Hardware Security Modules Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 2.18 Billion |

| Market Size (2031) | USD 3.51 Billion |

| Growth Rate (2026 - 2031) | 10.02% CAGR |

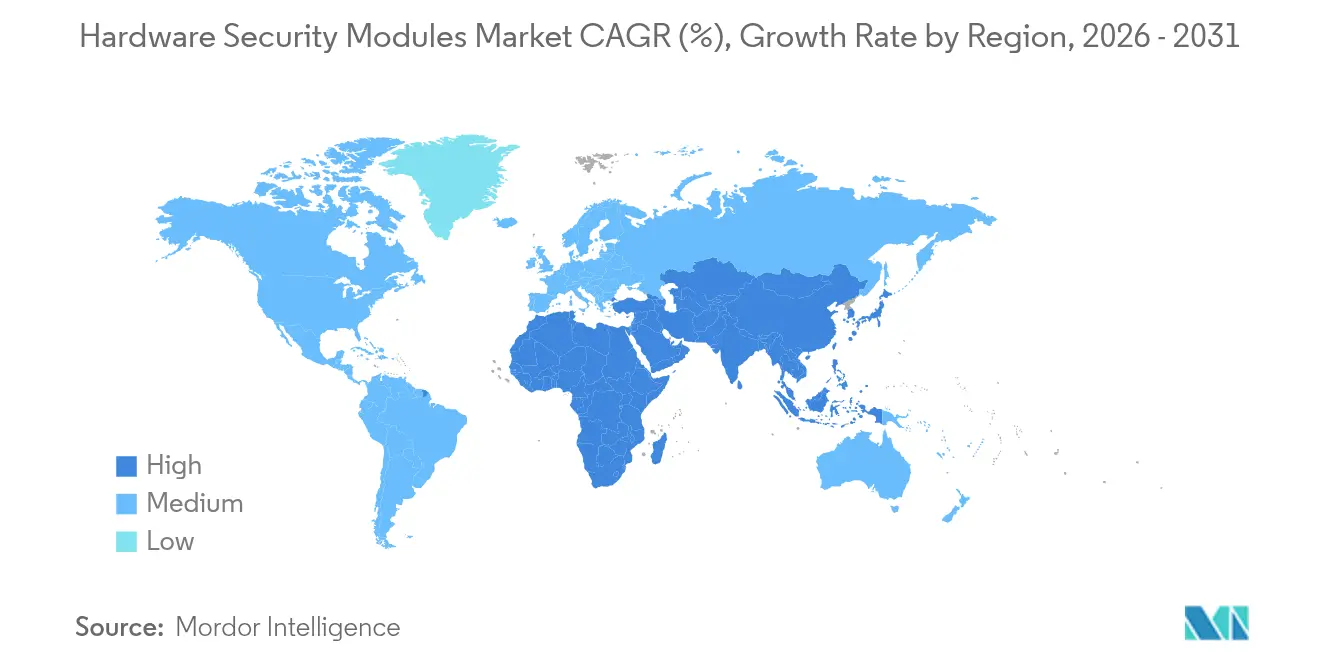

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Hardware Security Modules Market Analysis by Mordor Intelligence

The Hardware Security Modules Market size is expected to increase from USD 1.98 billion in 2025 to USD 2.18 billion in 2026 and reach USD 3.51 billion by 2031, growing at a CAGR of 10.02% over 2026-2031.

Growing adoption of post-quantum cryptography, rising cloud migration, instant-payment infrastructure roll-outs and MiCA-driven crypto-custody requirements are propelling demand across sectors. North America continues to lead due to early regulatory mandates, yet Asia delivers the fastest acceleration as hyperscalers localize sovereign key management platforms. Supply constraints for FIPS 140-3 chips inflate lead times and pricing, prompting buyers to lock multi-year allocations with established vendors. Meanwhile, cloud HSM services democratize access for smaller enterprises and create subscription-based revenue pools that complement traditional appliance sales.[1]Thales Group, “Luna HSMs FIPS 140-3 Validation,” cpl.thalesgroup.com

Key Report Takeaways

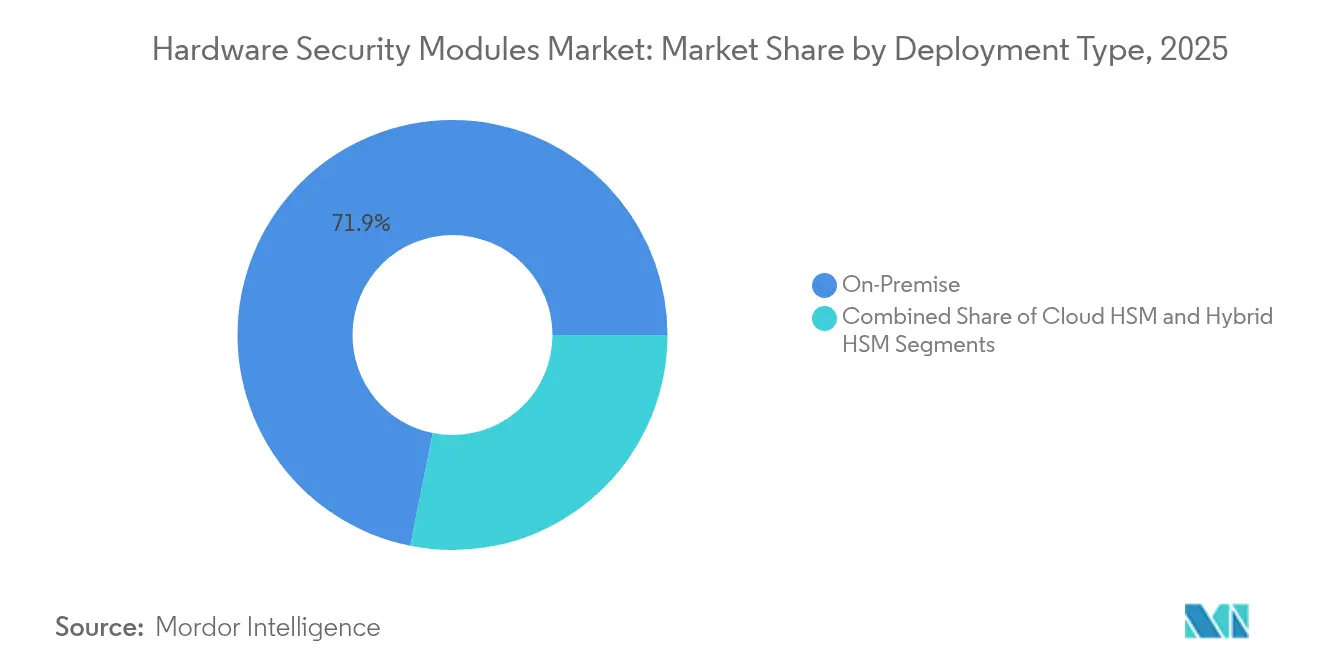

- By deployment type, on-premise appliances held 71.85% of the Hardware Security Modules market share in 2025, while cloud HSMs are projected to advance at a 10.62% CAGR through 2031.

- By type, general-purpose units led with 59.45% revenue share in 2025; cloud-hosted HSMs represent the fastest segment at an 10.74% CAGR.

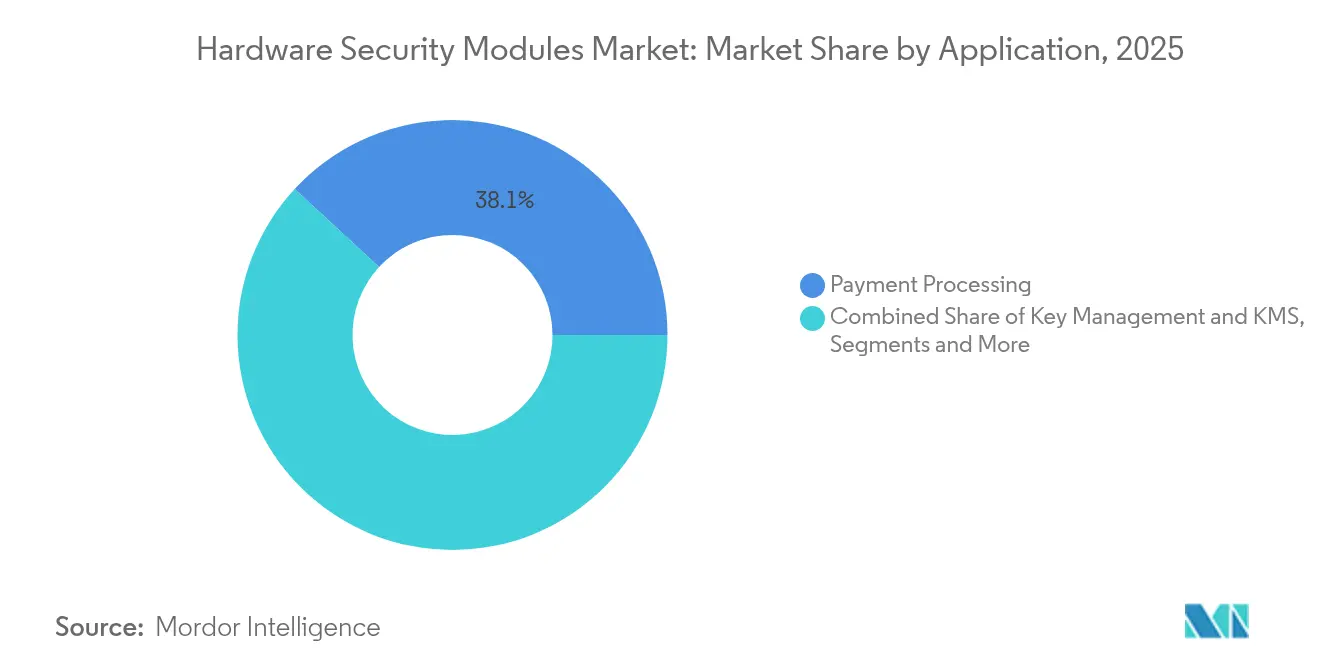

- By application, payment processing captured 38.12% of the HSM market size in 2025; blockchain and cryptocurrency custody is set to expand at a 10.18% CAGR.

- By end-user vertical, the BFSI sector accounted for 33.92% of demand in 2025, whereas cloud service providers will record the highest 10.96% CAGR to 2031.

- By geography, North America commanded 37.10% share of the Hardware Security Modules market in 2025; Asia Pacific is forecast to post a 12.17% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Hardware Security Modules Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Post-quantum compliance deadlines accelerating HSM refresh (N. America & Europe) | +2.8% | North America & Europe | Short term (≤ 2 years) |

| Hyperscaler cloud-native key-management boom in APAC | +2.1% | APAC core, spill-over to MEA | Medium term (2-4 years) |

| Instant-payment rails fuelling payment HSM uptake (Americas) | +1.7% | Americas, with European expansion | Short term (≤ 2 years) |

| Crypto-custody MiCA rules driving EU demand for FIPS HSMs | +1.4% | Europe, with global compliance spillover | Medium term (2-4 years) |

| Automotive UNECE R155 mandate pushing embedded HSM IP | +1.2% | Global, with early gains in Europe & Japan | Long term (≥ 4 years) |

| Multi-tenant HSM-as-a-Service monetisation | +0.9% | Global, concentrated in developed markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Post-quantum compliance deadlines accelerating HSM refresh

NIST finalized three post-quantum algorithms in 2024, triggering mandatory migrations across federal agencies and regulated industries.[2]NIST, “Post-Quantum Cryptography FIPS Approved,” csrc.nist.gov Enterprises now maintain dual cryptographic stacks to support ML-KEM, ML-DSA and SLH-DSA during transition periods, which doubles processing loads and precipitates accelerated appliance refresh cycles. The NSA’s Commercial National Security Algorithm Suite 2.0 obliges mission-critical systems to adopt quantum-resistant primitives well before 2035, compressing planning horizons. Thales Luna became the first FIPS 140-3 Level 3 certified HSM in April 2024, giving early adopters a procurement advantage. “Harvest now, decrypt later” threat models further reinforce urgency, particularly for entities that must guarantee multi-decade confidentiality.

Hyperscaler cloud-native key-management boom

Google Cloud, Microsoft Azure and AWS now embed FIPS-validated hardware in multitenant locations, enabling customers to bring their own keys while satisfying domestic data-residency rules. Marvell’s LiquidSecurity boards deliver 1 million operations per second to meet hyperscaler throughput targets. National frameworks such as Singapore’s PDPA and Japan’s cybersecurity guidelines require localized instances, stimulating region-specific capacity roll-outs. Financial-services newcomers like Indonesia’s Krom Bank leverage managed CloudHSM to accelerate digital-banking launches while retaining cryptographic control. These deployments substantially expand the HSM market in APAC.

Instant-payment rails fuelling payment HSM uptake

FedNow in the United States and SEPA Instant in Europe mandate real-time settlement, placing stringent millisecond-level latency on message validation. Futurex payment HSMs surpassed 50 000 operations per second in 2024, illustrating performance thresholds that payment processors now demand. PSD2 requires strong customer authentication throughout Europe, reinforcing the need for PCI-certified network-attached appliances. Thales payShield Cloud introduces subscription access for spikes in festive or prime-day volumes. These dynamics elevate the Hardware Security Modules market trajectory within transaction-heavy ecosystems.

Crypto-custody MiCA rules driving EU demand for FIPS HSMs

The MiCA framework became effective in December 2024, compelling crypto-asset service providers to store private keys inside FIPS 140-2 Level 3 or higher modules.[3]EUR-Lex, “Markets in Crypto-Assets Regulation,” eur-lex.europa.eu BaFin echoes this stance in its implementation circulars, obliging ART and EMT operators to implement redundant hardware clusters for resiliency. Exchanges therefore architect threshold-signature schemes inside multi-region HSM grids, maintaining compliance without compromising latency for high-frequency trading. The overlap with PCI DSS ignites demand for hybrid devices capable of handling both card and blockchain workloads, further enlarging the Hardware Security Modules market opportunity across European financial infrastructure.

Restraints Impact Analysis of Hardware Security Modules Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Scarcity of FIPS 140-3 chips | -1.8% | Global, acute in North America & Europe | Short term (≤ 2 years) |

| Legacy PKI-to-cloud migration complexity | -1.2% | Global, concentrated in enterprise segments | Medium term (2-4 years) |

| Secure-memory price spikes hitting SMBs (LATAM) | -0.8% | Latin America, with spillover to emerging markets | Short term (≤ 2 years) |

| Cross-border crypto-law fragmentation (e.g., China MLPS 2.0) | -0.7% | Global, with concentration in Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Scarcity of FIPS 140-3 chips

Semiconductor capacity remains constrained because only a handful of foundries can fabricate secure processors that meet FIPS 140-3 test vectors. SK Hynix and Micron have sold out high bandwidth memory allocations through most of 2025, forcing HSM makers to ration supply and raise prices. Certification introduces lengthy zeroization and tamper-response validations, slowing new tape-outs and reinforcing dependence on incumbent suppliers. Smaller entrants therefore face extended lead times, tipping HSM market economics toward vendors with pre-reserved wafers.

Legacy PKI-to-cloud migration complexity

Enterprises with decade-old certificate hierarchies grapple with proprietary key formats, fragmented trust anchors and bespoke authentication flows that resist lift-and-shift approaches. Parallel CA operations inflate costs and heighten audit risk during transition. Paddy Power Betfair’s Vault deployment highlighted the engineering overhaul needed to automate issuance pipelines. Skills shortages in cloud cryptography prolong projects, tempering near-term Hardware Security Modules industry expansion.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Hardware Security Modules Market Segment Analysis

By Deployment Type:

On-premise Control with Cloud AccelerationOn-premise appliances retained 71.85% of Hardware Security Modules market share in 2025 due to direct control over keys required by defense, banking and critical-infrastructure operators. Many firms keep root-of-trust inside data centers to satisfy sovereign data mandates. Nevertheless, cloud HSM subscriptions are scaling at a 10.62% CAGR as hyperscalers guarantee FIPS validations, availability SLAs and API-first consumption. This hybrid approach enlarges the HSM market size because organizations often run dual footprints during transitional years.

Managed offerings reduce capital outlay and refresh risk, attracting startups and mid-tier banks that previously relied on software keystores. Edge computing adds another layer, prompting distributed clusters that enforce local encryption at the 5G boundary while synchronizing policies centrally. Vendors address this by shipping container-based connectors so DevSecOps teams can call hardware services from Kubernetes pods. Over the forecast period, spending tilts toward subscription models even as sizeable regulated workloads remain locked inside private racks. Second-generation deployment strategies now bundle HSM functionality into micro-data-centers that support smart-factory use cases, connected-vehicle update signing and city-wide public-safety networks.

By Type:

General-Purpose Leadership with Service-Driven SpecializationGeneral-purpose units captured 59.45% of revenue in 2025 because they handle PKI root protection, code signing, tokenization and database encryption in a single chassis. Their algorithm agility makes them indispensable for post-quantum migrations that demand both RSA/ECC and lattice-based primitives during a prolonged overlap period. Meanwhile, cloud-hosted variants demonstrate an 10.74% CAGR, supported by hyperscaler pay-per-use economics and uniform regional roll-outs. Payment-class boxes remain essential for PCI DSS, yet vendors are embedding payment and general-purpose firmware on shared boards to optimize inventory under chip constraints.

Containerized plugins translate PKCS#11 calls into REST interfaces, letting builders request secure key operations from micro-services without learning low-level drivers. Specialized silicon for AI model sealing has emerged, as Fortanix integrates confidential-computing enclaves with HSM orchestration to protect machine learning assets at rest and in inference.

By Application:

Payment Strength with Blockchain MomentumPayment processing controlled 38.12% of 2025 demand because real-time rails, card-issuer mandates and strong customer authentication obligations place immutable reliance on hardware-backed cryptography. Instant-payment clearing houses specify throughput numbers that only dedicated payment HSMs can sustain. Conversely, blockchain and digital-asset custody constitutes the fastest-growing niche at a 10.18% CAGR, propelled by MiCA and institutional adoption of tokenized deposits. Exchanges are converging on multi-signature, threshold-based key paradigms that require clustered HSM farms distributed across continents for location-based disaster recovery.

SSL/TLS termination, software-bill-of-materials signing and zero-trust micro-segmentation renew interest in general-purpose devices, while IoT identity and secure firmware updates open emerging sub-segments. Automotive OEMs working toward UNECE R155 integrate embedded HSM IP blocks into domain controllers, expanding the Hardware Security Modules market size for on-chip designs.

By End-User Vertical:

BFSI Core with Cloud Provider SurgeBFSI institutions accounted for 33.92% of 2025 spending because they must comply with Basel, PCI, SWIFT CSCF and regional cybersecurity statutes. Treasury operations underpinning high-value payments and digital-banking authentication rely on deterministic key custody, making appliance refresh a board-level priority. Still, cloud service providers show the sharpest 10.96% CAGR, driven by customer insistence on bring-your-own-key controls within shared infrastructure. Hyperscalers co-design boards with silicon vendors to optimize slot density and performance per watt, thereby expanding their margin pools while capturing incremental Hardware Security Modules market opportunities.

Government and defense entities purchase certified units for classified networks, with quantum-resistance mandates advancing timelines. Telecom operators embed HSM clusters into 5G core slices for SIM credential management and lawful intercept compliance. Manufacturers investing in Industry 4.0 deploy device-identity foundations that couple chip-level secure elements with back-office HSM orchestrators, reinforcing supply-chain provenance.

Geography Analysis

North America Hardware Security Modules Market

North America held 37.10% of global Hardware Security Modules market share in 2025 thanks to early FIPS 140-3 adoption, quantum-safe directives across federal agencies and a dense cluster of payment processors that refresh devices on three-year cycles. Ongoing public-sector modernization grants and zero-trust executive orders sustain steady procurement pipelines. Canada follows suit with treasury modernization and open-banking rulemaking, while Mexico shows emerging acceleration as fintechs connect to CoDi and SPEI fast-payment rails, demanding lower-cost cloud HSM gateways.

APAC Hardware Security Modules Market

Asia Pacific exhibits the highest 12.17% CAGR through 2031, buoyed by hyperscaler data-center construction and digital-banking licenses that require sovereign key regimes. China’s MLPS 2.0 imposes domestic algorithm usage, compelling dual-stack appliances capable of operating SM2 alongside NIST curves. Japan’s automakers integrate embedded IP to comply with connected-vehicle cybersecurity provisions, and India’s data-localization policies steer banks toward region-specific key vaults hosted on AWS Mumbai and GCP Delhi zones. ASEAN markets implement interoperable real-time payments, prompting regional banks to adopt shared-service HSM utilities that cut per-transaction costs without sacrificing compliance.

Europe Hardware Security Modules Market

Europe remains a strategic arena shaped by MiCA, GDPR and PSD2. Germany’s industrial Mittelstand invests in on-premise clusters to secure IP as factories adopt OPC-UA over 5G. The United Kingdom focuses on post-Brexit divergence in critical-data classifications, driving bespoke appliance certifications. France expands cloud-first mandates under the SecNumCloud label, which still requires root keys inside qualified hardware. Eastern European fintech hubs, notably Lithuania, deploy multi-tenant HSM grids to attract passporting crypto-service providers. Collectively these measures lift the Hardware Security Modules market size across the continent despite slower headline GDP growth.

Competitive Landscape

The Hardware Security Modules market is moderately fragmented, with legacy leaders Thales, Utimaco and Entrust maintaining technological edge through continuous certification cycles and broad software-ecosystem integrations. Thales exploits its aerospace security heritage to secure early FIPS 140-3 validations, reinforcing credibility in defense and critical-infrastructure bids. Utimaco differentiates via automotive-grade IP and free simulators that lower developer entry barriers. Entrust capitalizes on more than 150 application connectors, easing adoption across heterogeneous stacks.

Hyperscalers have entered via managed services, compressing margins on low-end hardware yet expanding overall TAM by onboarding untapped small and medium enterprises. Strategic acquisitions illustrate portfolio consolidation: CyberArk bought Venafi for USD 1.54 billion in 2024 to merge machine and human identity management.

Vendors emphasize post-quantum readiness; Thales and Utimaco now ship hybrid cryptography firmware that runs ML-KEM side-by-side with RSA, preserving backward compatibility. Supply-chain resilience emerges as a key differentiator: firms with priority wafer allocations secure larger frame agreements as chip shortages linger. White-space opportunities in edge AI security encourage newer entrants offering containerized HSM apps deployable on ruggedized servers. Over the horizon, confidential-computing fusion is expected to trigger the next competitive realignment as data-in-use protection converges with traditional encryption.

Hardware Security Modules Industry Leaders

Thales Group

Hewlett Packard Enterprise Development LP

Eviden SAD (Atos Group)

Utimaco Management Services GmbH

Futurex

- *Disclaimer: Major Players sorted in no particular order

Hardware Security Modules Market Companies Covered in this Report

- Thales Group

- Utimaco Management Services GmbH

- Entrust Corporation

- IBM Corporation

- Hewlett Packard Enterprise (HPE)

- Eviden SAD (Atos Group)

- Futurex

- Amazon Web Services (AWS)

- Microsoft Azure Dedicated HSM

- Yubico

- Securosys SA

- Swissbit AG

- Secunet Security Networks AG

- Infineon Technologies AG

- Marvell Technology Inc.

- Fortanix Inc.

- Microchip Technology Inc.

- Broadcom Inc.

- Crypto4A Technologies

- Nitrokey GmbH

- nCipher (nShield)

- Rambus

Recent Industry Developments in Hardware Security Modules Market

- May 2024: Thales showcased HSM-centred post-quantum protection for Google Workspace, underscoring joint go-to-market strategies in sovereign cloud offerings.

- April 2025: Fortanix previewed Armet AI to secure entire AI lifecycles within confidential-computing enclaves, signaling expansion beyond key management into holistic data protection.

- January 2025: SEALSQ achieved Common Criteria EAL5+ for its MS600X platform and passed FIPS 140-3 testing for VaultIC 408, strengthening its positioning in quantum-ready secure silicon.

- August 2024: Microsoft embedded Marvell LiquidSecurity boards into Azure Key Vault, enabling 100 000 key pairs and 1 million operations per second for mission-critical workloads.

Global Hardware Security Modules Market Report Scope

A hardware security module (HSM) is a physical device designed to generate, manage, and store securely cryptographic keys used for encryption, decryption, authentication, and digital signatures. HSMs provide a high level of security by safeguarding sensitive data and cryptographic operations from unauthorized access, cyberattacks, and tampering. THey are widely used in industries like banking, government, and telecommunications to ensure data integrity, confidentiality, and compliance with regulatory standards.

The study tracks the revenue generated from the sale and services of hardware security modules by various manufacturers worldwide. It also tracks the key market parameters, underlying growth influencers, and major manufacturers operating in the industry, which supports the market estimations and growth rates over the forecast period. The study further analyses the overall impact of macroeconomic factors on the market. The report’s scope encompasses market sizing and forecasts for the various market segments.

The hardware security modules market is segmented by type (general purpose HSM, payment HSM), by deployment (on-premise, cloud based), by application (payment processing, code and document signing, key management, ssl/tls encryption), by end user vertical (banking and financial services, government, healthcare, retail, telecommunications, and others) and by geography (North America, Europe, Asia-Pacific, Latin America, and Middle East and Africa). the market sizes and forecasts are provided in terms of value (USD) for all the above segments.

Segmentation Overview

| On-Premise |

| Cloud HSM |

| Hybrid HSM |

| General Purpose HSM |

| Payment HSM |

| Cloud/Hosted HSM (HSM-aaS) |

| USB/Portable HSM |

| PCIe-based HSM |

| Network-attached HSM |

| Payment Processing |

| Key Management and KMS |

| SSL/TLS and Code-Signing |

| PKI and Certificate Authorities |

| Blockchain and Cryptocurrency Custody |

| Database and Document Encryption |

| IoT/Edge Device Identity |

| Post-Quantum Crypto Acceleration |

| BFSI |

| Government and Defense |

| Healthcare and Life Sciences |

| Retail and E-commerce |

| Telecommunications and IT |

| Industrial and Manufacturing |

| Energy and Utilities |

| Cloud Service Providers |

| Others |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN | ||

| Australia | ||

| New Zealand | ||

| Rest of Asia Pacific | ||

| Middle East and Africa | Middle East | GCC |

| Turkey | ||

| Israel | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| By Deployment Type | On-Premise | ||

| Cloud HSM | |||

| Hybrid HSM | |||

| By Type | General Purpose HSM | ||

| Payment HSM | |||

| Cloud/Hosted HSM (HSM-aaS) | |||

| USB/Portable HSM | |||

| PCIe-based HSM | |||

| Network-attached HSM | |||

| By Application | Payment Processing | ||

| Key Management and KMS | |||

| SSL/TLS and Code-Signing | |||

| PKI and Certificate Authorities | |||

| Blockchain and Cryptocurrency Custody | |||

| Database and Document Encryption | |||

| IoT/Edge Device Identity | |||

| Post-Quantum Crypto Acceleration | |||

| By End-User Vertical | BFSI | ||

| Government and Defense | |||

| Healthcare and Life Sciences | |||

| Retail and E-commerce | |||

| Telecommunications and IT | |||

| Industrial and Manufacturing | |||

| Energy and Utilities | |||

| Cloud Service Providers | |||

| Others | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| ASEAN | |||

| Australia | |||

| New Zealand | |||

| Rest of Asia Pacific | |||

| Middle East and Africa | Middle East | GCC | |

| Turkey | |||

| Israel | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is driving the rapid growth of the Hardware Security Modules market?

Post-quantum cryptography mandates, cloud migration, instant-payment rails and MiCA-driven crypto custody are together pushing the market toward a 10.02% CAGR through 2031.

Which deployment model is expanding the fastest?

Cloud or hosted HSM services are forecast to grow at 10.62% annually as organizations favor subscription economics and hyperscaler managed offerings.

How large is the Hardware Security Modules market size for payment processing?

Payment applications accounted for 38.12% of total revenues in 2025, anchoring the single-largest use-case segment.

Why are FIPS 140-3 chips in short supply?

Limited secure-foundry capacity and lengthy validation cycles restrict availability, lowering near-term supply and nudging appliance prices higher.

Which region shows the highest growth potential?

Asia Pacific is projected to achieve a 12.17% CAGR through 2031, propelled by data-center expansion, digital banking and stringent local compliance rules.

How will quantum computing affect existing HSM investments?

Enterprises will operate dual cryptographic stacks during migration, requiring FIPS 140-3 modules capable of hybrid classical and quantum-resistant algorithms to safeguard data against future quantum attacks.

Page last updated on: