Medical Talent Management IT Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

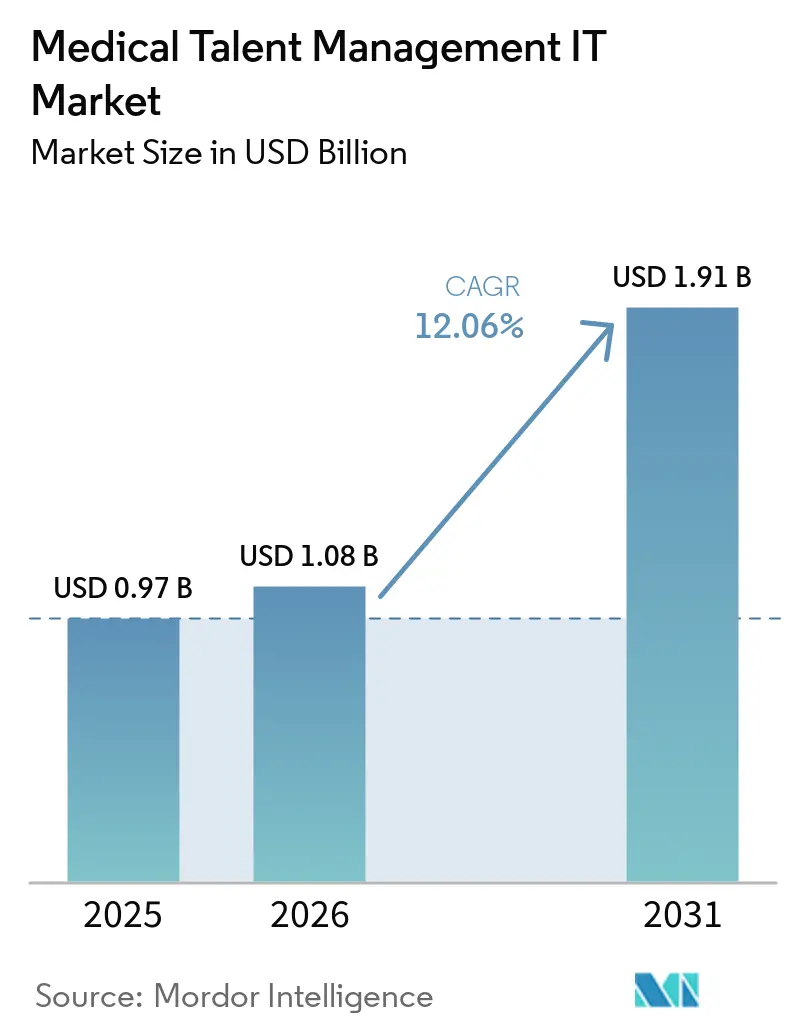

| Market Size (2026) | USD 1.08 Billion |

| Market Size (2031) | USD 1.91 Billion |

| Growth Rate (2026 - 2031) | 12.06% CAGR |

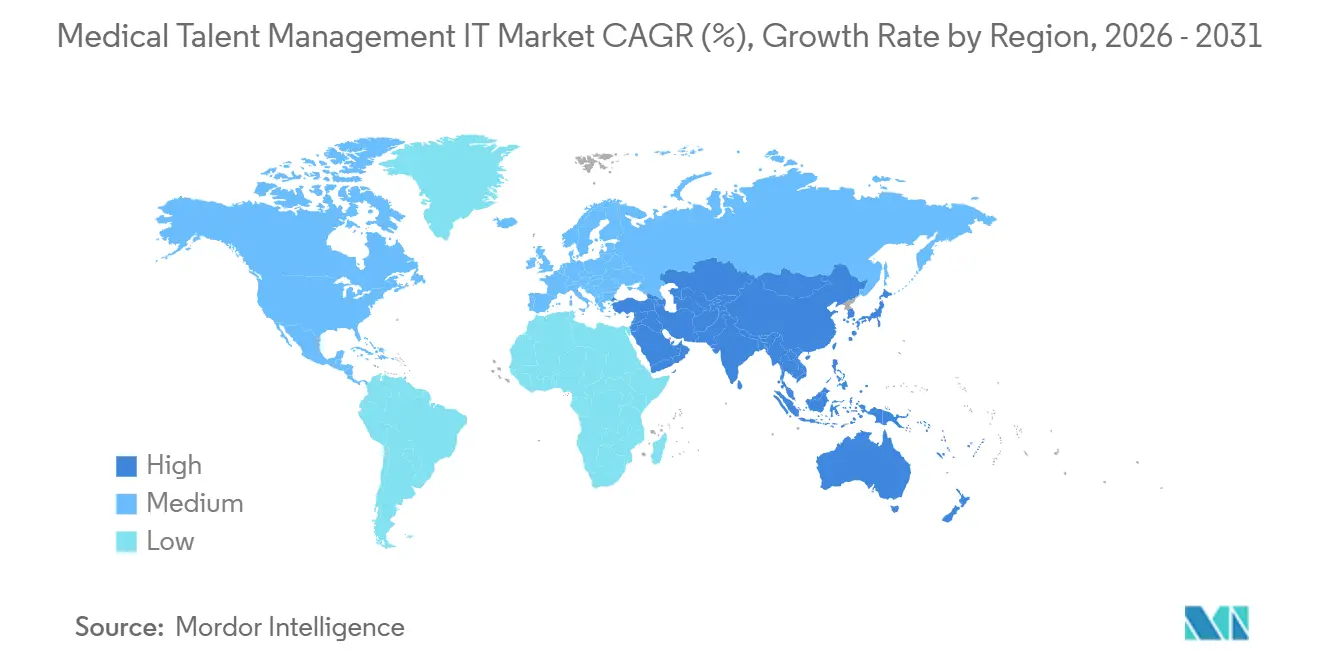

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

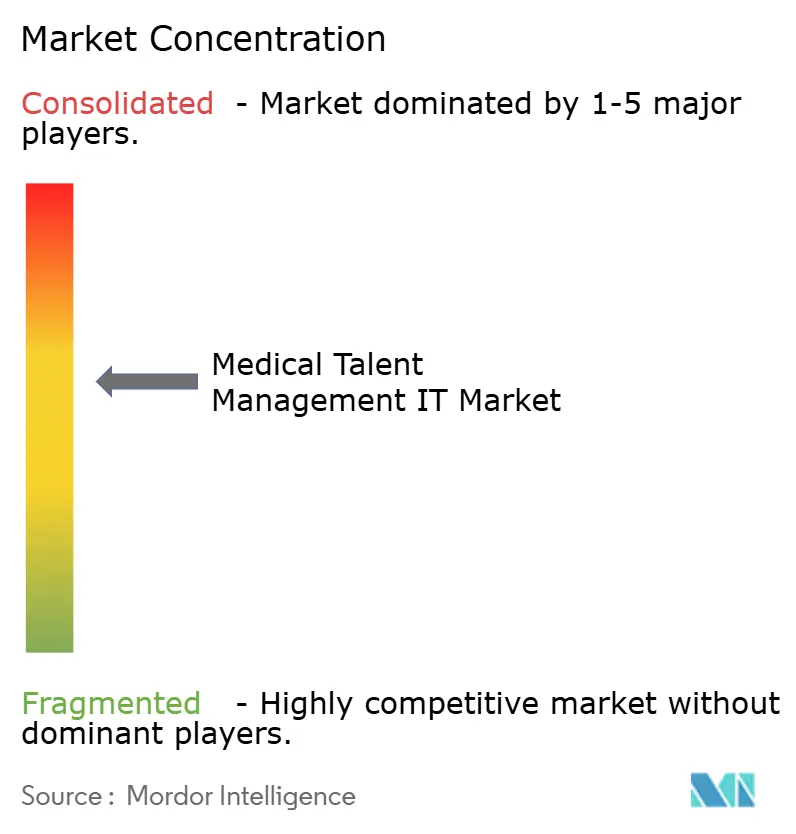

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Medical Talent Management IT Market Analysis by Mordor Intelligence

The Medical Talent Management IT Market size was valued at USD 0.97 billion in 2025 and is estimated to grow from USD 1.08 billion in 2026 to reach USD 1.91 billion by 2031, at a CAGR of 12.06% during the forecast period (2026-2031).

Persistent workforce shortages, fast-rising cloud adoption, and intensifying compliance mandates are pushing hospitals and other care providers to treat talent platforms as strategic infrastructure rather than back-office software [1]Health Resources and Services Administration, “Projecting Health Workforce Supply and Demand,” hrsa.gov. Labor costs account for up to 60% of hospital operating expenses, so even a modest productivity gain from automated scheduling or real-time credentialing creates measurable budget relief. Cloud deployment already accounts for a significant share, reshaping procurement toward subscription models that bundle cybersecurity, uptime SLAs, and continuous feature updates into a single price. Platform choice is now driven less by feature checklists and more by a vendor’s ability to integrate recruiting, scheduling, learning, and credentialing in one workflow that eliminates swivel-chair data entry between HR, EHR, and payroll systems.

Key Report Takeaways

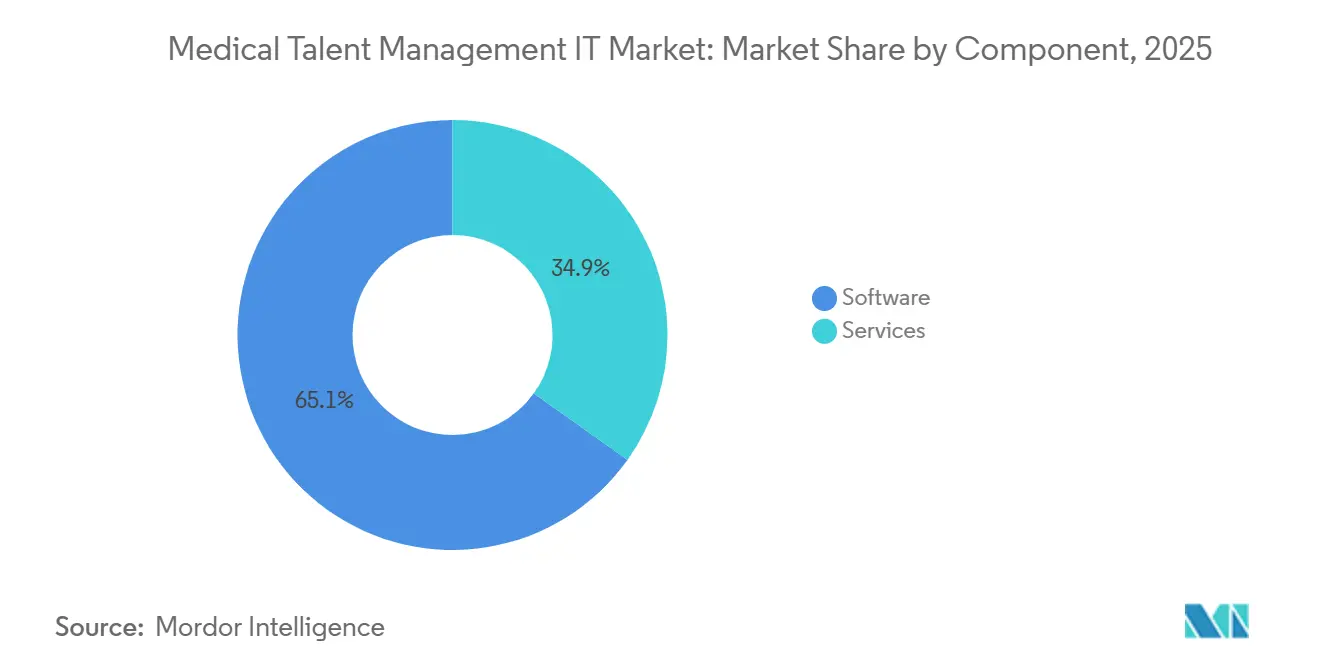

- By component, software led with 65.12% of the Medical talent management IT market share in 2025, while services are advancing at a 14.78% CAGR through 2031.

- By deployment, the web/cloud-based segment led the Medical talent management IT market with 59.24% market share in 2025 and is expected to grow at a CAGR of 15.61% by 2031.

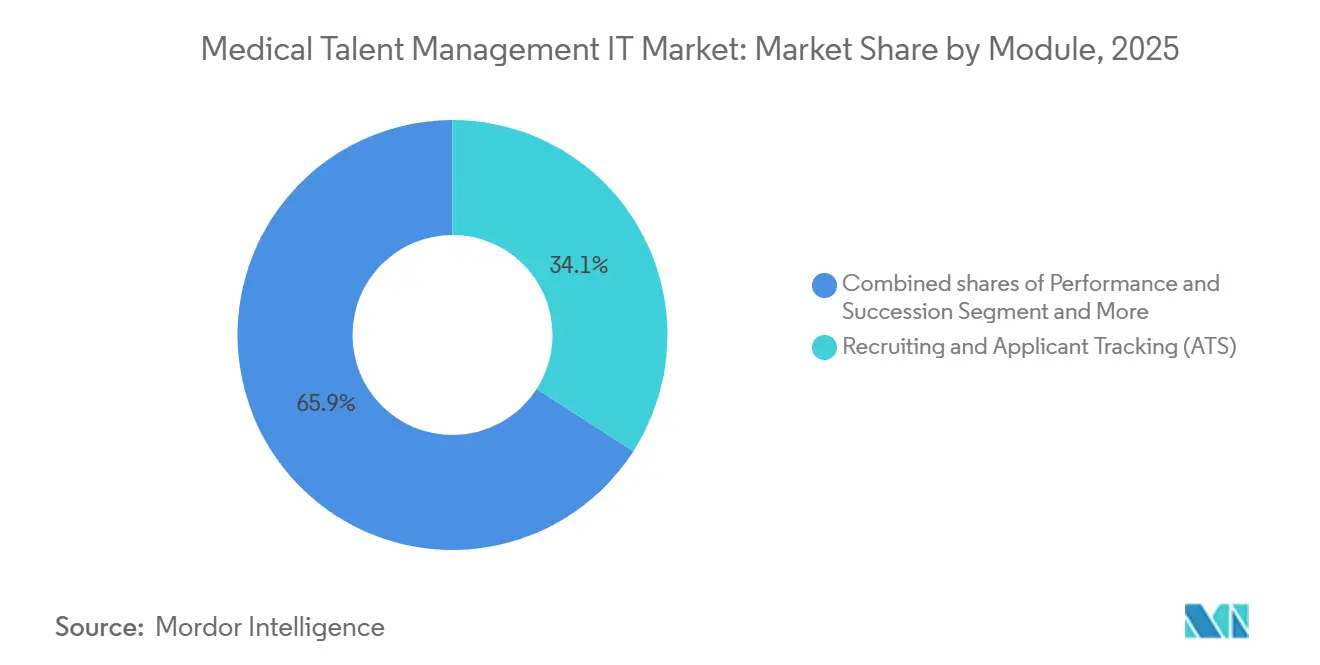

- By module, recruiting and applicant tracking accounted for 34.09% of revenue in 2025, and learning & compliance are projected to grow at a 16.21% CAGR through 2031.

- By end user, hospitals and health systems accounted for 45.09% of revenue in 2025; ambulatory/clinics & physician groups are the fastest-growing end-user segment at a 13.41% CAGR through 2031.

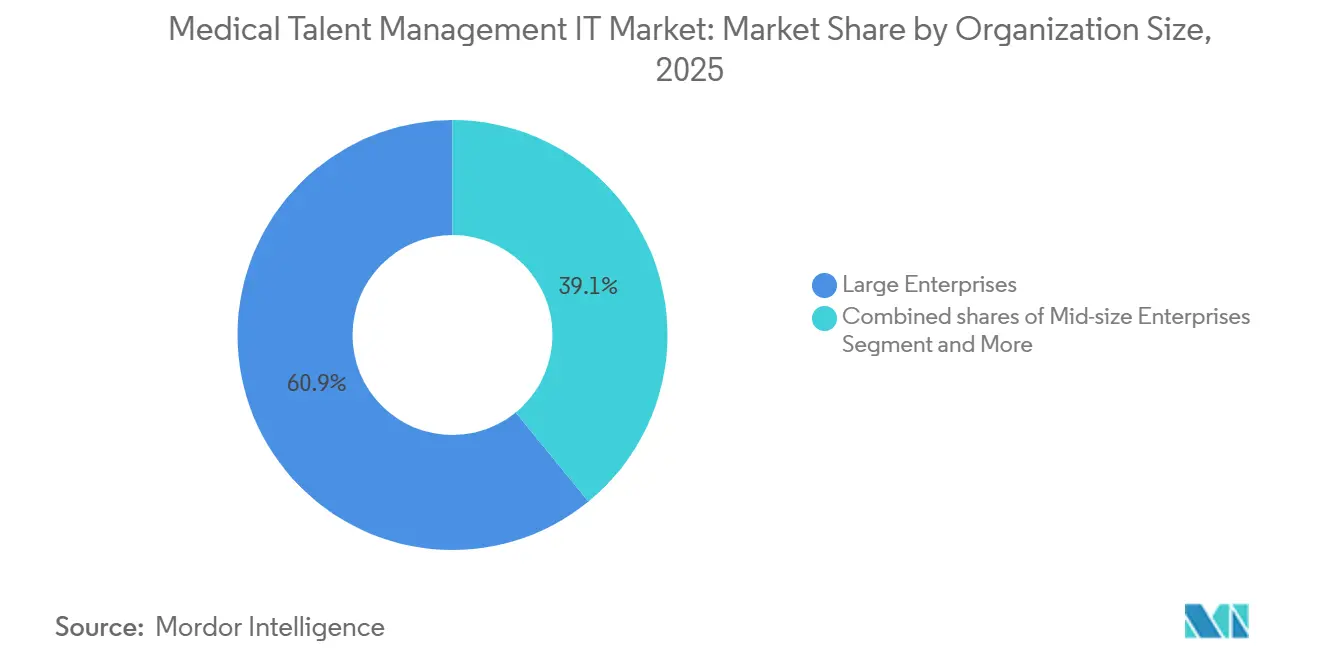

- By organization size, large enterprises accounted for 60.89% of revenue in 2025, and mid-sized enterprises are projected to grow at a 14.31% CAGR to 2031.

- By geography, North America commanded 45.23% value in 2025, whereas Asia-Pacific is forecast to expand at a 14.13% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Medical Talent Management IT Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Workforce shortages and labor cost pressure intensify adoption of recruiting, scheduling, retention and analytics tools | +3.2% | Global, acute in North America and Europe | Medium term (2-4 years) |

| Cloud-first and AI-enabled workforce analytics/scheduling accelerate modernization | +2.8% | Global, led by North America and Asia-Pacific | Short term (≤ 2 years) |

| Compliance-driven training and competency tracking (HIPAA, TJC) embed LMS usage | +1.9% | North America, expanding to Europe and Middle East | Long term (≥ 4 years) |

| Value-based care models driving workforce productivity and cost-per-outcome analytics | +1.8% | North America and Europe, early adoption in Asia-Pacific | Medium term (2-4 years) |

| PBJ staffing-data enforcement in long-term care accelerates time/attendance and scheduling digitization | +1.6% | United States (federal mandate), spillover to Canada | Medium term (2-4 years) |

| NCQA credentialing/delegation tightening (shorter verification windows, continuous monitoring) catalyzes credentialing automation | +1.4% | North America, payer-driven markets globally | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Workforce Shortages and Labor Cost Pressure Intensify Adoption of Recruiting, Scheduling, Retention and Analytics Tools

Global nurse and allied-health shortfalls continue to widen, with the United States alone projecting a gap of 108,960 registered nurses by 2038. Hospitals already devote more than half of their operating budgets to labor, so CFOs are prioritizing predictive turnover models and AI-driven scheduling that can redeploy staff hours toward direct patient care. Real-time analytics that flag likely resignations 90 days in advance allow managers to intervene early with coaching or shift-pattern adjustments, which costs roughly one-tenth of back-filling an open role. Such tools convert talent systems from administrative record keepers into frontline operational dashboards that directly affect throughput and quality metrics. As value-based reimbursement expands, executives increasingly tie staffing optimization projects to readmission penalties and patient-experience bonuses, cementing budget support for Medical talent management IT market investments.

Cloud-First and AI-Enabled Workforce Analytics/Scheduling Accelerate Modernization

The Change Healthcare cyberattack in 2024 demonstrated that single-vendor or on-premise architectures create systemic risk when payroll and credentialing feeds are disrupted for weeks. Consequently, cloud deployment has become the default procurement model for mid-sized and community hospitals that lack the resources for round-the-clock security monitoring. Multi-site systems are layering AI algorithms on top of cloud databases to adjust staffing to live census and acuity scores, trimming overtime hours by double-digit percentages in the first six months after go-live. Increasingly, vendors emphasize shift-preference prediction rather than résumé screening because granular scheduling improvements yield faster ROI and avoid bias litigation concerns. As a result, the Medical talent management IT market sees cloud-native releases arriving quarterly, shortening innovation cycles and reinforcing subscription revenue growth.

Compliance-Driven Training and Competency Tracking Embed LMS Usage

The Joint Commission’s 2024 standards overhaul added 18 new competencies that must be documented for every clinical role, turning learning-management systems into audit-defense linchpins. Hospitals that automate role-based course assignment and send escalating reminders cut accreditation findings tied to staff education by 40% versus manual tracking. Mobile micro-learning modules—three-minute updates on revised sepsis bundles, for example, achieve completion rates near 80%, far outperforming traditional one-hour annual refreshers. Because penalties for non-compliance can exceed software license fees, boards now treat LMS outlays as risk-mitigation spend that protects both revenue and brand.

NCQA Credentialing/Delegation Tightening Catalyzes Credentialing Automation

NCQA now mandates primary-source verification within 120 days and continuous license monitoring, compressing timelines that manual spreadsheets cannot meet [2]National Committee for Quality Assurance, “Credentialing and Delegation Standards 2024,” ncqa.org. Automated credentialing platforms pull nightly feeds from state boards and the National Practitioner Data Bank, cutting time-to-panel from 120 to 45 days and preventing payer denials tied to lapsed documents. Because a single day of enrollment delay translates into lost billing, CFOs now fund credentialing automation from revenue-cycle budgets instead of HR line items. Health systems that implement real-time credential monitoring report fewer denied claims, highlighting a direct earnings benefit that accelerates platform adoption.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cybersecurity/privacy risk and HIPAA compliance costs slow rollouts | -1.2% | Global, acute in North America and Europe | Short term (≤ 2 years) |

| Integration complexity with EHR/HR/payroll ecosystems raises implementation burden | -0.9% | Global, concentrated in multi-vendor environments | Medium term (2-4 years) |

| Budget constraints and competing IT priorities delay workforce platform investments | -0.8% | Global, pronounced in small and mid-size organizations | Short term (≤ 2 years) |

| Policy volatility around LTC staffing minimums reduces compliance-driven urgency in nursing homes | -0.6% | United States, state-level variation | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Cybersecurity/Privacy Risk and HIPAA Compliance Costs Slow Rollouts

Healthcare experienced 725 reportable breaches in 2024, with an average cost of USD 10.93 million per incident [3]U.S. Department of Health and Human Services, “Breach Portal,” hhs.gov. Talent platforms store personal identifiers, disciplinary notes, and Social Security numbers, high-value data that attract ransomware gangs. Mid-size vendors must spend up to USD 300,000 annually to maintain HITRUST or SOC 2 certifications, eroding product-development budgets and limiting their ability to enter new Medical talent management IT market niches. Some health systems, therefore defer full-suite migration, keeping core HR or payroll on-premise while selectively adopting cloud modules only where clear ROI outweighs risk.

Integration Complexity with EHR/HR/Payroll Ecosystems Raises Implementation Burden

A 400-bed hospital maintains roughly 16 enterprise systems, and every additional interface multiplies error paths that can delay paychecks or create duplicate employee IDs. Workforce data, such as shift preferences or competency scores, lack standardized HL7-FHIR resources, requiring custom APIs that break when any upstream vendor releases a major update. Overruns are common; two-thirds of integration projects overshoot timelines by at least six months, causing budget fatigue and stakeholder frustration. As a defensive measure, some CIOs choose native workforce modules from their incumbent EHR supplier even when independent products offer richer features, reinforcing vendor lock-in across the Medical talent management IT industry.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Gain Momentum as Complexity Trumps Licensing

Software accounted for 65.12% of 2025 spending, yet services revenue is forecast to rise at a 14.78% CAGR through 2031, outpacing software growth in the Medical talent management IT market. Implementation, data migration, and change management consulting now account for a significant share of total project costs for large health systems as they consolidate disparate ATS, LMS, and scheduling products into unified suites.

Managed services, where a vendor operates credentialing or scheduling on the client’s behalf, are expanding fastest, converting one-time projects into recurring contracts that smooth revenue. Oracle’s workforce-as-a-service bundle embeds certified credentialing specialists within hospital teams and shifts platform administration off IT’s plate, signaling a broader move toward outcome-based pricing. The transition reshapes vendor profitability models, rewarding companies that pair software IP with deep domain expertise rather than pure-play code bases.

By Deployment: Cloud Uptake Surges, Yet On-Premises Holds in Regulated Pockets

Web and cloud implementations accounted for 59.24% of total installations in 2025 and are projected to grow at a 15.61% CAGR, reflecting buyer preference for subscription economics and vendor-managed security updates in the Medical talent management IT market. Community hospitals cite the inability to recruit cybersecurity talent as a top reason for exiting on-premises data centers.

Even so, a significant number of deployments remain on-premise, especially in academic medical centers, federal institutions, and regions with strict data-residency laws. Germany’s Cloud Compliance Controls Catalogue, for instance, requires credential files to be stored within EU borders, prompting hybrid architectures that store sensitive documents locally while sending anonymized scheduling data to the cloud for machine learning optimization. Vendors now offer containerized versions of their SaaS code bases, letting customers switch between hosting models without functional trade-offs

By Module/Function: Recruiting Leads Revenue; Credentialing and Analytics Post Fastest Growth

Recruiting and ATS modules accounted for 34.09% of 2025 revenue, and Learning & Compliance is expected to expand at a 16.21% CAGR. Turnover among hospital nurses grew significantly in 2024, pushing HR teams to modernize job-posting, candidate-scoring, and interview-scheduling workflows to cut time-to-fill. Learning and compliance systems rank second, cemented by HIPAA and Joint Commission mandates.

Credentialing and payer-enrollment tools are the Medical talent management IT market’s breakout categories, expected to grow significantly through 2031 as NCQA shortens verification windows. Workforce analytics remains a smaller but strategic segment: dashboards linking labor cost to patient outcomes attract CFO oversight and justify platform expansions. Scheduling and time-attendance suites benefit from CMS staffing rules in long-term care, fueling double-digit growth where paper timecards cannot generate compliant PBJ files.

By End User: Hospitals Remain Dominant while Home-Based Care Accelerates

Hospitals and integrated delivery networks generated 45.09% of revenue in 2025, reflecting their scale and regulatory exposure. They purchase integrated suites that cover the entire employee lifecycle, seeking to harmonize thousands of job codes across multiple campuses.

Conversely, ambulatory/clinics & physician groups represent the Medical talent management IT market’s fastest-growing niche at 13.41% CAGR. Value-based care incentives have shifted high-acuity episodes out of inpatient wards into domiciliary settings, where mobile apps must verify caregiver credentials and timestamps of visits in real time. Behavioral health organizations also quicken adoption to manage cross-state licensing and high counselor turnover.

By Organization Size: Large Enterprises Lead Spend, Mid-Size Firms Lead Growth

Large health systems captured 60.89% of 2025 sales, but mid-size enterprises are expanding at a 14.31% CAGR, slightly below that of smaller cohorts. Complex unions, multiple EHRs, and legacy payroll engines elongate deployment cycles, so large buyers emphasize configurable workflows that escalate professional-services costs.

Mid-size and community providers adopt modular cloud bundles that can be live in under 90 days, achieving faster payback and accelerating the Medical talent management IT industry’s penetration curve. Vendors are experimenting with AI-driven “configuration-light” templates that auto-generate approval chains based on organization type, shrinking the historical gap in implementation timelines between small and large enterprises.

Geography Analysis

North America generated 45.23% revenue in 2025 as CMS staffing mandates and HIPAA security rules forced providers to digitize scheduling, learning, and credentialing workflows. U.S. health systems increasingly embed workforce analytics into board-level dashboards, framing them as levers for margin expansion amid inflationary labor markets. Canada’s provincial fragmentation slows national roll-outs, yet a federal CAD 200 million allocation for interoperable provider registries is boosting demand for cloud credentialing platforms. Mexico’s private hospitals deploy bilingual recruiting portals to serve cross-border medical tourists, signaling a niche growth path for vendors fluent in both English and Spanish regulatory frameworks.

Europe contributed a significant share of the 2025 spending. Germany’s EUR 4.3 billion hospital digitization fund reimburses the majority of software costs, spurring rapid procurement but also reinforcing on-premise hosting preferences to meet GDPR residency clauses. The United Kingdom’s NHS Workforce Data Initiative centralizes staffing records for 1.3 million employees, pushing trusts to adopt standardized APIs for time-and-attendance and competency feeds. Southern European countries face budget constraints, so they favor open-source talent suites bundled with local integrator services.

Asia-Pacific is projected to grow at a 14.13% CAGR through 2031, the fastest among all regions in the Medical talent management IT market. China aims to license 1 million new general practitioners by 2030, requiring mass-scale credentialing automation across provincial health bureaus. India’s National Digital Health Mission sets interoperability guidelines that indirectly compel provider organizations to adopt cloud credentialing and scheduling to participate in government reimbursement programs. Japan’s aging workforce drives AI-based scheduling pilots that match nurse skills to geriatric-care acuity scores, while Australia and South Korea prioritize telemedicine credential validation to sustain cross-jurisdiction video consultations.

Competitive Landscape

The Medical talent management IT market remains moderately concentrated, with the top five suppliers holding significant combined revenue in 2025. Oracle Health offers the only fully integrated EHR-to-workforce suite, yet protracted post-merger integration has enabled niche specialists such as QGenda and symplr to gain share in physician scheduling and credentialing, respectively. Workday and SAP SuccessFactors bundle talent modules at zero incremental license cost when health systems buy financial or supply-chain suites, trading software margin for account lock-in.

Pure-play vendors differentiate through depth: HealthStream’s Joint Commission-aligned course catalog and Relias’ competency mapping deter customer churn because migrating historical learning records into a new system risks non-compliance. Emerging disruptors focus on AI-native features like automated shift swapping and burnout prediction, but large buyers proceed cautiously amid uncertainty over algorithmic bias. Federal opportunities are opening as Infor and Microsoft deploy FedRAMP High-authorized instances for Veterans Affairs facilities, a sector worth an estimated USD 300 million over five years.

Behavioral health, home health, and payer credentialing stand out as white-space segments where no incumbent commands double-digit share. Vendors able to plug into dominant EHRs (Epic, Oracle Health) and dominant payroll engines (ADP, Ceridian) without custom code gain a distribution advantage, because CIOs increasingly treat seamless interoperability as the top buying criterion. Price competition centers on professional-services day rates rather than subscription fees, underscoring the shift toward services-heavy revenue models.

Medical Talent Management IT Industry Leaders

Oracle Health

QGenda

Symplr

HealthStream

Ceridian

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Oracle invested USD 150 million to embed real-time acuity data into its scheduling engine, enabling dynamic nurse-to-patient ratios across multi-hospital networks.

- January 2026: Workday integrated its scheduling module inside Epic’s EHR UI, trimming shift-assignment time by 35% during a 12-site pilot.

- November 2025: Ceridian (Dayforce) acquired HealthcareSource for USD 425 million, adding pre-built clinician hiring workflows.

Global Medical Talent Management IT Market Report Scope

| Software |

| Services |

| Web/Cloud-based |

| On-premise |

| Recruiting & Applicant Tracking (ATS) |

| Learning & Compliance (LMS/LXP; CE tracking) |

| Performance & Succession |

| Compensation & Benefits |

| Scheduling & Time & Attendance |

| Credentialing & Payer Enrollment |

| Workforce Analytics |

| Hospitals & Health Systems |

| Ambulatory/Clinics & Physician Groups |

| Long-term Care / Skilled Nursing |

| Behavioral Health |

| Home Health & Hospice |

| Payers / Health Plans (credentialing-focused) |

| Large Enterprises |

| Mid-size Enterprises |

| Small Enterprises |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Component | Software | |

| Services | ||

| By Deployment | Web/Cloud-based | |

| On-premise | ||

| By Module / Function | Recruiting & Applicant Tracking (ATS) | |

| Learning & Compliance (LMS/LXP; CE tracking) | ||

| Performance & Succession | ||

| Compensation & Benefits | ||

| Scheduling & Time & Attendance | ||

| Credentialing & Payer Enrollment | ||

| Workforce Analytics | ||

| By End User | Hospitals & Health Systems | |

| Ambulatory/Clinics & Physician Groups | ||

| Long-term Care / Skilled Nursing | ||

| Behavioral Health | ||

| Home Health & Hospice | ||

| Payers / Health Plans (credentialing-focused) | ||

| By Organization Size | Large Enterprises | |

| Mid-size Enterprises | ||

| Small Enterprises | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the Medical talent management IT market?

The market is valued at USD 1.08 billion in 2026 and is on track to reach USD 1.91 billion by 2031.

How fast is the Medical talent management IT market growing?

It is expanding at a 12.06% CAGR over 2026-2031, fueled by workforce shortages, cloud migration, and new compliance mandates

Which module holds the largest revenue share?

Recruiting and applicant tracking systems commanded 34.09% revenue in 2025, leading all other modules.

Which region is expected to grow the fastest?

Asia-Pacific is forecast to register a 14.13% CAGR through 2031 as China and India invest in large-scale credentialing and staffing systems.

Page last updated on: