Sample Preparation Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 9.87 Billion |

| Market Size (2031) | USD 12.18 Billion |

| Growth Rate (2026 - 2031) | 4.31% CAGR |

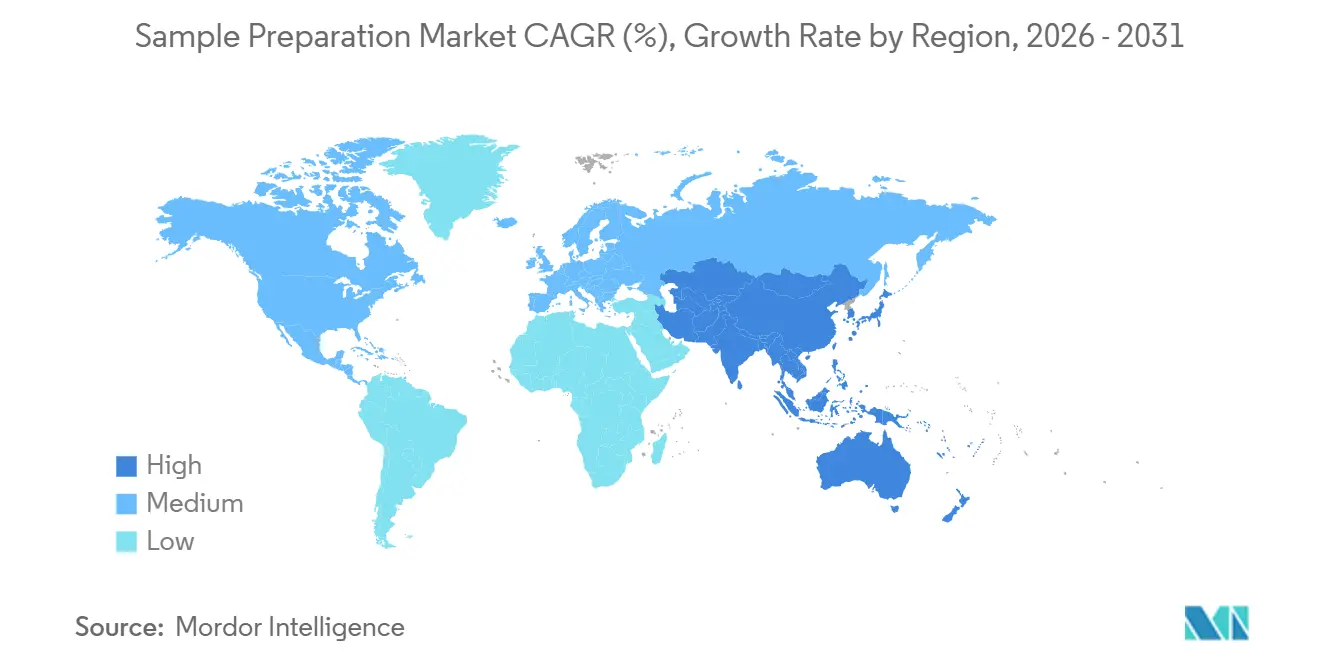

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Sample Preparation Market Analysis by Mordor Intelligence

The global sample preparation market size is expected to grow from USD 9.46 billion in 2025 to USD 9.87 billion in 2026 and is forecast to reach USD 12.18 billion by 2031 at 4.31% CAGR over 2026-2031. Sustained investments in omics research, stricter data-quality standards, and increased adoption of automated, high-throughput instruments in clinical and pharmaceutical laboratories drive the market. By 2030, fully automated platforms are expected to capture a significant share of the market as laboratories address workforce shortages while striving for enhanced reproducibility and accuracy. The growing implementation of precision-medicine programs in secondary and tertiary care settings is further fueling the demand for standardized upstream processing of genomic, proteomic, and metabolomic specimens. This shift is strengthening the influence of consumables vendors, whose proprietary chemistries ensure recurring revenue streams despite extended instrument replacement cycles. Additionally, regional trends indicate that the Asia Pacific market is steadily narrowing the gap with established players, supported by domestic innovation policies and the strategic relocation of biomanufacturing capacities.

Key Report Takeaways

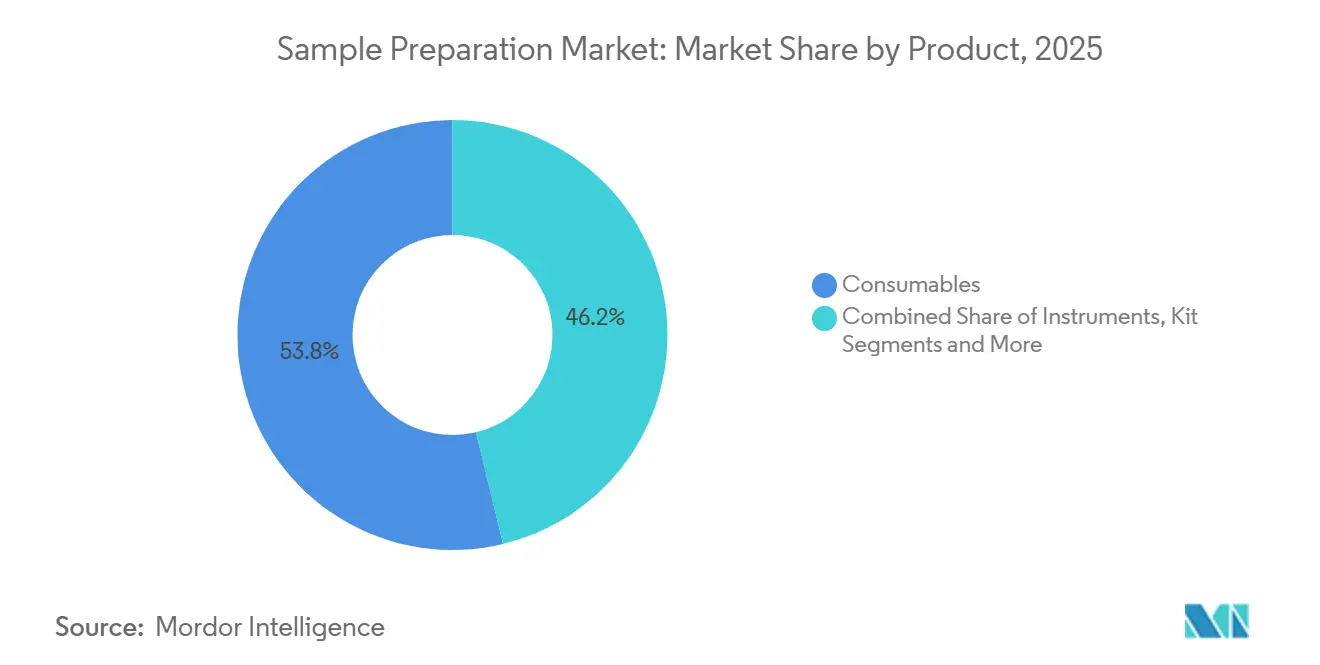

- By product category, consumables captured 53.78% of the sample preparation market share in 2025, while sample-preparation kits are projected to grow at a 9.02% CAGR through 2031.

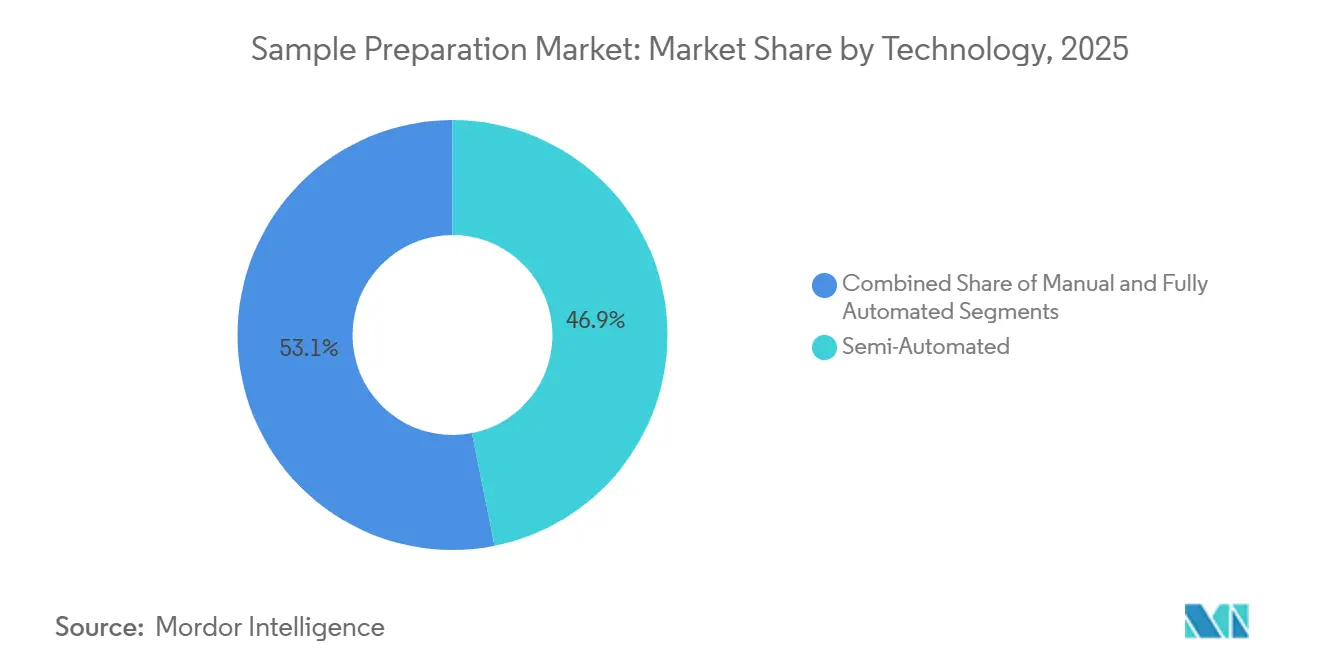

- By technology, semi-automated platforms commanded a 46.85% market share; fully automated systems are forecast to register the fastest growth at a 10.22% CAGR from 2026 to 2031.

- By application, genomics contributed 40.92% of 2025 revenue, whereas epigenomics is expected to expand at an 11.55% CAGR to 2031.

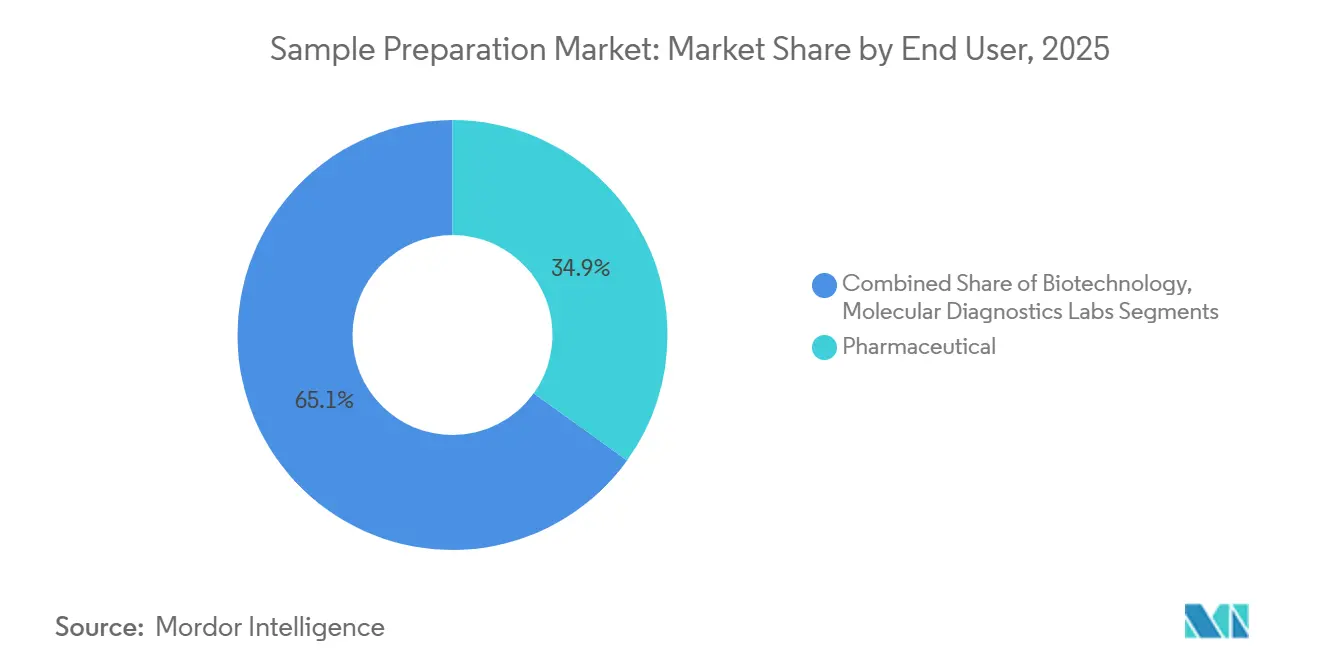

- By end-user, pharmaceutical companies held 34.92% of the 2025 market share, while molecular diagnostics laboratories are anticipated to post the highest growth with a 10.44% CAGR during 2026-2031.

- By geography, North America captured 35.10% of the market share in 2025, whereas the Asia-Pacific region holds the strongest growth at an 8.58% CAGR outlook through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Sample Preparation Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging global investment in omics research and precision-medicine | +1.2 | Global | Medium term (~3-4 yrs) |

| Growing demand for automated, high-throughput sample-prep to boost laboratory productivity | +0.9 | North America & EU; spill-over to APAC | Short term (≤2 yrs) |

| Increasing clinical adoption of genomic sequencing and liquid-biopsy diagnostics | +1.0 | North America, APAC core, selective EU markets | Medium term (~3-4 yrs) |

| Expansion of biopharma R&D and manufacturing volumes requiring robust sample preparation | +0.8 | Global, with early gains in APAC manufacturing hubs | Long term (≥5 yrs) |

| Supportive government funding and public-private partnerships for life-science tool innovation | +0.7 | North America, EU, select APAC nations | Short term (≤2 yrs) |

| Advancements in automation, microfluidics and reagent chemistries enhancing workflow efficiency | +0.6 | Global | Medium term (~3-4 yrs) |

| Source: Mordor Intelligence | |||

Surging Global Investment in Omics Research and Precision-Medicine

The integration of multi-omics data into electronic medical records[1]K. M. Mendez, “A Roadmap to Precision Medicine Through Post-Genomic Electronic Medical Records,” Nature Communications, nature.comis driving significant advancements in data harmonization, fueling the demand for sophisticated sample preparation technologies. Hospitals that deploy unified genomics and proteomics dashboards have identified sample inconsistencies as a critical factor contributing to analytical variances. To address this challenge, they are increasingly adopting validated, kit-based workflows that standardize extraction efficiencies across various specimen types, ensuring reliable results and enabling the identification of actionable biomarkers. This shift is propelling the sample preparation market, with vendors striving to certify their chemistries for compatibility with both next-generation sequencing and high-resolution mass spectrometry platforms. The growing overlap between clinical and research laboratories, driven by shared requirements for traceability, is reshaping market dynamics. In response, regulatory bodies are updating guidelines on pre-analytical variables, creating additional compliance challenges and raising the entry barriers for new market players.

Growing Demand for Automated, High-Throughput Sample-Prep to Boost Laboratory Productivity

In response to rising test volumes and staffing shortages, laboratories are increasingly investing in automated liquid-handling stations capable of processing 96- or 384-well plates in under an hour. Automation is proving to be a strategic asset, delivering a 1.8-fold reduction in sample-to-sample variation for proteomics workflows, thereby enhancing both quality and productivity. This trend is driving growth in the sample preparation market, with hardware OEMs and reagent specialists forming strategic partnerships to offer turnkey solutions that reduce the validation burden for end users. Early adopters report that reallocating technicians from repetitive pipetting tasks to data interpretation not only improves workforce morale but also shortens report-generation timelines, a critical competitive advantage in the contract-research market. Consequently, procurement committees are adopting a broader valuation framework, assessing return on investment not only through throughput metrics but also by factoring in opportunity cost savings. This evolving perspective is accelerating the shift from semi-automated to fully automated platforms, further driving market adoption.

Increasing Clinical Adoption of Genomic Sequencing and Liquid-Biopsy Diagnostics

Whole-genome sequencing is transitioning from reference laboratories to major regional hospitals, driving significant growth in the sample preparation market. Oncology testing, particularly liquid biopsy, is setting a new industry standard. Clinicians increasingly demand ultra-pure nucleic-acid extracts to ensure variant-calling accuracy, even at allele frequencies below 1%. Systems like EMAG and similar centrifuge-free extractors are gaining market traction due to their ability to minimize contamination risks while integrating seamlessly into compact molecular-pathology workflows. Intermountain Precision Genomics exemplifies this shift by combining automated pre-analytics with in-house bioinformatics pipelines, enabling faster report turnaround times and improved patient management outcomes[2]Srinivasan Mani, “Genomics and Multiomics in the Age of Precision Medicine,” Nature, nature.com. This trend is fostering closer collaboration between laboratory managers and IT departments, who now co-specify reagent kits and data pipelines as part of a unified procurement strategy. These integrated purchasing decisions are accelerating vendor consolidation, as buyers increasingly prefer suppliers that offer both reagents and informatics support under a single service level agreement (SLA).

Expansion of Biopharma R&D and Manufacturing Volumes Requiring Robust Sample Preparation

As cell-therapy and mRNA-based products dominate the landscape, contract development and manufacturing organizations face an uptick in daily sample counts due to stringent lot-release analytics. Biopharma sponsors, in turn, are prioritizing sample-prep instrumentation that meticulously documents each step for compliance audits and seamlessly integrates with manufacturing execution systems. This heightened focus on compliance is nudging the sample preparation market towards platforms that incorporate barcode readers, electronic batch records, and automated reagent-lot verification. Vendors boasting these features enjoy heightened renewal rates for consumables, a trend driven by regulatory protocols that mandate continuity of validated kits throughout clinical phases. Moreover, the industry's pivot towards gentler lysis chemistries, moving away from harsh solvents, underscores the challenge of balancing high throughput with the preservation of biological activity. By fine-tuning sample-prep parameters to align with critical-quality-attribute frameworks, manufacturers are subtly bolstering the robustness of their CMC dossiers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital and operating costs of fully automated sample-prep platforms | −0.7 | Global, pronounced in emerging markets | Short term (≤2 yrs) |

| Shortage of skilled personnel to operate and maintain sophisticated systems | −0.6 | North America & EU, expanding to APAC | Medium term (~3-4 yrs) |

| Stringent regulatory requirements for clinical-grade reagents extending time-to-market | −0.5 | North America & EU | Medium term (~3-4 yrs) |

| Supply-chain vulnerabilities for specialty enzymes, magnetic beads and plastics | −0.4 | Global, acute in APAC & MEA | Short term (≤2 yrs) |

| Source: Mordor Intelligence | |||

High Capital and Operating Costs of Fully Automated Sample-Prep Platforms

High costs of comprehensive workstations, often exceeding USD 100,000, create a significant barrier for small laboratories and price-sensitive regions, impacting market adoption. Additionally, annual operating expenditures, including service contracts, calibrations, and proprietary consumables, account for 15% to 20% of the workstation's list price, driving laboratories to adopt cautious budgeting strategies. This cost dynamic has segmented the sample preparation market: high-throughput reference centers justify investments in premium machines, while community hospitals prefer modular systems or reagent-rental models to optimize cost efficiency. In response, vendors are strategically launching scalable systems with core decks designed to accommodate optional modules. These systems allow laboratories to add magnetic-bead or vacuum-filtration units as demand grows, aligning with evolving operational needs. This modularity not only extends asset lifecycles but also reduces the risk of technological obsolescence, enhancing resale values in the secondary-equipment market and strengthening market competitiveness.

Shortage of Skilled Personnel to Operate and Maintain Sophisticated Systems

The increasing complexity of sample preparation technologies is creating a significant skills gap in the market, with laboratories facing challenges in recruiting and retaining qualified personnel to operate and troubleshoot advanced automated systems. This issue is particularly critical in high-growth segments like proteomics and epigenomics, where intricate sample preparation workflows demand both technical expertise and a thorough understanding of instrument functionality. The extended training periods for new staff are delaying automation implementation and diminishing initial productivity, leading to hesitancy among laboratory directors to invest in automation solutions. In response, system vendors are introducing advanced user interfaces, remote monitoring features, and comprehensive training programs. However, workforce development remains a key market constraint. This shortage of skilled personnel is driving demand for cloud-connected instruments, which enable remote diagnostics and operations. These solutions allow centralized expertise to support multiple laboratory locations, reducing the dependency on on-site specialists, as highlighted by Malvern Panalytical in October 2024.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Consumables Drive Recurring Revenue Streams

In 2025, consumables dominated the sample preparation market, securing a 53.78% share and emerging as the top revenue source for vendors. This stronghold is attributed to consistent repurchase cycles; each test relies on extraction columns, beads, or buffer kits, ensuring stable cash flows that remain unaffected by capital-equipment cycles. Within the consumables realm, sample-prep kits are projected to grow at a 9.02% CAGR from 2026 to 2031, surpassing the growth of general reagents. This shift is driven by laboratories' preference for method-validated kits, which reduce inter-operator variability. The trend is especially evident in liquid-biopsy workflows, where kits designed for cell-free DNA extraction achieve superior recovery from minimal plasma volumes. Furthermore, once a laboratory commits to a proprietary chemistry linked to specific instrumentation, it gains enhanced pricing power over consumables. This trend motivates vendors to create cartridges and columns that are either physically or electronically compatible with their platforms, bolstering customer loyalty.

By Technology: Automation Reshapes Laboratory Workflows

In 2025, semi-automated technologies held a 46.85% share of the sample preparation market, appealing to labs that seek moderate throughput improvements without overhauling their operations. These systems often integrate bench-top magnetic-bead processors with manual pipetting stations, striking a balance between cost and performance. However, fully automated platforms are projected to grow at a 10.22% CAGR through 2031, fueled by escalating labor costs and stringent reproducibility standards. Labs that have embraced fully automated solutions frequently highlight added advantages, including enhanced traceability and reduced cross-contamination, both of which diminish expensive re-runs. Furthermore, as software updates roll out new protocols remotely, the longevity of automation hardware increases, making it more appealing for budget committees assessing the total cost of ownership.

By Application: Genomics Maintains Leadership Position

Genomics held a commanding 40.92% Sample Preparation market share in 2025, underpinned by mature commercial sequencing platforms and established reimbursement pathways. Although the segment’s growth now trails nascent fields, its absolute market size continues to rise as sequencing read depths increase and as pan-cancer panels move into standard testing menus. Epigenomics, meanwhile, posts an 11.55% forecast CAGR for 2026-2031, reflecting heightened interest in methylation and chromatin-accessibility markers as predictors of disease progression. Single-cell epigenomic analysis multiplies data richness per specimen, further lifting consumables demand because each cell becomes a separate library prep event. By driving new kit development, epigenomics indirectly elevates the innovation rate for core chemistries that later diffuse back into genomics and transcriptomics routines.

By End-User: Pharmaceutical Companies Lead Adoption

Pharmaceutical companies captured 34.92% of the sample preparation market size in 2025, a reflection of their expansive clinical-trial pipelines and stringent regulatory documentation standards. Their purchasing decisions often set industry benchmarks; therefore, vendors securing pharma contracts not only gain volume but also credibility that cascades into academic and hospital segments. Molecular diagnostics laboratories, however, are projected for a 10.44% CAGR through 2031, propelled by expanded oncology and rare-disease testing menus. These labs prioritize turnkey platforms that combine minimal hands-on time with LIS connectivity, features that directly influence patient-result turnaround. The steady transition of genetic testing to community hospital settings underscores the need for user-friendly instruments requiring limited specialist oversight, shaping future product-design roadmaps.

Geography Analysis

North America leads the sample preparation market with 35.10% market share, buoyed by strong federal research grants, swift adoption of next-gen lab automation, and a concentration of biopharma headquarters. The region's regulatory framework, guided by FDA and CLIA standards, enforces pre-analytical quality controls, driving demand for standardized kits and traceable workflows. Partnerships, like QIAGEN's with Bio-Manguinhos/Fiocruz, highlight established vendors' efforts to adapt North American solutions for emerging public health markets, enhancing global presence and tailoring products to diverse resources. Consequently, academic medical centers, seeking distinction, are channeling investments into single-cell multi-omics platforms. This boosts consumables throughput, even as instrument installations plateau. The regional market leans towards integrated, compliance-focused solutions, streamlining documentation for accreditation cycles.

Asia Pacific is witnessing the fastest growth, driven by a surge in pharmaceutical manufacturing and robust government incentives bolstering domestic biotech ecosystems. China's Five-Year Plans allocate significant funds towards high-end instrumentation, pushing local labs to bypass intermediate technologies in favor of fully automated workflows. In Japan and South Korea, an ageing population is driving up the demand for molecular-diagnostic testing, particularly in oncology and inherited disorders. The rise of local-language software and smaller reagent pack sizes underscores the potential of regional customization in capturing market share, all while keeping core chemistries intact. Notably, recent geopolitical disruptions have underscored the importance of supply-chain resiliency, prompting multinationals to set up manufacturing hubs in the region to secure tenders.

Europe's Sample Preparation industry thrives on initiatives like Horizon Europe, channeling funds into omics projects that demand meticulous sample handling. EU mandates on lab sustainability spark a shift towards eco-friendly consumables, urging vendors to innovate kits that minimize environmental harm while maximizing yield. The rise of academic-industrial partnerships accelerates the development of specialized extraction chemistries, birthing start-ups that flourish through licensing agreements with industry giants. Concurrently, the stringent data-protection mandates of GDPR heighten the demand for secure, audit-compliant instrument software, reshaping procurement decisions alongside traditional performance benchmarks. Collectively, these dynamics reinforce Europe's pivotal role as a trendsetter in global regulatory and sustainability movements.

Competitive Landscape

The sample preparation market demonstrates a moderately concentrated structure, where established multinational vendors coexist with agile, application-focused specialists. Leading firms leverage extensive product portfolios and global service networks but face increasing competition from emerging players. These new entrants, equipped with microfluidic and AI-enhanced platforms, offer comparable performance in smaller, more efficient designs. Strategic collaborations, such as the partnership between Agilent and Thermo Fisher to co-develop control protocols, indicate a competitive shift from proprietary lock-in to ecosystem efficiency. Concurrently, mid-tier companies are carving out defensible niches by optimizing chemistries for specific sample matrices, such as extracellular vesicles or low-input FFPE tissue. This approach validates a segmentation strategy that prioritizes sample complexity over instrument throughput.

Market opportunities are emerging in cost-effective automation solutions for mid-volume laboratories, integrated sample-to-answer workflows for point-of-care diagnostics, and consumables tailored for new analytes like cell-free RNA. Disruptive technologies, including solvent-free lysis and bead-free binding matrices, are gaining traction among environmental-testing labs aiming to reduce hazardous-waste disposal costs. Competitive analysis reveals that vendors capable of delivering certified end-to-end workflows—including reagents, instruments, and bioinformatics—achieve higher customer retention rates. This trend underscores laboratories' preference for streamlined, single-vendor support models.

Technology differentiation in the market now hinges on reducing cross-contamination, minimizing hands-on time, and ensuring downstream compatibility. Thermo Fisher’s AccelerOme platform exemplifies this trend by offering pre-validated methods and self-sealing reagent cartridges, which significantly reduce operator error in proteomics sample preparation. Similar moves by competitors suggest that turnkey validation packages are rapidly becoming a baseline expectation rather than a premium feature.

Sample Preparation Industry Leaders

Thermo Fisher Scientific

Agilent Technologies

Merck KGaA (MilliporeSigma)

Danaher Corporation

QIAGEN N.V.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Thermo Fisher Scientific updated its AccelerOme automated sample-prep platform with remote workflow-download functionality, enabling protocol deployment across global lab networks from a central hub.

- December 2024: Hamilton Company introduced a mid-throughput modular deck allowing incremental automation upgrades, targeting resource-constrained clinical labs seeking phased adoption.

- November 2024: Beckman Coulter Life Sciences released an eco-friendly extraction kit that reduces plastic waste by 40 % via refillable reagent reservoirs, aligning with European green-lab initiatives.

- October 2024: Agilent Technologies introduced the 5977B High Efficiency Source GC/MSD System at the Beijing Conference on Instrumental Analysis. This system enables the detection of pollutants at levels 10 times lower than existing single-quadrupole systems while reducing sample volume requirements and preparation time.

- September 2024: QIAGEN expanded its collaboration with Bio-Manguinhos/Fiocruz to enhance blood screening capabilities in Brazil, providing molecular biology technologies and custom solutions for public health initiatives.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the global sample preparation market as all instruments, semi- and fully automated workstations, consumables, and ready-to-use kits that convert biological or chemical specimens into homogeneous aliquots for analytical techniques such as sequencing, chromatography, or spectroscopy.

Scope Exclusions: We exclude histopathology tissue processors and consumables bundled exclusively with downstream analyzers.

Segmentation Overview

- By Product

- Sample-Preparation Instruments

- Extraction Systems

- Automated Workstations

- Evaporation Systems

- Liquid-Handling Platforms

- Other Instruments

- Consumables

- Sample-Preparation Kits

- Purification Kits

- Isolation Kits

- Extraction Kits

- Accessories & Software

- Sample-Preparation Instruments

- By Technology

- Manual

- Semi-Automated

- Fully Automated

- By Application

- Genomics

- Proteomics

- Epigenomics

- Other Application

- By End-User

- Pharmaceutical Companies

- Biotechnology Companies

- Molecular Diagnostics Labs

- Academic & Research Institutes

- CROs & CDMOs

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

We interview lab managers, genomics service providers, reagent distributors, and automation engineers across North America, Europe, and Asia-Pacific. Their insights calibrate utilization rates, kit replacement cycles, and emerging adoption triggers that secondary material alone cannot reveal.

Desk Research

We review tier-1 public datasets, NIH RePORTER, Eurostat Prodcom, UN Comtrade HS 8479/9027 flows, and FDA/EMA device notices to map installed bases and trade volumes.

Our team then mines Analytical Chemistry, AACC and SLAS briefs, company 10-Ks, investor decks, Questel patent counts, D&B Hoovers financials, and Factiva news to refine revenue splits and technology diffusion.

The sources listed are illustrative; many additional references support data capture and checks.

Market-Sizing & Forecasting

Our model starts top-down by reconstructing the global stock of extraction systems and liquid handlers from production and trade data, then layers kit pull-through ratios, regional omics-test penetration, and average selling prices. Supplier roll-ups and channel checks give bottom-up anchors that adjust totals. Key variables include funded omics projects, sequencing run volumes, kit price erosion, automation uptake, and clinical-trial starts. A multivariate regression with ARIMA smoothing projects demand to 2030, while scenario analysis guards against funding or policy shocks.

Data Validation & Update Cycle

We run anomaly flags, peer reviews, and variance checks before sign-off. Reports refresh every twelve months; material events trigger interim tweaks, and a final pass ensures clients receive the latest view.

Why Mordor's Sample Preparation Baseline Commands Reliability

Published estimates often diverge because providers pick different scopes, base years, or currency assumptions. Mordor analysts, by bounding the market around laboratory sample preparation only and refreshing data annually, deliver a steadier benchmark.

We find others may omit semi-automated systems, merge sample prep reagents with broader analytical supplies, or rely on older exchange rates, all of which shift totals away from Mordor's 2025 view.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 9.46 B | Mordor Intelligence | - |

| USD 8.39 B | Global Consultancy A | Leaves out semi-automated systems; uses 2023 ASP set |

| USD 8.63 B | Industry Research Group B | Blends sample prep reagents with general analytical disposables |

| USD 9.72 B | Business Analytics Firm C | Adds electron microscopy prep tools; applies 2024 currency averages |

These contrasts show that our clearly bounded scope, transparent variables, and regular refresh make Mordor's baseline a balanced, reproducible foundation for strategic decisions.

Key Questions Answered in the Report

What is the projected value of the global sample preparation market by 2031?

The segment is forecast to reach USD 12.18 billion by 2031, reflecting a 4.31% CAGR.

Which product category accounts for the largest revenue share in sample preparation?

Consumables dominate with a 53.78% share in 2025, underpinned by recurring kits and reagent sales.

How fast are fully automated sample preparation systems expected to grow?

They are set to expand at a 10.22% CAGR between 2026 and 2031 as labs pursue higher throughput and reproducibility.

Why is epigenomic sample prep gaining momentum?

Epigenomics posts an 11.55% CAGR because chromatin and methylation markers are becoming essential in translational research and oncology diagnostics.

Which region is witnessing the fastest uptake of sample preparation technologies?

Asia Pacific leads growth, driven by expanding biomanufacturing capacity and government biotech incentives.

How are vendors tackling the skills gap in advanced sample prep workflows?

Manufacturers embed guided-workflow software and remote diagnostics so fewer on-site specialists are needed to run and maintain automated systems.

Page last updated on: