GNSS Chip Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 8.84 Billion |

| Market Size (2031) | USD 11.58 Billion |

| Growth Rate (2026 - 2031) | 5.56% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

GNSS Chip Market Analysis by Mordor Intelligence

The GNSS chip market size was valued at USD 8.37 billion in 2025 and estimated to grow from USD 8.84 billion in 2026 to reach USD 11.58 billion by 2031, at a CAGR of 5.56% during the forecast period (2026-2031). Mounting demand for multi-constellation reception across smartphones, autonomous vehicles, and precision agriculture keeps volume growth steady while opening premium niches for centimeter-level accuracy solutions. Evolving 5G timing requirements, along with BeiDou’s full global deployment and sovereign programs in India and the Middle East, continue to diversify revenue streams for GNSS chip vendors. Competitive intensity remains moderate, with integrated mobile SoCs driving high-volume cost pressure even as specialist suppliers carve out profitable positions in survey-grade, anti-jamming, and ultra-low-power designs. Energy efficiency and secure positioning are now core differentiators as customers weigh battery endurance against the rising threat of jamming and spoofing.

Key Report Takeaways

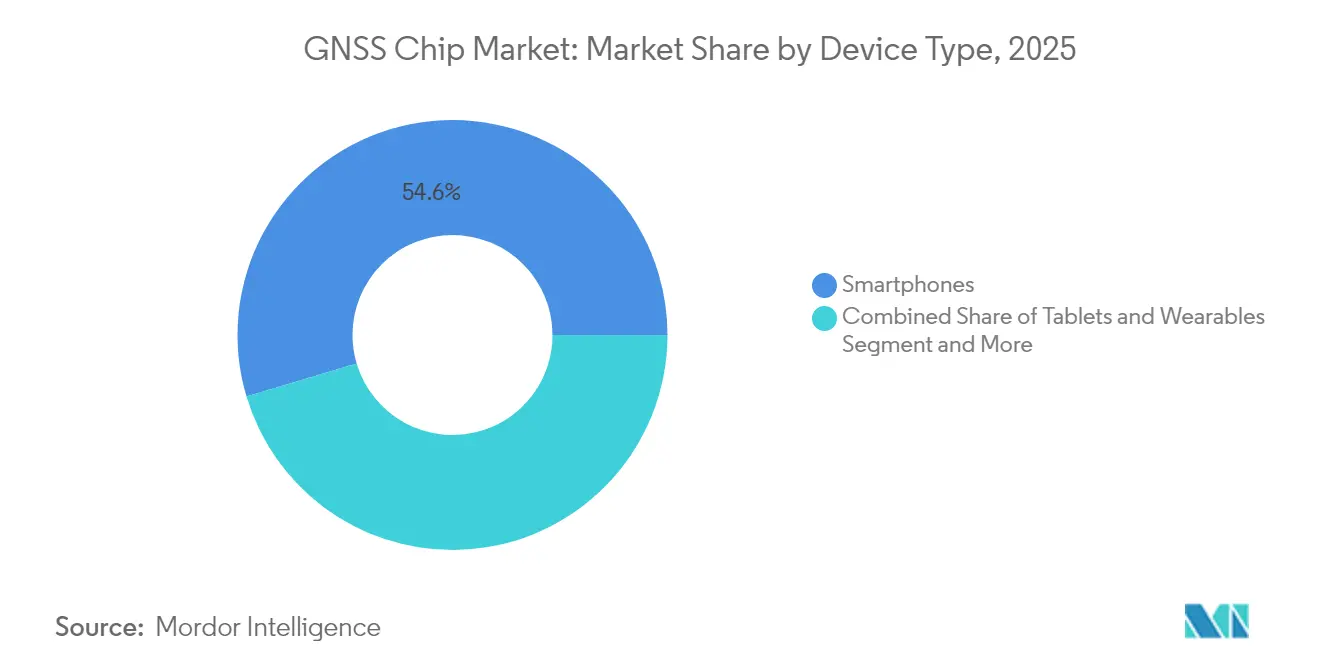

- By device type, smartphones held 54.62% of the GNSS chip market share in 2025; drones are projected to expand at a 7.55% CAGR through 2031.

- By frequency band, single-frequency L1 captured 66.45% of the GNSS chip market size in 2025; multi-frequency solutions are forecasted to post an 7.86% CAGR through 2031.

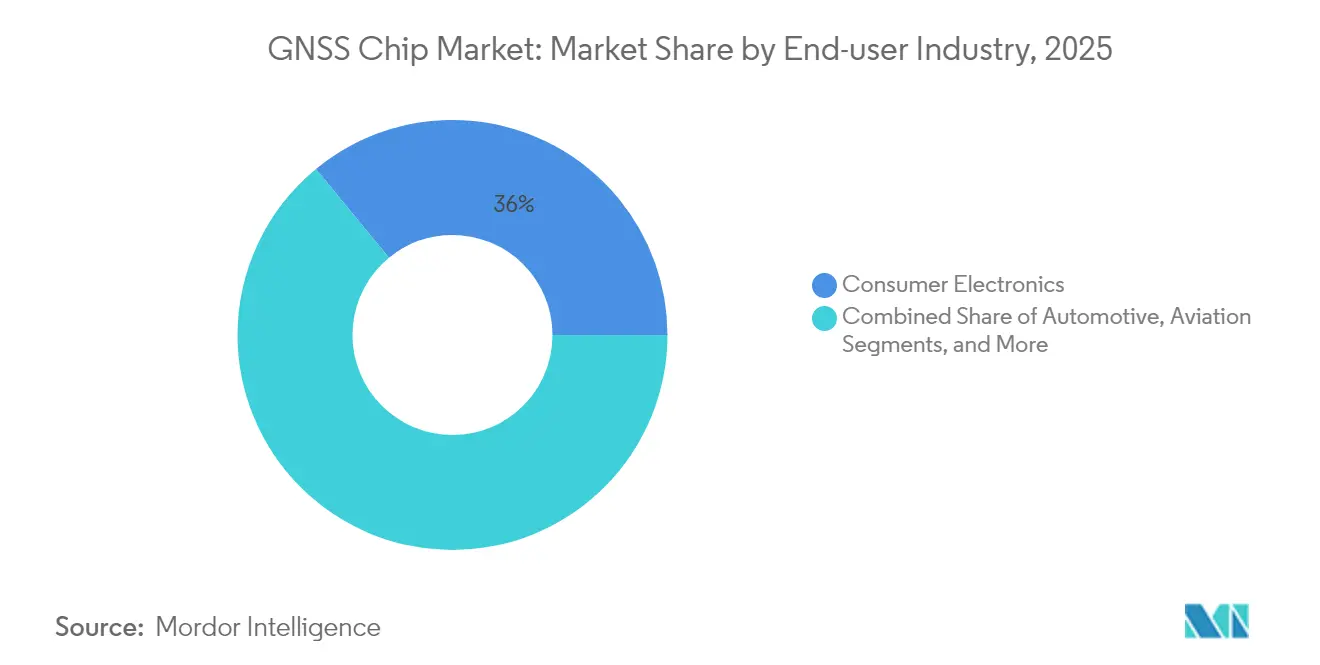

- By end-user industry, consumer electronics led with a 35.95% revenue share of the GNSS chip market in 2025; agriculture is projected to advance at a 7.48% CAGR through 2031.

- By application, navigation commanded 41.25% of the GNSS chip market size in 2025; timing and synchronization are growing at a 7.38% CAGR through 2031.

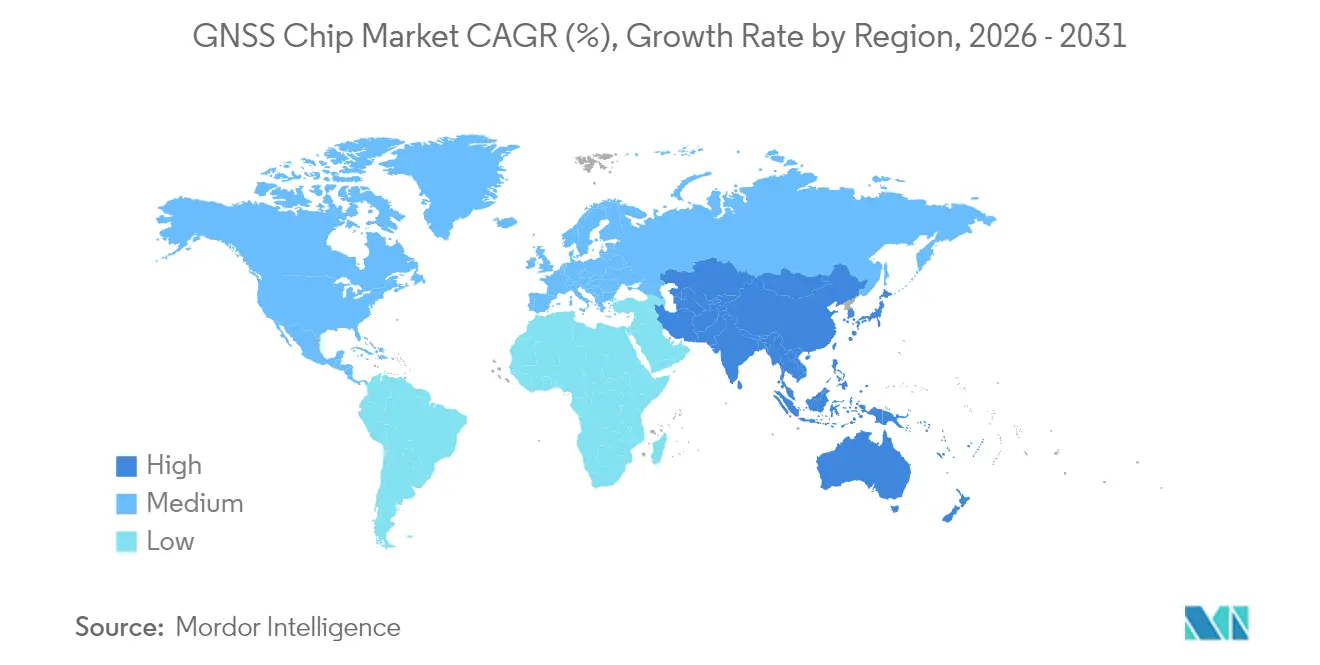

- By geography, the Asia-Pacific region accounted for a 42.10% revenue share of the GNSS chip market in 2025 and is projected to rise at a 6.33% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global GNSS Chip Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in multi-frequency GNSS smartphone shipments | +1.2% | Global, with APAC leading adoption | Medium term (2-4 years) |

| Rising ADAS and autonomous-driving precision needs | +0.9% | North America and EU, expanding to APAC | Long term (≥ 4 years) |

| Expansion of precision agriculture and logistics tracking | +0.8% | Global, with strong growth in Americas and APAC | Medium term (2-4 years) |

| Centimeter-level positioning for drone last-mile delivery | +0.6% | North America and EU initially, global expansion | Short term (≤ 2 years) |

| Miniaturized dual-band chips for medical wearables | +0.4% | Global, led by North America and Europe | Long term (≥ 4 years) |

| Sovereign constellation investments spurring local demand | +0.7% | APAC core, spill-over to MEA and Latin America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in Multi-frequency GNSS Smartphone Shipments

Premium handsets now integrate dual-band L1/L5 and even tri-band receivers, which enhance location accuracy from meters to decimeters, enabling reliable augmented-reality navigation in dense urban cores.[1]STMicroelectronics, “Teseo VI GNSS Receiver Family,” STMicroelectronics, st.com Flagship launches across China, South Korea, and the United States accelerate the refresh cycle because older single-frequency designs cannot support emerging indoor–outdoor continuity. Developers leverage the improved accuracy to enrich gaming, social-media tagging, and emergency-caller location services, which in turn sustains a high-volume pull for advanced chipsets inside the GNSS chip market.

Rising ADAS and Autonomous-Driving Precision Needs

Level 3 and higher autonomy demands consistent lane-level positioning, prompting automakers to pair multi-frequency GNSS with IMUs and vehicle-to-everything radios.[2]IEEE Standards Association, “IEEE Standards for Navigation and Positioning,” IEEE, ieee.org Survey-grade accuracy elevates silicon content per vehicle and justifies premium ASPs, while over-the-air software functions multiply recurring revenue potential for chip suppliers that offer firmware-upgradable navigation stacks.

Expansion of Precision Agriculture and Logistics Tracking

RTK-enabled farm machinery reduces seed overlap and fertilizer waste by up to 20%, and rugged asset trackers cut theft losses for high-value freight, together broadening the GNSS chip market beyond consumer devices.[3]NovAtel Inc., “Construction, Mining and Industrial Applications,” NovAtel, novatel.com Regional subsidies in the United States, Brazil and India sweeten growers’ return on investment and speed volume adoption of dual-band modules tolerant of dust, vibration and temperature extremes.

Centimeter-Level Positioning for Drone Last-mile Delivery

Pilot projects in the United States and Europe routinely achieve 5 cm landing accuracy by fusing RTK GNSS with visual odometry, unlocking fully automated parcel drop-off in suburban backyards.[4]General Dynamics Mission Systems, “GPS III Satellites,” gdmissionsystems.com Commercial scaling of such services amplifies the demand for lightweight, low-power, multi-frequency receivers that can coexist with cameras and LiDAR on battery-constrained airframes.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| GNSS vulnerability to jamming and spoofing | -0.8% | Global, concentrated in conflict zones and Eastern Europe | Short term (≤ 2 years) |

| High power draw of multi-constellation chipsets | -0.6% | Global, particularly affecting battery-powered devices | Medium term (2-4 years) |

| Advanced RF-front-end node supply constraints | -0.5% | Global, with acute impact in APAC manufacturing hubs | Short term (≤ 2 years) |

| Regulatory delays in L-band spectrum re-allocation | -0.3% | North America and EU primarily, with global implications | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

GNSS Vulnerability to Jamming and Spoofing

More than 1,000 interference incidents were reported by European aviation authorities in 2024, resulting in rerouting and in-flight system resets. Civil agencies now mandate multi-constellation reception, interference detection, and encrypted services, which inflate hardware costs and complicate certification timelines for GNSS chip market vendors.

High Power Draw of Multi-constellation Chipsets

Continuous tracking across four constellations raises the active current to 90–100 mW, five times higher than single-system designs, thereby reducing battery life in wearables and asset tags. Synaptics’ snapshot navigation architecture reduces average consumption by 80%, but trade-offs in reacquisition time persist, limiting its use to latency-tolerant workloads.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Type: Smartphone Volume Versus Drone Upside

Smartphones accounted for 54.62% of the GNSS chip market size in 2025, driven by the widespread adoption of location-based services in consumer devices, according to. Although shipment growth is maturing, dual-band upgrades sustain silicon value per handset, enabling suppliers to maintain their margins. Tablets, wearables, and personal trackers represent steady but lower-ASP outlets. In-vehicle systems post mid-single-digit growth as automakers embed navigation redundancy for ADAS.

Drones, with a modest base today, are forecasted to grow at a 7.55% CAGR and thus provide the fastest incremental revenue among device classes. Commercial inspection, delivery, and precision-spray agriculture collectively demand centimeter accuracy under strict weight and power budgets, creating a premium for compact multi-frequency receivers. Low-power asset trackers and specialty industrial devices round out niche demand with ruggedized requirements, reinforcing design diversity in the GNSS chip market.

By Frequency Band: L1 Dominance Amid Multi-Frequency Momentum

Cost-sensitive consumer electronics are expected to maintain a single-frequency L1 solution at 66.45% of the GNSS chip market share in 2025, solidifying their role as the entry-level option. However, urban-canyon multipath and ionospheric errors limit L1 performance, prompting automotive, surveying, and drone clients to adopt dual- or tri-band architectures.

Multi-frequency shipments are rising at an 7.86% CAGR, helped by falling filter prices and new quad-band single-die offerings that streamline board design. For many tier-one automotive platforms, dual-band L1/L5 is now a hard requirement, while aviation regulators move toward mandatory L5 for safety-critical navigation.

By End-user Industry: Consumer Electronics Scale, Agriculture Acceleration

Consumer electronics accounted for 35.95% of the GNSS chip market size in 2025, driven by the refresh cycles of smartphones and wearables. Price elasticity limits ASP increases, so vendors lean on integration with Wi-Fi and Bluetooth to stay competitive.

Agriculture is forecast to grow at a rate of 7.48% annually as RTK guidance and autonomous tractors enhance input efficiency. The segment values accuracy and robustness over die size, allowing higher margins. Automotive customers seek ISO 26262-qualified chips and secure update pipelines, which add complexity but offer longer program lifecycles. Defense and public safety niches demand anti-jam features and encrypted signals, underscoring the heterogeneous nature of the GNSS chip market.

By Application: Navigation Scale, Timing Upswing

Navigation remained the largest bucket at 41.25% of the GNSS chip market size in 2025. Its growth flattens but still absorbs vast L1 volumes. Positioning and mapping for surveying and BIM workflows retain loyal professional users willing to pay for centimeter precision and post-processing services.

Timing and synchronization are scaling at the fastest rate, with a 7.38% CAGR, because 5G macro and small-cell rollouts require sub-microsecond phase alignment. Power utilities and data centers replicate this demand as they modernize grid and server timing. Specialized timing receivers with oven-controlled oscillators command premiums and help diversify revenue beyond pure navigation.

Geography Analysis

Asia-Pacific held 42.10% of the GNSS chip market size in 2025, supported by China’s BeiDou build-out, high-volume smartphone assembly, and strong local demand for precision agriculture equipment. Government incentives for indigenous silicon, combined with the growing ecosystem around India’s NavIC and Japan’s QZSS, further accelerate regional uptake. Suppliers that certify full BeiDou and NavIC compliance gain preferred-vendor status, locking in design wins with OEMs across handsets and farm machinery.

North America contributes a stable share anchored in automotive ADAS, defense contracts, and large-scale 5G timing deployments. Federal procurement emphasizes resilience and encrypted M-code capability, prompting vendors to adopt anti-jam front-ends and SAASM compatibility. The region’s thriving drone-delivery pilots and Silicon Valley wearable brands maintain a technology leadership loop that keeps ASPs elevated despite lower unit volumes.

Europe prioritizes the adoption of Galileo dual-frequency in both aviation and road transport regulations. The 2024 spike in spoofing incidents over Eastern Europe accelerated airline retrofits with multi-constellation receivers. Meanwhile, South America, the Middle East and Africa adopt GNSS to bolster smart-city builds, mining automation and climate-smart farming. Brazil leverages precision soybean planting to defend its export competitiveness; Gulf countries embed GNSS into mega infrastructure projects; and pan-African mobile operators invest in 5G timing to leapfrog fixed networks, cumulatively enlarging the GNSS chip market.

Regulatory Landscape

GNSS chip commercialization is shaped by radio equipment, spectrum, and conformity regimes that increasingly intersect with cybersecurity and foreign-constellation access. In the European Union, the Radio Equipment Directive (RED) 2014/53/EU governs radio determination equipment and CE marking, and the European Commission has activated RED cybersecurity requirements (Articles 3.3 d, e, and f) for internet-connected radio products (referenced as activated in August 2025), pushing GNSS-enabled devices to incorporate security controls alongside RF performance compliance.

In the United States, FCC rules influence both device emissions and constellation operations. FCC Part 15 compliance remains central for GNSS-enabled digital devices, while the FCC also manages non-US constellation operations under its satellite licensing framework. In March 2026, the FCC adopted a Notice of Inquiry (FCC 25-20) examining national PNT data security and foreign GNSS provider market access requirements, and in May 2026 the FCC issued Order DA 26-525 introducing provider certification requirements tied to authorizations for use of non-US GNSS signals. In China, standardization is also tightening: GB/T 47326-2026 for BeiDou/GNSS broadband RF chip performance and testing is cited as implemented in July 2026, adding a country-specific testing and performance anchor for suppliers targeting BeiDou-enabled designs.

Value Chain Analysis

The GNSS chip value chain starts with GNSS baseband and RF front-end IP development, then moves through wafer fabrication, packaging and test. It continues with module design, where GNSS is commonly paired with filters, oscillators, and antennas, before OEM integration into smartphones, vehicles, drones, industrial trackers, and timing equipment. High-volume consumer deployments are typically driven by integrated mobile SoCs (such as Qualcomm and MediaTek) that bundle GNSS with cellular and Wi-Fi, while industrial and automotive programs more often use discrete or specialized GNSS chipsets and modules from suppliers such as STMicroelectronics and u-blox, followed by correction services (RTK/PPP) and application software.

Partnerships and manufacturing moves point to where value concentrates. Trimble and STMicroelectronics (March 2025) combined Trimble ProPoint Go with ST Teseo VI to deliver an integrated positioning stack for automotive and IoT, and Swift Navigation with Sony Semiconductor Solutions (November 2024) paired Swift Skylark Precise Positioning Service with a Sony GNSS chipset, reflecting a shift from standalone silicon toward silicon plus software plus correction services. On the supply side, a sovereignty-driven example emerged in June 2026 when GlobalFoundries and Qualinx completed an end-to-end, fully European manufacturing flow for a GNSS SoC and analog front end at GlobalFoundries Dresden using FDX technology, addressing a known dependency where advanced manufacturing and final packaging are still concentrated in Asia for many GNSS-related components.

Competitive Landscape

The GNSS chip market is moderately consolidated: Qualcomm, MediaTek, and Broadcom collectively dominate consumer-grade volumes, while u-blox, STMicroelectronics, and Trimble capture precision niches. Smartphone SoCs from Qualcomm and MediaTek embed GNSS alongside cellular and Wi-Fi, securing multi-year design slots with handset OEMs. Their integration prowess pressures discrete receiver vendors on price, but also leaves performance gaps that specialists can exploit.

u-blox, Septentrio, and Unicore focus on multi-band, multi-constellation parts tuned for centimeter-level accuracy. STMicroelectronics’ Teseo VI quad-band die pairs low power with survey-grade performance, making inroads in automotive Telematics Control Units. Trimble leverages its software ecosystem to bundle receivers with correction services for construction and agriculture.

Strategic moves in 2024-25 include u-blox and Topcon’s joint service, which fuses hardware with RTK network subscriptions. Additionally, Quectel’s LG580P module extends Broadcom silicon into industrial IoT, and Synaptics launches the ultra-low-power SYN4778 for wearables. Supply-chain resilience has become a key procurement criterion, prompting handset OEMs to dual-source across Taiwanese and European fabs.

GNSS Chip Industry Leaders

Qualcomm Technologies, Inc.

Mediatek Inc.

STMicroelectronics N.V.

Broadcom Corporation

Intel Corporation

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Assured and authenticated positioning is creating design space for GNSS chip vendors beyond baseline navigation, particularly in applications exposed to jamming, spoofing, and multipath. A clear commercialization signal arrived in July 2026, when Iridium Communications announced commercial availability of its Iridium PNT ASIC aimed at protecting GNSS-dependent devices from interference, indicating a productized market for resilient PNT silicon alongside conventional receivers. Integration around authentication is also moving closer to the receiver, with Qualinx disclosing Galileo OSNMA support for its QLX3Gx series (June 2026), reflecting demand from safety- and liability-sensitive sectors seeking proof-of-origin signals and tighter security postures in GNSS-enabled devices.

Regionalized supply and platformization are another white-space area, where hardware, software, and manufacturing footprints are packaged to meet procurement requirements in automotive, infrastructure timing, and government-linked programs. The June 2026 completion of a fully European GNSS SoC manufacturing flow by GlobalFoundries and Qualinx at Dresden provides a visible sourcing pathway for suppliers targeting Europe-based supply, while software-defined performance upgrades are becoming a differentiator in degraded environments. For example, Focal Point Positioning and STMicroelectronics entered a commercial agreement (July 2026) to apply S-GNSS Auto software on ST Teseo V and Teseo VI devices to enhance automotive positioning reliability without requiring a full hardware redesign, aligning with OEM needs for multi-constellation robustness and maintainable positioning stacks across long vehicle program lifecycles.

Recent Industry Developments

- July 2026: Iridium Communications announced commercial availability of its Iridium PNT ASIC designed to protect GNSS-dependent devices from jamming and spoofing. The move productizes resilient PNT at the chip level for device makers that need interference-tolerant positioning and timing beyond conventional GNSS-only designs.

- August 2025: Qualcomm announced Snapdragon W5+ Gen 2 and W5 Gen 2 wearable platforms with integrated NB-NTN satellite support. Satellite-aware connectivity in wearables increases the strategic value of highly efficient GNSS reception and power management in compact platforms where location and messaging functions share tight battery budgets.

- February 2025: STMicroelectronics released the Teseo VI family as a single-die quad-band GNSS receiver targeting automotive and industrial applications. By consolidating multi-band capability into a monolithic design, the launch supports higher-accuracy positioning and simplifies integration for OEMs seeking robust GNSS performance in challenging RF environments.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the GNSS chip market includes revenue generated from GNSS receiver chipsets and modules that enable positioning, navigation, and timing functions across consumer and industrial devices, covering major constellations and frequency bands.

Scope exclusions: We exclude GNSS-enabled end devices and services (such as navigation apps, mapping subscriptions, and installation labor) and only count the chip and module hardware value.

Segmentation Overview

- By Device Type

- Smartphones

- Tablets and Wearables

- Personal Tracking Devices

- Low-power Asset Trackers

- In-vehicle Systems

- Drones

- Other Device Types

- By Frequency Band

- Single-frequency L1

- Dual-frequency L1/L5

- Dual-frequency L1/L2

- Multi-frequency (Tri-band and above)

- By End-user Industry

- Automotive

- Consumer Electronics

- Aviation

- Agriculture

- Construction and Mining

- Defense and Public Safety

- Other End-users

- By Application

- Navigation

- Positioning and Mapping

- Timing and Synchronization

- Remote Sensing

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Rest of Europe

- Asia-Pacific

- China

- Japan

- South Korea

- India

- Rest of Asia-Pacific

- Middle East

- Saudi Arabia

- United Arab Emirates

- Rest of Middle East

- Africa

- South Africa

- Rest of Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work started by building a clean fact base on GNSS deployments, device categories, and semiconductor shipment signals, then mapping those into demand pools for GNSS-capable hardware. Public sources used in this step typically include government spectrum and telecom releases such as the FCC, satellite navigation program updates such as the U.S. GPS program office and the European Union Agency for the Space Program, and standards bodies such as 3GPP for timing related requirements.

We also reviewed non-paywalled technical and usage indicators from sources such as ITU publications, customs and trade statistics for electronics categories, and peer-reviewed journals that discuss multi-frequency adoption and interference resilience. Company filings, investor presentations, product briefs, and reputable press were used to ground ASP direction and product mix shifts across smartphones, vehicles, and industrial trackers. Where needed, paid company financials and an intelligence subscription, a patent database, and an import-export shipment-level database were used to confirm revenue splits and validate shipment intensity. These examples are not exhaustive, and other public and paid sources were also used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on verifying what actually drives GNSS chip revenue, typically the mix of single-frequency versus dual and multi-frequency designs, the share of integrated solutions, and how quickly new designs move into high volume devices. We spoke with a broad set of participants across the value chain, including chip designers, module makers, device OEM teams, and downstream integrators, and we covered APAC, EMEA, and the Americas so regional demand patterns and pricing differences were not missed.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 25% | CXOs: 12% | APAC: 38% |

| Mid tier: 57% | Functional/Unit leaders: 39% | EMEA: 37% |

| Smaller Players: 18% | Managers: 49% | Americas: 25% |

Market-Sizing & Forecasting

Sizing was built using a top-down approach where device shipment categories and attach rates were used to reconstruct GNSS chip demand, then price and mix assumptions were applied to translate units into revenue. The model tracks practical inputs such as smartphone and wearable volumes, in-vehicle GNSS penetration, tracker and telematics device shipments, the share of dual and multi-frequency chipsets, and observed ASP movement as integration rises.

Once the demand pool was formed, selective bottom-up checks were used to keep totals realistic, including supplier roll-ups from sampled product lines, channel checks on module pricing, and ASP times volume cross-checks for large device clusters. When gaps existed for smaller industrial uses, conservative proxies were applied using adjacent device categories and then adjusted after expert feedback.

For forecasting, scenario analysis was used, since adoption of multi-frequency designs and automotive content per vehicle can shift faster than a smooth trend line suggests. Assumptions were stress-tested using interview inputs on design win cycles, replacement timing, regulatory pushes for resilient timing, and regional manufacturing shifts, before the final set of year-by-year values was locked.

Data Validation & Update Cycle

Outputs were cross-checked against independent signals like device shipment direction, disclosed semiconductor revenue trends, and the pace of GNSS feature upgrades in mainstream devices, then any inconsistencies were reviewed and corrected. Large variances triggered a second pass on input logic, followed by targeted re-contact with industry participants to confirm whether the change reflected reality or an assumption error.

Before sign-off, the model and its assumptions are reviewed in multiple steps by analysts so arithmetic, unit consistency, and currency handling are aligned across regions. The report is refreshed annually, and interim updates are made when material events occur, such as major constellation policy changes or sharp pricing shifts. Right before delivery, a final update sweep is completed so clients receive the most current view available.

Mordor Intelligence's Gnss Chip Market Size Measured Against Other Published Estimates

It is common to see different market sizes for GNSS chips because each publisher draws the line differently between chips, modules, and GNSS-enabled devices, and they also choose different base years and pricing assumptions. Timing also matters, since exchange rates, handset cycles, and automotive build schedules can move the number even when long-term demand stays intact.

In our checks, the biggest spread usually comes from whether multi-year device shipment pools are mapped into chip revenue using realistic attach rates and frequency-band mix, or whether broader GNSS-enabled hardware gets included by default. Some estimates also lean on aggressive ASP progression or longer forecast windows without enough validation on how quickly dual and multi-frequency designs become standard. This separation is kept explicit in the model used by Mordor Intelligence.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 8.84 B (2026) | |

| Industry Publisher A | USD 5.27 B (2024) | Uses an earlier base year and a broader mix of segment definitions, and the smaller value suggests either narrower inclusion of modules or more conservative attach rate and ASP assumptions for high-volume devices. |

| Trade Brief B | USD 5.83 B (2024) | Quotes a nearer-term figure but provides limited clarity on whether pricing is tied to chipset-only revenue versus blended device-level value, and the long-range projection shown appears inconsistent with typical GNSS chip ASP and adoption patterns. |

Overall, the table shows that the gap is driven less by one single growth rate and more by what is counted as chip revenue, how attach rates are applied across device pools, and how ASP changes are handled as integration rises. By keeping these inputs visible and testable, the resulting number is easier to replicate and adjust when new shipment or mix signals emerge.

Key Questions Answered in the Report

How large is the GNSS chip market in 2026?

The GNSS chip market size stands at USD 8.84 billion in 2026 and is set to reach USD 11.58 billion by 2031.

Which device category leads GNSS chip demand?

Smartphones account for 54.62% of 2025 revenue, reflecting their ubiquity and the steady rollout of dual-band positioning features.

What is the fastest-growing GNSS application?

Timing & synchronization is expanding at a 7.38% CAGR as 5G networks and power utilities seek sub-microsecond accuracy.

Which region shows the highest growth?

Asia-Pacific leads in both share and momentum, rising at a 6.33% CAGR on the back of BeiDou expansion and OEM manufacturing scale.

Why are multi-frequency chips gaining popularity?

Dual- and tri-band receivers overcome urban multipath errors and deliver centimeter-level accuracy vital for drones, ADAS and precision farming.

What are the main risks facing GNSS adoption?

Jamming, spoofing, and high power consumption add cost and design complexity, prompting investments in anti-jam hardware and low-power architectures.

Page last updated on: