Camping Tent Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 5.98 Billion |

| Market Size (2031) | USD 8.14 Billion |

| Growth Rate (2026 - 2031) | 6.38% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Camping Tent Market Analysis by Mordor Intelligence

The camping tent market size was valued at USD 5.62 billion in 2025 and estimated to grow from USD 5.98 billion in 2026 to reach USD 8.14 billion by 2031, at a CAGR of 6.38% during the forecast period (2026-2031). Rising participation in outdoor recreation after 2024 and the steady conversion of casual participants into repeat campers are supporting a broad-based expansion of entry-level and mid-tier tents, while premium technical designs continue to gain traction among experienced users who value durability and advanced materials. Regulatory clarity on flammability standards in North America is reducing compliance friction for brands that align construction and labeling with updated test methods, helping streamline new product introductions across channels. Material innovation remains a defining theme as tent makers shift toward PFAS-free waterproofing, solution-dyed textiles, and recycled yarns that meet safety standards without chemical treatments, which supports both performance and environmental goals. Retail remains omnichannel, where in-store evaluation coexists with product discovery through brand-owned sites and social communities, and that blend is shaping how the camping tent market communicates product claims and user education in 2026.

Key Report Takeaways

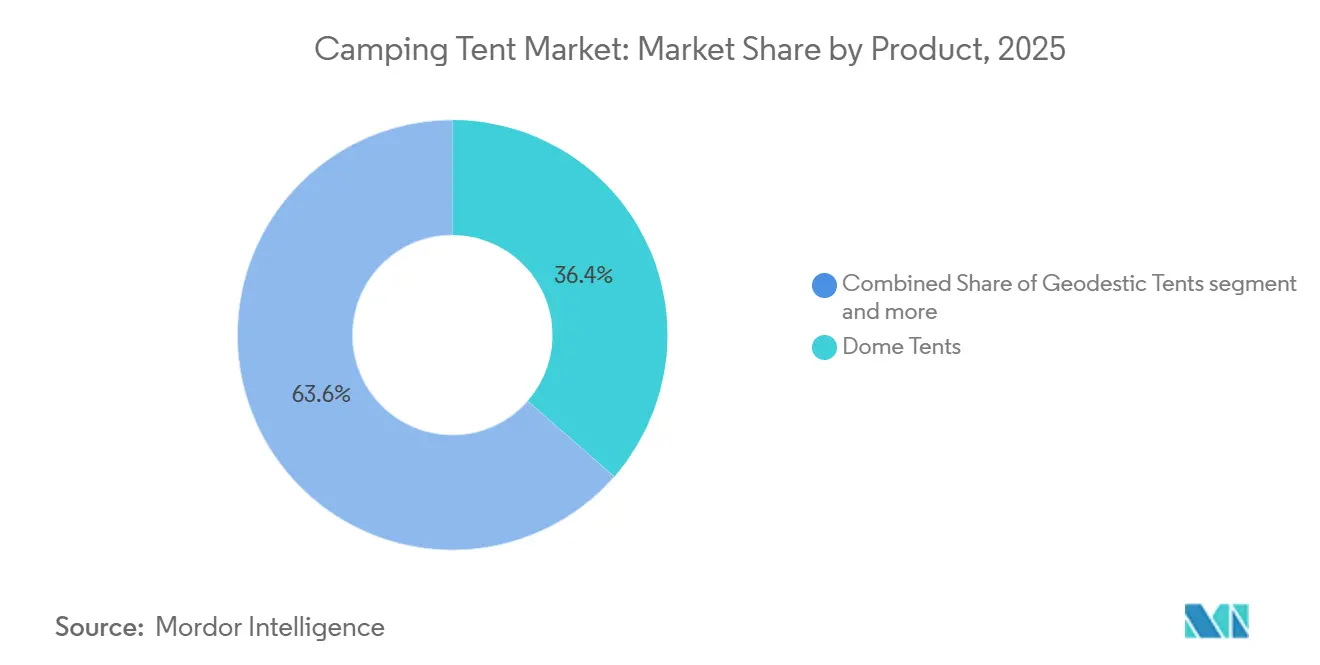

- By product type, Dome tents led with 36.43% revenue share in 2025, while geodesic tents are forecast to expand at an 8.21% CAGR through 2031.

- By capacity, Below 4-Person tents accounted for 65.58% of the market share in 2025, while 4-Person and Above configurations are projected to grow at a 7.36% CAGR through 2031.

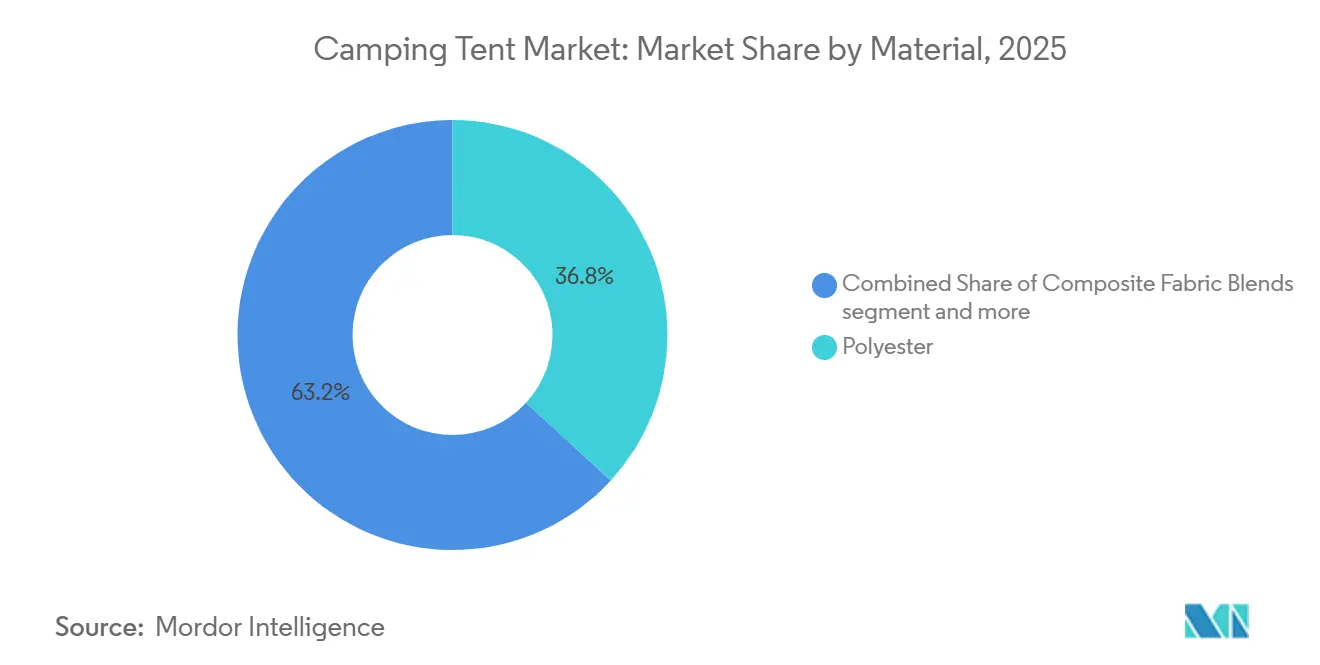

- By material, Polyester held 36.84% share in 2025, while Composite Fabric Blends are projected to advance at a 6.84% CAGR over 2026-2031.

- By distribution channel, Offline retail stores captured 69.57% share in 2025, while online retail stores are expected to grow at an 8.45% CAGR to 2031.

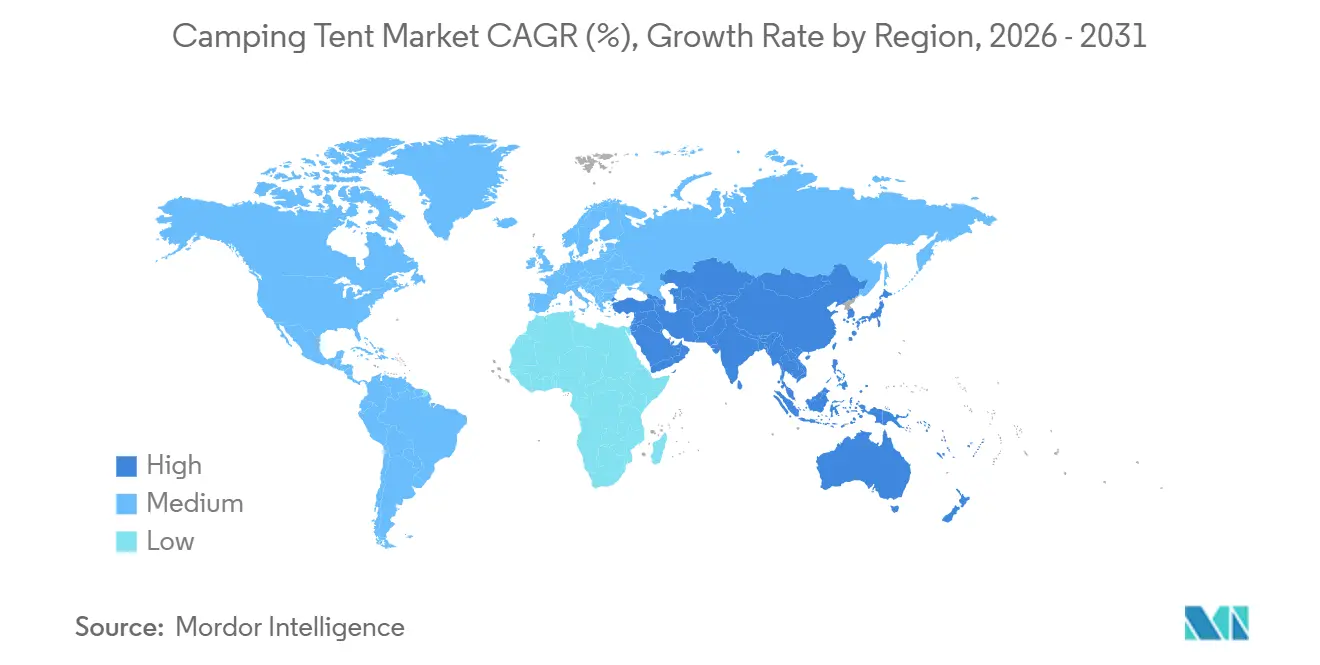

- By geography, North America accounted for a 34.46% share in 2025, while Asia-Pacific is projected to be the fastest-growing region at a 7.73% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Camping Tent Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Adventure tourism and outdoor leisure growth | +1.8% | Global with stronger gains in North America and Asia-Pacific | Medium term (2-4 years) |

| Lightweight and easy-to-install designs | +1.4% | North America and Europe, rising among urban weekend users in APAC | Short term (≤ 2 years) |

| Higher disposable income supporting recreation | +1.2% | Asia-Pacific, Middle East, Latin America | Long term (≥ 4 years) |

| Social media and outdoor influencers | +0.9% | Global urban cohorts in Gen Z and Millennials | Short term (≤ 2 years) |

| Advanced weatherproof and all-season fabrics | +0.7% | North America, Northern Europe, high-altitude destinations | Medium term (2-4 years) |

| Expansion of e-commerce access to outdoor gear | +0.4% | Asia-Pacific and North America with spillover to Middle East and Africa | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising popularity of adventure tourism and outdoor leisure activities

Outdoor participation in the United States expanded in 2024, with 181.1 million participants aged six and older, and camping among the top gateway activities, which sustained demand for entry tents and crossover all-season models in 2026, according to the Outdoor Foundation Association[1]Source: Outdoor Foundation, “2025 Outdoor Participation Trends Report,” Outdoor Foundation, outdoorfoundation.org. Growth within youth and diverse communities widened the pool of prospective owners, supporting a larger addressable pool for beginner-friendly formats and education-led retailing that clarifies setup, fit, and care. Brands that reduce setup friction or offer clear sizing claims convert casual interest into ownership as users migrate from rentals or shared gear to first purchases that balance weight, space, and weather protection. At the same time, a visible wave of product introductions in 2025 and 2026 reset performance expectations by discarding PFAS treatments and moving toward solution-dyed and recycled textiles that hold up across seasons while easing compliance in North America. This broadening of the user base favors scalable designs, so the camping tent market is seeing continued interest in easy-pitch dome formats for mainstream buyers and expedition-grade geodesic formats for experienced users who want to keep using their gear in harsh conditions without sacrificing long-term durability.

Rising demand for lightweight and easy-to-install tent designs

Ultralight backpacking tents continued to gain momentum during 2025–2026 as manufacturers prioritized sub-1 kg shelters without compromising durability or weather protection. Innovations such NEMO's Dragonfly OSMO, updated for 2025-2026, leverages proprietary 100% recycled composite yarns delivering 4x longer water repellency, 3x less stretch when wet, and 20% greater strength versus similar fabrics, meeting flame-retardancy standards without added chemicals highlight the use of recycled high-performance fabrics, enhanced waterproofing, reduced fabric stretch, and chemical-free flame-retardant compliance, while also improving condensation control and overall strength[2]Source: NEMO Equipment, “Dragonfly OSMO,” NEMO Equipment, nemoequipment.com . At the same time, inflatable airframe tents from brands including Heimplanet, Vango, and Zempire have simplified setup processes, with some models pitching in under five minutes, increasing their appeal among first-time and family campers seeking convenience. Regulatory changes, including Canada’s adoption of the CAN/CGSB-182.1-2020 standard in November 2024, are further supporting innovation by reducing reliance on flame-retardant chemicals and lowering material costs for compliant manufacturers.

Increasing disposable income supporting recreational travel spending

Rising disposable incomes across emerging markets continue to support growth in camping gear adoption, particularly in the Asia-Pacific region, where expanding middle-class populations are driving demand for outdoor equipment. Naturehike, a Ningbo-based outdoor brand, illustrates this trend, with annual sales surpassing RMB 1.5 billion (USD 200 million) by 2026 and distribution across 72 countries. The company has gained strong traction in Southeast Asia, where the outdoor sports market exceeds USD 300 million and is expanding at an annual growth rate of over 100%. Its mid-range pricing strategy, with tents typically priced between USD 100 and 200, positions the brand between premium Western manufacturers and low-cost entry-level products, appealing to aspirational consumers in markets such as Vietnam, Thailand, the Philippines, and Indonesia. Similar patterns are emerging in Latin America, where affordable camping options are broadening participation beyond higher-income consumers; for example, Argentina’s Tierra del Fuego National Park recorded 800-1,200 daily visitors during the January 2026 peak season, with camping fees at Lago Roca remaining accessible at ARS 3,000 (USD 4-5) per night. In North America, consumer spending on outdoor recreation has remained resilient despite inflationary pressures, supported by a growing preference for experience-oriented purchases. Demand has strengthened across multiple income and education groups, while premium tent categories continue to benefit from consumers upgrading to feature-rich products incorporating multi-room layouts, UV-protection coatings, and integrated lighting systems such as Big Agnes’s mtnGLO technology.

Increasing influence of social media and outdoor lifestyle influencers

Short-form video and community content now play a visible role in how shoppers learn about new tents, what fabrics and coatings mean in real use, and which setup methods they can trust in bad weather. Brands and retailers with strong educational content convert better because users seek specific answers around interior space, waterproof ratings, and condensation management before buying a tent online. This has pushed the camping tent market to invest in owned channels that blend technical walk-throughs with real-world clips from parks and campgrounds, which helps bridge the gap between in-store demos and online discovery. Companies that use their own ambassadors and product specialists to demonstrate proper pitching and care help reduce misuse, lower returns, and build a base of repeat owners. These tactics help newer participants feel confident enough to buy online and arrive at the campsite prepared, which sustains satisfaction and keeps participation trending upward for 2026.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Seasonal Nature of Camping Limiting Year-Round Product Demand | -0.9% | Temperate climates: North America, Europe, parts of Asia-Pacific | Long term (≥ 4 years) |

| Counterfeit and Low-Quality Products Impacting Brand Reputation | -0.5% | Asia-Pacific (manufacturing hubs), online marketplaces globally | Medium term (2-4 years) |

| Volatility in Raw Material Prices Affecting Tent Manufacturing Costs | -0.7% | Global, with acute pressure in import-dependent markets (Middle East, Latin America) | Short term (≤ 2 years) |

| Stringent Regulations on Fire-Retardant Chemicals Increasing Compliance Costs | -0.3% | North America, Europe, Canada | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Counterfeit and low-quality products impacting brand reputation

Counterfeit camping tents sold through e-commerce platforms are increasingly affecting brand reputation and product safety. Tentsile reported an increase in complaints about fake products made with low-quality fabrics, substandard carabiners, and misleading sizing claims, while ToyouTent issued an authenticity alert in February 2026 after fraudulent websites copied internal production visuals to mislead buyers. Product quality concerns are also growing: in November 2024, China’s Liaoning Provincial Market Supervision Administration tested 15 batches of outdoor tents and found none compliant, with failures in tear strength, UV protection, waterproofing, and flame-retardant standards. Similarly, the UK Office for Product Safety and Standards detained a two-person tent in 2021 after its polyester fabric failed flammability requirements under the General Product Safety Regulations 2005. These issues are increasing pressure on legitimate manufacturers that invest in ISO 5912 testing and certifications such as Bluesign and OEKO-TEX. Naturehike responded by adopting a “trademark first” strategy after surpassing RMB 1.5 billion in sales, registering intellectual property ahead of market entry in Southeast Asia, and segmenting supply chains to reduce component leakage. Regulatory measures are also tightening, with the EU’s 2024 General Product Safety Regulation (GPSR) requiring manufacturers to maintain technical documentation and product traceability, raising compliance standards across the industry.

Stringent regulations on fire-retardant chemicals increasing compliance costs

Canada’s Tents Regulations (SOR/2024-217), effective November 2024, mandate CAN/CGSB-182.1-2020 compliance, which uses balanced mass-loss testing to reduce reliance on flame-retardant chemicals and address health concerns linked to PBDEs and TDCPP, reported at levels 29 times higher on hands after handling treated tents and detected in tent air samples, according to the Government of Canada. The International Association of Fire Fighters (IAFF) notes that firefighting is classified as carcinogenic to humans by IARC (2022), and that flame-retardant exposure contributes to occupational cancer risk, supporting a shift toward smolder-test alternatives. In comparison, ASTM F3431-21 in the U.S. references CGSB standards but applies only to tents used with camping appliances, offering narrower consumer coverage[3]Source: ASTM International, “F3431-21 Standard Specification for Determining Flammability of Materials for Recreational Camping Tents,” ASTM, astm.org . Compliance costs range from USD 1,200-2,500 per model for CPAI-84 testing and USD 500-5,000 for ASTM F3431/CAN/CGSB-182.1 testing, depending on fabric complexity, while Canada’s transition framework allows adjustments until November 2026 with 180-day manufacturer and 365-day seller compliance windows. Additional layers, such as California’s Proposition 65 and EU REACH/EN 5911 standards, further increase regulatory complexity and chemical restrictions, while innovations like NEMO’s OSMO and Big Agnes’s HyperBead fabrics achieve flame-retardancy without added chemicals, reducing recurring treatment costs and meeting ISO 5912 and ASTM F3431 performance standards.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Geodesic Designs Propel Technical Migration

Dome tents captured 36.43% of the camping tent market share in 2025, supported by balanced interior space, familiar setup, and a wide range of price points for casual buyers and weekend users. Growth in geodesic tents is forecast at 8.21% CAGR through 2031, reflecting greater interest in expedition-grade stability that has moved into lighter formats and more accessible price tiers for advanced consumers. New models emphasize structural strength without heavy materials, encouraging users to upgrade as they seek better wind performance and snow-load handling for shoulder seasons and higher elevations. Recycled and solution-dyed fabrics now appear in technical lines alongside established designs, and that pairing signals to buyers that environmental and safety standards can coexist with field durability. Brands that present clear hydrostatic head ratings and pole specifications help new owners match tents to climate and terrain, which supports satisfaction and lowers returns.

The projected rise of geodesic designs is reshaping how the camping tent market communicates value to experienced users who spend more nights outdoors and want confidence when forecasts turn. Retailers and brand sites that compare dome and geodesic architectures educate users on when to trade weight for strength and when marginal ounces are worth additional stability in exposed sites. Multi-vestibule and larger-volume floor plans continue to appear in the upper end of this category as buyers ask for both storm-worthiness and habitability that feels comfortable during longer trips. Terra Nova’s geodesic entries illustrate how established technical brands are reconciling weight, recycled content, and waterproof ratings in a single build that appeals to advanced hikers and mountaineers. Across the category, easy-to-follow pitch steps, color cues, and simplified guy-out systems are now standard expectations, aligning technical adoption with usability that limits setup errors for new owners.

By Capacity: Family Configurations Accelerate Amid Multi-Generational Trends

Below 4-Person tents held the largest share at 65.58% in 2025, mirroring the needs of solo backpackers, couples, and small groups who value weight savings and compact packed size. Families and multi-generational groups are influencing the top end of the capacity range, with demand for 4-person and larger tents that offer greater live-in comfort over several consecutive nights. The expected 7.36% CAGR for larger capacities reflects how repeat participation leads buyers toward room dividers, taller peak heights, and vestibules that ease daily living at crowded campgrounds, and those features now arrive in packages that remain manageable to transport. Retailers that stage full-size family models allow shoppers to try standing height, cots, and storage arrangements, helping align purchases with planned use and reducing first-trip surprises. This matching of format to need supports lasting satisfaction and fuels repeat purchases when the same household later adds a dedicated backpacking shelter for adult-only trips.

Family buyers also respond to clear messaging around fabric safety, waterproof claims, and ventilation, and they expect to see those assurances across online product pages and in-store displays. Transparent specs narrow the field and make brand comparisons easier as parents seek predictable comfort for longer weekends or holiday weeks on the road. The camping tent market reflects this by presenting capacity, floor plans, and weather ratings in consistent templates so that larger models are easier to grasp when buyers weigh setup time and campsite space. Easy-pitch features and guidance around ground cloths and guyline placement serve as lightweight education that reduces setup stress at arrival and improves the first-night experience. As a result, the larger-capacity segment benefits from clear sizing guidance and repeatable setup, and that clarity underpins its faster growth profile through the forecast.

By Material: Composite Blends Gain as Recycled Fibers Mainstream

Polyester led with a 36.84% share in 2025, helped by its UV resilience and dimensional stability, which appeal to mainstream users who camp in sunny regions and want fabric that resists long-term degradation. Composite fabric blends are expected to grow at a 6.84% CAGR over 2026-2031, driven by combined benefits that include lower stretch when wet, higher tear strength, and credible waterproof performance without PFAS treatments. The camping tent market has pivoted toward solution-dyed and recycled yarn construction, where environmental benefits align with stable color and fewer finishing steps, thereby improving quality consistency at scale. Companies now explain how fabric recipes relate to test methods, so customers can read hydrostatic head, tear strength, and flammability compliance with confidence across multiple product families. That clarity elevates material choice from a niche detail to a purchase driver, especially among buyers who camp often and want textiles that remain strong over repeated seasons.

Within this shift, brands are emphasizing both comfort and longevity rather than weight reduction alone, keeping polyester relevant in family and basecamp formats while blends and advanced nylon constructions compete in the ultralight tier. Clear care instructions around UV exposure, drying, and storage are also more available at the point of sale, which helps owners preserve fabric integrity across years of use. As regulations standardize in North America, manufacturers that avoid legacy chemical treatments and still meet flammability and weatherproof standards can point to both health and performance benefits. The resulting material landscape makes it easier to ladder up through price points with real performance steps as shoppers mature from occasional use to more frequent travel under mixed weather. This progression supports durable demand across the category and positions composite blends to capture more volume as costs fall with scale.

By Distribution Channel: Omnichannel Strategies Reconcile Tactile and Digital Discovery

Offline retail stores accounted for 69.57% of the market share in 2025, since tents are a tactile purchase and many shoppers want to step inside to gauge space, ventilation, and headroom before they commit. Store staff play a role in education by showing how to pitch a tent, address condensation, and stake out vestibules correctly, which reduces user error and avoidable returns. The camping tent market continues to blend this tactile validation with online research and long-form product education that shoppers digest at home. Retailers that synchronize messaging across web pages, shelf talkers, and hangtags improve trust because buyers see the same claims and ratings no matter which channel they use. That alignment is reinforced as more brands publish detailed product pages, setup videos, and care instructions that echo what store staff recommend in person, reducing friction when moving between channels.

Online retail stores are projected to grow at an 8.45% CAGR through 2031 as more shoppers become comfortable buying higher-priced tents digitally once they can verify geometry, floor size, and pole materials. Clear taxonomy, filters by capacity and seasonality, and robust warranty information give users enough confidence to click buy after watching setup content and reading fit guidance. Brands with both physical displays and strong online content can serve the widest range of scenarios, from first-timers who start in store to returning buyers who reorder a known format online. This combination ensures a balanced channel strategy that supports shoppers throughout the research and ownership lifecycle, which in turn sustains repeat sales and upgrades over time.

Geography Analysis

North America accounted for 34.46% of the camping tent market in 2025, supported by a large and diverse participant base that continued to expand in 2024 and stabilized above pre-pandemic levels in 2026. Product adoption reflects both frequent local trips and seasonal destination travel, which pushes retailers to stock a range of capacities and weather ratings that match regional climates and varied terrain. Updated flammability standards and clearer labeling practices are streamlining product introductions in the United States and Canada, and this consistency helps omnichannel retailers maintain unified staff training and consistent education for shoppers. Large-format retailers with vertical integration use displays and education to drive confident first purchases, serving the influx of new participants who prioritize simplicity and value. Technical brands continue to thrive by offering PFAS-free fabric performance and reliable weatherproofing, which resonate with buyers who camp year-round in Northern states and Western high country.

Asia-Pacific is projected to be the fastest-growing region at 7.73% CAGR through 2031, supported by rising participation in urban and peri-urban markets and quality-focused product introductions that balance price, weight, and durability. As retailers and brands expand digital guides and setup content in local languages, barriers to entry fall for first-time owners who want straightforward pitch steps and clear fabric claims. The camping tent market sees strong crossover interest in sub-4 person ultralight shelters for hikers along with 4 to 6 person family configurations for drive-to campgrounds, and both ends of the range benefit from advances in composite fabrics and solution-dyed construction. Manufacturers with consistent labeling and regional compliance documentation can expand faster because their models meet expectations and reduce surprises at delivery. Education and clarity around waterproof ratings, pole materials, and ventilation choices give buyers enough confidence to adopt tents suited to the region’s monsoon and summer heat patterns.

Europe maintains steady growth with a mature base of frequent users who value longevity, easy care, and credible environmental improvements in materials. Technical brands in the region continue to publish detailed handbooks and yearbooks that educate buyers on fabric selection, construction, and field care, and this tradition supports informed upgrades to newer tent generations. The EU’s evolving product safety and chemical frameworks continue to shape material choices for camping tents, and brands that meet strict requirements while avoiding legacy chemicals can strengthen their quality signal to retail partners and consumers. In this context, composite blends and solution-dyed options help deliver the UV stability, tear strength, and waterproofing that European buyers demand without complex finishing steps. The camping tent market remains diversified across geographies within Europe, with coastal and alpine use cases both sustaining interest in formats that can handle wind, rain, and cooler shoulder seasons.

Competitive Landscape

The camping tent market remains moderately fragmented in 2026, with a long tail of specialty and direct-to-consumer brands competing on innovation, sustainability, and channel mix. Portfolio decisions by legacy brands illustrate how companies are refocusing on core segments, and changes in 2024 set the stage for more targeted investment into high-utility formats and premium builds that can defend margins against input cost pressure. Vertical integration provides an efficiency edge at scale, since brands that design and retail in-house can align product roadmaps with merchandising and education, thereby shortening learning curves for new campers and stabilizing pricing. Retailers with large footprints continue to leverage rapid pitch innovations and PFAS-free materials as selling points, tying in-store demos to online education so users are confident about setup and care from day one.

On the innovation front, PFAS-free waterproofing and recycled, solution-dyed textiles have moved from early adopters into wider availability in 2025 and 2026, and that shift aligns environmental, regulatory, and performance incentives for premium ranges. Brands with clear technical documentation and third-party compliance references can scale across North America and Europe with fewer frictions, which helps focus engineering resources on durability and ease-of-use improvements. Premium makers are also publishing detailed product pages and long-form educational content to explain tradeoffs between weight and weatherproofing, which raises buyer confidence when purchasing at higher price points. The result is a more informed shopper who can choose models that serve specific trips, from lightweight overnighters to multi-day front-country stays, without feeling forced into one compromise across all use cases.

Sustainability and safety are now front-and-center differentiators, and company communications showcase how new fabric systems meet or exceed flammability and performance standards without legacy chemical finishes. Product launches in 2026 reflect that story, with tents that integrate recycled composites, improved waterproof ratings, and stronger tear resistance while avoiding PFAS, which directly addresses consumer and regulatory expectations. The camping tent market also rewards brands that publish clear care instructions, because correct drying, storage, and periodic maintenance extend product life and reduce complaints that stem from avoidable misuse. In a competitive field where claims look similar on paper, consistent documentation and visible customer support can tip purchase decisions, especially for households that are making their first significant tent investment.

Camping Tent Industry Leaders

Newell Brands (Coleman)

VF Corporation (The North Face)

Decathlon S.A. (Quechua & Forclaz)

Cascade Designs (MSR)

Johnson Outdoors Inc. (Eureka)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Big Agnes introduced the ultralight VST Series featuring recycled 20D HyperBead fabric, achieving 4,000mm waterproofing without PFAS chemicals. The String Ridge VST 1.5 weighs 19 oz and is priced at USD 549.95, targeting fast-moving backpackers and thru-hikers.

- January 2026: MSR launched the Hubba Hubba HD Series for Spring 2026, featuring enhanced weatherproofing with a 3,000mm HH rainfly, a 6,000mm HH bathtub floor, and solution-dyed fabrics that reduce carbon emissions by 80%, available exclusively on MSR's website before US and Canadian retail distribution.

- March 2025: iKamper teamed up with Rivian to introduce camping tents tailored for Rivian trucks. The Skycamp 3.0 Mini boasts a PFAS-free construction, ensuring a premium camping experience with a focus on sustainability and compatibility with Rivian’s electric vehicles.

- March 2025: Nemo unveiled its eco-friendly backpacking tent. The 2025 Dagger Osmo, crafted from solution-dyed, 100% recycled, PFAS- and FRC-free fabrics, offers enhanced livable space without added weight. The tent reflects meticulous attention to detail in its design, catering to environmentally conscious backpackers seeking high performance and sustainability.

Global Camping Tent Market Report Scope

Camping tents are portable shelters designed for outdoor recreational activities, providing temporary accommodation and protection from weather conditions. The camping tent market is segmented by product type, capacity, material, distribution channel, and geography. By product type, the market includes dome tents, tunnel tents, geodesic tents, and other tent types. Based on capacity, the market is categorized into tents with capacities below 4 persons and those with capacities of 4 persons or more. By material, the market covers nylon, polyester, composite fabric blends, and other materials. Based on the distribution channel, the market is segmented into online and offline retail stores. Geographically, the report covers North America, Europe, Asia-Pacific, South America, and the Middle East and Africa, with market sizes and forecasts for each region. Market sizing and forecasts for all segments are calculated based on value (USD).

| Dome Tents |

| Tunnel Tents |

| Geodesic Tents |

| Others |

| Below 4 Person |

| 4-Person and Above |

| Nylon |

| Polyester |

| Composite Fabric blends |

| Others |

| Online Retail stores |

| Offline Retail Stores |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Indonesia | |

| Thailand | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Dome Tents | |

| Tunnel Tents | ||

| Geodesic Tents | ||

| Others | ||

| By Capacity | Below 4 Person | |

| 4-Person and Above | ||

| By Material | Nylon | |

| Polyester | ||

| Composite Fabric blends | ||

| Others | ||

| By Distribution Channel | Online Retail stores | |

| Offline Retail Stores | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Indonesia | ||

| Thailand | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the camping tent market growth outlook through 2031

The camping tent market size is projected to reach USD 8.14 billion by 2031 at a 6.38% CAGR over 2026-2031, supported by rising outdoor participation and scaling PFAS-free, solution-dyed fabrics that improve durability and compliance.

Which region leads demand for camping tents in 2026?

North America leads with a 34.46% share in 2025 on the back of broad participation and strong retail coverage, while Asia-Pacific is projected to be the fastest growing region at 7.73% CAGR through 2031.

Which product types are growing fastest in camping tents?

Geodesic tents are projected to grow the fastest at an 8.21% CAGR as expedition-grade stability migrates into lighter, more accessible builds for experienced users.

What materials define new premium camping tent launches?

Composite blends and solution-dyed, recycled fabrics are defining the premium tier by delivering waterproof ratings without PFAS and improved UV stability, all aligned with updated flammability standards.

Page last updated on: