Graphic Film Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 34.96 Billion |

| Market Size (2031) | USD 44.66 Billion |

| Growth Rate (2026 - 2031) | 5.03% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

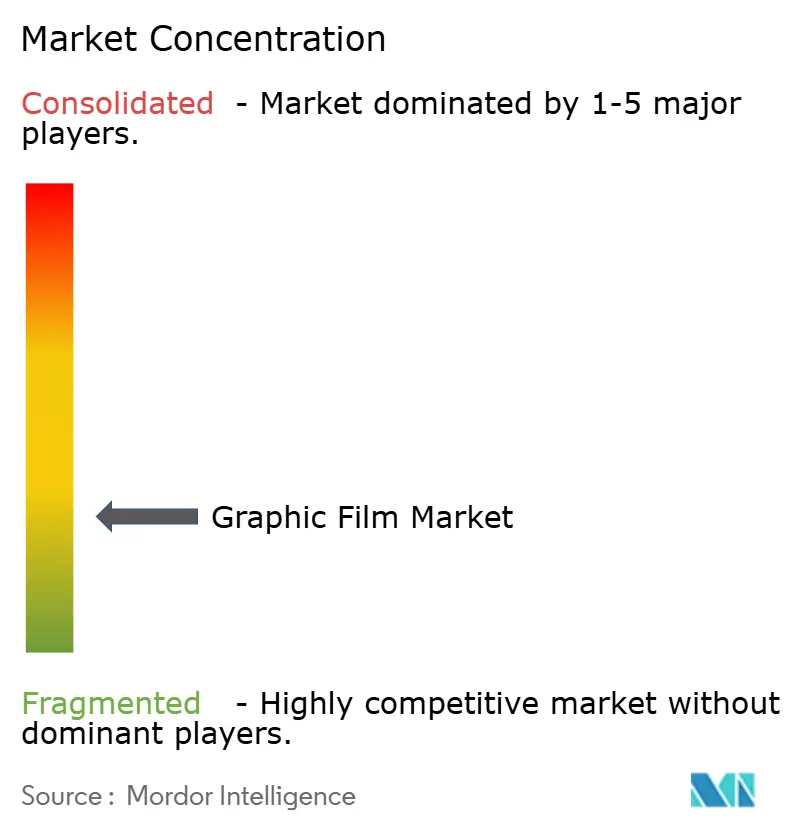

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Graphic Film Market Analysis by Mordor Intelligence

The graphic films market size in 2026 is estimated at USD 34.96 billion, growing from 2025 value of USD 33.29 billion with 2031 projections showing USD 44.66 billion, growing at 5.03% CAGR over 2026-2031. Rising construction modernization, rapid adoption of digital printing, and widening brand‐promotion needs keep demand resilient. Manufacturers are channeling R&D efforts into UV-inkjet-compatible products that reduce curing times, enhance color fidelity, and lower volatile organic compound emissions. Meanwhile, the Asia-Pacific region benefits from a growing polymer production scale and burgeoning infrastructure pipelines, making it the volume and growth engine of the graphic films market. Despite PVC’s dominance, regulatory pressure is steering the fastest growth toward recyclable PET substrates, while volatile raw material prices and photoinitiator shortages intermittently erode margins.

Key Report Takeaways

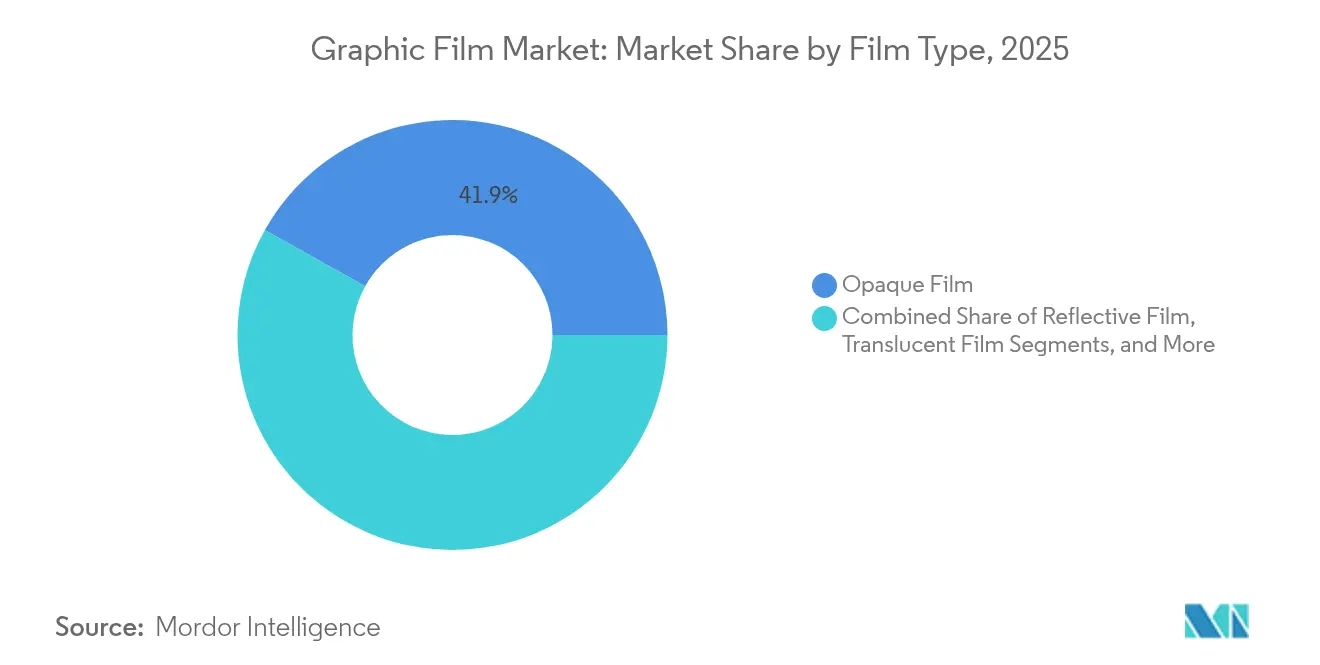

- By film type, opaque films accounted for 41.88% of the graphic film market share in 2025.

- By polymer, the graphic film market size for PET is projected to expand at a 6.12% CAGR between 2026-2031.

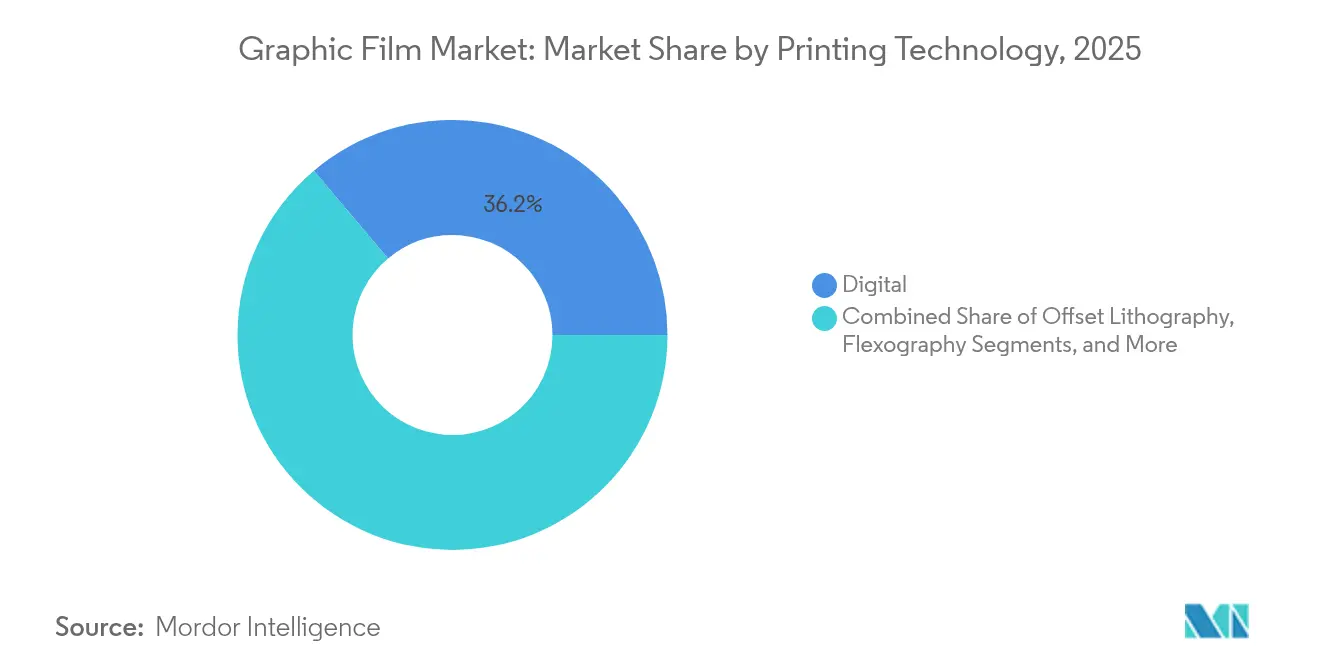

- By printing technology, digital captured a 36.15% share of the graphic films market size in 2025.

- By end-user industry, the graphic film market size for building and construction applications is expected to grow at a 6.6% CAGR between 2026-2031.

- By region, the Asia-Pacific region led with a 45.30% market share of the graphic films market in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Graphic Film Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growth in the construction industry and higher living standards | 1.8% | Global, with APAC and Middle East leading | Medium term (2-4 years) |

| Rising demand for vehicle-wrap and fleet graphics | 1.2% | North America and Europe core, expanding to APAC | Short term (≤ 2 years) |

| Penetration of digital and UV-inkjet printing technologies | 1.5% | Global, with early adoption in developed markets | Medium term (2-4 years) |

| Expansion of retail PoS and way-finding signage | 0.9% | Global, concentrated in urban centers | Short term (≤ 2 years) |

| Emerging antimicrobial graphic films in healthcare settings | 0.4% | North America and Europe, expanding globally | Long term (≥ 4 years) |

| Adoption of electrochromic/smart glazing graphic films | 0.3% | North America and Europe, pilot projects in APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growth in the construction industry and higher living standards

Urbanization across Asia-Pacific and the Middle East spurs large-scale infrastructure builds that specify graffiti-resistant, long-life graphic films for wayfinding and façade branding. Project owners integrate Building Information Modeling with graphic film specifications, enabling precise material planning and lower installation waste. Architects favor customizable finishes that merge aesthetics with energy-efficient glazing, widening application breadth. Government stimulus for transport hubs, public housing, and smart cities anchors volume commitments. As living standards rise, residential developers are adopting interior decorative films that meet green certification goals, thereby reinforcing the medium-term growth of the graphic films market.

Rising demand for vehicle-wrap and fleet graphics

Fleet operators shift from paint to film wraps to achieve rapid brand makeovers and paint protection in one step. Surging electric vehicle fleets intensify demand for lightweight, easily updatable graphics that minimize drag and power consumption. Ride-sharing and last-mile delivery companies frequently refresh their campaign artwork, favoring removable, low-adhesion films. Premium wraps enhance resale values and reduce downtime, as entire fleets can be rebranded overnight. Growth momentum in APAC follows the U.S. and European adoption curves as small businesses adopt wraps for hyper-local marketing, supporting a near-term uplift in the graphic films market.

Penetration of digital and UV-inkjet printing technologies

UV-inkjet presses eliminate plate-making steps, reduce cure cycles, and improve scratch resistance, thereby significantly reducing turnaround times for converters. Digital workflows integrate with cloud-based color management and predictive maintenance, reducing waste while enabling mass personalization at scale. Lower minimum order quantities invite small retailers and artisans who previously lacked access to professional-grade films. As solvent-based emissions decline, compliance costs fall, widening global acceptance. Equipment upgrades accelerate film innovation because converters demand substrates engineered for higher ink loads and faster throughput, raising the value of digital-ready products within the graphic films market.

Expansion of retail PoS and way-finding signage

Omnichannel retailers rely on durable yet replaceable films for seasonal promotions and QR-enabled shopper engagement that bridges online and in-store journeys. High-contrast films enhance accessibility compliance for visually impaired patrons ADA regulations. Urban transit authorities deploy reflective way-finding graphics that reduce maintenance costs compared to painted signs and withstand the removal of graffiti solvents. Integrated Near-Field Communication tags turn static signage into data-rich touchpoints that track shopper flows. These factors sustain steady demand for premium films in retail and smart public-space environments, thereby enhancing overall growth prospects for the graphic films market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in prices of PVC, PET and specialty additives | -1.1% | Global, with Asia-Pacific manufacturing most affected | Short term (≤ 2 years) |

| Stringent regulations on PVC and solvent-based inks | -0.8% | Europe and North America leading, expanding globally | Medium term (2-4 years) |

| Limited recyclability hindering green-building certification | -0.5% | Europe and North America, expanding to APAC | Medium term (2-4 years) |

| Supply shortages of photoinitiators for UV-cure inks | -0.3% | Global, concentrated in specialized chemistry supply chains | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Volatility in prices of PVC, PET and specialty additives

Swinging crude oil and energy costs ripple through PVC and PET resin markets, compressing converter margins on long-term contracts. Concentrated supply in Asia magnifies geopolitical and weather-related disruptions that can idle downstream coating lines. Specialty additives, such as UV stabilizers and plasticizers, often come from narrow supplier pools with limited ramp-up capability, resulting in spot shortages. Producers respond by dual-sourcing, expanding resin capacity closer to demand centers, and introducing price-adjustment clauses, yet cost unpredictability remains a drag on the graphic films market.

Stringent regulations on PVC and solvent-based inks

European REACH and evolving U.S. state laws restrict certain plasticizers and solvent emissions, forcing reformulation and capital spending on alternative chemistries. LEED and BREEAM scoring frameworks discount PVC content, influencing specifiers to favor PET or polypropylene even when performance trade-offs exist.[1]U.S. Green Building Council, “LEED v4.1 Building Design and Construction,” usgbc.org Compliance testing and label changes can significantly increase overhead, particularly for small converters. Although complete PVC bans are rare, mounting certification hurdles slow the adoption of PVC in new green-building projects, tempering the medium-term expansion of the graphic films market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Film Type: Opaque films cement broad utility

Opaque films accounted for 41.88% of the graphic films market share in 2025, driven by their universal suitability for vehicle wraps, storefronts, and façade graphics. These films mask substrate flaws and deliver vivid branding, sustaining high-volume demand. Innovations now target UV-inkjet compatibility and low-temperature pliability, broadening end-use scenarios across climates. In contrast, reflective films, driven by safety regulations and energy-saving mandates, outpace the total graphic films market at a 7.05% CAGR. Transparent and translucent variants gain niche share in retail showcases and backlit architectural elements. Suppliers expand their portfolios with antimicrobial and graffiti-resistant topcoats, which help lift average selling prices.

Reflective film adoption accelerates as transportation departments mandate higher retroreflectivity for road signs and railcars. Architects specify heat-reflective window films that cut HVAC loads, linking optics to sustainability targets. Meanwhile, installers favor next-generation opaque films featuring repositionable adhesives that cut labor time by 10-15%. ORAFOL’s USD 165–175 million expansion underpins supply security for multiple film classes, underscoring confidence in long-range demand. Collectively, these dynamics entrench film-type diversity and fuel healthy revenue streams in the graphic films market.

By Polymer: PVC retains scale as PET rises

PVC controlled 62.98% of the global graphic films market size in 2025, owing to its low cost, ease of calendering, and robust adhesion on irregular surfaces. Yet, sustainability drivers and scrutiny of plasticizers propel PET volumes, driving the material at a 6.12% CAGR. PET’s recyclability appeals to specifiers chasing circular-economy credits, especially in Europe. Polypropylene and polyethylene remain in specialized niches where chemical resistance or tearability is essential.

The pending PFAS phase-out forces value-chain adjustments in high-durability topcoats, creating white space for novel resins. PET investments in Alabama by Polyplex diversify the North American supply and shorten lead times for converters hit by freight volatility. Producers hedge by developing PVC-free portfolios that match flexibility and printability benchmarks. Success here would realign polymer shares, yet near-term economics keep PVC at the helm of the graphic films market.

By Printing Technology: Digital gains critical mass

Digital platforms accounted for 36.15% of the graphic films market share in 2025, as converters adopted instant changeover and data-driven personalization. UV-inkjet heads drive sub-segment growth at a 7.58% CAGR, combining speed with low emissions. Screen printing retains niches that require heavy ink laydown or special textures, while flexography and offset printing are more suitable for very high-run jobs where per-unit economics dominate.

Artificial intelligence now predicts nozzle health, aligning quality with first-time-right goals that save media waste. Photoinitiator shortages briefly capped UV capacity in 2024, but supply stabilized after specialty chemical producers added reactors, reinstating confidence for expansion. Inline color management tools assure brand consistency across global campaigns. Consequently, the technology mix continues to shift towards digital, reinforcing structural changes within the graphic films market.

By End-User Industry: Construction pulls ahead

Advertising and promotion maintained a 41.22% revenue share in 2025 by leaning on quick-change graphics for omnichannel campaigns. Film suppliers offer high-tack, bubble-free adhesives that speed up window-front installations. Construction outpaces all others at 6.6% CAGR as architects fold films into curtain walls, elevator cabs, and smart façades that double as energy moderators. Automotive wraps are growing alongside the rollouts of electric vehicles, and healthcare is adopting antimicrobial films to curb hospital-acquired infections.

Growing public-sector budgets for smart transit nodes diversify demand beyond retail, expanding it to other sectors. Silver-ion embedded films receive approvals under EPA antimicrobial listings, enabling hospital and mass transit deployments that command premium pricing. Such varied use cases shield suppliers from cyclical dips in any single vertical, lending stability to the broader graphic films market.

Geography Analysis

The Asia-Pacific region secured 45.30% of global revenue in 2025 and is expected to grow at a 7.28% CAGR to 2031, driven by unmatched polymer capacity and government infrastructure agendas. China’s Belt and Road projects, India’s smart-city initiatives, and the relocation of Southeast Asian manufacturing continually widen their application breadth. Domestic converters benefit from short lead times and rising middle-class consumption that lifts automotive wraps and retail signage volumes.

North America’s demand is mature yet value-rich, centered on premium wraps, solar-control window films, and antimicrobial coatings. Polyplex’s new PET line in Alabama secures local feedstock, trimming dependency on imports and sharpening cost predictability. Regulatory leadership in low-VOC inks and recyclable substrates prompts converters to pioneer sustainable offerings, which later cascade worldwide.

Europe matches North America in terms of technology adoption and sustainability regulations. REACH updates and discussions on the plastic tax accelerate the adoption of PVC alternatives and the migration to solvent-free inks, influencing product formulation globally. Elsewhere, the Middle East leverages tourism and mega-event developments for signage demand, while South America’s infrastructure revival in Brazil and Mexico nurtures moderate growth. These multi-regional trends collectively reinforce the expansion outlook for the graphic films market.

Regulatory Landscape

In Europe, Regulation (EU) 2025/40 on packaging and packaging waste entered into force on 11 February 2025 and applies from 12 August 2026. It tightens requirements that affect substrate selection, recyclability design, and labeling practices for film-based packaging and related applications. The PPWR also clarifies scope boundaries, including exclusions for certain adhesive process films used as manufacturing enablers rather than packaging, which influences how some pressure-sensitive and functional film products are classified and managed for compliance.

In the United States, food-contact uses relevant to pressure-sensitive label constructions are governed by the FDA framework for Food Contact Substances and requirements such as 21 CFR 175.125 for pressure-sensitive adhesives used as food-contact surfaces for labels and tapes. Alongside VOC and chemicals management pressures referenced in the market context (including constraints on certain plasticizers and solvent-based systems), these rules keep reformulation, documentation, and testing requirements central to product development and commercialization for graphic film suppliers and converters.

Competitive Landscape

The graphic films market remains moderately concentrated. 3M, Avery Dennison, and ORAFOL utilize global distribution, extensive R&D, and robust patent portfolios to maintain their market share. Mid-tier and regional firms compete on cost or niche capabilities, such as specialty textures or eco-labels.

Acquisition trails, such as ORAFOL’s purchases of Reflexite, Rowland, Kay Automotive Graphics, and NUPRO, illustrate capability stacking to fill portfolio gaps.[3]ORAFOL Europe GmbH, “Strategic Growth Through Acquisitions,” orafol.com Technology alliances with printer OEMs ensure substrate-ink compatibility that lowers field failures and brand recalls. Capacity investments cluster near demand centers to hedge freight and geopolitical risks.

Meanwhile, sustainability keys open new revenue corridors: antimicrobial coatings for healthcare settings and smart glazing for electrochromic façades. The race to deliver PVC-free or solvent-free solutions without cost penalties will shape future competitive order in the graphic films market.

Graphic Film Industry Leaders

3M Company

Avery Dennison Corporation

CCL Industries Inc.

Spandex AG

Hexis S.A.S.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A visible whitespace is emerging for PVC-free and recycling-stream-friendly graphic film constructions as brand owners and specifiers respond to packaging circularity rules and green-building scoring systems that penalize higher-impact polymers and solvent-heavy systems. Product activity in 2026 reinforces this direction: Cosmo Films introduced Green Graphic Films positioned as PVC-free options for indoor and outdoor retail branding and signage, and Avery Dennison broadened its CleanFlake-focused portfolio with constructions designed to improve compatibility with established recycling streams (including cavitated white BOPP and optimized rPET liners). For converters, these moves add pathways to align graphics performance with sustainability requirements.

Differentiation is also being pursued through digital-ready films and material efficiency. Digital printing already holds a meaningful installed base in this market (36.15% share in 2025), and converter interest in digital workflows that reduce steps and waste aligns with demand for UV-inkjet-compatible, lower-VOC solutions described in the report context. In parallel, material-lightweighting avenues are progressing across the film ecosystem, including NanoXplore and Techmer PM commercializing a graphene masterbatch platform aimed at higher mechanical strength and thickness reduction. These developments can translate into cost and performance levers for specialty film structures where stiffness, durability, and down-gauging are key.

Recent Industry Developments

- May 2026: Cosmo Films introduced Green Graphic Films for PVC-free indoor and outdoor retail, branding, and signage applications at InStore Asia 2026. The launch highlights the shift toward alternative polymer choices and sustainability-positioned portfolios as specifiers push for lower-impact materials across promotional and architectural graphics.

- January 2025: Polyplex commenced operations at its new USD 100 million PET film plant in Alabama, expanding North American PET substrate availability. This investment supports shorter lead times and supply diversification for converters seeking recyclable PET-based alternatives amid tightening requirements on PVC and solvent-related chemistries.

- September 2024: 3M outlined timelines for phasing out PFAS chemistries, affecting certain high-performance graphic film lines that rely on durable functional coatings. The transition pressure accelerates reformulation and qualification cycles across suppliers and can shift demand toward PFAS-free topcoat technologies while maintaining durability targets for wraps and long-life signage.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the graphic film market covers plastic film materials designed to carry printed graphics or visual communication, used on surfaces such as vehicles, windows, walls, equipment, and signboards, across end users like advertising, construction, and automotive.

Scope exclusions: We exclude inks, printers, laminating equipment, and installation labor because these are services or supplies that sit outside the film material value.

Segmentation Overview

- By Film Type

- Opaque Film

- Transparent Film

- Translucent Film

- Reflective Film

- By Polymer

- Polyvinyl Chloride (PVC)

- Polypropylene (PP)

- Polyethylene (PE)

- Polyethylene Terephthalate (PET)

- Other Polymers

- By Printing Technology

- Digital

- Flexography

- Offset Lithography

- Rotogravure

- Screen Printing

- By End-User Industry

- Automotive

- Advertising and Promotion Agencies

- Building and Construction

- Institutional and Public Infrastructure

- Other End-User Industries

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Chile

- Rest of South America

- Europe

- United Kingdom

- Germany

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research starts by building the demand context for printed and applied films, so the model has a realistic base before assumptions are added. We rely on public sources such as US Census manufacturing and trade tables, UN Comtrade trade statistics, Eurostat industrial production and trade series, and national statistical offices in major consuming countries for plastics and sign-related activity.

We also use association and standards references, such as sign and advertising bodies, packaging and plastics associations, and regulatory agencies that publish materials guidance (for example, chemicals compliance and recycling-related rules). Company annual reports, investor presentations, and press releases are read to understand product positioning, capacity moves, and pricing commentary. Where needed, paid subscriptions are used only for company financials and intelligence, patent databases, and shipment-level import/export datasets to cross-check volume direction. These examples are not exhaustive, and many other public sources were also consulted for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work is used to pressure-test what desk research cannot settle cleanly, such as average selling price movement by film type, typical waste and yield in converting, and the split between short-run promotional graphics and longer-life architectural or automotive uses. We speak with film producers, converters and printers, distributors, and large buying organizations, and we balance inputs across APAC, EMEA, and the Americas so regional differences in signage demand and vehicle wrap adoption are captured rather than averaged out.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 33% | CXOs: 12% | APAC: 44% |

| Mid tier: 47% | Functional/Unit leaders: 41% | EMEA: 37% |

| Smaller Players: 20% | Managers: 47% | Americas: 19% |

Market-Sizing & Forecasting

Sizing is built using a top-down approach where plastics film demand signals, signage and advertising activity indicators, and regional production and trade data are used to reconstruct the addressable pool for graphic films, then filtered with application penetration assumptions. To keep the totals grounded, we corroborate the outcome with selective bottom-up checks such as sampled supplier revenue splits, distributor channel checks, and a volume-times-average-price sanity test for key film categories.

Key inputs used in the model include the share of PVC, PP, and PE within graphic applications, printed area growth tied to outdoor advertising spend direction, vehicle parc and wrap adoption trends, construction and renovation cycles that drive architectural graphics, and average price progression by film type (opaque, transparent, translucent, reflective). When a country-level data gap appears, we proxy using trade-linked apparent consumption, nearby market ratios, and interview-based correction factors, and then we re-check the assumptions for consistency.

Forecasts are produced using scenario analysis supported by short time-series smoothing on the most stable indicators, followed by expert validation on the likely range of changes in pricing and adoption. Where volatility is higher, we keep a conservative and an accelerated case, then narrow the range after follow-up calls with industry participants.

Data Validation & Update Cycle

Validation is handled through repeated cross-checks so the final number matches multiple independent signals, not just one dataset. Our analysts compare model outputs against import and export direction, capacity announcements, and reported sales commentary, then review any sharp year-to-year jumps to confirm whether a real market event explains them.

If large variances show up across regions or film types, interviews are revisited and assumptions are adjusted only after the reason is documented. A second analyst review is done before sign-off, and the report is refreshed annually, with interim updates triggered by material events like major plant expansions, regulatory shifts affecting PVC usage, or sudden price changes in key resin inputs. Before delivery, a fresh pass is completed so clients receive the latest updated view.

Mordor Intelligence's Graphic Film Market Estimate Compared With Other Published Estimates

It is normal to see different market sizes for graphic film because each publisher draws the line differently on what counts as a graphic film and how prices are averaged across short-life and durable applications. Differences also come from the year chosen as the base, how trade and production data are converted into consumption, and how quickly the model is refreshed after cost swings.

Some published figures appear to fold in adjacent printed film categories and wider print-related materials, which can lift totals even if end uses overlap. In our split, Mordor Intelligence counts graphic films only when the product is sold as a printable or graphic-ready film used for visual communication, and it keeps out inks, equipment, and installation services so the value reflects the film material market more cleanly.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 34.96 B (2026) | |

| Global Consultancy A | USD 34.80 B (2025) | Uses a different base year and may apply a broader application roll-up that blends window graphics, safety signage films, and decorative uses without the same price normalization across film types. |

| Industry Publisher B | USD 35.08 B (2025) | Reports a 2025 base that can be influenced by spot pricing and conversion assumptions, and the scope description is less explicit on excluding non-film elements like installation and related print supplies. |

Taken together, the spread is mainly explained by year alignment and how closely the scope is kept to film material revenue instead of a wider print ecosystem. By tying the model to repeatable signals like trade direction, adoption in wraps and signage, and film-type price ladders, we can show each adjustment step and keep the final number practical to audit.

Key Questions Answered in the Report

How large is the graphic films market in 2026?

It reached USD 34.96 billion and is forecast to register a 5.03% CAGR to 2031 over 2026-2031.

Which polymer type leads current demand?

PVC accounts for 62.98% share due to cost and processing advantages, but PET is gaining fastest.

Why is Asia-Pacific dominant?

The region mixes vast polymer production scale with heavy infrastructure investment, securing 45.30% share in 2025.

What technology is growing quickest?

UV-inkjet digital printing is expanding at 7.58% annually thanks to swift curing and low emissions.

Which end-use segment is accelerating fastest?

Building and construction applications are rising at a 6.6% CAGR as projects integrate durable and aesthetic films.

Page last updated on: