Global Medical Billing Outsourcing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

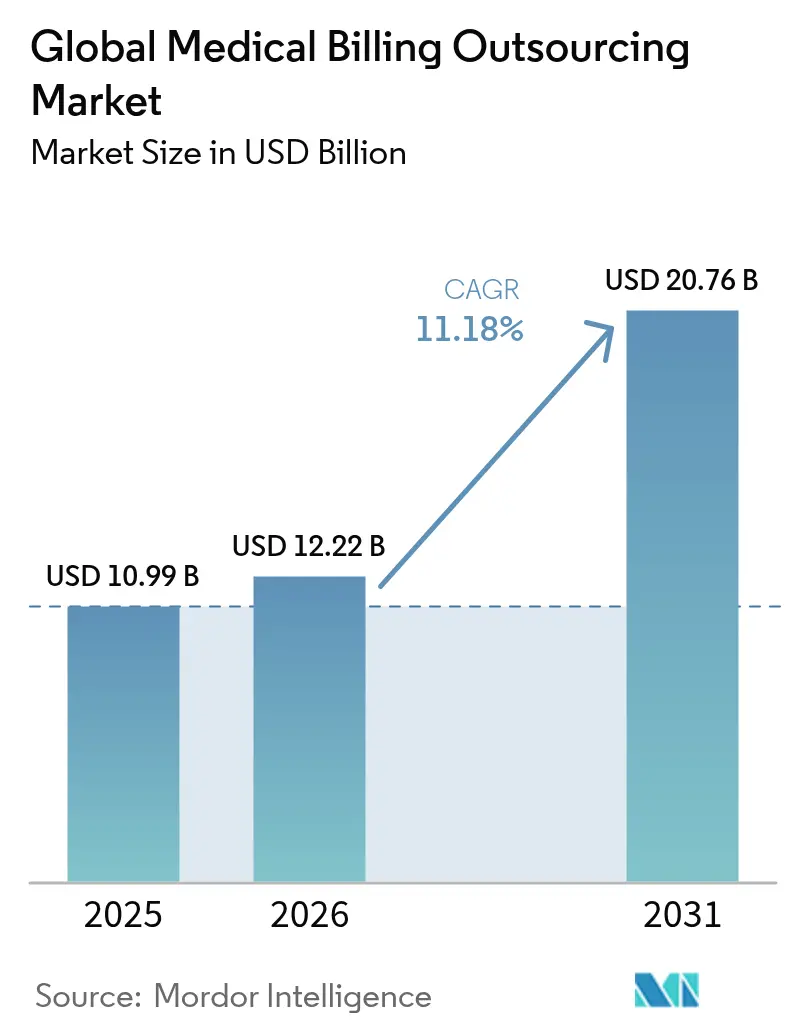

| Market Size (2026) | USD 12.22 Billion |

| Market Size (2031) | USD 20.76 Billion |

| Growth Rate (2026 - 2031) | 11.18% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

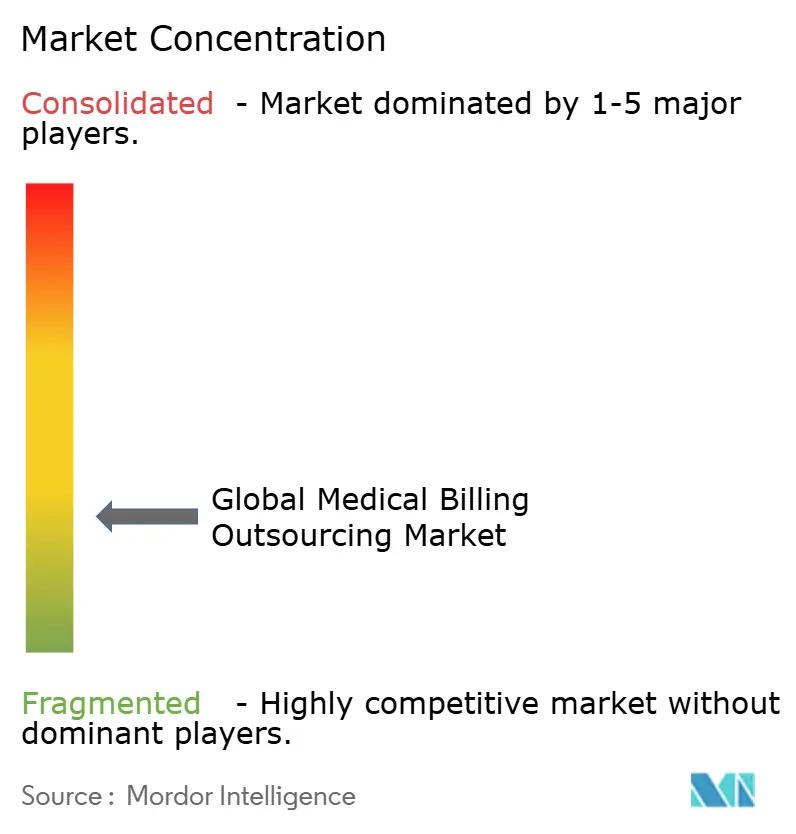

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Global Medical Billing Outsourcing Market Analysis by Mordor Intelligence

The medical billing outsourcing market size in 2026 is estimated at USD 12.22 billion, growing from 2025 value of USD 10.99 billion with 2031 projections showing USD 20.76 billion, growing at 11.18% CAGR over 2026-2031. Demand is powered by providers moving work away from costly internal billing toward specialist partners who improve cash‐flow velocity with higher first-pass claim acceptance. Growing coding complexity, payor denials and coder shortages have made external expertise indispensable. Technology-first vendors that embed artificial intelligence and cloud delivery now cut processing costs by as much as 40% while raising accuracy, prompting larger health systems and ambulatory centers alike to view outsourcing as an operational imperative. Intensifying cybersecurity rules and the price-tag of HIPAA Security updates are nudging even security-sensitive providers toward scale partners whose compliance investments outstrip most internal budgets.

Key Report Takeaways

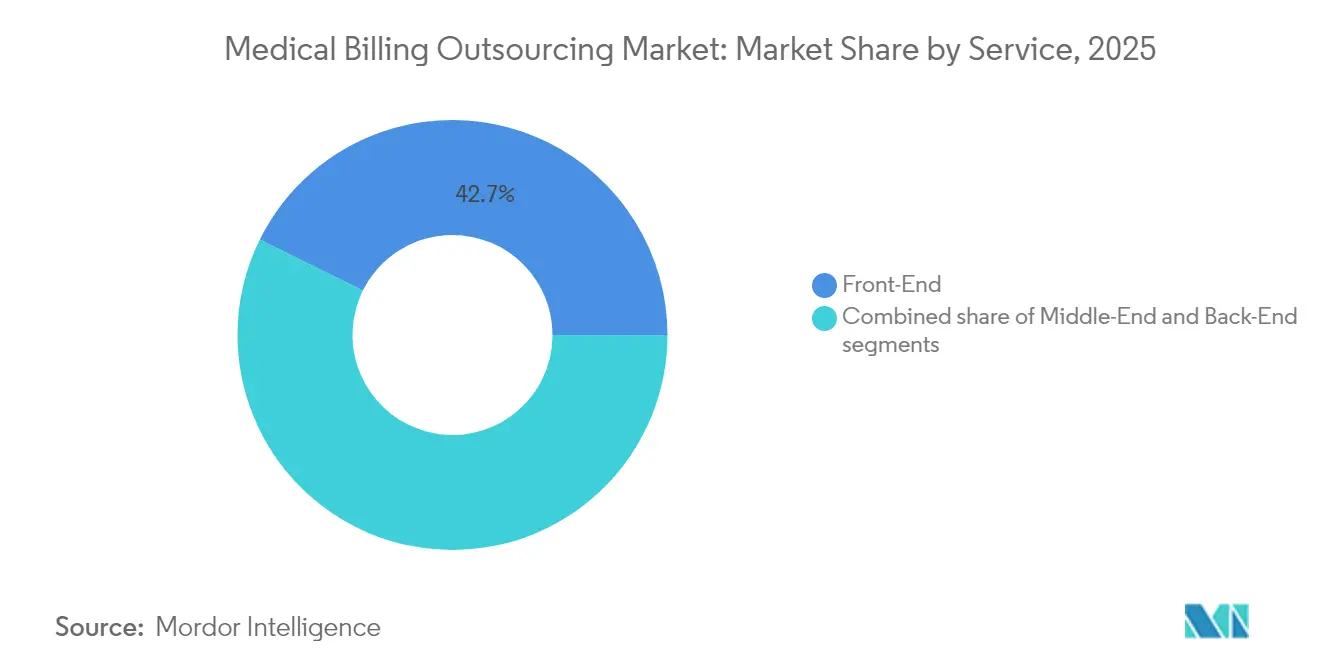

- By service, Front-End held 42.68% revenue in 2025, while Middle-End coding and claims processing are advancing fastest at 12.26% CAGR through 2031.

- By deployment, cloud-based delivery commanded 61.02% of the medical billing outsourcing market share in 2025 and is expanding at 11.84% CAGR.

- By end user, hospitals led with 55.74% share of the medical billing outsourcing market size in 2025; ambulatory/other providers register the top growth at 11.55% CAGR to 2031.

- By geography, North America contributed 49.21% revenue in 2025, whereas Asia Pacific posts the quickest 12.85% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Global Medical Billing Outsourcing Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising claim complexity & documentation burden | +2.1% | Global, with acute impact in North America & Europe | Medium term (2-4 years) |

| Surge in telehealth & digital-health billing volumes | +1.8% | North America & APAC core, spill-over to Europe | Short term (≤ 2 years) |

| Efforts to contain and decrease in-house processing costs | +2.3% | Global | Long term (≥ 4 years) |

| Climbing payor denial rates & audit intensity | +1.9% | North America & Europe primarily | Medium term (2-4 years) |

| Global coder workforce shortages | +1.7% | Global, most severe in North America | Long term (≥ 4 years) |

| Shift to value-based reimbursement models | +1.4% | North America leading, Europe following | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Claim Complexity & Documentation Burden

Coding rules continue to multiply, forcing providers to secure outside specialists who track every update and maintain year-round training programs. Outsourcing partners now supply AI-aided documentation tools that raise clean claim rates and shorten revenue cycles. As 46% of hospitals already use AI-enabled billing services, the medical billing outsourcing market gains strategic rather than tactical relevance.

Surge in Telehealth & Digital-Health Billing Volumes

Virtual visits require unique modifiers and cross-state eligibility checks that many internal teams cannot master quickly. Specialist vendors fill the gap, preventing revenue leakage by aligning telehealth codes with diverse payer rules. Demand spikes in North America and Asia Pacific help sustain double-digit growth for the medical billing outsourcing market.

Efforts to Contain In-House Processing Costs

Labor, software licensing and compliance overhead have pushed internal billing costs above sustainable thresholds. MGMA reports 36% of practice leaders intend to outsource in 2025 to lower cost per claim while boosting accuracy.[1]Source: MGMA Staff Members, “Automating and outsourcing medical practice revenue cycle management: Building partnerships for financial success,” MGMA, mgma.com Clients increasingly weigh total cost of ownership, which makes the medical billing outsourcing market the economically favorable route for both large systems and independent groups.

Climbing Payor Denial Rates & Audit Intensity

Tighter prior-authorization rules drive denials beyond what most business offices can overturn. Outsourced partners dedicate teams to appeals and root-cause prevention, improving first-pass acceptance and safeguarding cash flow. North American providers account for the bulk of this driver, yet European hospitals follow suit as audit scrutiny widens.

Restraints Impact Analysis of Global Medical Billing Outsourcing Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data-privacy & cybersecurity concerns | -1.2% | Global, most stringent in Europe & North America | Short term (≤ 2 years) |

| Increasing legislative and regulatory pressure | -0.9% | North America & Europe primarily | Medium term (2-4 years) |

| High costs of technology | -0.8% | Global, acute impact in emerging markets | Medium term (2-4 years) |

| In-house platform investments by large IDNs | -0.7% | North America & Europe, selective impact | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Data-Privacy & Cybersecurity Concerns

Proposed HIPAA Security amendments could cost the industry USD 9.3 billion in year one compliance, a burden likely to lift service prices and prompt closer vendor vetting.[2]Source: National Law Review Editors, “HHS Publishes Notice of Proposed Rulemaking to Amend HIPAA Security Rule Requirements,” natlawreview.com Larger third-party partners invest heavily in encryption and multi-factor authentication, yet some providers hesitate to place sensitive data off-premise, tempering short-term adoption in privacy-focused regions.

Increasing Legislative and Regulatory Pressure

No Surprises Act rules and price-transparency mandates add complexity for vendors that must update workflows across every payer. Smaller outsourcing firms sometimes lag, narrowing provider choices and raising switchover barriers. This uncertainty limits aggressive outsourcing plans until regulatory clarity stabilizes.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Global Medical Billing Outsourcing Market Segment Analysis

By Service:

Middle-End Billing Services AccelerateMiddle-End outsourcing grew at 12.26% CAGR and is poised to widen its contribution as coding precision defines net reimbursement. The segment’s 2024 expansion illustrates how clean-claim performance shapes the medical billing outsourcing market size for providers seeking immediate cash impacts. Artificial-intelligence coders funded by USD 40 million rounds demonstrate investor confidence.

Health systems report that AI-guided coding drives 96% first-pass rates against 88% for manual efforts, pushing more organizations toward specialist partners. Front-End tasks keep their 42.68% lead due to universal need for eligibility verification, but growth centers on Middle-End accuracy tools. Back-End collections remain essential for difficult balances, yet the medical billing outsourcing market increasingly markets full-cycle bundles anchored by coding excellence.

By Type of Deployment:

Cloud-Based Outsourcing DominatesCloud platforms captured 61.02% of 2025 revenue, reflecting provider demand for anywhere access and lower capital outlay. When paired with secure APIs into major EHR suites, cloud vendors shorten implementation to weeks, allowing faster gains in the medical billing outsourcing market.

Pandemic-era remote work validated the model, prompting even data-sensitive hospitals to shift roadmaps. Vendors answer breach concerns with zero-trust architectures, earning HITRUST certifications that on-premise rivals struggle to match. A 11.84% CAGR signals ongoing migration, with only mega-systems retaining on-premise hybrids where data-sovereignty mandates apply.

By End User:

Ambulatory Providers Drive Outsourcing AdoptionHospitals still generate 55.74% of 2025 revenue thanks to volume and service-line breadth, yet outpatient centers log the swiftest 11.55% CAGR. High procedure mix and multiple payer contracts stretch ambulatory revenue-cycle teams, turning them toward the medical billing outsourcing market for scalable help.

AI-driven denial tools tailored to ambulatory surgery coding now recover 9% previously lost income, tightening margins for in-house rivals. Physician groups also consolidate their billing with external partners that excel in value-based contract analytics, though growth runs steadier than the ambulatory surge.

Geography Analysis

North America Medical Billing Outsourcing Market

North America’s 49.21% revenue share in 2025 highlights providers’ reliance on external partners to navigate HIPAA updates and value-based payments. United States hospitals, burdened by rising denial volumes, choose vendors with specialized appeals teams and AI labs that push the medical billing outsourcing market forward. Canadian institutions align with cross-border firms now permitted to handle claims under modernized privacy pacts.

APAC Medical Billing Outsourcing Market

Asia Pacific’s 12.85% CAGR reflects dual momentum. Offshore centers in Manila and Bangalore process global claims at scale, while domestic hospitals in Japan, Australia and Southeast Asia adopt outsourcing to handle growing digital-health workloads. Government e-health initiatives raise documentation complexity, further lifting regional demand.

EMEA and South America Medical Billing Outsourcing Market

Europe remains a mature but evolving opportunity. GDPR shapes strict data-handling rules, favoring regional providers with compliant cloud setups. Providers use outsourcing to curb cost pressures tied to aging populations, keeping the medical billing outsourcing market stable. Middle East and Africa experience brisk growth off small bases as EHR penetration expands past 75% in GCC public hospitals. South America’s progress is uneven, slowed by economic swings yet buoyed by public-sector modernization programs in Brazil and Colombia.

Competitive Landscape

The sector shows moderate fragmentation with quickening consolidation. R1 RCM’s USD 8.9 billion sale to TowerBrook and CD&R underlines private-equity faith in the medical billing outsourcing market.[3]Source: R1 RCM, “R1 RCM to be Acquired by TowerBrook and CD&R for $8.9 Billion,” r1rcm.com Scale players pursue tuck-in buys for specialty coding or regional language capacity, driving steady concentration.

Technology stakes dominate rivalry. Providers integrate AI that lowers manual touches by 40% and raises coding precision to 98%. Thoughtful AI, Adonis and Amperos Health collectively secured more than USD 50 million since 2024 to automate denial prevention. Traditional health-IT vendors, including EHR giants, bundle revenue-cycle services to lock in clients seeking end-to-end solutions.

Strategic focus now turns to vertical specializations such as telehealth billing and oncology coding. Vendors able to deliver predictive analytics for value-based contracts win long-term deals. The top five firms process an estimated 80% of outsourced North American hospital revenue, indicating rising entry barriers and steady gains for incumbents.

Global Medical Billing Outsourcing Industry Leaders

Mckesson Corporation

EClinicalWorks

R1 RCM, Inc.

Kareo, Inc.

Allscripts (Veradigm)

- *Disclaimer: Major Players sorted in no particular order

Global Medical Billing Outsourcing Market Companies Covered in this Report

- R1 RCM

- Optum / Change Healthcare

- Allscripts (Veradigm)

- Cerner (Oracle Health)

- GE Healthcare

- eClinicalWorks

- Experian Health

- Genpact

- Kareo Inc.

- Mckesson

- Quest Diagnostics

- The SSI Group

- Conifer Health Solutions

- GeBBs Healthcare Solutions

- Athenahealth

- AdvantEdge Healthcare Solutions

- Firstsource Solutions

- 247 MBS

Read Analysis of Global Medical Billing Outsourcing Companies

Recent Industry Developments in Global Medical Billing Outsourcing Market

- June 2025: Amperos Health raised USD 4.2 million for its Amanda AI billing platform targeting denial reduction.

- May 2025: R1 received funding from Khosla Ventures to advance automated outsourcing capabilities.

- May 2025: Infinx acquired i3 Verticals’ healthcare billing wing, expanding its AI-driven services.

Global Medical Billing Outsourcing Market Report Scope and Research Methodology

Market Definition and Coverage

Our study defines the medical billing outsourcing market as all third-party services that manage claim preparation, submission, and follow-up on behalf of healthcare providers, capturing fees earned for front, middle, and back-end revenue-cycle tasks.

Scope exclusion: purely in-house software licenses and standalone clearinghouse networks are not counted.

Segments Covered in This Report

- By Service

- Front-End

- Middle-End

- Back-End

- By Type of Deployment

- On-Premise

- Cloud-based

- By End User

- Hospitals

- Physicians’ Offices

- Ambulatory/Other Providers

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Primary Research

We interview billing service executives, hospital CFOs, practice managers, and RCM consultants across North America, Europe, and Asia Pacific to cross-check adoption mixes, price points, and forecast assumptions. Targeted surveys gauge average outsourcing penetration among midsize physician groups, closing gaps left by secondary sources.

Desk Research

Mordor analysts first compile macro and sector datasets from free, high-credibility bodies such as the Centers for Medicare & Medicaid Services, American Medical Association, Healthcare Financial Management Association, World Health Organization, and national statistics portals. Company filings, investor decks, trade-press archives in Dow Jones Factiva, and patent trends in Questel help us verify vendor shares and technology shifts. Cost-per-claim statistics, denial rates, coder workforce data, and cloud-adoption figures are pulled from open HFMA surveys and CMS rulebooks, then aligned into a single evidence pack. This list is illustrative; many additional public and paid references underpin our desk work.

Market-Sizing & Forecasting

A blended top-down and bottom-up model anchors the 2025 baseline. Top-down reconstruction starts with national health-care expenditure and claims volumes, adjusts for the share processed externally, and multiplies by sampled average service fees. Select bottom-up roll-ups of leading outsourcers' revenues, validated through D&B Hoovers profiles and channel checks, test the totals. Key variables include annual professional claim submissions, average denial rate, coder salary inflation, EHR adoption growth, payer mix shifts, and regional healthcare spend. Multivariate regression with scenario analysis projects 2026-2030 values, letting us flex assumptions around regulatory change or staffing shortages. Where vendor disclosures are partial, sampled ASP times volume estimates fill gaps before final reconciliation.

Data Validation & Update Cycle

Every draft model runs through variance scans versus external metrics and peer signals; anomalies trigger re-checks with sources. Two-stage analyst reviews precede sign-off. Reports refresh yearly, with mid-cycle revisions for material events so clients receive an up-to-date view.

How Mordor Intelligence's Global Medical Billing Outsourcing Market Size Compares to Other Published Estimates

Published estimates often diverge because firms pick different revenue pools, unit prices, and refresh cadences.

Key gap drivers include whether in-house clearinghouse software is folded into totals, how aggressively telehealth coding is extrapolated, and if region-specific ASPs are applied or a single global average is used. Mordor's disciplined scope, variable vetting, and annual updates keep our baseline tightly aligned with observable provider spend.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 10.99 B | Mordor Intelligence | - |

| USD 16.59 B | Global Consultancy A | Includes software license revenues and telehealth coding bundles without separating overlap |

| USD 18.20 B | Industry Association B | Relies solely on provider spend survey; lacks reconciliation with claims and fee data |

| USD 19.32 B | Trade Journal C | Uses vendor press releases and updates biennially, creating timing and scope drifts |

In sum, by pairing transparent source hierarchies with repeatable modeling steps and tight scope control, Mordor Intelligence delivers a balanced, decision-ready baseline that users can trace, question, and reproduce with confidence.

Key Questions Answered in the Report

What primary forces are prompting healthcare providers to shift billing work to external partners?

Escalating coding complexity, higher payor denial rates, and persistent workforce shortages have convinced many organizations that specialized vendors can protect revenue, accelerate collections, and reduce administrative strain better than in-house teams.

How are artificial intelligence and automation reshaping vendor selection in medical billing outsourcing?

Providers increasingly favor partners that embed AI for coding assistance, denial prediction, and robotic claim submission because these tools deliver cleaner claims, faster appeals, and lower processing costs without expanding internal labor.

Why are ambulatory surgery centers adopting outsourcing more quickly than other settings?

Outpatient facilities face diverse payer rules and procedure-specific codes that change frequently; outsourcing firms with specialty expertise relieve staff from constant updates and help centers focus on clinical throughput.

What influence do evolving cybersecurity requirements have on outsourcing decisions?

Stricter data-privacy mandates push providers to vet vendors’ encryption, authentication, and monitoring capabilities; those able to demonstrate rigorous compliance and rapid incident response win contracts over less security-mature competitors.

Which deployment model is becoming the preferred option for outsourced billing services and why?

Cloud-based delivery is favored because it integrates smoothly with existing electronic health records, supports remote work, scales on demand, and shifts maintenance responsibilities to the vendor, freeing providers from costly infrastructure upgrades.

How is ongoing consolidation among billing vendors shaping the competitive landscape?

Acquisitions are producing larger firms that offer end-to-end revenue-cycle suites, deeper specialty knowledge, and broader geographic coverage, raising the bar for smaller competitors and giving providers single-source partners for multiple billing needs.

Page last updated on: