Healthcare Content Management System Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

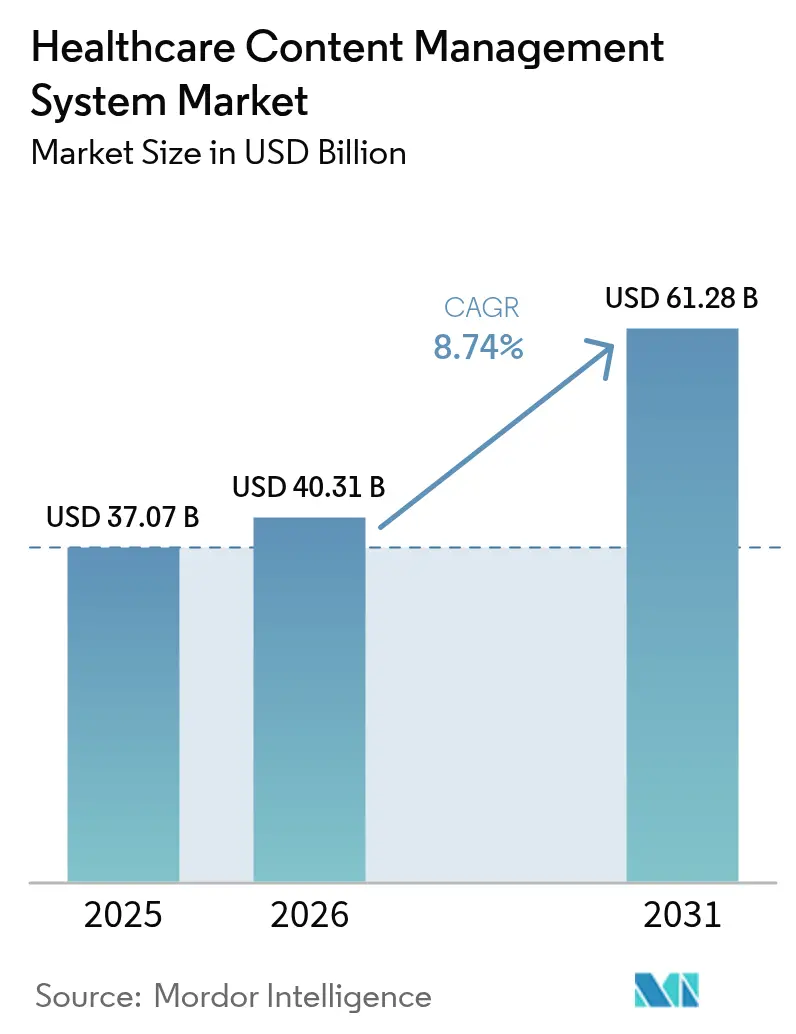

| Market Size (2026) | USD 40.31 Billion |

| Market Size (2031) | USD 61.28 Billion |

| Growth Rate (2026 - 2031) | 8.74% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Healthcare Content Management System Market Analysis by Mordor Intelligence

The healthcare content management system market size was valued at USD 37.07 billion in 2025 and estimated to grow from USD 40.31 billion in 2026 to reach USD 61.28 billion by 2031, at a CAGR of 8.74% during the forecast period (2026-2031). Rapid expansion reflects providers’ need to modernize document workflows in response to EHR-driven interoperability mandates, HIPAA/GDPR retention rules that extend data life cycles, and the cost advantages of cloud-based services over on-premise platforms. Added momentum comes from telehealth adoption, which requires real-time access to unstructured content, and from AI-enabled intelligent document processing that automates data capture from clinician notes and imaging reports. Competition intensifies as cloud-native disruptors challenge legacy vendors on scalability, security, and embedded analytics, pushing incumbents to invest in managed services and AI add-ons to defend share. Implementation skills shortages and rising compliance costs encourage healthcare organizations to outsource integration and support, which accelerates the services revenue pool relative to core software licenses. Collectively, these forces confirm a long-run shift from document repositories to cloud-delivered, workflow-centric, and AI-augmented platforms within the healthcare content management system market.

Key Report Takeaways

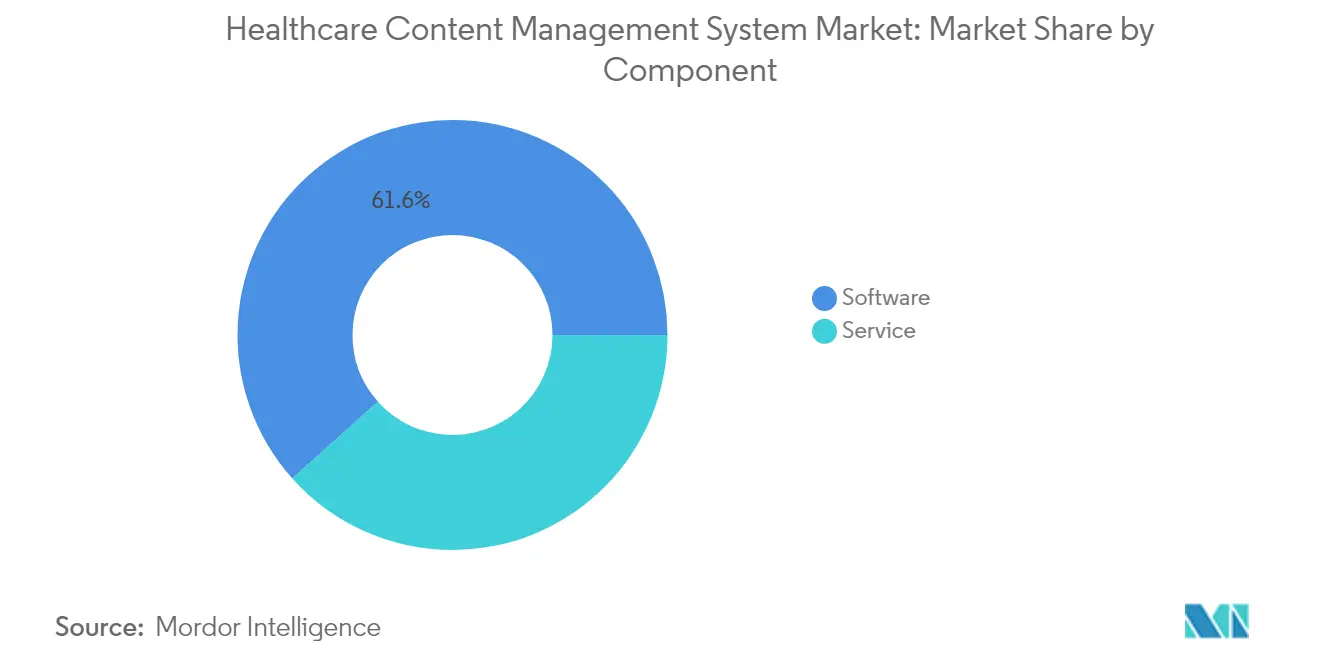

- By component, software commanded 61.62% of healthcare content management system market share in 2025, yet services are growing fastest at a 9.78% CAGR through 2031.

- By deployment mode, the cloud segment held 53.89% of 2025 revenue; hybrid cloud solutions are expanding at a 10.21% CAGR to 2031.

- By application, clinical content management accounted for a 40.74% share of the healthcare content management system market size in 2025, while AI-enabled intelligent document processing is advancing at an 10.58% CAGR.

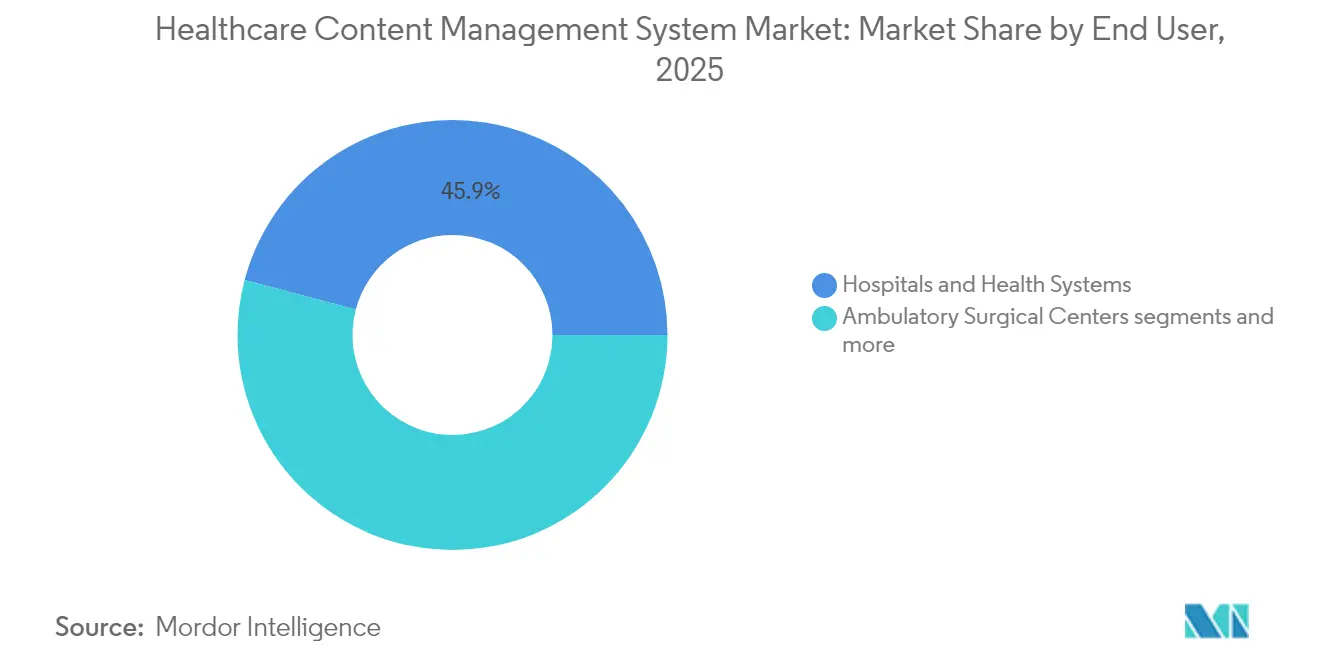

- By end user, hospitals and health systems led with 45.89% revenue share in 2025; payers are forecast to grow at an 10.92% CAGR through 2031.

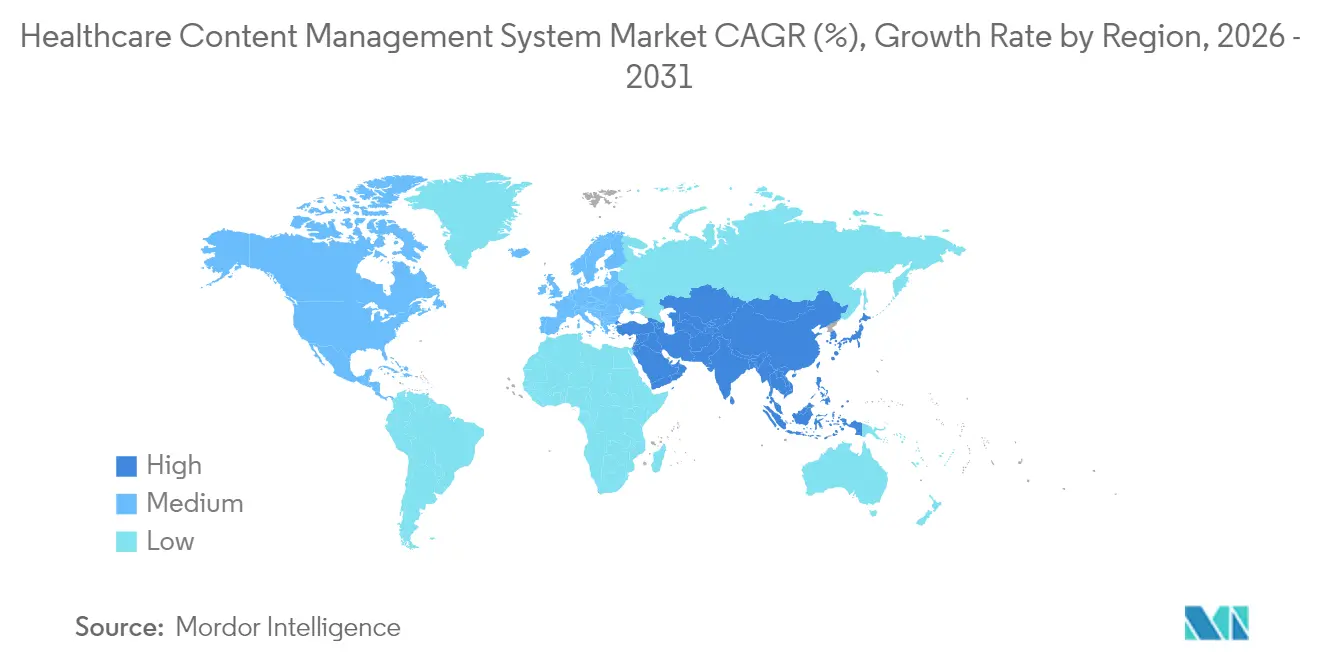

- By geography, North America captured 38.41% of 2025 revenue; Asia-Pacific is the fastest-growing region at an 11.32% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Healthcare Content Management System Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in EHR adoption mandates integrated document & imaging workflows | +2.1% | Global, with North America & EU leading compliance | Medium term (2-4 years) |

| Regulatory push for data retention & HIPAA/GDPR compliance | +1.8% | North America & EU primary, APAC emerging | Long term (≥ 4 years) |

| Shift from on-premise to cloud content services lowering TCO | +1.6% | Global, with enterprise adoption in developed markets | Short term (≤ 2 years) |

| Rising telehealth & remote workforce needs real-time content access | +1.4% | Global, accelerated in rural and underserved regions | Medium term (2-4 years) |

| AI-powered Intelligent Document Processing unlocks unstructured clinical data | +1.2% | North America & APAC core markets | Long term (≥ 4 years) |

| Value-based care contracts require longitudinal patient content repositories | +1.0% | North America primary, EU secondary adoption | Long term (≥ 4 years |

| Source: Mordor Intelligence | |||

Surge in EHR Adoption Mandates Integrated Document & Imaging Workflows

The 21st Century Cures Act’s interoperability deadlines now link Medicare reimbursements to seamless data exchange, driving providers to embed imaging and document management directly inside core EHR workflows[1]Source: Centers for Medicare & Medicaid Services, “Calendar Year 2024 Program Requirements,” cms.gov . Hospitals running Epic or Oracle Health increasingly demand vendor-neutral archives and FHIR-based repositories, forcing content management vendors to swap proprietary interfaces for open APIs that satisfy Merit-based Incentive Payment System metrics. This realignment elevates the healthcare content management system market from compliance utility to clinical workflow enabler, reshaping competitive priorities around latency, embedded analytics, and clinician user experience[2]Source: Journal of Medical Internet Research, “25 Years of EHR Implementation,” jmir.org.

Regulatory Push for Data Retention & HIPAA/GDPR Compliance

HIPAA’s six-year minimum retention rule, coupled with state mandates that stretch to ten years, obligates U.S. providers to maintain scalable archives with automated deletion policies, encryption, and audit trails. Across the EU, GDPR adds “right-to-erasure” and data residency provisions that require granular lifecycle controls, steering multinational health systems toward cloud vendors offering region-specific storage nodes and policy engines hl7.org. As compliance complexity rises, buyers reward vendors that embed rules libraries and evidence logging, lifting average selling prices and locking in multiyear subscription contracts within the healthcare content management system market.

Shift from On-Premise to Cloud Content Services Lowering TCO

Academic medical centers report up to 95% infrastructure cost avoidance after retiring mainframe imaging archives in favor of cloud-based object storage and serverless processing. Predictable operating-expense models appeal to value-based care organizations, while automatic patching and disaster recovery satisfy looming HIPAA Security Rule encryption mandates without capital outlays. Consequently, the cloud slice of the healthcare content management system market continues to eclipse on-premise installations even as security assessments prolong procurement cycles.

Rising Telehealth & Remote Workforce Needs Real-Time Content Access

With telehealth stabilizing at 23% of total encounters, clinicians require instant retrieval of longitudinal records from mobile devices and home offices. Persistent workforce shortages push administrative teams to remote models, expanding VPN traffic and elevating zero-trust security in content repositories. Systems that combine federated search, automated redaction, and role-based access win deals where providers must balance accessibility with HIPAA compliance across distributed care settings

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront migration & integration costs with legacy systems | -1.5% | Global, particularly acute in resource-constrained markets | Short term (≤ 2 years) |

| Data security & privacy concerns slowing cloud deployments | -1.2% | Global, with heightened sensitivity in regulated markets | Medium term (2-4 years) |

| Vendor lock-in risk limits interoperability across imaging platforms | -0.9% | North America & EU, where Epic dominance creates challenges | Long term (≥ 4 years) |

| Shortage of health-IT staff skilled in metadata governance | -0.7% | Global, most severe in APAC and emerging markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Upfront Migration & Integration Costs with Legacy Systems

Full-scale data conversion, interface development, and user re-training push typical six-month deployments beyond USD 10 million for large health systems, delaying ROI and depressing near-term healthcare content management system market spending. Although cloud pay-as-you-go pricing offsets hardware purchases, parallel-run periods inflate labor costs until legacy systems fully sunset.

Data Security & Privacy Concerns Slowing Cloud Deployments

Ransomware attacks against U.S. hospitals rose 94% in 2024, reinforcing board-level scrutiny on off-premise storage and extending vendor due-diligence cycles by months. Shared-responsibility confusion and cross-border residency rules further limit multi-national rollouts, tempering the otherwise strong cloud-driven growth of the healthcare content system management market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Growth Outpaces Software Dominance

In 2025, software contributed USD 22.84 billion, equal to 61.62% of the healthcare content management system market, while the services slice reached USD 14.23 billion. Professional, managed, and support engagements are expected to add USD 8.42 billion new revenue by 2031 as buyers seek integration, optimization, and compliance outsourcing. The healthcare content management system market size for services is projected to climb at a 9.78% CAGR, reflecting growing reliance on third-party expertise to navigate HIPAA audits and AI model validation.

Healthcare systems adopting image-enabled EHRs typically allocate 45% of project budgets to consulting and training, underscoring why service partners hold center stage in complex deployments. Managed services appeal to mid-tier hospitals lacking 24×7 security operations centers, driving multi-year contracts that stabilize vendor revenue and reinforce platform lock-in within the healthcare content management system market.

By Deployment Mode: Cloud Acceleration Continues Despite Security Concerns

Cloud installations retained 53.89% of 2025 revenue, and are tracking a 10.21% CAGR to 2031—outpacing overall market growth as providers retire aging data centers. Hybrid models—on-premise edge nodes combined with regional cloud zones—account for most new contracts, especially in Europe where GDPR data-sovereignty clauses restrict full public-cloud adoption.

The healthcare content management system market size for cloud deployments capturing two-thirds of total spend, aided by automatic uptime SLAs and built-in AI accelerators unavailable in legacy servers. However, prolonged vendor-risk assessments and cyber-insurance underwriting slow(continued) contract finalization cycles, suggesting security certifications—FedRAMP, HITRUST, ISO 27001—will remain decisive differentiators for cloud vendors.

By End User: Payers Accelerate Adoption for Value-Based Care Support

Hospitals and health systems drove 45.89% of 2025 spend, but payer investments are rising at an 10.92% CAGR as insurers seek longitudinal repositories to quantify shared-savings contracts and automate claims touch-points. The healthcare content management system market size attributable to payers could top USD 9.63 billion by 2031 if current digital quality-measure mandates extend beyond Medicare Advantage.

Ambulatory clinics, imaging centers, and long-term care facilities form a long-tail segment with steady but lower growth, often choosing software-as-a-service bundles that combine archiving with e-fax and patient portal modules. These buyers help sustain a fragmented vendor landscape that balances enterprise giants with niche cloud players inside the healthcare content management industry.

By Application: AI-Enabled IDP Disrupts Clinical Content Leadership

Clinical content management retained a 40.74% revenue share in 2025 as radiology, cardiology, and oncology workflows continue to anchor imaging archives jacr.org. Yet AI-enabled IDP is forecast to expand at 10.58% CAGR, narrowing the gap by 2031 as providers automate chart abstraction and prior-authorization documentation. Healthcare content management system market share for IDP-centric solutions could surpass 25% by the end of the forecast period should current adoption curves persist.

Unstructured progress notes, referral letters, and faxed lab reports still account for more than 80% of inbound documents, making AI essential for actionable analytics. Vendors bundling pre-trained clinical language models and explainability dashboards differentiate from commodity storage rivals in the healthcare content management system market.

Geography Analysis

North America contributed 38.41% of 2025 revenue, supported by mature EHR penetration, HIPAA audit activity, and a consolidated hospital landscape that prioritizes integrated clinical-imaging workflows. Multi-factor authentication and encryption mandates, coupled with ransomware fears, sustain demand for zero-trust repositories—a trend expected to keep regional CAGR at 7.74% through 2031.

Asia-Pacific is the fastest-growing territory at 11.32% CAGR, buoyed by national EHR rollouts in India, Thailand, and Australia, plus strong government funding for AI in diagnostics whitecase.com. Public-private telehealth programs in rural provinces add incremental volume, especially for cloud-native vendors licensed to host medical records under evolving local data-sovereignty laws.

Europe delivers mid-single-digit expansion as GDPR compliance and cross-border data-exchange initiatives stabilize buyer demand. Hybrid-cloud architectures dominate new engagements, with sovereign-cloud nodes mitigating residency constraints in Germany, France, and the Nordics hl7.org. Meanwhile, Middle-East markets begin adopting AI-driven repositories tied to medical tourism and national insurance digitization, adding a modest but strategic growth corridor for global vendors.

Competitive Landscape

The healthcare content management system market remains moderately fragmented. Hyland, OpenText, IBM, and Microsoft continue to compete head-to-head on enterprise breadth, while Epic, Oracle Health, and athenahealth bundle native repositories with their EHRs to cement account control. Vendors differentiate through:

- Embedded AI and analytics—Hyland’s 2024 IDP release processes 1,000 pages per minute, enabling real-time clinical note abstraction.

- Cloud managed services—OpenText’s Azure-based platform offers 99.99% uptime SLAs and FedRAMP certification, attracting U.S. federal health agencies.

- Interoperability leadership—IBM leverages FHIR gateways and blockchain consent layers to sidestep information-blocking scrutiny and court large IDNs.

Consolidation persists as smaller IDP specialists seek scale. Oracle’s 2025 AI-enabled EHR launch threatens standalone content vendors, as fully integrated platforms promise simplified purchasing and unified governance. Litigation over information blocking increases transparency pressure, nudging competitive differentiation toward open standards and value-added analytics instead of lock-in tactics.

Healthcare Content Management System Industry Leaders

Microsoft

IBM

Hyland Software Inc

IQVIA

Xerox Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Hyland partnered with Northern Care Alliance NHS Foundation Trust to deploy a centralized electronic document management system across four hospitals.

- March 2022: Epic announced development of a healthcare-specific ERP suite adjoining its EHR, extending competitive scope beyond clinical documentation.

Global Healthcare Content Management System Market Report Scope

As per the scope of this report, the healthcare content management system helps to streamline the workflow by managing contents and documents and is responsible for maintaining the websites of healthcare organizations. The healthcare content management system market is segmented by Solution (Document Management, Web Content Management, Data Records, and Other Solutions), by End-User (Hospitals & Clinics, Ambulatory Surgical Centers, Other End Users), and Geography (North America, Europe, Asia-Pacific, Middle East, and Africa, South America). The market report also covers the estimated market sizes and trends for 17 different countries across major regions, globally. The report offers the value (in USD million) for the above segments.

| Software |

| Services |

| On-premise |

| Cloud |

| Hybrid |

| Clinical Content Management |

| Administrative / Non-clinical |

| Imaging & Diagnostics |

| Patient Portals & Engagement |

| Hospitals & Health Systems |

| Ambulatory Surgical Centers |

| Diagnostic & Imaging Centers |

| Payers / Insurance Providers |

| Long-Term Care Facilities |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa |

| By Component | Software | |

| Services | ||

| By Deployment Mode | On-premise | |

| Cloud | ||

| Hybrid | ||

| By Application | Clinical Content Management | |

| Administrative / Non-clinical | ||

| Imaging & Diagnostics | ||

| Patient Portals & Engagement | ||

| By End User | Hospitals & Health Systems | |

| Ambulatory Surgical Centers | ||

| Diagnostic & Imaging Centers | ||

| Payers / Insurance Providers | ||

| Long-Term Care Facilities | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected size of the healthcare content management market by 2031?

The healthcare content management system market is forecast to reach USD 61.28 billion by 2031 on a 8.74% CAGR trajectory.

Which segment is growing fastest in the healthcare content management system market?

Services are expanding at a 9.78% CAGR because providers need integration, compliance, and AI-training support

How quickly is cloud deployment advancing?

The cloud segment is rising at 10.21% CAGR, driven by lower total cost of ownership and built-in security updates

Why are payers investing in content management solutions?

Value-based care contracts require detailed longitudinal records to calculate shared-savings outcomes, pushing payer CAGR to 10.92%

What role does AI play in modern content management?

AI-enabled intelligent document processing extracts data from unstructured notes and images, cutting manual entry errors and improving coding accuracy, and is the fastest-growing application at 10.58% CAGR

Page last updated on: