Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

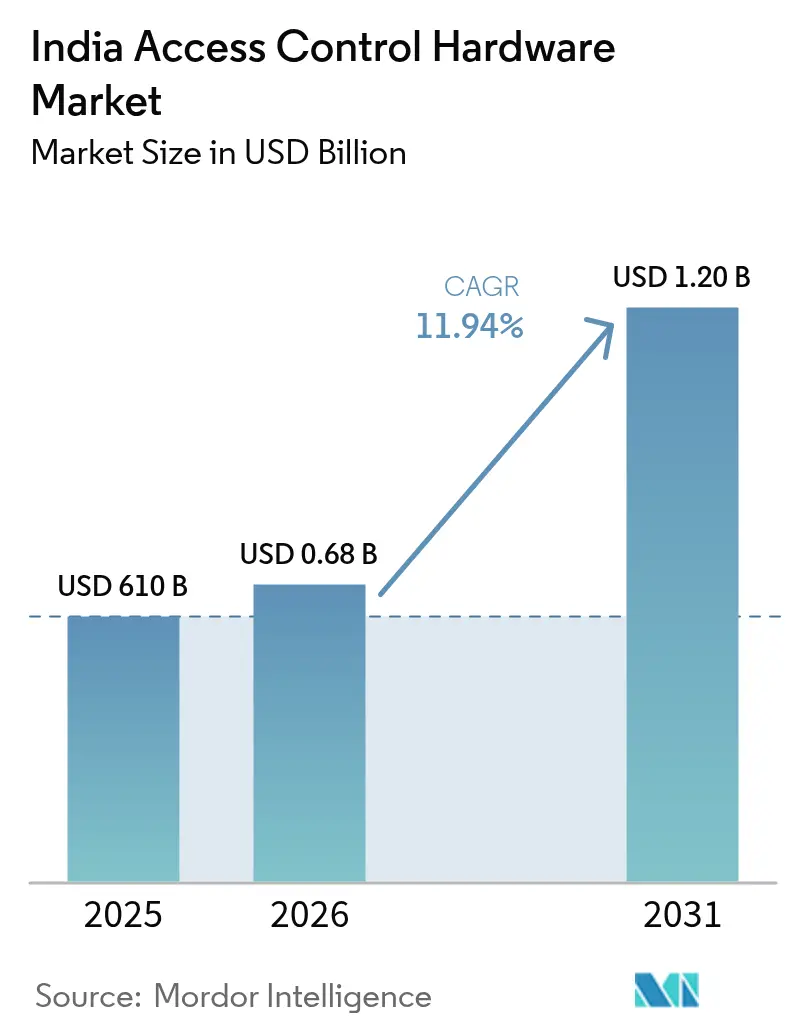

| Base Year Market Size (2025) | USD 610 Billion |

| Market Size (2026) | USD 0.68 Billion |

| Market Size (2031) | USD 1.2 Billion |

| Growth Rate (2026 - 2031) | 11.94% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Access Control Hardware Market Analysis by Mordor Intelligence

India access control hardware market size in 2026 is estimated at USD 682.83 million, growing from 2025 value of USD 610 million with 2031 projections showing USD 1.2 billion, growing at 11.94% CAGR over 2026-2031. This brisk expansion stems from sovereign digital-identity programs, the doubling of domestic data center capacity, and the Smart Cities Mission, which together create sustained demand for card readers, biometric panels, controllers, and electronic locks across public and private sectors.[1]Ministry of Housing and Urban Affairs, “Smart Cities Mission Extended Till March 2025,” Press Information Bureau, pib.gov.in Vendors benefit from Make-in-India incentives that shorten component lead times, while falling average selling prices for Internet-of-Things-enabled smart locks spur residential adoption. The Reserve Bank of India’s 2024 Master Direction requires banks and payment operators to deploy multi-factor authentication at server rooms, driving demand for tamper-alert locks and biometric readers.[2]Reserve Bank of India, “Master Direction on IT Framework for Payment System Operators,” rbi.org.in Meanwhile, fragmented state procurement rules raise integration costs; however, the recent standardization of GeM reduces bid cycles, allowing smaller municipalities to adopt hardware that was previously limited to metropolitan projects.

Key Report Takeaways

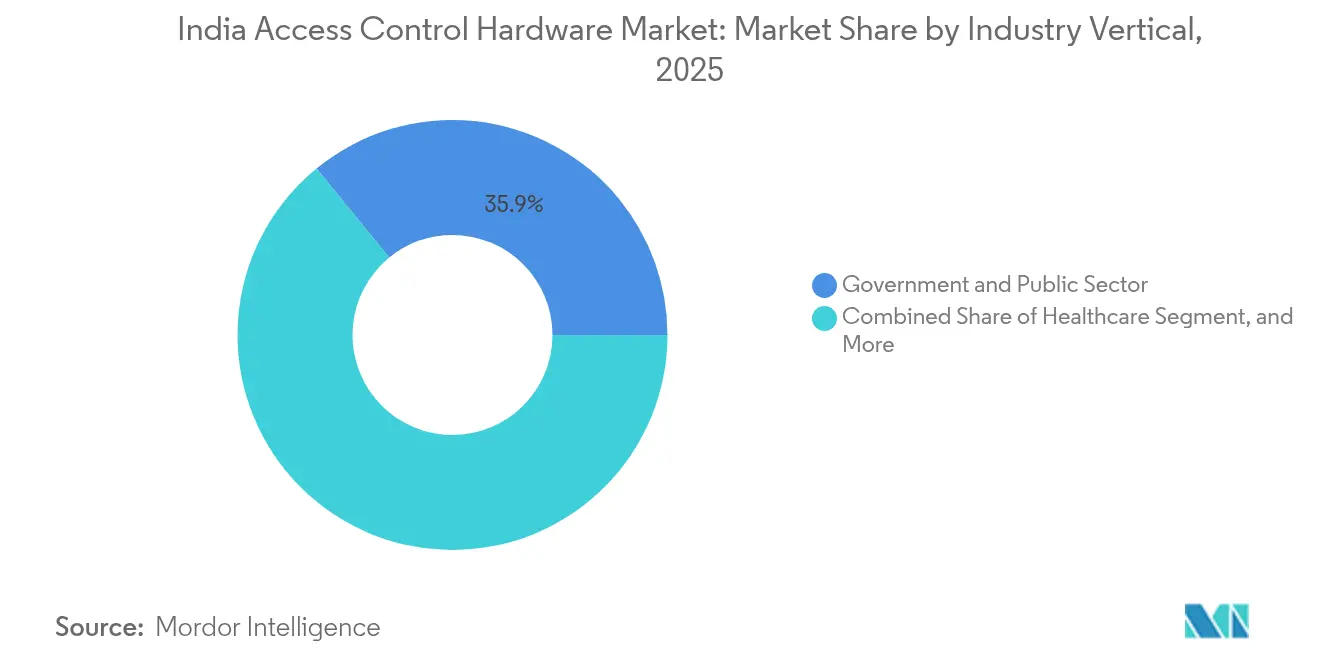

- By industry vertical, the government and public sector segment held a 35.90% share of the India access control hardware market in 2025, while the Healthcare segment is advancing at a 14.72% CAGR through 2031.

- By product type, card readers led with 43.20% revenue share of the India access control hardware market in 2025; biometric readers are forecast to expand at a 13.98% CAGR to 2031.

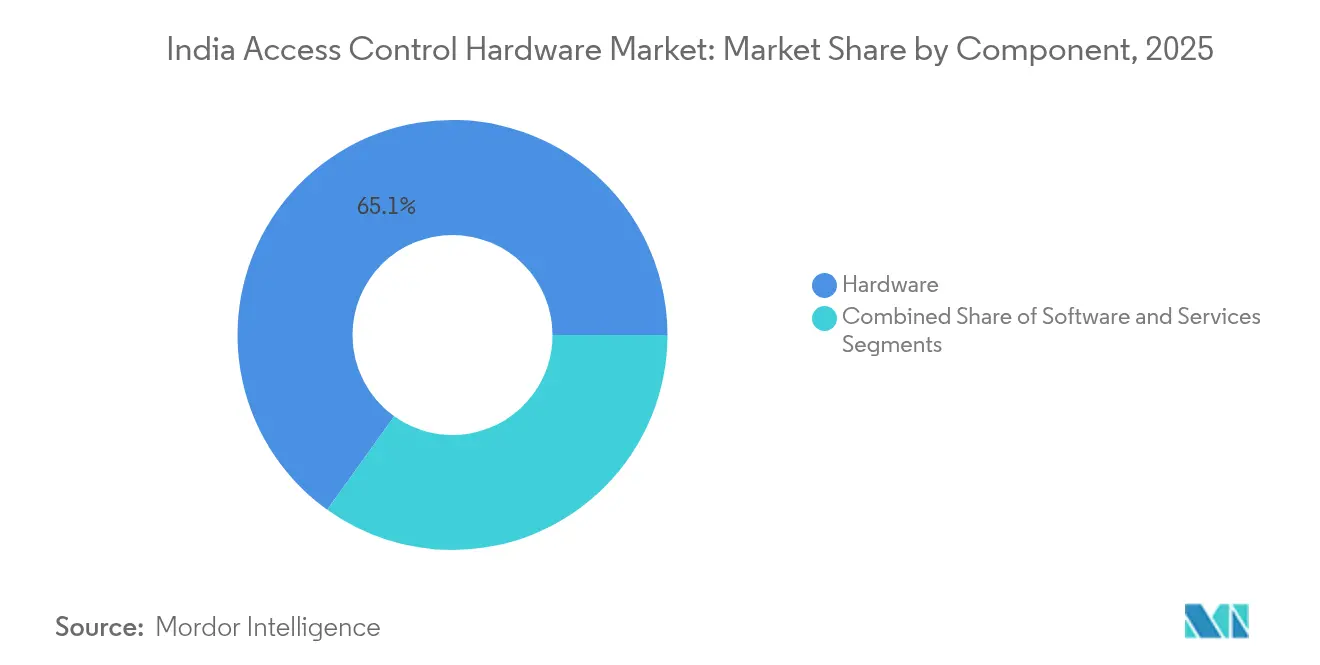

- By component, hardware accounted for 65.10% of the India access control hardware market size in 2025; however, services are expected to represent the fastest-growing segment at a 13.05% CAGR from 2025 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Access Control Hardware Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in Government Smart-City Public-Safety Spending | +2.1% | National, with early gains in Tier-1 and Tier-2 cities under Smart Cities Mission | Medium term (2-4 years) |

| Rising Adoption of Mobile-Credential and Cloud-Based Access Management | +1.8% | National, concentrated in IT and Telecom hubs (Bengaluru, Hyderabad, Pune, NCR) | Short term (≤2 years) |

| Rapid Growth of Contactless Biometrics in Post-Pandemic Workplaces | +2.3% | National, accelerated in metros and state capitals with high office density | Short term (≤2 years) |

| Expansion of Data-Center Infrastructure Demanding High-Security Hardware | +2.0% | National, led by Maharashtra, Tamil Nadu, Telangana, Haryana | Medium term (2-4 years) |

| Falling ASPs of IoT-Enabled Smart Locks Boosting Residential Uptake | +1.4% | Urban clusters (Mumbai, Delhi, Bengaluru, Chennai, Kolkata) | Long term (≥4 years) |

| Make-in-India Incentives Catalyzing Local Hardware Manufacturing | +1.7% | National, with manufacturing clusters in Gujarat, Tamil Nadu, Karnataka | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surge in Government Smart-City Public-Safety Spending

The Smart Cities Mission extension allocated INR 48,000 crore (USD 5.76 billion) through March 2025 and installed more than 83,000 CCTV cameras plus integrated command-and-control centers across 100 cities. Municipalities have progressed from passive cameras to active identity verification, procuring card readers, biometric gates, and electronic locks for civic buildings and transport hubs. Tamil Nadu’s Safe City Project awarded contracts in late 2024 to deploy facial-recognition turnstiles at 42 district headquarters, while Uttar Pradesh is fitting biometric panels at 75 police stations. The Government e-Marketplace portal accelerated hardware uptake by publishing unified specifications, letting smaller towns buy proven devices with 90-day procurement cycles. Collectively, these deployments amplify baseline demand in the India access control hardware market as states replicate flagship models in second-tier cities.

Rapid Growth of Contactless Biometrics in Post-Pandemic Workplaces

Touchless modalities, including facial recognition, iris scanning, and palm-vein analysis, became mainstream in 2024 when enterprises replaced fingerprint scanners to curb infection risks. Digi Yatra’s facial-recognition boarding processed 15 million passengers across 24 airports by mid-2024, validating sub-two-second authentication at scale. Corporate campuses in Bengaluru and Hyderabad subsequently shifted to kiosk-based face readers linked to cloud dashboards that log entries in real time. AIIMS New Delhi reduced outpatient wait times by 40% after implementing similar technology in early 2024. Falling sensor costs and Aadhaar interoperability reduce integration expenses, allowing domestic suppliers such as Mantra Softech to win state tenders with contactless kits priced 18% below those of their multinational equivalents. As deployment experience compounds, the India access control hardware market gains a virtuous cycle of cost decline and feature enrichment.

Expansion of Data-Center Infrastructure Demanding High-Security Hardware

Domestic data-center capacity is set to double to roughly 2,100 MW by FY 2027, driven by investments topping INR 55,000 crore (USD 6.6 billion). The Reserve Bank of India’s 2024 mandate enforces multi-factor authentication, biometric logs, and SIEM integration for server-room doors. In response, hyperscalers in Mumbai, Chennai, Hyderabad, and Noida specify dual-sensor readers, tamper-alert locks, and PoE controllers capable of 10,000 events per second. Given the high value of each rack, operators pay premiums for hardware-software bundles that include 24/7 managed access, fuelling services revenue within the India access control hardware market.

Rising Adoption of Mobile-Credential and Cloud-Based Access Management

IT parks and telecom campuses are pushing toward badgeless entry, issuing smartphone credentials that revoke instantly upon role change. Early pilots at fintech towers in Gurugram cut card issuance costs by 60% while improving visitor throughput. Cloud-native controllers synchronize over secure APIs, allowing facilities teams to adjust access zones without the need for on-site technicians. Although the Digital Personal Data Protection Act 2023 requires local storage of biometric templates, vendors now deliver India-hosted instances that comply with this rule. As telcos roll out 5G campuses, low-latency connectivity further enhances mobile credential performance, adding momentum to the Indian access control hardware market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented State-Level Procurement Standards Delaying Roll-outs | -1.3% | National, with acute friction in states lacking unified e-governance frameworks | Short term (≤2 years) |

| High Initial CAPEX for Multi-Modal Systems Deterring SME Adoption | -1.1% | National, concentrated in Tier-2 and Tier-3 cities with limited access to credit | Medium term (2-4 years) |

| Supply-Chain Volatility for Semiconductor Components | -0.9% | National, affecting vendors reliant on imported microcontroller units and sensors | Short term (≤2 years) |

| Increasing Cyber-Physical Convergence Raising Data-Privacy Risks | -0.8% | National, with heightened scrutiny in metros and state capitals | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Fragmented State-Level Procurement Standards Delaying Roll-outs

Maharashtra mandates iris scanners for police armories, Karnataka prefers palm-vein readers for citizen centers, and Rajasthan still specifies fingerprint modules. Such divergence forces vendors to maintain multiple SKUs and certifications, eroding scale economies. Although GeM published unified specs in 2024, only 18 states adopted them by November, leaving integrators to juggle legacy clauses. Documentation rework and variant testing add 8-10 weeks to project timelines and increase integration costs by up to 12%, dampening the near-term uptake of the India access control hardware market.

High Initial CAPEX for Multi-Modal Systems Deterring SME Adoption

A dual-sensor terminal with card, face, and fingerprint recognition still costs approximately INR 50,000 (USD 600), a figure that exceeds the budget of many manufacturing SMEs. A 2024 FICCI survey found that 62% of such firms cited hardware cost as their primary barrier, despite paybacks under two years.[3]Federation of Indian Chambers of Commerce and Industry, “SME Technology Adoption Survey 2024,” ficci.in Credit to SMEs grew only 8.3% year-over-year, constraining discretionary tech spend. Vendors now market phased deployments, cards first, biometrics later, and subscription models that convert capital outlay to opex, but uptake outside metros remains tepid, trimming upside for the India access control hardware market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Industry Vertical: Government Dominates, Healthcare Accelerates

Government and Public Sector deployments accounted for 35.90% of the Indian access control hardware market share in 2025, with widespread installations at smart city command centers, police stations, and bus depots. The vertical keeps steady procurement funnels via GeM, though price sensitivity invites competition from domestic integrators. Healthcare is forecast to compound at 14.72% through 2031, the fastest among verticals, driven by Ayushman Bharat Health Account requirements that mandate biometric verification at registration desks in more than 150,000 health and wellness centers.

Other verticals reinforce volume. BFSI entities retrofit biometric panels into branch server rooms to comply with the RBI directive, while manufacturing sites implement zone-based controls that feed attendance data into HR systems. Transport hubs are testing facial-recognition gates, with the Delhi Metro reporting a 30% faster throughput on its pilot line. IT and telecom campuses advance mobile credentials, while defense facilities maintain a niche demand for multi-factor authentication. Altogether, diverse end-user mandates sustain the India access control hardware market.

By Product Type: Cards Lead, Biometrics Surge

Card readers retained 43.20% of the revenue in 2025, anchored by long-running installations and standardized specifications that simplify replacement cycles. Yet, biometric readers are projected to clock the highest 13.98% CAGR to 2031 as workplaces abandon touch surfaces. Face recognition scales fastest, validated by Digi Yatra’s 1.5 crore passenger milestones. As a result, the India access control hardware market size for biometric readers is projected to exceed USD 0.51 billion by 2031, doubling its 2025 base. Electronic locks ride on residential momentum; Godrej’s Wi-Fi model, priced at INR 12,000 (USD 144), undercuts earlier products by 25% and illustrates ASP declines.

Controllers and panels serve as the system's brain, shifting toward cloud management despite data localization constraints. Vendors address privacy challenges by hosting instances in India and implementing edge encryption, enabling compliance without compromising analytics. Ancillary hardware, including turnstiles, bollards, and vehicle barriers, rounds out perimeter defense at industrial parks and logistics yards, providing integrators with upsell avenues within the Indian access control hardware market.

By Component: Hardware Dominates, Services Scale

Hardware contributed 65.10% of 2025 revenue; however, managed services and integration are expected to grow at an annual rate of 13.05% to 2031, as enterprises outsource 24/7 monitoring. Data-center operators, in particular, sign five-year contracts that blend hardware refresh, cloud software, and manned guarding. Consequently, the India access control hardware market size allocated to services is forecast to surpass USD 0.41 billion by 2031.

Software revenues are shifting to subscriptions, blurring the lines between software and services. Vendors that combine devices, cloud dashboards, and analytics lock in sticky margins, whereas pure-hardware players risk attrition unless they cultivate partner ecosystems.

Geography Analysis

North India attracts smart-city and data-center investments in Delhi-NCR, Agra, and Lucknow, with Gurugram alone securing over INR 10,000 crore (USD 1.2 billion) in data-center commitments in 2024. Inter-state spec divergence, however, pushes integrators to customize SKUs, stretching project lead times.

South India is the fastest-growing region in the India access control hardware market, driven by IT corridors in Bengaluru, Hyderabad, and Chennai that adopt mobile credentials and cloud dashboards. Tamil Nadu’s Safe City rollout and Telangana’s 500 MW data center pipeline accelerate biometric demand. Abundant electronics and automotive factories further lift hardware volumes, while channel partners in Bengaluru and Coimbatore provide after-sales density.

West and Central India concentrate hyperscale data centers in Mumbai and Pune, together hosting almost 60% of the installed capacity in 2024. Gujarat’s semiconductor fabs, backed by Tata Electronics and CG Power, localize the supply of microcontrollers and insulate vendors from overseas shortages.

East India trails in absolute numbers yet posts swift percentage growth as Kolkata IT parks and Bhubaneswar smart-city projects adopt standardized readers via GeM.

Competitive Landscape

The India access control hardware industry displays moderate concentration. Multinationals such as Honeywell, Johnson Controls, ASSA ABLOY, HID Global, and IDEMIA retain dominance in critical infrastructure and Fortune 500 campuses, due to their legacy accounts and brand assurance. Domestic integrators Matrix Comsec, Mantra Softech, eSSL Security, Godrej & Boyce, and Realtime Biometrics capture cost-sensitive sectors through value-added compliance and agile customization. The 2025 Electronics Component Manufacturing Scheme awards subsidies for PCB and connector production, allowing Indian firms to trim their bills of material by 15%.[4]Ministry of Electronics and Information Technology, “Electronics Component Manufacturing Scheme,” pib.gov.in

Strategic moves underline vertical integration and partnerships. Matrix Comsec acquired a Tamil Nadu contract manufacturer in 2024 to secure supply and reduce lead times. Honeywell and Johnson Controls co-develop India-hosted cloud controllers with local system integrators to satisfy data-residency mandates. Emergent challengers such as ZKTeco and Suprema leverage AI edge analytics to bypass cloud storage, highlighting a privacy-first differentiation in the Indian access control hardware market.

M&A appetite centers on niche biometric technologies, such as palm vein and 3D facial algorithms, as well as regional distribution networks. Vendors increasingly bundle managed services, driving recurring revenue above 30% of topline. This transition elevates barriers to entry, even as Make-in-India policies level hardware cost differentials.

India Access Control Hardware Industry Leaders

Honeywell International Inc.

Johnson Controls International plc

Robert Bosch GmbH

ASSA ABLOY AB

IDEMIA Identity and Security India Private Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: The Ministry of Electronics and Information Technology cleared the INR 22,919 crore Electronics Component Manufacturing Scheme to subsidize domestic PCB and semiconductor assembly, targeting a 50% domestic value-add threshold for government tenders.

- February 2025: Tata Electronics and CG Power have committed over USD 10 billion to semiconductor fabs in Gujarat and Maharashtra, with wafer starts scheduled for 2027.

- January 2025: Digi Yatra's facial-recognition boarding has been expanded to 24 airports, processing 15 million passengers, and plans to implement Aadhaar-enabled authentication by late 2025.

- December 2024: RBI’s Master Direction on IT Framework for Payment System Operators took effect, mandating biometric access logs for server rooms.

India Access Control Hardware Market Report Scope

The India Access Control Hardware Market Report is Segmented by Industry Vertical (IT and Telecom, Banking, Financial Services and Insurance, Government and Public Sector, Manufacturing, Healthcare, Transportation and Logistics, Defense and Aerospace, and Other Industry Verticals), Product Type (Card Readers and Access Devices, Biometric Readers, Electronic Locks, Controllers and Panels, and Other Types), and Component (Hardware, Software, and Services). The Market Forecasts are Provided in Terms of Value (USD).

By Industry Vertical

| IT and Telecom |

| Banking, Financial Services and Insurance |

| Government and Public Sector |

| Manufacturing |

| Healthcare |

| Transportation and Logistics |

| Defense and Aerospace |

| Other Industry Verticals |

By Product Type

| Card Readers and Access Devices |

| Biometric Readers |

| Electronic Locks |

| Controllers and Panels |

| Other Types |

By Component

| Hardware |

| Software |

| Services |

| By Industry Vertical | IT and Telecom |

| Banking, Financial Services and Insurance | |

| Government and Public Sector | |

| Manufacturing | |

| Healthcare | |

| Transportation and Logistics | |

| Defense and Aerospace | |

| Other Industry Verticals | |

| By Product Type | Card Readers and Access Devices |

| Biometric Readers | |

| Electronic Locks | |

| Controllers and Panels | |

| Other Types | |

| By Component | Hardware |

| Software | |

| Services |

Key Questions Answered in the Report

How big is the India access control hardware market in 2026?

The India access control hardware market size stands at USD 682.83 million in 2026.

What CAGR is forecast for access-control hardware in India to 2031?

The market is projected to post a 11.94% CAGR between 2026 and 2031.

Which industry vertical shows the fastest demand growth?

Healthcare is predicted to grow at a 14.72% CAGR through 2031, driven by biometric mandates under Ayushman Bharat Health Account guidelines.

Why are biometric readers outpacing card readers?

Post-pandemic hygiene priorities and rapid facial-recognition adoption at airports, metros, and corporate campuses fuel a 13.98% CAGR for biometric readers.

How do Make-in-India policies influence pricing?

Subsidies for PCB and semiconductor assembly cut bill-of-material costs by about 15%, allowing domestic vendors to price competitively against imports.

What restrains SME uptake of advanced systems?

Multi-modal terminals still cost around INR 50,000 (USD 600) per door, and limited credit access in Tier-2 and Tier-3 cities slows adoption despite quick payback periods.

Page last updated on: