HbA1c Testing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

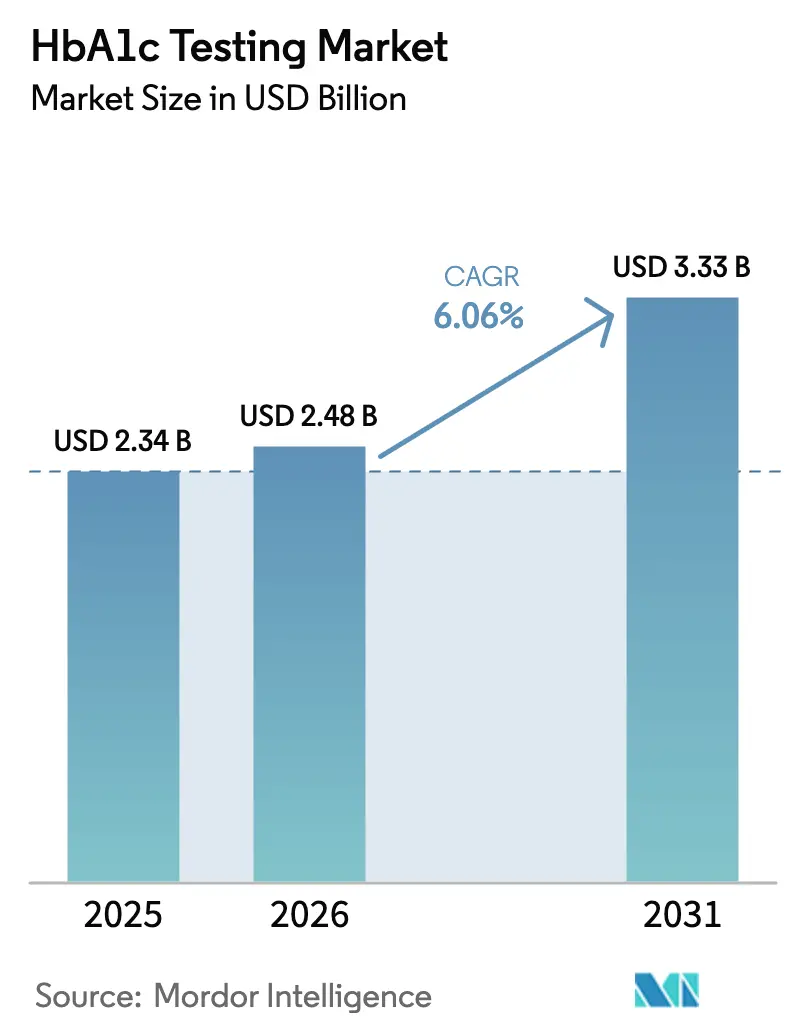

| Market Size (2026) | USD 2.48 Billion |

| Market Size (2031) | USD 3.33 Billion |

| Growth Rate (2026 - 2031) | 6.06% CAGR |

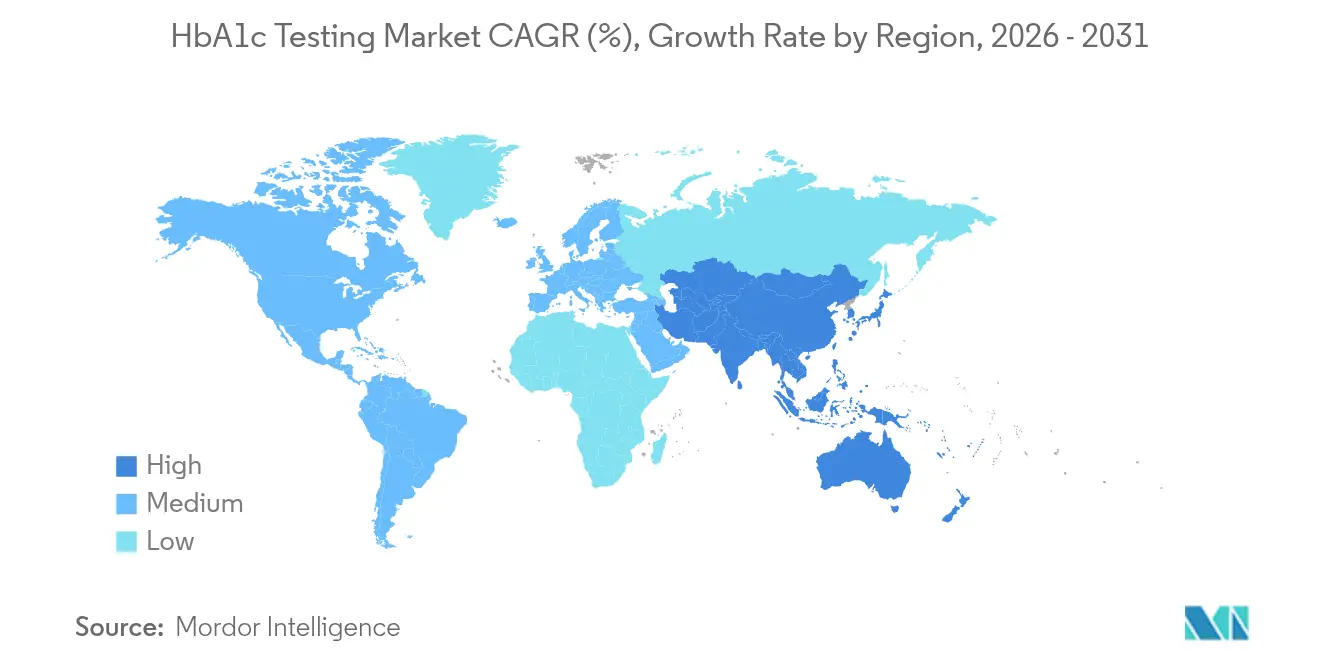

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

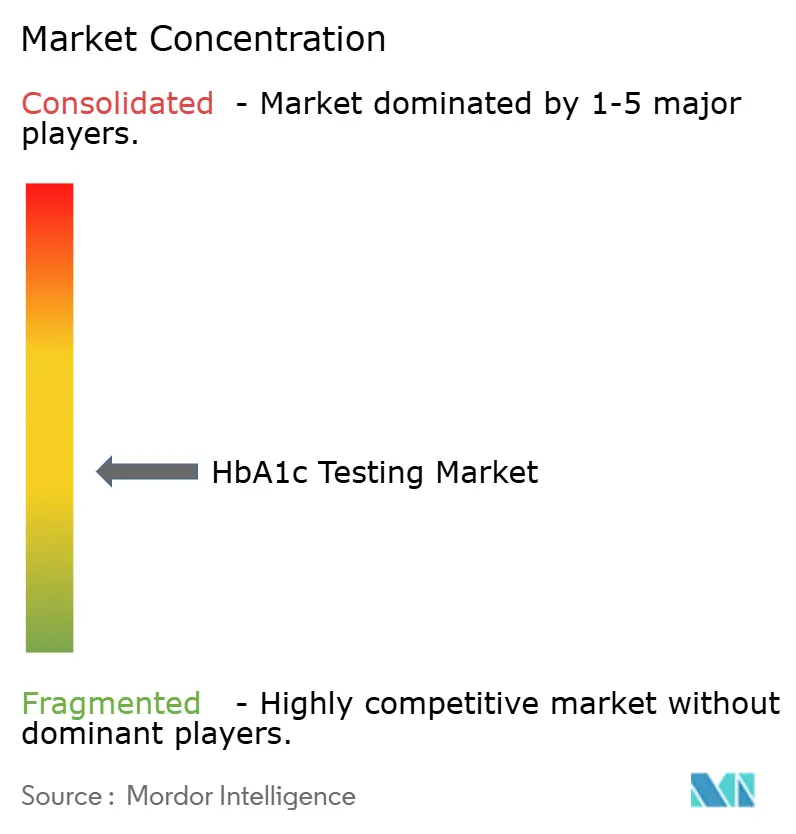

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

HbA1c Testing Market Analysis by Mordor Intelligence

The HbA1c testing market size was valued at USD 2.34 billion in 2025 and estimated to grow from USD 2.48 billion in 2026 to reach USD 3.33 billion by 2031, at a CAGR of 6.06% during the forecast period (2026-2031). Demand is expanding as diabetes prevalence rises [1]International Diabetes Federation, “IDF Diabetes Atlas 10th Edition,” idf.org , point-of-care technologies mature and value-based care reimbursement models widen test coverage. Integrated care programs that couple continuous glucose monitoring with routine HbA1c measurement are accelerating procurement cycles, while supply chain normalization is restoring steady access to reagents and cartridges. Leading manufacturers are investing in microfluidic single-use test formats that reduce per-test costs, making decentralized screening financially viable for primary care clinics in low- and middle-income countries. Larger reference laboratories are simultaneously scaling high-throughput HPLC capacity to manage growing specimen volumes linked to earlier screening guidelines across North America, Europe and parts of Asia-Pacific.

Key Report Takeaways

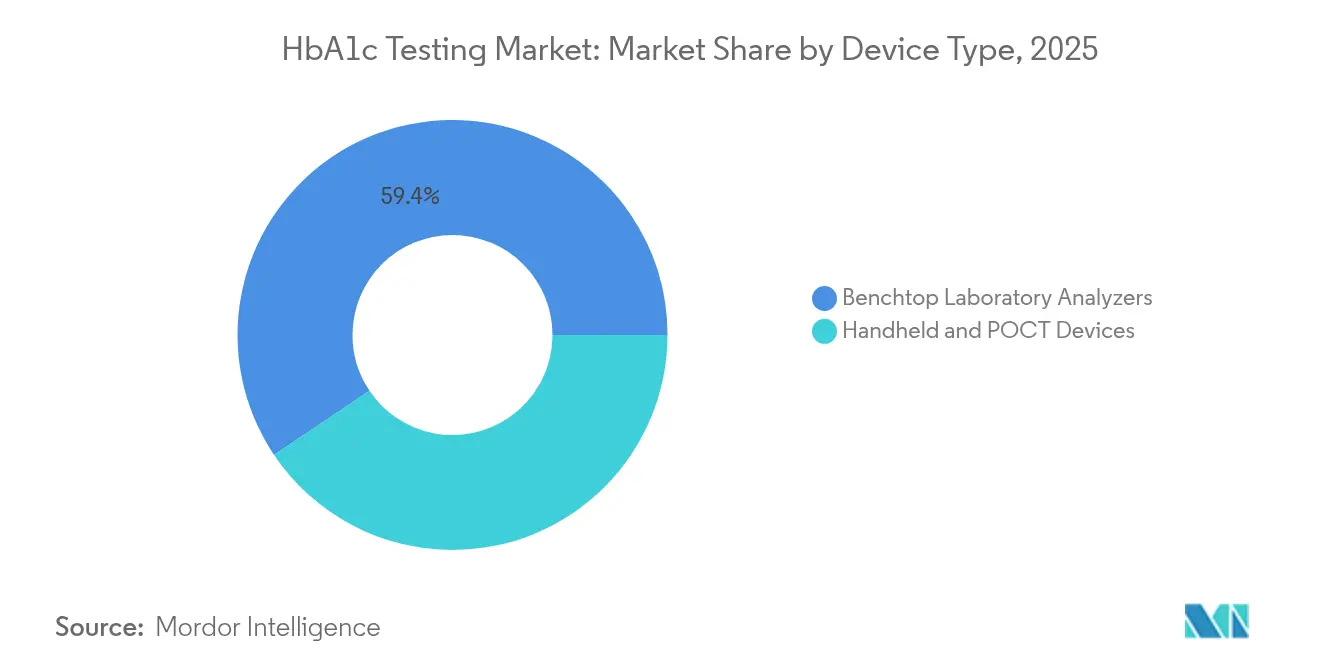

- By device type, benchtop analyzers led with 59.42% revenue share in 2025; handheld point-of-care systems are projected to expand at a 6.92% CAGR to 2031.

- By technology, HPLC held 61.12% of the HbA1c market share in 2025; immunoassay platforms are advancing at a 7% CAGR through 2031.

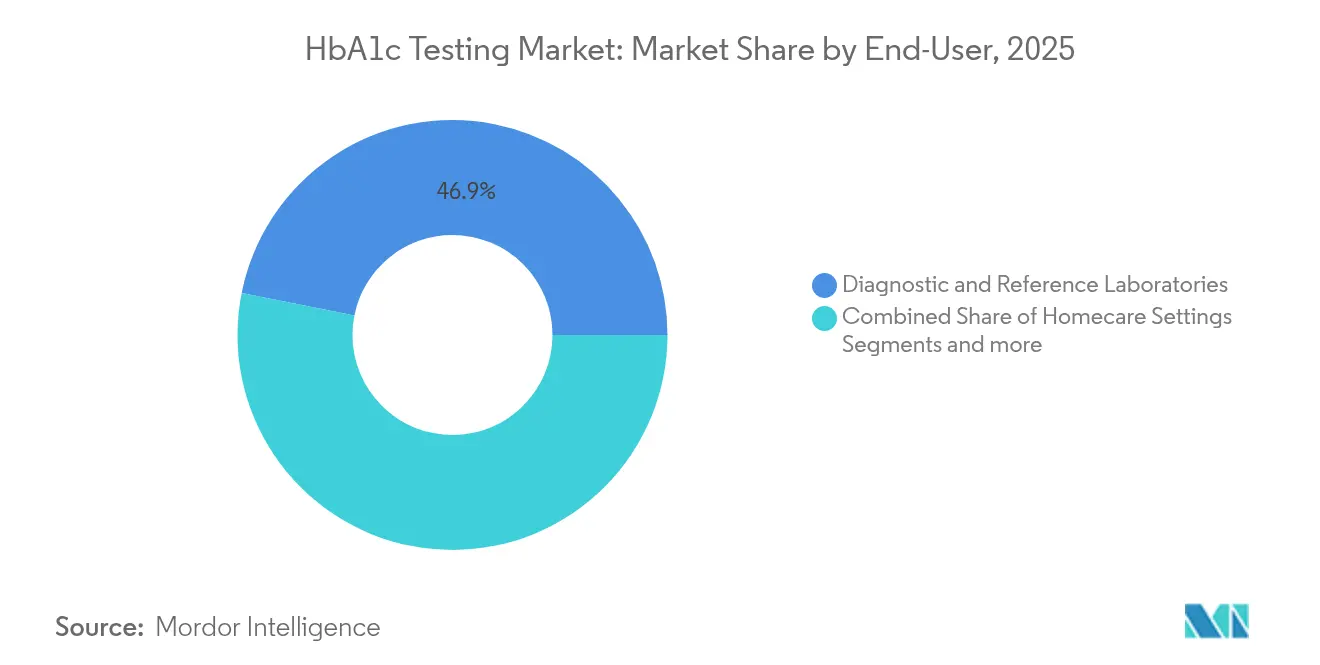

- By end-user, diagnostic and reference laboratories accounted for 46.87% of the HbA1c market size in 2025, while homecare settings post the highest 7.05% CAGR through 2031.

- By patient age group, adults represented 58.03% revenue share in 2025; the geriatric cohort is set to grow the quickest at 6.95% CAGR.

- By geography, North America dominated with 41.12% share in 2025; Asia-Pacific is the fastest-growing region at a 7.13% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global HbA1c Testing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Global Diabetes Prevalence & Earlier Screening Guidelines | +1.8% | Global, with highest impact in Asia-Pacific and Middle East | Long term (≥ 4 years) |

| Growing Uptake of Point-Of-Care HbA1c Analyzers in Primary Care Settings | +1.2% | North America & Europe, expanding to APAC | Medium term (2-4 years) |

| Expansion Of HbA1c-Based Reimbursement/Quality Metrics in Value-Based Care Contracts | +0.9% | North America primarily, early adoption in Europe | Medium term (2-4 years) |

| Rapid Price Declines in Microfluidic Single-Use HbA1c Cartridges for LMIC Mass-Screening | +0.7% | Asia-Pacific, Latin America, Sub-Saharan Africa | Long term (≥ 4 years) |

| Employer-Funded Wellness Programs Mandating Annual HbA1c Checks | +0.4% | North America, expanding to developed APAC markets | Short term (≤ 2 years) |

| AI-Enabled Decision-Support Improving Demand for Lab-Quality HbA1c Datasets | +0.3% | Global, with early adoption in North America & Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising global diabetes prevalence & earlier screening guidelines

Diabetes prevalence is projected to reach 1.31 billion individuals by 2025, intensifying demand for accessible HbA1c testing solutions. Earlier screening recommended by the American Diabetes Association places HbA1c as the primary diagnostic metric, prompting laboratories to expand throughput [2]American Diabetes Association, “Standards of Care in Diabetes 2024,” diabetesjournals.org . Health systems face rising economic burdens, with the United States spending USD 413 billion on diabetes care in 2022, reinforcing the push for early detection. The World Health Organization includes HbA1c on its Essential Diagnostics List, underscoring its global relevance [3]Ke‐Jie He, "Global burden of type 2 diabetes mellitus from 1990 to 2021, with projections of prevalence to 2044: a systematic analysis across SDI levels for the global burden of disease study 2021," Frontiers in Endocrinology, frontiersin.org. Greater awareness in low-income regions is stimulating procurement of cost-efficient test kits suitable for decentralized programs.

Growing uptake of point-of-care HbA1c analyzers in primary care settings

Devices such as the Siemens DCA Vantage deliver results in under 7 minutes, complying with NGSP performance criteria. Real-time feedback improves glycemic control by enabling immediate treatment adjustments. Roche’s cobas b 101 provides finger-stick results in 5 minutes and benefits from Medicare reimbursement, expanding use in family practices. Comparative studies show 76% uptake for capillary HbA1c screening versus 37.5% for venous draws in community programs. Chinese cost-utility analyses confirm favorable economics with incremental ratios below urban and rural willingness-to-pay thresholds.

Expansion of HbA1c-based reimbursement metrics in value-based care contracts

Aetna recorded a 49% rise in members achieving HbA1c control under value-based agreements, saving USD 660 million compared with fee-for-service models. The 2025 Medicare Physician Fee Schedule mandates glycemic status assessment measures within the APP Plus set, supporting widespread test reimbursement. Oregon’s primary care payment model and EmblemHealth incentive programs align provider bonuses to HbA1c outcomes. CPT Category II codes now reimburse documentation activities, encouraging higher testing frequency.

Rapid price declines in microfluidic single-use HbA1c cartridges for LMIC mass-screening

Orange Biomed’s OBM Rapid A1C leverages protein-free microfluidics to lower calibration requirements and reduce per-test cost by 60-70% once regulatory clearance is obtained. Paper-based analytical devices produced through wax printing or inkjet methods further compress prices while sustaining analytical precision. Dried blood spot protocols remain stable for more than 10 days at room temperature, enabling rural outreach programs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital/Maintenance Cost of HPLC Analyzers for Small Labs | -0.8% | Global, particularly affecting emerging markets and rural areas | Long term (≥ 4 years) |

| Analytical Interference from Hemoglobin Variants Lowering Test Confidence | -0.6% | Asia-Pacific, Sub-Saharan Africa, Mediterranean regions | Medium term (2-4 years) |

| Periodic Shortages of Ion-Exchange Resins & HPLC Columns Disrupting Supply Chain | -0.4% | Global, with highest impact in regions dependent on single suppliers | Short term (≤ 2 years) |

| Ethnicity-Specific HbA1c Bias Delaying Regulatory Harmonization in Emerging Markets | -0.3% | Asia-Pacific, Sub-Saharan Africa, Latin America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High capital and maintenance cost of HPLC analyzers for small labs

Initial purchase prices range from USD 50,000 to USD 200,000 and annual service contracts can exceed 15% of acquisition cost. CLIA 2024 updates tightened performance targets to ±8%, adding operational complexity for laboratories with limited budgets. Consumable costs, including ion-exchange columns and calibration standards, further strain finances, prompting smaller facilities to shift toward immunoassay analyzers.

Analytical interference from hemoglobin variants lowering test confidence

Around 7% of the global population carries hemoglobin variants that alter test accuracy. Hemoglobin E underestimates HbA1c using ion-exchange chromatography, common in Southeast Asia. Elevated fetal hemoglobin in sickle cell disease or β-thalassemia affects results at levels as low as 7%, necessitating alternative methodologies or confirmatory testing. FDA regulation 21 CFR 862.1373 requires manufacturers to disclose variant interference and label limitations.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Type: Point-of-care systems accelerate decentralization

Benchtop analyzers accounted for the largest share in 2025, capturing 59.42% of the HbA1c testing market. They remain the backbone of high-throughput laboratories that process thousands of specimens daily. Systems such as Beckman Coulter’s DxC 500 AU accept whole blood without manual preparation, sustaining workflow efficiency. In contrast, handheld devices drive the fastest expansion at a 6.92% CAGR as health services prioritize patient-centric delivery. The Siemens DCA Vantage, which delivers NGSP-traceable results in 6 minutes, exemplifies the reliability that now characterizes decentralized testing.

Growth momentum for handheld formats reflects rising chronic disease management in primary care and retail clinics. Many providers integrate data into electronic health records through middleware solutions, enabling population health analytics and AI-driven decision support. Manufacturers are layering cybersecurity features to comply with data protection regulations while safeguarding wireless connectivity in ambulatory environments. The price curve for single-use test cartridges is trending downward as production scales in Asia, further encouraging adoption among community practitioners and remote outreach programs. Consequently, the HbA1c market is witnessing a dual-track investment pattern where centralized laboratories upgrade high-volume HPLC lines while distributed care sites procure compact analyzers to meet on-the-spot diagnostic needs.

By Technology: Immunoassay platforms narrow the gap

HPLC commanded 61.12% of 2025 revenue, supported by its established accuracy and variant detection. Recent chemistry enhancements, such as ARKRAY’s HA-8160 buffer optimization, have improved precision to coefficients of variation below 1% across 4.4%–17.3% HbA1c ranges. Yet immunoassay systems are posting a 7% CAGR, driven by compatibility with point-of-care devices and lower operator training requirements. The Biolabo Kenza 450TX immunoturbidimetric assay demonstrates strong correlation with HPLC while operating on benchtop photometric analyzers that many small laboratories already use.

Hybrid architectures are emerging. Vendors now ship combined HPLC-immunoassay platforms that auto-route specimens based on sample type, urgency or suspected variant presence. Capillary electrophoresis and MALDI-TOF mass spectrometry occupy niche segments but introduce high sensitivity alternatives for complex hemoglobinopathies. These advances diversify the HbA1c market, allowing laboratories to match technique to clinical requirement, throughput and budget. As immunoassay reagents mature, they are expected to reduce the historical performance gap while maintaining immunity to common hemoglobin variants, thereby sustaining their near-term growth advantage.

By End-User: Homecare gains momentum

Diagnostic and reference laboratories captured 46.87% of the HbA1c market size in 2025, buoyed by established logistics networks and payer contracts. Hospitals also command a sizeable portion as they embed analyzers in core labs and emergency departments. However, homecare settings exhibit the highest 7.05% CAGR. At-home sample collection kits and finger-stick microfluidic devices allow patients to monitor long-term glycemic control without clinic visits. Orange Biomed’s pending OBM Rapid A1C platform highlights this direction, offering laboratory-grade accuracy from a single drop of capillary blood.

Technology convergence supports the homecare surge. Continuous glucose monitoring sensors interface with mobile applications that aggregate daily readings and quarterly HbA1c results. Abbott’s FreeStyle Libre users who combine sensor data with GLP-1 therapies record a 2.4% HbA1c reduction, surpassing medicine alone. Telehealth services integrate these inputs to personalize medication titration and lifestyle coaching, reinforcing adherence. As broadband connectivity and digital literacy improve among older adults, home testing penetration is expected to deepen, solidifying its role as the fastest-growing end-user segment within the HbA1c market.

By Patient Age Group: Older adults steer incremental demand

Adults retained 58.03% share in 2025 due to the high prevalence of type 2 diabetes in working-age populations. Nonetheless, the geriatric cohort is registering the strongest 6.95% CAGR. Longer lifespans and comorbid conditions necessitate frequent glycemic assessment to mitigate cardiovascular and cognitive complications. Diabetes technology adoption among seniors, including insulin pumps and automated insulin delivery, correlates with fewer hypoglycemic events and improved quality of life.

Pediatric testing remains specialized but pivotal. The American Diabetes Association revised guidelines in 2024, recommending targets below 7% HbA1c for children with type 1 diabetes, tightening control thresholds. These stringent targets demand reliable assays with minimal sample volume. Laboratories are therefore validating collection protocols tailored to low-volume pediatric draws.

Geography Analysis

North America maintained leadership with 41.12% revenue share in 2025 as insurers expanded screening coverage and employer wellness programs mandated annual biometric checks. Medicare’s 2024 addition of HbA1c to the diabetes screening benefit notably increased test volumes in federally funded clinics. Europe ranks second, supported by coordinated national diabetes plans across Germany, the United Kingdom and France. Laboratory networks have modernized with integrated LIS-middleware infrastructures to meet ISO 15189 accreditation standards, fostering timely result transmission to primary care teams.

Asia-Pacific is forecast to grow at a 7.13% CAGR, driven by surging prevalence and infrastructure investment. India’s diabetes burden is projected to rise from 74 million cases in 2021 to 124 million by 2045, catalyzing laboratory expansion and point-of-care deployment. China’s urban and rural cost-utility analyses validate the economic logic of decentralized screening, encouraging provincial health budgets to fund pilot programs. Southeast Asian countries are integrating dried blood spot sampling into outreach initiatives to overcome transportation barriers in archipelagic regions, thus broadening test reach.

The Middle East and Africa region faces variant-related analytical complexity. Hemoglobin S and C prevalence requires method selection sensitive to interference profiles, directing some laboratories toward immunoassay or capillary electrophoresis systems. South America experiences steady testing uptick as public health campaigns raise diabetes awareness and private laboratories align their service menus with international guidelines. Across all regions, the HbA1c market is benefiting from policy emphasis on early detection and the broader shift toward value-based healthcare financing.

Competitive Landscape

Leading suppliers pursue dual strategies that combine portfolio breadth with digital integration. Abbott, Roche, Siemens Healthineers and Danaher collectively account for a sizable portion of global revenues. Abbott’s partnership with Medtronic integrates FreeStyle Libre continuous glucose monitoring with insulin pumps, creating an ecosystem that synchronizes real-time glucose readings with insulin delivery adjustment. Roche secured CE Mark for Accu-Chek SmartGuide, an AI-enabled CGM delivering predictive analytics, underscoring the convergence of sensing, cloud analytics and decision support.

Siemens Healthineers differentiates on networked data management. Its RAPIDComm system allows centralized oversight of distributed DCA Vantage analyzers, ensuring quality compliance over multi-site primary care rollouts. Danaher’s Beckman Coulter targets high-volume laboratories with automated sample preparation and reagent-on-board cooling to minimize downtime. Emerging challengers such as Orange Biomed focus on microfluidic innovation that reduces per-test cost, appealing to low-resource settings.

Regulatory compliance shapes competition. The FDA requires demonstrable performance in the presence of prevalent hemoglobin variants, favoring incumbents with deep validation data. Supply chain resilience is also a differentiator as manufacturers mitigate resin and column shortages by onboarding secondary suppliers and vertical-integrating critical components. Overall, rivalry is moderate. Leaders invest in AI, connectivity and user-centric design, while new entrants seek regional niches or novel chemistries to bypass entrenched HPLC dominance.

HbA1c Testing Industry Leaders

-

Abbott

-

Bio-Rad Laboratories, Inc.

-

F. Hoffmann-La Roche Ltd.

-

Arkray, Inc.

-

Beckman Coulter, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Orange Biomed to present breakthrough microfluidic test for lab-accurate HbA1c in minutes at ADLM 2025.

- August 2024: Abbott entered a global partnership with Medtronic to integrate its FreeStyle Libre continuous glucose monitoring technology with Medtronic insulin delivery systems, benefiting more than 11 million users worldwide.

- July 2024: Roche received CE Mark for the AI-enabled Accu-Chek SmartGuide CGM, offering predictive alerts through the Accu-Chek Care digital platform.

- June 2024: Abbott introduced Lingo and Libre Rio consumer biowearables, aiming to expand Libre portfolio revenue to USD 10 billion by 2028.

Global HbA1c Testing Market Report Scope

The HbA1c test is a blood test used to determine the average blood sugar level over two to three months. The HbA1c testing market is segmented by type (handheld device, benchtop device), by end-user (hospitals and clinics, diagnostic laboratories, other end-users), and by geography (North America, Europe, Asia-Pacific, Middle East and Africa, and Latin America).

The report offers the value (in USD) for the above segments.

| Handheld and POCT Devices |

| Benchtop Laboratory Analyzers |

| HPLC |

| Immunoassay |

| Enzymatic Assay |

| Capillary Electrophoresis |

| Others |

| Hospitals and Clinics |

| Diagnostic and Reference Laboratories |

| Homecare Settings |

| Others |

| Adults |

| Pediatric |

| Geriatric |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Malaysia | |

| Indonesia | |

| Thailand | |

| Philippines | |

| Vietnam | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Device Type | Handheld and POCT Devices | |

| Benchtop Laboratory Analyzers | ||

| By Technology | HPLC | |

| Immunoassay | ||

| Enzymatic Assay | ||

| Capillary Electrophoresis | ||

| Others | ||

| By End-User | Hospitals and Clinics | |

| Diagnostic and Reference Laboratories | ||

| Homecare Settings | ||

| Others | ||

| By Patient Age Group | Adults | |

| Pediatric | ||

| Geriatric | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Malaysia | ||

| Indonesia | ||

| Thailand | ||

| Philippines | ||

| Vietnam | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the HbA1c market?

The HbA1c market is valued at USD 2.48 billion in 2026 and is projected to reach USD 3.33 billion by 2031.

Which region is expected to grow the fastest?

Asia-Pacific is forecast to register the highest 7.13% CAGR through 2031, driven by rapid increases in diabetes prevalence and expanding healthcare infrastructure.

Why are point-of-care HbA1c devices gaining popularity?

Point-of-care analyzers provide results within minutes, enable immediate treatment adjustments, and support decentralized care models favored in primary care and telehealth settings.

How do hemoglobin variants impact HbA1c accuracy?

Variants such as HbE or elevated fetal hemoglobin can cause under- or over-estimation in some analytical methods, prompting laboratories to select techniques validated against local variant profiles.

What is driving home-based HbA1c testing?

Patient preference for convenience, growth in telehealth, and new microfluidic devices that deliver lab-grade accuracy from finger-stick samples are accelerating homecare adoption.

How are value-based care contracts influencing testing demand?

Insurers increasingly link reimbursement to glycemic control metrics, incentivizing providers to conduct HbA1c testing more regularly and accurately to meet quality benchmarks.

Page last updated on: