Global Navigation Satellite System (GNSS) Chip Market Size

Market Overview

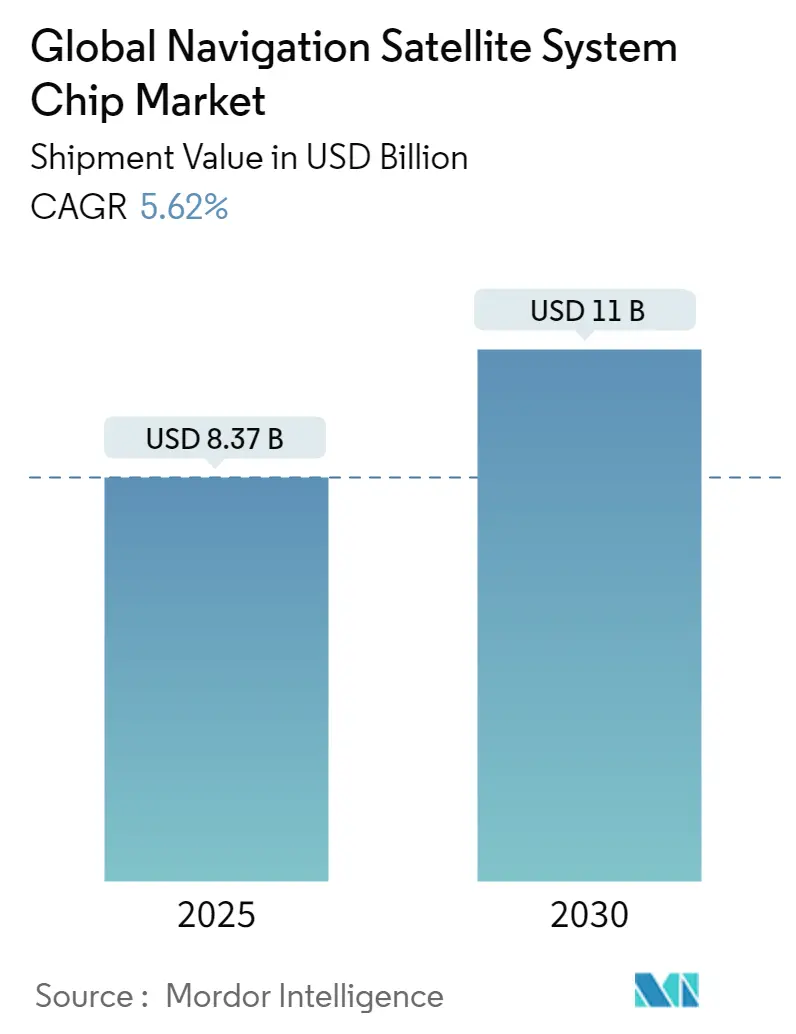

| Study Period | 2019 - 2030 |

| Market Size (2025) | USD 8.37 Billion |

| Market Size (2030) | USD 11.00 Billion |

| Growth Rate (2025 - 2030) | 5.62% CAGR |

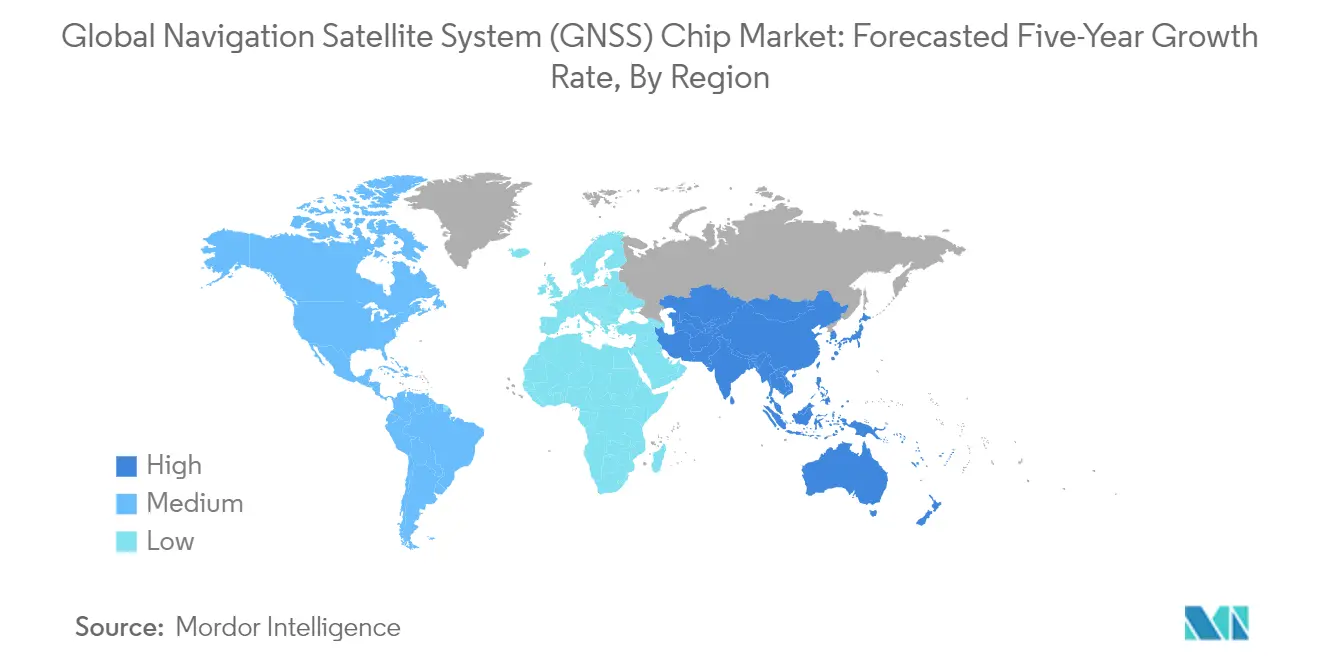

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia-Pacific |

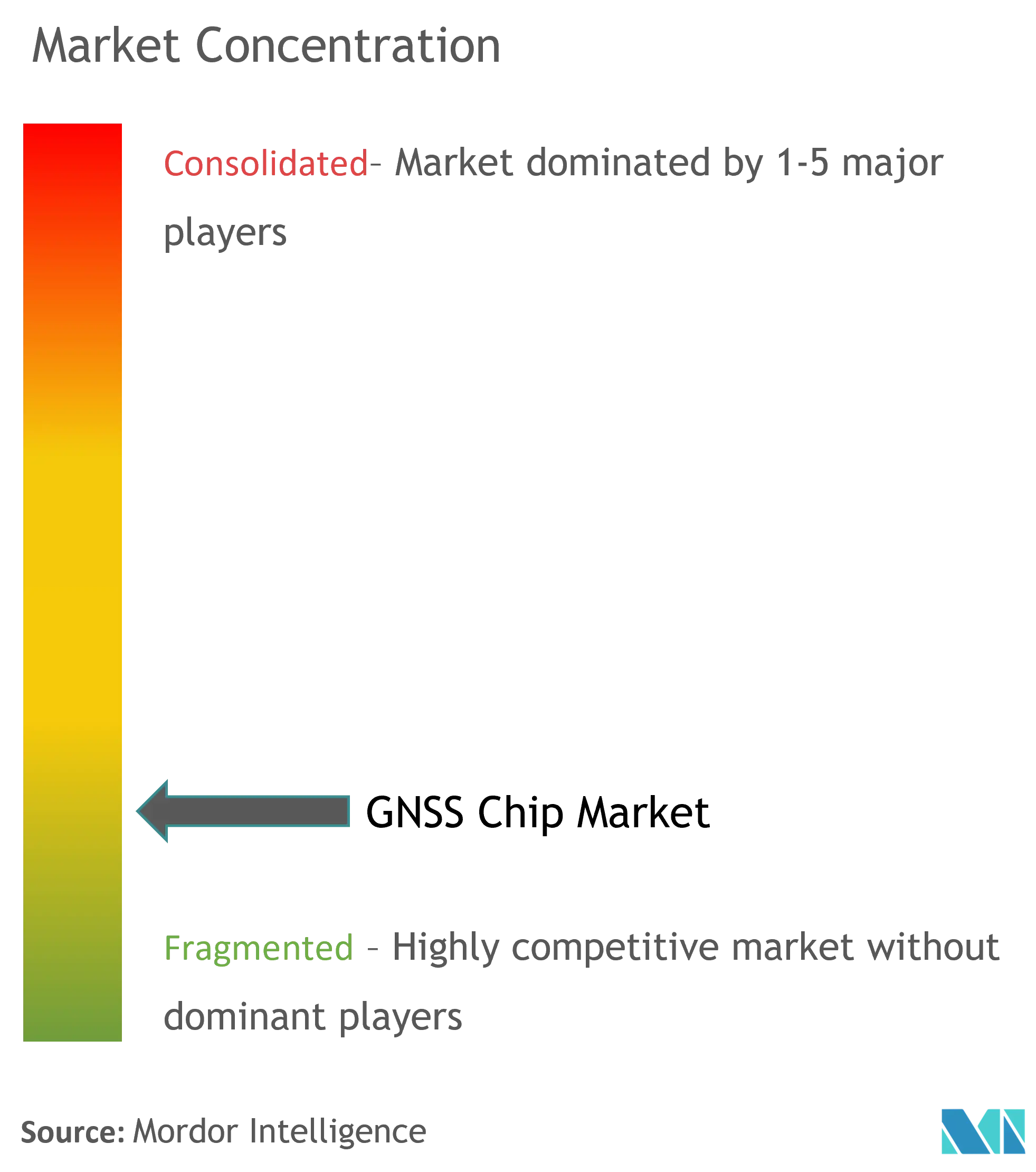

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Global Navigation Satellite System (GNSS) Chip Market Analysis

The Global Navigation Satellite System Chip Market size in terms of shipment value is expected to grow from USD 8.37 billion in 2025 to USD 11.00 billion by 2030, at a CAGR of 5.62% during the forecast period (2025-2030).

The GNSS chip industry operates within a complex ecosystem where only six major players—the United States, Russia, China, India, Japan, and the European Union—maintain their own satellite navigation systems. This concentrated control of satellite infrastructure has led to an increased focus on interoperability and compatibility between different GNSS systems, with multiple constellation support becoming a standard feature in modern GNSS chips. Currently, approximately 50% of the global population utilizes tech-advanced wearable devices equipped with GNSS capabilities, highlighting the widespread adoption of this technology in consumer applications.

The industry is witnessing a significant shift toward multi-frequency GNSS receivers, particularly in high-precision applications. More than 30 companies are now producing Galileo-ready chips both within and outside the European region, demonstrating the growing importance of multi-constellation compatibility. This technological evolution has been particularly evident in the automotive sector, where high-precision GNSS chips are being integrated with other sensors and technologies to enable advanced driver assistance systems (ADAS) and autonomous driving capabilities.

The integration of GNSS technology with Internet of Things (IoT) applications has emerged as a defining trend in the GNSS market. Manufacturers are increasingly focusing on developing low-power consumption chips that can support multiple constellations while maintaining extended battery life for IoT devices. This development is particularly crucial for applications in asset tracking, smart cities, and industrial IoT, where precise positioning and efficient power management are essential requirements.

The market is characterized by strategic collaborations between GNSS manufacturers and technology providers to enhance positioning accuracy and reliability. These partnerships are focused on developing innovative solutions that combine GNSS capabilities with other technologies such as inertial sensors, cellular networks, and artificial intelligence. The industry has also seen increased attention to security features in GNSS chips, with manufacturers incorporating advanced anti-spoofing and anti-jamming capabilities to protect against potential threats to positioning accuracy and reliability.

Global Navigation Satellite System (GNSS) Chip Market Trends

Adoption of Environmentally Friendly Transport Solutions, Sustainable Agriculture, and Meteorological Monitoring

The increasing focus on environmentally conscious transportation solutions has become a significant driver for GNSS chip adoption across multiple sectors. The technology provides essential positioning and navigation capabilities for electric vehicles, autonomous driving systems, and smart mobility solutions. GNSS technology delivers the accuracy and reliability required for vehicle positioning down to the lane level, which is crucial for V2X (Vehicle-to-Everything) applications and genuine automated driving functionality. The integration of GNSS with other sensors like LiDAR, HD maps, and cameras has become fundamental for computer-aided technology in sustainable transport solutions, as it serves as the primary source of absolute positioning data.

In the agricultural sector, GNSS technology has emerged as a cornerstone for precision agriculture and sustainable farming practices. The agricultural industry was an early adopter of EGNOS (European Geostationary Navigation Overlay Service), with more than 95% of agricultural receivers in Europe currently being EGNOS-enabled. GNSS applications in agriculture span from basic operations like plowing and fertilizing to more precise operations such as sowing and transplanting. The technology enables farmers to implement site-specific monitoring, soil condition monitoring, and real-time updates on moisture levels, fertility, and diseases, contributing to more sustainable and efficient farming practices while optimizing resource utilization.

Increasing Demand for Accurate Real-Time Data

The growing requirement for precise real-time positioning and timing applications has become a crucial market driver, spanning across surveying, mapping, smart cities, connected vehicles, and environmental monitoring sectors. The advancement in GNSS technology has significantly improved positioning accuracy, as demonstrated by the latest dual-frequency smartphones. For instance, the first dual-frequency GNSS smartphone equipped with a Broadcom BCM47755 achieves vertical and horizontal accuracy of 0.51 meters and 6 meters respectively, compared to single-frequency smartphones that only achieve 5.64 meters and 15 meters for horizontal and vertical positioning.

The demand for accurate real-time data has also driven innovations in GNSS IC design and functionality. Modern GNSS receivers are being developed with enhanced capabilities for simultaneous reception of multiple satellite signals, improved multipath mitigation, and advanced signal processing techniques. The new generation of Android smartphones, starting from version 9, incorporates high-performance GNSS chips capable of tracking dual-frequency multi-constellation data, with the ability to disable duty cycle power-saving options for better quality pseudo-range and carrier phase raw data availability. This evolution in technology has enabled more precise positioning services for applications ranging from urban navigation to asset tracking and emergency response systems.

Evolution of GNSS Infrastructure, Such as the Appearance of New Signals and Frequencies

The continuous evolution of GNSS infrastructure has been marked by the emergence of new satellite systems and signal frequencies, significantly enhancing the global positioning ecosystem. The market now benefits from multiple operational GNSS systems, including GPS, GLONASS, Galileo, and BeiDou, with regional systems like NavIC from India and QZSS from Japan providing additional coverage. BeiDou alone has deployed 48 satellites in orbit, transmitting signals across multiple frequencies including B1I (1561.098 MHz), B1C (1575.42 MHz), B2a (1175.42 MHz), B2I and B2b (1207.14 MHz), and B3I (1268.52 MHz), offering improved signal availability and accuracy.

The modernization of GNSS infrastructure has also led to enhanced interoperability between different satellite systems and the introduction of new service capabilities. According to the European GNSS Agency, over 95% of the satellite navigation system market now supports Galileo in new products, including major manufacturers of smartphone chipsets. This evolution has prompted significant investments in research and development, as evidenced by China's 14th Five-Year Plan's emphasis on GNSS industry innovation and South Korea's development of the Korean Positioning System (KPS). These developments in infrastructure continue to drive the market by enabling new applications and improving existing services through better accuracy, reliability, and coverage.

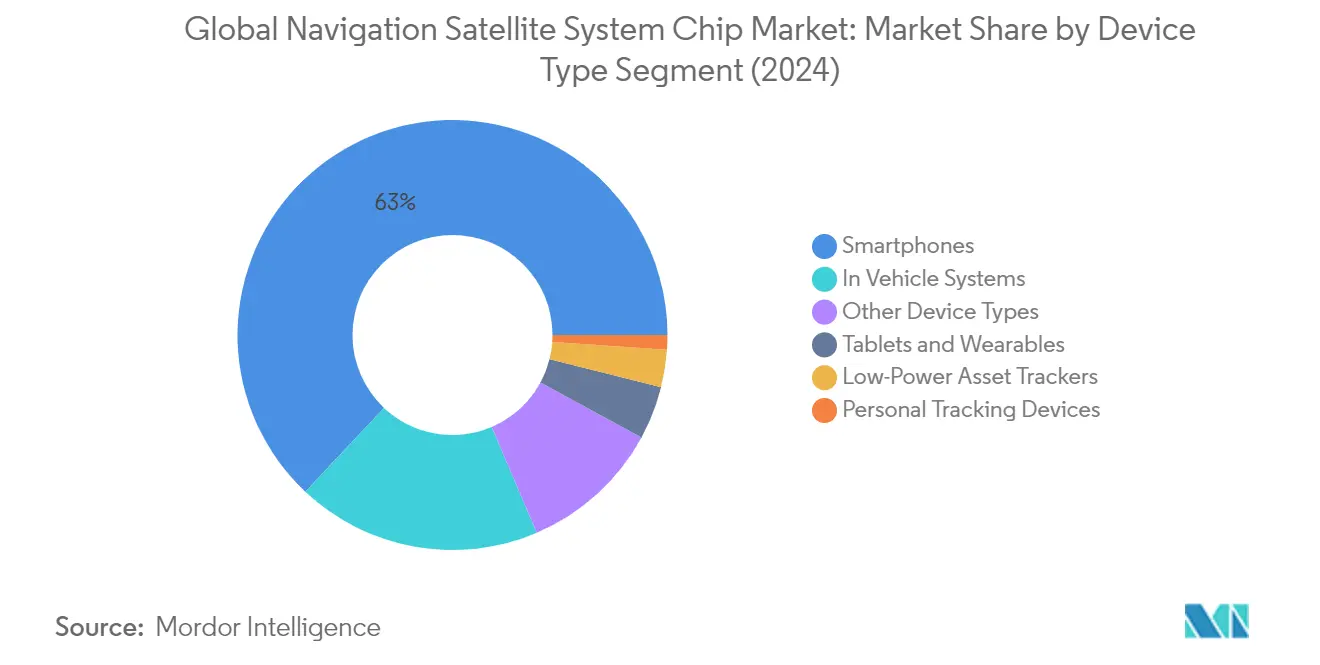

Segment Analysis: By Device Type

Smartphones Segment in Global Navigation Satellite System Chip Market

The smartphones segment continues to dominate the Global Navigation Satellite System (GNSS) chip market, commanding approximately 63% of the total market share in 2024. This substantial market leadership is driven by the increasing integration of GNSS chips in modern smartphones for various applications, including navigation, location-based services, and emerging augmented reality applications. The segment's dominance is further strengthened by the European Commission's regulation mandating new smartphones to include satellite and Wi-Fi location services, with chipsets requiring access to the EU's satellite system, Galileo. The widespread adoption of multi-constellation GNSS receivers in smartphones, supporting GPS, GLONASS, Galileo, and BeiDou systems, has enhanced positioning accuracy and reliability, making smartphones the primary device category for GNSS chipsets deployment.

Low-Power Asset Trackers Segment in Global Navigation Satellite System Chip Market

The low-power asset trackers segment is experiencing remarkable growth in the GNSS chip market, projected to expand at approximately 19% during the forecast period 2024-2029. This exceptional growth is driven by the increasing demand for efficient asset tracking solutions across various industries, particularly in supply chain management and logistics. The segment's growth is fueled by innovations in power-efficient GNSS ICs that enable extended battery life while maintaining accurate positioning capabilities. The development of specialized tracking solutions for supermarkets, industrial equipment, and high-value assets has created new opportunities for GNSS chip manufacturers. Advanced features such as geofencing, real-time monitoring, and integration with IoT platforms are further accelerating the adoption of low-power asset tracking solutions across global markets.

Remaining Segments in GNSS Chip Market by Device Type

The other significant segments in the GNSS chip market include tablets and wearables, personal tracking devices, and in-vehicle systems, each serving distinct market needs and applications. The in-vehicle systems segment has emerged as a crucial component in the automotive industry, supporting advanced driver assistance systems and autonomous driving capabilities. The tablets and wearables segment continues to evolve with the integration of high-precision GNSS capabilities in fitness trackers, smartwatches, and professional tablets. Personal tracking devices serve specialized applications in child safety, pet tracking, and elderly care, while maintaining a steady market presence. These segments collectively contribute to the market's diversification and technological advancement, offering specialized solutions for different user requirements and applications.

Segment Analysis: By End-User Industry

Consumer Electronics Segment in Global Navigation Satellite System Chip Market

The consumer electronics segment dominates the global navigation satellite system chip market, commanding approximately 69% of the total market share in 2024. This significant market presence is primarily driven by the widespread integration of GNSS chips in smartphones, tablets, wearables, and other consumer electronic devices. The increasing adoption of location-based services, fitness tracking applications, and navigation features in consumer devices continues to fuel the demand for GNSS chips. Additionally, the emergence of dual-frequency GNSS capabilities in modern smartphones and wearables has enhanced positioning accuracy for pedestrian navigation and location-based services, further strengthening the segment's market position.

Automotive Segment in Global Navigation Satellite System Chip Market

The automotive segment is experiencing rapid growth in the GNSS chip market, driven by the increasing integration of navigation systems in vehicles and the rising demand for advanced driver assistance systems (ADAS). The segment is witnessing substantial technological advancements, particularly in high-precision positioning solutions for autonomous vehicles and connected car applications. The development of multi-constellation GNSS receivers that can simultaneously track multiple satellite systems has significantly improved accuracy and reliability for automotive applications. The integration of GNSS with other technologies such as inertial sensors and dead reckoning capabilities has enhanced navigation performance in challenging environments like urban canyons and tunnels, making these systems increasingly valuable for automotive applications.

Remaining Segments in End-user Industry

Other end-user industries utilizing GNSS chip technology include agriculture, maritime, aviation, railways, and critical infrastructure sectors. These segments leverage GNSS technology for various applications such as precision farming, fleet management, vessel navigation, and infrastructure monitoring. The integration of GNSS chips in drones and unmanned aerial vehicles (UAVs) has opened new opportunities in surveying, mapping, and inspection applications. Additionally, the adoption of GNSS technology in industrial IoT applications and smart city initiatives continues to drive innovation and create new use cases across these diverse sectors. The nano GPS chip market and GPS positioning chip market are also seeing growth as these technologies become more prevalent in various applications.

Global Navigation Satellite System Chip Market Geography Segment Analysis

Global Navigation Satellite System Chip Market in North America

North America represents a crucial market for GNSS chip technology, driven by extensive adoption across automotive, consumer electronics, and industrial applications. The United States leads the regional market with advanced technological infrastructure and a strong presence of major GNSS chip manufacturers. The region's growth is supported by increasing integration of GNSS technology in autonomous vehicles, precision agriculture, and smart city initiatives. The widespread adoption of IoT devices and connected technologies further amplifies the demand for GNSS chips across various sectors.

Global Navigation Satellite System Chip Market in United States

The United States dominates the North American GNSS market, accounting for approximately 27% of the global market share in 2024. The country's market leadership is reinforced by its ownership and operation of the GPS constellation, comprising up to 32 medium Earth orbit satellites across six different orbital planes. The US Space Force maintains a commitment to having at least 24 operational GPS satellites available 95% of the time. The country's robust ecosystem of GNSS applications spans across sectors including automotive navigation, precision farming, surveying, and mobile device navigation, supported by continuous technological innovations and investments in satellite infrastructure.

Global Navigation Satellite System Chip Market in Europe

Europe maintains a strong position in the global GNSS market, distinguished by its operation of the Galileo navigation system. The region's market is characterized by significant investments in GNSS technology development and applications across various sectors, including transportation, agriculture, and urban development. The European GNSS industry benefits from strong institutional support and research initiatives, fostering innovation and technological advancement in satellite navigation systems.

Global Navigation Satellite System Chip Market in Russia

Russia holds a significant position in the European GNSS chip market, with approximately 8% market share in 2024. The country's market strength is built upon its GLONASS (Global Navigation Satellite System) constellation, which consists of 24+ operational satellites. Russia's GNSS infrastructure serves both domestic and international users, providing critical navigation and positioning services across various applications, including transportation, emergency services, and precision timing.

Global Navigation Satellite System Chip Market in Asia-Pacific

The Asia-Pacific region represents a dynamic market for GNSS chip technology, characterized by rapid technological adoption and diverse application areas. The region benefits from multiple satellite navigation systems, including China's BeiDou, Japan's QZSS, and India's IRNSS, creating a robust infrastructure for GNSS applications. The market is driven by increasing smartphone penetration, a growing automotive sector, and expanding industrial applications across countries.

Global Navigation Satellite System Chip Market in China

China leads the Asia-Pacific GNSS chip market through its BeiDou Navigation Satellite System, which has established a comprehensive network of 48 satellites. The country's dominance is supported by strong government initiatives, extensive manufacturing capabilities, and widespread adoption across various sectors, including transportation, agriculture, and consumer electronics. The Chinese market benefits from significant research and development investments, particularly in areas like autonomous driving and smart city applications.

Global Navigation Satellite System Chip Market in South Korea

South Korea demonstrates remarkable growth potential in the GNSS chip market, driven by its ambitious plans to develop the Korean Positioning System (KPS) by 2034. The country's focus on high-precision positioning technologies and a strong electronics manufacturing base positions it favorably in the regional market. South Korea's advancement in GNSS technology is particularly evident in its automotive and mobile device sectors, where precise positioning capabilities are crucial for emerging applications.

Global Navigation Satellite System Chip Market in Latin America

Latin America's GNSS chip market is characterized by growing adoption across various sectors, particularly in transportation, agriculture, and urban development. The region benefits from multiple GNSS Information Centers that promote the use of European GNSS technology and foster collaboration between European and Latin American partners. Mexico City serves as a hub for GNSS technology advancement in the region, with a significant focus on developing applications for urban mobility and precision agriculture. Brazil emerges as both the largest and fastest-growing market in the region, driven by increasing adoption in agricultural applications and urban transportation systems.

Global Navigation Satellite System Chip Market in Middle East & Africa

The Middle East and Africa region demonstrates significant potential in the GNSS chip market, with growing applications in navigation, tracking, and precision timing services. The market is characterized by increasing adoption in oil and gas exploration, transportation, and urban development projects. The United Arab Emirates leads regional development with plans for navigation satellite launches, while Israel advances in developing non-GPS navigation systems. The region shows particular strength in developing GNSS applications for natural resource management and transportation infrastructure, with the UAE emerging as both the largest and fastest-growing market in the region.

Global Navigation Satellite System (GNSS) Chip Industry Overview

Top Companies in Global Navigation Satellite System Chip Market

The GNSS chip market features prominent players like Qualcomm, MediaTek, STMicroelectronics, Broadcom, Intel, u-blox, and Thales Group, leading technological advancement and market development. These companies demonstrate a strong commitment to product innovation through substantial R&D investments, particularly in developing multi-constellation receivers supporting GPS, GLONASS, Galileo, BeiDou, and other satellite systems. Operational agility is evidenced through strategic partnerships with technology providers, automotive manufacturers, and telecom operators to enhance positioning accuracy and expand application scope. Companies are increasingly focusing on vertical integration and expanding their product portfolios through strategic acquisitions and collaborations, while simultaneously working on reducing power consumption and improving chip performance for emerging applications like IoT, autonomous vehicles, and precision agriculture.

High Barriers Shape Competitive Market Structure

The GNSS chip market exhibits characteristics of an oligopolistic structure dominated by large-scale global semiconductor manufacturers with significant technological capabilities and financial resources. These established players have built strong barriers to entry through extensive patent portfolios, long-term supply agreements with major device manufacturers, and sophisticated manufacturing capabilities. The market shows a high degree of consolidation, with top players controlling substantial market share through their established relationships with smartphone manufacturers, automotive companies, and other major end-users.

The competitive landscape is characterized by increasing merger and acquisition activities as companies seek to strengthen their technological capabilities and expand their geographic presence. Major semiconductor conglomerates are acquiring specialized GNSS manufacturers to enhance their positioning solutions portfolio and gain access to emerging markets. The industry also sees strategic partnerships between chip manufacturers and regional players to establish stronger distribution networks and provide localized solutions, particularly in growing markets across Asia-Pacific and emerging economies.

Innovation and Integration Drive Market Success

Success in the GNSS market increasingly depends on companies' ability to develop integrated solutions that combine multiple positioning technologies and support various satellite constellations. Incumbent players are focusing on developing specialized solutions for high-growth segments like autonomous vehicles and IoT devices, while investing in advanced manufacturing processes to improve chip performance and reduce costs. Companies are also emphasizing the development of secure positioning solutions with enhanced anti-jamming and anti-spoofing capabilities to address growing security concerns in critical applications.

For new entrants and smaller players, success lies in identifying and serving niche market segments with specialized requirements, such as high-precision agriculture or industrial automation. The ability to provide comprehensive support services, including software development tools and technical assistance, is becoming increasingly important for market success. Companies must also navigate complex regulatory environments, particularly regarding export controls and national security considerations, while maintaining flexibility to adapt to evolving technical standards and customer requirements. The growing emphasis on environmental sustainability and energy efficiency in end-user industries is also shaping product development strategies in the GNSS devices market.

Global Navigation Satellite System (GNSS) Chip Market Leaders

-

Qualcomm Technologies, Inc.

-

Mediatek Inc.

-

STMicroelectronics N.V.

-

Broadcom Corporation

-

Intel Corporation

- *Disclaimer: Major Players sorted in no particular order

Global Navigation Satellite System (GNSS) Chip Market News

- In October 2021, STMicroelectronics announced Teseo-VIC3DA, a new member of the Teseo module family, to serve the positioning market with state-of-the-art GNSS chipset and modules. Teseo-VIC3DA is a simple, automotive-qualified navigation module that combines ST's high-performance Automotive Teseo III GNSS1 IC with the automotive 6-axis MEMS inertial measurement unit (IMU) and dead reckoning software.

- In September 2021, Broadcom Inc. announced low power L1/L5 GNSS receiver chip, the BCM4778, intended for mobile and wearable applications. The third-generation chip is 35% smaller and uses five times less power than the previous generation, owing to the newest GNSS improvements.

Global Navigation Satellite System (GNSS) Chip Industry Segmentation

A global navigation satellite system (GNSS) primarily refers to a constellation of satellites, which provides signals from space that transmit positioning and timing data to GNSS receivers. The receivers then use this data to determine various factors, such as location, speed, and altitude, combined with several sensors. The study covers the market numbers and unit shipments based on device type and uses of GNSS in different end-user industries across various geographies. Further, the study also covers the impact of the COVID-19 pandemic on the market.

| Device Type | Smartphones | ||

| Tablets and Wearables | |||

| Personal Tracking Devices | |||

| Low-power Asset Trackers | |||

| In-vehicle Systems | |||

| Drones | |||

| Other Device Types | |||

| End-user Industry | Automotive | ||

| Consumer Electronics | |||

| Aviation | |||

| Other End-user Industries | |||

| Geography | North America | United States | |

| Europe | Russia | ||

| Asia-Pacific | China | ||

| Japan | |||

| South Korea | |||

| Latin America | |||

| Middle-East and Africa | |||

| Smartphones |

| Tablets and Wearables |

| Personal Tracking Devices |

| Low-power Asset Trackers |

| In-vehicle Systems |

| Drones |

| Other Device Types |

| Automotive |

| Consumer Electronics |

| Aviation |

| Other End-user Industries |

| North America | United States |

| Europe | Russia |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| Latin America | |

| Middle-East and Africa |

Global Navigation Satellite System (GNSS) Chip Market Research FAQs

How big is the Global Navigation Satellite System Chip Market?

The Global Navigation Satellite System Chip Market size is expected to reach USD 8.37 billion in 2025 and grow at a CAGR of 5.62% to reach USD 11.00 billion by 2030.

What is the current Global Navigation Satellite System Chip Market size?

In 2025, the Global Navigation Satellite System Chip Market size is expected to reach USD 8.37 billion.

Who are the key players in Global Navigation Satellite System Chip Market?

Qualcomm Technologies, Inc., Mediatek Inc., STMicroelectronics N.V., Broadcom Corporation and Intel Corporation are the major companies operating in the Global Navigation Satellite System Chip Market.

Which is the fastest growing region in Global Navigation Satellite System Chip Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Global Navigation Satellite System Chip Market?

In 2025, the Asia-Pacific accounts for the largest market share in Global Navigation Satellite System Chip Market.

What years does this Global Navigation Satellite System Chip Market cover, and what was the market size in 2024?

In 2024, the Global Navigation Satellite System Chip Market size was estimated at USD 7.90 billion. The report covers the Global Navigation Satellite System Chip Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Global Navigation Satellite System Chip Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.