Helium Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Volume (2026) | 6.78 Billion Cubic Feet |

| Market Volume (2031) | 8.95 Billion Cubic Feet |

| Growth Rate (2026 - 2031) | 5.72% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Helium Market Analysis by Mordor Intelligence

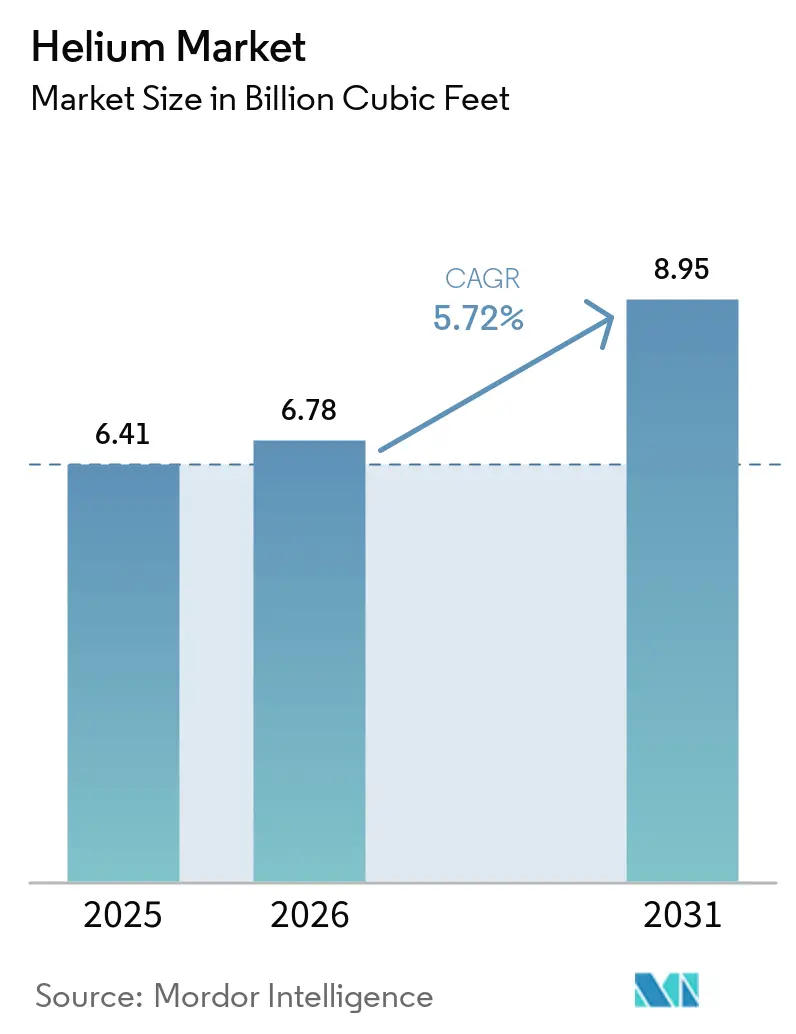

The Helium Market size was valued at 6.41 Billion Cubic Feet in 2025 and estimated to grow from 6.78 Billion Cubic Feet in 2026 to reach 8.95 Billion Cubic Feet by 2031, at a CAGR of 5.72% during the forecast period (2026-2031). Robust demand stems from semiconductor manufacturing, medical imaging, commercial space launch, and quantum computing, each relying on helium’s ultra-low boiling point and chemical inertness. The helium market continues to face supply volatility because fewer than 15 producers dominate global output, and the 2024 privatization of the U.S. Federal Helium Reserve removed subsidized stock from the system. New capacity from South Africa, Qatar, and Russia is temporarily easing scarcity, but structural concentration keeps users focused on long-term contracts and recycling investments. Semiconductor capacity additions under the U.S. CHIPS Act, the European Chips Act, and multiple Asian government incentive programs intensify demand, while MRI fleet growth in mid-income nations sustains healthcare’s position as the largest end-user.

Key Report Takeaways

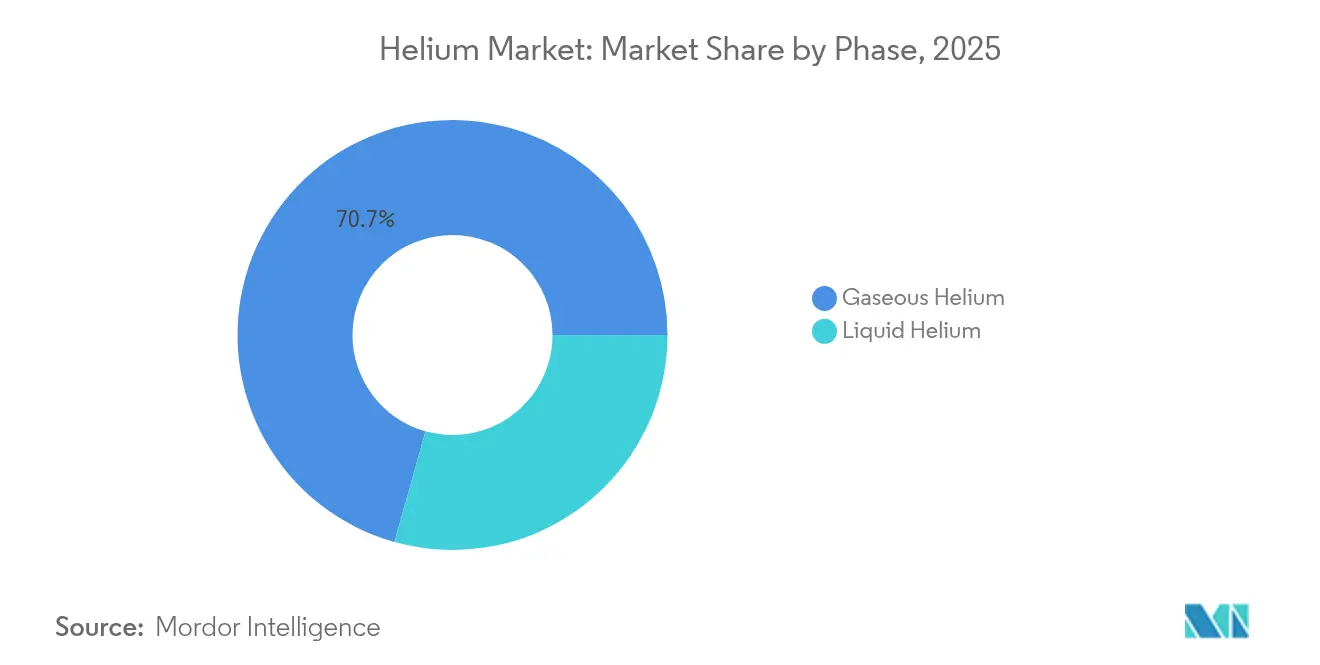

- By phase, gaseous helium led with 70.65% revenue share in 2025, and is posting the highest forecast CAGR at 6.03% through 2031 in the helium market.

- By application, cryogenics accounted for 33.10% of the helium market share in 2025 and is projected to advance at a 6.98% CAGR to 2031.

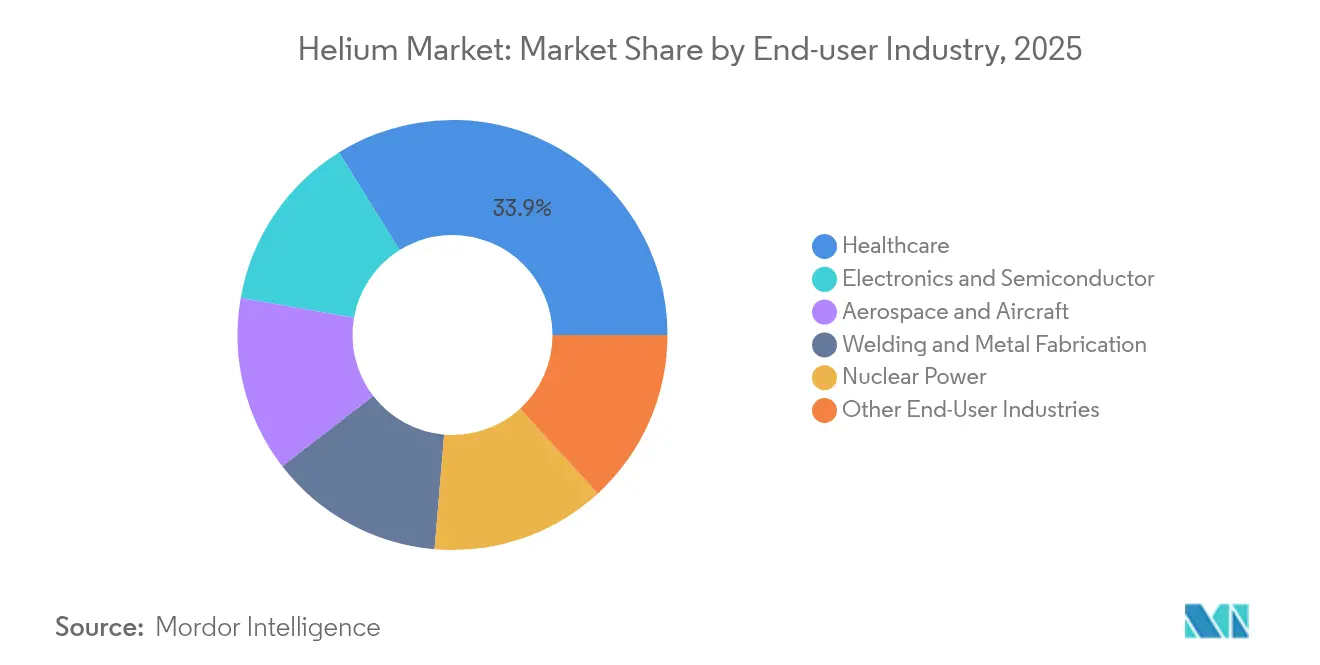

- By end-user industry, healthcare captured 33.86% of the helium market size in 2025 and is forecast to grow fastest at 6.92% CAGR through 2031.

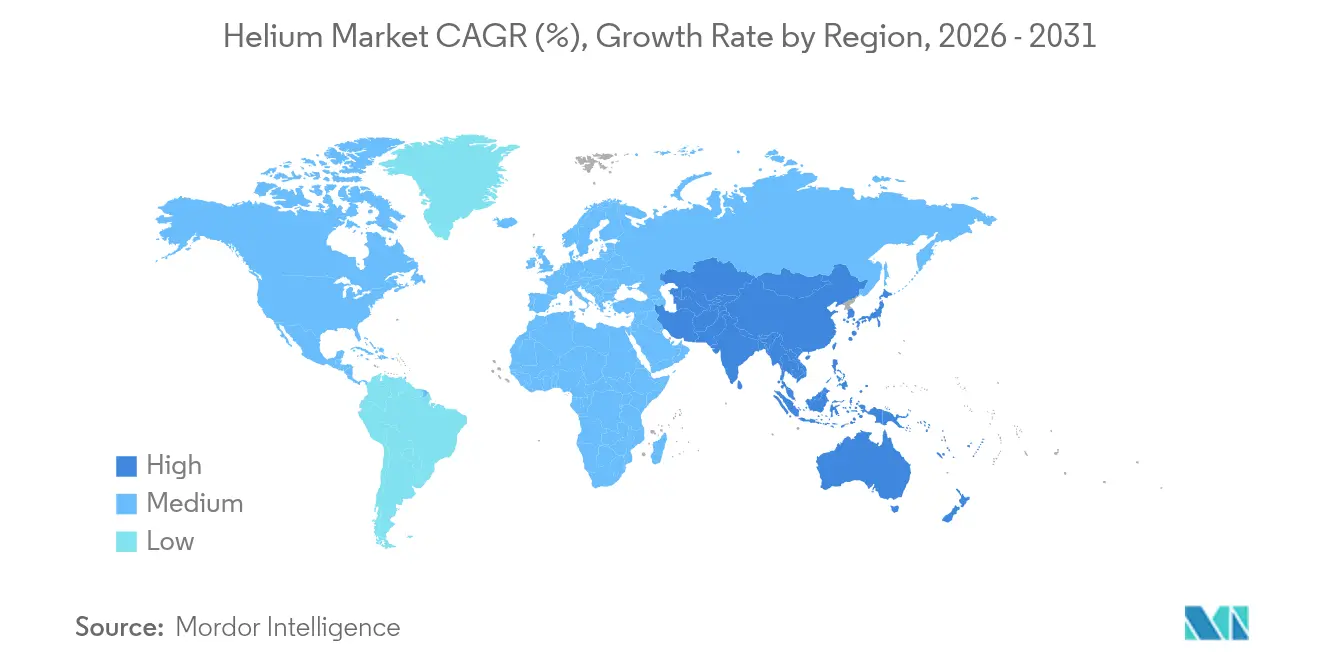

- By geography, North America commanded 38.55% of the helium market share in 2025, while Asia-Pacific is expected to record the highest regional CAGR at 7.05% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Helium Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Explosive semiconductor fab build-out in East Asia | +2.1% | Asia-Pacific core, spill-over to North America | Medium term (2-4 years) |

| MRI fleet expansion across mid-income hospitals | +1.8% | Global, with concentration in Asia-Pacific and MEA | Long term (≥ 4 years) |

| Commercial space-launch boom raising liquid-He demand | +1.2% | North America and Europe, emerging in Asia-Pacific | Short term (≤ 2 years) |

| Quantum-computing cryostats moving from lab to pilot lines | +0.9% | North America and EU, selective APAC markets | Medium term (2-4 years) |

| Pilot-scale Helium-3 extraction for neutron detection and fusion research and development | +0.4% | Global, concentrated in advanced nuclear markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Explosive Semiconductor Fab Build-Out in East Asia

Foundry expansions in China, Taiwan, Japan, and South Korea are propelling the helium market as chip plants rely on gaseous helium for wafer cleaning, lithography atmosphere control, and plasma etching. Intel, TSMC, and Samsung are building new U.S. and Asian fabs funded by the CHIPS Act and parallel regional programs, each fab requiring hundreds of millions of standard cubic feet of high-purity helium over its lifecycle. Taiwan’s clustering effect compounds regional demand, as advanced packaging lines consume helium for die bonding and encapsulation. Overall, semiconductor consumption intensity increases with each node shrink, locking in double-digit demand growth for the helium market through 2030.

MRI Fleet Expansion Across Mid-Income Hospitals

Hospitals in Asia-Pacific, Latin America, and Africa are adding MRI scanners to meet chronic disease diagnostics despite newer helium-light technologies. A conventional 1.5-ton unit needs 1,500–2,000 liters of liquid helium at installation and up to 10,000 liters across its service life. Helium conservation skids that recapture 92% of boil-off gas are spreading to tertiary hospitals, although upfront costs near USD 100,000 restrict adoption mainly to teaching centers. GE HealthCare’s Freelium and Siemens Healthineers’ DryCool platforms cut helium usage by 99%, yet slow fleet turnover leaves conventional magnets dominant into the next decade, sustaining long-term demand within the helium industry.

Commercial Space-Launch Boom Raising Liquid-He Demand

Private launch cadence is multiplying liquid helium needs for tank pressurization and purge operations. SpaceX’s Falcon 9 and Starship, Blue Origin’s New Glenn, and Rocket Lab’s Neutron each rely on helium to maintain cryogenic propellant integrity, with helium shortages cited for launch delays in 2024. NASA’s Artemis program likewise specifies helium for hydrogen tank purging, further tightening supplies. Launch sites are now installing on-site helium recovery units to recycle pressurant gas and shield schedules from market volatility helping mitigate supply risks in the helium industry.

Quantum-Computing Cryostats Moving from Lab to Pilot Lines

Superconducting-qubit platforms use dilution refrigerators that blend helium-3 and helium-4 to reach millikelvin temperatures, a trend that continues to shape the helium market. IBM, Google, and regional start-ups are scaling pilot production, turning research-scale consumption into industrial demand. Closed-cycle cryostats offer a long-term path to helium-free cooling; however, procurement costs and performance requirements keep helium in the loop today. Ultra-high purity needs and isotope separation add price premiums that suppliers monetize through dedicated production lines.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Finite reserves and concentration in a few countries | -1.4% | Global, with acute impact on import-dependent regions | Long term (≥ 4 years) |

| High liquefaction and logistics costs vs. substitutes | -0.8% | Global, particularly affecting price-sensitive applications | Medium term (2-4 years) |

| Tightened flare-gas rules limiting co-produced helium | -0.6% | North America, with regulatory spillover to other regions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Finite Reserves and Concentration in a Few Countries

Roughly 70% of known helium reserves sit in the United States, Qatar, Algeria, and Russia, fostering geopolitical leverage and supply manipulation that directly influence the helium market. China imports 95% of its helium needs, underscoring exposure to diplomatic friction and maritime logistics risks. EU sanctions on Russian helium illustrate how quickly policy can reroute trade and spike prices. Co-produced helium may remain trapped underground as natural-gas production tapers under decarbonization agendas. Recycling can cut wastage, but cannot create a new primary supply, reinforcing the imperative for strategic reserves.

Tightened Flare-Gas Rules Limiting Co-Produced Helium

U.S. waste-prevention regulations now impose royalties on avoidable flaring, compelling upstream operators to capture or re-inject gas streams[1], shifting economic signals throughout the helium market. While beneficial for methane mitigation, the rules can reduce economic incentive to recover helium where volumes are low relative to capture costs. Nigeria’s experience shows similar policy outcomes, with a 9.26 percentage-point reduction in flaring after tariff hikes, but with limited helium recovery.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Phase: Gaseous Helium Anchors Industrial Consumption

Gaseous helium held 70.65% of the 2025 volume, reflecting large-scale use in pressurization, purging, and leak-testing, and is growing at a 6.03% CAGR as leading-edge nodes tighten contamination tolerances, sustaining a substantial share of the helium market size for process gases. The gaseous segment also benefits from aerospace welding and additive-manufacturing processes that rely on helium’s high thermal conductivity for deep, narrow weld profiles.

Emerging hydrogen-fuel testing and electric-vehicle battery leak detection add incremental volumes, extending gaseous helium’s dominance well into the forecast horizon across the helium market. MRI fleet expansion, quantum-system scale-out, and high-energy physics laboratories anchor baseline liquid helium demand. Increasing deployment of on-site liquefiers and 92% efficient recovery skids mitigates boil-off losses, but absolute volumes continue to rise.

By Application: Cryogenics Captures Volume and Value Upside

Cryogenics retained the largest 2025 share at 33.10% and is on course for a 6.98% CAGR through 2031, underpinned by quantum-computing pilot lines and a stable MRI installed base. Every 1 MW of quantum processing power requires approximately 12,000 liters of helium annually for dilution refrigeration, translating into a multibillion-cubic-foot pull on the helium market by decade-end. Particle accelerators and fusion pilot facilities in North America and Europe reinforce cryogenic momentum.

Leak detection, pressurizing, purging, and welding collectively exceed 40% of non-cryogenic demand, reinforcing diversified end-use stability within the helium market. Rocket programs from government and commercial operators keep pressurization needs rising, while predictive maintenance adoption in automotive and petrochemical plants drives helium leak-testing growth. Controlled-atmosphere packaging for shelf-life extension in electronics and premium foods is another pocket of steady consumption. Across these varied uses, helium’s inertness and low viscosity afford operational safety that competing gases cannot match.

By End-User Industry: Healthcare Holds Leadership as Electronics Accelerate

Healthcare retained a 33.86% share in 2025 and will progress at a 6.92% CAGR through 2031 as emerging economies equip hospitals with advanced MRI systems. Even with helium-light technology adoption, the sheer volume of new scanners sustains absolute demand. Hospital groups in India, Brazil, and Saudi Arabia are installing helium recovery plants to mitigate cost and supply risk, ensuring long-term dependence on helium supply chains.

Electronics and semiconductors are expected to overtake aerospace as the fastest-growing end-user, driven by logic and memory fabs coming online in East Asia and North America. Fab operators prioritize multi-year helium contracts and on-site micro-liquefaction to stabilize pricing. Nuclear power continues to trial helium-cooled high-temperature reactors, and early fusion prototypes deepen helium-3 demand. Aerospace, welding, and scientific research round out the consumption mix, each leveraging helium’s thermal and inertness advantages for mission-critical operations across the helium industry.

Geography Analysis

North America commanded 38.55% of 2025 volume, supported by the world’s largest proven reserves and mature midstream infrastructure. The Federal Helium Reserve privatization in 2024 shifted the procurement landscape, compelling end-users to negotiate directly with private producers at market rates, but Honeywell’s Dry Piney and smaller Rockies projects are filling the gap. Semiconductor fab construction in Arizona, Ohio, and Texas further supports regional consumption growth, reinforcing North America's leadership in the helium industry.

Asia-Pacific is projected to post the highest 7.05% CAGR through 2031 as China, Japan, India, and South Korea ramp up semiconductors, satellite manufacturing, and medical imaging. China’s 95% import dependence creates a strategic imperative for contract diversification and micro-liquefier deployment at industrial parks. Japan’s incentive packages for next-generation memory plants accelerate helium spending, while India’s nascent fab ecosystem and fast-growing healthcare sector widen demand. Regional investment in unconventional helium fields, notably in Australia and Tanzania, aims to hedge supply exposure and strengthen the region’s position in the helium industry.

Though smaller in volume, Europe faces structural supply restructuring after sanctions eliminated Russian helium flows. End-users now source from Qatar and the U.S. Gulf Coast, absorbing freight premiums and installation of on-site recovery to cushion volatility.

Competitive Landscape

Leading helium producers such as Air Liquide, Linde, and Air Products maintain leadership through integrated extraction, liquefaction, and distribution networks, complemented by long-term contracts with semiconductor, aerospace, and healthcare clients. Technology competition centers on membrane separation, cryogenic recovery, and closed-cycle refrigeration. Producers able to supply ultra-high purity grades and isotope-specific blends secure long-term contracts with quantum-computing, fusion, and medical-device clients. Meanwhile, regulatory frameworks such as U.S. waste-prevention rules reward operators that integrate methane capture with helium recovery, adding compliance-driven differentiation.

Helium Industry Leaders

Air Liquide

ExxonMobil Corporation

Air Products and Chemicals, Inc.

Gazprom

Linde plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Air Liquide entered exclusive negotiations to acquire DIG Airgas for more than USD 3.3 billion, marking the company's return to the Korean market, providing access to major semiconductor clients.

- January 2024: Messer, in partnership with the U.S. Bureau of Land Management, delivered its billionth standard cubic foot of helium from the Crude Helium Enrichment Unit, affirming supply reliability commitments.

Global Helium Market Report Scope

Helium is a chemical element with the symbol He. It is a colorless, odorless, and tasteless gas and is the second lightest and most abundant element in the universe. It is a non-renewable resource, and its supply is limited. Helium has several important applications in cryogenics and superconductivity, balloons and airships, welding and leak detection, breathing mixtures, aerospace and rockets, nuclear energy research, etc.

The helium market is segmented by phase, application, end-user industry, and geography. By phase, the market is segmented into liquid and gas. By application, the market is segmented into breathing mixes, cryogenics, leak detection, pressurizing and purging, welding, controlled atmosphere, and other applications. By end-user industry, the market is segmented into aerospace and aircraft, electronics and semiconductors, nuclear power, healthcare, welding and metal fabrication, and other end-user industries. By geography, the market is segmented into Asia-Pacific, North America, Europe, and Rest of the World). The report also covers the market sizes and forecasts for the helium market in 14 countries across the major regions. For each segment, the market sizes and forecasts are provided based on volume (cubic feet).

| Liquid Helium |

| Gaseous Helium |

| Breathing Mixes |

| Cryogenics |

| Leak Detection |

| Pressurizing and Purging |

| Welding |

| Controlled Atmosphere |

| Other Applications |

| Aerospace and Aircraft |

| Electronics and Semiconductor |

| Nuclear Power |

| Healthcare |

| Welding and Metal Fabrication |

| Other End-User Industries |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Malaysia | |

| Taiwan | |

| Thailand | |

| Indonesia | |

| Vietnam | |

| Australia | |

| New Zealand | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Poland | |

| Spain | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| Egypt | |

| South Africa | |

| Rest of Middle-East and Africa |

| By Phase | Liquid Helium | |

| Gaseous Helium | ||

| By Application | Breathing Mixes | |

| Cryogenics | ||

| Leak Detection | ||

| Pressurizing and Purging | ||

| Welding | ||

| Controlled Atmosphere | ||

| Other Applications | ||

| By End-User Industry | Aerospace and Aircraft | |

| Electronics and Semiconductor | ||

| Nuclear Power | ||

| Healthcare | ||

| Welding and Metal Fabrication | ||

| Other End-User Industries | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Malaysia | ||

| Taiwan | ||

| Thailand | ||

| Indonesia | ||

| Vietnam | ||

| Australia | ||

| New Zealand | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Poland | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| Egypt | ||

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the current size of the helium market?

The helium market size stands at 6.78 billion cubic feet in 2026.

How fast is helium demand expected to grow?

Global volume is projected to rise at a 5.72% CAGR, reaching 8.95 billion cubic feet by 2031.

Which region is growing fastest in helium consumption?

Asia-Pacific is forecast to post the highest regional CAGR at 7.05% through 2031 due to semiconductor and healthcare expansion.

Why is helium critical to semiconductor manufacturing?

Foundries use high-purity gaseous helium for wafer cleaning, lithography atmosphere control, and thermal management, and consumption increases with each node shrink.

How are hospitals managing helium shortages?

Many install recovery skids that recapture up to 92% of boil-off, while newer MRI designs like Freelium sharply cut helium needs.

Page last updated on: