Gluten-Free Beer Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 228.97 Million |

| Market Size (2031) | USD 449.16 Million |

| Growth Rate (2026 - 2031) | 14.42% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Gluten-Free Beer Market Analysis by Mordor Intelligence

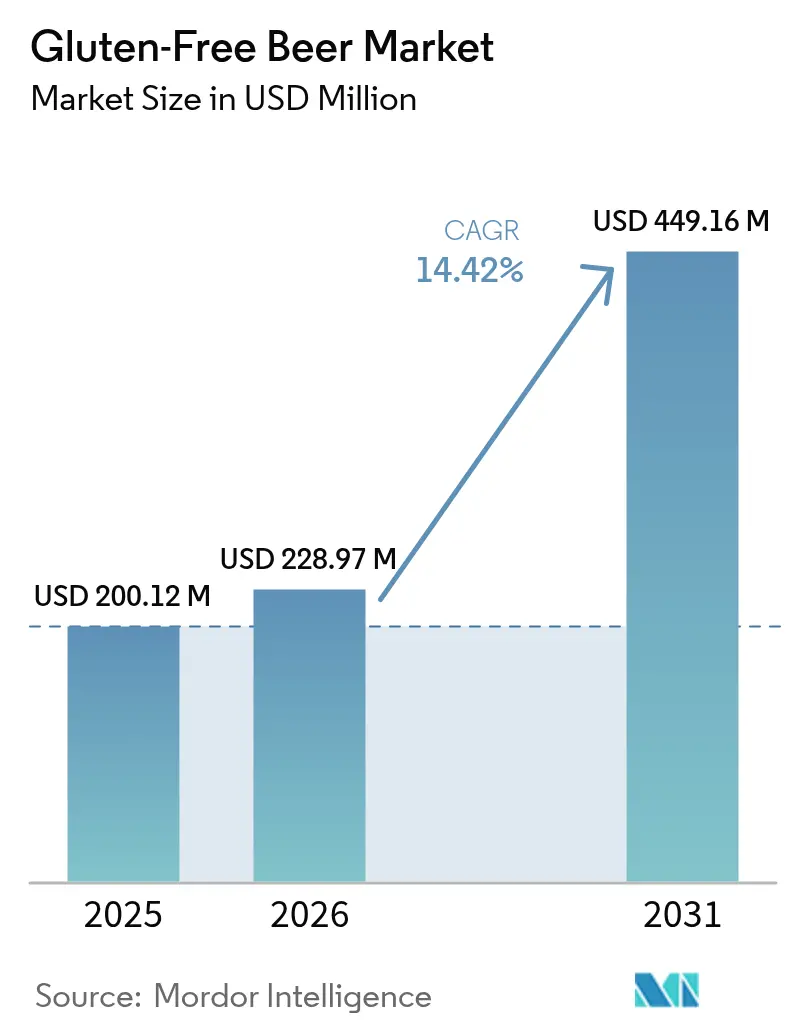

The gluten-free beer market size was valued at USD 200.12 million in 2025 and estimated to grow from USD 228.97 million in 2026 to reach USD 449.16 million by 2031, at a CAGR of 14.42% during the forecast period (2026-2031). This surge is largely driven by an uptick in celiac disease diagnoses, the establishment of clear U.S. labeling rules under TTB Ruling 2020-2, and a growing consumer shift towards health-oriented, clean-label alcoholic beverages. As reported by the Ministero della Salute, Italy had around 265,000 diagnosed celiac disease cases in 2023[1]Source: Ministero della Salute, "Relazione annuale al Parlamento sulla celiachia - Anno 2023", static.celiachia.it. Ingredient diversification, a premium craft positioning, and the rising accessibility of e-commerce further fuel the market's momentum. Stability in sorghum and corn supplies helps buffer against fluctuations in input costs. While dedicated gluten-free breweries ramp up production, mainstream brewers are introducing specialized lines, both groups leveraging new enzyme processing and alternative-grain malting technologies to achieve traditional beer taste profiles. This has led to a moderate competitive intensity in the market. Moreover, regulatory alignment across North America, Europe, and the pivotal Asia Pacific regions is fostering investment, spurring innovation, and facilitating cross-border brand growth.

Key Report Takeaways

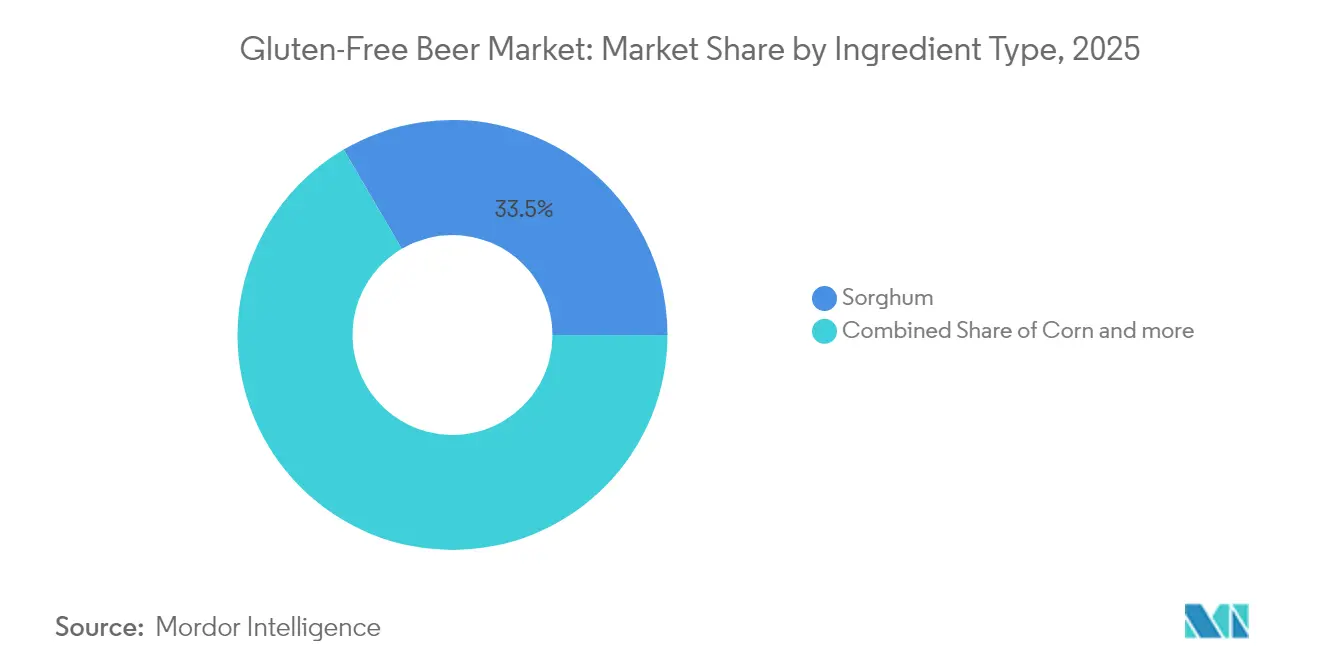

- By ingredient, sorghum led with 33.45% of gluten-free beer market share in 2025, while corn is poised to post a 15.55% CAGR through 2031.

- By product type, lager accounted for 67.10% of the gluten-free beer market size in 2025, and ale is projected to expand at a 15.89% CAGR over 2026-2031.

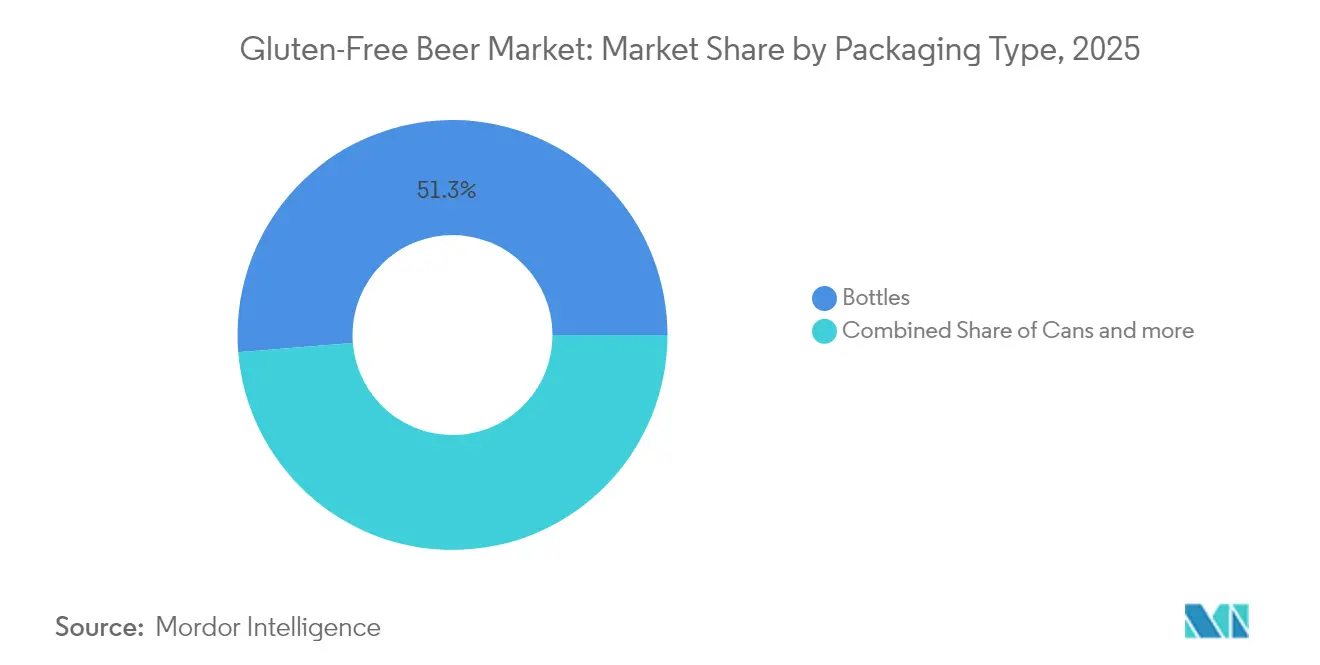

- By packaging, bottles retained a 51.28% revenue share in 2025, while cans are projected to advance at a 16.09% CAGR to 2031.

- By distribution, on-trade held a 59.10% share in 2025, whereas off-trade channels are forecast to rise at a 17.32% CAGR through 2031.

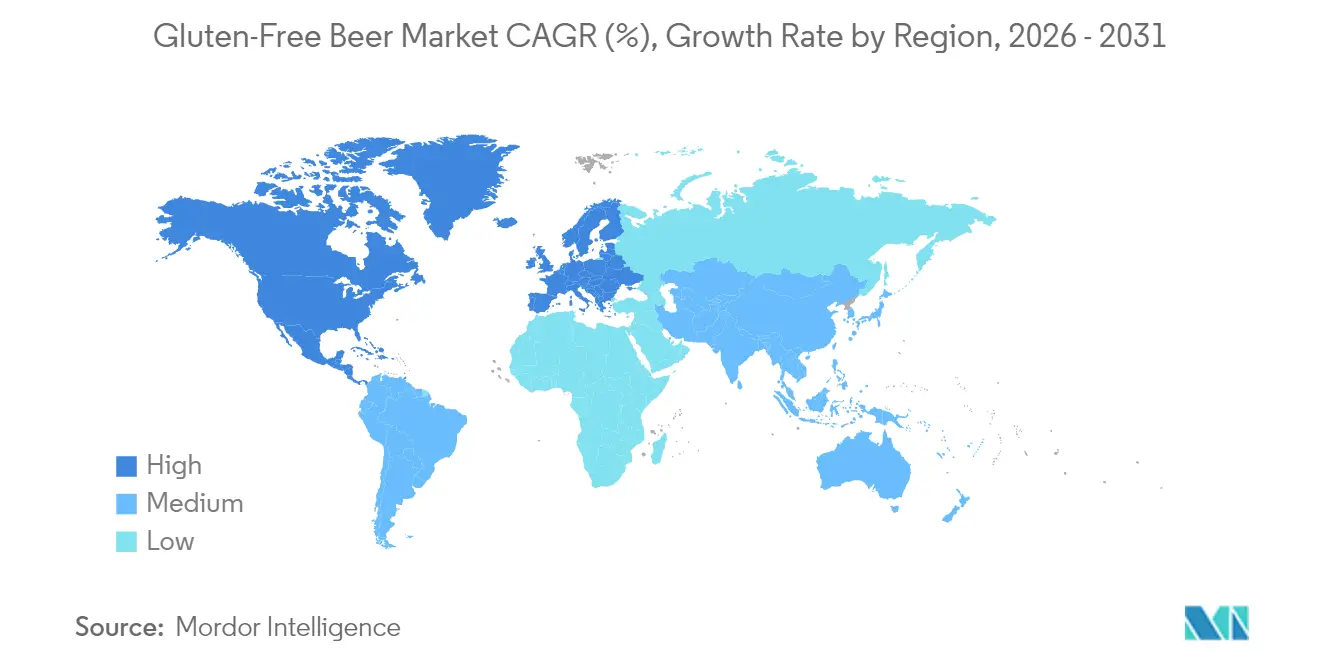

- By region, North America dominated with a 40.05% share in 2025, while the Asia Pacific is expected to grow at a 15.62% CAGR during the outlook period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Gluten-Free Beer Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising diagnosis of celiac disease and gluten sensitivity | +2.8% | Global, with higher impact in North America and Europe | Medium term (2-4 years) |

| Expansion and innovation in product variety | +2.1% | Global, concentrated in developed markets | Short term (≤ 2 years) |

| Technological advancements in brewing | +1.9% | North America and Europe, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Shift toward premium and craft offerings | +2.3% | North America, Europe, Australia | Medium term (2-4 years) |

| Demand for clean-label and natural ingredients | +1.7% | Global, led by North America and Europe | Short term (≤ 2 years) |

| The rise of the no-and-low alcohol segment | +1.4% | Global, strongest in Europe and North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Diagnosis of Celiac Disease and Gluten Sensitivity

Rising consumer health awareness, enhanced diagnosis of gluten-related conditions, improved product quality, and supportive regulatory standards are fueling the surging demand for gluten-free beers. A key driver is the heightened awareness and diagnosis of celiac disease, a serious autoimmune disorder triggered by gluten, with a global prevalence hovering around 1%. Organizations like the Celiac Disease Foundation are at the forefront, championing improved diagnosis and visibility. They host events such as Celiac Awareness Month in May 2025 and Celiac Strong Day on May 16, 2025, to enlighten patients, schools, and communities. Concurrently, a growing number of individuals are embracing gluten-free lifestyles, not just for celiac concerns but for general wellness, citing perceived health benefits and a shift towards healthier dietary choices. This backdrop has ignited notable product innovations in the gluten-free beer sector. For example, in 2024, South African brewery Darling Brew enriched its Break Free gluten-free line with a new Red Ale, crafted from naturally gluten-free ingredients. In May 2025, Japanese brewery Rice Hack unveiled the Oryvia range, a collection of rice-based, gluten-free, and allergen-free beers, with the Miyabi variant as its centerpiece. These strides, coupled with broader market trends and heightened accessibility via online retail, underscore that the demand for gluten-free beer has evolved from a niche interest to a burgeoning global market, shaped by shifting consumer preferences and proactive industry initiatives.

Expansion and Innovation in Product Variety

Product diversification strategies are transforming gluten-free beer from a mere medical necessity into a trendy lifestyle choice, broadening its market appeal beyond those diagnosed with gluten sensitivities. Collaborative brewing efforts underscore this shift. For instance, Ghostfish Brewing collaborated with Deschutes Brewery to craft a limited-edition West Coast Pilsner, utilizing premium gluten-free malts and experimental hops, and showcasing advanced craft brewing methods tailored for gluten-free formulations. On the international front, Kati Patang's strategic move in January 2025 to acquire a 23% stake in the UK's Chadlington Brewery underscores the trend. This partnership aims to produce the gluten-free Saffron Lager, highlighting how blending flavor innovation with cultural nuances can effectively penetrate new markets. Research into alternative grains is not just enhancing product quality but also making them more cost-competitive. For example, studies on rice malt reveal that its production costs are only 17-20% higher than those of barley malt, yet it boasts superior brewing capabilities compared to rice adjuncts. Innovations in enzyme technology, such as DSM-Firmenich's Brewers Clarex – a staple in one in five beers globally – are revolutionizing gluten reduction processes. This advancement broadens production avenues for established breweries. Furthermore, the expansion in variety introduces diverse price points and flavor profiles, enticing consumers who once shied away from gluten-free options due to limited choices or concerns over quality.

Technological Advancements in Brewing

Brewing technology has evolved to tackle the challenge of crafting gluten-free beer that rivals the taste, texture, and shelf stability of its traditional counterpart. Investments in cross-contamination prevention systems are vital, with the Master Brewers Association of the Americas offering HACCP guidance tailored for allergen control and specialized production protocols. Gluten-free production faces heightened microbiological control challenges, given the unique fermentation traits of alternative grains and the lack of traditional antimicrobial compounds present in barley. Technologies such as sterile sampling systems at critical control points facilitate real-time monitoring, ensuring production integrity and preventing contamination. Malting processes for alternative grains, such as rice, necessitate specialized equipment and longer processing times. While these extended steeping, germination, and kilning cycles complicate operations, they produce self-saccharifying malts rich in free amino nitrogen. Despite advancements in analytical testing to meet regulatory standards, both TTB and FDA concede the absence of a scientifically valid method to quantify gluten in fermented products, posing persistent hurdles for process validation and labeling.

Shift Toward Premium and Craft Offerings

Premium positioning strategies capitalize on consumers' willingness to pay a premium for specialized products that cater to specific dietary needs, while offering an enhanced taste experience. The merger of Fort Point Beer Co. and HenHouse Brewing Co. in April 2025 resulted in Northern California's fifth-largest craft brewery, with an annual production of 40,000 barrels, underscoring the scale needed for sustainable craft operations. Trends in the Asia Pacific region, which are leaning towards premiumization, are bolstering the gluten-free positioning. This shift is driven by consumers' eagerness to discover craft brands and their willingness to pay more for distinctive offerings. With around 964 brewers, California alone boasts a significant presence in the U.S. craft beer market, as highlighted by the Brewers Association, paving the way for distribution opportunities for premium gluten-free brands[2]Source: Brewers Association, "State Craft Beer Sales & Production Statistics, 2024", brewersassociation.org. Bellfield Brewery, recognized as the UK's first entirely gluten-free brewery, exemplifies successful premium positioning. Their focus on quality, accolades, and gradual entry into major supermarket chains, such as Aldi, Morrisons, and Asda, underscores their strategy. This premium approach not only counters the inherent cost challenges of gluten-free production but also fosters brand loyalty among consumers who perceive gluten-free beer as a lifestyle choice rather than merely a dietary necessity.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Sustained competition from traditional beers | -1.8% | Global, strongest in price-sensitive markets | Long term (≥ 4 years) |

| Supply chain disruptions and limited raw material availability | -1.2% | Global, concentrated in grain-dependent regions | Short term (≤ 2 years) |

| Cross-contamination risk and dedicated facilities | -0.9% | Global, higher impact in shared facility markets | Medium term (2-4 years) |

| Inconsistent regulatory frameworks and labeling confusion | -0.7% | Global, varying by jurisdiction complexity | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Sustained Competition from Traditional Beers

Traditional beer's stronghold in the market, bolstered by cost advantages, consistently hampers the penetration of gluten-free beer, confining its appeal largely to medically driven consumers. In 2023, Czechia led Europe in beer consumption, with an impressive 128 liters per capita, as reported by the Brewers of Europe. Notably, Czechia stood alone, being the only nation to surpass the 100-liter mark that year. Concurrently, the Beverage Information Group highlighted a staggering consumption of approximately 2.65 billion cases (each equivalent to 2.25 gallons) of beer in 2023. Major brewers, including Anheuser-Busch, showcased the dominance of traditional beer production. They adjusted contract terms multiple times and scaled back contracted acres for 2024, responding to an oversupply of malting barley, an outcome of robust crops and waning beer demand. In India, the beer market is projected to grow by 10%, reaching 450 million cases in 2024-25. With three dominant brewers accounting for 85% of sales, this underscores the distribution advantages and economies of scale that traditional beer enjoys, which gluten-free alternatives struggle to replicate. While research indicates younger consumers are leaning towards seltzers and mixed drinks over traditional beer, this shift favors non-beer alternatives broadly, rather than specifically propelling gluten-free beer into the limelight. The challenge amplifies in price-sensitive markets, where consumers, unless medically inclined, gravitate towards the more affordable traditional options, curtailing the market's expansion beyond the core audience of celiac and gluten-sensitive individuals.

Supply Chain Disruptions and Limited Raw Material Availability

Gluten-free beer producers grapple with cost pressures and availability risks due to the volatility and capacity constraints of alternative grain supply chains. The International Trade Centre reports that Bulgaria's grain sorghum exports saw a significant decline in value of EUR 87 thousand (-31.52%) from the previous year, highlighting vulnerabilities in the sorghum market dynamics[3]Source: International Trade Centre, "Value of grain sorghum exported from Bulgaria", trademap.org. An analysis of rice malt production shows it commands a 17-20% cost premium over barley malt. The processing of rice malt is intricate, involving longer steeping, germination, and kilning times, which not only reduce throughput but also inflate fixed costs per unit. While the corn market offers some stability, with USDA forecasting a supply of 16,907 million bushels at USD 4.40 per bushel for 2024/25, global forecasts for coarse grains production were trimmed by 1.4 million tons, primarily due to a dip in barley output. Limitations in specialized malting infrastructure hinder the processing capacity for alternative grains. Most malting facilities, tailored for barley, need extensive modifications to accommodate sorghum, millet, or rice. Furthermore, transportation and logistics costs for these alternative grains surge due to their smaller volumes and specialized handling requirements, especially when compared to the established barley supply chains. This scenario intensifies cost pressures for gluten-free beer producers, who find it challenging to match the economies of scale enjoyed by traditional brewers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Ingredient Type: Sorghum Dominance Faces Corn Challenge

In 2025, sorghum holds a dominant 33.45% market share, solidifying its status as the go-to gluten-free grain for brewing, thanks to its superior fermentation properties and neutral flavor profile. Meanwhile, corn is making waves as the fastest-growing ingredient, boasting a 15.55% CAGR from 2026 to 2031, thanks to its cost benefits and dependable supply chain. The USDA forecasts a steady corn supply of 16,907 million bushels for the 2024/25 period, priced at a predictable USD 4.40 per bushel, making it an attractive option for budget-conscious producers. Millet, although a smaller player, is gaining traction due to its nutritional benefits and traditional brewing significance in certain areas. Other ingredients, like buckwheat and quinoa, are carving out niche markets with premium strategies.

Research on rice malt highlights its versatility, noting that while its production costs are 17-20% higher than those of barley malt, its self-saccharifying trait eliminates the need for added enzymes. In 2024, sorghum faced supply chain challenges, with U.S. exports lagging behind as China dominated, accounting for 87% of global imports, underscoring the geopolitical risks associated with availability and pricing. The ingredient market mirrors larger agricultural patterns: rice yields 2-3 times more per hectare than barley, suggesting a potential 50-67% reduction in acreage for the same extract output. Under the Food Safety Modernization Act, the FDA mandates ingredient traceability and prevention of cross-contact, benefiting suppliers with specialized gluten-free facilities and certified supply chains.

By Product Type: Lager Leadership Challenged by Ale Innovation

In 2025, Lager holds a commanding 67.10% market share, leveraging both consumer familiarity and established brewing processes that have been adeptly adapted for gluten-free methods. Ale, on the other hand, is on a robust growth path, boasting a 15.89% CAGR from 2026 to 2031. This surge is largely attributed to craft brewing innovations and flavor experiments that resonate with premium-seeking consumers. A testament to this evolution is the collaboration between Ghostfish Brewing and Deschutes Brewery, which produced a limited-edition West Coast Pilsner. Such partnerships demonstrate the seamless integration of traditional craft techniques into gluten-free formulations, while upholding stringent quality standards. Meanwhile, other beer varieties, like stouts, porters, and seasonal specialties, are carving out niches, presenting avenues for product differentiation and premium market positioning.

International flavor innovations hint at a broader potential for product type expansion. For instance, Kati Patang's gluten-free Saffron Lager melds Indian flavors with British brewing traditions, thanks to strategic production partnerships in the UK. The ale segment's upward trajectory mirrors the wider craft beer movement's tilt towards hop-centric profiles and avant-garde ingredients. However, producers face challenges, notably the TTB's labeling mandates. While health claims are off-limits, accurate ingredient declarations are allowed. Furthermore, enzyme technologies, like DSM-Firmenich's Brewers Clarex, are making waves. Used in one out of every five beers globally, these technologies facilitate gluten reduction, broadening lager production avenues for breweries without specialized gluten-free setups. As breweries diversify their product types, they must strike a balance: meeting consumer expectations for traditional beer styles while seizing opportunities for innovation. This delicate dance is crucial, especially when justifying the premium pricing that often accompanies gluten-free brewing's heightened production costs.

By Packaging Type: Bottles Lead While Cans Accelerate

In 2025, traditional bottle packaging commands a 51.28% market share, underscoring consumer preferences for premium presentation and established ties with on-premise venues. Meanwhile, cans are surging ahead, boasting a robust 16.09% CAGR growth rate projected from 2026 to 2031. This surge is largely attributed to the convenience of cans, their enhanced barrier properties, and their alignment with the premiumization trends in the craft beer market. The industry's pivot towards cans isn't just a trend; it's a strategic move. Canned formats offer superior shelf stability and transportation efficiency. This is especially crucial for gluten-free products, which have distinct storage needs compared to their traditional counterparts. Additionally, while kegs cater to on-premise services and specialty bottles target premium positioning, these formats address specific market segments with tailored value propositions.

As sustainability takes center stage, packaging choices are evolving. Aluminum cans, with their superior recyclability, are becoming the preferred choice. They not only outshine glass bottles in recyclability but also offer enhanced protection against light and oxygen. This is a significant advantage for maintaining the stability of gluten-free beers. The shift in packaging aligns seamlessly with distribution channel trends. Off-trade channels, witnessing a 17.32% growth, are gravitating towards cans, valuing their retail convenience and ease of inventory management. In Japan, there's a distinct preference for smaller, visually appealing packaging and portion-specific sizes. This opens doors for specialized packaging formats that resonate with regional consumer behaviors. While TTB labeling requirements are uniform across all packaging formats, the constraints of labeling space necessitate meticulous design. It's essential to balance mandatory gluten-free claims and qualifying statements with brand visibility and consumer appeal.

By Distribution Channel: On-Trade Strength Meets Off-Trade Growth

In 2025, on-trade channels command a 59.10% market share, underscoring the pivotal role of restaurants, bars, and taprooms in promoting gluten-free beers and educating consumers. Meanwhile, off-trade channels are on a growth trajectory, boasting a 17.32% CAGR from 2026 to 2031. This surge is fueled by the rise of specialty retail, the embrace of e-commerce, and the expansion of supermarket categories. Within off-trade channels, specialty and liquor stores play a crucial role, providing premium gluten-free brands with essential market access. Their knowledgeable staff and curated selections enhance consumer discovery and encourage product trials. Additionally, supermarkets, convenience stores, and online platforms broaden accessibility, making it easier for regular consumers to purchase gluten-free beers.

In Australia, distribution dynamics pose challenges. Major distributors, which hold about 85% of the market share, create hurdles for smaller gluten-free producers seeking retail visibility. Conversely, Japan's distribution scene offers a mixed bag. Convenience stores, boasting an 18% market share and round-the-clock accessibility, present golden opportunities for gluten-free beer trials and spur-of-the-moment purchases. However, the intricate multi-layered distribution systems necessitate collaborations with local partners. E-commerce emerges as a game-changer, offering niche dietary products a straightforward entry. These platforms facilitate direct-to-consumer sales, sidestepping traditional distribution hurdles while simultaneously amplifying brand visibility. This shift in channels mirrors evolving consumer shopping habits. Demand for specialty dietary products, especially gluten-free ones, is outpacing traditional retail growth, presenting a lucrative avenue for brands adept at harnessing digital marketing and efficient fulfillment strategies.

Geography Analysis

In 2025, North America captured 40.05% of the gluten-free beer market share, driven by heightened awareness initiatives for celiac disease and stringent labeling mandates following the TTB Ruling 2020-2. U.S. surveys confirm a 0.75% prevalence of celiac disease, ensuring steady demand. National grocery chains now feature dedicated gluten-free sections, and with a surge in e-commerce alcohol sales, off-trade growth has been bolstered. Canada, benefiting from streamlined import processes due to aligned Health Canada thresholds, is witnessing a similar trend.

The Asia Pacific is poised to lead the gluten-free beer market, with a projected 15.62% CAGR through 2031. Japan's expansive food and beverage sector is embracing specialty diets, with urban-centric convenience stores and online grocers highlighting gluten-free products. China's premium beer market's growth indicates a readiness to invest in unique labels, paving the way for the import of gluten-free products. Meanwhile, India's government aims to achieve USD 1 billion in alcoholic-beverage exports by 2030, encouraging local breweries to develop gluten-free options that cater to both the diaspora and domestic health-conscious consumers.

Europe, while mature, remains pivotal, bolstered by the AOECS “Crossed Grain” symbol that fosters consumer confidence. In the U.K., Italy, and Spain, dedicated gluten-free breweries are partnering with supermarket chains, maintaining stable volumes amidst fierce shelf competition. Germany's Reinheitsgebot revisions now embrace alternative-grain beers, broadening domestic production. Though Eastern Europe is slower to adopt, major retailers are introducing private-label gluten-free products, signaling growth.

In South America, Brazil's craft-beer surge is experimenting with sorghum-based lagers targeting health-savvy millennials. ANVISA's regulatory alignment with EU ppm standards is easing import processes for U.S. and European brands. The Middle East and Africa, still in its infancy, sees premium off-trade sales buoyed by duty-free and specialty retailers in Gulf expatriate hubs. As awareness initiatives expand, these burgeoning markets offer a fresh revenue stream, diversifying income from the fiercely competitive Western landscape.

Competitive Landscape

The gluten-free beer market is moderately fragmented, with dedicated specialty breweries, enzyme-enabled entrants, and conglomerate sub-brands vying for dominance through taste parity, distribution, and certification. Holidaily Brewing, boasting the largest dedicated gluten-free facility in the U.S., employs closed-loop grain handling to prevent cross-contact and enjoys strong regional loyalty. Similarly, Bellfield Brewery in the U.K. employs a single-site strategy, leveraging award accolades to secure shelf space at Aldi, Morrisons, and Asda, while scaling its volume and upholding certification standards.

Mainstream brewers are tapping into the gluten-free trend through specialized labels. Anheuser-Busch's Redbridge enjoys nationwide distribution, thanks to strategic partnerships with multi-state wholesalers that ensure its presence in chain stores. Meanwhile, Heineken's Spanish division promotes Ambar Gluten-Free, emphasizing its cross-site gluten removal method that aligns with EU labeling standards. Enzyme technology is broadening the playing field; breweries are adopting Brewer’s Clarex, enabling them to introduce gluten-reduced SKUs without the hefty costs of segregation. However, some regions impose labeling restrictions, preventing the use of “gluten-free” terminology.

Craft supply dynamics are shifting due to consolidation: Tilray Brands, in a series of deals wrapping up between August and September 2024, brought four Molson Coors breweries, along with Terrapin and Revolver, into its fold. This move catapults Tilray to the rank of the fifth-largest craft producer in the U.S., amplifying its beer distribution to 15 million cases. The merger between Fort Point and HenHouse, pooling their 40,000-barrel capacity, underscores the industry's trend towards scale, as they channel resources into research and development and self-distribution across the state. Cross-border collaborations, like Kati Patang's investment in Chadlington Brewery, are not just about capital; they seamlessly weave emerging-market brands into established retail frameworks, all while infusing gluten-free expertise into the local operations.

Competitive dynamics are influenced by supermarket shelf fees, the costs of acquiring online customers, and the cycles of certification audits. Producers who can clinch third-party gluten-free certifications and deliver appealing sensory profiles stand poised to seize a larger slice of the market as global awareness of the category grows.

Gluten-Free Beer Industry Leaders

-

Anheuser-Busch InBev

-

Bard's Brewing LLC

-

Ghostfish Brewing Company

-

Lakefront Brewery Inc.

-

New Belgium Brewing Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Japanese brewery Rice Hack, led by Yasuo Michiguchi, launched a five-variety range of gluten- and allergen-free rice-based beers called Oryvia. The first variety, Miyabi, was released in May 2025 and aims to closely mimic the classic hop flavor of traditional beer.

- December 2024: Prime Drink Group announced the resolution of production issues that had plagued its renowned Glutenberg beer line for several months. By December 2024, the company had resumed production at near-normal levels and began fulfilling large orders for its best-selling Blonde and IPA varieties. This expansion aimed to meet increasing consumer demand in Canada and the U.S. and return the brand to full market presence in 2025.

- October 2024: Darling Brew expanded its portfolio with a Red Ale crafted for gluten-intolerant consumers. This ale distinguishes itself with a complex flavor profile that includes malty sweetness, a spicy hop character, and a fruity aroma. The launch was strategically timed to align with a major cycling event, the Darling Brew Extreme 2025, using the marketing slogan to celebrate both the beer and the outdoor event.

- May 2024: In a collaboration with Deschutes Brewery, Ghostfish launched a limited-release, gluten-free West Coast Pilsner. This launch involved in-person release events at both breweries and was distributed throughout the Western U.S. The partnership was notable for demonstrating the ability of specialty brewers to team up with mainstream craft brewers, with Ghostfish taking the opportunity to refine its techniques for gluten-free brewing.

Global Gluten-Free Beer Market Report Scope

Gluten-free beer is crafted from gluten-free ingredients like millet, rice, sorghum, buckwheat, or corn, steering clear of traditional wheat or barley.

The global gluten-free beer market is categorized by ingredient type, beer type, and distribution channel. Ingredient-wise, the market includes corn, sorghum, millet, and others. In terms of beer type, offerings include ale, lager, and more. Distribution channels are divided into on-trade and off-trade stores. Off-trade stores further break down into online stores, liquor outlets, and supermarkets/hypermarkets, among others. The study also delves into the gluten-free beer landscape in both emerging and established markets worldwide, spanning North America, Europe, Asia-Pacific, South America, and the Middle East & Africa.

The report provides market size and forecasts in USD for each segment.

| Corn |

| Sorghum |

| Millet |

| Others |

| Ale |

| Lager |

| Other Beer Types |

| Bottles |

| Cans |

| Others |

| On-Trade | |

| Off-Trade | Specialty/Liquor Stores |

| Other Off-Trade Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| South Africa | |

| Rest of Middle East and Africa |

| By Ingredient Type | Corn | |

| Sorghum | ||

| Millet | ||

| Others | ||

| By Product Type | Ale | |

| Lager | ||

| Other Beer Types | ||

| By Packaging Type | Bottles | |

| Cans | ||

| Others | ||

| By Distribution Channel | On-Trade | |

| Off-Trade | Specialty/Liquor Stores | |

| Other Off-Trade Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

Which regions lead demand for gluten-free beer?

North America currently holds a 40.05% share, driven by strong celiac awareness and clear labeling rules.

What ingredient is most used in gluten-free beer production?

Sorghum leads with a 33.45% share, though corn is the fastest-growing grain at a 15.55% CAGR.

How fast is Asia Pacific’s consumption expanding?

Asia Pacific is projected to log a 15.62% CAGR through 2031, the quickest worldwide.

Which packaging format is gaining ground fastest?

Cans are rising at a 16.09% CAGR, favored for portability and recyclability.

Are mainstream brewers active in this space?

Yes, Anheuser-Busch markets Redbridge and Tilray’s 2024 acquisitions position it among the top U.S. craft players.

What is the main regulatory hurdle for producers?

Maintaining <20 ppm gluten and documenting cross-contact controls to satisfy FDA and TTB rules.

Page last updated on: