026 to reach USD 7.37 billion by 2031, at a CAGR of 5.12% during the forecast period (2026-2031). Demand persisted as construction firms, professional cleaners, and households replaced aging units with models that conserve water and integrate digital controls. Battery-powered lines, holding 13.5% of global 2024 demand, re-shaped competitive strategy because they deliver portability without tail-pipe emissions. Asia-Pacific retained the revenue lead, while North America and Europe favored premium features such as app-linked trigger guns and reclaimed-water loops. E-commerce further democratized access, enabling first-time buyers to research specifications, compare bundles, and schedule doorstep delivery.

Key Report Takeaways

- By product type, mobile units held 61.35% of 2025 revenue; stationary systems are forecast to grow at a 6.18% CAGR to 2031.

- By power source, electric lines represented 47.60% of 2025 pressure washer market share, whereas battery models are projected to expand at a 12.85% CAGR through 2031.

- By component, water pumps accounted for 40.55% of 2025 revenue; smart nozzle assemblies are set to grow at an 8.55% CAGR to 2031.

- By water operation, cold-water units claimed 89.60% of the pressure washer market size in 2025; hot-water models will advance at a 9.45% CAGR.

- By output pressure, the 1,501–3,000 PSI band produced 45.70% of 2025 sales; units above 4,000 PSI are projected to rise at a 11.65% CAGR.

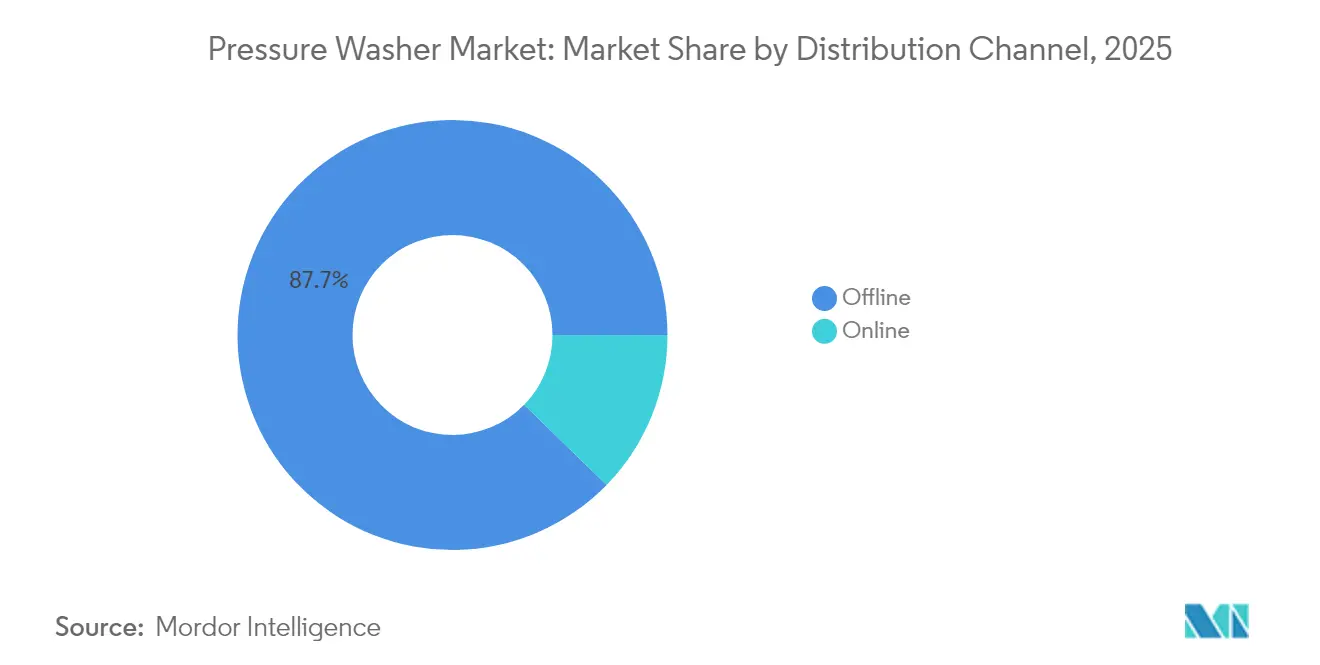

- By distribution, offline retail generated 87.72% of 2025 revenue, while online channels are heading for an 11.05% CAGR.

- By end-user, residential customers generated 56.40% of 2025 demand; professional contract cleaners should rise at a 8.84% CAGR to 2031.

- Regionally, Asia-Pacific led with 5.55% 2025 share, and North America is expected to post the fastest 2026-2031 CAGR at 5.65%.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Pressure Washer Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand from residential and commercial cleaning | +1.2% | North America and Europe strongest | Medium term (2-4 years) |

| Rising global construction activities | +0.9% | APAC core, spill-over to MEA and LATAM | Long term (≥4 years) |

| Expansion of professional car-wash chains | +0.7% | North America and EU, emerging APAC | Medium term (2-4 years) |

| Rapid e-commerce penetration in outdoor power equipment | +0.6% | Global, led by North America and Europe | Short term (≤2 years) |

| Emergence of cordless battery-powered portable washers | +0.8% | Early adoption in developed markets | Medium term (2-4 years) |

| Water-efficient high-pressure technologies | +0.5% | California, Australia, Southern Europe | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Growing demand from residential and commercial cleaning

Pandemic-era hygiene expectations persisted into 2025, accelerating purchases of mid-range electrics and contract-grade mobile rigs. Kärcher reported EUR 3.446 billion turnover for 2024, a 4.6% year-on-year gain that underscored rising volumes across its pressure washer lines. [1]Alfred Kärcher SE and Co. KG, “Financial Year 2024 Results,” kaercher.com Restaurateurs deployed 200 °F hot-water units to remove grease build-up, trimming manual scrubbing time by half. Homeowners in suburban corridors invested in compact 1,800–2,000 PSI tools that protect siding and decks, boosting unit turnover in DIY channels. Commercial property managers used scheduled façade washing to reinforce brand image, translating cleanliness standards into measurable foot-traffic gains. These multi-segment increases fed directly into the pressure washer market’s mid-term expansion prospects.

Rising global construction activities

Komatsu’s construction division posted JPY 3,798.2 billion (USD 26.13 billion) revenue in FY 2024, signalling sustained site activity. Builders specified trailer-mounted washers to clear formwork, mud, and adhesive overspray, while rental houses bulk-ordered stationary pump banks to meet cyclical upticks. Mining operators adopted 1,000 PSI dual-gun bays to demuck haul trucks, pushing average reservoir capacity above 500 gallons. These industrial use-cases lengthened run-time requirements, steering component suppliers toward hardened plungers and ceramic seals. The resulting equipment rotation preserved a resilient demand layer for the pressure washer market well beyond residential peaks.

Expansion of professional car-wash chains

Chain operators scaled express tunnels that recycle 70-90% of process water, satisfying local discharge mandates while enhancing throughput. Industry data show automated bays use 8–70 gallons per vehicle versus 100+ gallons for driveway washing. Equipment makers delivered corrosion-resistant pumps and PLC-controlled arches to withstand 20-hour shifts. Turtle Wax Pro cited multi-store operators upgrading to touch-less arches at record pace during 2024. This chain rollout created predictable service parts revenue and propelled higher-pressure spec adoption, lifting the pressure washer market trajectory inside the automotive service vertical.

Rapid e-commerce penetration in outdoor power equipment

Online platforms captured 11.7% of global 2024 volume as retailers curated detailed comparison hubs. Home Depot’s web catalog allowed shoppers to filter by PSI, flow, and decibel ratings, compressing purchase cycles. [2]Home Depot, “Pressure Washers Catalog,” homedepot.com Direct-to-consumer landing pages offered un-boxed demonstrations, subscription detergent bundles, and priority warranty registration. Brands leveraged clickstream analytics to refine SKU counts and accessory mix, reinforcing cross-sell opportunities. Electric and battery categories benefited most because freight class restrictions on gasoline engines did not apply. The logistics efficiencies reduced landed cost, broadening consumer access and deepening the pressure washer market footprint.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Availability of alternative cleaning technologies | −0.4% | Greater impact in industrial niches | Medium term (2-4 years) |

| Stringent water-usage and discharge regulations | −0.6% | California, Australia, Middle East | Long term (≥4 years) |

| Advent of autonomous robotic surface cleaners | −0.3% | High-labor-cost economies | Long term (≥4 years) |

| Price volatility of synthetic-rubber hoses | −0.2% | Global supply chain | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Availability of alternative cleaning technologies

Factories processing sensitive alloys migrated part-cleaning from high-pressure water to ultrasonic cavitation baths that reach tight crevices without blast abrasion. Utilities tested drone-borne sprayers capable of 40-foot vertical reach, halving tower maintenance time and eliminating fall-protection overhead. Food processors championed dry-ice blasting to sidestep wastewater handling, diverting some capex away from hot-water rigs. Although these technologies served narrower niches, they trimmed replacement cycles for premium washers in high-spec facilities, dampening potential lifts in the pressure washer market.

Stringent water-usage and discharge regulations

The US EPA classifies wash effluent as process wastewater when it contacts oil or debris, obligating contractors to obtain NPDES permits. WSSC Water issued best-practice guidelines requiring on-site capture and pre-treatment before sewer discharge in Maryland jurisdictions. [3]WSSC Water, “Best Management Practices for Pressure Washing,” wsscwater.com California drought levies further restricted outdoor washing windows, forcing operators to add reclaim tanks or recycle modules that raise upfront cost. Some small fleets deferred upgrades, creating local plateaus within the pressure washer market despite national growth averages.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Mobile Units Drive Market Flexibility

Mobile rigs captured 61.35% of worldwide revenue in 2025. Their wheeled frames, quick-disconnect hose reels, and integrated detergent tanks equip crews to tackle parking lots at dawn and amusement rides by noon. Service firms exploit this portability to schedule dense route stacks, yielding attractive revenue-per-asset ratios. Conversely, stationary pump stations, though representing a smaller slice, are projected for a 6.18% CAGR because tunnel car-washes, distribution centers, and fabrication lines prefer centralized pumping to cut downtime. Hot-dip-galvanized skids with auto-shutdown features extend pump life past 3,000 hours, reinforcing ROI logic.

In 2025, mobile product designers prioritized molded-poly housings and fold-flat handles to reduce curb weight by 15%. Cloud-connected usage counters feed maintenance dashboards, letting renters bill by trigger-time instead of calendar days, an innovation widening yield spreads within the pressure washer market. Fixed installations added VFD drives that ramp motors smoothly, protecting seals and slashing energy peaks during shift start-ups. By dovetailing these design iterations with end-user workflows, manufacturers enhanced lifetime economics for both formats, underpinning recurring parts and service sales.

By Power Source: Battery Technology Revolutionizes Portability

Electric cords still dominated commercial kitchens and light-duty retail storefronts where silent operation and zero fumes mattered. Gasoline engines remained indispensable on construction acreage and farmland, yet their share is projected to narrow by 2031 as lithium-ion energy density crosses 350 Wh/kg. Battery models already claimed 13.20% of 2025 global shipments and are expected to post the fastest CAGR among all segments. DiBO’s 2024 release featured 90-minute fast charging and dual spray modes, alleviating runtime hesitation.

Fleet managers calculate payback not solely on fuel savings but also on crew setup times: cordless frames roll straight from van to jobsite without refueling or spark-arrester checks. Municipal buyers earmark grants for zero-emission landscape tools, further tilting bid specs. Nonetheless, 4,000 PSI+ ratings still require petro engines or three-phase electric hookups, so multi-fuel catalogs remain crucial for OEM coverage across the pressure washer market.

By Component: Smart Nozzles Lead Innovation Wave

Water pumps represented the largest revenue driver because every specification cascade—PSI, flow rate, duty cycle—stems from pump architecture. Yet smart nozzles grew the fastest at 8.55% CAGR through 2031. Kärcher’s LCD-trigger guns display pressure and detergent mix in real time, reducing user error on painted surfaces. Briggs and Stratton’s POWERflow+ pump delivered a high-flow, low-pressure rinse without swapping tips, appealing to detailers who feared etching clear-coat.

Hose suppliers faced styrene-butadiene rubber volatility; some substituted thermoplastic elastomers, extending bend radius while slimming wall thickness. Quick-change upstream filters caught grit before it mauled ceramic plungers, driving aftermarket accessory revenue. Integrated sensor blocks now tee to Bluetooth dongles, forwarding vibration and temperature signatures to predictive-maintenance dashboards. These digital add-ons elevate ASPs, giving component innovators an outsized influence on margin structure inside the pressure washer market.

By Water Operation: Hot-Water Systems Serve Specialized Applications

Cold-water models met 89.60% of 2025 needs because most soils surrender under 2,000 PSI streams plus surfactant. Yet units with diesel or electric boilers accelerated grease breakup and pathogen kill, achieving a 9.45% CAGR. Landa restaurant packages reached 200 °F at 4 GPM, cutting fry-hood downtime. Food processors also valued hot-water sanitation because steam-in-place grids cannot reach conveyor undersides.

Cold-water OEMs answered with higher flow rates and rotary nozzle kits that mimic scalding impact without burners, catering to buyers nervous about fuel surcharges. Boiler manufacturers compressed coil footprints, shaving 18% off frame length so rigs could fit cargo elevators. Taken together, divergent application priorities ensured both hot and cold lines advanced in parallel, keeping SKU breadth wide and stimulating cross-selling inside the pressure washer market.

By Output Pressure: High-Pressure Segment Targets Professional Applications

The 1,501–3,000 PSI bracket produced 45.70% of 2025 sales because it balances cleaning punch with surface safety. Gearbox-driven 4,000–5,000 PSI units gained traction among concrete contractors and shipyards, yielding a 11.65% CAGR forecast. Hustler’s 4,400 PSI gasoline frame delivered 4 GPM, giving painters flash-rust-free steel in one pass. Sub-1,500 PSI electrics served the RV and soft-wash niche, avoiding vinyl wrap damage.

Ultra-high-pressure rigs (>10,000 PSI) remained rare, leased mostly for refinery outage work. OEMs widened ceramic plunger choices to resist cavitation at elevated pressures. Safety regulators pushed for dual-trigger handles and whip-check lanyards, hiking compliance costs but also raising barrier-to-entry for low-quality imports. This bifurcated ladder created stepping stones for contractors to scale up gradually, locking them into brand ecosystems across the pressure washer market.

By Distribution Channel: Online Sales Transform Market Access

Brick-and-mortar outlets still grabbed 87.72% of 2025 revenue thanks to demo areas and instant pickup. Yet web stores delivered double-digit gains as shoppers leveraged unfiltered reviews and next-day freight. Dealer networks protected relevance by bundling free startup training and priority repair lanes for equipment bought in-store. Manufacturers ran “ship-to-store” programs that funnel online orders through local dealers, preserving territorial integrity while capturing data visibility. The hybrid loop amplifies customer lifetime value, ensuring neither channel cannibalizes the other but rather broadens the pressure washer market surface area.

By End-User: Professional Contract Cleaners Drive Service Demand

Residential owners generated 56.40% of 2025 units, using weekend warrior electrics to spruce up patios and vehicles. Yet contract cleaners booked a 8.84% CAGR because businesses offloaded non-core chores. Trailer skids costing USD 23,000 offered 300-gallon tanks, reclaim vacuums, and toolboxes, letting crews chase commercial plazas dawn to dusk. Hospitals and logistics depots, wary of slip lawsuits, outsourced walkway flush cycles, specifying minimum 3,000 PSI at 4 GPM.

Industry newcomers financed rigs through 60-month loans bundled with maintenance contracts, giving OEMs a second revenue pass at filter, oil, and nozzle consumables. Meanwhile, in-house industrial teams stuck with high-horsepower diesel carts to de-ice conveyors and purge paint booths. Catering to these divergent duty cycles obliges manufacturers to maintain broad feature sets and invest in modular platform architectures, sustaining diversity inside the pressure washer market.

Geography Analysis

Asia-Pacific kept its lead with 5.55% of global 2025 sales and posted a matching 5.55% CAGR outlook. Chinese infrastructure megaprojects required job-site de-mud cleaning, while India’s Smart Cities program invested in street-wash fleets. Japanese buyers paid premiums for ultra-quiet pumps to satisfy dense urban ordinances. Kärcher opened a Vietnam cloud-linked plant in 2024 to slash lead-times and localize voltage configurations. These moves entrenched the brand and buoyed the wider pressure washer market in the region.

North America ranked second in value and is forecast to clock the fastest continental growth at 5.65% CAGR from 2026–2031. DIY culture, high disposable income, and the spread of express car-wash chains created steady throughput. California drought fines pressured operators to adopt 80% reclaim loops, steering demand to systems with onboard filtration. Nilfisk’s Q1 2025 report revealed US revenue stress from tariff turbulence, but its Consumer unit still climbed 12.9%. This illustrates how product-mix agility offsets regional shocks inside the pressure washer market.

Europe charted mid-single-digit expansion as Eco-Design rules pushed energy-efficient motors and condensing boilers. Southern Europe’s water scarcity spurred interest in on-gun auto-shut valves. Eastern trucking corridors renovated fueling depots and mandated bi-weekly pad washing, lifting mid-pressure diesel frame orders. The region’s preference for repairability over replacement yielded strong aftermarket parts turnover, shoring up EBITDA margins for distributors.

Latin America logged moderate 4% gains, propelled by Brazil’s agro-exporters who flushed packing sheds each shift. Currency risk curtailed premium imports, but lease-to-own schemes eased sticker shock. Middle East and Africa recorded similar trends; Gulf desalination plants required salt-resistant housings, while South African mines leased 5,000 PSI skids for dragline clean-downs. Collectively, regional variegation provided hedges that cushioned the global pressure washer market against localized downturns.

Competitive Landscape

The top five brands accounted for an estimated 48% of 2025 turnover, establishing a moderate-concentration sector. Kärcher dedicated EUR 200 million (USD 230.49 million) to AI-enabled autonomous scrubbers and recycled-plastic casings. Nilfisk initiated a strategic review of its US high-pressure washer line after 2024 revenue ebbed, signaling possible divestiture. [4]Nilfisk A/S, “Interim Report Q1 2025,” nilfisk.com Briggs and Stratton leveraged its POWERflow+ patent to embed dual-mode pumps in OEM private-label deals, defending share in the North American pressure washer market.

Mid-tier challengers targeted lithium-ion R&D. DiBO’s all-battery range added 5-year warranties to dispel cycle-life anxiety. Component supplier Gates expanded its hose catalog to over 130 countries while sustaining USD 847.6 million Q1 2025 sales. Drone-cleaning start-ups secured venture funding, but their narrow use-case kept substitution risk contained. Sustainability claims intensified: Kärcher used 2,200 tonnes of recycled plastic in 2024 products and set a 21% Scope 1-and-2 reduction target by 2025. These green metrics increasingly influence municipal procurement, adding a reputational axis to the pressure washer market contest.

Value-chain integration deepened as pump, hose, and nozzle makers partnered on “system-rated” kits that guarantee performance, mitigating warranty conflicts. Service apps relayed hour-meter logs to dealers, automatically queuing oil-change visits and locking customers into supply ecosystems. Such stickiness lifted lifetime value per unit even as headline ASPs moderated. Overall, innovation cadence, channel data capture, and carbon credentials defined the new competitive perimeter.

Pressure Washer Industry Leaders

Alfred Kärcher SE & Co. KG

Nilfisk A/S

Briggs & Stratton LLC

FNA Group

Bosch Power Tools (GmbH)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Nilfisk posted Q1 2025 revenue of EUR 256.5 million; Consumer and Specialty advanced 12.9% and 11.7% respectively, while Americas dipped 17.7%.

- April 2025: Gates Industrial reported Q1 2025 net sales of USD 847.6 million and maintained full-year growth guidance.

- February 2025: Nilfisk announced 2024 revenue of EUR 1,027.9 million USD 1183.49 million and began a review of its US high-pressure washer business.

- January 2025: Kärcher published its Sustainability Report 2024, reporting 2,200 tonnes of recycled plastics used and a 21% Scope 1-2 cut target versus 2020 baselines.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the pressure washer market as the sale of brand-new, purpose-built machines that propel water at pressures above 700 psi using an electric motor, gasoline engine, or battery pack, together with core components such as the pump, hose, spray gun, and interchangeable nozzles.

Scope Exclusion: Rental services, aftermarket parts, and detergents sit outside the present sizing.

Segmentation Overview

- By Product Type

- Mobile

- Stationary

- By Power Source

- Electric

- Gasoline

- Battery / Cordless

- By Component

- Water Pump

- Electric Motor / Gas Engine

- High-Pressure Hose

- Nozzle and Spray Gun

- By Water Operation

- Cold-Water

- Hot-Water

- By Output Pressure

- Up to 1,500 PSI

- 1,501-3,000 PSI

- 3,001-4,000 PSI

- Above 4,000 PSI

- By Distribution Channel

- Online (DTC and Marketplaces)

- Offline (DIY Stores, Specialty OPE Dealers)

- By End-User

- Residential

- Commercial and Industrial

- Professional Contract Cleaners

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- South Korea

- India

- Southeast Asia

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Rest of Africa

- Middle East

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed equipment makers, component suppliers, facility managers, and specialist cleaning contractors across North America, Europe, and Asia Pacific. These discussions tested price bands, typical duty cycles, and emerging battery adoption rates, giving us first-hand insight that desk sources alone could not deliver.

Desk Research

We began by mapping global production and trade under HS 8424, reviewing shipment statistics on the UN Comtrade portal, U.S. Census Bureau manufacturing shipments, and Eurostat PRODCOM tables. Industry groups such as the International Carwash Association and ISSA provided usage benchmarks, while safety advisories from the U.S. EPA and OSHA guided regulatory context. Paid datasets, notably D&B Hoovers for company revenue splits and Dow Jones Factiva for press activity, helped us anchor supplier footprints. This list is illustrative; many additional open datasets and journals were referenced during validation.

Market-Sizing & Forecasting

We applied a top-down production-plus-trade reconstruction, which was then cross-checked through sampled average selling price times unit volumes collected from key brands and channels. Where shipment gaps appeared, regional import values were redistributed using primary interview ratios. Key variables fed into the model include new housing completions, global car-wash outlet counts, non-residential floor area additions, construction spending, and outdoor power equipment retail indices. A multivariate regression tying these drivers to historical sales generated the 2025-2030 forecast, while scenario analysis adjusted for currency swings and raw-material cost shocks.

Data Validation & Update Cycle

Outputs pass three layers of analyst review, variance thresholds trigger re-checks with interviewees, and models refresh every twelve months, with interim revisions after material events.

Why Our Pressure Washer Baseline Earns Strong Credibility

Published estimates often differ because each firm frames the market, conversion factors, and refresh cadence in its own way.

Key gap drivers include whether replacement demand is counted, how offline and online channels are weighted, the currency year used for historical data, and the depth of primary validation. Mordor's baseline, reported in constant 2025 dollars, integrates both residential and professional demand and is updated annually, which limits scope drift.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 5.46 B (2025) | Mordor Intelligence | |

| USD 3.06 B (2024) | Global Consultancy A | Omits replacement units and online sales |

| USD 2.22 B (2024) | Trade Journal B | Relies only on historical shipments, limited primary checks |

| USD 3.22 B (2024) | Industry Association C | Focuses on stationary industrial systems, excludes DIY segment |

The comparison shows that when scope is narrowly drawn or primary interviews are light, totals skew lower or higher. By combining clearly stated boundaries with disciplined variable selection, Mordor Intelligence delivers a balanced, transparent baseline that decision-makers can trust.

Key Questions Answered in the Report

What is the current pressure washer market size in 2026?

The pressure washer market size reached USD 5.74 billion in 2026 and is forecast to grow to USD 7.37 billion by 2031.

Which product type dominates global sales?

Mobile units led the pressure washer market with 61.35% revenue share in 2025 thanks to their versatility and lower infrastructure needs.

How fast are battery-powered pressure washers growing?

Battery models held 13.20% of 2025 demand and are projected to expand at a 12.85% CAGR through 2031, the fastest among all power sources.

Which region is expanding the quickest?

North America is expected to post the highest regional CAGR of 5.65% between 2026 and 2031, driven by robust replacement demand and e-commerce penetration.

What regulations affect pressure washer operations?

Operators in the United States must comply with EPA NPDES discharge rules, while local bodies such as WSSC Water mandate on-site wastewater reclamation in sensitive watersheds.

Who are the major market players?

Key brands include Kärcher, Nilfisk, Briggs and Stratton, DiBO, and Gates, collectively accounting for about 48% of global revenue.

Page last updated on: