Biodegradable Packaging Solutions Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

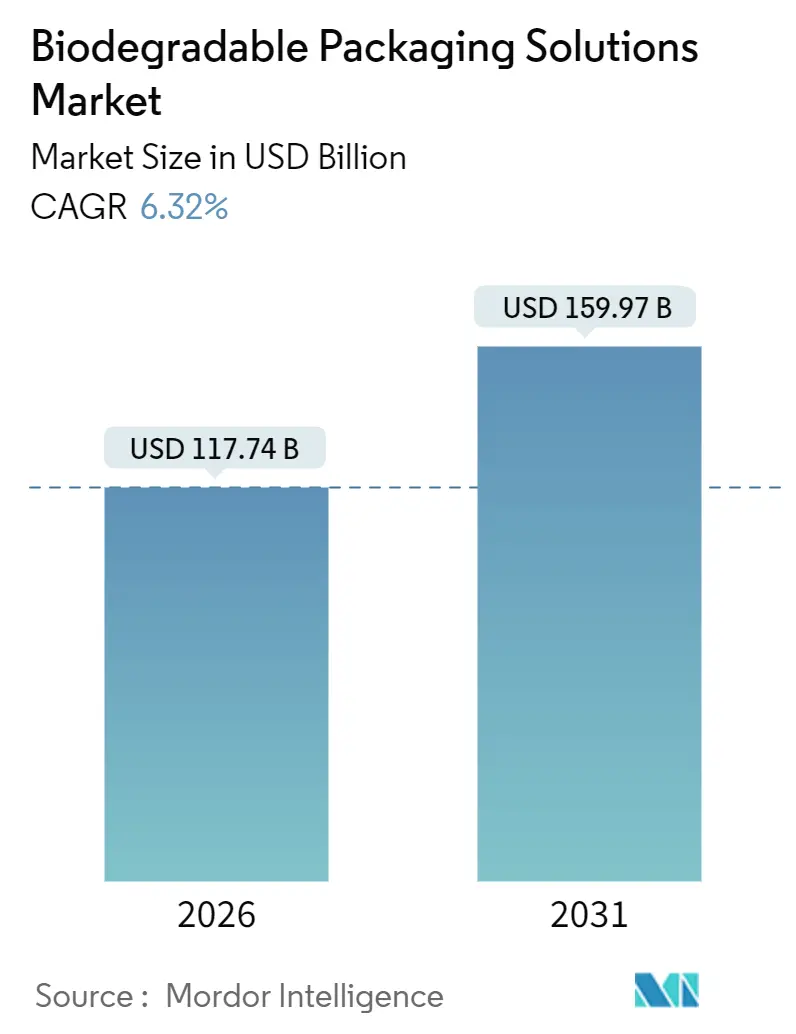

| Market Size (2026) | USD 117.74 Billion |

| Market Size (2031) | USD 159.97 Billion |

| Growth Rate (2026 - 2031) | 6.32% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players.webp) *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Biodegradable Packaging Solutions Market Analysis by Mordor Intelligence

The biodegradable packaging solutions market size reached USD 117.74 billion in 2026 and is projected to advance to USD 159.97 billion by 2031, reflecting a CAGR of 6.32% over 2026-2031 and confirming the sector’s steady upward trajectory. Rising compliance costs for conventional plastics, stronger Extended Producer Responsibility (EPR) laws, and the accelerating pivot by brand owners toward end-of-life design are reinforcing demand across food, beverage, and personal-care value chains. Material innovation, particularly in polylactic acid (PLA) and polyhydroxyalkanoates (PHA), is enhancing process compatibility, while improvements in high-barrier bio-coatings are expanding shelf-stable and refrigerated applications previously reserved for aluminum-laminated or metallized films. Regional composting infrastructure additions, most notably in Europe and key urban areas of North America and the Asia-Pacific region, are alleviating a historic disposal bottleneck. Feedstock volatility remains a headline risk, yet vertically integrated players that control both agricultural inputs and polymerization assets are beginning to neutralize cost swings.

Key Report Takeaways

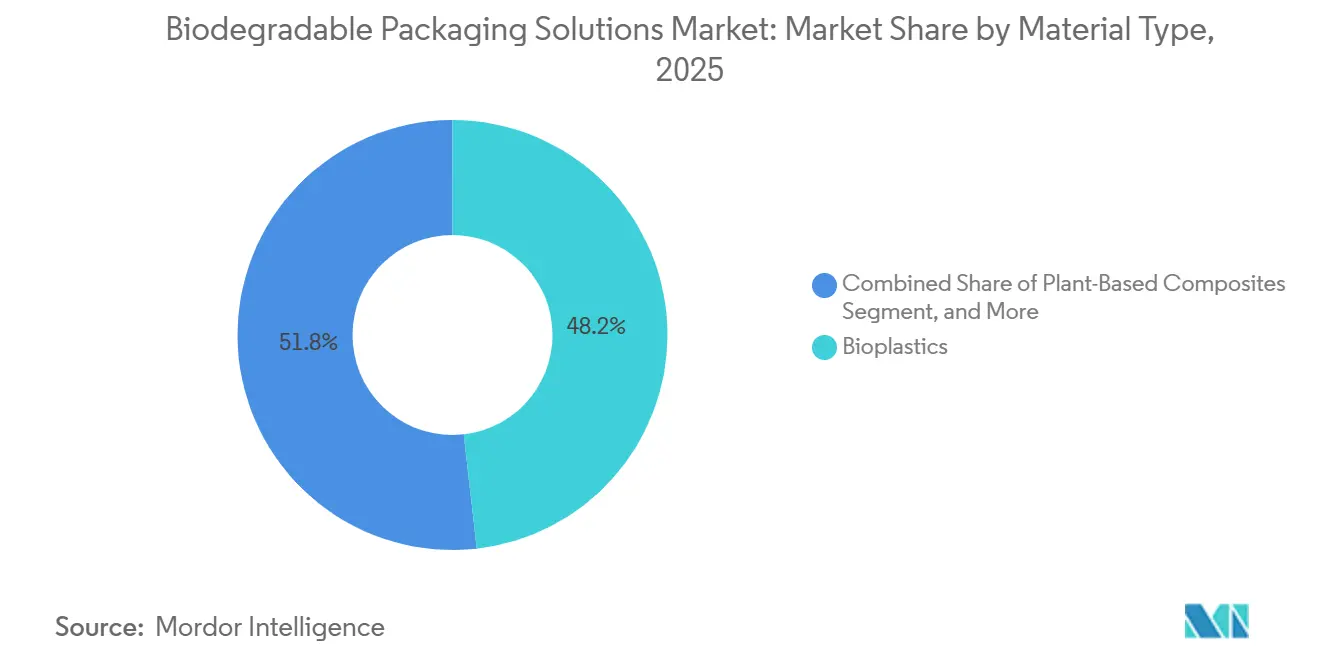

- By material type, bioplastics led with 48.21% revenue share in 2025, while plant-based composites are forecast to expand at 7.42% CAGR through 2031.

- By packaging format, flexible solutions commanded 56.32% of the revenue in 2025, whereas rigid formats are projected to post the fastest CAGR of 7.89% from 2026 to 2031.

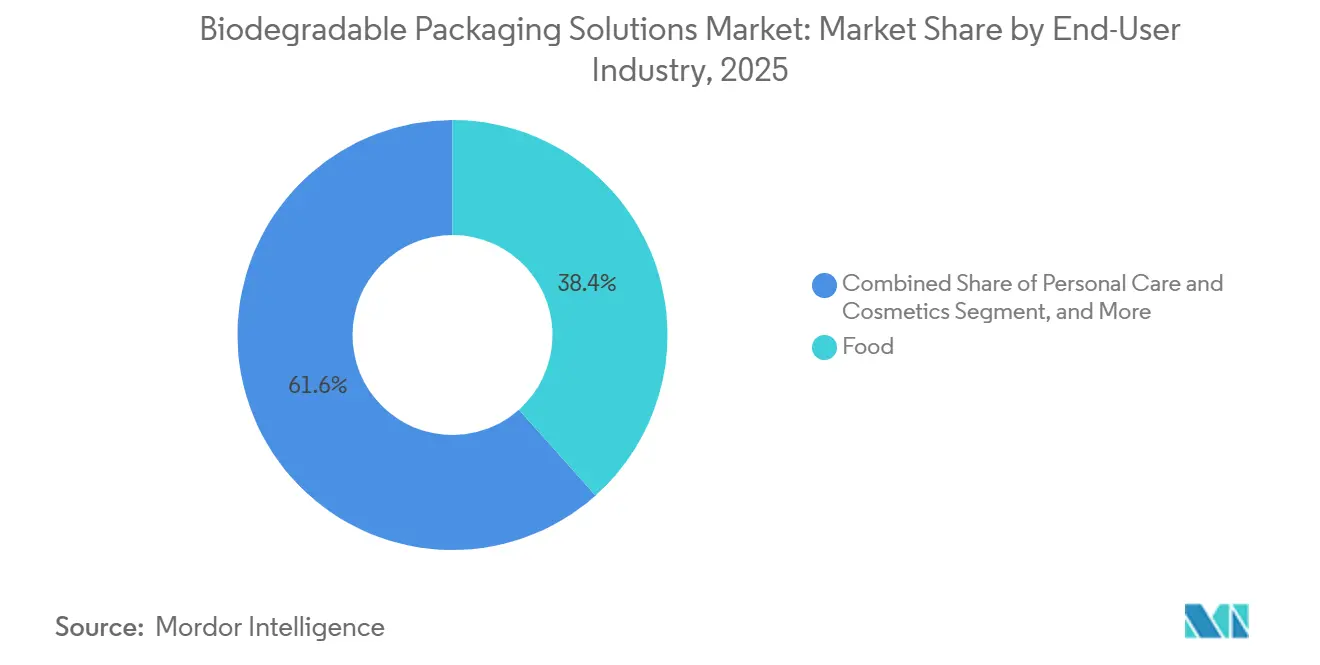

- By end-user industry, food applications accounted for a 38.42% share in 2025, while the personal care and cosmetics sector is expected to grow at an 8.23% CAGR over the forecast period.

- By distribution channel, direct sales secured a 58.31% share in 2025, while indirect channels are expected to register a 7.56% CAGR through 2031.

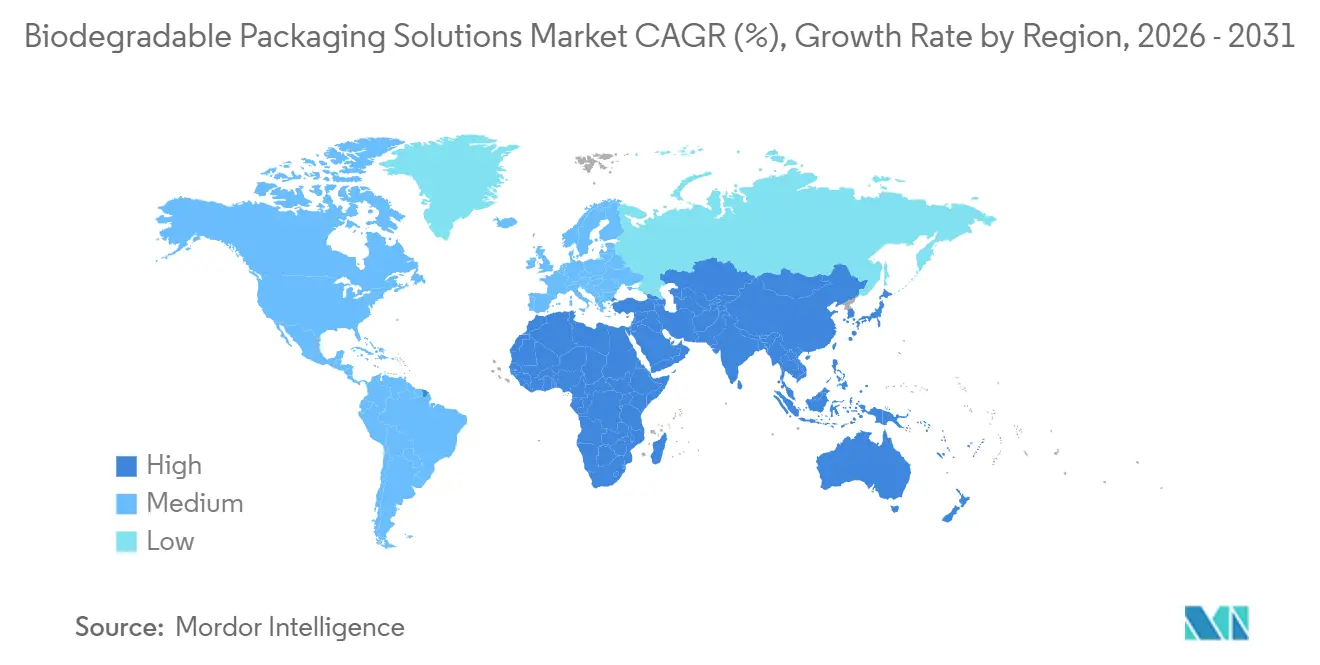

- By geography, Europe held a 40.21% revenue share in 2025, whereas the Asia-Pacific region is anticipated to record the highest 8.85% CAGR from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Biodegradable Packaging Solutions Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Consumer Demand for Circular, Zero-Waste Packaging | +1.2% | Global, highest in North America and Europe | Medium term (2-4 years) |

| Expansion of Composting Infrastructure in Urban Centers | +0.9% | Europe core, North America and Asia-Pacific clusters | Long term (≥ 4 years) |

| Mandatory Extended Producer Responsibility Schemes Globally | +1.5% | Europe, Canada, select U.S. states, emerging Asia-Pacific | Short term (≤ 2 years) |

| Advances in High-Barrier Bio-Based Coatings Unlocking New Applications | +0.8% | Global, R&D in North America and Europe | Medium term (2-4 years) |

| Rapid Capacity Additions for PLA and PHA in Asia-Pacific | +1.1% | Asia-Pacific core, spill-over to Middle East and Africa | Short term (≤ 2 years) |

| Retailers' Private-Label Sustainability Targets Accelerating Adoption | +0.7% | Global, led by North America and Europe retail chains | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing Consumer Demand for Circular, Zero-Waste Packaging

Consumer surveys conducted in 2025 indicate that 67% of shoppers in Europe and North America now consider end-of-life disposal when making purchasing decisions, up from 52% in 2023. Millennials and Gen Z buyers, in particular, switch brands when sustainability claims appear weak, prompting quick-service restaurants to pilot compostable cutlery and clamshells that trimmed plastic waste by 15-20% in trial cities. Converters are responding by bolstering their technical-support teams, which help brands navigate certification processes and on-pack disposal messaging. Retailers use private-label lines as low-risk test beds for new materials, accelerating commercial validation cycles. This behavioral shift underpins stable price premiums that offset higher biopolymer costs and reinforces long-run demand for the biodegradable packaging solutions market.

Expansion of Composting Infrastructure in Urban Centers

The European Union allocated EUR 2.3 billion (USD 2.60 billion) from the 2024-2025 cohesion funds to build anaerobic digestion and windrow facilities across Eastern Europe, targeting a 50% organic waste diversion rate by 2030.[1]European Commission, “Packaging and Packaging Waste Regulation,” EUROPA.EU North American cities, such as San Francisco and Toronto, mandate curbside organics collection, ensuring a steady feedstock for compost operators and validating packaging performance under real-world conditions. China’s Ministry of Housing and Urban-Rural Development is piloting food-waste separation programs in 46 cities, while India’s Smart Cities Mission ties municipal grants to composting performance. Greater infrastructure density lowers reputational risk for brand owners and grants converters near composting hubs a logistics advantage through closed-loop take-back schemes.

Mandatory Extended Producer Responsibility Schemes Globally

The European Packaging and Packaging Waste Regulation, effective January 2025, imposes modulated fees that raise the cost of non-compostable plastics by 8-12%. Canada introduced a harmonized EPR framework in 2024, and four U.S. states enacted similar laws by 2025. These programs directly link material choice to producer levies, making compostable substrates a cost-avoidance strategy. Flexible films and pouches, which have historically been multilayered and non-recyclable, face the heaviest surcharges, prompting a rapid switch to certified compostable alternatives. Compliance schemes such as EN 13432 and ASTM D6400 have become de facto market-entry requirements, pushing converters to secure third-party certifications swiftly.

Advances in High-Barrier Bio-Based Coatings Unlocking New Applications

BASF’s Ecovio PS 1606 achieves oxygen transmission rates below 5 cm³/(m²·day·bar), enabling modified-atmosphere packaging for leafy greens.[2]BASF, “Ecovio PS 1606 Product Information,” BASF.COM NatureWorks’ Ingeo 3D850 withstands 110 °C, clearing hot-fill hurdles for sauces and beverages. These breakthroughs expand the addressable universe beyond dry foods to include refrigerated and shelf-stable categories, which represent roughly two-thirds of total packaging demand. The premium for bio-barrier coatings, currently USD 0.15-0.25 per kg, is still tolerable for premium personal-care and health-food brands. As production scales, cost curves are expected to decline, allowing mid-tier brand adoption by the late 2020s, thereby sustaining momentum in the biodegradable packaging solutions market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile Availability of Agricultural Feedstocks for Biopolymers | -0.8% | Global, acute in North and South America | Short term (≤ 2 years) |

| Inadequate Sorting and Certification Standards Across Regions | -0.6% | Asia-Pacific, Middle East and Africa, Latin America | Medium term (2-4 years) |

| Performance Gaps in Moisture and Oxygen Barrier vs Conventional Plastics | -0.5% | Global | Medium term (2-4 years) |

| Risk of Greenwashing Litigations Increasing Compliance Costs | -0.4% | North America and Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Volatile Availability of Agricultural Feedstocks for Biopolymers

Corn and sugarcane prices fluctuated 18-24% during 2024-2025, with U.S. corn yields down 12% after severe droughts.[3]U.S. Department of Agriculture, “Corn Yield Report 2024,” USDA.GOV Brazilian growers diverted acreage from sugarcane to soybeans, cutting cane output by 7% and tightening supply for PLA producers. Smaller converters lacking hedging capacity struggle to absorb these swings, sometimes delaying brand rollouts or ceding share to larger, vertically integrated rivals such as Total Corbion. Feedstock price instability can dampen substitution momentum if compostable formats exceed brand owners’ cost ceilings, potentially moderating near-term expansion of the biodegradable packaging solutions market.

Inadequate Sorting and Certification Standards Across Regions

Disparate compostability criteria, including EN 13432 in Europe, ASTM D6400 in the United States, and GreenPla in Japan, force multinational brands to maintain separate SKUs or limit geographic reach. Emerging markets often lack recognized certification bodies, creating space for unverified claims that erode consumer confidence. The Biodegradable Products Institute reported a 22% year-over-year increase in non-compliant packages submitted for testing in 2024. Waste processors also face contamination risks when uncertified films mix with mechanical-recycling streams. Without accelerated international harmonization, the resulting complexity will continue to restrain the biodegradable packaging solutions market through the mid-2020s.

Segment Analysis

By Material Type: Bioplastics Anchor Share, Plant Composites Surge

Bioplastics retained a 48.21% share of the biodegradable packaging solutions market size in 2025, largely due to PLA’s compatibility with existing extrusion and thermoforming assets, which minimizes capital outlay during the transition. Starch-based polymers occupy low-performance niches such as loose-fill and agricultural mulch, while cellulose derivatives satisfy premium personal-care labels that demand transparency and printability. PHA fetches a price premium for marine biodegradability, appealing to coastal hospitality and seafood chains. PBS grades offer superior heat resistance, unlocking shelf-stable sauces and ready meals.

Plant-based composites, such as mushroom mycelium, seaweed films, and bagasse fibers, are forecast to grow at a 7.42% CAGR through 2031, the fastest among materials, as luxury electronics and cosmetics adopters seek texture-rich, story-driven substrates. Ecovative Design’s mycelium cushioning wins with electronics brands seeking plastic-free protective formats. Seaweed-based sachets that dissolve in water offer a novel user experience for condiment packets, while bagasse trays are gaining favor with quick-service restaurants seeking to eliminate expanded polystyrene. This diversity underscores how the biodegradable packaging solutions market benefits when functional performance and narrative marketing intersect.

Note: Segment shares of all individual segments available upon report purchase

By Packaging Format: Flexible Leads, Rigid Accelerates

Flexible formats commanded a 56.32% share in 2025, reflecting their lower mass-to-product ratio and transport efficiency, which are crucial for e-commerce mailers and quick-service wraps. Pouches for pet food and coffee gained traction as bio-barrier coatings narrowed oxygen-permeation gaps. Conversely, rigid formats are projected to track a robust 7.89% CAGR to 2031, driven by molded-pulp bottles and jars that beverage and dairy players are piloting to replace PET.

Stora Enso’s wood-fiber composite bottle demonstrates progress, pairing a fiber body with a thin bio-liner. Bottles and jars still face melt-strength hurdles with biopolymers, but active R&D is aimed at closing these gaps. The coexistence of flexible leadership and rigid acceleration reflects trade-offs between material efficiency and post-use sorting clarity within the biodegradable packaging solutions market.

By End-User Industry: Food Dominates, Personal Care Sprints

Food accounted for 38.42% of 2025 revenue, spanning the fresh produce, bakery, meat, and dairy segments, whose short shelf lives align with the performance windows of compostable films. Beverage players are trialing PLA bottles for still drinks, although carbonated variants remain PET-centric due to the retention of CO₂. Healthcare adoption remains cautious, given the need for sterility validation cycles.

Personal care and cosmetics are projected to grow at an 8.23% CAGR to 2031, as luxury brands adopt compostable packaging to reinforce natural ingredient narratives and justify premium pricing. L’Oréal’s pledge to eliminate virgin plastics from mass-market lines by 2030 exemplifies this momentum. E-commerce adopters also scale demand, catalyzed by Amazon’s commitment to transition 75% of fulfillment packaging to compostable formats by 2028, adding durable pull for the biodegradable packaging solutions market.

Note: Segment shares of all individual segments available upon report purchase

By Distribution Channel: Direct Sales Lead, Indirect Gains

Direct sales channels captured 58.31% share in 2025, reflecting large food-service and retail chains’ preference for bespoke formulations and volume contracts. McDonald’s and Starbucks co-develop compostable cups and cutlery directly with converters, locking in multiyear volume.

Indirect channels, projected to grow at a 7.56% CAGR through 2031, are gaining relevance as distributors build technical service capabilities for mid-tier brands that demand smaller batch sizes and faster lead times. Firms operating a dual-channel model secure revenue diversity and insulation against single account dependency, a critical strategy as the biodegradable packaging solutions market matures.

Geography Analysis

Europe contributed 40.21% of the biodegradable packaging solutions market share in 2025, driven by the Packaging and Packaging Waste Regulation, which mandates recyclability or compostability by 2030, and by well-established composting networks in Germany, France, and the Netherlands. Germany’s Verpackungsgesetz further tightened recycled-content thresholds, while France extended its ban on single-use plastics to fresh produce packaging in 2025, accelerating material substitution. The United Kingdom aligned its Plastic Packaging Tax post-Brexit, maintaining regulatory coherence with continental Europe.

Asia-Pacific is on track for the fastest 8.85% CAGR through 2031. China’s 2024 guidelines aim for a 40% reduction in single-use plastics by 2030 and spur investments in PLA and PHA capacity. India’s amended Plastic Waste Management Rules encourage the use of compostable alternatives, although enforcement varies by state. Japan’s Green Purchasing Law boosts demand in public procurement, and Australia’s 2025 packaging targets push national brands toward compostable formats. An expanding middle class and rapid e-commerce growth add consumption tailwinds, amplifying regional pull for the biodegradable packaging solutions market.

North America benefits from EPR rollouts in California, Oregon, Colorado, and Maine, yet lacks federal harmonization, creating patchwork compliance terrain. Canada’s 2024 federal EPR framework simplifies provincial divergence and elevates compostable adoption rates. Mexico’s proximity to U.S. brands positions it as a near-shoring hub for converters. South America remains nascent, with Brazil and Argentina hindered by uneven compost infrastructure and price sensitivity. The Middle East and Africa show sporadic adoption most notably in the United Arab Emirates and South Africa, where tourism and export-oriented sectors value sustainability credentials, though broader market development awaits infrastructure build-out.

Competitive Landscape

The biodegradable packaging solutions market remains moderately fragmented, as the top 10 players hold an estimated 35-40% combined share. Large, vertically integrated firms such as Amcor, Mondi, and Smurfit WestRock leverage global reach to co-design high-barrier laminates and secure multi-year supply contracts with multinationals. Polymer innovators, including BASF, NatureWorks, and Novamont, compete through performance enhancements, simultaneously acquiring or partnering with downstream converters to capture market share and margin. Regional specialists exploit niche substrates, Ecovative’s mycelium cushioning or Notpla’s seaweed films to serve premium segments demanding brand differentiation.

Patent filings in bio-based barrier technologies increased 34% between 2024 and 2025, led by BASF, NatureWorks, and Stora Enso. White space remains in carbonated beverages and aseptic cartons, where current bio-coatings cannot yet match a 12-18-month shelf life; the first mover to crack this code could unlock a multi-billion-dollar opportunity. Closed-loop take-back programs, though logistics-intensive, offer compelling brand stories and customer lock-in for firms that can finance the infrastructure. Enzymatic depolymerization startups aiming to convert post-consumer PLA back into lactide monomers suggest future circularity pathways that could redefine competitive parameters within the biodegradable packaging solutions market.

Biodegradable Packaging Solutions Industry Leaders

Mondi Group

Tetra Pak International SA

Sealed Air Corporation

International Paper Company

Amcor plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Amcor committed USD 180 million to expand PLA film capacity in Thailand by 40%, with commissioning slated for Q3 2027.

- November 2025: Mondi Group partnered with Total Corbion to co-develop high-barrier PLA laminates for modified-atmosphere produce packaging, targeting a Q2 2026 European launch.

- October 2025: Stora Enso acquired a molded-pulp line in Poland for EUR 45 million (USD 50.85 million), adding 15,000 t of annual output for fiber-based bottles.

- September 2025: NatureWorks secured USD 200 million project finance for a 75,000 t PHA plant in Iowa, with start-up planned for 2028.

Global Biodegradable Packaging Solutions Market Report Scope

Biodegradability refers to the ability of materials to break down and return to nature. To qualify as biodegradable, packaging products or materials must completely break down and decompose into natural elements within a short time after disposal, typically in a year or less.

The Biodegradable Packaging Solutions Report is Segmented by Material Type (Bioplastics, Paper, Molded Pulp Fiber, and Plant-Based Composites), Packaging Format (Rigid, and Flexible), End-User Industry (Food, Beverage, Healthcare, Personal Care, E-Commerce, and Other End-user Industry), Distribution Channel (Direct, and Indirect), and Geography (North America, South America, Europe, Asia-Pacific, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Bioplastics | Starch-Based Plastics |

| Cellulose-Based Plastics | |

| Polylactic Acid (PLA) | |

| Polyhydroxyalkanoates (PHA) | |

| Polybutylene Succinate (PBS) | |

| Other Compostable Polymers | |

| Paper | |

| Molded Pulp Fiber | |

| Plant-Based Composites (Mushroom, Seaweed, Bagasse) |

| Rigid Packaging | Bottles and Jars |

| Trays and Clamshells | |

| Boxes and Cartons | |

| Other Rigid Packagings | |

| Flexible Packaging | Films and Wraps |

| Pouches and Bags | |

| Other Flexible Packagings |

| Food |

| Beverage |

| Healthcare and Pharmaceuticals |

| Personal Care and Cosmetics |

| E-Commerce and Retail |

| Other End-user Industries |

| Direct Sales |

| Indirect Sales |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Nigeria | ||

| Rest of Africa | ||

| By Material Type | Bioplastics | Starch-Based Plastics | |

| Cellulose-Based Plastics | |||

| Polylactic Acid (PLA) | |||

| Polyhydroxyalkanoates (PHA) | |||

| Polybutylene Succinate (PBS) | |||

| Other Compostable Polymers | |||

| Paper | |||

| Molded Pulp Fiber | |||

| Plant-Based Composites (Mushroom, Seaweed, Bagasse) | |||

| By Packaging Format | Rigid Packaging | Bottles and Jars | |

| Trays and Clamshells | |||

| Boxes and Cartons | |||

| Other Rigid Packagings | |||

| Flexible Packaging | Films and Wraps | ||

| Pouches and Bags | |||

| Other Flexible Packagings | |||

| By End-User Industry | Food | ||

| Beverage | |||

| Healthcare and Pharmaceuticals | |||

| Personal Care and Cosmetics | |||

| E-Commerce and Retail | |||

| Other End-user Industries | |||

| By Distribution Channel | Direct Sales | ||

| Indirect Sales | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the projected value of the biodegradable packaging solutions market in 2031?

The market is expected to reach USD 159.97 billion by 2031.

Which material category is growing fastest within biodegradable packaging?

Plant-based composites such as mushroom mycelium, seaweed films, and bagasse products are forecast to grow at 7.42% CAGR through 2031.

Why is Asia-Pacific considered the high-growth region?

Robust policy mandates in China and India, coupled with rapid PLA and PHA capacity expansions, drive an anticipated 8.85% CAGR to 2031.

How do Extended Producer Responsibility schemes affect adoption?

EPR laws impose higher fees on non-compostable plastics, incentivizing brand owners to switch to certified biodegradable materials to lower compliance costs.

Which packaging format currently leads market share?

Flexible packaging, including films, wraps, and pouches, held 56.32% revenue share in 2025.

What major technical hurdle remains for biodegradable packaging?

Achieving moisture and oxygen barriers comparable to conventional plastics in carbonated beverage and aseptic applications continues to be a key challenge.