HDMI Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

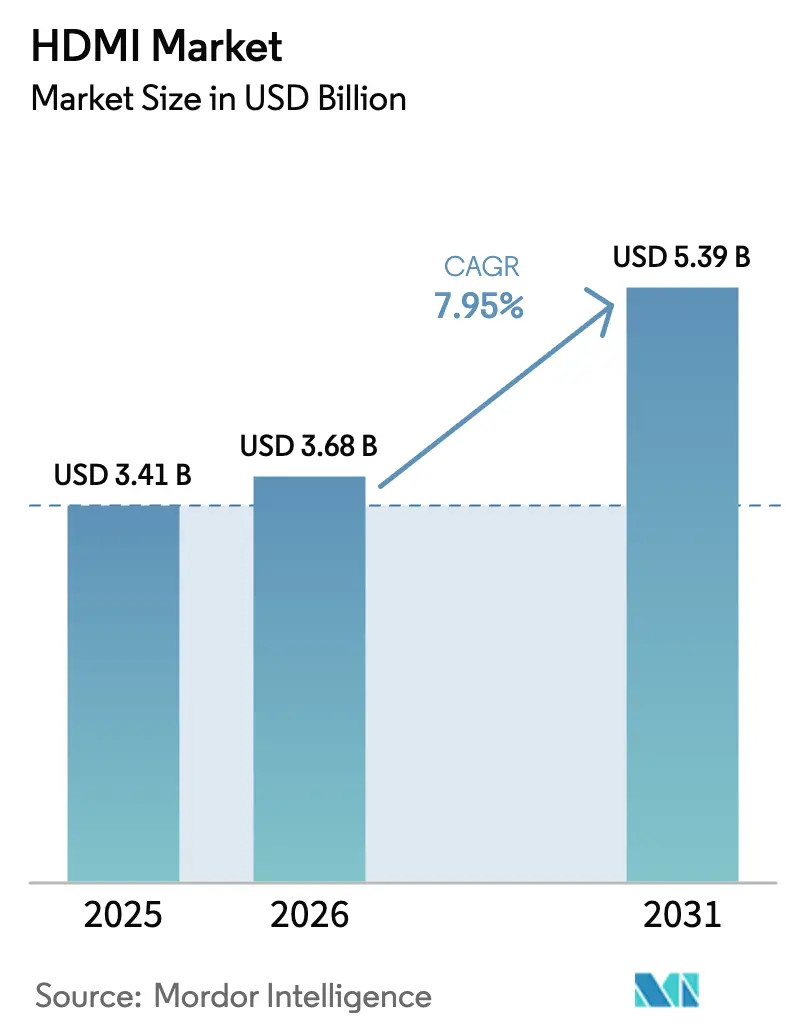

| Market Size (2026) | USD 3.68 Billion |

| Market Size (2031) | USD 5.39 Billion |

| Growth Rate (2026 - 2031) | 7.95% CAGR |

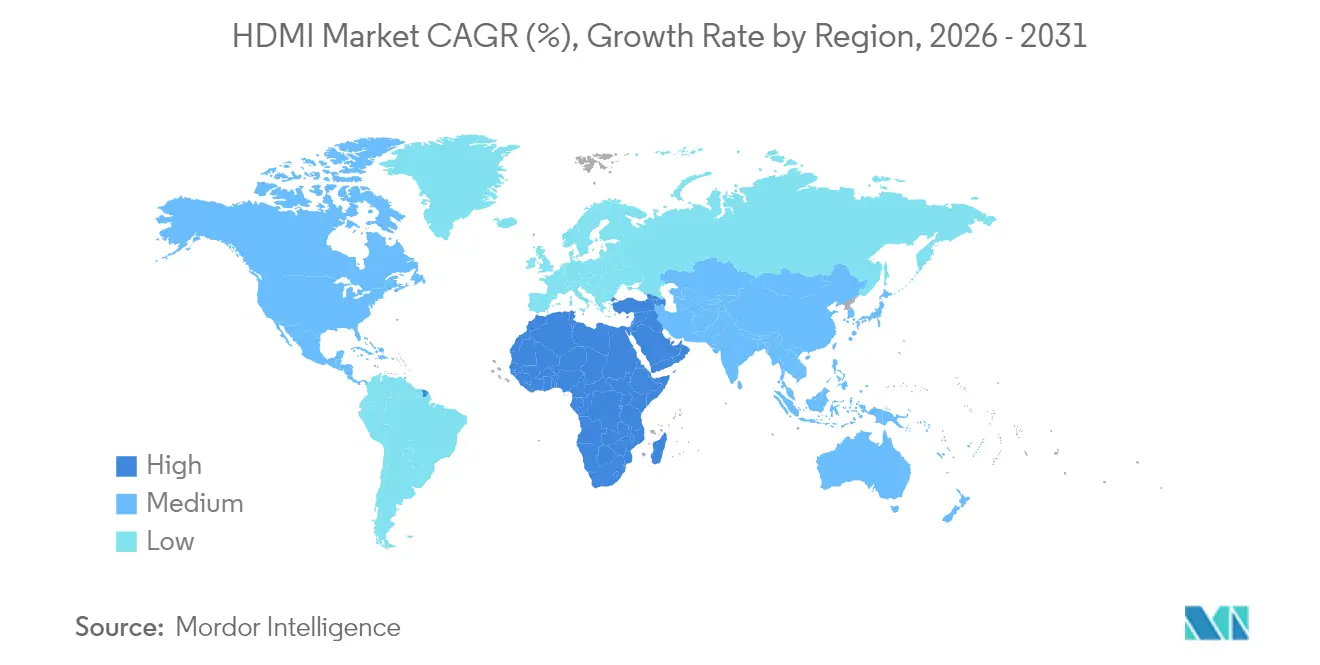

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

HDMI Market Analysis by Mordor Intelligence

The HDMI market size was valued at USD 3.41 billion in 2025 and estimated to grow from USD 3.68 billion in 2026 to reach USD 5.39 billion by 2031, at a CAGR of 7.95% during the forecast period (2026-2031). Demand is expanding as 8K and 16K display ecosystems move from concept to commercial reality, automotive infotainment systems migrate toward multi-screen cockpits, and professional AV installations standardize on single-cable infrastructure. The roll-out of HDMI 2.2 with 96 Gbps bandwidth ensures the interface remains relevant for ultra-high-resolution video while supporting emerging latency-sensitive use cases in gaming and e-sports. Asia-Pacific dominates the HDMI market on the strength of vertically integrated electronics supply chains, whereas the Middle East & Africa is accelerating fastest as governments fund smart-city projects and digital-learning initiatives. Continued consolidation-in particular Amphenol’s acquisition of CommScope’s mobile-networks units-signals a strategic shift toward vertically integrated portfolios spanning wired, optical and RF connectivity.

Key Report Takeaways

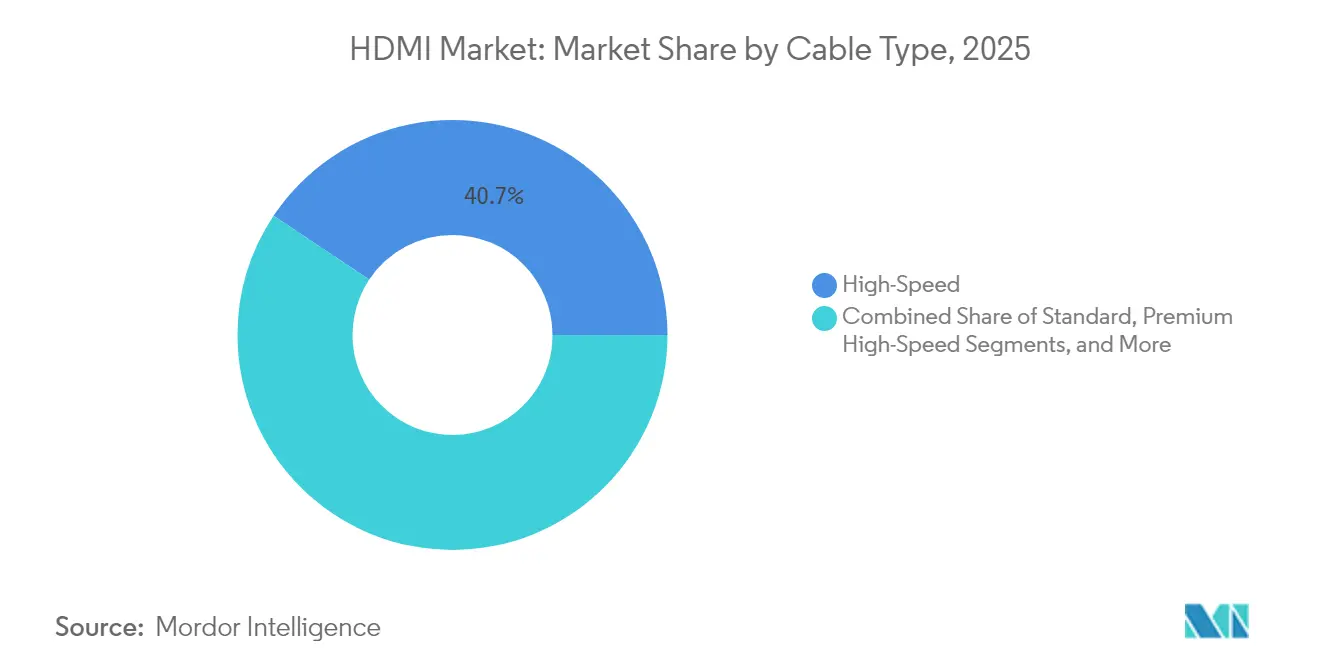

- By cable type, High-Speed held 40.65% of the HDMI market share in 2025, while Ultra High-Speed is on track for the highest 9.28% CAGR through 2031.

- By connector, Type A led with 75.92% share of the HDMI market size in 2025; Type E automotive connectors are forecast to expand at 8.32% CAGR out to 2031.

- By HDMI version, Version 2 retained 58.02% share in 2025, yet Version 2.1 is advancing at a 10.06% CAGR on the back of 8K TV adoption.

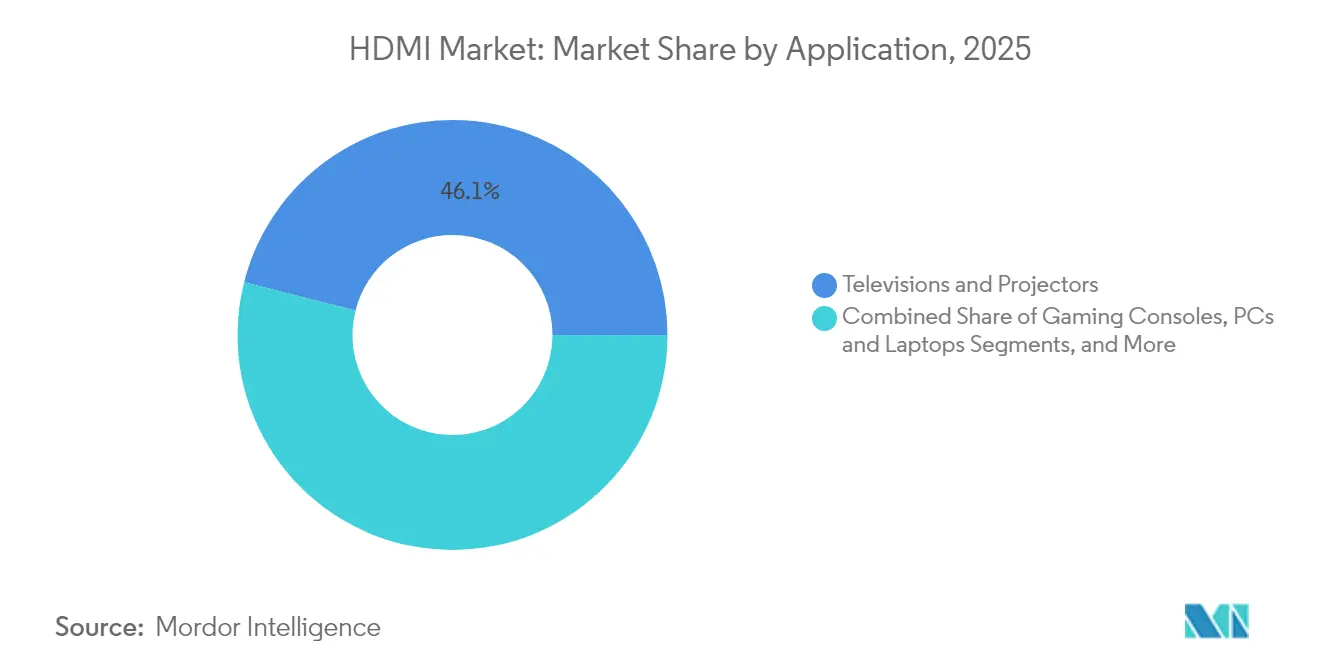

- By application, televisions and projectors captured 46.05% of the HDMI market share in 2025, while automotive infotainment is expected to post the fastest 9.74% CAGR to 2031.

- By geography, Asia-Pacific contributed 38.12% revenue in 2025; the Middle East & Africa region is projected to grow at 9.41% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global HDMI Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in 8K TV adoption requiring Ultra High-Speed HDMI 2.1 cables | +1.8% | East Asia, North America | Medium term (2-4 years) |

| Automakers integrating advanced infotainment & ADAS connectivity | +1.5% | Global, notable in North America & EU | Long term (≥ 4 years) |

| Expansion of e-sports arenas demanding low-latency switchers | +0.9% | North America, rising in APAC | Short term (≤ 2 years) |

| EU mandates for single-cable smart-classroom AV infrastructure | +0.7% | Europe, spillover to other developed markets | Medium term (2-4 years) |

| Rapid OTT set-top uptake driving low-cost dongles | +1.2% | South Asia, emerging markets | Short term (≤ 2 years) |

| Semiconductor advances enabling 100 m active optical HDMI cables | +1.1% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in 8K television adoption requiring Ultra High-Speed HDMI 2.1 cables

Ultra High-Speed cabling is moving into mainstream retail channels as display makers upgrade port counts from two to four full-bandwidth interfaces. MediaTek’s Pentonic 800 system-on-chip allows mid-tier TV brands to support four HDMI 2.1 inputs, eliminating prior multi-device bottlenecks.[1]MediaTek Inc., “Pentonic 800 Press Release,” mediatek.com The Consumer Technology Association confirms that 4K sets now exceed 50% penetration in US households, laying the groundwork for an 8K replacement cycle that will reinforce premium cable demand.[2]Consumer Technology Association, “Ultra HD Television Fact Sheet,” cta.tech Hisense has committed to ship 2025 models with four HDMI 2.1 ports, underscoring how high-end I/O is cascading into mass-market segments.

Automakers integrating advanced infotainment and ADAS connectivity

Automotive OEMs are embedding multiple 4K interior displays, gesture interfaces and augmented-reality head-up units that each require multi-gigabit links. Type E ruggedized HDMI connectors meet automotive vibration and temperature standards, propelling an 8.7% CAGR for this form-factor. While MIPI A-PHY offers stronger EMI immunity, HDMI’s broad ecosystem and backward compatibility motivate consortium initiatives to tighten reliability specs for in-vehicle deployments.

Expansion of e-sports arenas demanding low-latency switchers

Professional gaming venues are investing in latency-monitored matrices that juggle dozens of simultaneous 4K120 streams without compression. The new Latency Indication Protocol introduced in HDMI 2.2 gives integrators real-time path diagnostics, a prerequisite for time-synced tournament broadcasting. Gaming console traffic, already 46.7% of application revenue in 2024, continues to anchor this specialist demand.

EU mandates for single-cable smart-classroom AV infrastructure

A EUR 210 million European Commission framework for education technology stipulates unified audio-video wiring, accelerating HDMI-over-single-cable roll-outs. Professional integrators now specify hybrid copper-fiber solutions that future-proof learning spaces against upcoming 16K displays while retaining HDMI’s universal device compatibility.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising adoption of USB-C Alt-Mode in mobile & laptop segments | -1.3% | Global, premium devices | Medium term (2-4 years) |

| Copper & rare-earth volatility elevating average selling prices | -0.8% | Global | Short term (≤ 2 years) |

| Thermal-reliability limits in automotive extremes vs MIPI A-PHY | -0.6% | Global automotive markets | Long term (≥ 4 years) |

| HDMI 2.1 IP royalty burden on smaller OEMs | -0.4% | Global, emerging markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising adoption of USB-C Alt-Mode in mobile & laptop segments

USB-C Alt-Mode transports 4K video over a reversible connector, permitting thinner devices to drop a discrete HDMI jack.[3]HDMI Licensing Administrator, “USB-C Alt-Mode Specification,” hdmi.org Yet it commandeers all four high-speed lanes, precluding simultaneous USB data throughput and capping scalability beyond HDMI 1.4 performance levels. Industry observers expect coexistence rather than replacement, particularly in gaming laptops and creator notebooks that need full-bandwidth HDMI 2.1 outputs.

Copper and rare-earth volatility elevating average selling prices

Benchmark copper prices have climbed 75% since 2020 as energy-transition projects strain supply. UNCTAD warns demand could outstrip refined capacity by more than 40% by 2040, squeezing cable gross margins and disadvantaging small assemblers with limited hedging options.[4]UNCTAD, “Global Trade Update – Copper,” unctad.org Tier-one suppliers counteract volatility through optical-fiber substitution that reduces copper content per meter and unlocks premium positioning.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Cable Type: Ultra High-Speed Commands the Upgrade Cycle

High-Speed cables retained the largest 40.65% share of the HDMI market in 2025, underpinning a sizeable installed base of 4K televisions and consoles. Ultra High-Speed, however, leads growth at a 9.28% CAGR, propelled by 8K60 and 4K144 gaming requirements. Hybrid active-optical designs are entering volume as OEMs seek to exceed 10 m runs without amplifiers, signalling a qualitative shift toward fiber-rich architectures.

Active optical innovation elevates carrying capacity to 48 Gbps and beyond while mitigating electromagnetic interference, essential in medical imaging theatres and broadcast back-bones. Amphenol’s 100 m HDMI 2.0 AOC validates the commercial case for long-distance, zero-latency transport. As component costs fall, active optical is expected to erode copper’s dominance and broaden the addressable HDMI market across enterprise and defense installations.

By Connector Type: Type A Ubiquity Faces Automotive Disruption

Type A connectors accounted for 75.92% of the HDMI market size in 2025, reflecting near-universal integration across TVs, set-top boxes and PCs. Automotive-grade Type E variants, sealed against vibration and fluid ingress, are forecast to record the fastest 8.32% CAGR through 2031 as cockpit digitization accelerates. Mini (Type C) and Micro (Type D) footprints remain common in action cameras and single-board computers but confront pressure from USB-C Alt-Mode convergence.

Vehicle OEMs demand connectors validated to 125 °C ambient and 1,000 h cyclic vibration, hurdles that most consumer-grade HDMI sockets cannot meet. Suppliers capable of meeting AEC-Q100 and ISO 16750 test regimens therefore command pricing premiums, tilting competitive balance toward entrenched interconnect specialists. The specialized nature of Type E also reduces substitution risk, underpinning a defensible growth niche within the broader HDMI market.

By HDMI Version: 2.1 Becomes the New Baseline

Version 2.0 maintained 58.02% revenue share in 2025, yet Version 2.1 is scaling fastest at 10.06% CAGR as 120 Hz gaming and 8K streaming migrate to mid-range products. Feature sets such as Variable Refresh Rate, Dynamic HDR and Auto Low-Latency Mode are now prerequisites for console certification programs, speeding OEM transition timelines.

The launch of HDMI 2.2 doubles aggregate bandwidth to 96 Gbps and introduces a real-time latency metric, pre-empting competitive claims from DisplayPort 2.1 and proprietary automotive links. Semiconductor IP vendors already offer drop-in PHY blocks for FPGAs and ASICs, which compress R&D cycles and democratize access to the latest revision. Ecosystem momentum, therefore, remains a strong tail-wind for the HDMI market.

By Application: Automotive Infotainment Races Ahead

Televisions and projectors delivered 46.05% of the HDMI market share in 2025 and continue to anchor volumes. Automotive infotainment, however, is the fastest-expanding application with a 9.74% CAGR as electric-vehicle architectures favor centralized compute and high-resolution dashboards. Gaming consoles sustain demand for ultra-low-latency signal chains, while professional digital signage benefits from single-cable power-data solutions deployed in transportation hubs and sports arenas.

Automotive platforms now integrate rear-seat entertainment, instrument clusters and augmented-reality HUDs, each linked via shielded high-bandwidth connections. As Level-3 autonomy proliferates, display count-and therefore interface points-will rise, further enlarging the HDMI market size within the mobility sector.

By End-user Industry: OEM Consolidation Shapes Demand

Consumer-electronics companies held 60.22% revenue share in 2025, yet automotive OEMs and tier-1 suppliers exhibit the highest 9.02% CAGR through 2031. Media and entertainment venues deploy professional switchers to support live 8K feeds, whereas healthcare adopts HDMI for endoscopic imaging and surgical robotics. Industrial automation vendors integrate rugged mini-connectors into operator panels, illustrating HDMI’s reach beyond its entertainment roots.

Automotive growth catalyzes partnerships between chipmakers, interconnect specialists and dashboard integrators. Suppliers that offer AEC-Q-qualified connectors plus optical-copper hybrids differentiate themselves in a segment intolerant of packet errors or thermal failures, reinforcing barriers to entry for commodity cable assemblers.

By Distribution Channel: OEM-Direct Engagement Rises

Retail and e-commerce retained 57.25% of the HDMI market in 2025, reflective of consumer-skewed volumes. OEM-direct supply is expanding at 8.12% CAGR as automakers, display manufacturers and avionics firms demand customized pin-outs, over-moldings and in-line signal conditioners. Tight design-win cycles and the need for application-specific compliance testing shift procurement from catalog distribution to strategic supplier alliances.

As product complexity climbs-particularly with active-optical hybrids-deep technical support becomes a differentiator, encouraging closer OEM-supplier relationships. This channel evolution reinforces the strategic importance of vertically integrated connectivity providers.

Geography Analysis

Asia-Pacific contributed 38.12% of global revenue in 2025 on the back of China’s scale manufacturing, Japan’s advanced display fabs and South Korea’s leading TV brands. Regional chip houses such as MediaTek accelerate HDMI port proliferation, while local standards initiatives explore next-generation 192 Gbps interfaces to hedge against foreign IP reliance. Integrated supply chains compress development cycles and underpin competitive pricing, helping Asia maintain leadership in the HDMI market.

North America exhibits high per-capita spending on premium home theater, e-sports arenas and automotive innovation. This translates into above-average ASPs for 48 Gbps Ultra High-Speed cables and professional-grade matrix switchers. Europe prioritizes regulatory compliance; a EUR 210 million procurement for smart-classroom AV solutions formalizes single-cable mandates, ensuring predictable demand for certified vendors.

The Middle East & Africa is projected to chart a 9.41% CAGR through 2031 as smart-city, hospitality and education projects roll out UHD signage and distance-learning platforms. Gulf Cooperation Council investments catalyze large-venue display deployments, while African telecoms expansion stimulates set-top uptake. South America shows steady uptake led by Brazil, although currency volatility occasionally tempers consumer electronics imports.

Competitive Landscape

The HDMI market displays moderate concentration: the five largest vendors account for just under 50% of revenue, yielding room for niche specialists and regional assemblers. Amphenol’s USD 2.1 billion purchase of CommScope’s outdoor wireless assets in 2025 illustrates a strategy of broadening connectivity portfolios across copper, optical and RF. TE Connectivity is investing in active-optical R&D to capture long-run broadcast and medical opportunities, whereas Molex leverages automotive design-in experience to secure dashboard interface contracts.

Intellectual-property stewardship remains central; the HDMI Licensing Administrator lists nearly 1,900 active adopters, creating a large yet controlled ecosystem that penalizes non-compliant clones. Cost-sensitive OEMs in emerging markets face licensing-fee and test-lab hurdles, indirectly encouraging consolidation toward better-capitalized suppliers. Meanwhile, automotive-specific links like MIPI A-PHY threaten share within vehicles, prompting the HDMI Forum to prioritize electromagnetic robustness in upcoming revisions.

Product innovation is tilting toward fiber-rich hybrids: Amphenol Socapex’s 100 m HDMI 2.0 active-optical cable won navy-sector accolades and validates a premium tier unsuited to low-cost rivals. Strategic direction therefore revolves around integrating optical transceivers, refining automotive thermals and reinforcing compliance services—each raising new entry barriers and shaping future HDMI market dynamics.

HDMI Industry Leaders

Aten International Co. Ltd.

Belkin International Inc.

Nordost Cables

The Chord Company Ltd.

Extron

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: HDMI Forum released the HDMI 2.2 specification supporting 16K60 and doubling throughput to 96 Gbps.

- May 2025: HDMI Licensing Administrator promoted the new standard at Computex, spotlighting AI workloads and Ultra96 gaming features.

- April 2025: Amphenol reported record Q1 2025 sales of USD 4.8 billion, citing IT datacom and interconnect demand.

- January 2025: Amphenol closed its USD 2.1 billion purchase of CommScope’s mobile-networks businesses, adding USD 1.2 billion in projected annual sales.

- December 2024: Amphenol Socapex introduced a 100 m HDMI 2.0 active-optical cable that needs no external power.

Global HDMI Market Report Scope

HDMI, or high-definition multimedia interface, is a standard for transmitting top-notch audio and video signals. It was designed to supersede analog audio/video cables, including the DVI connector, which is used for specific applications. The study tracks the revenue generated from selling several types of HDMI cables utilized in several applications. It also tracks the market's drivers, challenges, and macroeconomic factors.

HDMI market is segmented by cable type (standard, high-speed, premium high-speed, and ultra high-speed), connector type (type A [standard], type B [dual-link], type C [mini], type D [micro], and type E), application (gaming consoles, TVs, mobile phones, automotive systems, laptops and tablets, and others), and geography (North America, Europe, Asia, Australia and New Zealand, Latin America, and Middle East and Africa). The market sizes and forecasts are provided in terms of value in USD for all the above segments.

| Standard |

| High-Speed |

| Premium High-Speed |

| Ultra High-Speed |

| Active Optical |

| Type A (Standard) |

| Type B (Dual-link) |

| Type C (Mini) |

| Type D (Micro) |

| Type E (Automotive) |

| 1.4 and Earlier |

| 2 |

| 2.1 |

| Gaming Consoles |

| Televisions and Projectors |

| Smartphones and Tablets |

| Automotive Infotainment Systems |

| PCs and Laptops |

| Digital Signage and Commercial Displays |

| Other Applications |

| Consumer Electronics OEMs |

| Automotive OEMs and Tier-1s |

| Media and Entertainment Venues |

| IT and Telecom |

| Healthcare |

| Industrial and Others |

| OEM Direct |

| Retail and E-commerce |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Nordics | ||

| Rest of Europe | ||

| South America | Brazil | |

| Rest of South America | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South-East Asia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Gulf Cooperation Council Countries |

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Cable Type | Standard | ||

| High-Speed | |||

| Premium High-Speed | |||

| Ultra High-Speed | |||

| Active Optical | |||

| By Connector Type | Type A (Standard) | ||

| Type B (Dual-link) | |||

| Type C (Mini) | |||

| Type D (Micro) | |||

| Type E (Automotive) | |||

| By HDMI Version | 1.4 and Earlier | ||

| 2 | |||

| 2.1 | |||

| By Application | Gaming Consoles | ||

| Televisions and Projectors | |||

| Smartphones and Tablets | |||

| Automotive Infotainment Systems | |||

| PCs and Laptops | |||

| Digital Signage and Commercial Displays | |||

| Other Applications | |||

| By End-user Industry | Consumer Electronics OEMs | ||

| Automotive OEMs and Tier-1s | |||

| Media and Entertainment Venues | |||

| IT and Telecom | |||

| Healthcare | |||

| Industrial and Others | |||

| By Distribution Channel | OEM Direct | ||

| Retail and E-commerce | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Nordics | |||

| Rest of Europe | |||

| South America | Brazil | ||

| Rest of South America | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South-East Asia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Gulf Cooperation Council Countries | |

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size of the HDMI market?

The HDMI market is valued at USD 3.68 billion in 2026 and is projected to reach USD 5.39 billion by 2031 at a 7.95% CAGR during 2026-2031.

Which cable type is growing fastest?

Ultra High-Speed cables are expanding at a 9.28% CAGR through 2031, driven by 8K and high-frame-rate gaming requirements.

Why is the automotive sector important for HDMI?

Automotive infotainment and ADAS displays need rugged, high-bandwidth links; Type E connectors are therefore posting an 8.32% CAGR, making vehicles the fastest-growing application.

How does HDMI 2.2 improve on previous versions?

HDMI 2.2 doubles aggregate bandwidth to 96 Gbps, supports 16K60 video, and introduces latency-indication metrics for real-time synchronization in gaming and pro-AV.

What regions are seeing the fastest market growth?

The Middle East and Africa region is projected to grow at 9.41% CAGR through 2031 as smart-city and digital-learning investments accelerate connectivity demand.

How is supply-chain volatility affecting HDMI pricing?

Copper price inflation and rare-earth scarcity are pushing average selling prices higher, prompting suppliers to adopt fiber-rich active-optical designs that reduce copper dependence while supporting premium margins.

Page last updated on: