Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

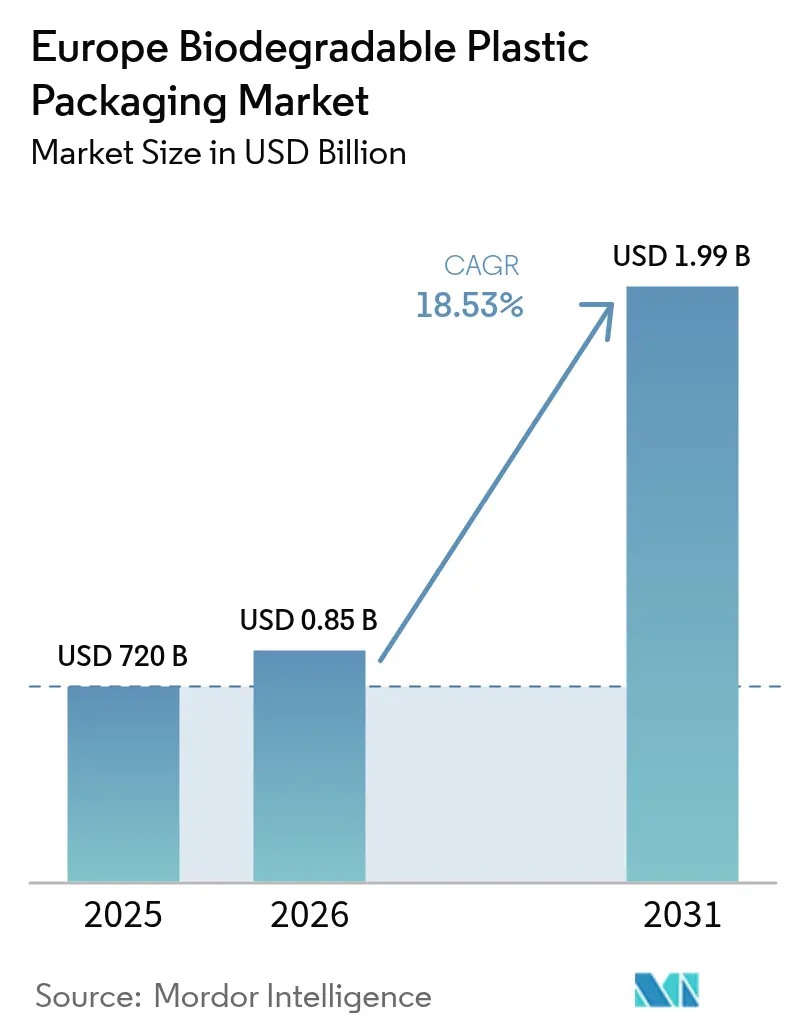

| Base Year Market Size (2025) | USD 720 Billion |

| Market Size (2026) | USD 0.85 Billion |

| Market Size (2031) | USD 1.99 Billion |

| Growth Rate (2026 - 2031) | 18.53% CAGR |

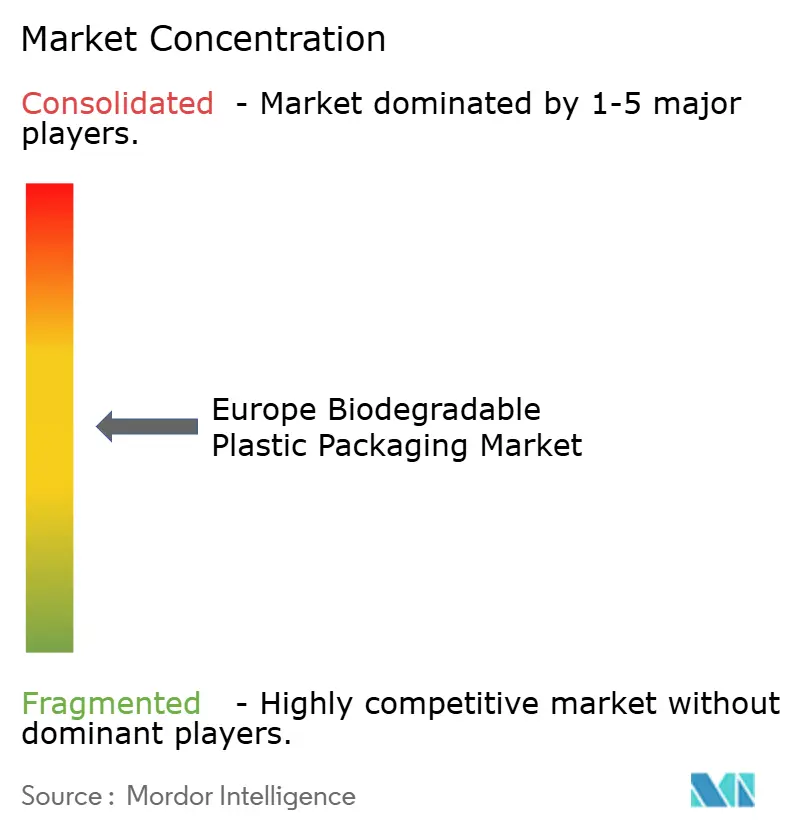

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Biodegradable Plastic Packaging Market Analysis by Mordor Intelligence

The Europe biodegradable plastic packaging market size is expected to grow from USD 720 million in 2025 to USD 853.4 million in 2026 and is forecast to reach USD 1.99 billion by 2031 at 18.53% CAGR over 2026-2031. Market momentum reflects the synchronized impact of the EU Packaging and Packaging Waste Regulation that enters force in 2026, national EPR levies such as Germany’s EUR 5.22 (USD 5.9) per-capita charge, and brand commitments to slash virgin resin use. PLA maintains scale leadership after the USD 565 million Normandy line reached nameplate output, while fast-rising PHA captures premium demand for marine-biodegradable claims. Flexible pouches and bags dominate volumes thanks to material efficiency and watermark-enabled sortation pilots showing up to 93.8% detection accuracy. Food packaging drives baseline demand, but foodservice registers the sharpest uptake as single-use plastic bans reshape institutional procurement.

Key Report Takeaways

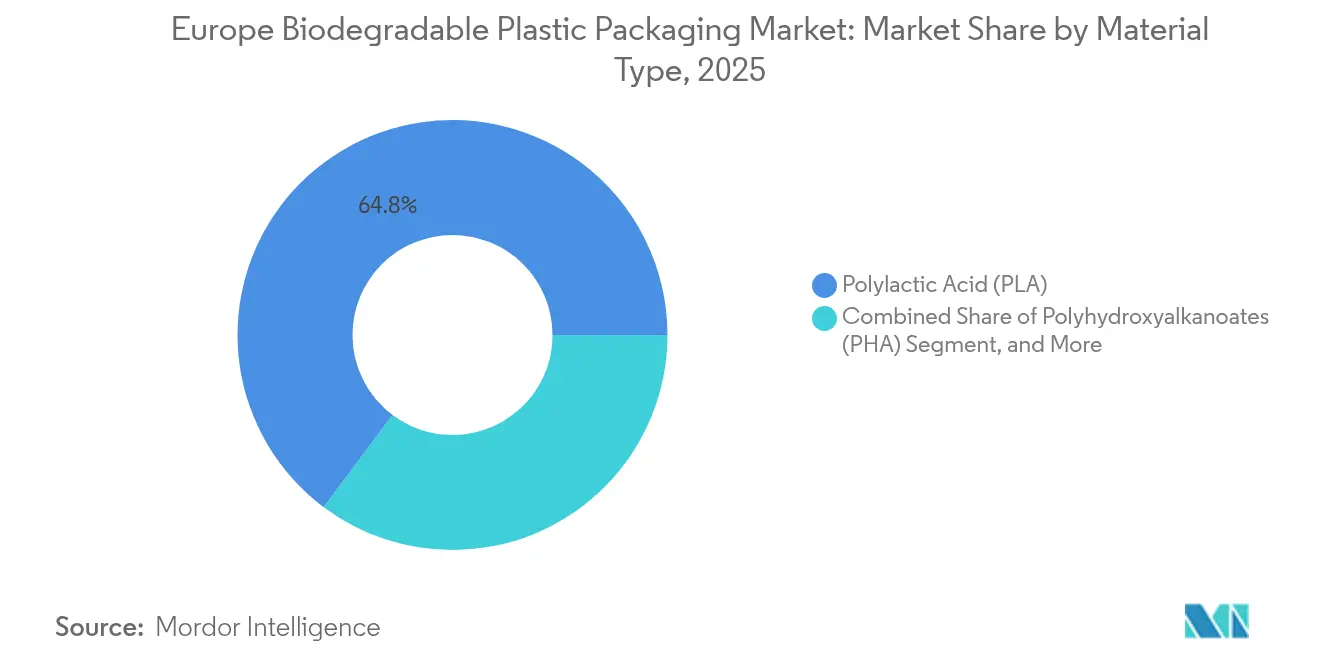

- By material type, PLA led with 64.78% of the Europe biodegradable plastic packaging market share in 2025; PHA is projected to expand at a 21.71% CAGR through 2031.

- By packaging type, flexible formats accounted for 57.91% of the Europe biodegradable plastic packaging market size in 2025, while rigid formats are forecast to have a 18.97% CAGR to 2031.

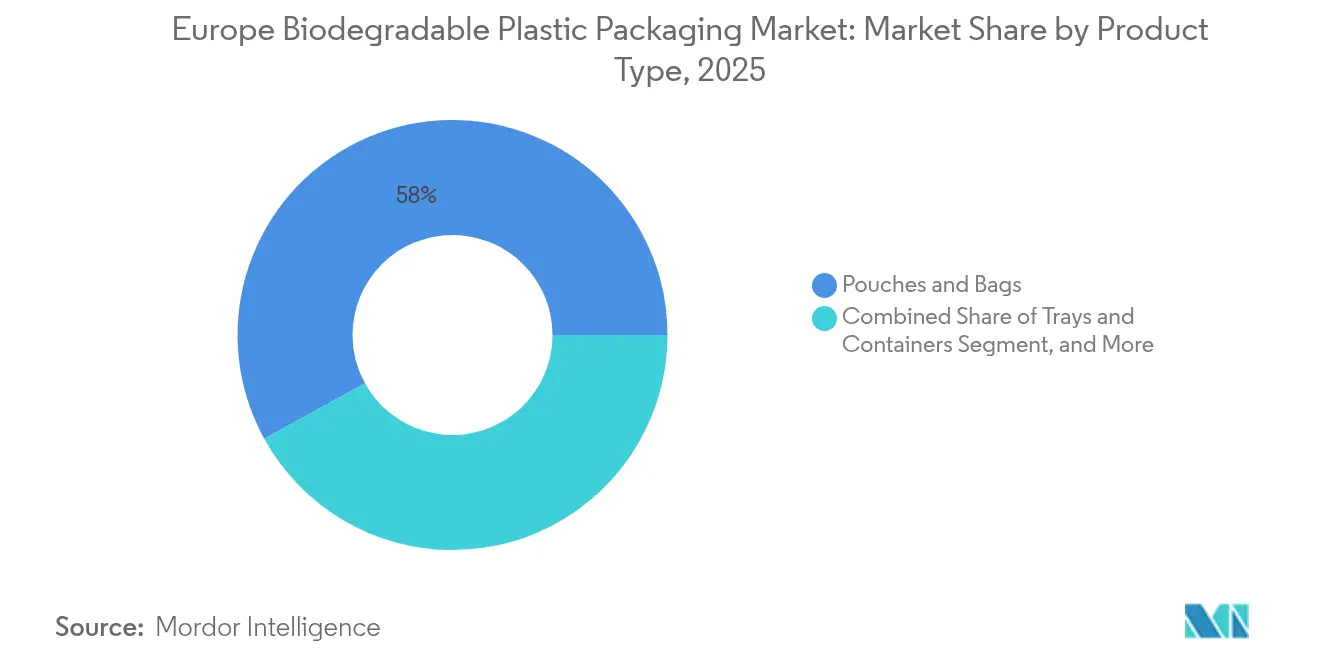

- By product type, pouches and bags held 58.02% revenue share in 2025; trays and containers are poised for a 19.98% CAGR to 2031.

- By end-user industry, food applications captured 29.21% share in 2025, whereas foodservice is advancing at a 21.85% CAGR between 2026-2031.

- By country, Germany commanded 22.22% of 2025 revenue, and France is expected to post a 19.74% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Biodegradable Plastic Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent EU single-use plastics and packaging waste regulations | +4.2% | EU27, UK, Norway, Switzerland | Medium term (2-4 years) |

| Rising consumer preference for sustainable packaging solutions | +2.5% | Western Europe, Nordics | Short term (≤ 2 years) |

| Corporate sustainability commitments among FMCG and retail brands | +3.8% | Western Europe | Medium term (2-4 years) |

| Expansion of composting and biowaste collection infrastructure | +2.1% | Core EU | Long term (≥ 4 years) |

| Beverage brand shift from glass to bio-PET/PEF bottles | +1.3% | Northern Europe | Medium term (2-4 years) |

| Convergence of digital watermarking with compostable films | +0.8% | Advanced waste hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent EU Single-Use Plastics and Packaging Waste Regulations

The 2026 PPWR deadline creates narrow but high-volume demand channels by limiting mandatory compostable use cases to tea bags, fruit labels, and ultra-light carrier bags. [1]European Commission, “Regulation (EU) 2024/1040 on Packaging and Packaging Waste,” Official Journal of the European Union, europa.euClarity on scope reduces investment risk, prompting converters to commit capacity to identified niches rather than resorting to blanket substitution. Germany amplifies the signal through its per-capita EPR fee, translating regulatory intent into immediate cost incentives. Synchronization of policy and plant start-ups, such as France’s Normandy PLA line reaching nameplate output in August 2024, illustrates public-private coordination that lowers market uncertainty. Brand owners now embed compliance clauses in multiyear supply contracts, locking in offtake and accelerating commercialization cycles.

Rising Consumer Preference for Sustainable Packaging Solutions

Seventy-three percent of European shoppers actively seek biodegradable options, with Nordics showing the highest willingness to pay premiums. [2]European Bioplastics, “Consumer Attitudes Toward Bioplastics,” european-bioplastics.orgThe consumer shift has evolved from generic eco-friendly messaging to material-specific literacy, pushing brands to substantiate claims under ISO and EN standards. Premium labels initially roll out biodegradable formats in high-income regions, then scale to price-sensitive southern markets as the cost curve falls. Nestlé’s paper-based wrappers, which cut plastic by up to 97%, exemplify how brand equity is leveraged to trial new substrates before mass rollout. As awareness grows, labeling accuracy and third-party certification become core purchase triggers rather than optional proof points.

Corporate Sustainability Commitments Among FMCG and Retail Brands

Net-zero and virgin plastic reduction pledges from leading FMCG groups translate directly into procurement targets that exceed minimum legal thresholds. Unilever’s 2025 goal to halve virgin plastic and PepsiCo’s 2030 objective to cut virgin resin in half have created a forward-order book for bio-based materials irrespective of near-term price premiums. These commitments cluster around mid-decade milestones, producing a demand bulge that underpins investment decisions such as BASF’s ecovio capacity expansion and Paques Biomaterials’ 6,000-tonne PHA unit slated for 2026. Supplier scorecards are increasingly weighing carbon intensity and end-of-life performance, transforming sustainability from a marketing differentiator into a qualifying attribute for vendor selection.

Expansion of Composting and Biowaste Collection Infrastructure

Europe operates roughly 5,800 bio-waste treatment sites with a combined capacity of 71 million tonnes, yet distribution is uneven. Germany, France, and Italy house most capacity, enabling mass-market compostable packaging, whereas Eastern Europe lags due to funding constraints. Grass-roots models, such as France’s 1,150-member Réseau Compost Citoyen, supplement municipal plants and increase collection density. EU Cohesion Fund and Interreg CORE initiatives earmark rural composting grants that will unlock new demand pockets post-2026. Suppliers now align product launches with rollouts of separate bio-waste bins, ensuring the disposal route is available at the point of sale.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Higher production costs of biodegradable polymers versus conventional plastics | -2.3% | Global | Short term (≤ 2 years) |

| Limited industrial composting capacity across EU member states | -1.8% | Eastern Europe | Medium term (2-4 years) |

| Risk of feedstock competition with the food chain amid CAP reforms | -1.2% | EU27 | Long term (≥ 4 years) |

| Residual microplastics from incompletely digested PLA | -0.9% | Northern Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Higher Production Costs of Biodegradable Polymers Versus Conventional Plastics

PLA continues to trade at 2-3× and PHA at 5-7× fossil plastic benchmarks, reflecting fermentation complexity and specialized feedstock logistics. Although global bioplastic nameplate capacity is expected to rise from 2.47 million tonnes in 2024 to 5.73 million tonnes by 2029, unit costs remain sticky because lactide and PHA monomer supply chains are still maturing. Carbon taxes or plastic levies could narrow the delta, yet the timing and uniformity of such fiscal tools remain uncertain. Producers therefore focus on premium niches, such as marine-throwable items and high-barrier snack pouches, where performance advantages justify price gaps.

Limited Industrial Composting Capacity Across EU Member States

Infrastructure scarcity outside the Western core slows rollout. Italy counts 275 composting plants, but Eastern bloc states have single-digit facilities, creating logistical dead zones for certified compostable packs. [3]Italian Composting and Biogas Consortium, “Industrial Composting Capacity,” compostaggio.it Cross-border shipment of bio-waste faces regulatory hurdles and cost penalties, so converters hesitate to ship compostable SKUs into regions lacking treatment options. Spain’s 97 compost sites and mandatory bio-waste segregation for towns with over 5,000 residents illustrate how regulatory carrots and sticks can unlock capacity; however, build-out timelines mean full parity with Western Europe is still several years away.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: PLA Dominance Faces PHA Disruption

PLA delivered 64.78% of the Europe biodegradable plastic packaging market size in 2025, supported by Normandy’s new PLA line that adds regional supply security. PHA is accelerating at a 21.71% CAGR and is viewed as the go-to option for marine-exposed packaging, from coastal foodservice to aquaculture products. The cost challenge is higher, yet early adopters accept a premium to secure jurisdictional compliance in Baltic and North Sea markets that are tightening litter rules. The European biodegradable plastic packaging market share for PBAT and PBS remains modest; however, these polyesters carve out specific use cases, with the former in starch-based flexible blends and the latter in rigid, high-barrier trays.

Growth pathways diverge: PLA suppliers prioritize cost-down through scale, adding polymers with higher heat stability for microwaveable ready meals, whereas PHA developers pursue functional white spaces, such as medical absorbables. As brands implement supplier diversification programs, dual-sourcing between PLA and PHA has become increasingly common, ensuring resilience against fluctuations in feedstock supply.

By Packaging Type: Flexible Formats Drive Innovation

Flexible packs contributed 57.91% to the Europe biodegradable plastic packaging market size in 2025 and are tracking a 18.86% CAGR. Their thinner gauge reduces resin need, aligning with PPWR’s weight-reduction targets. HolyGrail 2.0’s watermark pilots confirm that compostable films can be recognized at MRF speed, clearing a critical sortation hurdle. Rigid formats lag but innovate in bio-PET and PEF: Avantium’s Dutch plant went online in October 2024, enabling premium beverage brands to switch without sacrificing barrier performance.

Developers of rigid solutions focus on multilayer simplification, allowing caps, labels, and closures to co-degrade or be mechanically removed without contaminating the compost. The emergence of thermoformable PLA grades is expanding application scope into deli trays and blister packs, adding incremental volume to the Europe biodegradable plastic packaging market.

By Product Type: Pouches Lead Volume Growth

Pouches and bags, already 58.02% of 2025 volumes, benefit from high line-speed compatibility and lower pack-to-product ratios. Adoption has surged in dried food, coffee, and pet nutrition lines where oxygen and moisture barriers can now be met with metallized PLA. Trays and containers register the fastest growth at 19.98% CAGR because canteens and quick-service restaurants phase out EPS clamshells in favor of compostable solutions.

Films and agricultural wraps provide functional benefits like soil biodegradation, reducing post-harvest clean-up costs for farmers. Bottle formats remain niche; yet the high visibility of Coca-Cola’s 100% plant-based prototype signals that mainstream beverage conversion is plausible once PEF supply scales.

By End-User Industry: Food Dominance Contrasts Foodservice Growth

Food maintained 29.21% revenue share in 2025 as brand owners capitalized on consumer trust in certified compostable packs for direct contact. In contrast, foodservice is advancing at a 21.85% CAGR, driven by local bans on plastic cutlery and takeaway ware. Centralized purchasing by contract caterers accelerates volume ramp-up once specifications shift. Beverage producers remain technology scouts: Carlsberg’s fiber bottle consortium targets a 2025-2026 market entry, potentially unlocking a new rigid subsegment if performance metrics are met.

Personal care and pharma uptake is slower but steady, leveraging biodegradable caps and tubes to strengthen “clean-label” positioning among affluent consumers. Compliance with migration limits under EU Regulation 10/2011 adds qualification lead times, tempering speed to market for high-risk categories.

Geography Analysis

Germany leads the adoption with a 22.22% share in 2025, driven by its per-capita EPR fee, extensive biogas network, and successful watermarked sorting pilots that validate downstream recovery. France follows with the fastest trajectory, a 19.74% CAGR, underpinned by the Normandy PLA complex and a grassroots composting network comprising over 1,150 local schemes. Italy leverages 275 composting plants, including 61 integrated aerobic-anaerobic sites, to support starch-PBAT blends in deli and produce trays. Spain’s mandate for bio-waste segregation in municipalities above 5,000 residents unlocks incremental capacity at 97 compost facilities, positioning the country for mid-decade volume surges. The United Kingdom relies on more than 180 AD plants generating 6.6 TWh of biogas to process compostable liners, although regulatory divergence post-Brexit is slowing EN 13432 harmonization. The Nordics log the highest per-capita consumption of certified compostables, thanks to strong eco-label literacy and high household sorting rates, whereas Eastern Europe remains constrained by minimal composting infrastructure, despite EU Cohesion Fund allocations. Across the region, market penetration correlates with organic-waste treatment density, EPR-derived price signals, and proximity to domestic biopolymer supply.

Competitive Landscape

Market concentration is moderate as legacy converters and specialty bioplastic firms share the field. Tetra Pak pushes plant-based caps and wrapper laminates, Amcor markets high-barrier compostable films, and Mondi pilots water-soluble sachets for personal care. These incumbents wield distribution muscle but face cost erosion when scaling small-volume specialty resins. Specialty suppliers like NatureWorks (PLA), Novamont (PBAT-starch blends), and Paques Biomaterials (PHA) set technology benchmarks, but their limited nameplate capacity makes long-term offtake deals critical for financial closure.

Vertical integration is the emerging playbook: Futerro’s polymer-to-lactide back-integration secures margin, while Avantium’s PEF capacity pairs monomer production with downstream bottle partnerships. Partnerships flourish, Carlsberg’s fiber bottle consortium unites resin producers, bottle makers, and brand owners to hedge development risk. Digital watermarking provides a new competitive axis as converters that license the technology can promise higher recovery rates, addressing a frequent retailer concern.

Cost pressure is rising as sugar-based feedstock prices react to CAP revisions that incentivize alternate crop rotations. Converters hedge via multiyear feedstock contracts or by switching to waste-oil pathways where certification allows. Certification complexity around EN13432, ASTM D6400, and marine biodegradation standards adds compliance overhead that favors larger, better-capitalized players. Mergers between converters and resin start-ups are expected once early-stage facilities achieve stable yields.

Europe Biodegradable Plastic Packaging Industry Leaders

Tetra Pak International SA

Amcor Limited

Mondi PLC

Minima Technology

Tipa-corp Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2024: Avantium opened a flagship PEF plant in the Netherlands to supply premium beverage brands.

- September 2024: Paques Biomaterials raised EUR 14 million for a 6,000-tonne PHA plant scheduled for 2026.

- August 2024: Futerro’s EUR 500 million (USD 565 million) PLA biorefinery in Normandy reached full capacity.

- July 2024: HolyGrail 2.0 watermark trials in Germany achieved up to 93.8% detection efficiency for compostable packs.

Europe Biodegradable Plastic Packaging Market Report Scope

The Biodegradable Plastic Packaging Market includes the usage to environment friendly plastic packaging material in the wake of environmental concerns and the demand of this form of packaging in on an upward spring since the last decade. The scope of the study extends to the type of application of biodegradable plastics i.e. Bags, Rigid Packaging, Flexible Packaging, Consumer goods and other types of polymers, the end user industry of bioplastics and the material type of Biodegradable plastics.

By Material Type

| Starch Blends |

| Polylactic Acid (PLA) |

| Polybutylene Adipate Terephthalate (PBAT) |

| Polybutylene Succinate (PBS) |

| Polyhydroxyalkanoates (PHA) |

| Other Material Types |

By Packaging Type

| Rigid Packaging |

| Flexible Packaging |

By Product Type

| Films and Wraps |

| Pouches and Bags |

| Trays and Containers |

| Bottles and Jars |

| Other Product Types |

By End-User Industry

| Food |

| Beverages |

| Foodservice |

| Pharmaceutical |

| Personal Care and Home Care |

| Other End-User Industries |

By Country

| United Kingdom |

| Germany |

| France |

| Italy |

| Spain |

| Rest of Europe |

| By Material Type | Starch Blends |

| Polylactic Acid (PLA) | |

| Polybutylene Adipate Terephthalate (PBAT) | |

| Polybutylene Succinate (PBS) | |

| Polyhydroxyalkanoates (PHA) | |

| Other Material Types | |

| By Packaging Type | Rigid Packaging |

| Flexible Packaging | |

| By Product Type | Films and Wraps |

| Pouches and Bags | |

| Trays and Containers | |

| Bottles and Jars | |

| Other Product Types | |

| By End-User Industry | Food |

| Beverages | |

| Foodservice | |

| Pharmaceutical | |

| Personal Care and Home Care | |

| Other End-User Industries | |

| By Country | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe |

Key Questions Answered in the Report

How large will the Europe biodegradable plastic packaging market be by 2031?

It is projected to reach USD 1.99 billion by 2031, supported by an 18.53% CAGR driven by EU regulation and corporate sustainability mandates.

Which material is growing fastest in European biodegradable packages?

PHA is expected to expand at a 21.71% CAGR through 2031 due to its marine-biodegradation advantage.

Why is France showing the highest growth among major markets?

France benefits from a new USD 565 million PLA plant and rapid expansion of local composting networks, pushing growth to 19.74% CAGR.

What segments lead volume in flexible biodegradable packs?

Pouches and bags hold 58.02% share because they use less material and align with smart-sorting pilots.

How do higher resin costs impact adoption?

PLA and PHA premium pricing, 2-7× fossil plastics, slows uptake in price-sensitive regions, but EPR fees and brand pledges offset some cost barriers.

What technologies improve end-of-life sorting for compostable films?

Digital watermarking trials under HolyGrail 2.0 show up to 93.8% detection efficiency, enabling automated identification at material recovery facilities.

Page last updated on: