US Property Management Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

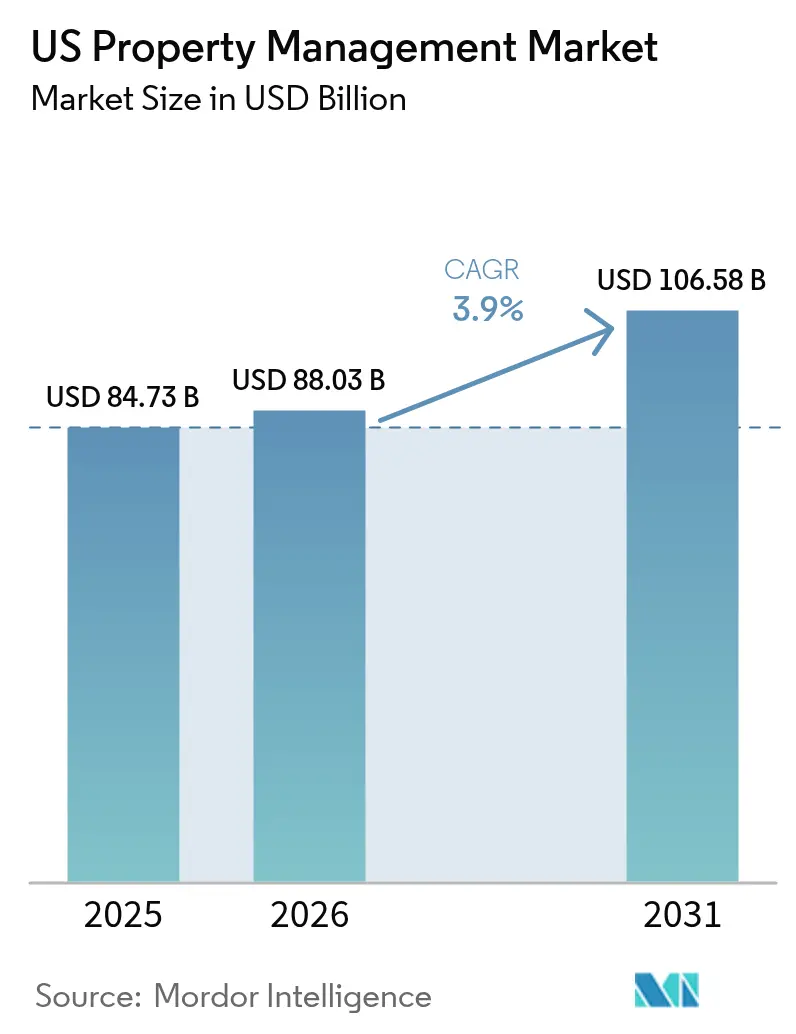

| Base Year Market Size (2025) | USD 84.73 Billion |

| Market Size (2026) | USD 88.03 Billion |

| Market Size (2031) | USD 106.58 Billion |

| Growth Rate (2026 - 2031) | 3.90% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

US Property Management Market Analysis by Mordor Intelligence

The US Property Management Services Market size was valued at USD 84.73 billion in 2025 and estimated to grow from USD 88.03 billion in 2026 to reach USD 106.58 billion by 2031, at a CAGR of 3.9% during the forecast period (2026-2031). Growth rests on resilient rental demand, institutional ownership of both single-family and multifamily assets, and renewed leasing activity in premium office buildings. Federal Reserve surveys show 27% of U.S. adults rent their homes, underpinning a large tenant base that requires professional oversight. Institutional investors use scale to drive professional management, while environmental, social, and governance (ESG) regulations accelerate demand for compliance-oriented services. Technology adoption, especially artificial-intelligence tools that automate leasing, maintenance, and resident engagement, further supports efficiency and tenant retention. Competitive intensity is rising as national firms buy tech-enabled specialists to widen service breadth and geographic reach[1]Board of Governors, “Report on the Economic Well-Being of U.S. Households,” federalreserve.gov.

Key Report Takeaways

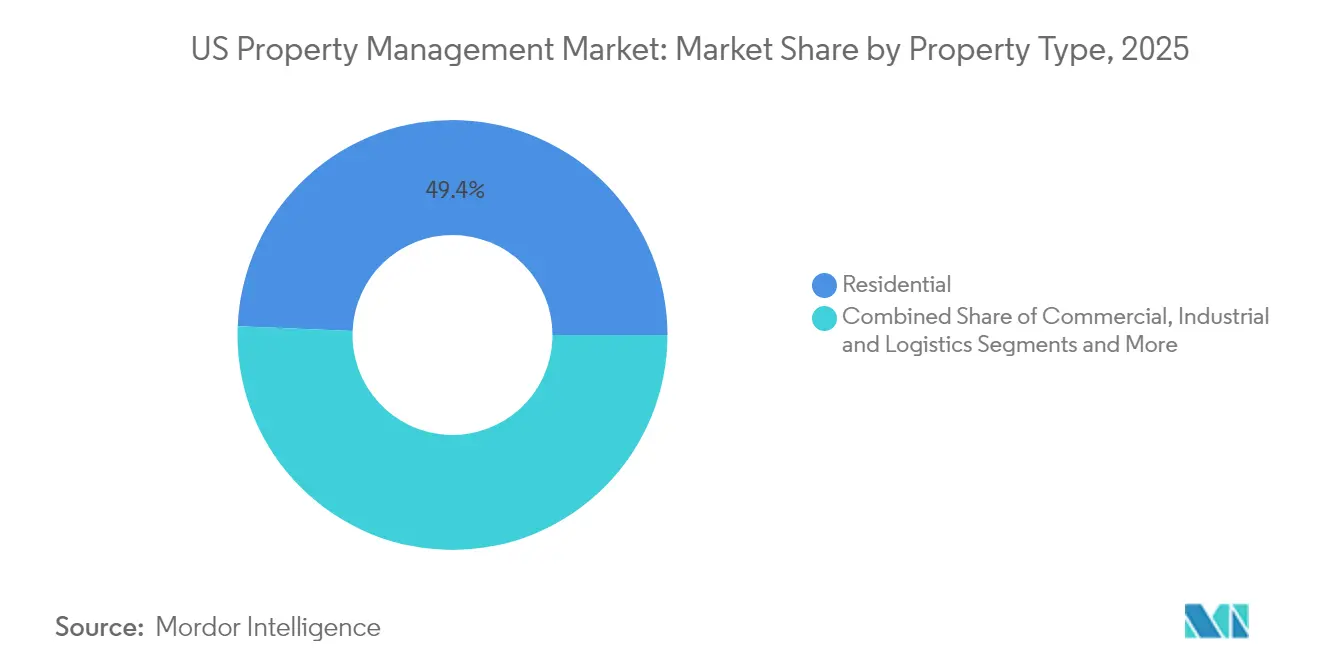

- By property type, residential assets held 49.35% of the US property management services market share in 2025. Commercial properties are projected to log the fastest 4.82% CAGR through 2031.

- By service type, tenant and resident services captured 34.12% revenue share in 2025. Other services, led by compliance and legal work, are forecast to grow at 4.6% CAGR to 2031.

- By geography, the Southeast commanded 20.10% of 2025 revenue, while the West is set to expand at a 4.93% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

US Property Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of single-family rental portfolios | +1.2% | Sunbelt states, Western U.S., Southeast | Long term (≥4 years) |

| Rising demand from Class-A commercial real estate | +0.8% | California, New York, Texas major metros | Medium term (2-4 years) |

| Aging U.S. housing stock needs maintenance | +0.7% | Northeast, Midwest legacy markets | Long term (≥4 years) |

| Growing institutional outsourcing by pension/SWF investors | +0.6% | National, major metropolitan areas | Long term (≥4 years) |

| Adoption of AI-enabled leasing & service tech | +0.4% | Tech-forward markets, urban centers | Short term (≤2 years) |

| ESG & green-lease compliance pressure | +0.3% | California, New York, and federal properties | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Expansion of Single-Family Rental (SFR) Portfolios

Institutional ownership of single-family homes grew from bulk foreclosure purchases in the early 2010s to sophisticated build-for-rent programs by 2024. The GAO traced holdings of 170,000-300,000 homes by 2015, with larger footprints today as funds accelerate acquisitions. American Homes 4 Rent, for example, managed 61,336 homes and generated USD 1.729 billion rental revenue in 2024. Scale drives demand for standardized leasing, maintenance, and compliance processes that individual landlords rarely provide. Consequently, residential specialists and integrated REIT platforms gain pricing power and recurring revenue inside the US property management services market[2]U.S. Government Accountability Office, “Rental Housing: Institutional Investors in the Single-Family Market,” gao.gov.

Rising Demand from Class-A Commercial Real Estate

Premium office assets are regaining tenant attention as employers seek high-amenity space to support hybrid work models. CBRE recorded 18% leasing revenue growth in 2024, including a 28% jump in office leasing in New York. Owners of trophy buildings deploy concierge teams, smart-building platforms, and curated tenant experiences to differentiate supply. These value-added services typically require large management budgets, allowing professional firms to command higher fees. Performance benchmarking and amenity upgrades also create cross-selling potential for energy management and workplace consulting. The result is durable revenue growth for managers focused on Class-A portfolios within the US property management services market.

Aging U.S. Housing Stock Needs Professional Maintenance

The median age of occupied homes exceeded 41 years in 2024, according to Census Bureau data. Older properties demand systematic upkeep to remain habitable and code-compliant. Regional shortages of skilled trades heighten the need for coordinated vendor networks and preventive maintenance programs. Professional managers provide bundled repair services, capital-planning tools, and purchasing leverage that individual owners cannot replicate. This maintenance imperative is particularly acute in Northeast and Midwest cities where housing stock dates to the mid-20th century, reinforcing steady fee growth in the US property management services market.

Growing Institutional Outsourcing by Pension/SWF Investors

Public pension systems and sovereign wealth funds have expanded U.S. real estate allocations above 10% of their portfolios since 2023. Many lack in-house resources to run day-to-day property operations across multiple cities. Outsourcing offers standardized reporting, local compliance knowledge, and technology platforms that improve risk control. Management contracts typically span five years, creating sticky fee income. As allocation momentum continues, outsourced mandates are expected to add several basis points to overall growth in the US property management services market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Interest-rate–driven transaction slowdown | -0.9% | National, concentrated in high-value markets | Short term (≤ 2 years) |

| State & city rent-control legislation | -0.5% | California, New York, select urban markets | Medium term (2-4 years) |

| Skilled trade-labor shortages raising OPEX | -0.4% | National, acute in Texas, Florida, California | Medium term (2-4 years) |

| Owners' shift to DIY prop-tech platforms | -0.3% | Suburban markets, smaller property portfolios | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Interest-Rate-Driven Transaction Slowdown

Elevated borrowing costs since late 2023 have caused a pause in property sales and ground-up development. CBRE noted that investment volume fell sharply even as existing portfolios remained relatively stable. Less trading means fewer property takeovers and new-build assignments for managers who earn onboarding and construction-management fees. Smaller firms that rely on deal flow face near-term revenue stress. Nonetheless, recurring management contracts cushion the impact, allowing the broader US property management services market to continue expanding, albeit at a slower clip until rates normalize.

State & City Rent-Control Legislation

Revisions to rent-stabilization laws in California, New York City, and other metros cap annual rent hikes and lengthen eviction timelines. AvalonBay highlighted these rules as a material business risk that constrains rental revenue and complicates pricing algorithms. Management firms must invest in compliance staff and reporting systems, adding overhead. Fee structures tied to gross rent may compress, especially for operators with heavy exposure to regulated units. Over time, sophisticated compliance capability becomes a competitive differentiator, yet near-term margin pressure weighs on segment growth inside the US property management services market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Property Type: Residential Dominance Drives Institutional Scale

Residential properties accounted for 49.35% of 2025 revenue, making them the largest slice of the US property management services market share. Institutional single-family rentals and multifamily portfolios deliver predictable, recurring fees based on rent rolls, while amenity-rich communities drive ancillary income from parking, storage, and smart-home subscriptions. Commercial properties are projected to register a 4.82% CAGR and will narrow the gap as leasing rebounds in Class-A offices and experiential retail.

The residential segment benefits from concentrated holdings by REITs such as Invitation Homes, which invested USD 425.2 million in property upgrades in 2024. Scale improves vendor pricing, technology adoption, and response times, reinforcing professional management as table stakes for institutional owners. Commercial growth is fueled by corporate flight to quality and new flexible-workspace models integrated into traditional buildings. Industrial and logistics assets add further upside as e-commerce firms seek proximity to consumers and rely on specialized maintenance and security protocols. Together, these dynamics sustain balanced momentum in the US property management services market.

By Service Type: Compliance Services Accelerate Growth

Tenant and resident services generated 34.12% of segment revenue in 2025 and remain the core of the US property management services market. Activities include marketing, leasing, rent collection, and resident engagement. Other services, consisting of legal, compliance, and renewal work, are set to grow the fastest at 4.6% CAGR.

Regulatory expansion drives this outperformance. The EPA’s building-performance standards now require benchmarking, public disclosure, and retrofit planning across more than 40 jurisdictions. Managers with in-house compliance teams and digital dashboards capture the rising demand for specialized reporting. Maintenance and facility services are also leveraging Internet-of-Things sensors for predictive analytics, creating cross-selling opportunities. As complexity rises, full-service providers gain fee share at the expense of niche operators in the US property management services market.

Geography Analysis

The Southeast accounted for 20.10% of 2025 industry revenue, buoyed by sustained in-migration, corporate relocations, and a comparatively light regulatory touch that appeals to institutional capital. Florida, Georgia, North Carolina, and South Carolina sit at the center of this trend, offering large pipelines of single-family rental homes and garden-style multifamily projects that require professional oversight. Investors appreciate the region’s lower operating costs and expanding tenant base, which together create predictable fee income for managers operating in the US property management services market.

The West is projected to deliver the fastest 4.93% CAGR through 2031, powered by technology-sector expansion and premium property values in California, Washington, and Nevada. Owners face complex building-performance rules and ESG disclosure mandates, prompting demand for managers with deep compliance and PropTech capabilities. High asset values also translate into elevated management fees, reinforcing the West as an attractive growth frontier despite its regulatory hurdles.

The Northeast, Midwest, and Southwest form a balanced core of mature markets. High property values and intricate rent-control regimes in the Northeast favor large operators with legal depth. Midwest cities present an aging housing stock that needs cost-effective maintenance and capital-improvement planning. The Southwest, led by Texas and Arizona, continues to attract population inflows and institutional funds that establish regional platforms spanning residential, commercial, and industrial assets. Together, these dynamics sustain nationwide momentum in the US property management services market while highlighting varying regional strategies for growth.

Competitive Landscape

National managers, regional specialists, and tech-oriented newcomers contend for a share in a fragmented but consolidating arena. CBRE’s USD 400 million purchase of Industrious in January 2025 created a Building Operations & Experience segment comprising 7 billion-plus square feet under oversight, illustrating how scale plus flexible-workspace capabilities differentiate full-service platforms.

Strategic acquisitions remain a favorite playbook. Firms seek data-rich portfolios, ESG advisory practices, and AI application suites that accelerate tenant service and reduce operating costs. Integration of these capabilities often unlocks new fee pools, such as compliance consulting and smart-building retrofits, thereby raising switching barriers for owners.

Technology disruptors focus on cloud-based leasing, maintenance marketplaces, and predictive analytics that promise lower costs and enhanced tenant satisfaction. While many start-ups cater to small landlords, larger incumbents have begun white-labeling similar tools, blurring competitive lines. Specialized managers of healthcare and logistics facilities, such as Medical Properties Trust with 439 U.S. hospitals, carve niches where domain expertise outweighs pure scale. These varied strategies collectively propel continuous innovation across the US property management services market.

US Property Management Industry Leaders

Greystar Real Estate Partners

CBRE Group, Inc.

Lincoln Property Company

Jones Lang LaSalle (JLL)

Cushman & Wakefield plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: American Homes 4 Rent reported USD 1.729 billion in 2024 rental revenue while managing 61,336 single-family homes across 24 states.

- February 2025: AvalonBay Communities raised its full-year core FFO growth outlook to 3.7% and increased projected development starts to USD 1.05 billion.

- January 2025: CBRE Group completed the acquisition of the remaining equity in Industrious National Management Company for approximately USD 400 million, folding the business into its new Building Operations & Experience segment.

- December 2024: UDR posted rental income of USD 1.664 billion and maintained 60,000 apartments across 21 U.S. markets.

US Property Management Market Report Scope

A property management company deals directly with the tenants or prospects, saving the property owner's time, as they do not have to worry about marketing the rentals, negotiating with the tenants, handling maintenance and repair issues, collecting rent, responding to tenant complaints, and even pursuing evictions. A property management company brings experience in terms of handling property and provides the owner with optimal solutions.

The US property management market is segmented by end user (commercial and residential) and service (marketing, property evaluation, tenant services, maintenance, and other services). The report offers market size and forecasts for the US market in value (USD) for all the above segments.

| Commercial |

| Residential |

| Industrial & Logistics |

| Institutional & Mixed-Use |

| Marketing & Leasing |

| Property Evaluation & Due Diligence |

| Tenant & Resident Services (Renting, Leasing, etc.) |

| Maintenance, Repair & Facility Management |

| Lease Administration & Compliance |

| Other Services (Compliance, Legal Services, Renewals, etc.) |

| Northeast |

| Midwest |

| Southeast |

| West |

| Southwest |

| By Property Type | Commercial |

| Residential | |

| Industrial & Logistics | |

| Institutional & Mixed-Use | |

| By Service Type | Marketing & Leasing |

| Property Evaluation & Due Diligence | |

| Tenant & Resident Services (Renting, Leasing, etc.) | |

| Maintenance, Repair & Facility Management | |

| Lease Administration & Compliance | |

| Other Services (Compliance, Legal Services, Renewals, etc.) | |

| By Geography | Northeast |

| Midwest | |

| Southeast | |

| West | |

| Southwest |

Key Questions Answered in the Report

What was the US property management services market size in 2026?

It reached USD 88.03 billion, with a 3.9% CAGR forecast through 2031.

Which property type led revenue in 2025?

Residential assets held the top position with 49.35% market share.

Which service category is expanding the quickest?

Compliance, legal, and renewal services are projected to grow at 4.6% CAGR to 2031.

Why is California so important to property managers?

High property values, strict ESG mandates, and extensive tenant-protection laws support premium fee opportunities.

How are interest rates affecting the sector?

Higher borrowing costs have delayed property sales, reducing onboarding and development-management fees in the short term.

What role does technology play in market growth?

AI-enabled leasing, predictive maintenance, and smart-home integrations enhance efficiency and tenant experience, supporting margin expansion.

Page last updated on: