Healthcare And Medical Devices TIC Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

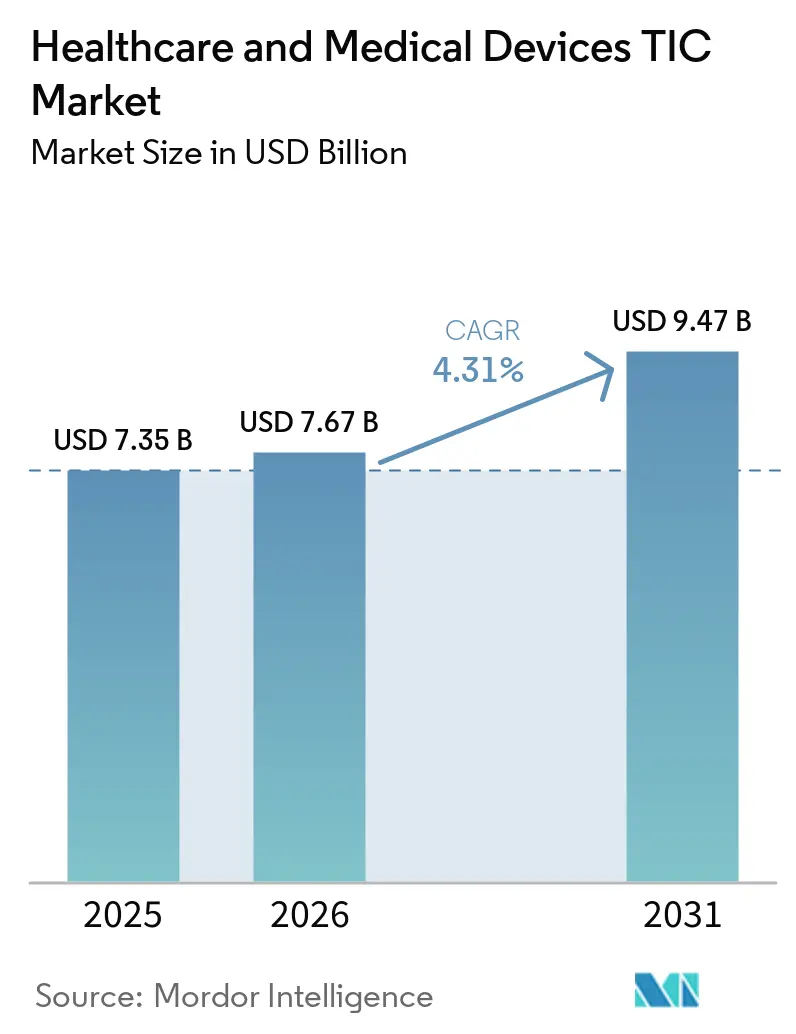

| Market Size (2026) | USD 7.67 Billion |

| Market Size (2031) | USD 9.47 Billion |

| Growth Rate (2026 - 2031) | 4.31% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Healthcare And Medical Devices TIC Market Analysis by Mordor Intelligence

The healthcare and medical devices TIC market size is expected to increase from USD 7.35 billion in 2025 to USD 7.67 billion in 2026 and reach USD 9.47 billion by 2031, growing at a CAGR of 4.31% over 2026-2031. The healthcare and medical devices TIC market is expanding because regulatory rules in North America, Europe, and Asia-Pacific are becoming stricter and more continuous, which is turning compliance into an ongoing service need rather than a one-time approval event. Demand is also rising because device portfolios now include more connected products, software-enabled systems, and drug-device combinations that require a wider set of testing, inspection, and certification steps across the product cycle. The healthcare and medical devices TIC market is also benefiting from a clear shift toward outsourced compliance support, as many manufacturers now prefer external experts over maintaining full in-house capabilities across several jurisdictions. Multi-country audit programs, quality system alignment, and post-market obligations are increasing the value of providers with broad authorization footprints and access to notified bodies. At the same time, specialist laboratories in sterilization, biocompatibility, combination product testing, and cybersecurity are shaping competition by taking share at the service-line level even when the top global groups remain strong at the firm level.

Key Report Takeaways

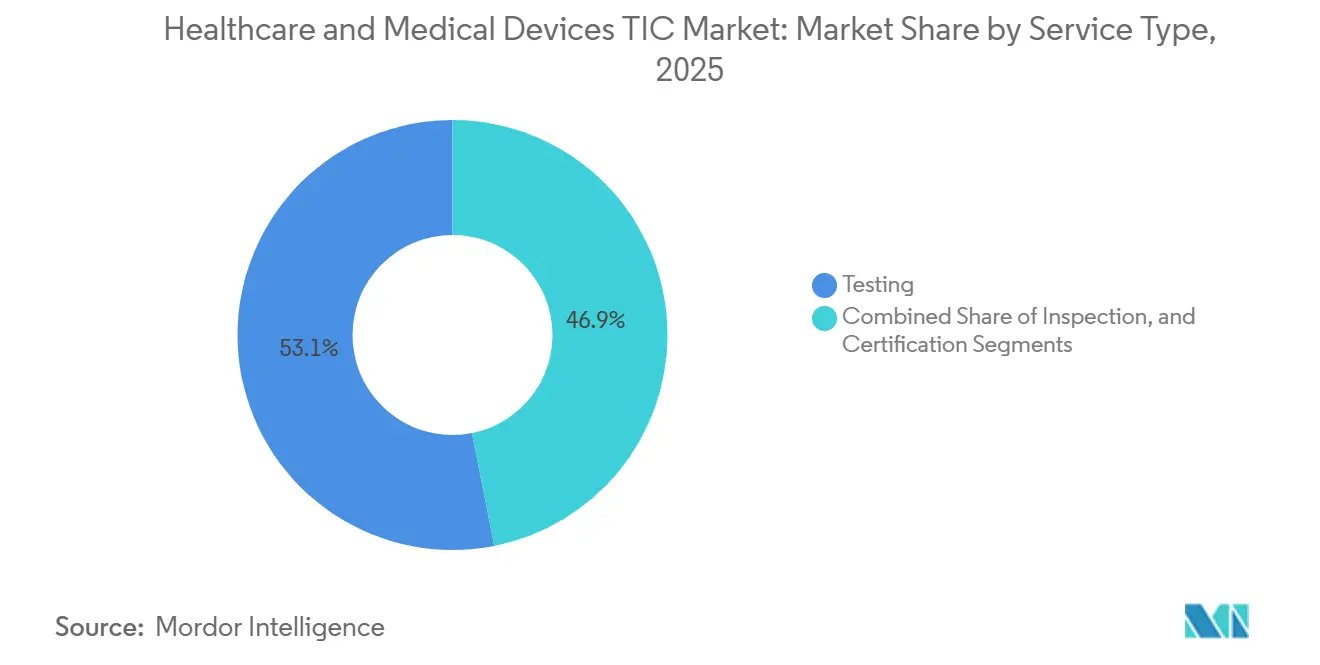

- By service type, testing held 53.11% share of the healthcare and medical devices TIC market in 2025, while certification is projected to record the fastest growth at a 5.05% CAGR through 2031.

- By sourcing type, outsourced services accounted for 69.32% share of the healthcare and medical devices TIC market in 2025 and are also projected to expand at a 4.74% CAGR through 2031.

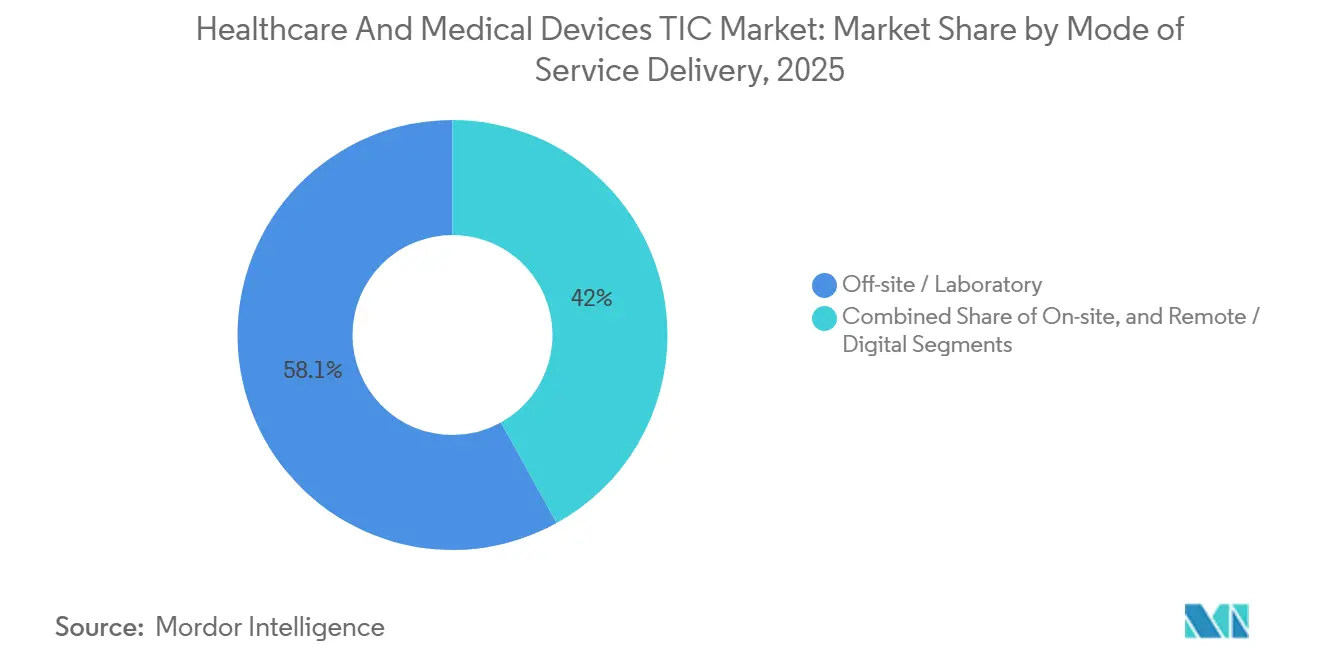

- By mode of service delivery, off-site and laboratory delivery accounted for 58.05% of the healthcare and medical devices testing, inspection, and certification (TIC) market in 2025, while remote and digital delivery is forecast to grow fastest at a 4.56% CAGR through 2031.

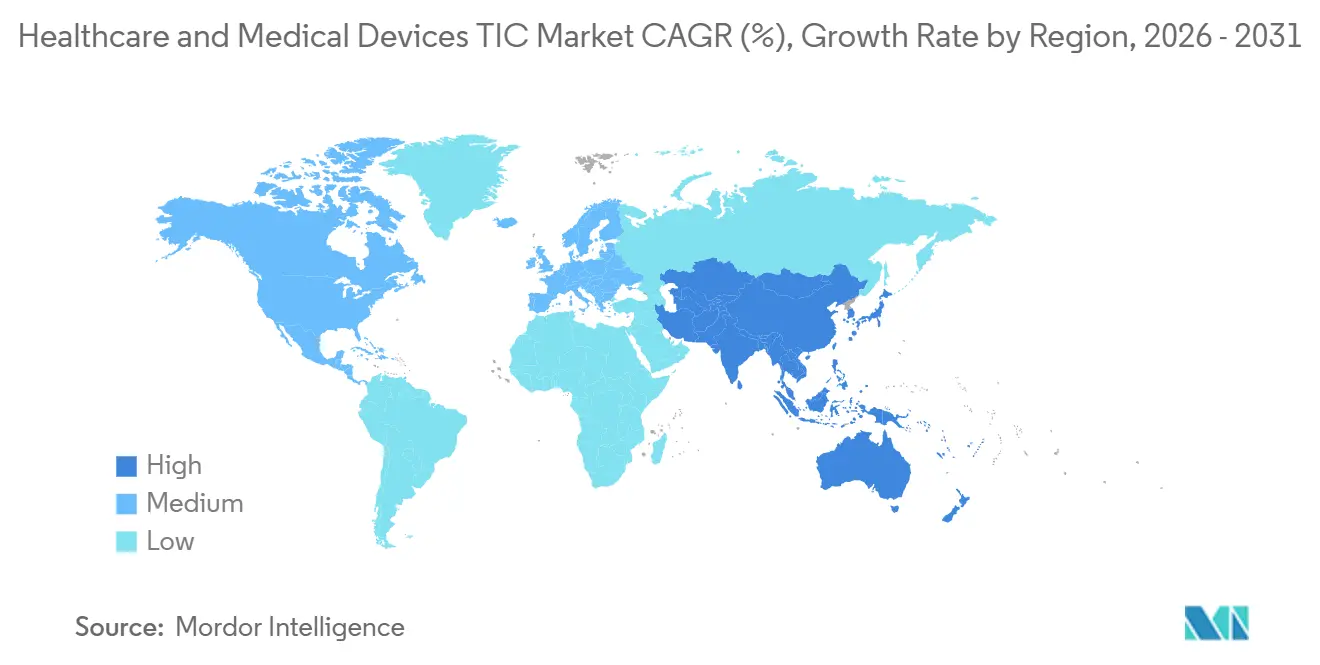

- By geography, Asia-Pacific held 44.73% share of the healthcare and medical devices TIC market in 2025 and is also expected to post the highest regional CAGR at 4.87% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Healthcare And Medical Devices TIC Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tightening Global Regulatory and Market-Access Requirements | +1.4% | Global | Long term (≥ 4 years) |

| Rising Device Complexity and Combination Product Testing Needs | +0.9% | North America and Europe, spill-over to Asia-Pacific | Medium term (2-4 years) |

| Growing Outsourcing by Small and Mid-Sized Medtech Firms | +0.7% | Global | Medium term (2-4 years) |

| Expansion of Asia-Pacific Medical Device Manufacturing Hubs | +0.5% | Asia-Pacific core, spill-over to Middle East and Africa | Long term (≥ 4 years) |

| Cybersecurity and Software Validation Workloads for Connected Devices | +0.4% | North America and Europe | Short term (≤ 2 years) |

| Post-Market Evidence and Real-World Performance Testing Demand | +0.3% | North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Tightening Global Regulatory and Market-Access Requirements

Multiple regulatory systems are now moving through increasingly enforcement-heavy phases simultaneously, which is a major demand driver for the healthcare and medical devices TIC market. In the United States, the QMSR took effect on February 2, 2026, and aligned device quality expectations more closely with ISO 13485, which raised the importance of design controls, supplier oversight, and software documentation in routine compliance work.[1]U.S. Food and Drug Administration, “Combination Products Guidance Documents,” FDA In Europe, Commission Implementing Regulation (EU) 2026/977 introduced uniform procedural and quality requirements for conformity assessment activities carried out by notified bodies, providing manufacturers with a more formal, more demanding review environment to navigate. Technical documentation expectations also remain extensive under the EU MDR, and Team-NB’s 2026 best-practice guidance shows the extent of the structured evidence manufacturers must assemble to support conformity review. This raises the value of providers that can guide manufacturers through multiple rulebooks rather than running single test programs. As a result, the healthcare and medical devices TIC market is moving toward longer client relationships built around recurring compliance oversight rather than isolated certification events.

Rising Device Complexity and Combination Product Testing Needs

The healthcare and medical devices TIC market is also gaining support from the rising complexity of devices, especially drug-device combinations and software-rich platforms. In June 2025, the FDA published draft guidance on unique device identifier requirements for combination products, adding another documentation layer to products already subject to a complex multi-center review pathway. Under EU MDR Article 117, integral drug-device combinations require a notified body's opinion on the device constituent, creating a new certification step that did not exist under the older framework. A connected drug delivery product can now require electrical safety, software validation, usability, biocompatibility, and drug-related manufacturing reviews within the same development cycle, which often spreads work across several specialist providers. The FDA also clarified current good manufacturing practice expectations for combination products under 21 CFR Part 4, which widened the quality system documentation perimeter that auditors and test partners must assess. That expands the revenue-per-device program and strengthens the role of specialist testing and certification support in the healthcare and medical devices TIC market.

Growing Outsourcing by Small and Mid-Sized Medtech Firms

Growing outsourcing by smaller manufacturers remains a steady growth lever for the healthcare and medical devices TIC market. The EU MDR requires manufacturers to appoint a Person Responsible for Regulatory Compliance, and that role carries competency expectations that many smaller companies cannot support internally across several markets. RQM+ stated in 2026 that medtech companies are increasingly adopting outsourced and hybrid product life cycle support to manage quality, regulatory, and clinical work without building parallel internal teams. The QMSR has also raised expectations for supplier quality oversight and formalized relationships with external partners, making outsourced TIC providers part of the regulated quality system rather than optional vendors. ISO 13485 is also serving as a supply-chain entry gate for many contract manufacturers and component suppliers, thereby extending certification demand deeper into the value chain. This shift is turning the healthcare and medical devices TIC market into a more embedded operating partner for mid-sized manufacturers that need steady compliance support across the United States, Europe, and other export markets.

Increasing Recalls Driving Preventive Testing Spend

The expansion of medical device manufacturing across the Asia-Pacific is creating a long-term demand base for the healthcare and medical devices TIC market. New plants across the region require process validation, equipment qualification, sterility validation, technical documentation support, and export certification before full commercial output can scale. In May 2026, Winner Medical broke ground on a new production base in Vietnam intended to support global medical supply chains through local manufacturing, pointing to fresh testing and certification demand tied to new lines and future export programs. In April 2026, CJ Medtech broke ground on a new factory in South Korea to expand orthopedic device production, which reflects the same pattern of investment-led demand for qualification and regulatory services. These investments matter because manufacturers in the region often need to meet both domestic regulations and export-market requirements simultaneously. That creates layered service needs and gives the healthcare and medical devices TIC market a wider revenue base per facility than a purely domestic approval path would create.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Cost of Multijurisdictional Compliance Programs | -0.7% | Global | Long term (≥ 4 years) |

| Notified Body and Specialist Lab Capacity Bottlenecks | -0.5% | Europe and North America | Medium term (2-4 years) |

| Divergent Cybersecurity Documentation Rules Across Jurisdictions | -0.3% | North America and Europe, spill-over to Asia-Pacific | Medium term (2-4 years) |

| AI-Enabled Device Validation and Change-Control Uncertainty | -0.2% | North America and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Cost of Multijurisdictional Compliance Programs

The cost of running parallel compliance programs across the United States, the European Union, the United Kingdom, China, Japan, and Brazil remains a real constraint on the healthcare and medical devices TIC market. The European Commission’s 19th Notified Body Survey showed that many product-level MDR assessments were taking 13 to 18 months, which means compliance budgets are now tied up for longer periods before revenue can be realized. Manufacturers that adopt MDSAP can simplify some audit pathways, but the initial cycle still requires multiple qualified audit days across registered sites, which remains expensive for companies with limited scale. Smaller firms, academic spinouts, and single-site manufacturers often carry the weakest compliance budgets even when their product pipelines are technically strong. That mismatch reduces the number of programs that move into full certification readiness at any one time. It also means the healthcare and medical devices TIC market can lose near-term volume from sub-scale innovators, even while larger manufacturers continue to spend.

Notified Body and Specialist Lab Capacity Bottlenecks

Capacity bottlenecks remain another important restraint for the healthcare and medical devices TIC market, especially in Europe and in specialist laboratory categories. The European Commission’s 19th survey recorded 33,175 MDR applications against 17,549 issued certificates through December 2025, indicating the scale of the backlog manufacturers and service providers are working through.[2]European Commission, “Study Supporting the Monitoring of the Availability of Medical Devices on the EU Market - 19th Notified Body Survey,” European Commission The same survey found that 59% of notified bodies reported certification timelines of 13 to 18 months for product-level assessments, which defer revenue recognition even when demand to engage is already high. At the laboratory level, biocompatibility studies, sterilization validation, and extractables and leachables programs can be stacked in sequence, creating long handoff times between work packages. These delays reduce throughput per engagement and can push manufacturers to delay launch or resubmission plans. Even so, the scarcity of qualified review and test capacity is also reinforcing pricing power for the most capable providers in the healthcare and medical devices TIC market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Certification Growth Outpaces Volume In The TIC Revenue Mix

Testing held 53.11% of the healthcare and medical devices testing, inspection, and certification (TIC) market in 2025, reflecting the fact that every new product or market entry usually begins with a mandatory testing package. The healthcare and medical devices TIC market still relies heavily on testing because electrical safety, biocompatibility, electromagnetic compatibility, sterility validation, and software verification are separate workstreams rather than a single bundled task. A single device can require 6 to 10 parallel or sequential protocols across accredited laboratories before the regulatory dossier is ready, front-loading revenue into testing even before certification is completed. Inspection services sat between testing and certification in terms of revenue, supported by supplier audits, factory acceptance tests, goods-in-process checks, and post-market review activities. This part of the healthcare and medical devices TIC industry has also benefited from EU MDR expectations for continuous post-market data collection, which supports recurring inspections after the initial launch phase.

Certification is the fastest-growing service segment and is projected to expand at a 5.05% CAGR from 2026 to 2031, indicating that the revenue mix is moving toward approval and system-level assurance. The healthcare and medical devices TIC market is seeing this shift because legacy devices still need transition work under the EU MDR, while North American quality systems are also aligning more closely with ISO 13485. Providers with notified body status are in the strongest position because certification demand is compressed into tight windows for higher-risk classes, and manufacturers cannot move forward without those approvals. ISO 13485 requirements are also expanding certification beyond finished device manufacturers to contract manufacturers, component suppliers, and software developers, who now need recognized quality credentials to remain in approved supply chains. The MDSAP model adds another layer of pull toward firms that can support multiple jurisdictions through a single structured audit cycle, giving scale players an edge in the healthcare and medical devices TIC industry.

By Sourcing Type: Structural Outsourcing Accelerates Alongside Regulatory Complexity

Outsourced services accounted for 69.32% of the healthcare and medical devices testing, inspection, and certification (TIC) market share in 2025 and are projected to grow at a 4.74% CAGR through 2031, which confirms that outsourcing is the dominant sourcing model. The healthcare and medical devices TIC market is moving this way because maintaining full in-house capability across testing, audits, quality system interpretation, and cross-border documentation is becoming too costly for many manufacturers.

The QMSR also embedded supplier quality oversight more firmly into the quality management system, meaning outsourced TIC partners now sit within a more formal compliance framework rather than outside it. Companies that once relied on informal lab relationships now need more structured agreements, clearer controls, and auditable records for those engagements. This deepens dependence on third-party providers and makes outsourcing a structural model rather than a short-term purchasing choice.

By Mode of Service Delivery: Digital Channels Expand Access Without Replacing Labs

Off-site and laboratory-based delivery dominated with 58.05% of revenue in 2025, which shows that physical test infrastructure still anchors the healthcare and medical devices testing, inspection, and certification (TIC) market. The reason is straightforward because biocompatibility, sterility, electrical safety, and chemical characterization work require controlled lab environments, traceable standards, and validated methods that cannot be virtualized. ISO/IEC 17025 remains the benchmark for laboratory competence, and that keeps accredited physical capacity at the center of regulatory-grade testing activity.[3]Nelson Labs, “Designing a Test Plan That Works Globally - A Medtech Makers Q&A,” Nelson Labs Nelson Labs alone supports more than 800 laboratory tests across 15 facilities, underscoring the significant fixed infrastructure that underpins specialist device testing programs. This makes laboratory delivery the default mode for authorization-critical work, even as documentation and audit processes become increasingly digital.

Remote and digital delivery is the fastest-growing mode and is forecast to expand at a 4.56% CAGR from 2026 to 2031, which shows how the healthcare and medical devices TIC market is widening access through digital workflows. Digital quality systems, AI-assisted documentation review, and greater acceptance of remote audit elements are helping providers serve smaller customers that may not have engaged as early in the past. At the same time, on-site delivery remains important for facility qualification, installation checks, process validation, and factory inspections, especially in the Asia-Pacific region, where new manufacturing sites continue to come online. Nelson Labs highlighted in April 2026 that globally oriented test planning is becoming a value-added advisory layer on top of physical testing capacity, reflecting the growing blend of lab work and digital planning support. The result is a service model in which digital tools expand reach and speed, but accredited laboratories still play the core economic role in the healthcare and medical devices TIC industry.

Geography Analysis

Asia-Pacific held 44.73% of the healthcare and medical devices TIC market share in 2025 and is also the fastest-growing regional market at a 4.87% CAGR through 2031. China remains the largest national market in the region because of its broad manufacturing base and the pull of local registration requirements that favor established testing and certification capacity. The healthcare and medical devices TIC market in Asia-Pacific is also benefiting from a broader manufacturing map, with strong investment across India, Vietnam, South Korea, and Thailand. Each new facility increases demand for qualification, validation, submission testing, and export compliance before output can scale to commercial levels. In April 2026, CJ Medtech broke ground on a new orthopedic device factory in South Korea, which reflects the kind of plant expansion that directly feeds regional demand for inspection and certification services.[4]Asia Business Daily, “Yonghyeon Industrial Complex in Uijeongbu Transforms into Bio Hub - CJ Medtech Co. Breaks Ground on New Factory,” The Asia Business Daily

North America holds the second-largest regional position and continues to generate some of the highest-value assignments in the healthcare and medical devices TIC market. The United States remains the core of that demand because it combines a large research and development base, a deep commercial pipeline, and strict regulatory expectations across software, cybersecurity, and quality systems. The FDA’s 2026 guidance cycle widened the documentation burden for connected devices and products that rely on real-world data after launch, thereby increasing testing and review workloads for service providers. Canada continues to channel manufacturers toward MDSAP-recognized audit routes, and Mexico supports testing demand through its role in regional supply chains tied to the United States. North America also retains the deepest pool of specialist laboratories for biocompatibility, cybersecurity, and combination product assessment, though some of that capability is now being mirrored in Asia-Pacific as manufacturing shifts closer to end markets.

Europe holds a notable share of the healthcare and medical devices TIC market and remains central, as the MDR and IVDR transition continues to reshape compliance needs across the region. The European Commission’s 19th Notified Body Survey confirmed 33,175 MDR applications and 17,549 issued certificates through December 2025, which shows why backlog-driven support demand remains elevated. Germany and the United Kingdom remain the largest individual markets in Europe, and manufacturers serving both the EU and UK still face extra work because the approval paths are no longer identical. Providers such as SGS have used their notified body and UK Approved Body positions to meet that dual requirement, thereby supporting recurring regional revenue from certification, surveillance, and system audits. Middle East and Africa, along with South America, remain smaller in current value, but hospital investment, rising local production ambitions, and growing regulatory formalization are giving the healthcare and medical devices TIC market a broader long-term geographic base.

Competitive Landscape

The healthcare and medical devices TIC market is moderately consolidated, with SGS, Intertek, Bureau Veritas, TÜV SÜD, TÜV Rheinland, and Eurofins Scientific forming the top competitive tier through scale, authorizations, and notified body reach. The healthcare and medical devices TIC market favors these firms because large medtech customers increasingly want providers that can manage testing, audits, certification, and documentation across multiple jurisdictions under a single commercial relationship. SGS strengthened that position in January 2026 when it closed the acquisition of Applied Technical Services, a North American TIC platform with projected 2026 revenue of USD 460 million. In May 2026, SGS also acquired Keystone Bioanalytical to deepen its GLP-compliant bioanalytical capabilities in North America and expand its role across drug development and medical device life-cycle testing. SGS has also highlighted its ability to support MDR, IVDR, UKCA, MDSAP, and ISO 13485 pathways through a unified model, which shows why multi-authorization breadth matters so much in this market.

Portfolio moves across the top tier also show how firms are repositioning within the healthcare and medical devices TIC market. UL Solutions signed an agreement in 2026 to acquire Eurofins Scientific’s Electrical and Electronics business, a move that expands capability across medical device, electromagnetic compatibility, and wireless testing in Europe, the Middle East and Africa, and Asia-Pacific. Intertek announced a strategic review in April 2026 to assess a separation into 2 independently listed businesses, which could change how its healthcare TIC assets are organized and deployed against specialist rivals.[5]Intertek, “U.S. FDA Reissues Medical Device Cybersecurity Guidance to Align with QMSR,” Intertek Element Materials Technology also expanded its Huntsville laboratory in May 2026, reinforcing the importance of regulated test capacity as a competitive asset in high-compliance sectors, including medical devices. These moves matter because scale alone is no longer enough, and providers now need targeted depth in bioanalytical work, wireless testing, cybersecurity, and advanced materials characterization. The healthcare and medical devices TIC market is, therefore, rewarding firms that combine broad regulatory access with selective specialist strength.

Even with strong global leaders, competition in the healthcare and medical devices TIC market remains active at the service-line level. Specialist players such as Nelson Laboratories, NAMSA, and Element Materials Technology continue to defend their position through deep capability in sterilization validation, biocompatibility, and extractables and leachables testing that generalist networks do not always match at the same quality level. This is why disruption is happening more within specific test categories than across the entire provider landscape. Pricing power is strongest where notified body access is scarce or where specialist laboratory capacity is hard to replicate, especially in Europe and in higher-complexity device classes. At the same time, digital documentation review, remote audit support, and cybersecurity testing remain open areas where focused entrants can still challenge the largest firms in the healthcare and medical devices TIC market.

Healthcare And Medical Devices TIC Industry Leaders

SGS SA

Intertek Group plc

TÜV SÜD AG

Eurofins Scientific SE

Bureau Veritas SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: SGS acquired Keystone Bioanalytical, a Philadelphia, Pennsylvania-based GLP-compliant bioanalytical testing provider, strengthening its end-to-end drug development and medical device lifecycle testing services in North America, directly advancing its Strategy 27 objective to double North American sales between 2023 and 2027.

- May 2026: Commission Implementing Regulation (EU) 2026/977 was published in the Official Journal of the EU on May 5, 2026, establishing uniform quality management and procedural requirements for notified bodies under MDR and IVDR, including maximum certification timelines and clock-stop rules, which apply from February 25, 2027.

- May 2026: Element Materials Technology expanded its Huntsville, Alabama, laboratory into a strategic hub for innovation, deepening testing capabilities across highly regulated industries, including medical devices. Its global network now exceeds 270 laboratories and 8,500 scientists, engineers, and technologists.

- April 2026: Intertek announced a strategic review to assess whether to separate into 2 independently listed businesses, Intertek Testing and Assurance, and Intertek Energy and Infrastructure, with significant implications for how its healthcare TIC assets are deployed and competitively positioned.

Global Healthcare And Medical Devices TIC Market Report Scope

The Healthcare and Medical Devices Testing, Inspection, and Certification (TIC) market comprises services that assess, verify, validate, and certify healthcare products, medical devices, equipment, components, manufacturing processes, and quality management systems to ensure compliance with regulatory requirements, safety standards, performance specifications, and industry best practices. These services support manufacturers, healthcare providers, and other stakeholders in meeting national and international regulations, enhancing product quality, mitigating risks, and facilitating market access.

The Healthcare and Medical Devices TIC Report is Segmented by Service Type (Testing, Inspection, and Certification), Sourcing Type (In-house, and Outsourced), Mode of Service Delivery (On-site, Off-site/Laboratory, and Remote/Digital), and Geography (North America, Europe, Asia-Pacific, Middle East, Africa, and South America). The Market Forecasts are Provided in Terms of Value (USD).

| Testing |

| Inspection |

| Certification |

| In-house |

| Outsourced |

| On-site |

| Off-site / Laboratory |

| Remote / Digital |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Service Type | Testing | |

| Inspection | ||

| Certification | ||

| By Sourcing Type | In-house | |

| Outsourced | ||

| By Mode of Service Delivery | On-site | |

| Off-site / Laboratory | ||

| Remote / Digital | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the 2026 size of the healthcare and medical devices TIC market?

The healthcare and medical devices TIC market stands at USD 7.67 billion in 2026 and is projected to reach USD 9.47 billion by 2031 at a 4.31% CAGR.

Which service area leads revenue in healthcare and medical devices TIC?

Testing leads the revenue mix with a 53.11% share in 2025 because every device program needs multiple mandatory test protocols before filing or approval.

Why are outsourced TIC services growing faster in medical devices?

Outsourced services held 69.32% of revenue in 2025 and are growing at 4.74% CAGR because smaller and mid-sized manufacturers increasingly rely on external compliance expertise.

Which region is strongest for healthcare and medical devices TIC demand?

Asia-Pacific leads with 44.73% of global revenue in 2025 and is also the fastest-growing region through 2031, supported by expanding manufacturing and export certification needs.

What is driving certification demand in this sector?

Certification is projected to grow at a 5.05% CAGR as legacy devices move through MDR transition requirements and manufacturers seek broader ISO 13485 and multi-country audit coverage.

How are digital services changing medical device TIC delivery?

Remote and digital delivery is the fastest-growing mode at 4.56% CAGR, but it is expanding access and speed rather than replacing physical laboratory testing infrastructure.

Page last updated on: