Hadoop Big Data Analytics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 29.37 Billion |

| Market Size (2031) | USD 57.23 Billion |

| Growth Rate (2026 - 2031) | 14.28% CAGR |

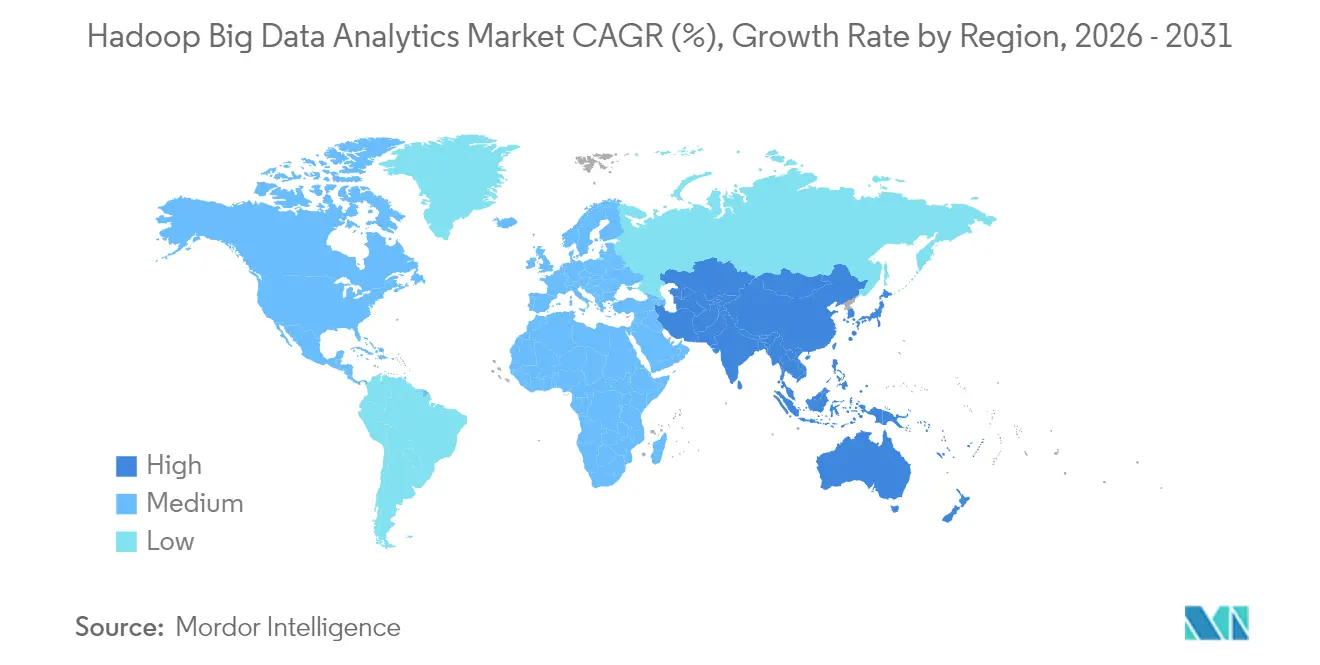

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Hadoop Big Data Analytics Market Analysis by Mordor Intelligence

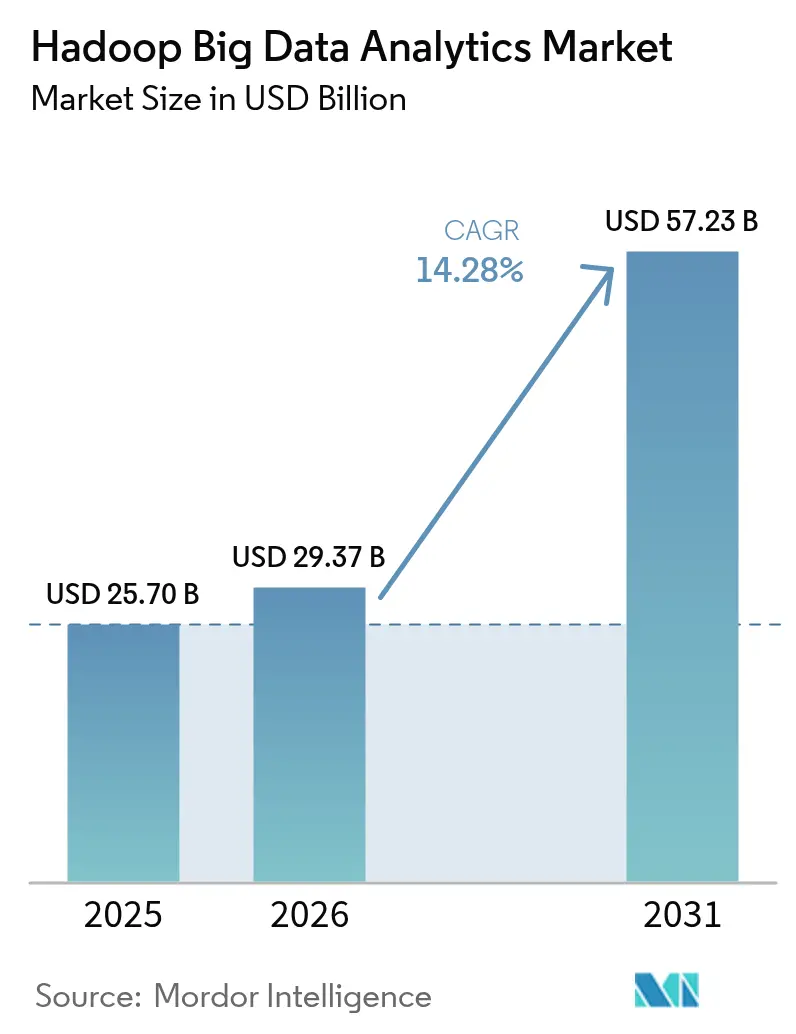

The Hadoop Big Data Analytics Market size market is expected to grow from USD 25.70 billion in 2025 to USD 29.37 billion in 2026 and is forecast to reach USD 57.23 billion by 2031 at 14.28% CAGR over 2026-2031.

Accelerated enterprise demand for distributed processing, the fusion of Hadoop with Spark- and TensorFlow-based AI workloads, and widening IoT data streams are the prime growth catalysts.[1]Acceldata, “Observability for Modern Data Systems,” acceldata.io Cloud-native Hadoop services are reshaping ownership economics, with documented 50% reductions in public-cloud costs and 30 times faster data-management speeds reported by tier-one vendors.[2]Cloudera, “Cloudera Data Platform Cloud Economics,” cloudera.com Concurrently, stringent data-localization mandates in banking and telecom, notably in the United States, European Union, and India, lock in fresh on-premise and hybrid deployments that complement the expansion of managed cloud clusters. Competitive tension is rising as lakehouse platforms such as Databricks and Snowflake target Hadoop workloads, yet traditional vendors defend share by hardening security, embracing open table formats, and deepening vertical add-ons for BFSI, healthcare, and manufacturing

Key Report Takeaways

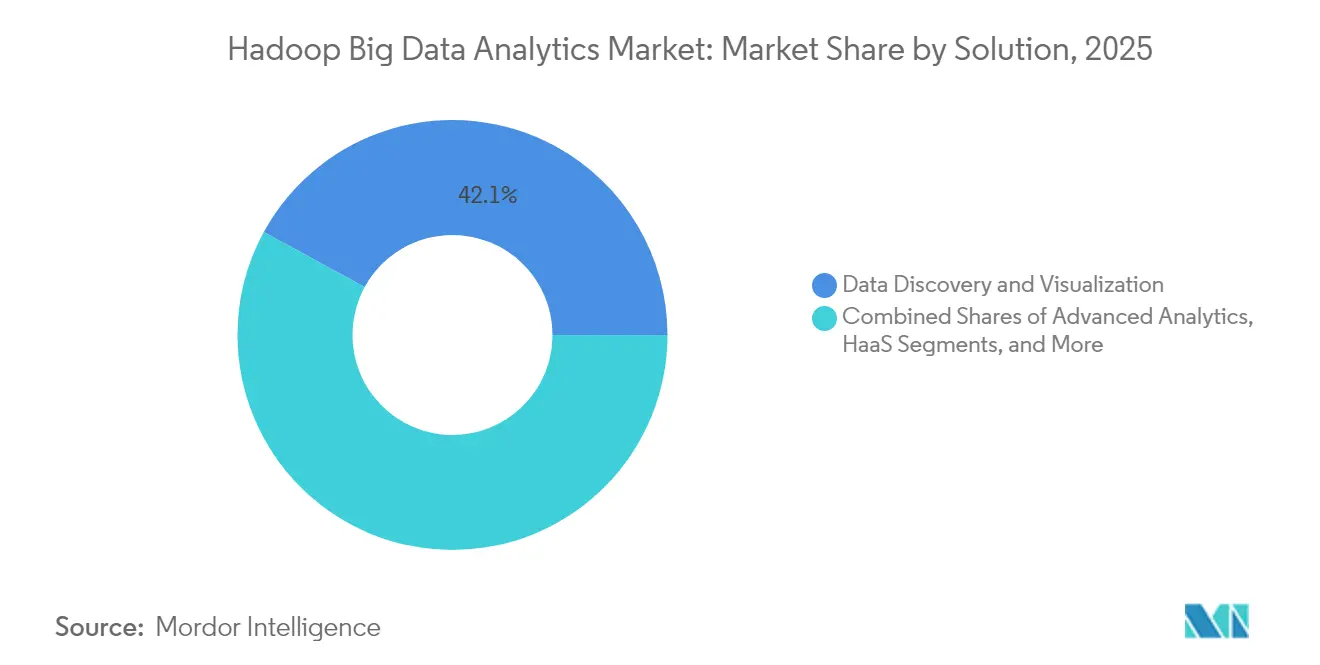

- By solution, data discovery and visualization held 42.05% revenue share in 2025 in the Hadoop big data analytics market, while Hadoop-as-a-Service is projected to advance at a 15.34% CAGR through 2031.

- By end-use industry, IT and Telecom led with 27.55% of Hadoop big data analytics market share in 2025; Healthcare and Life Sciences is forecast to expand at a 14.81% CAGR to 2031.

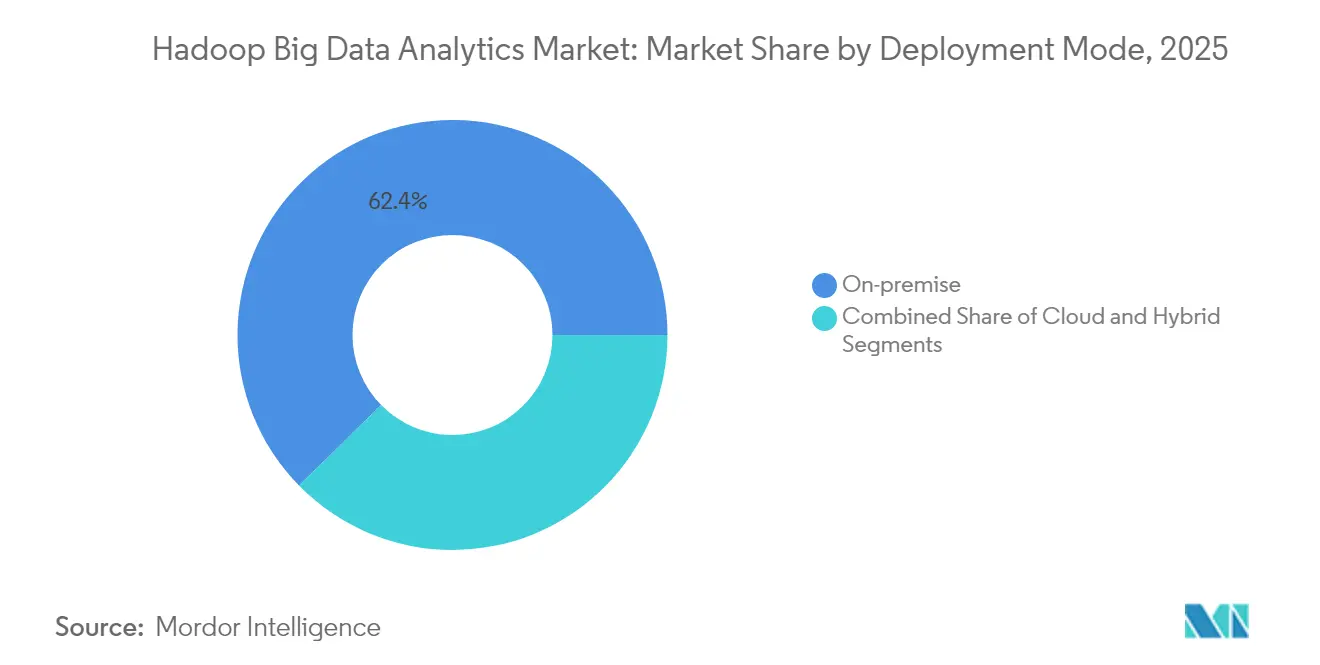

- By deployment mode, on-premise clusters accounted for 62.35% of the Hadoop big data analytics market size in 2025, whereas cloud deployments are growing at 15.69% CAGR.

- By organization size, large enterprises commanded 53.45% share in 2025 in the Hadoop big data analytics market, but SMEs are set to grow at 15.41% CAGR on the back of managed services.

- By geography, North America retained 37.55% share in 2025 in the Hadoop big data analytics market; Asia-Pacific is the fastest-growing region at 15.42% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Hadoop Big Data Analytics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data explosion from connected devices and streaming sources | +3.2% | Global, led by APAC IoT hubs | Medium term (2-4 years) |

| Cloud-native Hadoop platforms cutting TCO for SMEs | +2.8% | North America and EU, expanding to APAC | Short term (≤ 2 years) |

| Convergence of Hadoop with AI/ML workloads | +2.5% | Global tech centers | Medium term (2-4 years) |

| Government data-localization mandates | +2.1% | EU, India, China | Long term (≥ 4 years) |

| Real-time cyber-threat analytics in BFSI and telecom | +1.9% | North America and EU, expanding to APAC | Short term (≤ 2 years) |

| Edge-to-core architectures for predictive quality in manufacturing | +1.6% | Global hubs led by Germany, China, US | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Data explosion from connected devices and streaming sources

Unrelenting growth in IoT endpoints is transforming Hadoop from a batch engine into a real-time analytics backbone. Industrial firms have trimmed network bandwidth by up to 90% after shifting sensor analytics to edge-integrated Hadoop clusters. German and Chinese manufacturers report double-digit productivity gains after embedding Hadoop-driven predictive-maintenance workflows across multi-plant networks. The platform’s schema-on-read flexibility lets data teams fuse structured SCADA logs with semi-structured quality images and unstructured video streams in one federated fabric.

Cloud-native Hadoop platforms cutting TCO for SMEs

Managed Hadoop services are democratizing big-data workloads for smaller firms by eliminating racking, patching, and tuning overhead. A leading telco cut root-cause analysis cycles from several weeks to one minute while lowering analytics spend 70% after adopting a cloud-native observability layer. Parallel cases in healthcare show 3–5 × query-performance lifts and 90% storage savings compared with legacy relational stacks. These economics, coupled with usage-based billing, enable SMEs to rival enterprise-class insight programs without hiring scarce distributed-systems engineers.[3]IEEE Spectrum Editors, “The Data-Center Workforce Gap,” ieee.org

Convergence of Hadoop with AI/ML workloads

Embedding Spark, TensorFlow, and emerging LangGraph libraries on YARN transforms Hadoop into an AI-ready substrate. Enterprises deploying hybrid cloud AI agents now use the same HDFS backbone for feature stores and model-inference pipelines, compressing data-to-decision latency to seconds. IBM recorded a doubling of watsonx bookings in Q4 2024 on the back of customers co-locating AI training with Hadoop-resident data. Early patent activity around cooperative caching signals ongoing R&D aimed at shrinking shuffle overhead for large-scale gradient descent.[4]U.S. Patent Office, “Decentralized Caching for Distributed Analytics,” uspto.gov

Government data-localization mandates

Jurisdictions from the European Union to India oblige critical data to remain onshore, pushing enterprises toward in-country Hadoop clusters that blend security with low-latency analytics. France’s Heritage Code, for instance, enforces domestic storage of public archives, directly steering cultural institutions to local Hadoop infrastructure. The shared-responsibility model in public cloud heightens compliance risk, so regulated firms increasingly deploy hybrid blueprints in which sensitive workloads sit on-premise while less restricted analytics burst to managed services.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Talent scarcity in distributed-systems engineering | −2.3% | Global, acute in North America and EU | Long term (≥ 4 years) |

| Rising popularity of lakehouse engines | −1.8% | North America and EU, expanding globally | Medium term (2-4 years) |

| Vendor lock-in risks after Cloudera HDP/CDH end-of-support | −1.5% | Global, focused on enterprise segments | Short term (≤ 2 years) |

| Escalating privacy fines under GDPR and CCPA on mis-governed data lakes | −1.2% | EU and California, with global spillover | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Talent scarcity in distributed-systems engineering

Uptime Institute’s 2024 survey found 58% of operators unable to fill critical data-engineering roles, inflating total cost of ownership for self-managed Hadoop estates. Salary bands topping USD 218,000 for senior data engineers push some adopters to defer or shelve on-premise projects in favor of fully managed alternatives. Universities have ramped dedicated programs, yet graduate throughput still trails enterprise demand, signaling a multi-year structural constraint.

Rising popularity of lakehouse engines

Unified lakehouse platforms challenge legacy Hadoop spend by combining ANSI-SQL performance with open table formats. Databricks passed USD 3.7 billion in annualized revenue by mid-2025, a watershed that underlines buyers’ appetite for simplified management layers. In response, core Hadoop suppliers integrate Iceberg and Delta connectors while emphasizing strengths in streaming analytics, edge deployments, and rigorous data-governance tooling to slow workload attrition.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Solution: Hadoop-as-a-Service spearheads service innovation

Data Discovery and Visualization captured 42.05% of the Hadoop big data analytics market in 2025 as business users demanded intuitive querying on ever-larger clusters. Hadoop-as-a-Service (HaaS) is the breakout, tracking a 15.34% CAGR that outpaces every other solution group. The SaaS-like model outsources cluster orchestration and patching, freeing customers from low-level tuning and aligning spend with usage spikes. Cloudera’s public-cloud blueprint shows 50% cost savings against lift-and-shift alternatives, a clear driver of its HaaS momentum.

Managed elasticity also underpins real-time AI inference on shared YARN pools, allowing developers to launch short-lived GPU nodes without upfront capex. Independent tooling vendors fold ETL and cataloging into unified consoles so data teams traverse ingest, preparation, and visualization inside a single pane. Patent activity around decentralized caching and intent-based job scheduling suggests continued efficiency improvements, especially for high-concurrency dashboards surfaced through native BI plug-ins

By End-Use Industry: Healthcare accelerates digital transformation

IT and Telecom retained 27.55% revenue share in 2025 by relying on Hadoop for fraud detection, network telemetry, and customer-behavior analytics.Yet, healthcare is the fastest climber, advancing at 14.81% CAGR as genomics, EHR interoperability mandates, and connected-device telemetry flood data lakes with petabyte-scale feeds. England’s 100,000 Genomes Project and similar oncology initiatives require distributed stores to crunch variant calls and longitudinal patient records at production speed.

Precision-medicine pipelines benefit from Hadoop-backed feature stores that accelerate model retraining, while HIPAA-aligned HDFS encryption modules satisfy strict compliance needs. Hospitals reporting 90% storage TCO savings after migrating historical imaging archives add financial impetus to adoption. The sector’s growth trajectory signals a pivot from pilot projects to clinical-grade, AI-infused workflows that demand synchronized compute and storage scale.

By Deployment Mode: Cloud migration accelerates

On-premise clusters represented 62.35% of Hadoop big data analytics market size in 2025, anchored by data-sovereignty and latency sensitivities. Nonetheless, cloud deployments are racing ahead at a 15.69% CAGR. Amazon EMR alone serves thousands of production customers and benefits from native integration with S3, Glue, and SageMaker to streamline AI pipelines. Microsoft Azure HDInsight and Google Dataproc record similar momentum following the rise of delta-lake storage on object buckets.

The migration surge is accelerated by end-of-support milestones for legacy HDP/CDH releases, prompting enterprises to evaluate lift-and-shift versus refactor pathways. Cost-optimization levers such as spot-instance fleets and tiered object storage cut long-running job expense without compromising SLA. Hybrid blueprints persist where sovereignty or low-latency workloads require edge processing, leveraging Kubernetes-managed Cloudera Data Platform on-premise with policy-driven spillover to public cloud.

By Organization Size: SMEs embrace managed services

Large enterprises controlled 53.45% revenue in 2025 and continue to run petabyte-scale clusters for risk scoring, supply-chain orchestration, and omnichannel personalization. The SME cohort, however, is growing 15.41% annually as managed HaaS offers remove entry barriers. A Bangladesh telecom reduced troubleshooting cycles from multi-week to minutes while slashing analytics cost 70% after adopting a cloud-native observability suite.

Self-service templates now provision production-ready stacks in hours, pairing schema-evolution wizards with built-in lineage graphs so lean teams uphold governance without hiring specialized architects. Cross-region replication and pay-as-you-grow pricing give mid-market firms enterprise-grade resiliency, further leveling the competitive field. Training marketplaces attached to vendor portals mitigate skills gaps, accelerating time-to-value for data-driven initiatives in finance, retail, and smart manufacturing.

Geography Analysis

North America generated 37.55% of 2025 revenue as financial-services majors and hyperscalers cemented Hadoop’s role in mission-critical analytics. JPMorgan Chase runs more than 150 PB across fraud-detection and liquidity-risk models, an exemplar of production-scale deployment. Healthcare innovators report triple-digit query-speed gains on encrypted Hadoop stores, a dynamic reinforced by abundant cloud infrastructure from AWS, Microsoft, and Google, each disclosing record quarterly cloud revenue above USD 12 billion in early 2025.

Asia Pacific is the fastest-moving theatre, charting a 15.42% CAGR as multiyear investments from Alibaba, Tencent, and Huawei add sovereign capacity and AI-optimized silicon to regional clouds. China alone committed USD 40 billion to cloud build-out in 2024, with an additional CNY 380 billion earmarked for AI and data centers through 2027. India’s data-localization edicts further boost domestic Hadoop rollouts, especially in BFSI and e-governance.

Europe maintains steady expansion under GDPR’s strict residency rules. Cultural institutions comply with France’s Heritage Code by placing digitized archives on local Hadoop clusters, while public-sector agencies rely on in-country object stores fronted by Spark engines for budget analytics. Emerging regions in South America and MEA are nascent but rising, driven by smart-city pilots and telecom analytics that tap cloud-hosted HaaS to bypass capex constraints.

Regulatory Landscape

Data governance, privacy, and AI accountability requirements influence Hadoop big data analytics deployments, especially when distributed data lakes support regulated workloads. In the European Union, Regulation (EU) 2023/2854 (Data Act) and Regulation (EU) 2024/1689 (AI Act) raise expectations for data access governance, documentation, and controls for AI systems that use large-scale enterprise datasets. The AI Act timeline is a planning reference for platform owners because initial enforcement starts from August 2, 2026, pushing earlier investments in data lineage, auditability, and model-data governance across hybrid Hadoop estates.

Public-sector data management directives also shape standards and procurement patterns. In the United States, the Federal Big Data R&D Strategic Plan (2024) and the Federal Data Strategy and associated OMB guidance (M-25-05, issued January 2025) reinforce structured practices for managing government data assets, with proposed legislation (for example, S. 4098 and H.R. 7907) pointing toward AI-ready dataset and framework requirements through bodies such as NIST. For global enterprises, these shifts translate into jurisdiction-specific compliance architectures, where data residency, access controls, and governance metadata become key inputs for Hadoop, HaaS, and hybrid data platform design.

Value Chain Analysis

The value chain is anchored in open-source foundations (Apache Hadoop ecosystem components such as HDFS, YARN, and Hive), commercial platform distributors and hybrid data platform vendors (for example, Cloudera), and cloud infrastructure and managed-service providers (AWS EMR, Microsoft Azure HDInsight, Google Dataproc). It also includes an expanding layer of data integration, governance, observability, and analytics tooling. Data producers include IoT/OT systems, enterprise applications, telecom networks, and digital channels, while downstream consumers include BI teams, fraud and cyber analytics, and AI/ML engineering groups running Spark and TensorFlow workloads adjacent to Hadoop data. Procurement increasingly factors in interoperability with open table formats and catalogs, so Hadoop-resident datasets can feed broader lakehouse patterns.

Service delivery and operations are a midstream link: systems integrators and managed service providers package migrations, security hardening, and day-2 operations, while vendors use cloud-native and Kubernetes-based control planes to reduce the burden of patching and scaling. Telecom and BFSI remain anchor buyers that keep long-lived HDFS clusters in production where migration risk and data gravity are high, and they shift new workloads toward object storage and modern orchestration. Industry coordination is also visible through alliances, such as Cloudera joining the AI-RAN Alliance (June 2025), which reflects how real-time, edge-adjacent analytics and AI-native network operations are pulling Hadoop-related platforms deeper into telecom infrastructure modernization programs.

Competitive Landscape

The vendor arena is moderately concentrated. AWS, Microsoft, and Google capture a combined 63% of global cloud infrastructure spend and couple that muscle with native Hadoop services such as EMR, HDInsight, and Dataproc. Databricks’ USD 3.7 billion run rate and net-retention above 140% validate the lakehouse thesis and intensify competition for SQL analytics and AI workloads.

Traditional distributors pivot by embedding open table formats, extending governance layers, and bundling MLOps to protect their install bases. Cloudera’s survey showing 96% of enterprises planning AI-agent expansion underscores why platform roadmaps now spotlight vector-search and low-latency serving.. IBM leverages watsonx to position its hybrid-cloud narrative, doubling software bookings and patenting encryption-at-rest innovations that resonate in regulated sectors.

White-space opportunities emerge in edge-to-core manufacturing analytics, SME-centred managed services, and verticalized compliance blueprints. Start-ups focus on click-through deployment, auto-scaling, and observability, touting 30–40% performance lifts and 70% cost downs compared with traditional support contracts. The resulting landscape balances scale advantages of hyperscalers with niche agility of specialized providers.

Hadoop Big Data Analytics Industry Leaders

Alteryx Inc.

IBM Corporation

Microsoft Corporation

Oracle Corporation

Cloudera

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Hybrid modernization programs are creating near-term whitespace for tools and services that connect legacy Hadoop estates to open table formats and unified catalogs without requiring disruptive migrations. Enterprises still hold substantial on-premise footprints (on-premise held 62.35% of deployment share in 2025) for regulated or latency-sensitive workloads, and they need governed interoperability across HDFS, object storage, and multi-cloud environments. Product roadmaps that emphasize open data interoperability and elastic scaling align with this requirement, supported by Cloudera highlighting long-term stability, elastic scale, and open data interoperability in its hybrid data and AI platform updates (April 2026).

A second opportunity area sits at the intersection of big data operations and agentic AI, where governed business logic and analytics workflows run closer to data rather than being moved into separate AI silos. Alteryx actions in 2026, including an AI Insights Agent distributed via Google Cloud Marketplace (April 2026) and additions such as Agent Studio and an MCP Server to operationalize autonomous agents in enterprise tools (May 2026), point to active buyer demand for AI-enabled automation that respects governance boundaries. For Hadoop-centric organizations, this supports platforms and partners that can expose curated datasets, lineage, and policy controls to AI agents and real-time applications across Slack, Microsoft Teams, and cloud data services, while maintaining compliance obligations under privacy rules and emerging AI governance requirements.

Recent Industry Developments

- June 2026: Alteryx expanded cloud-native analytics execution with Live Query for Snowflake, enabling transformations and orchestration to run where data already resides in the Snowflake AI Data Cloud. This reduces data movement and supports tighter governance for analytics workflows that interact with large data lakes and enterprise catalogs.

- June 2025: Databricks confirmed a USD 3.7 billion annualized revenue run rate and introduced Lakebase to expand beyond classic warehousing use cases. The move intensified competitive pressure on Hadoop-centric analytics as lakehouse platforms bundle SQL, governance, and AI workloads into unified operating models.

- March 2024: NITRD published the US Federal Big Data R&D Strategic Plan (2024), reinforcing priorities around scalable data management, analytics, and trustworthy data use across government programs. The plan supports continued public-sector demand for governed, distributed data platforms and influences vendor roadmaps aligned to compliance, metadata, and reproducible analytics.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers revenues earned from Hadoop-based big data analytics solutions that help enterprises store, process, and analyze large datasets across on-premises, cloud, and hybrid environments.

Scope exclusions: Excludes general BI and data analytics tools that do not run on, or are not sold for, Hadoop ecosystem workloads.

Segmentation Overview

- By Solution

- Data Discovery and Visualization

- Advanced Analytics

- Data Integration and ETL

- Hadoop-as-a-Service (HaaS)

- Consulting and Support Services

- By End-Use Industry

- BFSI

- Retail and E-commerce

- IT and Telecom

- Healthcare and Life Sciences

- Manufacturing and Industrial

- Media and Entertainment

- Government and Public Sector

- Other End-Use Industries

- By Deployment Mode

- On-premise

- Cloud

- Hybrid

- By Organization Size

- Large Enterprises

- Small and Medium Enterprises

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- United Kingdom

- Germany

- France

- Italy

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research started with compiling a fact base around enterprise data growth and analytics adoption, then narrowing it to Hadoop-led workloads. Public sources were used to anchor macro direction, including the US Bureau of Economic Analysis (industry IT spend signals), US Bureau of Labor Statistics (data and software employment trends), the World Bank (digital infrastructure indicators), the OECD (ICT statistics), and National Institute of Standards and Technology publications (cloud and data security guidance).

We also reviewed vendor public filings, investor presentations, product documentation, and standards bodies to understand typical pricing logic and how deployments shift between on-premises and cloud. Where needed, paid subscriptions for company financials and news, patent databases, and contract and tender tracking were used to confirm product positioning and customer wins, so the work did not rely on a single dataset. These sources were treated as illustrative only, with additional public references used for cross-checking, validation, and clarification during the work.

Primary Interviews and Surveys

Primary work was used to validate what portion of big data analytics spending is truly Hadoop-tied, and how that mix changes by industry and deployment model. We spoke with solution providers, system integrators, cloud-focused delivery teams, and enterprise buyers across APAC, EMEA, and the Americas to pressure-test adoption drivers, discounting patterns, and replacement cycles. The goal was to reconcile desk assumptions with what is actually being purchased today for Hadoop-based analytics use cases.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 27% | CXOs: 19% | APAC: 48% |

| Mid tier: 51% | Functional/Unit leaders: 21% | EMEA: 30% |

| Smaller Players: 22% | Managers: 60% | Americas: 22% |

Market-Sizing & Forecasting

Sizing uses a top-down and bottom-up approach, where enterprise analytics spend is first reconstructed into a Hadoop-relevant demand pool using deployment penetration and workload mix, and then corroborated through selective supplier and channel checks. To keep the model repeatable, we tied key drivers to inputs such as cloud versus on-premises share shifts, Hadoop-as-a-Service uptake, typical subscription and support renewal patterns, the pace of data integration and ETL modernization, and spending momentum in data-heavy industries like BFSI, retail and e-commerce, and IT and telecom.

Forecasting is mainly done through scenario analysis supported by a light multivariate view. Drivers like cloud migration pace, security and compliance emphasis, and enterprise budget sentiment are stress-tested with expert feedback. When a bottom-up proxy is incomplete, gaps are handled using peer clustering by delivery model and industry focus, followed by a reasonableness check against known adoption and pricing bands.

Data Validation & Update Cycle

Validation is done by triangulating the modeled totals against independent signals, such as regional IT spending direction, cloud workload indicators, and observed deal and renewal activity from public announcements. Outliers are investigated through variance checks at the region and deployment level, and analysts re-contact interviewees when assumptions move materially, or when a major market event can shift demand.

Before sign-off, the full workbook is reviewed in steps, starting with input sanity checks and then moving to growth logic and sensitivity tests. Reports are refreshed annually, and interim updates are made when major pricing, regulation, or platform shifts occur. Right before delivery, a final review pass is completed so clients receive the most current view possible.

Mordor Intelligence's Hadoop Big Data Analytics Market Sizing Compared With Other Published Estimates

Published market sizes for Hadoop big data analytics can vary because teams do not always count the same revenue streams, and the base year and currency timing can also differ. Differences also show up when one estimate leans on broad big data signals, while another ties demand to Hadoop-specific deployments.

Standalone managed data warehouses and non-Hadoop analytics platforms sit outside Mordor Intelligence's scope, which narrows the demand pool to Hadoop-linked solutions and related services and helps avoid double counting across adjacent analytics categories.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 29.37 B (2026) | |

| Industry Publisher A | USD 12.86 B (2024) | Uses an earlier base year and a broader component structure that can mix general big data analytics demand with Hadoop-linked spending, which pulls the current-year value down versus a later base year. |

| Global Publisher B | USD 14.78 B (2024) | Anchors sizing on a different starting year and applies a higher long-range growth path, and it is less clear how cloud-managed Hadoop services versus adjacent analytics software are separated, which can widen the spread over time. |

The table indicates that base-year selection and scope cuts are the biggest reasons the values do not line up. By keeping inputs tied to Hadoop workload adoption, deployment mix, and renewal and service revenue patterns, our estimate stays traceable to clear variables that can be rechecked as the market evolves.

Key Questions Answered in the Report

What is the current value of the Hadoop big data analytics market?

The Hadoop Big Data Analytics Market generated USD 29.37 billion in 2026 and is on track to reach USD 57.23 billion by 2031

Which solution segment grows the fastest?

Hadoop-as-a-Service leads with a 15.34% CAGR as firms opt for managed, cloud-native deployments

Why is Asia Pacific the fastest-growing region?

Massive cloud capex from providers like Alibaba and data-localization mandates in India and China push regional CAGR to 15.42%

How are healthcare organizations using Hadoop?

Hospitals employ distributed clusters for genomics, real-time patient monitoring, and cost-efficient storage, driving a 14.81% CAGR in the segment

How are vendors responding to lakehouse competition?

Traditional Hadoop suppliers integrate open table formats, strengthen governance, and bundle AI workflows to retain workloads migrating toward unified lakehouse platforms

Page last updated on: