Global Healthcare IT Integration Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

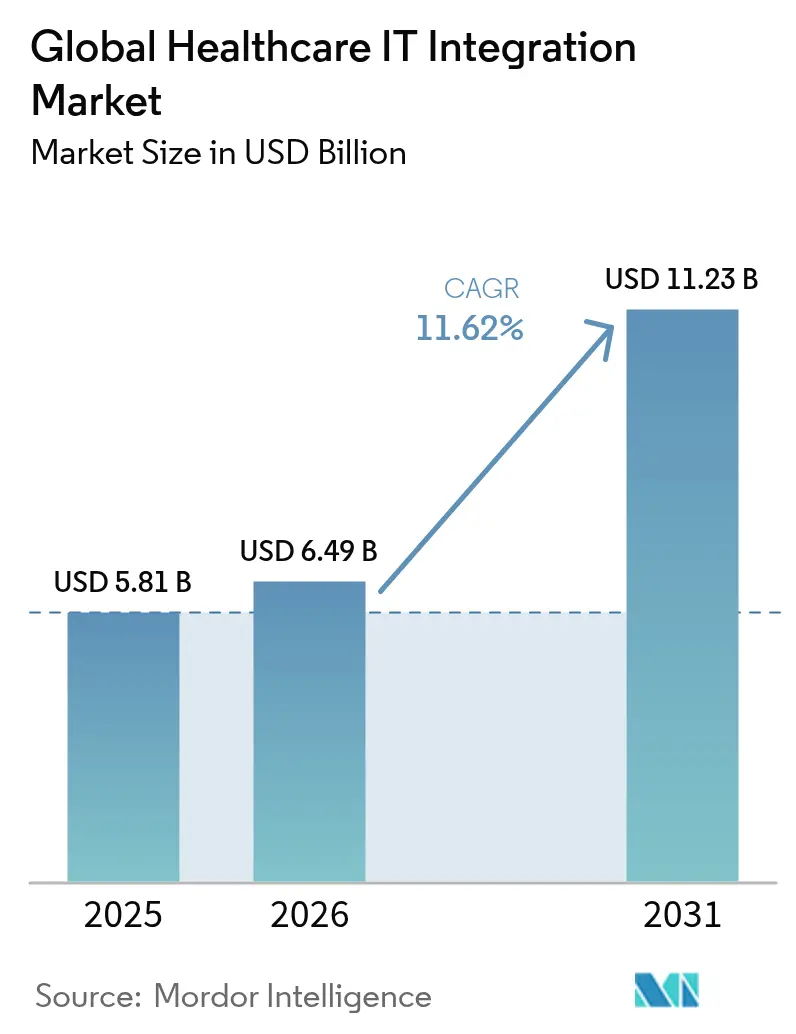

| Market Size (2026) | USD 6.49 Billion |

| Market Size (2031) | USD 11.23 Billion |

| Growth Rate (2026 - 2031) | 11.62% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Global Healthcare IT Integration Market Analysis by Mordor Intelligence

The Global Healthcare IT Integration market size is expected to grow from USD 5.81 billion in 2025 to USD 6.49 billion in 2026 and is forecast to reach USD 11.23 billion by 2031 at 11.62% CAGR over 2026-2031.

Strong growth stems from the need to consolidate fragmented data systems, comply with interoperability mandates, and support value-based care models that depend on friction-free data exchange. Provider consolidation, the steady rise of connected medical devices, and payer-provider convergence amplify demand for robust integration architectures. At the same time, FHIR-driven application programming interfaces (APIs) are redefining technical baselines, forcing both incumbent vendors and new entrants to modernize interface engines, API gateways, and data normalization pipelines. Heightened cyber-security expectations and the search for implementation talent, especially for HL7/FHIR specialists, are shaping investment priorities as organizations balance speed, security, and cost

Key Report Takeaways

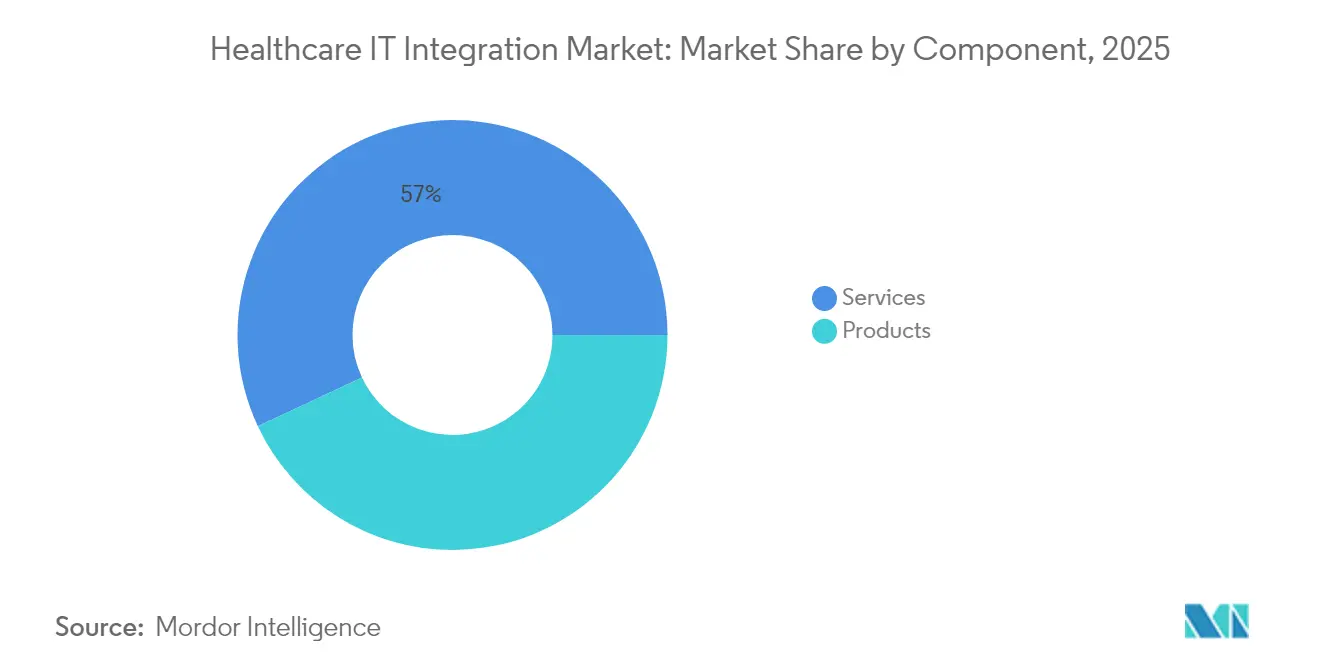

- By component, Services held a 56.98% revenue share of the Healthcare IT Integration market in 2025; Products are set to post the fastest 13.05% CAGR to 2031.

- By deployment, on-premise solutions commanded 61.78% of Healthcare IT Integration market share in 2025, whereas cloud offerings are projected to grow at 12.22% CAGR through 2031.

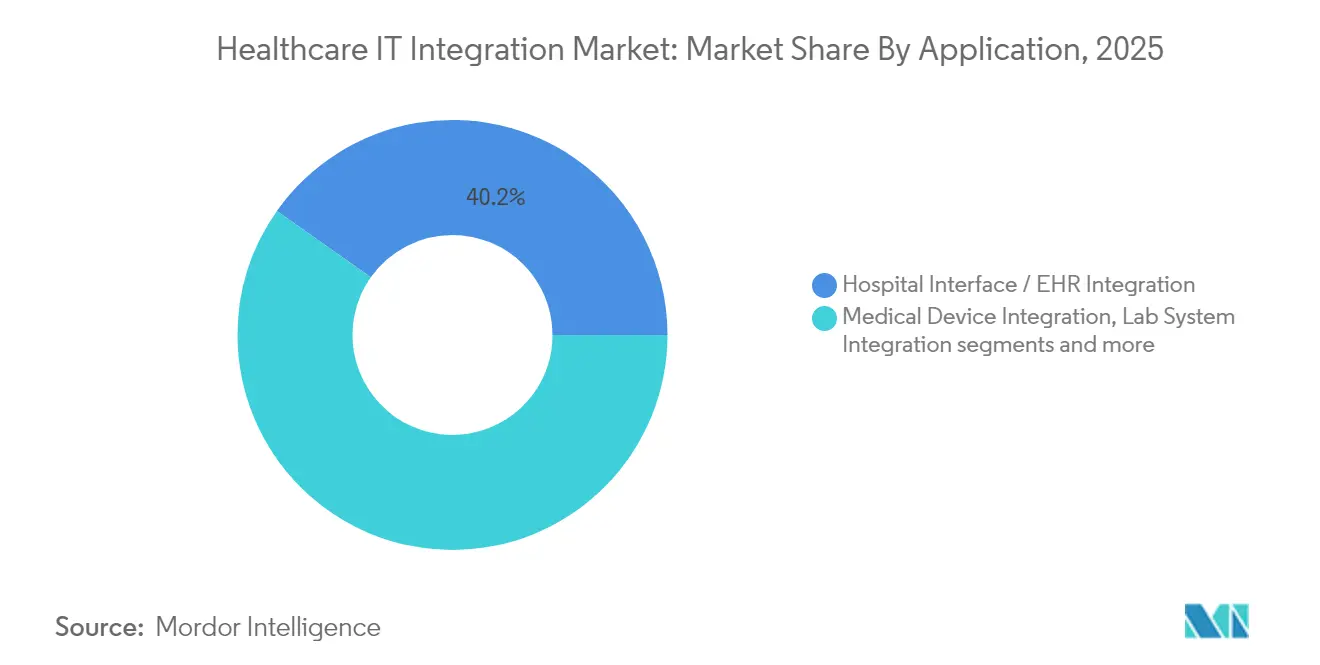

- By application, hospital interface/EHR integration accounted for 40.21% share of the Healthcare IT Integration market size in 2025; medical device integration is expanding at 11.76% CAGR to 2031.

- By end user, hospitals and clinics controlled 63.64% of Healthcare IT Integration market share in 2025, while diagnostic & imaging centers will grow most rapidly at 11.88% CAGR.

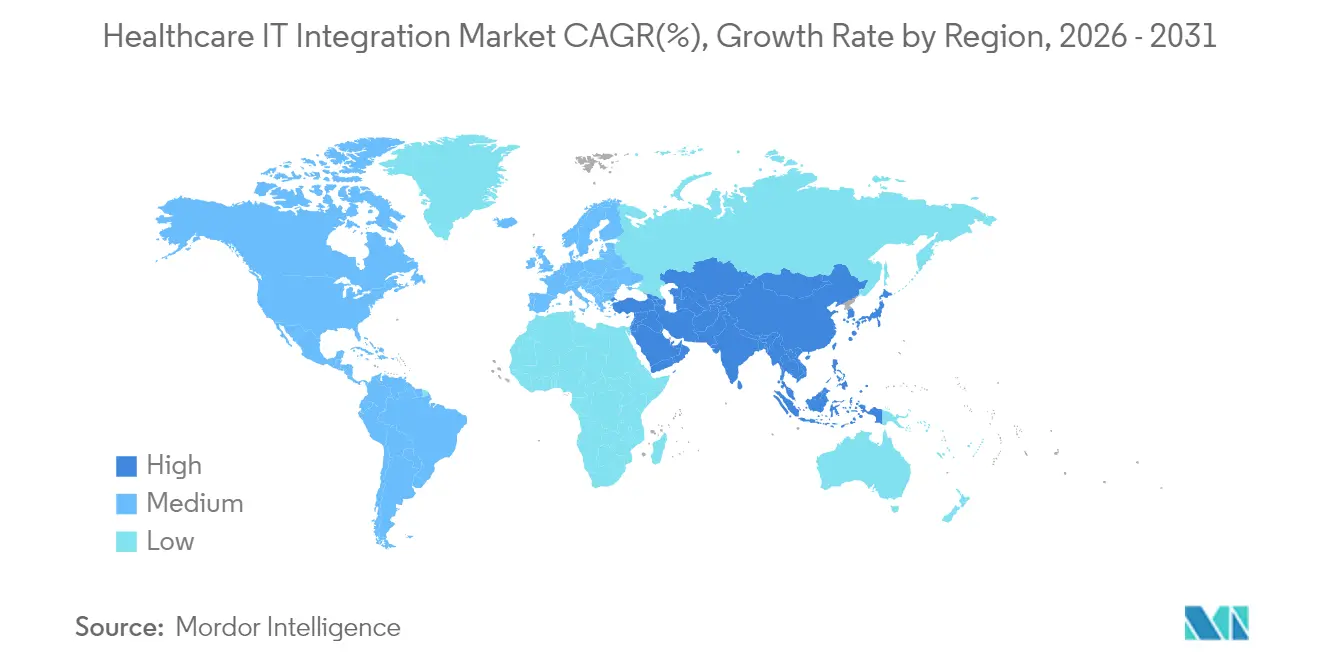

- North America dominated with 42.95% of the Healthcare IT Integration market in 2025; Asia-Pacific is the fastest-growing region with a 14.12% CAGR forecast

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Healthcare IT Integration Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Transition to FHIR-based APIs Mandated by US ONC & EU EHDS | 3.20% | North America, Europe | Medium term (2-4 years) |

| Multi-system Integration Demand from Remote Patient Monitoring Programs | 2.50% | Global, with emphasis on developed markets | Medium term (2-4 years) |

| Increasing Need of Electronic Health Records and Other Healthcare IT Solutions | 2.10% | Global | Long term (≥ 4 years) |

| Device Integration Needs in Smart Operating Rooms across Middle East | 1.40% | Middle East, with spillover to Asia-Pacific | Short term (≤ 2 years) |

| Payer-Provider Convergence Requiring Seamless Claims-Clinical Data Fusion in US | 1.80% | North America | Medium term (2-4 years) |

| Surge in M&A Spurring Interface Engine Replacement Cycles in North America | 1.30% | North America, with spillover to Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Transition to FHIR-based APIs Mandated by US ONC & EU EHDS

The ONC final rule taking effect January 2026 and the EHDS regulation in force since March 2025 compel payers, providers, and vendors to support real-time, patient-authorized data flows built on FHIR resources, accelerating capital outlays for interface engine refreshes, API management, and semantic mapping tools[1]Source: European Commission, “European Health Data Space Regulation (EHDS),” health.ec.europa.eu. With 67% of organizations already running FHIR APIs in 2024, the Healthcare IT Integration market must absorb a steep learning curve in mapping legacy HL7v2 feeds to granular FHIR entities, promoting specialist demand even in mature North American settings. Providers unable to comply risk financial penalties and strategic disadvantages, prompting alliances between EHR vendors and niche integrators to co-develop migration accelerators and conformance testing frameworks.

Multi-system Integration Demand from Remote Patient Monitoring Programs

Demand surges as payers reimburse for remote patient monitoring (RPM) and hospital-at-home models. Nearly 50 million US patients use RPM devices, and outcomes improve markedly when monitoring feeds are embedded in EHR workflows—readmissions drop 38% compared with non-integrated deployments [2] Source: United States Department of Health and Human Services, “Strategic Plan for the Use of Artificial Intelligence in Health,” nih.gov. Data flows now span wearables, smartphone apps, and cloud analytics, placing the Healthcare IT Integration market at the core of device-to-EHR orchestration, alert routing, and longitudinal record enrichment. Vendors with pre-built EHR connectors and FHIR-first architectures rank higher on purchasing shortlists, while hospitals tighten technical due-diligence criteria to ensure device data harmonize with quality-reporting metrics.

Device Integration Needs in Smart Operating Rooms across Middle East

Middle Eastern health systems are outfitting hybrid operating rooms with robotics, high-definition imaging, and voice-activated assistants. Up to 75% of ICU devices remain isolated from hospital systems, causing manual charting burdens and incomplete data trails costing USD 35 billion in administrative waste annually in the US alone. Regional flagships such as UAE hospitals deploy IP-based video platforms that integrate surgical feeds directly into electronic records, setting benchmarks that spill into broader Asia-Pacific markets pro.sony. The Healthcare IT Integration market meets demand through device-agnostic middleware that normalizes proprietary protocols into FHIR Observation resources, improving perioperative analytics.

Increasing Need of Electronic Health Records and Other Healthcare IT Solutions

With EHR saturation exceeding 90% of US medical school programs, the imperative shifts from basic connectivity to deep optimization, embedding AI routines for medication safety, scheduling, and revenue-cycle automation. Integration budgets favor end-to-end pipelines that feed predictive models with structured and unstructured records, widening the Healthcare IT Integration market as hospitals upgrade message brokers and data lakes to support machine-learning workloads. AI-ready EHR add-ons raise interface complexity, reinforcing the value of standards-based adapters and low-code transformation layers that reduce turnaround times for algorithm deployment.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Implementation Talent Shortage for HL7/FHIR Specialists in Africa | -1.20% | Africa, with global implications | Medium term (2-4 years) |

| Cyber-security Compliance Costs under GDPR & HIPAA Escalate Integration TCO | -1.60% | Global, with emphasis on North America and Europe | Long term (≥ 4 years) |

| Vendor-Locked Legacy HIS Architectures in Public Hospitals across South America | -0.90% | South America, with spillover to developing markets | Long term (≥ 4 years) |

| ROI Ambiguity for Cross-Platform Integration in Small Physician Practices | -0.80% | Global, with emphasis on fragmented healthcare markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Implementation Talent Shortage for HL7/FHIR Specialists in Africa

African public and private providers confront delays of 6–12 months on critical projects due to a limited pool of integration engineers versed in HL7 and FHIR semantics healthtechafrica.org. Remote consulting alleviates only part of the gap, because onsite change-management and infrastructure work remain essential. The shortage raises labor costs, stretches go-live schedules, and reduces the addressable Healthcare IT Integration market until capacity-building programs mature. Emerging national eHealth strategies, such as Namibia’s, earmark workforce development grants to expand certification programs.

Cyber-security Compliance Costs under GDPR & HIPAA Escalate Integration TCO

HIPAA audits and GDPR enforcement elevate encryption, access-logging, and breach-notification requirements, adding USD 10,000–30,000 in certification expenses for mid-sized entities and influencing design decisions for every new interface. Healthcare data breaches average USD 9.77 million per incident, compelling IT teams to harden integration layers with tokenization and zero-trust architectures. The resulting cost pressures hinder smaller practices, dampening segments of the Healthcare IT Integration market that cannot quickly recoup compliance overhead.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Dominate Integration Landscape

Services captured 56.98% of Healthcare IT Integration market share in 2025, a level that underlines the knowledge-intensive character of cross-platform interoperability projects. Advisory teams conduct workflow mapping, build interface specifications, run validation scripts, and maintain 24/7 support desks, all of which exceed the scope of off-the-shelf technology. This services heft is expected to persist as FHIR regulations tighten deliverables and as multi-vendor ecosystems demand continuous governance. Large health systems allocate rising operational budgets to managed-integration contracts that guarantee uptime and regulatory audit readiness.

The Products segment is forecast to grow 13.05% CAGR, outpacing overall Healthcare IT Integration market size expansion as interface engines, API gateways, and device-connect software adopt low-code design studios. Infor Cloverleaf alone processes more than 300 million daily transactions across one-third of US hospitals, illustrating how modern engines take over legacy script-heavy brokers. Cloud-based toolchains bundled with pre-validated FHIR implementation guides lower entry thresholds for mid-tier hospitals. Nevertheless, product success remains contingent on service partners who customize configurations and ensure data governance, reinforcing the intertwined growth paths of both segments.

By Deployment Mode: Security Concerns Sustain On-Premise Dominance

On-premise deployments held 61.78% of Healthcare IT Integration market in 2025, underscoring hospitals’ preference for sovereign control over protected health information and direct grasp of network segmentation strategies amid escalating ransomware threats. High breach penalties incentivize chief information security officers to keep mission-critical integration engines behind institutional firewalls, coupled with custom hardware acceleration for message parsing. The Healthcare IT Integration market size attached to on-premise models, therefore, remains material even as cloud adoption climbs.

Cloud-hosted integration is gaining a 12.22% CAGR on the back of cost-effective scaling, elastic compute for peak transaction traffic, and pre-certified compliance blueprints. Hybrid patterns flourish, allowing clinical message routing and storage on-premise while leveraging cloud analytics for secondary use cases. Parallels’ 2025 survey reveals 86% of enterprises experimenting with selective workload repatriation to strike an economic balance. For rural providers without Tier 3 data centers, hardened healthcare clouds now provide FHIR sandbox environments that shorten go-live cycles, broadening the total Healthcare IT Integration market.

By Application: EHR Integration Drives Market Growth

Hospital interface/EHR integration led with 40.21% of Healthcare IT Integration market size in 2025, reflecting the centrality of unified patient records to clinical decision-making. Epic ecosystem supports HL7v2, C-CDAs, and FHIR endpoints, enabling bi-directional data flows with ancillary systems such as lab analyzers, oncology registries, and patient-engagement portals. Value-based reimbursement further enlarges this slice of the Healthcare IT Integration market as payers demand real-time quality-measure feeds from provider EHRs.

Medical device integration is projected to be the fastest-growing application at 11.76% CAGR. Smart pumps, ventilators, and wearable sensors generate high-frequency metrics that must be harmonized with EHR timelines for closed-loop alerting. Evidence shows 72% of randomized studies linking device data to clinical pathways achieve reduced hospitalization metrics. Middleware that converts raw device signals into FHIR Observation or DeviceMetric resources anchors this momentum, positioning vendors with protocol-agnostic libraries to capture expanding Healthcare IT Integration market share in acute and ambulatory settings.

By End User: Hospitals Lead While Diagnostic Centers Grow Rapidly

Hospitals and clinics commanded 63.64% of Healthcare IT Integration market in 2025. Tertiary care centers juggle hundreds of departmental systems, making enterprise integration governance a strategic imperative. Multi-hospital groups embarking on mergers leverage interface-modernization projects for post-acquisition synergy capture, pushing demand for horizontally scalable brokers and master patient indices. Budget justification often hinges on reduced duplicate testing and shorter admission-to-treatment times, benefits tightly coupled to integration maturity.

Diagnostic and imaging centers, though a smaller base, show a 11.88% CAGR and illustrate the diversification of the Healthcare IT Integration industry beyond inpatient settings. Cloud-native picture archiving and communication systems (PACS) now publish DICOM studies via FHIR ImagingStudy endpoints, expediting cross-provider image exchange and second-opinion workflows. The upcoming HL7 Europe Imaging Study Report aims to unify continental specifications—an initiative expected to propel Healthcare IT Integration market size in outpatient diagnostician networks.

Geography Analysis

North America occupied 42.95% of the Healthcare IT Integration market in 2025, supported by mature EHR ecosystems, rigorous federal mandates, and active M&A pipelines. The ONC Interoperability and Prior Authorization rule anchors regulatory certainty by 2027, compelling both payers and providers to upgrade interface engines for real-time prior-approval data sharing mahealthdata.org. Concurrently, payer-provider convergence projects inject demand for claims-clinical fusion, reinforcing regional growth.

Asia-Pacific is the fastest-expanding territory with a 14.12% CAGR through 2031. Government-backed digitization strategies in Japan, India, and Australia fund broadband health networks, EHR rollouts, and mobile triage platforms. Local vendors collaborate with global interface leaders to localize FHIR profiles in multiple scripts, elevating the Healthcare IT Integration market across urban and remote clinics. Mobile-first care models and high consumer app engagement spur API marketplaces that connect teleconsultation, pharmacy delivery, and chronic-care coaching services in near real time.

Europe’s trajectory is shaped by the European Health Data Space regulation, which harmonizes EHR interoperability and patient data portability across EU member states. Anticipated cost savings of EUR 11 billion over 10 years motivate national projects to align legacy systems with the common framework. Vendors must embed consent-management modules and multilingual coding dictionaries into their offerings, expanding addressable Healthcare IT Integration market segments around pan-European tele-specialty networks. Emerging Middle East and South American markets show healthy appetites for smart-hospital inclusion, yet legacy HIS lock-in and uneven skill availability temper roll-outs.

Regulatory Landscape

Interoperability certification and cross-border data rules are tightening the technical baseline for healthcare IT integration. In the United States, ASTP/ONC continues to advance standards through mechanisms such as the Standards Version Advancement Process (SVAP), with the 2026 SVAP approving newer specifications (including updated HL7 FHIR US Core Implementation Guide versions) for use in the ONC Health IT Certification Program. ONC also moved the US data content baseline forward as earlier USCDI versions sunset, and it opened public comment on Draft USCDI v7 in January 2026, keeping data element expansion and FHIR alignment central to compliance roadmaps.

In Europe, Regulation (EU) 2025/327 (European Health Data Space, EHDS) entered into force on March 26, 2025, establishing a common legal and technical framework for EHR systems and data portability across member states. Implementation measures continued in 2026, including Commission Implementing Regulation (EU) 2026/771, effective April 7, 2026, which established the EHDS Board to steer implementation guidance and promote consistent cross-border exchange. Together, these actions raise the bar for integration platforms that can operationalize consent, auditability, and standards-based APIs across multi-vendor clinical and administrative systems.

Competitive Landscape

The Healthcare IT Integration market demonstrates moderate concentration: a handful of dominant EHR vendors, several best-of-breed interface-engine specialists, and a swarm of API-native start-ups. Epic, Oracle Cerner, and Allscripts continue to expand their internal interoperability toolkits, sometimes crowding smaller middleware firms yet also creating partnership opportunities to cover edge cases. Infor’s Cloverleaf maintains stronghold positions by processing 300 million messages daily, while InterSystems, Lyniate, and Redox scale FHIR gateways that plug into cloud providers and specialty software.

Competition pivots on time-to-value. Pre-built connectors, bundled FHIR implementation guides, and low-code orchestration canvases differentiate platforms aiming to shorten project lifecycles from months to weeks. AI-infused data-quality modules that auto-detect mapping errors further appeal to resource-constrained IT teams. The US HHS strategic plan for AI in health underscores federal interest in cognitive integration utilities, signaling that algorithm-ready data threads will command premium valuations in the Healthcare IT Integration market.

Strategic moves during 2024–2025 include Oracle Health’s FHIR API rollout, GE Healthcare’s smart-OR interoperability suite, and Infor’s population-health analytics module extensions. Vendors also court regional channel partners to counter talent shortages and deepen localization; example: RAIN Technology’s voice-assistant-led UAE push. As cloud titans enter through healthcare-optimized data platforms, incumbent integrators differentiate via domain-specific accelerators and 24×7 managed services, sustaining a dynamic but not fragmented competitive environment

Global Healthcare IT Integration Industry Leaders

Allscripts Healthcare Solutions Inc.

Cerner Corporation

IBM Corporation

Siemens Healthcare GmbH

General Electric Company (GE Healthcare)

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A key whitespace is compliance-grade, workflow-native integration for administrative transactions, not just clinical exchange. In April 2026, CMS issued a proposed rule on 2026 Interoperability Standards and Prior Authorization for Drugs, introducing requirements for impacted payers to adopt updated standards and to report interoperability API endpoints, with proposed compliance by October 1, 2027. ONC reinforced the technical path in June 2026 via the 2026 SVAP, which included updated HL7 FHIR US Core and updated Da Vinci implementation guides used for electronic prior authorization. This creates a near-term buying trigger for API management, identity and consent, and FHIR mapping services in payer and provider environments.

Another opportunity is integration platforms that package cloud AI enablement with standards-based interoperability. Enterprise programs are pairing AI workloads with Healthcare APIs and FHIR-based interfaces, and vendors are positioning governed integration as the data access layer for analytics. In January 2026, SAP and Fresenius announced a strategic partnership to develop an AI-supported digital healthcare platform for hospital information systems using HL7 FHIR standards, underscoring the demand for integration that can expose governed data to analytics and AI features without custom point-to-point interfaces. In March 2026, CVS Health and Google Cloud announced Health100 to connect ecosystem partners using cloud AI and interoperability infrastructure, which supports prebuilt connectors, managed API layers, and implementation services aimed at shortening time-to-value across retail health, payer-provider convergence, and hospital networks.

Recent Industry Developments

- July 2026: 1upHealth announced 1up Gateway to help health plans address the CMS-0057-F interoperability and prior authorization requirements through a managed API layer that connects to existing FHIR infrastructure. The release frames compliance-oriented integration tooling as a packaged product category, shifting some spend from bespoke interface builds to managed, standards-upgradeable services.

- March 2026: CVS Health and Google Cloud announced a strategic partnership that includes launching Health100 as a health technology services unit to connect partners using Google Cloud AI capabilities and interoperability infrastructure. The announcement highlights how cloud ecosystems are moving closer to the center of integration procurement, with Healthcare APIs and partner connectivity treated as platform-layer building blocks for payer and retail care workflows.

- April 2025: GE Healthcare unveiled AI-driven smart operating room integration at Arab Health 2025, highlighting imaging-to-HIS connectivity and interoperable surgical workflows. The focus on smart-OR integration points to demand for device and imaging integration middleware that can normalize high-frequency clinical data and route it into enterprise records for perioperative analytics.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the healthcare IT integration market covers software and related services used to connect clinical, administrative, and device systems so data can move reliably between applications and care settings.

Scope exclusions: We exclude stand-alone EHR modules, revenue-cycle tools, and general consulting work that does not directly enable system-to-system data exchange.

Segmentation Overview

- By Component

- Products

- Integration Engines

- Device Integration Software

- iPaaS / API Management Platforms

- EHR / HIE Interface Modules

- Services

- Implementation & Integration

- Support & Maintenance

- Consulting & Training

- Products

- By Deployment Mode

- On-premise

- Cloud-based

- Hybrid

- By Application

- Hospital Interface / EHR Integration

- Medical Device Integration

- Lab System Integration

- Pharmacy Integration

- Revenue Cycle & Claims Integration

- Population Health & Analytics Integration

- Others

- By End User

- Hospitals & Clinics

- Diagnostic & Imaging Centers

- Payers & TPAs

- Pharmacies

- Others

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was first used to map how integration demand forms in healthcare delivery and to anchor basic indicators that can be tracked year over year. Public sources such as the US Office of the National Coordinator for Health IT, the US Centers for Medicare and Medicaid Services, the World Health Organization, and the OECD helped us ground assumptions around digitization, interoperability policy signals, and care delivery volumes.

We also reviewed materials like annual reports and investor presentations from relevant solution providers and system integrators, along with hospital and payer announcements, association publications, and reputable press coverage to understand typical purchase cycles and service mix. Where needed, a paid subscription database for company financials and a paid patent database were referenced to cross-check revenue exposure and innovation activity in integration tools. These desk sources are illustrative only, and many other public references were also used for data collection, validation, and research clarification.

Primary Interviews and Surveys

Primary interviews and surveys were run with integration platform providers, implementation partners, hospital and lab IT leaders, and buyer-side teams responsible for interoperability programs. Inputs from these discussions were used to verify what gets budgeted as integration, how services are priced, and which deployment patterns are actually being adopted across major regions, before final assumptions were locked.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 28% | CXOs: 12% | APAC: 47% |

| Mid tier: 56% | Functional/Unit leaders: 32% | EMEA: 33% |

| Smaller Players: 16% | Managers: 56% | Americas: 20% |

Market-Sizing & Forecasting

Sizing starts with a top-down demand pool build where healthcare digitalization signals are translated into integration spend, and then shaped by how much data exchange is required across settings. We used bottom-up approximations as a cross-check, such as sampled supplier revenues tied to integration offerings, a volume-by-ASP sense check for interface and implementation work, and channel checks on typical contract sizes to adjust totals where needed.

Key inputs used in the model include EHR and interoperability program adoption, hospital and laboratory digitization intensity, healthcare IT spending direction, cloud migration pace for clinical systems, and the mix between software subscriptions and implementation and support services. Where data was patchy by geography, gaps were handled through proxy indicators like care delivery scale, policy push toward interoperability, and expert-confirmed pricing bands, which were then normalized to USD using consistent timing.

For forecasting, scenario analysis was used so the base case reflects expected rollout speed of integration initiatives, with upside and downside cases tied to budget cycles, regulatory deadlines, and cloud adoption rates. Assumptions on pricing progression and service attach rates were refreshed through primary inputs to keep the forward view realistic and repeatable.

Data Validation & Update Cycle

Validation is done through triangulation across the model output, independent healthcare IT spending signals, and what interviewees describe as real purchasing behavior. Large variances are flagged, and the drivers are re-checked, which can trigger follow-up calls when a scope boundary or pricing assumption seems inconsistent.

Before sign-off, the sizing file is reviewed in multiple steps by analysts so calculation logic, currency handling, and year mapping stay consistent. The report is refreshed annually, and interim updates are added when material events occur that can move demand, such as policy shifts or sudden spending slowdowns. Right before delivery, a final pass is completed so clients receive the latest updated view.

Mordor Intelligence's Global Healthcare IT Integration Market Market Sizing Compared With Other Published Estimates

It is normal to see different market sizes for healthcare IT integration because the boundary is easy to stretch. Differences usually come from what gets counted as integration (software only versus software plus services), how adjacent items are handled, and whether the estimate is anchored to a clear demand signal like installed systems and connectivity needs.

Key gaps also come from the forecast stance and timing, since some studies publish aggressive growth paths, apply faster price increases, or convert currencies using different average-year rates. By tracking interoperability program adoption and service attach rates, Mordor Intelligence keeps the total tied to integration-specific revenue and excludes stand-alone clinical applications that do not create data exchange.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 6.49 B (2026) | |

| Industry Publisher A | USD 4.90 B (2024) | Uses an earlier base year and a broader label of healthcare integration, which can undercount newer API and cloud integration spend while mixing scope across software and services differently. |

| Industry Publisher B | USD 5.29 B (2024) | Leans on product groupings like device integration and interface engines without clearly separating stand-alone clinical applications, and it applies a different CAGR and conversion timing across the forecast window. |

The spread mainly reflects timing and scope decisions, especially whether integration is counted only when it enables system-to-system data flow and whether services are attached in a consistent way. With clear inclusions, repeatable inputs, and multiple checks against real buying patterns, the sizing stays easier to audit and more stable for planning.

Key Questions Answered in the Report

What is the current size of the Healthcare IT Integration market?

The market stands at USD 6.49 billion in 2026 and is forecast to climb to USD 11.23 billion by 2031, reflecting an 11.62% CAGR.

Why do services dominate Healthcare IT Integration spending?

Integration projects require specialized consulting, custom mapping, validation, and ongoing support; these labor-intensive tasks explain the 56.98% service share captured in 2025.

How will FHIR regulations affect integration investments?

US ONC and EU EHDS mandates oblige payers and providers to adopt FHIR APIs by 2026–2027, adding around +3.2% to overall market CAGR as organizations refresh interface platforms.

Which application area is growing fastest?

Medical device integration is advancing at 11.76% CAGR as connected pumps, monitors, and imaging tools feed real-time data into clinical workflows.

Which region will see the highest growth?

Asia-Pacific leads with a 14.12% CAGR, driven by aggressive digital-health funding, expanding middle-class demand, and government-backed interoperability programs.

What are the biggest constraints on market expansion?

Cyber-security compliance costs and shortages of HL7/FHIR specialists in developing regions subtract 1.6% and 1.2% respectively from forecast CAGR, prolonging project timelines and inflating budgets.

Page last updated on: