Ventricular Assist Device Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

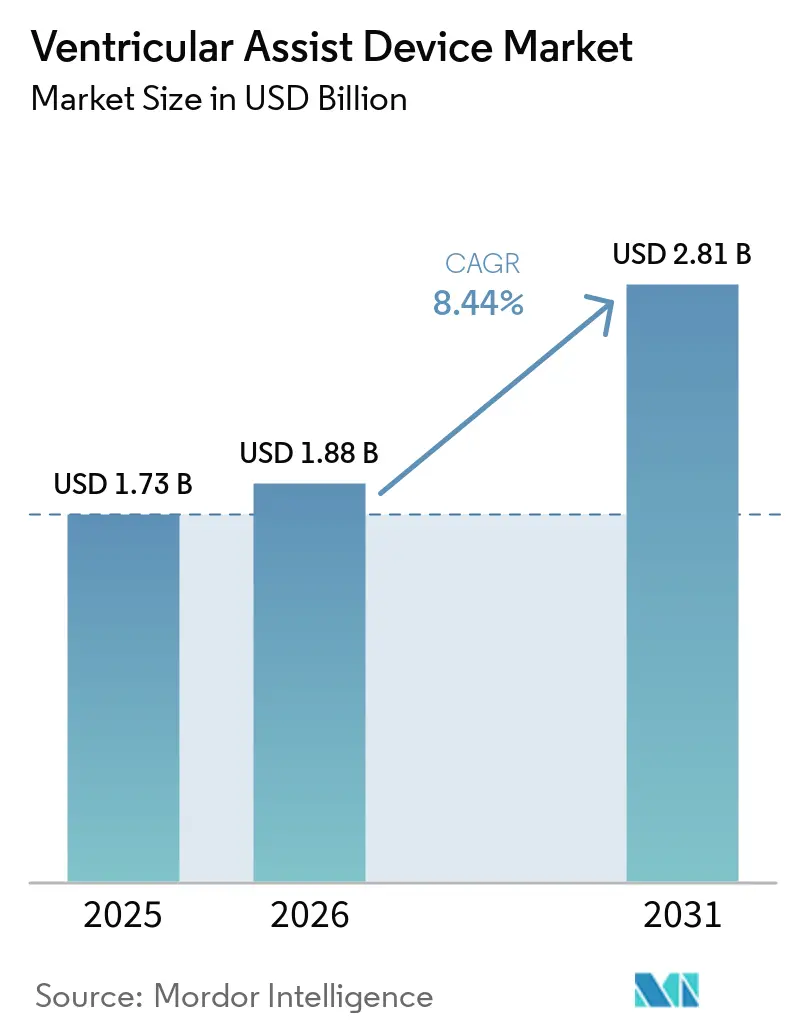

| Market Size (2026) | USD 1.88 Billion |

| Market Size (2031) | USD 2.81 Billion |

| Growth Rate (2026 - 2031) | 8.44% CAGR |

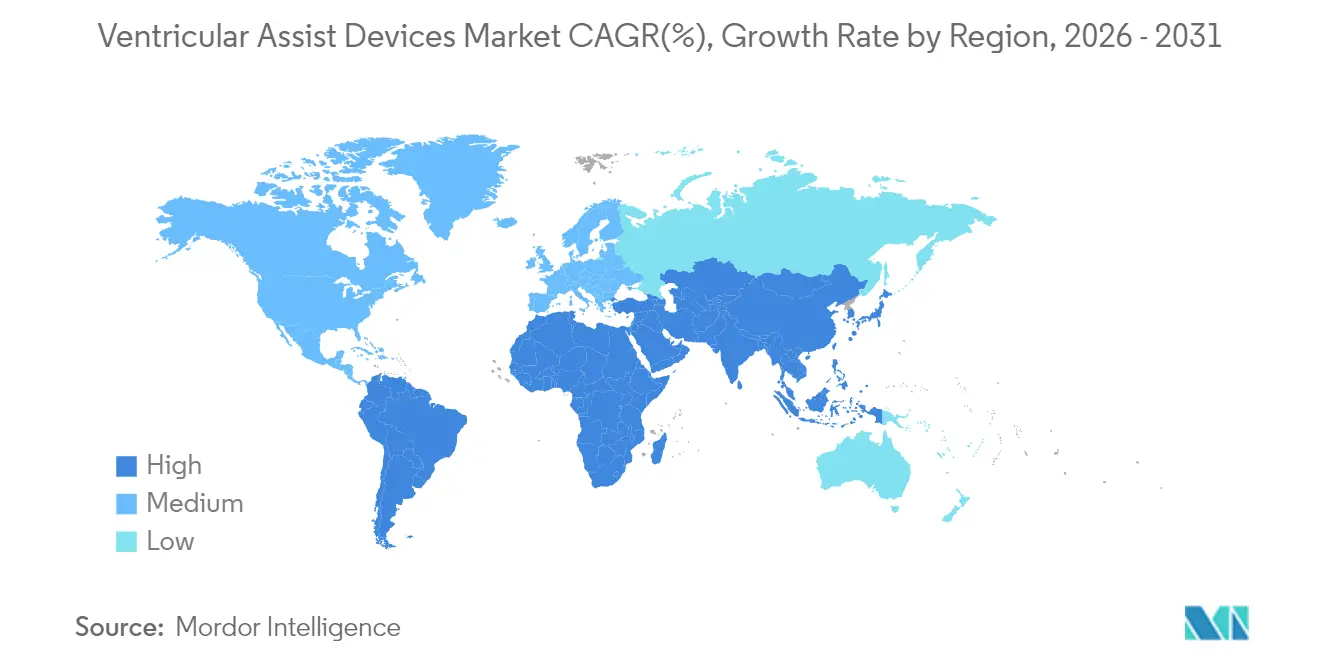

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

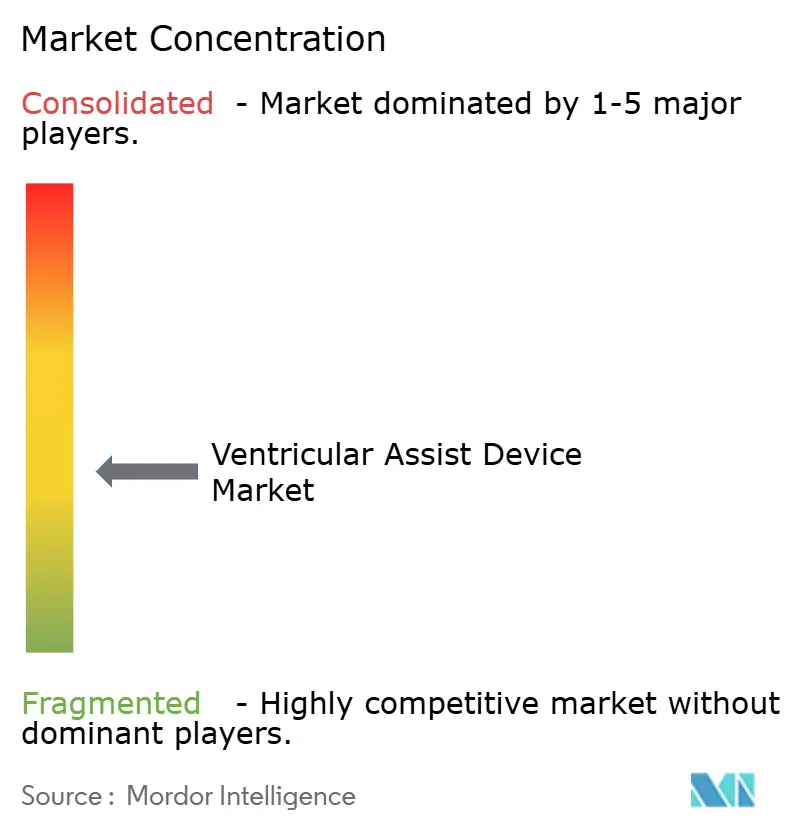

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Ventricular Assist Device Market Analysis by Mordor Intelligence

Ventricular Assist Devices market size in 2026 is estimated at USD 1.88 billion, growing from 2025 value of USD 1.73 billion with 2031 projections showing USD 2.81 billion, growing at 8.44% CAGR over 2026-2031. Demand grows as ageing populations swell the pool of advanced-heart-failure patients and technological progress raises the clinical ceiling for mechanical circulatory support.[1]Heart Failure Society of America, “HF Stats 2024: Heart Failure Epidemiology and Outcomes Statistics,” hfsa.org Device makers are moving beyond bridge-to-transplant use cases, widening the total addressable Ventricular Assist Devices market through permanent support indications and fully implantable designs. Real-world data from large registries such as INTERMACS is driving evidence-based refinements in patient selection, while reimbursement expansions in key regions strengthen provider confidence. Simultaneously, new magnetic-levitation pumps and wireless power platforms lower adverse-event rates, reinforcing their role as long-term cardiac replacements.

Key Report Takeaways

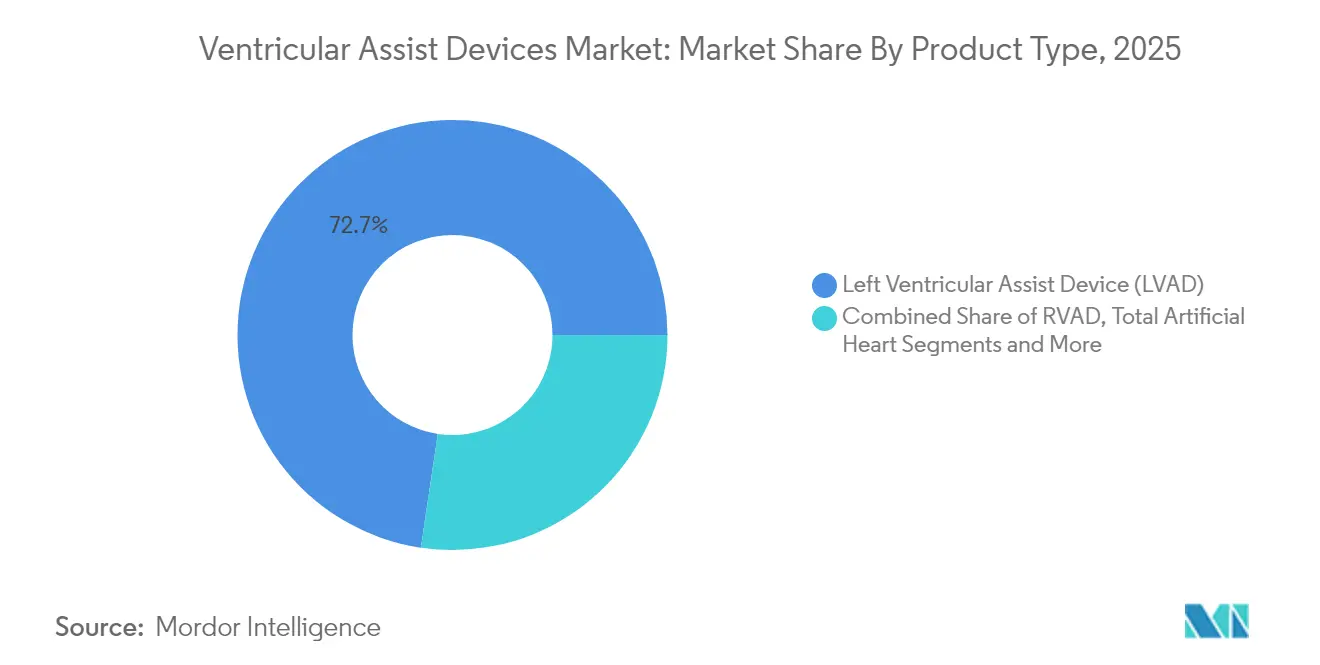

- By product type, Left Ventricular Assist Devices led with 72.65% revenue share in 2025 while expanding at a 9.08% CAGR through 2031.

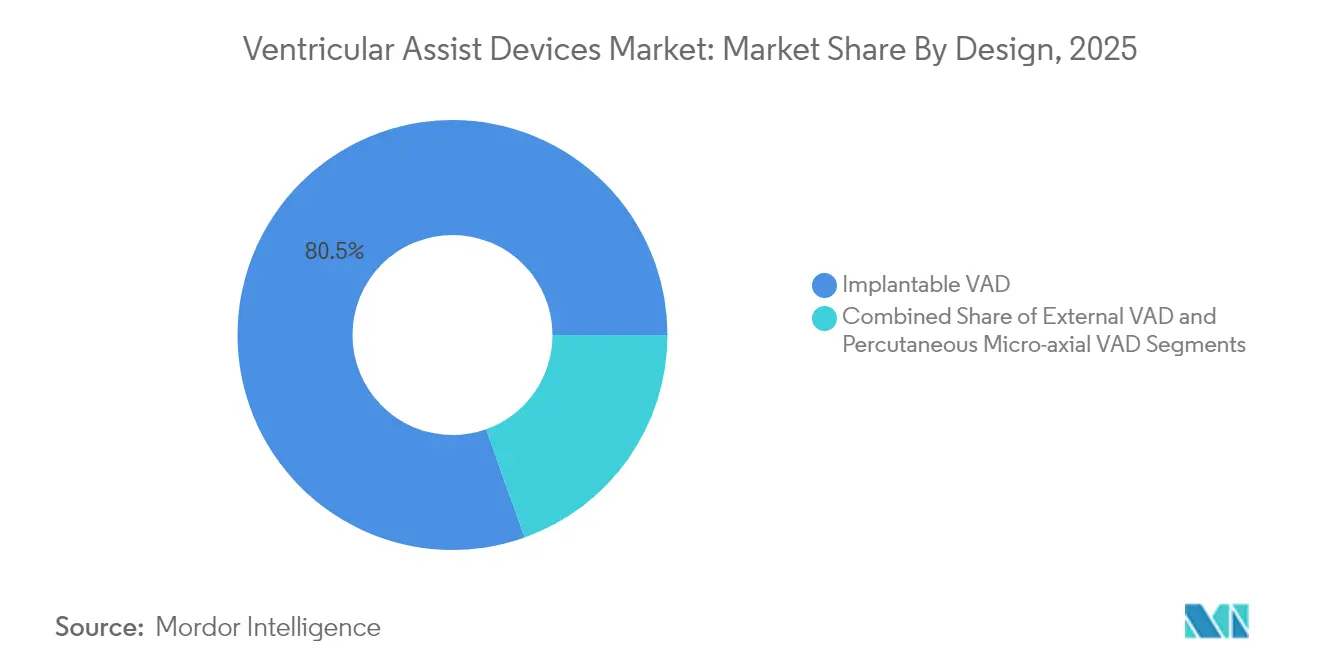

- By design, Implantable systems held 80.45% of Ventricular Assist Devices market share in 2025, whereas Percutaneous micro-axial pumps post a 11.86% CAGR to 2031.

- By therapy, Bridge-to-Transplant accounted for 48.78% of Ventricular Assist Devices market size in 2025, yet Destination Therapy is set to grow at 11.25% CAGR to 2031.

- By geography, North America captured 42.10% of revenues in 2025; Asia-Pacific registers the fastest 10.43% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Ventricular Assist Device Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) (%) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing burden of cardiac diseases | +2.1% | Global, highest in North America and Europe | Long term (≥ 4 years) |

| Technological advances | +1.8% | Global, led by North America and Europe | Medium term (2-4 years) |

| Expanding destination therapy amid donor gap | +1.5% | Global, especially North America and Europe | Medium term (2-4 years) |

| Ageing population and higher health spend | +1.3% | Global, concentrated in developed markets | Long term (≥ 4 years) |

| More clinical trials and faster approvals | +0.9% | North America and Europe, extending to Asia-Pacific | Short term (≤ 2 years) |

| Wider uptake of minimally invasive pumps | +0.7% | Global, early adoption in North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing burden of cardiac diseases & heart failure

Heart-failure prevalence rose to 6.7 million Americans in 2025 and will climb to 11.4 million by 2050, widening the patient base for mechanical support.[1]Heart Failure Society of America, “HF Stats 2024: Heart Failure Epidemiology and Outcomes Statistics,” hfsa.org Younger cohorts and racial minorities are showing steeper incidence curves, which shifts device demand toward patients likely to need decades of circulatory assistance. Estimates place the cumulative cost of heart failure at USD 420 billion by mid-century, encouraging payers to support durable devices over repeated hospitalizations.

Technological advances

Magnetic levitation pumps such as HeartMate 3 post 63.3% five-year survival and lower thrombosis risk than earlier bearings-based systems.[2]European Heart Journal, “Five-Year Survival with Fully Magnetically Levitated LVAD,” academic.oup.com Miniaturised percutaneous pumps now use 9 Fr delivery profiles with 100% valve-crossing success in more than 500 procedures. Early studies on wireless power transfer demonstrate safe energy delivery across seven meters, pointing to future cable-free, fully implantable platforms.

Expanding destination therapy amid organ donor shortage

Improved pump durability is pushing destination-therapy volumes upward despite a drop in transplant-linked implants, and data show LVAD survival near parity with transplant outcomes in patients younger than 50 years.[3]NewYork-Presbyterian, “LVAD Therapy Offers Similar Survival as Heart Transplantation for Younger Patients,” nyp.orgCentres such as Cleveland Clinic report multi-year survival surpassing registry averages, validating permanent-support pathways and encouraging guideline updates.

Ageing population and healthcare spending

Patients over 70 account for rising implant numbers even as mortality rates rise, reflecting clinical confidence that quality-of-life gains offset increased peri-operative risk. Cost-effectiveness studies cite USD 69,768 per quality-adjusted life year for bridge-to-transplant therapy, moving LVADs inside accepted payer thresholds.[4]ASAIO Journal, “Cost-Effectiveness and Extended Support with Impella 5.5,” asaiojournal.com

Restraints Impact Analysis*

| Restraint | (~) (%) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High device and procedure costs | -1.4% | Global, amplified in emerging markets | Medium term (2-4 years) |

| Device-related complications and recalls | -1.1% | Global, regulatory focus in North America, Europe | Short term (≤ 2 years) |

| Alternatives and evolving heart therapies | -0.8% | Global, most visible in developed markets | Long term (≥ 4 years) |

| Scarcity of trained LVAD coordinators | -0.6% | Asia-Pacific, Middle East, Latin America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High device and procedure costs

Implantation averages USD 175,420 and total stay costs approach USD 193,192, with a further USD 52,068 for readmissions, frustrating adoption in cost-sensitive markets. Limited insurer coverage and large capital budgets deter smaller centres, even as cost-effectiveness improves with battery longevity and reduced complication rates.

Device-related complications and recalls

Abbott’s Class I recall of 13,883 HeartMate kits illustrates the reputational and financial impact of safety events, with 14 deaths and 273 injuries recorded. Bleeding and infection remain common obstacles, though the aspirin-free regimen approved in 2025 cut bleeding events 40% without raising thrombosis risk.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: LVAD Dominance Drives Innovation

Left Ventricular Assist Devices command 72.65% of 2025 revenues, the largest slice of the Ventricular Assist Devices market. Their 9.08% CAGR to 2031 reflects broad clinical eligibility and strong data on long-term survival. The Ventricular Assist Devices market size for LVADs is forecast to expand steadily as magnetic levitation platforms reduce thrombosis and pump stoppage rates. LVAD innovation now centres on wireless power and miniature control units, features that will narrow the gap with total artificial hearts.

Right Ventricular Assist Devices fill niche needs in isolated right-side failure, and Biventricular systems address complex bi-ventricle dysfunction, while total artificial hearts such as Aeson progress in pilot roll-outs. Clinical evidence highlights a 14-year support record for a single LVAD recipient, underscoring the destination-therapy potential of new models.

By Design: Percutaneous Innovation Challenges Implantable Dominance

Implantable pumps hold 80.45% revenue share today and remain the backbone of durable support. The category’s grip on the Ventricular Assist Devices market will hold through 2031, but percutaneous micro-axial devices are growing 11.86% per annum, buoyed by minimally invasive procedures that fit cath-lab workflows. The Impella 5.5 now offers 70-day bridge-to-transplant support, a capability once reserved for fully implantable systems.

The Ventricular Assist Devices market size tied to percutaneous platforms is climbing as hospitals adopt them for high-risk PCI, cardiogenic shock, and bridge-to-decision cases. Wireless charging prototypes point to a convergence where external and implantable categories blur, creating a spectrum rather than a split.

By Application/Therapy: Destination Therapy Accelerates Clinical Adoption

Bridge-to-Transplant remains the largest therapy class at 48.78% share, supported by decades of surgical and reimbursement infrastructure. Yet Destination Therapy posts the fastest 11.25% CAGR, and is projected to capture a growing proportion of Ventricular Assist Devices market share by 2031 as younger cohorts prove survivorship parity with transplant recipients.

Surgeons are embracing early referral for Destination Therapy, integrating palliative services to manage the lifelong nature of support. Bridge-to-Recovery and Bridge-to-Decision spheres are small but clinically significant, especially in myocardial recovery settings for younger patients.

Geography Analysis

North America holds 42.10% of 2025 sales, reflecting robust Medicare coverage, centre-of-excellence networks, and a rich innovation pipeline. Registry data and outcome transparency continue to boost clinician confidence. The region is the primary launch ground for new platforms granted FDA breakthrough designation, enhancing first-mover revenues.

Europe presents steady uptake, leveraging harmonised regulatory frameworks and established heart-failure networks. Adoption is tempered by slower reimbursement updates and occasional device lag, yet the region is home to landmark innovations like the Aeson total artificial heart and strong academic-industry partnerships.

Asia-Pacific is the fastest growing at a 10.43% CAGR. Urbanising economies and rising cardiovascular risk deepen unmet need, while policy reforms widen device reimbursement. However, limited trained personnel and cost constraints slow penetration in secondary cities, making training programmes and public–private financing critical.

Competitive Landscape

The Ventricular Assist Devices market shows moderate concentration: Abbott, Medtronic, and Johnson & Johnson capture roughly 60% of global revenue. Abbott leads with its magnetically levitated HeartMate 3 platform, which secured approval to remove aspirin from standard therapy, reducing bleeding complications by 40%. Medtronic leverages catheter-based Impella pumps to dominate percutaneous support, while Johnson & Johnson’s acquisition of V-Wave underscores its strategy to broaden the heart-failure toolkit.

Emerging challengers such as CARMAT and BiVACOR are advancing total artificial hearts with wireless energy transmission. ReliantHeart is developing cable-free LVADs that promise lower infection risk. Pediatric-device white space remains large, inviting niche entrants pursuing smaller pump profiles.

Patent activity clusters around magnetic bearing enhancements, biocompatible surfaces, and remote monitoring. Regulatory science programmes at the FDA seek to standardise hemocompatibility testing and durability metrics, signalling a maturing oversight ecosystem that balances safety with innovation.

Ventricular Assist Device Industry Leaders

Medtronic PLC

Abbott Laboratories

Berlin Heart GmbH

SynCardia Systems LLC

Johnson and Johnson (Abiomed)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: FDA granted breakthrough status to BiVACOR’s totally implantable artificial heart, accelerating U.S. trial timelines.

- April 2025: CARMAT received conditional FDA approval for the second cohort of its Aeson artificial heart feasibility study.

- March 2025: Cadrenal Therapeutics and Abbott launched the TECH-LVAD trial assessing tecarfarin anticoagulation in HeartMate 3 recipients.

- February 2025: Abbott secured CE Mark for the AVEIR DR dual-chamber leadless pacemaker, expanding its heart-failure device suite.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

We define the ventricular assist devices (VAD) market as the global sales value of implantable or transcutaneous mechanical pumps that partially or fully support one or both ventricles in patients with advanced heart failure, across adult and pediatric cohorts. Our study captures left, right, and biventricular assist devices, as well as percutaneous micro-axial pumps that remain in situ for more than 24 hours.

Scope Exclusions: Intra-aortic balloon pumps, extracorporeal membrane oxygenation circuits, and total artificial hearts limited to investigational use are outside this analysis.

Segmentation Overview

- By Product Type

- Left Ventricular Assist Device (LVAD)

- Right Ventricular Assist Device (RVAD)

- Biventricular Assist Device (BIVAD)

- Total Artificial Heart (TAH)

- By Design

- Implantable VAD

- Transcutaneous / External VAD

- Percutaneous Micro-axial VAD

- By Application / Therapy

- Bridge-to-Transplant (BTT)

- Destination Therapy (DT)

- Bridge-to-Recovery (BTR)

- Bridge-to-Decision

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Interviews were conducted with cardiothoracic surgeons, transplant coordinators, and procurement managers from North America, Europe, and key Asia-Pacific centers. Their inputs clarified real-world implant mix, typical ASP discounts, and the pace at which destination therapy is expanding. Follow-up surveys with biomedical engineers validated learning-curve driven cost declines and expected adoption of fully implantable driveline-free pumps.

Desk Research

Our analysts began with structured reviews of open clinical registries such as INTERMACS, EuroMedLVAD, and Japan VAD, which reveal annual implant volumes and survival trends. We then harvested import-export tallies from UN Comtrade and U.S. ITC codes that track pump controllers and cannulae movements. Policy and reimbursement updates were parsed from sources such as the U.S. Centers for Medicare & Medicaid Services and Germany's G-BA, while technology signals were followed through PubMed and the FDA 510(k)/PMA database. Paid repositories, D&B Hoovers for company revenue splits and Dow Jones Factiva for deal flow, helped triangulate competitive footprints. The sources cited are illustrative; many additional databases and journals informed our view.

A second sweep extracted pricing corridors from hospital charge master disclosures and tender portals, giving us average selling-price (ASP) benchmarks by geography. Device failure alerts logged in MAUDE rounded out reliability assumptions.

Market-Sizing & Forecasting

We constructed a top-down model that rebuilds demand from heart-failure prevalence, INTERMACS class distribution, and transplant eligibility pools, then applies region-specific penetration rates. Outputs are cross-checked with bottom-up approximations, sampled hospital implant counts multiplied by blended ASPs, to keep totals tethered to the ground.

• New end-stage HF incidence per 100,000 population • Average waiting time on transplant lists • Annual VAD explant rates (bridge-to-recovery) • Regulatory approvals logged per year • ASP erosion linked to miniaturization milestones

A multivariate regression with HF incidence, GDP per capita, and reimbursement coverage as predictors drives 2025-2030 projections; scenario analysis adjusts for breakthrough pediatric indications. Gaps in hospital-level data are bridged using moving-average substitution from nearest peer facilities and validated with expert panels.

Data Validation & Update Cycle

Every draft passes anomaly screens and peer review before sign-off. Models are refreshed annually; interim updates trigger when material events, major recalls, landmark trials, or reimbursement shifts, move the baseline. A final analyst audit is run just before client delivery to ensure the latest guidance is reflected.

Why Mordor Ventricular Assist Devices Baseline Offers Unmatched Reliability for Stakeholders

Published market values often diverge because firms vary device scope, price erosion curves, and refresh frequency. We acknowledge these differences up front so readers understand why numbers rarely align perfectly.

Key gap drivers include whether percutaneous short-term pumps are counted, the aggressiveness of ASP deflators, and how quickly pediatric indications are layered into forecasts. Some studies roll heart-pump accessories into revenues, while others assume flat pricing or apply a one-time COVID catch-up bump, choices that can swing 2025 totals by hundreds of millions.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 1.73 B (2025) | Mordor Intelligence | - |

| USD 2.70 B (2025) | Global Consultancy A | Includes short-term Impella and heart-pump accessories; applies uniform 8 % ASP decline worldwide |

| USD 1.49 B (2025) | Trade Journal B | Excludes right and bi-VAD units; uses conservative destination therapy uptake assumptions |

In sum, while external figures frame the discussion, Mordor's disciplined mix of registries, real-world pricing, and frequent updates yields a balanced baseline that decision-makers can trace back to clear variables and reproducible steps.

Key Questions Answered in the Report

What is the current size of the Ventricular Assist Devices market?

The market stands at USD 1.88 billion in 2026 and is on track to reach USD 2.81 billion by 2031.

Which product type leads the Ventricular Assist Devices market?

Left Ventricular Assist Devices hold 72.65% of 2025 revenues and remain the fastest growing segment.

How fast is the Asia-Pacific Ventricular Assist Devices market growing?

Asia-Pacific posts the quickest regional CAGR at 10.43% through 2031.

Why is destination therapy gaining traction in the Ventricular Assist Devices market?

Improved pump durability and transplant-comparable survival in younger patients support permanent therapy adoption.

What are the main obstacles to wider Ventricular Assist Devices adoption?

High upfront costs, device-related complications, and limited specialist personnel in emerging regions slow uptake.

Page last updated on: