Halal Cosmetic Products Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

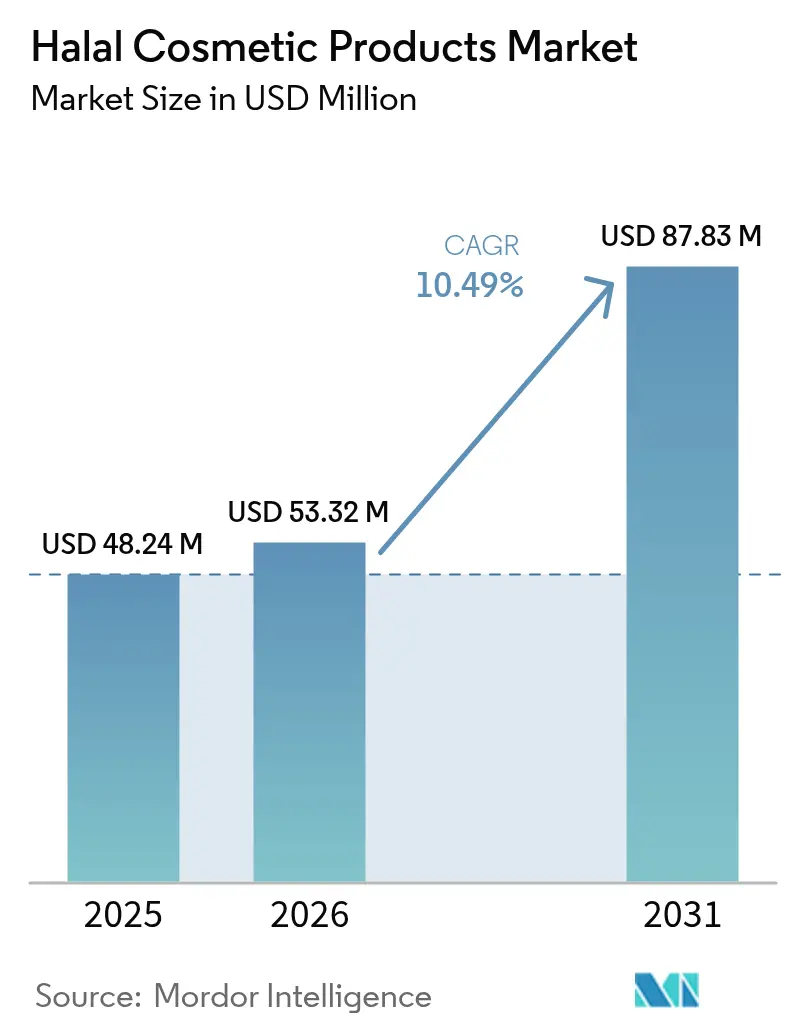

| Market Size (2026) | USD 53.32 Million |

| Market Size (2031) | USD 87.83 Million |

| Growth Rate (2026 - 2031) | 10.49% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Halal Cosmetic Products Market Analysis by Mordor Intelligence

The global halal cosmetics market size in 2026 is estimated at USD 53.32 million, growing from 2025 value of USD 48.24 million with 2031 projections showing USD 87.83 million, growing at 10.49% CAGR over 2026-2031. This growth trajectory reflects the intersection of regulatory mandates, demographic shifts, and evolving consumer preferences toward ethical beauty products that comply with Islamic principles. The rise of social media influencers and digital marketing strategies has significantly impacted consumer purchasing behavior, particularly among younger demographics. This digital shift influences market competition, as demonstrated by Wardah's expansion from Southeast Asia through e-commerce platforms. Indonesia's implementation of Government Regulation No. 42 of 2024 has introduced additional requirements for halal supervision and certification documentation. The regulatory landscape continues to evolve across different regions, with standardization efforts aimed at ensuring product authenticity and compliance with Islamic principles.

Key Report Takeaways

- By product type, skin care held 43.12% of the halal cosmetics market share in 2025, whereas fragrance is poised to grow at a 11.99% CAGR through 2031.

- By category, the mass segment commanded 66.45% revenue share in 2025, while the premium segment is projected to expand at an 11.42% CAGR during 2026-2031.

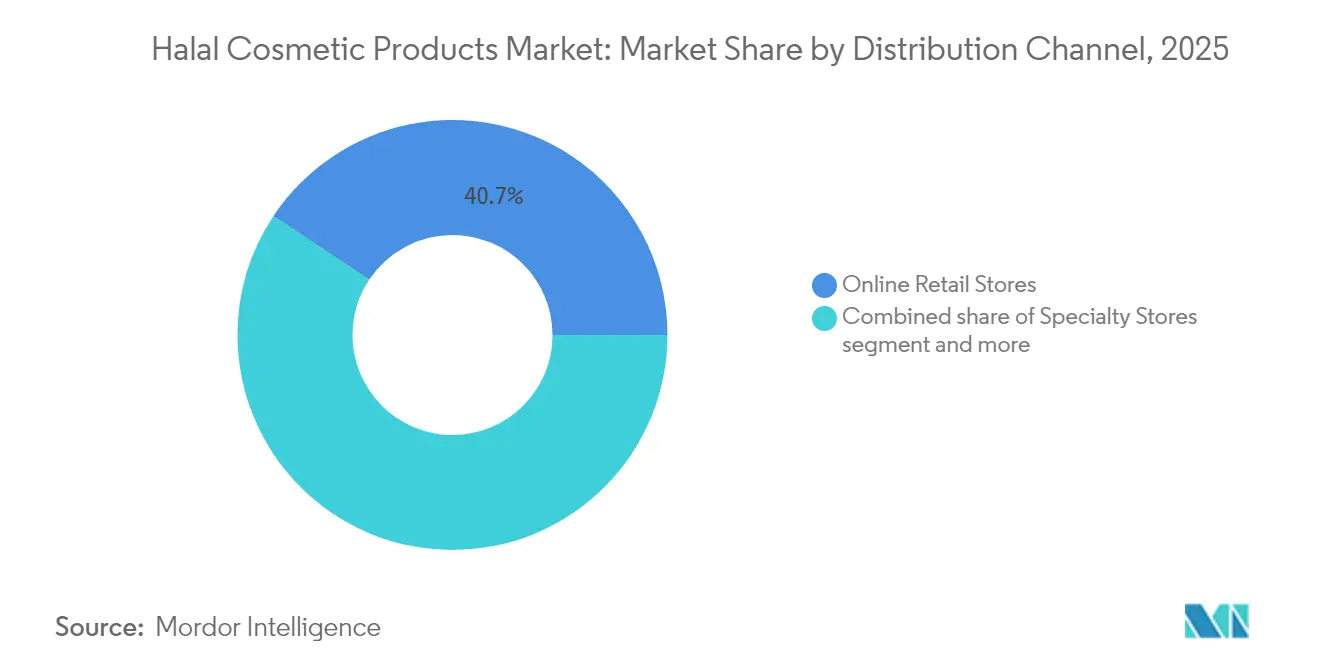

- By distribution channel, online retail stores captured 40.68% revenue in 2025 and are forecast to post the fastest 14.05% CAGR over the same period.

- By geography, Asia-Pacific accounted for 62.05% of 2025 sales, while the Middle East and Africa region is expected to register the highest 13.33% CAGR from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Halal Cosmetic Products Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand from Southeast Asian countries | +2.8% | ASEAN core, particularly Indonesia and Malaysia | Medium term (2-4 years) |

| Stringent regulatory framework gains consumer's trust | +2.1% | Global, with early adoption in Indonesia and Middle East | Long term (≥ 4 years) |

| Influence of Social Media Platforms | +1.9% | Global, strongest in Asia-Pacific and Middle East | Short term (≤ 2 years) |

| Growing concerns over the effects of synthetic products | +1.5% | Global, with premium segments leading adoption | Medium term (2-4 years) |

| Increased awareness about ethical and clean beauty | +1.4% | North America, Europe, and affluent Asian markets | Long term (≥ 4 years) |

| Growth in e-commerce and digital marketing | +1.1% | Global, accelerated in post-pandemic markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stringent regulatory framework gains consumer’s trust

The implementation of stricter halal certification standards is compelling cosmetics manufacturers to fundamentally rethink their formulation strategies. Indonesia's Law No. 33 mandates halal certification for all cosmetics by October 17, 2026, creating urgency for the 81% of registered cosmetics in the country that currently lack certification. This regulatory pressure extends beyond ingredient selection to production processes, where preventing cross-contamination has become a critical compliance challenge. Manufacturers must establish dedicated production lines and implement rigorous cleaning protocols between batches to maintain halal integrity. The certification process requires thorough facility audits and detailed documentation of ingredient sourcing and processing methods by certification bodies like LPPOM MUI in Indonesia and JAKIM in Malaysia. These requirements necessitate significant investments in facility upgrades, staff training, and quality control systems. Additionally, manufacturers must develop comprehensive documentation systems to track and verify the halal status of all ingredients throughout the supply chain.

Influence of social media platforms

In 2024, Saudi Arabia boasts a remarkable 99% internet penetration rate, as highlighted by the Communications, Space and Technology Commission[1]Communications, Space & Technology Commission, "The Saudi Internet Report 2024", www.cst.gov.sa. This digital landscape sees millennials and young adults actively engaging on social media, leading to heightened exposure to halal cosmetics. Beauty influencers on these platforms are not just promoting products; they're skillfully navigating the delicate balance between religious compliance and modern aesthetics. These influencers showcase application techniques that respect modesty principles while aligning with contemporary beauty standards, effectively bridging the gap between religious observance and self-expression. Furthermore, digital platforms empower consumers with knowledge about ingredient sourcing, certification processes, and brand values, often sidestepping traditional retailers who might not possess in-depth halal expertise. A surge in Google searches for "halal makeup" underscores a rising consumer awareness that transcends traditional Muslim-majority markets, hinting at a broader mainstream beauty audience that increasingly prioritizes ethical sourcing and ingredient transparency. Additionally, the integration of social commerce enables halal cosmetics brands to cultivate trust networks driven by community recommendations, a crucial strategy in an industry where authenticity is paramount.

Growing concerns over the effects of synthetic products

The growing consumer skepticism toward synthetic ingredients has created significant opportunities for halal cosmetics as natural alternatives in the beauty market. Companies must carefully balance halal certification requirements with clean beauty claims while maintaining product integrity. Generation Z and Generation Alpha consumers consider both environmental sustainability and personal health in their purchasing decisions, viewing halal certification as a comprehensive quality assurance system that addresses ethical and safety concerns. These consumer groups actively seek products that align with their values and demonstrate transparent sourcing practices. Halal cosmetics differentiate themselves from clean beauty products through strict certification standards and religious compliance rather than marketing claims. The certification process involves thorough documentation, ingredient verification, and manufacturing facility inspections. This has led to increased investment in specialized manufacturing facilities and the development of innovative natural alternatives to conventional cosmetic ingredients.

Growth in e-commerce and digital marketing

The online channel reduces entry barriers for niche halal brands while creating challenges in building consumer trust without physical sampling. Direct-to-consumer models enable brands to control their halal certification messaging and build customer communities. The digital environment facilitates education about halal standards, addressing certification differences across markets. Established companies are implementing omnichannel strategies to capture market share across consumer segments. Social media platforms have become crucial marketing channels, with influencer partnerships and user-generated content driving brand awareness and trust. Virtual try-on technologies and AI-powered skincare consultations are emerging as key tools for overcoming the limitations of online shopping.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Consumer inclination towards conventional product made with clean-label ingredients | -1.8% | Global, particularly in mature beauty markets | Medium term (2-4 years) |

| Proliferation of counterfeit products | -1.5% | Asia-Pacific and Middle East, with cross-border implications | Short term (≤ 2 years) |

| High cost of halal certification and compliance | -1.2% | Global, most acute for SMEs and new market entrants | Long term (≥ 4 years) |

| Complex supply chain issues | -0.9% | Global, with regional variations in certification recognition | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Consumer inclination towards conventional product made with clean-label ingredients

Mainstream beauty consumers increasingly gravitate toward familiar clean-label products rather than halal-certified alternatives, creating market segmentation challenges that limit halal cosmetics' addressable market expansion beyond Muslim demographics. Clean beauty positioning often overlaps with halal principles regarding ingredient purity and ethical sourcing, yet lacks the certification rigor and religious compliance framework that defines halal cosmetics. This consumer preference reflects marketing sophistication gaps where established beauty brands successfully communicate clean ingredient benefits while halal cosmetics struggle with mainstream positioning beyond religious compliance. The fragmentation creates competitive disadvantages for halal cosmetics in premium segments where clean beauty brands command higher price points through sophisticated brand storytelling and influencer partnerships. Market education requirements increase customer acquisition costs for halal cosmetics brands seeking to expand beyond core Muslim consumer segments into broader ethical beauty markets.

Proliferation of counterfeit products

Counterfeit halal cosmetics erode consumer trust and jeopardize the integrity of certifications. This issue is especially concerning given the religious significance and safety risks associated with products falsely marketed as halal-certified. In Muslim-majority markets, Chinese skincare brands, such as Skintific, are under scrutiny due to ambiguous origins and dubious halal certifications. Consumers are voicing concerns over the authenticity and compliance of these products. Indonesia's Food and Drug Authority (BPOM) has issued warnings about illegally imported cosmetics, underscoring the challenges regulators face in enforcing laws against counterfeit products, especially in the realm of cross-border e-commerce. In response to consumer concerns, BPOM introduced a new regulation in 2023 aimed at curbing the import of counterfeit products, including cosmetics, from abroad[2]Indonesian Food and Drug Supervisory Agency (BPOM), "REGULATION OF THE INDONESIAN FOOD AND DRUG AUTHORITY NUMBER 28 OF 2023", jdih.pom.go.id. Blockchain technology is being touted as a viable solution for authenticating supply chains. Research supports its potential, highlighting its ability to combat counterfeiting through unchangeable traceability records. Yet, the high costs and technical intricacies of blockchain deter many smaller halal cosmetics manufacturers, who often lack the resources for such advanced authentication systems.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Skin Care Dominates Innovation Pipeline

In 2025, skin care dominated the halal cosmetics market, accounting for 43.12% of its revenue. This highlights a daily reliance on moisturizers, serums, and cleansers, all steering clear of animal collagen and pork-derived emulsifiers. As Indonesia sets a certification deadline, even mainstream brands are being urged to reformulate, signaling a steady expansion for skin-focused halal items. Consumers increasingly link the absence of alcohol and harsh preservatives to safer, long-term use, leading to more frequent repeat purchases. While fragrance starts from a smaller base, it surges ahead of all other categories, boasting a 11.99% CAGR through 2031. This growth is fueled by the Middle East's appetite for oud-rich profiles, which navigate strict alcohol limits. The trend is further amplified by sensorial storytelling and travel-retail gifting bundles, boosting cross-border sales. Today's innovations spotlight water-based perfumes and encapsulated essential oils, ensuring scent longevity without ethanol. There's also a budding interest in probiotic skin fragrances, aiming to blend skin microbiome care with cultural scent preferences, enriching brand offerings.

Developing colour cosmetics and hair care poses a challenge, as their performance often hinges on polymer science, traditionally reliant on prohibited ingredients. However, with increasing investments in halal-certified pigments and plant-derived keratin, the performance gap is narrowing. Yet, the market still grapples with education. Brands adept at achieving colour payoff without carmine or standard silicones are seizing a first-mover edge in social media tutorials. Still, a complete shift across all SKUs may only materialize once more suppliers secure halal-compliant accreditation. To expedite this process, start-ups are forging partnerships with contract manufacturers already holding both Good Manufacturing Practice and halal certifications, significantly reducing their time-to-market.

By Category: Premium Segment Accelerates Growth

Mass products hold a 66.45% share of the halal cosmetics market in 2025, while the premium segment is expected to grow at a CAGR of 11.42% during 2026-2031. The expansion of premium products stems from increased disposable incomes in key markets and growing consumer awareness about ingredient quality and effectiveness. The rising middle class in Southeast Asian countries, particularly Indonesia and Malaysia, has contributed significantly to this premium segment growth, with consumers showing increased preference for high-end halal-certified products.

The GCC skincare market shows a notable shift toward premium products as consumers demonstrate a willingness to spend more on high-quality formulations that provide measurable results, according to a 2024 Chalhoub Group report. This trend is particularly evident in markets like the UAE and Saudi Arabia, where consumers are increasingly seeking products that combine luxury with religious compliance. Premium halal brands are establishing market presence through sophisticated formulations that integrate traditional ingredients with modern technology, enabling them to compete with established global brands while maintaining halal standards. For instance, Paragon Innovation's Crystallure brand demonstrates this approach by combining advanced skincare technology with halal compliance. The brand has successfully captured market share by offering products that feature innovative ingredients like niacinamide and peptides while ensuring all components meet halal requirements. Similar premium halal brands are emerging across various markets, focusing on clean beauty trends and sustainable packaging to appeal to environmentally conscious consumers who also prioritize halal certification.

By Distribution Channel: Digital Transformation Reshapes Access

Online Retail Stores achieve dual leadership with 40.68% market share in 2025 and fastest growth at 14.05% CAGR through 2031, fundamentally altering halal cosmetics distribution patterns and consumer education mechanisms. Digital channels enable direct brand-to-consumer relationships that bypass traditional retail intermediaries who may lack halal expertise or certification knowledge, particularly important for products requiring detailed ingredient and compliance information. E-commerce platforms facilitate consumer education through detailed product descriptions, certification documentation, and peer reviews that build trust in halal authenticity claims.

Supermarkets/Hypermarkets, Specialty Stores, and Other Distribution Channels face competitive pressure from digital transformation, though physical retail remains important for product trial and immediate gratification purchases. The online dominance reflects post-pandemic shopping behavior changes and younger consumer preferences for digital research and purchasing, particularly relevant for halal cosmetics, where certification verification and ingredient transparency are crucial decision factors.

Geography Analysis

Asia-Pacific holds 62.05% share of the halal cosmetics market in 2025, with Indonesia, the world's largest Muslim-majority nation, as the primary market. Indonesia's Government Regulation No. 42 of 2024, requiring halal certification for all cosmetics by October 2026, strengthens the region's market position. This regulation benefits local halal-certified brands and requires multinational companies to modify their production processes, as demonstrated by L'Oréal's investment in a halal-certified facility in Indonesia.

The Middle East and Africa region is expected to achieve a 13.33% CAGR from 2026-2031, despite its current smaller market share. This growth stems from its young population, digital connectivity, urbanization, and increasing disposable incomes. The market expansion aligns with a growing preference for Arabic beauty standards, creating demand for products that reflect local traditions.

Europe and North America represent developing markets for halal cosmetics, supported by Muslim diaspora populations and clean beauty trends among non-Muslim consumers. European regulations on ingredients complement halal requirements, enabling dual-certified products. In North America, regulatory frameworks like New Jersey's Halal Enforcement Unit, as reported by the New Jersey Division of Consumer Affairs in 2023, ensure product compliance, while organizations such as ISWA Halal Certification Department provide certification guidelines. South America shows growth potential, particularly in Brazil, where established cosmetics manufacturers can develop halal-certified products for domestic and international markets.

Regulatory Landscape

Regulation in halal cosmetic products is shaped by a mix of national halal assurance laws, cosmetics safety rules, and growing references to international standards. A central inflection point is Indonesia, where the Halal Product Assurance Agency (BPJPH) under the Ministry of Religious Affairs implements mandatory halal certification for cosmetics circulating or sold in the country by October 17, 2026, raising compliance urgency for brands that have historically marketed without halal certification. The certification ecosystem covers halal inspection and auditing, documentation of ingredient sourcing and processing, and controls to prevent cross-contamination across production and handling.

Malaysia also operates a mature halal certification framework led by JAKIM (Department of Islamic Development Malaysia), with Malaysian Standard MS 2634:2019 setting out general requirements for halal cosmetics. For cross-border alignment, OIC/SMIIC 4:2018 is commonly used as a reference point for halal cosmetics requirements, with SMIIC TC2 as the active technical committee. In Southeast Asia, the ASEAN Harmonized Cosmetic Regulatory Scheme (AHCRS) supports harmonization of cosmetics regulation and product registration, while halal certification remains under national jurisdiction, keeping multi-market certification planning and claim governance a key operational requirement for global brands.

Value Chain Analysis

The value chain starts upstream with suppliers of oils, waxes, surfactants, preservatives, fragrances, pigments, and specialty actives, where the highest halal-compliance sensitivity is tied to animal-, microbial-, and fermentation-derived inputs as well as processing aids. Ingredient sourcing is followed by formulation and manufacturing (brand owner facilities or contract manufacturers), then halal conformity assessment through accredited halal inspection bodies, and finally packaging, warehousing, and distribution across modern trade and e-commerce. In Indonesia in particular, compliance extends beyond finished goods to upstream documentation and auditability of raw materials, linking halal certification to conventional cosmetics registration and safety oversight.

Key bottlenecks are end-to-end traceability, segregation to prevent cross-contamination during production, transport, and storage, and limited availability of halal-certified inputs at scale, especially for performance-critical categories such as color cosmetics, hair care, and certain fragrance formats. Approaching the October 2026 BPJPH mandate in Indonesia increases operational demand for dedicated lines, validated cleaning procedures, traceable warehousing practices (clear coding and physical separation), and tighter coordination with inspection and certification bodies. As the online channel expands, documentation transparency and authentication become more central, supporting investments in digital traceability and stronger supplier qualification for brands targeting multi-country distribution.

Competitive Landscape

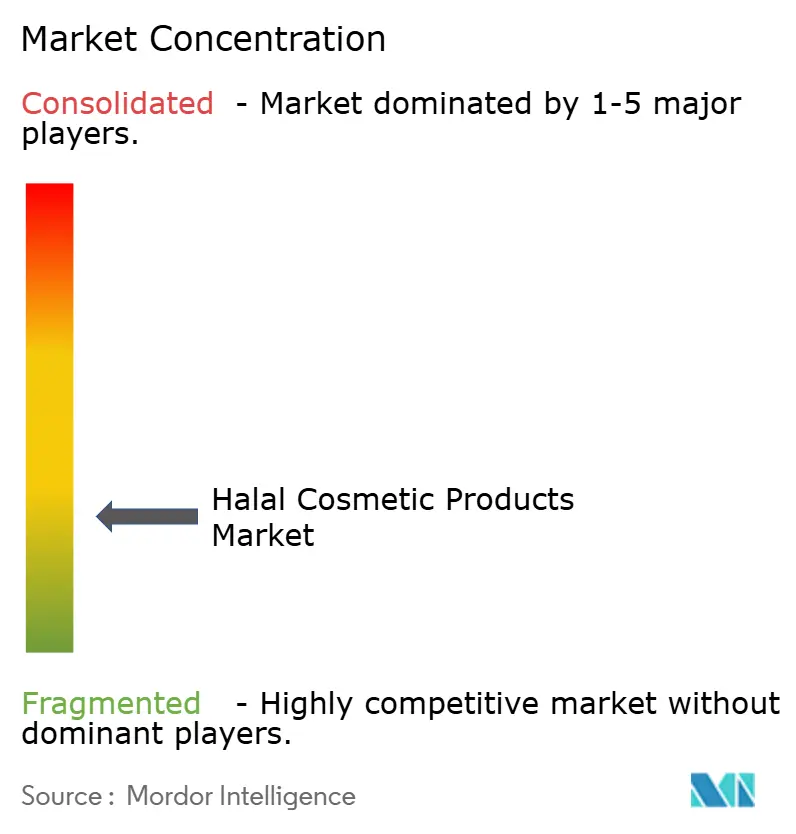

The halal cosmetics market shows fragmentation with a concentration score of 3 out of 10. This structure creates a competitive environment where regional leaders compete with multinational corporations that are adapting their products to meet halal requirements. Wardah, under Paragon Technology and Innovation, holds market leadership in Indonesia through its position as the country's first halal beauty brand. The company operates one of Southeast Asia's largest beauty research laboratories, collaborating with 300 global experts, demonstrating the increasing importance of scientific innovation in the halal segment.

Companies are increasingly adopting multi-brand portfolio strategies to target various price points and consumer segments. Paragon Innovation demonstrates this approach through its brand portfolio, which includes the mass-market teen brand Emina and the premium skincare line Crystallure. Market opportunities remain in specialized categories such as halal-certified color cosmetics and hair care, where product development faces formulation challenges.

The market structure continues to evolve as traditional beauty companies establish halal-certified production facilities. Additionally, digital-first brands are using e-commerce platforms to overcome distribution challenges while employing content marketing to educate consumers about halal certification and product benefits, enabling direct consumer relationships.

Halal Cosmetic Products Industry Leaders

-

PT Paragon Technology And Innovation

-

INIKA Organic

-

IVY Beauty Corporation

-

Ecotrail Personal Care Private Limited

-

Saba Personal Care SG

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Mandatory halal certification timelines are creating near-term whitespace in compliance-led product transitions and related service ecosystems, particularly in Indonesia where BPJPH requires halal certification for cosmetics by October 17, 2026. This is driving demand for halal-ready contract manufacturing capacity, ingredient documentation services, and audit-prepared quality systems that can help brands certify SKUs faster while maintaining cosmetics performance benchmarks. The opportunity is clearest in categories where halal formulation and supply constraints remain acute, including color cosmetics, hair care performance ingredients, and alcohol-free fragrance alternatives, because certification and cross-contamination controls extend from ingredients through production and logistics.

Cross-border growth is also supported by programs that reduce formulation friction for exporters and globalized beauty houses. In May 2026, South Korea announced support measures for halal certification, including on-site consulting for companies and a database of 4,000 halal-compliant ingredients to support K-Beauty firms, reinforcing the value of standardized ingredient intelligence for compliant product development. On the competitive front, multinational portfolio moves toward clean-label and ingredient transparency are intersecting with halal demand signals, including L'Oréal signing an agreement in June 2026 to acquire a majority stake in India-based Innovist (Bare Anatomy and Chemist at Play), which strengthens access to fast-growing personal care platforms where halal-compliant product lines can be built alongside clean and ethical positioning. With authenticity and documentation scrutiny increasing, investments in traceability infrastructure, stronger supplier qualification, and verifiable digital product information on e-commerce are practical routes for expanding distribution across Muslim-majority markets and diaspora-driven demand centers.

Recent Industry Developments

- June 2026: L'Oréal signed an agreement to acquire a majority stake in India-based personal care company Innovist, which includes brands such as Bare Anatomy and Chemist at Play. The deal strengthens L'Oréal's access to fast-scaling digital-first personal care platforms where halal-compliant and clean-label product roadmaps can be developed in parallel. It also raises competitive pressure on regional halal players as global groups add more formulation and brand-building capacity in Asia.

- November 2025: INIKA Organic launched Lip Alchemy, positioning the range as skincare-powered lip products aligned with natural and ethical beauty cues. The launch expands premium assortment depth, a key lever for halal and halal-adjacent brands competing on performance claims as well as ingredient provenance. It also supports higher-margin growth in categories where repeat purchase is driven by shade and finish innovation.

- October 2024: Vietnam introduced the National Halal Certification Center (HALCERT) and established new national halal standards covering categories that include cosmetics. The move adds a clearer pathway for certification and export readiness for brands targeting Southeast Asia and broader halal-consumer markets. It also increases the incentive for manufacturers and suppliers to align documentation and auditing practices with evolving national halal frameworks.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this methodology, the halal cosmetic products market covers the sales value of beauty and personal care products that are formulated and marketed to comply with halal requirements, and that are sold through offline and online channels to end consumers.

Scope exclusions: Products that contain alcohol, human-derived ingredients, or ingredients from animals that are prohibited for consumption by Muslims are excluded from the count.

Segmentation Overview

-

By Product Type

- Hair Care

- Color Cosmetics

- Fragrances

- Skin Care

- Others

-

By Category

- Mass

- Premium

-

By Distribution Channel

- Supermarkets/Hypermarket

- Specialty Stores

- Online Retail Stores

- Others Distribution Channel

-

By Geography

-

North America

- United States

- Canada

- Rest of North America

-

South America

- Brazil

- Argentina

- Rest of South America

-

Europe

- United Kingdom

- Germany

- France

- Italy

- Spain

- Rest of Europe

-

Asia-Pacific

- China

- Japan

- India

- South Korea

- Indonesia

- Australia

- Rest of Asia-Pacific

-

Middle East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle East and Africa

-

North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work started with building a clean definition and mapping the demand pool by country, category, and channel so the model has the right structure before numbers are added. We mainly relied on public sources such as national statistics portals, customs and trade data releases, and central bank FX series to keep the inputs comparable across markets.

To support the category and compliance lens, we also reviewed standards and guidance notes from halal certification bodies, trade association publications for cosmetics and personal care, and peer-reviewed papers on ingredient restrictions and consumer behavior. For company-level context like product mix and channel approach, we used public disclosures such as annual reports and investor presentations. Where company footprints were not fully available, we supplemented with licensed datasets focused on company financials and news, patent databases, and shipment-level trade datasets where available. These examples are not exhaustive, and many other sources were also checked for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work was used to sanity check the desk model and to pin down the practical meaning of halal compliance across product types, pricing tiers, and channels. We spoke with manufacturers, distributors, retailers, certification experts, and category specialists across APAC, EMEA, and the Americas, which helped confirm adoption levels, typical price ladders, and where informal claims differ from certified offerings.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 34% | CXOs: 15% | APAC: 50% |

| Mid tier: 45% | Functional/Unit leaders: 32% | EMEA: 32% |

| Smaller Players: 21% | Managers: 53% | Americas: 18% |

Market-Sizing & Forecasting

Sizing was built using top-down and bottom-up logic, with the top-down side anchored on the broader beauty and personal care spending pool, which is then filtered through halal relevant indicators by country. In practice, this meant we reconstructed demand using variables such as Muslim population and urbanization trends, category level consumption patterns in skincare and color cosmetics, online share progression, premiumization signals, and the share of products positioned as halal (certified or clearly compliant) in key channels.

Once the country and category layers were shaped, selective bottom-up checks were added so totals do not drift from reality. These included sampled average selling prices by category, channel checks on typical pack sizes and promo intensity, and supplier and distributor revenue benchmarks where public disclosures allowed it. When company level data was missing, gaps were handled through proxying from similar markets and then adjusting using primary feedback on penetration and price bands.

For forecasting, scenario analysis was used because demand is influenced by a mix of drivers that can shift quickly, such as certification tightening, retail channel changes, and macro conditions. Assumptions on adoption and pricing were stress tested with expert feedback, and then the final trajectory was selected only after the outputs matched the direction and magnitude seen in independent demand signals.

Data Validation & Update Cycle

Triangulation was done by comparing outputs against independent signals like category growth rates in personal care, changes in online penetration, and trade movement where cosmetics imports are a meaningful supply source. Outliers were flagged, reviewed, and recalculated, and where a variance could not be explained, we re-contacted respondents to clarify whether the issue came from scope, pricing, or timing.

Before sign-off, the model and assumptions go through a multi-step analyst review so the same logic holds across regions and categories. Reports are refreshed annually, and interim updates are made when material events occur, such as major regulatory shifts or sharp currency movements. Right before delivery, a fresh pass is completed so clients receive the latest updated view.

Mordor Intelligence's Halal Cosmetic Products Market Size Compared With Other Published Estimates

Published numbers for halal cosmetics can look far apart even when the topic sounds the same, since each publisher may be counting a different set of products and a different level of certification strictness. The year used as the base, the currency conversion timing, and whether the estimate is built from spending pools or from product roll-ups also tend to create visible gaps.

The main gap comes from whether loosely marketed claims are counted alongside certified halal lines, and Mordor Intelligence counts value only when the product aligns with clear ingredient restrictions and is positioned as halal in the market model, which keeps the total from being inflated by general natural or ethical beauty ranges.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 53.32 M (2026) | |

| Global Consultancy A | USD 53.12 B (2025) | Uses a much broader halal cosmetics framing that appears to sweep in wider beauty and personal care value pools, and the definition and compliance filters are not clearly stated, which can lift totals sharply. |

| Trade Journal B | USD 86.70 B (2023) | Reports consumer spending for halal compliant beauty and personal care at a high level, which can include indirect or loosely defined halal demand, and it is not presented with product-scope and pricing checks by category. |

The table shows that most of the spread is driven by how tightly the halal label is screened, and by whether the number represents a filtered cosmetics value pool or a wider spending figure. By keeping the steps traceable to product eligibility, category pricing, and channel adoption signals, our estimate is easier to reproduce and to update when market conditions change.

Key Questions Answered in the Report

How big is the halal cosmetics market in 2026?

It is valued at USD 53.32 million in 2026, with projections indicating USD 87.83 million by 2031 at a 10.49% CAGR.

Which product type leads the halal cosmetics market?

Skin care leads with 43.12% revenue in 2025, while fragrance grows fastest at a 11.99% CAGR.

Why is online retail critical for halal cosmetics brands?

Online channels account for 40.68% of 2025 sales and are set to expand at 14.05% CAGR, thanks to certification transparency tools and social-commerce integration.

Which region is expected to grow the fastest through 2031?

The Middle East and Africa are forecast to post a 13.33% CAGR, buoyed by Saudi Arabia’s Vision 2030 and high per-capita beauty spend.

Page last updated on: