Ayurvedic Toothpaste Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

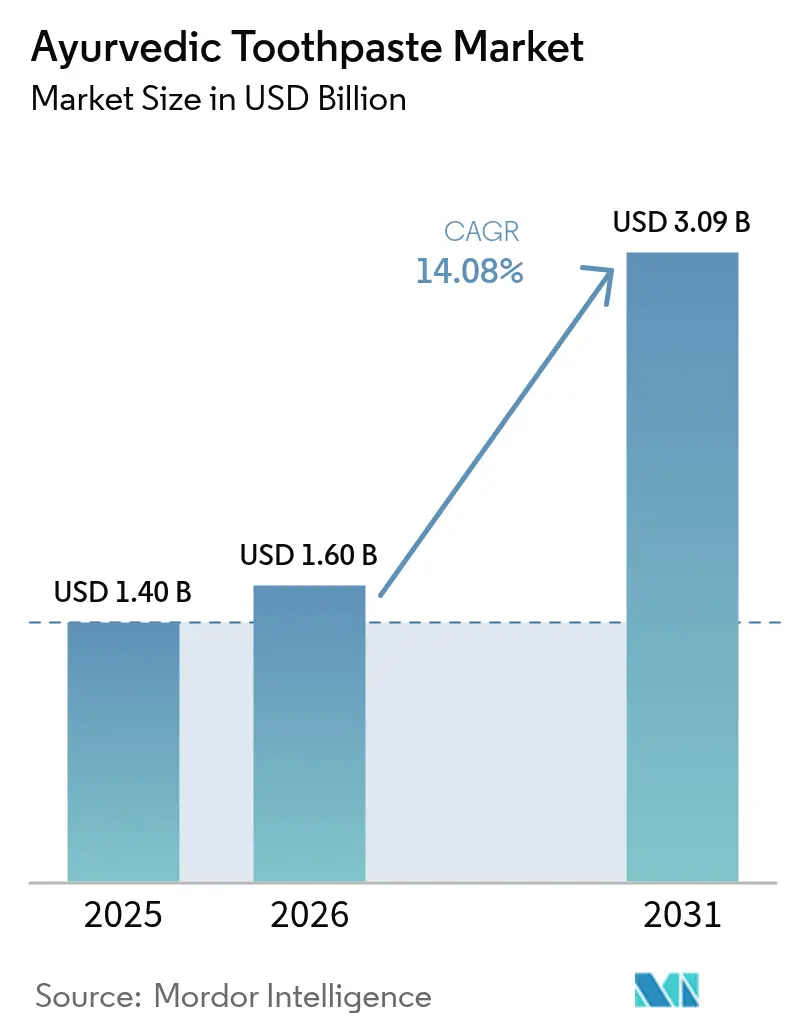

| Market Size (2026) | USD 1.6 Billion |

| Market Size (2031) | USD 3.09 Billion |

| Growth Rate (2026 - 2031) | 14.08% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Ayurvedic Toothpaste Market Analysis by Mordor Intelligence

The Ayurvedic Toothpaste market size is expected to grow from USD 1.40 billion in 2025 to USD 1.6 billion in 2026 and is forecast to reach USD 3.09 billion by 2031 at 14.08% CAGR over 2026-2031. This robust growth trajectory reflects a fundamental shift in consumer preferences toward traditional Indian medicine-based oral care solutions, driven by mounting concerns over synthetic chemicals and increasing acceptance of Ayurvedic principles in mainstream healthcare. The World Health Organization reports that 3.5 billion people globally are affected by oral diseases, creating substantial demand for effective yet gentle oral care alternatives rooted in ancient wisdom [1]Source: World Health Organization, "Oral Health", who.int. Consumer behavior studies from India demonstrate this transition, with 49.79% of respondents shifting from non-herbal to herbal toothpaste formulations, with Ayurvedic variants leading this transformation. Intensified branding, clinical trials that validate neem, miswak, turmeric and amla, and sustainability commitments such as recyclable HDPE tubes further accelerate category penetration. Asia-Pacific dominates the market, positioning the region as both the largest consumer base and fastest-growing segment with a 15.89% CAGR through 2030. This regional concentration stems from deep-rooted Ayurvedic traditions and government backing through India's AYUSH ministry, which has established international cooperation frameworks and allocated significant resources to promote Ayurvedic medicine systems globally [2]Source: Government of India AYUSH, "Ayurvedic medicine" ayush.gov.in. Overall, the market is poised to grow by a CAGR of 14.29% from 2025-2030 driven by growing consumer inclination towards natural and traditional toothpastes.

Key Report Takeaways

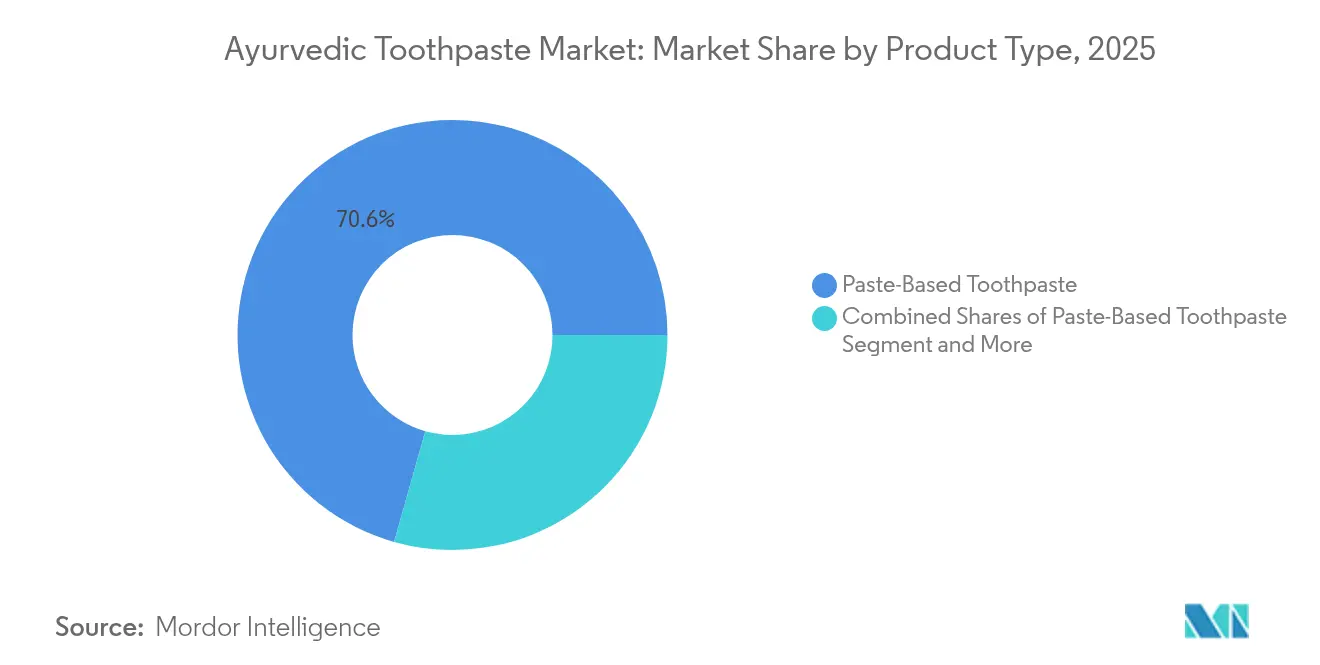

- By product type, paste-based formulations accounted for 70.62% share of the ayurvedic toothpaste market size in 2025 and are advancing at a 14.22% CAGR through 2031.

- By price-tier, mass-market variants held 73.45% of the ayurvedic toothpaste market share in 2025, while the premium segment is projected to expand at 16.1% CAGR to 2031.

- By packaging, conventional tubes captured 94.05% share in 2025; jars are forecast to post the highest 15.05% CAGR through 2031.

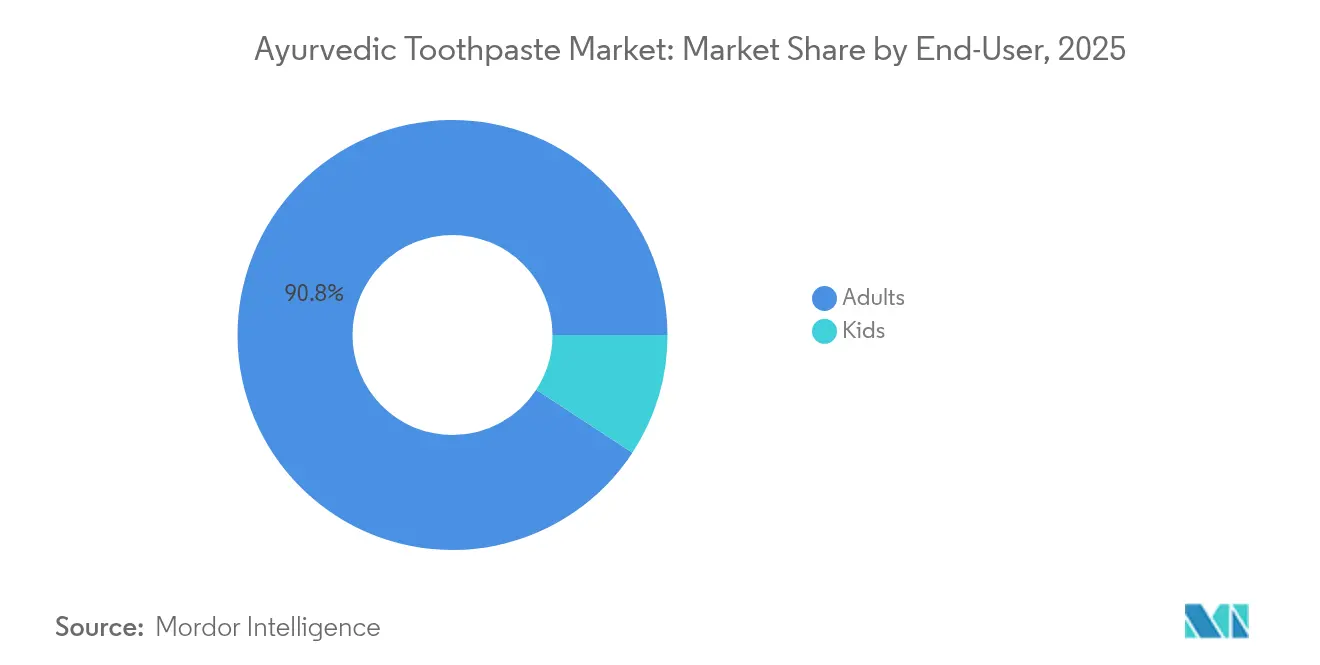

- By end-user, adults dominated with 90.78% revenue share in 2025, whereas children’s products are set to grow the fastest at 16.08% CAGR up to 2031.

- By distribution channel, convenience and grocery stores led with 43.01% contribution in 2025; online retail is predicted to grow at a 15.21% CAGR to 2031.

- By geography, Asia-Pacific commanded 82.44% of the ayurvedic toothpaste market in 2025 and is projected to maintain the highest 15.43% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Ayurvedic Toothpaste Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Preference for Natural Oral Care Products | +3.2% | Global, with strongest impact in Asia-Pacific and North America | Medium term (2-4 years) |

| Increasing Dental Disease Prevention Awareness | +2.8% | Global, particularly emerging markets with growing healthcare access | Long term (≥ 4 years) |

| Government Support for Traditional Medicine Systems | +2.1% | Asia-Pacific core, spill-over to Europe and North America | Long term (≥ 4 years) |

| Intense Brand Marketing and Promotions | +1.9% | Global, with emphasis on developed markets | Short term (≤ 2 years) |

| Growing Sustainability and Ethical Sourcing Focus | +1.7% | North America & EU, expanding to Asia-Pacific | Medium term (2-4 years) |

| Expansion of Online and Supermarket Channels | +1.5% | Global, led by North America and Asia-Pacific | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Preference for Natural Oral Care Products

Consumer preference for Ayurvedic ingredients has reached a tipping point, with over 70% of new toothpaste launches now featuring 'natural' positioning, with Ayurvedic formulations leading this transformation. This shift extends beyond marketing rhetoric to substantive formulation changes, as manufacturers replace synthetic chemicals with traditional Ayurvedic ingredients like neem, miswak, turmeric, and amla. Clinical evidence increasingly supports these Ayurvedic ingredients, with peer-reviewed studies demonstrating that formulations containing neem and propolis achieve plaque reduction comparable to chlorhexidine while producing fewer adverse effects. The trend particularly resonates with health-conscious consumers seeking authentic traditional medicine solutions over conventional alternatives. Companies responding to this demand are experiencing accelerated market penetration, with ayurvedic toothpastes now representing a siginificant share of India's overall oral care market.

Increasing Dental Disease Prevention Awareness

Global health initiatives have elevated oral health awareness to unprecedented levels, creating substantial market expansion opportunities for preventive care products based on traditional Ayurvedic principles. The WHO's comprehensive country profiles reveal that oral diseases affect 3.5 billion people worldwide, with untreated dental caries being the most common health condition globally. This awareness translates into increased consumer willingness to invest in premium oral care solutions, particularly those offering natural antimicrobial properties through time-tested Ayurvedic ingredients. Government health agencies increasingly recognize the connection between oral health and systemic conditions, driving public health campaigns that emphasize prevention over treatment. The economic burden of dental diseases, estimated at hundreds of billions annually in treatment costs, has prompted healthcare systems to explore traditional medicine alternatives. This macro-level awareness creates sustained demand for ayurvedic toothpastes that offer both therapeutic benefits and preventive protection through centuries-old formulation wisdom.

Government Support for Traditional Medicine Systems

Policy frameworks supporting Ayurvedic medicine have created institutional backing for ayurvedic oral care products across multiple jurisdictions. India's AYUSH ministry has established comprehensive international cooperation agreements and allocated substantial budget increases to promote Ayurvedic medicine globally, directly benefiting ayurvedic toothpaste manufacturers. The ministry's initiatives include research funding for clinical validation of traditional formulations, standardization protocols for Ayurvedic ingredients, and international market development programs. Similar recognition frameworks in Sri Lanka and Malaysia have integrated traditional medicine into national healthcare systems, creating regulatory pathways for Ayurvedic oral care products. The European Medicines Agency's recognition of traditional herbal medicines under specific regulatory frameworks provides market access for standardized Ayurvedic formulations. These government initiatives extend beyond domestic markets through bilateral cooperation agreements, enabling ayurvedic toothpaste companies to leverage official endorsements for international expansion while maintaining authenticity and traditional formulation integrity.

Intense Brand Marketing and Promotions

Marketing investment intensity has reached new heights as companies compete for consumer attention in the expanding Ayurvedic oral care segment. Colgate-Palmolive increased advertising expenditure to 13.6% of sales, up 30 basis points year-over-year, demonstrating the strategic importance of brand building in this competitive landscape. Digital marketing strategies increasingly target health-conscious consumers through educational content about traditional Ayurvedic ingredients and their historical applications in oral health. Companies are investing heavily in influencer partnerships and social media campaigns that emphasize ingredient authenticity and Ayurvedic heritage validation. The marketing arms race particularly intensifies around product launches, with companies allocating substantial budgets to establish new Ayurvedic variants in consumer consciousness through traditional medicine storytelling. This promotional intensity accelerates market growth by expanding consumer awareness and trial rates, though it also increases customer acquisition costs and pressures profit margins for smaller players lacking marketing scale.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Strong Competition From Synthetic Toothpaste | -2.3% | Global, particularly in developed markets with established brands | Medium term (2-4 years) |

| Regulatory and Compliance Challenges | -1.8% | Global, with varying intensity by jurisdiction | Long term (≥ 4 years) |

| Unpleasant Taste Limits Consumer Acceptance | -1.4% | Global, with cultural variations in taste preferences | Short term (≤ 2 years) |

| Low Awareness in Emerging Markets | -1.1% | Emerging markets in Africa, Latin America, and parts of Asia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Strong Competition From Synthetic Toothpaste

Established synthetic toothpaste brands maintain formidable competitive advantages through decades of consumer habit formation and extensive clinical validation. Colgate-Palmolive's market share demonstrates the entrenched position of conventional formulations, supported by massive distribution networks and marketing budgets. Synthetic toothpastes benefit from standardized manufacturing processes that ensure consistent quality and efficacy, while Ayurvedic alternatives face formulation challenges related to ingredient variability and seasonal availability of traditional herbs. Consumer switching costs remain significant, as established oral care routines create psychological barriers to adopting Ayurvedic alternatives. The competitive intensity has prompted some major brands to retreat from Ayurvedic positioning, with Colgate strategically shifting away from Ayurvedic positioning back to science-based product communication in certain markets. Price competition from synthetic alternatives limits premium pricing opportunities for Ayurvedic brands, particularly in price-sensitive market segments where mass-market synthetic options offer compelling value propositions despite lacking traditional medicine benefits.

Regulatory and Compliance Challenges

Regulatory complexity creates substantial barriers for ayurvedic toothpaste manufacturers navigating diverse global compliance requirements for traditional medicine products. China's new toothpaste regulations, effective December 2023, require comprehensive safety assessments and efficacy documentation for traditional ingredients, with new Ayurvedic components subject to 3-year monitoring periods[3]Source: National Medical Products Administration, "Provisions for Toothpaste Regulation", english.nmpa.gov.cn. The European Union's 2025 cosmetic regulations introduce multiple ingredient restrictions and nanomaterial bans that could affect traditional Ayurvedic formulations, requiring extensive reformulation and testing investments. FDA oversight of oral care products as cosmetics creates additional compliance burdens for companies seeking US market access, particularly regarding traditional medicine efficacy claims and ingredient safety documentation. Regulatory divergence across jurisdictions multiplies compliance costs and creates market entry delays, disproportionately affecting smaller Ayurvedic specialists lacking regulatory expertise. The evolving regulatory landscape requires continuous monitoring and adaptation, creating ongoing operational complexity that constrains rapid international market expansion for traditional medicine-based products.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Paste Formulations Dominate Ayurvedic Innovation

Paste-based toothpaste commands 70.62% market share in 2025 while simultaneously representing the fastest-growing segment at 14.22% CAGR through 2031, reflecting both consumer familiarity and successful integration of traditional Ayurvedic ingredients into conventional formats. This dual leadership position stems from manufacturers' ability to incorporate diverse Ayurvedic herbs like neem, babool, miswak, and turmeric into paste formulations while maintaining the sensory experience consumers expect from modern toothpastes. Gel-based alternatives serve niche consumer preferences for lighter textures and enhanced flavor delivery of traditional ingredients, particularly appealing to younger demographics seeking differentiated Ayurvedic experiences. The "Others" category, encompassing traditional powder and tablet formats, represents authentic Ayurvedic delivery methods gaining traction among purists seeking original formulation approaches.

Clinical research supports paste formulations' efficacy advantages, with studies demonstrating that Ayurvedic paste toothpastes containing bamboo salt and traditional herbs achieve significant antibacterial effects in controlled trials. Traditional powder formats face adoption challenges related to usage convenience and foaming expectations, though authenticity benefits create growth opportunities among consumers seeking pure Ayurvedic experiences. Manufacturing economies of scale favor paste formulations, enabling competitive pricing while supporting extensive Ayurvedic ingredient inclusion. The format's versatility allows for specialized variants targeting specific oral health concerns through traditional Ayurvedic principles, from sensitivity management using clove oil to whitening applications through turmeric and activated charcoal combinations.

By Price-Tier: Premium Positioning Reflects Ayurvedic Authenticity

Mass-market products maintain 73.45% market share in 2025, yet premium segments demonstrate superior growth dynamics at 16.1% CAGR, indicating consumer willingness to invest in authentic Ayurvedic formulations and traditional ingredient sourcing. This pricing bifurcation reflects market maturation, where established Ayurvedic brands command premium positioning through ingredient authenticity, traditional sourcing practices, and clinical validation of ancient formulations. Premium segments benefit from higher profit margins that support continued research into traditional medicine applications and marketing expenditure emphasizing Ayurvedic heritage. The price gap enables premium brands to incorporate expensive traditional extracts like saffron, gold bhasma, and rare medicinal plants that justify higher retail prices through authentic Ayurvedic positioning.

Consumer research indicates that premium ayurvedic toothpaste purchasers prioritize ingredient authenticity and traditional formulation methods over price considerations, creating relatively inelastic demand patterns. Mass-market segments face intense price competition and margin pressure, driving consolidation among smaller players lacking economies of scale for authentic ingredient sourcing. The premium segment's growth trajectory suggests successful brand building and consumer education efforts that establish ayurvedic toothpastes as legitimate alternatives to conventional premium oral care products. Distribution channel partnerships with Ayurvedic specialty stores and wellness retailers support premium positioning by providing expert recommendation opportunities and enhanced product credibility through traditional medicine context.

By Packaging Type: Traditional Meets Modern Sustainability

Traditional tube packaging maintains overwhelming 94.05% market share in 2025, reflecting consumer familiarity and manufacturing efficiency advantages that support mass-market distribution of Ayurvedic formulations. However, jar packaging emerges as the fastest-growing format at 15.05% CAGR, driven by sustainability initiatives and premium positioning strategies that align with Ayurvedic principles of environmental harmony and natural living. Jar packaging enables reduced plastic usage and enhanced recyclability, aligning with environmental consciousness trends that particularly resonate with Ayurvedic consumers seeking holistic lifestyle approaches. The format also supports premium brand positioning through enhanced shelf presence and perceived product quality that reflects traditional Ayurvedic medicine packaging heritage.

Sustainable packaging innovation represents a critical competitive battleground, with companies like Colgate investing over 5 years to develop recyclable HDPE tubes that maintain product integrity while supporting environmental goals aligned with Ayurvedic sustainability principles. Sachet packaging serves emerging market penetration strategies by reducing purchase barriers and enabling trial among price-sensitive consumers interested in Ayurvedic benefits. Manufacturing complexity and cost considerations favor tube formats for mass production, while jar packaging supports artisanal positioning and ingredient visibility that enhances premium Ayurvedic brand storytelling. The packaging evolution reflects broader sustainability trends that align with traditional Ayurvedic values of environmental stewardship and natural resource conservation.

By End-User: Adult Focus With Growing Pediatric Ayurvedic Acceptance

Adult consumers represent 90.78% market share in 2025, reflecting ayurvedic toothpastes' positioning as sophisticated oral care solutions targeting health-conscious mature consumers familiar with traditional medicine benefits. Yet the children's segment demonstrates the highest growth potential at 16.08% CAGR, driven by parental concerns about fluoride ingestion risks and preference for gentler, natural Ayurvedic formulations for developing oral health needs. Pediatric Ayurvedic toothpastes address specific safety concerns while incorporating traditional ingredients like fennel and cardamom for appealing flavors that encourage proper oral hygiene habits. The segment benefits from premium pricing opportunities as parents prioritize child safety and natural ingredients over cost considerations.

Product development for children requires specialized formulation approaches that balance traditional Ayurvedic efficacy with safety, often incorporating milder herbs and enhanced flavor profiles using traditional spices and natural sweeteners. Companies like Edinora have developed edible toothpaste formulations specifically targeting pediatric safety concerns, claiming safety even if accidentally swallowed through traditional ingredient selection. Adult segment growth remains robust due to increasing health consciousness and traditional medicine acceptance among mature consumers seeking authentic Ayurvedic alternatives to synthetic oral care products. The demographic split creates opportunities for targeted marketing strategies and specialized product development that address distinct user needs while maintaining authentic Ayurvedic formulation principles across age groups.

By Distribution Channel: Digital Platforms Enable Ayurvedic Education

Convenience and grocery stores maintain the largest 43.01% market share in 2025, leveraging extensive geographic coverage and impulse purchase opportunities that support ayurvedic toothpaste accessibility across diverse consumer segments. However, online retail emerges as the fastest-growing channel at 15.21% CAGR, reflecting fundamental shifts in consumer shopping behavior and the critical importance of product education for traditional medicine products. Digital channels enable direct-to-consumer relationships that support brand building and customer education about Ayurvedic ingredients, their traditional applications, and historical significance in oral health. Online platforms also facilitate niche product discovery and detailed ingredient information that benefits authentic Ayurvedic formulations requiring consumer education.

Supermarkets and hypermarkets provide essential mass-market distribution capabilities while pharmacies offer professional recommendation opportunities that enhance ayurvedic toothpaste credibility through healthcare professional endorsement. The channel mix evolution reflects changing consumer preferences for convenience and detailed product information access, with digital platforms offering comprehensive ingredient disclosure and customer reviews that support informed purchase decisions about traditional medicine products. Amazon's strategic focus on oral care within its everyday essentials portfolio demonstrates major e-commerce platforms' commitment to category expansion. Traditional retail channels maintain advantages in immediate product availability and sensory evaluation opportunities, while digital channels excel in Ayurvedic education and specialized variant availability that serves consumers seeking authentic traditional medicine experiences.

Geography Analysis

Asia-Pacific dominates the global ayurvedic toothpaste landscape with 82.44% market share in 2025 and leads growth projections at 15.43% CAGR through 2031, reflecting deep cultural integration of Ayurvedic medicine systems and government policy support for traditional healthcare products. India represents the region's primary growth engine, where ayurvedic toothpastes have captured a significant share of the overall oral care market, supported by companies like Dabur through strategic Ayurvedic positioning and authentic traditional formulations. China's market development follows distinct patterns, with new toothpaste regulations requiring comprehensive safety assessments for traditional ingredients while creating structured pathways for Ayurvedic medicine integration. Japan and Australia contribute to regional growth through premium positioning strategies that emphasize ingredient quality and clinical validation of traditional Ayurvedic principles, appealing to health-conscious consumers willing to pay premium prices for authentic traditional medicine solutions.

North America represents the second-largest regional market, driven by consumer health consciousness trends and increasing acceptance of alternative medicine approaches including traditional Ayurvedic oral care. The US oral care market, valued at USD 14.8 billion in 2022 with 4.2% CAGR through 2030, provides substantial opportunities for ayurvedic toothpaste penetration among consumers seeking natural alternatives to conventional formulations. FDA regulatory frameworks for oral care products create structured pathways for traditional ingredient validation while ensuring consumer safety standards for Ayurvedic formulations. Canadian market development follows similar patterns, with premium positioning and natural health product regulations supporting ayurvedic toothpaste market expansion. The region benefits from advanced e-commerce infrastructure that facilitates direct-to-consumer marketing and education about traditional Ayurvedic ingredients and their historical applications in oral health.

Europe demonstrates growing acceptance of ayurvedic oral care products, supported by traditional herbal medicine regulations that provide market access pathways for standardized Ayurvedic formulations. The European Medicines Agency's recognition frameworks for traditional herbal medicines create regulatory clarity while ensuring product safety and efficacy standards for traditional Indian medicine products. Germany and the United Kingdom lead regional adoption through established natural health product markets and consumer willingness to invest in premium oral care solutions based on traditional medicine principles. However, the region faces regulatory complexity with 2025 cosmetic regulations introducing ingredient restrictions that may affect traditional Ayurvedic formulations, requiring companies to navigate evolving compliance requirements. Southern European markets, including Italy, France, and Spain, show increasing interest in Ayurvedic oral care alternatives, though adoption rates remain below Northern European levels due to stronger conventional brand loyalty and limited familiarity with traditional Indian medicine principles.

Competitive Landscape

The ayurvedic toothpaste market exhibits moderate concentration, creating space for both established Ayurvedic specialists and multinational corporations entering the traditional medicine segment to compete effectively through differentiated positioning strategies. Market leaders pursue dual approaches of authenticity validation and geographic expansion while investing heavily in clinical research of traditional formulations and sustainable packaging innovations. Major players include Patanjali Ayurved Limited, Dabur India Limited, Colgate-Palmolive Company, Himalaya Wellness Company, and Viccolabs, among others.

Colgate-Palmolive's strategic retreat from Ayurvedic positioning in certain markets demonstrates the complexity of balancing global brand consistency with traditional medicine authenticity requirements, while companies like Dabur have successfully leveraged centuries-old Ayurvedic heritage in India's oral care segment. Technology adoption patterns reveal strategic emphasis on traditional formulation science and ingredient authentication rather than digital transformation initiatives. Companies are investing in modern extraction technologies to enhance traditional ingredient potency and bioavailability while maintaining authentic Ayurvedic preparation methods.

Opportunities exist in specialized therapeutic formulations, where traditional Ayurvedic principles can address specific oral health conditions through targeted ingredient combinations like Himalaya's HiOra-D for diabetic patients. Emerging disruptors focus on direct-to-consumer models that bypass traditional retail margins while building brand relationships through Ayurvedic education and ingredient transparency, though scaling challenges limit their immediate competitive threat to established players with extensive distribution networks and traditional medicine expertise.

Ayurvedic Toothpaste Industry Leaders

-

Colgate-Palmolive Company

-

Viccolabs

-

Dabur

-

Himalaya Wellness

-

Patanjali Ayurved Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Dabur Red Paste, the Ayurvedic toothpaste brand, launched the 'Switch To Fluoride Free' campaign on World Oral Health Day. The month-long campaign aimed to start a dialogue and sensitize the Indian population about the adverse effects of consuming further fluoride through toothpastes in Fluoride endemic regions of India.

- March 2025: Himalaya Wellness Company, one of India's leading wellness companies, announced the launch of HiOra-D toothpaste for diabetics. Himalaya Hiora-D Toothpaste was a herb-infused toothpaste designed for oral hygiene. The sugar-free and SLS-free formulation included a blend of botanical extracts such as Clove, Cinnamon, Jamun, and Turmeric to help support oral wellness.

- December 2024: Dabur India announced its entry into the kids' toothpaste category with the launch of Dabur Herb'l Kids Toothpaste, which was curated for cavity protection for children above 3 years of age. Unlike many fluoride toothpastes for kids, Dabur Herb'l Kids Toothpaste had no added chemicals and was available in strawberry flavor with characters like Iron Man for boys and Elsa from Frozen for girls. This was also the first time in India that famous characters like Iron Man and Elsa appeared on a kid's toothpaste.

Global Ayurvedic Toothpaste Market Report Scope

Ayurvedic toothpaste is an oral hygiene product made from natural and certified organic ingredients. The ingredients in herbal toothpaste are olive oil, aloe vera, eucalyptus oil, myrrh, camomile, calendula, neem, toothbrush tree, plant extracts, and essential oils. The global Ayurvedic toothpaste market is segmented by distribution channel and geography. The market is segmented by distribution channel into supermarkets/hypermarkets, convenience stores, online retail stores, pharmacies/drug stores, and other distribution channels. By geography, the market is segmented into the Americas, Europe, Asia-Pacific, the Middle East, and Africa. For each segment, the market sizing and forecast have been done based on value (in USD million).

| Gel-Based Toothpaste |

| Paste-Based Toothpaste |

| Others |

| Mass |

| Premium |

| Tubes |

| Jars |

| Others |

| Adults |

| Kids |

| Supermarkets/Hypermarkets |

| Convinience/Grocery Stores |

| Pharmacies/Drug Stores |

| Online Retail Stores |

| Other Distribution Channels |

| North America | United States |

| Canada | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Rest of Middle East and Africa |

| By Product Type | Gel-Based Toothpaste | |

| Paste-Based Toothpaste | ||

| Others | ||

| By Price-Tier | Mass | |

| Premium | ||

| By Packaging Type | Tubes | |

| Jars | ||

| Others | ||

| By End-User | Adults | |

| Kids | ||

| By Distribution Channel | Supermarkets/Hypermarkets | |

| Convinience/Grocery Stores | ||

| Pharmacies/Drug Stores | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the ayurvedic toothpaste market?

The ayurvedic toothpaste market was valued at USD 1.6 billion in 2026.

How fast is the ayurvedic toothpaste market expected to grow?

The category is forecast to register a 14.08% CAGR between 2026 and 2031.

Which region leads ayurvedic toothpaste sales?

Asia-Pacific accounted for 82.44% of global revenue in 2025 and continues to expand the fastest.

Which segment shows the highest growth potential?

Premium-priced ayurvedic toothpastes are projected to advance at 16.1% CAGR through 2031.

Page last updated on: