Industrial Control Systems Security Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

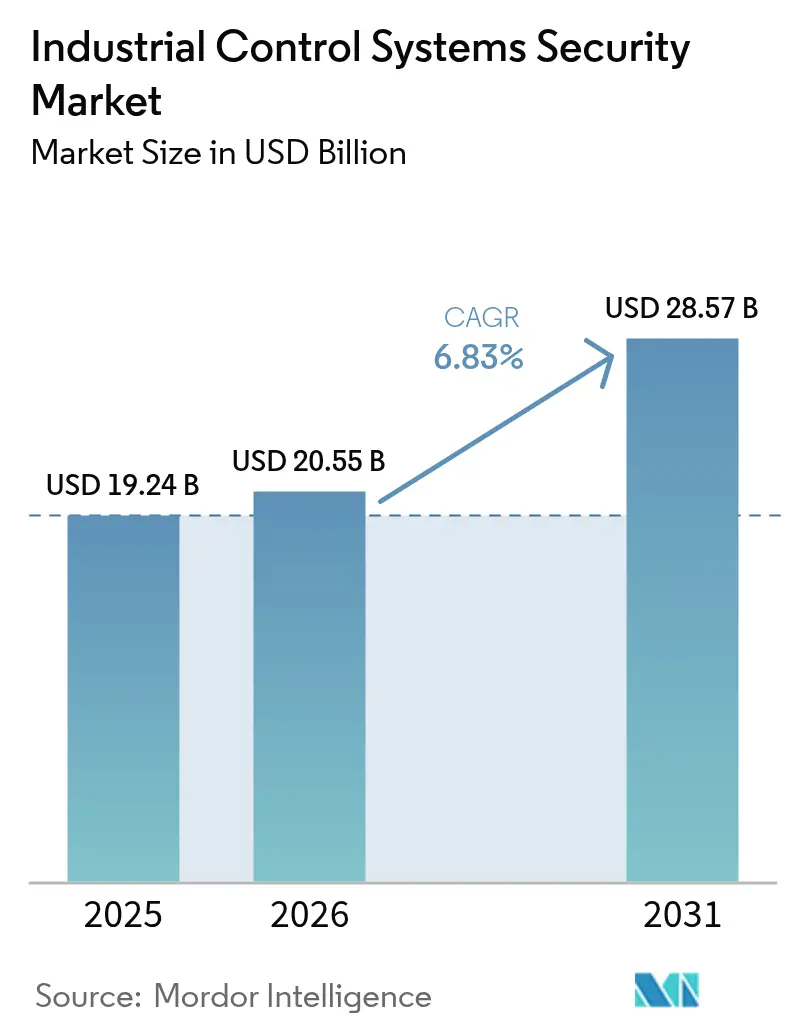

| Market Size (2026) | USD 20.55 Billion |

| Market Size (2031) | USD 28.57 Billion |

| Growth Rate (2026 - 2031) | 6.83% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

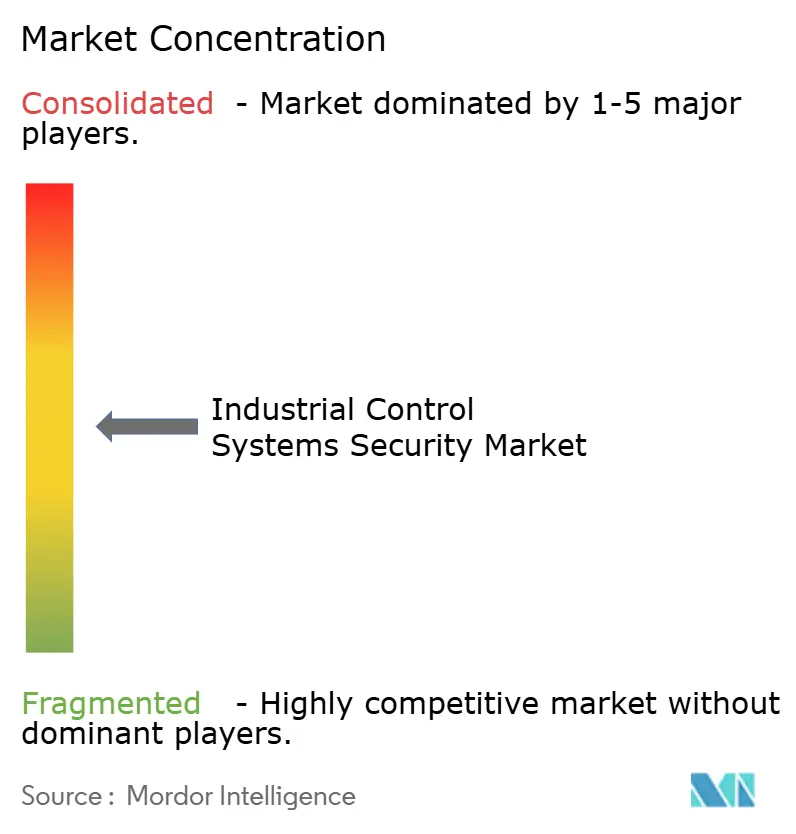

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Industrial Control Systems Security Market Analysis by Mordor Intelligence

The industrial control systems security market size is expected to increase from USD 19.22 billion in 2025 to USD 20.55 billion in 2026 and reach USD 28.37 billion by 2031, growing at a CAGR of 6.66% over 2026-2031. A surge in mandatory supply-chain audits under NERC CIP-013 and EU NIS2 is reshaping procurement priorities, compelling operators to replace compliance check-box approaches with real-time risk management. Ransomware groups have professionalized, with 80 identified crews now focusing on critical infrastructure, which is steering budgets toward behavioral analytics and zero-trust segmentation. Convergence of information technology and operational technology is creating new attack surfaces across discrete manufacturing, ports and smart grids, intensifying demand for asset visibility and secure remote access. Vendors with deep operational technology expertise are gaining ground because point-and-click security tools designed for enterprise networks cannot accommodate deterministic control loops and safety constraints.

Key Report Takeaways

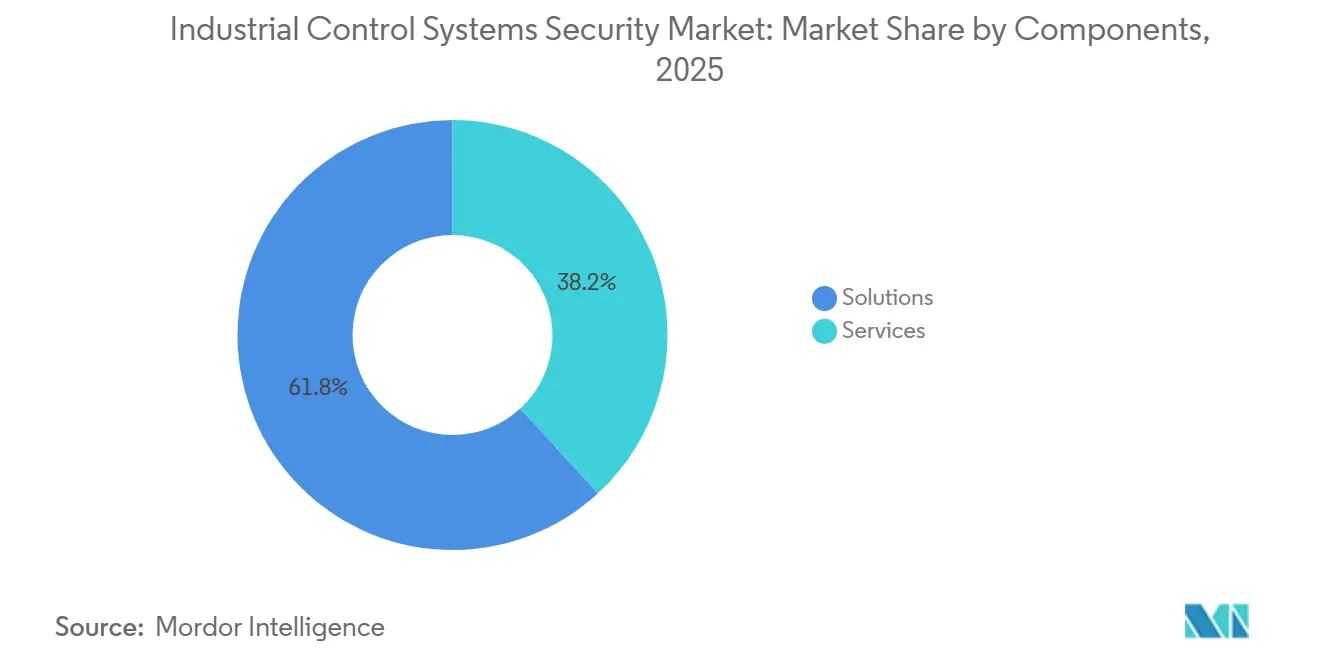

- By component, solutions held 61.83% of the industrial control systems security market share in 2025, while services are advancing at a 6.95% CAGR through 2031.

- By security type, network security led with 37.71% share in 2025 and application security is projected to post a 7.22% CAGR to 2031.

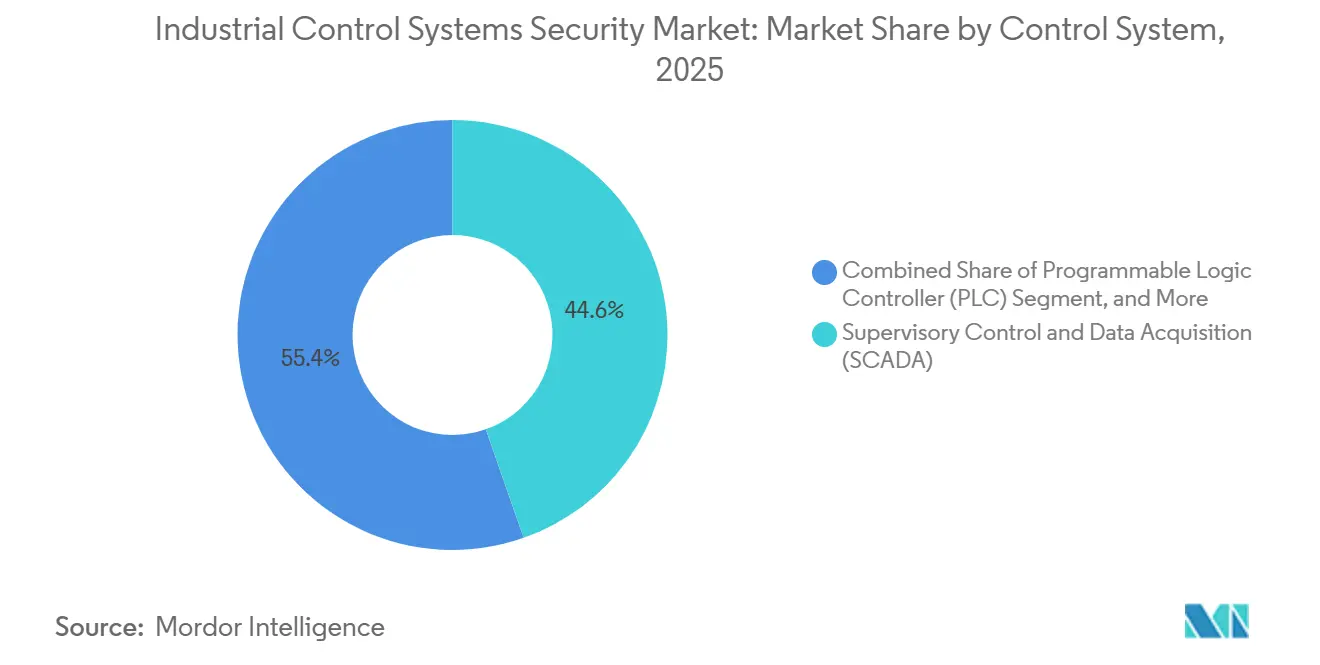

- By control system type, supervisory control and data acquisition platforms accounted for 44.62% of 2025 revenue, whereas programmable logic controller protection is expanding at a 7.54% CAGR.

- By end-user industry, power and utilities commanded a 28.91% share in 2025, and transportation and logistics are forecast to register the fastest 7.67% CAGR.

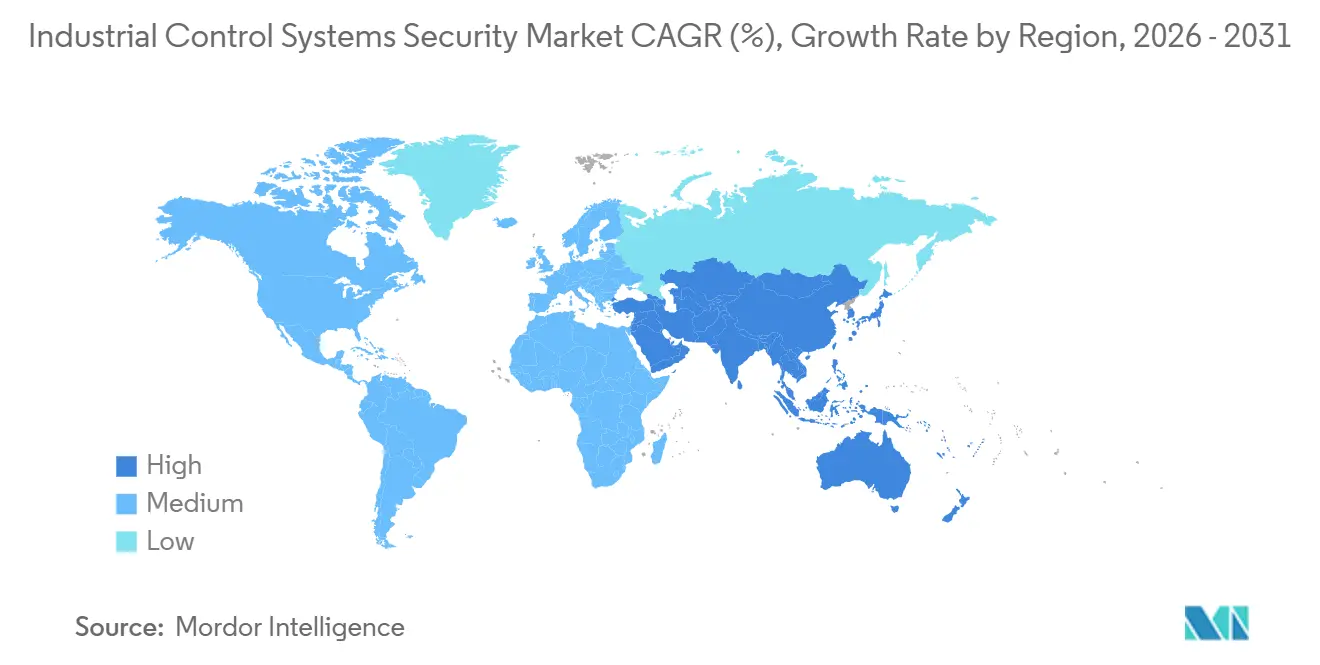

- By geography, North America captured 36.74% of global revenue in 2025, yet Asia Pacific is projected to grow at a 8.07% CAGR over the forecast window.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Industrial Control Systems Security Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating IIoT-Driven OT Connectivity in Discrete Manufacturing | +1.2% | Asia Pacific manufacturing hubs, North American automotive corridors | Medium term (2-4 years) |

| Mandatory NERC CIP-013 and EU NIS2 Compliance for Critical Infrastructure Operators | +1.5% | North America and European Union | Short term (≤ 2 years) |

| Surge in Ransomware Attacks on Oil and Gas Pipelines | +1.1% | North America, Europe, Middle East | Short term (≤ 2 years) |

| Edge-AI-Enabled Anomaly Detection for Real-Time Threat Response | +0.9% | North America, Europe, expanding Asia Pacific | Medium term (2-4 years) |

| Rapid Adoption of Zero-Trust Architectures in Industrial Networks | +1.0% | Global, led by North America and Europe | Medium term (2-4 years) |

| Digital-Twin-Based Pen-Testing of Legacy SCADA/DCS Assets | +0.7% | North America and Europe, emerging Asia Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Mandatory NERC CIP-013 and EU NIS2 Compliance for Critical Infrastructure Operators

New regulatory enforcement is compressing multi-year security roadmaps into tight funding cycles. Bulk electric system entities must now validate vendor risk programs, renegotiate contracts, and maintain continuous monitoring, which is driving sustained investment in supply-chain governance tools and unidirectional gateways. Boards are increasingly approving operational technology allocations because NIS2 imposes executive liability and fines up to EUR 10 million (USD 10.8 million). Vendors that can demonstrate IEC 62443 alignment are winning competitive tenders across power grids, water utilities, and transportation operators.

Surge in Ransomware Attacks on Oil and Gas Pipelines

Attackers have shifted to dual-extortion playbooks that encrypt billing servers while threatening to leak process data, forcing operators to shut down pipelines even when supervisory control and data acquisition assets remain intact.[1]U.S. Department of Justice, “Colonial Pipeline Ransomware Investigation,” Justice.gov Sophos recorded an 80% year-on-year rise in 2025 incidents in the energy sector, prompting operators to accelerate zero-trust segmentation and anomaly detection on engineering workstations.[2]Sophos, “State of Ransomware in Critical Infrastructure 2025,” Sophos.com The democratization of ransomware-as-a-service means smaller groups now mimic nation-state tactics, elevating baseline security requirements for regional pipeline firms.

Accelerating IIoT-Driven OT Connectivity in Discrete Manufacturing

Seventy-two percent of factories have installed Industrial Internet of Things sensors on at least half their production lines, yet only 38% segment operational technology traffic, exposing programmable logic controllers to ransomware propagation. Rising cyber-insurance premiums and exclusions for operational technology incidents are nudging mid-size electronics and automotive plants toward managed detection and response contracts. Asia Pacific manufacturers are compressing a decade of U.S. and European convergence experience into three-year projects, magnifying the urgency for ready-made security blueprints.

Rapid Adoption of Zero-Trust Architectures in Industrial Networks

Utilities and water authorities are piloting microsegmentation to contain lateral movement following a spate of remote desktop compromises in 2024. Applying zero trust to legacy protocols such as Modbus requires overlay gateways and identity brokers that add latency, so operators are rolling out phased programs, starting with remote vendor access. Budget justification rests on alignment with both NERC and NIS2, making zero trust a compliance and resilience imperative.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Retrofit Costs and Downtime for Legacy PLCs | -0.8% | North America and Europe, emerging Asia Pacific | Medium term (2-4 years) |

| OT-Skilled Cyber-Talent Shortage in Mid-Size Manufacturers | -0.6% | North America, Europe, expanding Asia Pacific | Long term (≥ 4 years) |

| Limited Interoperability of Proprietary Industrial Protocols | -0.4% | Multi-vendor environments worldwide | Long term (≥ 4 years) |

| Budget Re-Prioritization Amid Volatile Energy Prices | -0.5% | Global oil and gas and energy-intensive industries | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Retrofit Costs and Downtime for Legacy PLCs

Many programmable logic controllers from the 1990s lack memory for encryption or secure boot, yet replacement can exceed USD 50,000 per unit and requires planned outages that utilities schedule only once a year.[3]Rockwell Automation, “Legacy PLC Security Retrofit Guide,” RockwellAutomation.com Mid-size plants cannot absorb week-long shutdowns, so operators default to perimeter firewalls, which do not mitigate endpoint vulnerabilities. The cost hurdle is prolonging exposure windows and dampening near-term market expansion.

OT-Skilled Cyber-Talent Shortage in Mid-Size Manufacturers

The median hiring time for operational technology security analysts now exceeds 140 days, and salary premiums are widening versus traditional information technology roles. Plants unable to staff 24/7 coverage purchase managed detection but must still grant remote access, raising new supply-chain risks. Cross-training initiatives improve internal capacity but divert engineers from production optimization, reinforcing reliance on external service providers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Gain as Complexity Outpaces Internal Capabilities

Solutions retained a 61.83% share of the industrial control systems security market size in 2025, confirming the primacy of firewalls, intrusion prevention systems and security information and event management platforms inside substations and refineries. Services, however, are projected to expand faster at a 6.95% CAGR, because regulators now require documented gap assessments, penetration tests and continual monitoring that most operators cannot deliver in-house. Consultancy teams certified in IEC 62443 are leading large-scale remediation projects for board-mandated compliance timelines, and multi-year managed detection and response contracts are replacing ad-hoc site audits.

This momentum reflects a growing recognition that security is an operating expense scoped around threat evolution rather than a capital purchase timed to hardware refresh cycles. Industrial enterprises increasingly demand outcome-based service-level agreements covering mean-time-to-detect and false-positive thresholds, pushing vendors toward subscription models with integrated threat intelligence updates. The shift is especially visible in Asia Pacific, where greenfield smart factories bundle security services into initial automation budgets to avoid the legacy technical debt faced by North American plants.

By Security Type: Application Security Accelerates as Attackers Pivot to Engineering Workstations

Network controls accounted for 37.71% of 2025 revenue, mirroring decades of focus on boundary defense between corporate and operational domains. Yet application security is registering the fastest 7.22% CAGR, as ransomware crews now target human-machine interface binaries and engineering workstation software running on general-purpose operating systems. The industrial control systems security market is expanding as insurers mandate proof of secure coding practices and virtual patching for supervisory control and data acquisition (SCADA) systems and related databases and configuration tools.

Deep packet inspection remains foundational for anomaly detection, but operators are layering code-signing validation, runtime integrity checks, and whitelisting to protect custom supervisory control and data acquisition applications. Vendors that can integrate vulnerability scoring with functional safety metrics are gaining traction, as a patch window misaligned with batch processing cycles can trigger costly downtime. Cloud-delivered application firewalls tuned for operational technology traffic patterns are emerging to protect remote engineering access, underscoring the convergence of information technology and operational technology security stacks within a single DevSecOps workflow.

By Control System Type: PLC Security Surges with Manufacturing Digitalization

Supervisory control and data acquisition platforms still represent 44.62% of installed assets because utilities require wide-area visibility for grids, pipelines, and water networks. Nevertheless, programmable logic controller protection is on track for a 7.54% CAGR as discrete manufacturing plants link thousands of controllers to enterprise resource planning and Industrial Internet of Things analytics. Integrating lightweight endpoint detection agents into real-time operating systems without impairing cycle-time determinism is becoming a competitive differentiator for security vendors.

The industrial control systems security market share for distributed control systems in refining and chemical complexes remains stable, yet spending is tilting toward integrated safety-security modules to meet IEC 61511 and IEC 62443 audit requirements. Safety instrumented system controllers and building automation nodes, once overlooked, now figure prominently in threat modeling because adversaries can weaponize sensor tampering to force production shutdowns. Consequently, operators prioritize protocol-agnostic deep packet inspection engines capable of flagging anomalous commands across Profinet, EtherNet/IP, and OPC-UA within single dashboards.

By End-User Industry: Transportation and Logistics Emerges as Fastest-Growing Vertical

Power and utilities accounted for 28.91% of global 2025 spending, aligned with stringent oversight in North America and Europe. Ports, rail systems, and freight hubs, however, are driving the highest 7.67% CAGR as autonomous cranes, trackside sensors, and fleet telematics introduce operational technology vulnerabilities that attackers can exploit to disrupt supply chains. Insurance carriers now price maritime cyber cover based on real-time patch status of terminal operating systems, accelerating procurement of managed vulnerability assessment services.

Oil and gas, chemicals, and pharmaceuticals maintain steady allocations, yet budget emphasis is shifting from installation to optimization of detection rules and response playbooks. Food and beverage processors, operating on thin margins, remain underinvested relative to their exposure, but a series of 2025 ransomware incidents that halted bottling plants has triggered board-level reviews. Mining firms with satellite-connected remote operations are piloting secure enclave architectures to shield supervisory control and data acquisition links from spoofing attacks, a move that may lift spending above present baselines as commodity prices stabilize.

Geography Analysis

North America led the industrial control systems security market, accounting for 36.74% of 2025 revenue, driven by U.S. federal mandates, including Transportation Security Administration directives for pipelines, that compel near-term investment in continuous monitoring and incident response. Utilities allocate a growing share of capital to managed detection contracts that deliver North American Electric Reliability Corporation audit artifacts out of the box, and energy producers now include ransomware tabletop exercises in supplier qualification scorecards. Service providers headquartered in the United States also enjoy proximity advantages that shorten deployment cycles and support quick-response retainers during incident peaks.

Europe is undergoing a compliance-driven procurement wave following the transposition of NIS2 by all 27 member states in October 2024, which expanded the number of regulated entities from 2,000 to more than 160,000. German machinery builders and French grid operators are re-architecting perimeter-only defenses toward zero-trust micro-segments, while midsize Spanish water utilities are pooling budgets for shared security operations centers. Industrial automation vendors with IEC 62443-certified components are preferred because engineering houses want to avoid the expense of recertification once systems are live. The industrial control systems security market share attributable to Central and Eastern Europe is poised to rise as regional utilities fast-track grid modernization using European Union recovery funds.

Asia Pacific registers the highest 8.07% CAGR, underpinned by China’s Made-in-China 2025 mandate, India’s Production-Linked Incentive schemes and South Korea’s Smart Factory initiative, each embedding cybersecurity prerequisites into automation subsidies. Greenfield sites across Vietnam, Thailand and Indonesia adopt secure-by-design principles, deploying role-based access, network segmentation and anomaly detection from day one, which spares them the expensive retrofits now challenging Western peers. Japan focuses on virtual patching for supervisory control and data acquisition life-extension projects, whereas Australian mining consortia prioritize secure satellite backhauls for autonomous haulage systems across the outback.

Competitive Landscape

The top ten vendors, including Honeywell International, Cisco Systems, Palo Alto Networks, Fortinet, and Siemens, captured a considerable share of 2025 revenue, leaving a small revenue share distributed among over 100 regional systems integrators, niche protocol specialists, and managed detection providers. Information technology security giants are embedding industrial protocol parsers into enterprise firewalls to upsell existing accounts, while analysts pursuing acquisitions pursue bolt-on deals to plug operational technology skill gaps. For example, Siemens’ minority stake in Claroty integrates deep asset discovery into its Xcelerator platform, strengthening its bid for end-to-end factory digital twins.

Pure-play operational technology defenders differentiate through purpose-built anomaly detection trained on gigabytes of industrial protocol telemetry, claiming superior context versus repurposed information technology tools. Dragos, Nozomi Networks and Claroty now offer tiered managed detection services that include forensics and incident retainer clauses, thereby creating multi-year switching costs. At the same time, industrial automation originals such as Schneider Electric and Rockwell Automation embed Fortinet and Palo Alto Networks technology into control-system firmware, signaling a co-opetition model where hardware incumbents provide delivery channels for security software in exchange for revenue sharing.

White-space exists in food and beverage processing, small hydro and municipal water, where average cybersecurity spend remains below 1% of information technology budgets. Private-equity funds are actively scouting sub-USD 100 million revenue targets with recurring software subscriptions and sticky professional services, anticipating that consolidation will unlock cross-sell synergies and bolster data-lake scale for machine-learning engines. Vendors early to insurance-broker partnerships may capture incremental demand as underwriters stipulate approved security stacks for policy eligibility, an emerging sales conduit particularly effective among mid-size manufacturers.

Industrial Control Systems Security Industry Leaders

IBM Corporation

Cisco Systems Inc.

Fortinet, Inc.

Honeywell International Inc.

ABB Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Siemens AG acquired a minority stake in Claroty Ltd. to embed asset visibility and vulnerability management into the Siemens Xcelerator ecosystem.

- January 2026: Palo Alto Networks Inc. introduced Cortex XSIAM for Industrial Control Systems with deep packet inspection for Modbus, DNP3 and OPC UA.

- December 2025: Honeywell International Inc. closed its USD 200 million purchase of South Korea-based Nextnine, adding 24/7 security operations center capacity to Honeywell Forge.

- November 2025: Dragos Inc. raised USD 200 million in Series E funding led by Koch Disruptive Technologies, lifting valuation to USD 2.3 billion.

Global Industrial Control Systems Security Market Report Scope

Industrial control systems (ICS) security includes securing and safekeeping industrial control systems and the software and hardware used by the system. It focuses on keeping processes and machinery running smoothly. The offered solutions include integrated hardware and software packaged to control and monitor the operation of machinery and associated devices operating in industrial environments.

The Industrial Control Systems Security Market Report is Segmented by Component (Solutions including Firewall and IPS, Identity and Access Management, Antivirus and Antimalware, Security and Vulnerability Management, Data Loss Prevention and Recovery, Other Solutions; Services including Consulting and Assessment, Integration and Deployment, Support and Maintenance, Managed Security Services), Security Type (Network Security, Endpoint Security, Application Security, Database Security, Cloud/Remote Access Security), Control System Type (Supervisory Control and Data Acquisition, Distributed Control System, Programmable Logic Controller, Other Control Systems), End-User Industry (Automotive, Chemical and Petrochemical, Power and Utilities, Oil and Gas, Food and Beverage, Pharmaceuticals, Water and Wastewater, Mining and Metals, Transportation and Logistics, Other Industries), and Geography (North America, Europe, South America, Asia Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Solutions | Firewall and IPS |

| Identity and Access Management | |

| Antivirus and Antimalware | |

| Security and Vulnerability Management | |

| Data Loss Prevention and Recovery | |

| Other Solutions | |

| Services | Consulting and Assessment |

| Integration and Deployment | |

| Support and Maintenance | |

| Managed Security Services |

| Network Security |

| Endpoint Security |

| Application Security |

| Database Security |

| Cloud/Remote Access Security |

| Supervisory Control and Data Acquisition (SCADA) |

| Distributed Control System (DCS) |

| Programmable Logic Controller (PLC) |

| Other Control Systems |

| Automotive |

| Chemical and Petrochemical |

| Power and Utilities |

| Oil and Gas |

| Food and Beverage |

| Pharmaceuticals |

| Water and Wastewater |

| Mining and Metals |

| Transportation and Logistics |

| Other Industries |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia and New Zealand | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa |

| By Component | Solutions | Firewall and IPS |

| Identity and Access Management | ||

| Antivirus and Antimalware | ||

| Security and Vulnerability Management | ||

| Data Loss Prevention and Recovery | ||

| Other Solutions | ||

| Services | Consulting and Assessment | |

| Integration and Deployment | ||

| Support and Maintenance | ||

| Managed Security Services | ||

| By Security Type | Network Security | |

| Endpoint Security | ||

| Application Security | ||

| Database Security | ||

| Cloud/Remote Access Security | ||

| By Control System Type | Supervisory Control and Data Acquisition (SCADA) | |

| Distributed Control System (DCS) | ||

| Programmable Logic Controller (PLC) | ||

| Other Control Systems | ||

| By End-User Industry | Automotive | |

| Chemical and Petrochemical | ||

| Power and Utilities | ||

| Oil and Gas | ||

| Food and Beverage | ||

| Pharmaceuticals | ||

| Water and Wastewater | ||

| Mining and Metals | ||

| Transportation and Logistics | ||

| Other Industries | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the projected value of the industrial control systems security market by 2031?

The market is forecast to reach USD 28.37 billion by 2031, reflecting a 6.66% CAGR over 2026-2031.

Which component segment is growing fastest?

Services, covering consulting, integration and managed detection, are expanding at a 6.95% CAGR through 2031.

Why is application security gaining momentum in operational technology environments?

Attackers are shifting toward exploiting unpatched human-machine interface and engineering software, lifting application security demand at a 7.22% CAGR.

Which region is expected to deliver the highest growth rate?

Asia Pacific is projected to grow at a 8.07% CAGR thanks to embedded cybersecurity mandates within regional automation policies.

What regulatory frameworks most influence purchasing decisions?

NERC CIP-013 in North America and the EU NIS2 directive in Europe are the primary drivers of board-level cybersecurity investment in critical infrastructure.

Page last updated on: