Contrast Media Injectors Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

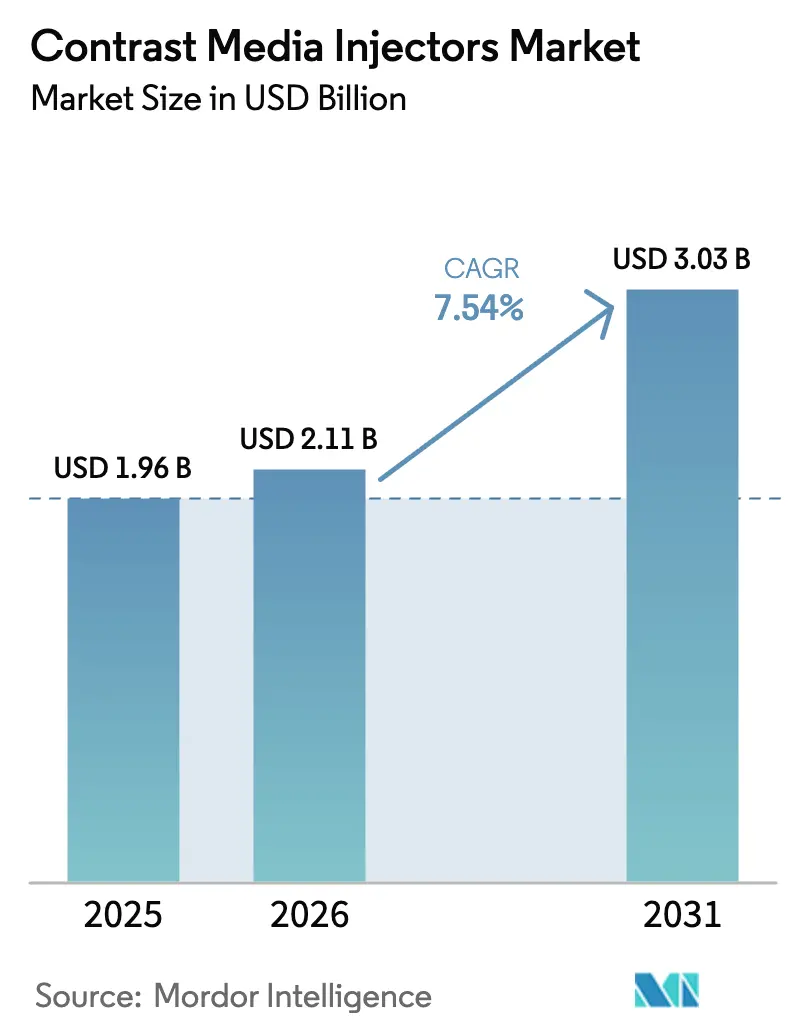

| Market Size (2026) | USD 2.11 Billion |

| Market Size (2031) | USD 3.03 Billion |

| Growth Rate (2026 - 2031) | 7.54% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Contrast Media Injectors Market Analysis by Mordor Intelligence

The Contrast Media Injectors Market size is expected to grow from USD 1.96 billion in 2025 to USD 2.11 billion in 2026 and is forecast to reach USD 3.03 billion by 2031 at 7.54% CAGR over 2026-2031.

Rapid automation of contrast delivery, mandatory dose-tracking features, and the first wave of FDA-cleared AI injection protocols are steadily replacing manual techniques and older single-head systems. Hospitals are refreshing fleets to align with infection-control guidelines, while vendors emphasize consumable tie-ins that lock customers into multiyear service contracts. Syringeless and dual-head platforms are becoming the default in mobile stroke units and interventional suites, where space constraints and workflow precision matter most. On the competitive front, the top five suppliers control a sizable installed base, yet regional challengers continue to win price-sensitive accounts through localized service and flexible financing.

Key Report Takeaways

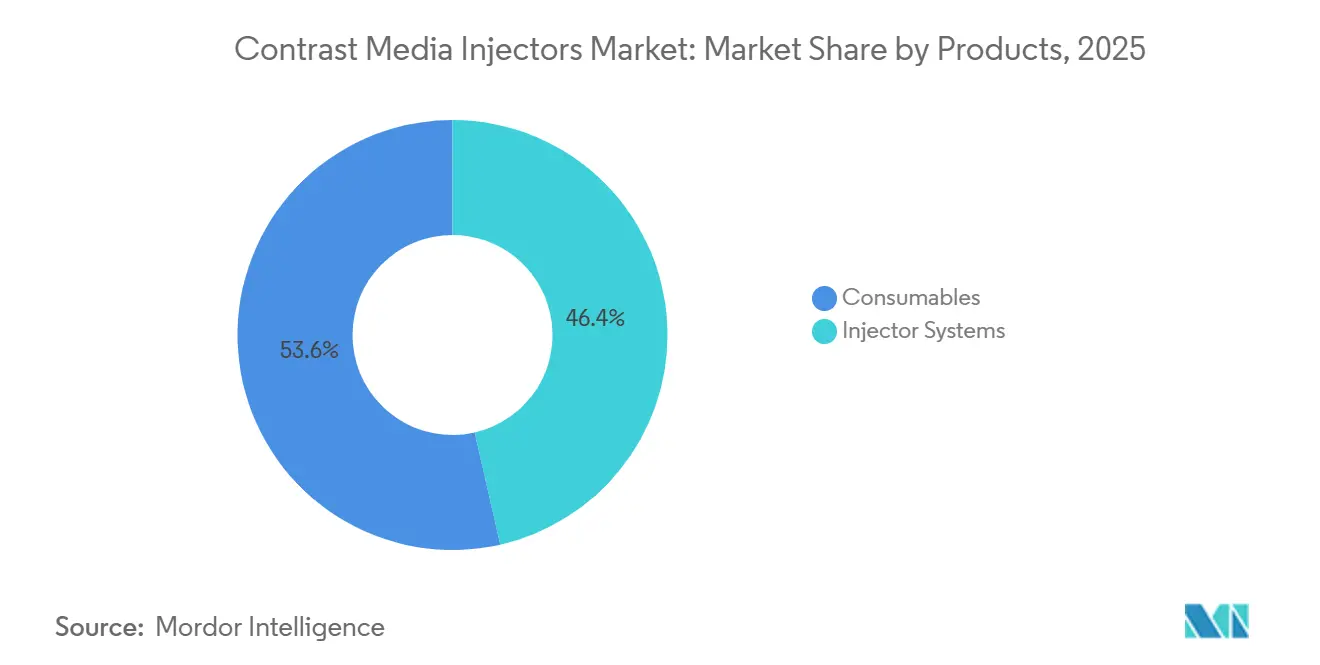

- By product category, consumables captured 53.56% revenue share in 2025, while injector systems are forecast to expand at an 8.25% CAGR through 2031.

- By injector type, single-head platforms represented 45.53% of the contrast media injectors market share in 2025, whereas syringeless designs are advancing at a 10.85% CAGR to 2031.

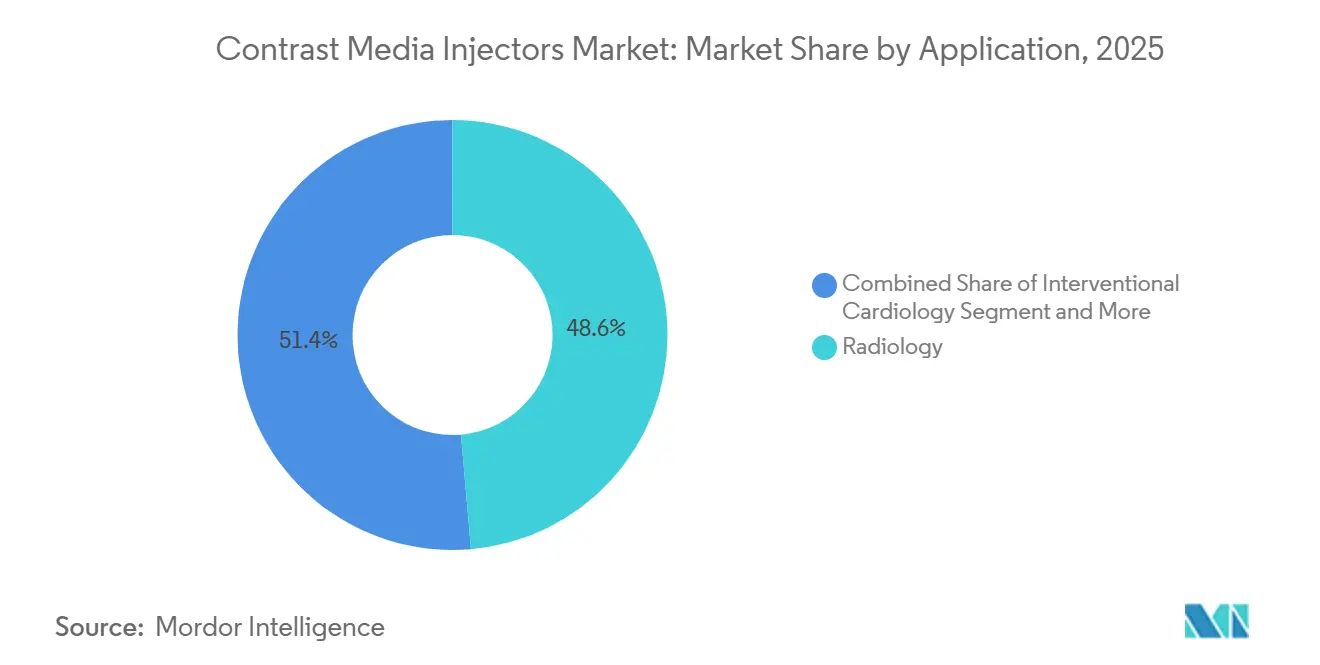

- By application, radiology held 48.63% of demand in 2025, and interventional cardiology is projected to grow at a 9.87% CAGR through 2031.

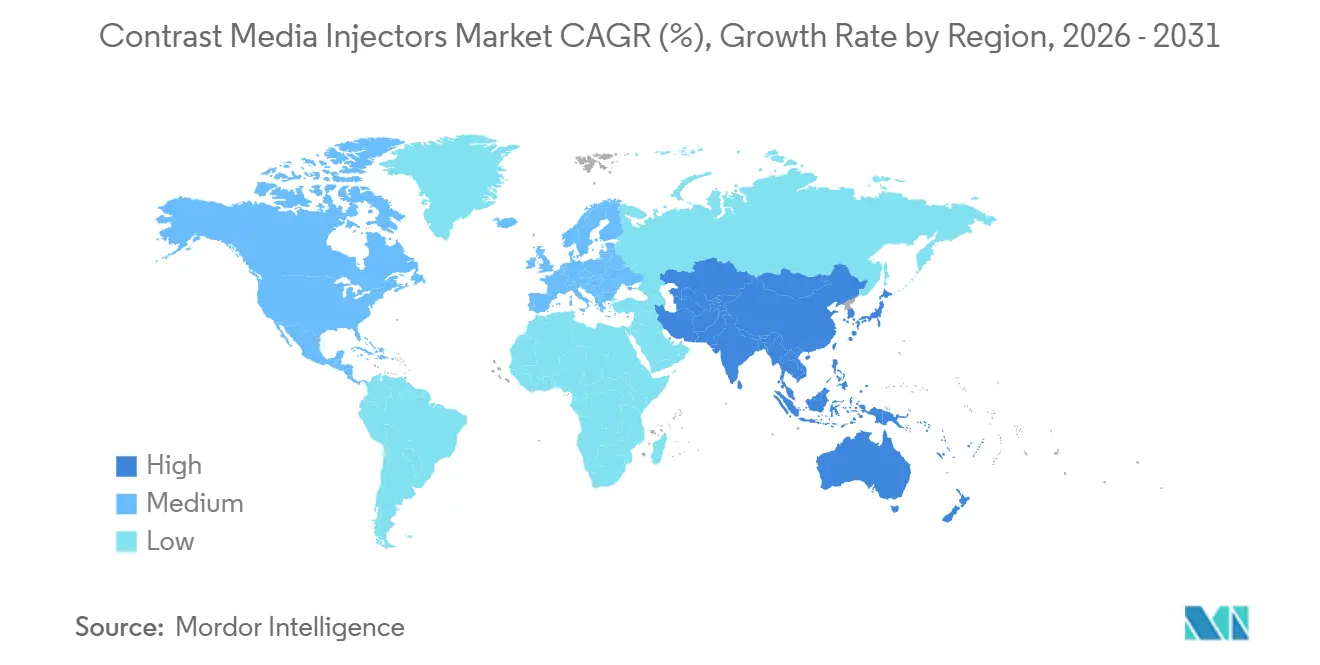

- By geography, North America accounted for 36.13% of 2025 revenue, yet Asia-Pacific is poised for a 9.51% CAGR that will narrow the gap by 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Market Trends and Insights

Drivers Impact Analysis of Contrast Media Injectors Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for minimally invasive diagnostic and interventional procedures | +2.1% | Global, highest in North America and Western Europe | Medium term (2-4 years) |

| Rapid CT/MRI installation growth in mid-income hospitals | +1.8% | Core Asia-Pacific, spill-over to Middle East and Latin America | Long term (≥4 years) |

| Regulatory push for contrast-dose tracking and safety automation | +1.3% | North America and EU, early adoption in Australia | Short term (≤2 years) |

| AI-powered injection protocols improving workflow and reducing waste | +1.0% | Global, led by U.S., Germany, and Japan | Medium term (2-4 years) |

| Emergence of value-based outpatient imaging chains | +0.7% | North America, growing in Western Europe | Medium term (2-4 years) |

| Growing adoption of dual- and syringeless systems in mobile stroke and cath labs | +0.6% | North America and EU for stroke units, Asia-Pacific for cath labs | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Minimally Invasive Diagnostic and Interventional Procedures

Real-time imaging now underpins CT-guided biopsies, valve replacements, and neuro-thrombectomies, each of which requires precise bolus timing that only automated injectors can deliver. NHS England logged 46.6 million diagnostic studies in 2024, including 7.65 million contrast-enhanced CT scans that overwhelmingly used power injectors. Updated cardiology guidelines published in 2024 recommend using the lowest feasible iodine volume, a standard achievable only with systems able to meter sub-milliliter flow. Dual-head injectors have been shown to cut cath-lab procedure time by close to 15% by eliminating manual syringe swaps[1]American College of Radiology, “ACR Manual on Contrast Media 2024,” acr.org. Vendors that synchronize injector parameters with scanner protocols through HL7 interfaces are well-positioned, because smaller manufacturers struggle to replicate this software depth. Taken together, procedure growth and workflow complexity safeguard demand for next-generation platforms across the contrast media injectors market.

Rapid CT/MRI Installation Growth in Mid-Income Hospitals

China, India, and Southeast Asia are buying high-slice CT and 3-Tesla MRI scanners at an unprecedented pace, and injector purchases are typically bundled into each scanner deal. Wipro GE Healthcare committed INR 8,000 crore (USD 960 million) in 2024 to scale Indian manufacturing aimed at tier-2 and tier-3 cities, where scanner density sits below two units per 100,000 residents. These hospitals are more price-sensitive than their metropolitan peers, so they favor basic single-head models but on volumes large enough to lift overall market value. Government stimulus programs that subsidize scanner acquisitions often overlook injectors, prompting vendors to create flexible leasing or pay-per-procedure plans. As mid-income facilities expand advanced imaging capacity, the pull-through effect materially lifts the contrast media injectors market.

Regulatory Push for Contrast-Dose Tracking and Safety Automation

The FDA continues to integrate contrast-dose reporting into certified electronic health records, effectively making auto-documentation a must-have feature. The American College of Radiology’s 2024 Manual on Contrast Media reaffirmed the safety of iodinated agents in patients whose eGFR is at least 45 mL/min/1.73 m², but it simultaneously advocated for dose-monitoring to curb unnecessary repeat exposure. European enforcement of the Medical Device Regulation, updated in 2024 to include granular post-market surveillance for Class IIb devices, has raised compliance costs and squeezed smaller vendors. Hospitals therefore lean toward trusted brands with proven quality systems and bidirectional HL7 connectivity that feeds dose, flow, and pressure data directly into patient charts. These requirements favor the current leaders in the contrast media injectors market.

AI-Powered Injection Protocols Improving Workflow and Reducing Waste

Bracco’s AiMIFY software, cleared by the FDA in October 2024, uses deep-learning reconstruction to double contrast conspicuity, allowing radiologists to cut iodine doses by as much as 50% while preserving image quality. Philips documented a 22% reduction in wasted contrast across a 12-hospital U.S. network after deploying CT Smart Workflow in 2025. Guerbet followed in June 2025 with Contrast&Care 2.0, a cloud engine that tailors injection settings to patient weight and renal function. These AI tools compress consumable revenue but lengthen existing contrast inventories, indirectly insulating hospitals from supply shocks. As academic centers demonstrate clinical equivalence at lower dose, community hospitals will adopt the same algorithms, reinforcing AI as a structural driver within the contrast media injectors market.

Restraints Impact Analysis of Contrast Media Injectors Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital cost of advanced multi-head systems | -1.2% | Global, acute in emerging markets and smaller community hospitals | Medium term (2-4 years) |

| Adverse events and nephrotoxicity concerns around contrast use | -0.9% | Global, higher scrutiny in North America and EU | Long term (≥4 years) |

| Supply-chain volatility for single-use tubing and syringes | -0.8% | Global, disruptive in North America and EU | Short term (≤2 years) |

| Regional reimbursement caps on consumables | -0.7% | Australia, U.S. Medicare, parts of Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Capital Cost of Advanced Multi-Head Systems

Dual-head and syringeless injectors are priced 40-60% above single-head models, putting them beyond the reach of many public hospitals and small outpatient facilities. Bracco’s Max 3 syringeless MR injector, FDA-cleared in December 2024, costs USD 80,000–100,000 per unit, a figure that only high-volume centers can amortize. Australia’s 2024-25 federal budget funded MRI scanners but left injector purchases to local capital budgets, forcing radiology departments to prioritize essential imaging hardware over ancillary systems. CFOs still recovering from pandemic-era supply shocks continue to defer large equipment outlays. This headwind tempers near-term growth for premium platforms within the contrast media injectors market.

Adverse Events and Nephrotoxicity Concerns Around Contrast Use

While the 2024 ACR Manual reported negligible risk of contrast-induced kidney injury in patients with adequate renal function, medicolegal anxiety persists. A 2024 BMC Nephrology meta-analysis found AKI incidence ranging from 11% to 40% among select high-risk cohorts. Japan’s 2024 guidelines confirmed zero cases of nephrogenic systemic fibrosis with group II gadolinium agents even in dialysis patients. However, lingering perceptions from earlier formulations cause some clinicians to over-screen and occasionally defer indicated imaging. Vendors now embed eGFR checks and auto-dose reduction in software, which adds cost and complexity that smaller firms struggle to match.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Contrast Media Injectors Market Segment Analysis

By Products:

Consumables Anchor Recurring Revenue, Systems Drive InnovationConsumables commanded 53.56% of revenue in 2025, an outcome that underscores the large installed base still reliant on single-use tubing and syringes. Bayer’s Centargo platform, cleared in late 2024, uses a multi-patient reservoir that reduces per-scan disposable expense by close to 30%, a saving that high-volume centers see immediately. Injector systems are forecast to grow at an 8.25% CAGR through 2031 as hospitals refresh fleets to gain AI integration, dose-tracking, and wireless connectivity. CT injectors remain the largest sub-segment because CT generates more contrast studies than MR, though higher-field MRI installations are lifting demand for MR-conditional power injectors. The consumables stream is being squeezed by syringeless technology and AI-based dose reduction, but infection-control protocols still obligate single-use tubing, ensuring stable if slower growth for disposable lines within the contrast media injectors market size.

Consumable revenue is increasingly tied to service bundles in which hospitals sign multiyear deals that lock in tubing prices in exchange for discounted maintenance. Bracco’s 2024 investment to triple capacity at its Geneva ultrasound-contrast site signals confidence that volume gains will outpace per-unit dose declines. The bifurcation is clear: premium injectors with low consumable intensity appeal to research hospitals, while budget systems with higher disposable consumption continue to dominate community settings, sustaining a balanced revenue mix across the contrast media injectors market.

By Type of Injectors:

Syringeless Platforms Disrupt Traditional ArchitecturesSingle-head injectors represented 45.53% of the contrast media injectors market share in 2025, a testament to their entrenched position across routine CT and MRI rooms. Syringeless systems, however, are projected to progress at a 10.85% CAGR to 2031 on the strength of mobile stroke units and infection-control mandates. Bracco’s wireless Max 3, cleared by the FDA in December 2024, eliminates disposable syringes and trims setup time by roughly 40%. Dual-head injectors cater to interventional suites where rapid contrast-saline cycling is mandatory; studies published in 2024 showed procedure-time reductions of around 15% in busy cath labs.

China’s price-conscious hospitals still take a single-head first approach, though rising labor costs are sharpening interest in workflow-friendly dual-head options. Syringeless designs have found a niche in ambulatory settings because technologists can preload multiple doses without breaking sterile fields, a benefit highlighted by the 2024 JAMA Neurology evaluation of ambulance-based CT scanners. The convergence of workflow efficiency and infection control will keep syringeless units at the forefront of innovation, even as the legacy installed base anchors single-head volumes across the contrast media injectors market.

By Application:

Interventional Cardiology Outpaces Radiology GrowthRadiology carried 48.63% of demand in 2025, reflecting the high volume of oncologic and neurologic CT and MR studies. Nonetheless, interventional cardiology is set to expand at a 9.87% CAGR through 2031 as percutaneous coronary interventions rise and transcatheter valve therapies become mainstream. National Audit of PCI data for 2024 recorded more than 100,000 coronary interventions in the United Kingdom, each requiring precise bolus delivery that automated injectors provide[2]National Institute for Cardiovascular Outcomes Research, “PCI Audit 2024,” nicor.org.uk . Dual-head systems are standardizing in these labs because immediate saline flushing cuts iodine burden and reduces nephropathy risk.

Radiology growth is tempering as AI-optimized protocols lower per-study contrast volumes by up to 50%, a capability validated by Bracco’s AiMIFY clearance in 2024. Interventional radiology and neuro-thrombectomy segments trail cardiology on absolute size but are advancing at mid-single-digit rates as minimally invasive therapies replace surgery. Collectively, the shift toward complex vascular procedures is nudging the application mix toward high-specification injectors, reinforcing premium demand across the contrast media injectors market size.

Geography Analysis

North America Contrast Media Injectors Market

North America maintained 36.13% of global revenue in 2025, supported by more than 40,000 CT and 13,000 MR scanners in the United States alone. Early adoption of AI injection software and syringeless hardware drives replacement demand, while payer incentives push providers to document every dose. Yet volume growth has plateaued as mature hospitals prioritize utilization over expansion.

APAC Contrast Media Injectors Market

Asia-Pacific is forecast to post a 9.51% CAGR through 2031 as China, India, Indonesia, and Vietnam expand public hospital networks. Wipro GE’s 2024 investment underscores the scale of upcoming installations; injector sales typically track scanner shipments with a one-for-one ratio in mid-income facilities. Siemens Healthineers reported 8.2% organic growth in Asia-Pacific excluding China for fiscal 2024, confirming robust demand for imaging infrastructure[3]Siemens Healthineers, “Annual Report 2024,” siemens-healthineers.com. These conditions will sustain strong unit growth for the contrast media injectors market throughout the region.

EMEA, Oceania and South America Contrast Media Injectors Market

Europe remains sizable but slow growing, constrained by budget caps and longer equipment replacement cycles. Australia’s 2024 decision to trim CT fees by 2% evidences cost containment, compelling providers to seek injectors with lower consumable costs. The Middle East and parts of Africa continue to buy premium systems for medical-tourism hubs, while currency depreciation in South America inflates capital costs and lengthens replacement intervals. Divergent regional economics obligate suppliers to maintain dual portfolios that span entry-level single-heads and premium syringeless designs, a strategy that underpins global resilience of the contrast media injectors market.

Regulatory Landscape

In the United States, automatic contrast media injectors are regulated by the FDA as Class II devices under 21 CFR 870.1650 (product code IZQ), and market entry typically requires a 510(k) clearance. This framework focuses on predicate-based safety enhancements and compatibility with imaging workflows, rather than wholesale device redesigns.

In Europe, MDR 2017/745 governs conformity assessment for contrast injectors and raises expectations for clinical evidence and post-market surveillance. MDR Article 117 adds an additional Notified Body assessment for devices used with drug-device combination workflows when paired with contrast media, which increases the importance of aligning technical files and risk documentation early. Across regions, design verification and risk management follow ISO 11608 guidance for injection systems to support broader adoption of electronically controlled and software-enabled injectors.

Competitive Landscape

Bayer, GE Healthcare, Siemens Healthineers, and Bracco together supply a significant percentage of installed injector capacity, translating to moderate concentration. Bayer’s Centargo platform, cleared by the FDA in November 2024, surpassed 7 million patient uses across 49 countries by mid-2025 and recently gained single-dose vial clearance that broadens contrast options. Bracco differentiated its hardware with AiMIFY software, an FDA-cleared algorithm that halves iodine dose without losing lesion conspicuity, generating a new license revenue stream atop equipment sales.

Regional specialists such as Nemoto Kyorindo in Japan and ulrich medical in Germany win contracts where service proximity and 20-30% price discounts outweigh AI features. Chinese manufacturers are steadily improving quality yet lack the deep R&D resources needed for advanced software integrations demanded by academic centers. Siemens leveraged its EUR 22 billion revenue base to certify multiple injector generations under the updated European MDR framework, a hurdle that has already squeezed smaller European competitors.

Technology remains the chief battleground. Guerbet’s cloud-based Contrast&Care 2.0, launched in June 2025, personalizes injection settings to patient renal profiles, reducing extravasation events. Philips demonstrated 22% contrast savings with CT Smart Workflow in 2025, positioning itself as a value-added software partner even without a proprietary injector line. As hospitals adopt enterprise imaging strategies that favor integrated hardware-software ecosystems, multinationals with wider product stacks will consolidate their position in the contrast media injectors market.

Contrast Media Injectors Industry Leaders

GE Healthcare (GE Company)

Bracco Group

Bayer AG

Medtron AG

Ulrich GmbH & Co. KG

- *Disclaimer: Major Players sorted in no particular order

Contrast Media Injectors Market Companies Covered in this Report

- AngioDynamics (Navilyst)

- APOLLO RT Co., Ltd.

- Bayer AG (MEDRAD)

- Bracco Imaging S.p.A.

- Canon

- Cook Group

- CS Diagnostics GmbH

- GE Healthcare

- Guerbet Group

- Imaxeon Pty Ltd.

- Injekta A/S

- Medtron

- Nemoto Kyorindo Co., Ltd.

- SCITON Medical

- Shenzhen Anke High-Tech Co., Ltd.

- Shenzhen Seacrown Electromechanical Co., Ltd.

- Siemens Healthineers

- SinoMDT (Sino Medical-Device Tech.)

- Ulrich Medical GmbH & Co. KG

- Vivid Imaging

Market Opportunities and Future Outlook

Digitization efforts around dose tracking and protocol automation create room for injector platforms that fit into scanner and IT ecosystems. Hospitals increasingly want contrast dose, flow, and pressure captured directly into patient records, reducing reliance on manual documentation.

Regulatory-driven integration points also align with interventional cardiology and structural heart procedure demand, supporting opportunities for variable-rate contrast management that reduces manual steps and iodine load, particularly using dual-head configurations and automated flushing protocols. In March 2026, the FDA 510(k) clearance for Bayer's MEDRAD MRXperion MR Injection System, expanding compatibility with MRI up to 7T and enabling an Imaging Scanner Interface update, highlights this interoperability direction. In May 2026, Bracco and ACIST Medical Systems announced U.S. FDA clearance and launch of the ACIST Pro diagnostic system for cardiovascular procedures, reflecting continued vendor investment in catheter-lab specific contrast workflow tools, while the EU commercial launch of AiMIFY at ECR 2026 and the partnership with Avicenna.AI continue to reinforce software-led enhancements across enterprise imaging programs.

Recent Industry Developments in Contrast Media Injectors Market

- May 2026: Bracco and ACIST Medical Systems announced U.S. FDA clearance and launch of the ACIST Pro diagnostic system, a variable-rate contrast management solution for cardiovascular procedures. The rollout improves cath-lab protocol control and expands the installed base for catheterization-focused disposables and service contracts tied to contrast management platforms.

- December 2025: Bayer secured FDA 510(k) clearance to add single-dose vials across multiple iodinated agents on the Centargo multi-patient CT injector. The clearance increases operational flexibility for sites balancing multi-patient reservoirs with single-dose handling preferences and standardizes contrast presentation formats on the flagship CT injector platform.

- December 2024: Bracco Diagnostics received U.S. FDA 510(k) clearance for the Bracco-branded Max 3 rapid exchange and syringeless MR injector, developed through a partnership with ulrich GmbH & Co. KG. This clearance supports the shift away from syringe-based setups and strengthens sterile workflow in MRI suites, improving premium MR injector positioning.

Contrast Media Injectors Market Report Scope and Research Methodology

Market Definition and Coverage

This market covers revenue generated from devices and related disposables used to deliver contrast agents during diagnostic imaging and interventional procedures, where dose control and timed delivery are required for scan quality and patient safety.

Scope exclusions: Standalone contrast media drugs, imaging scanners, and general IV sets that are not designed for powered injection are excluded.

Segments Covered in This Report

- By Products

- Injector Systems

- CT Injector Systems

- MRI Injector Systems

- Cardiovascular/Angiography Injector Systems

- Consumables

- Tubing

- Syringes

- Other Consumables

- Injector Systems

- By Type of Injectors

- Single-Head Injectors

- Dual-Head Injectors

- Syringeless Injectors

- By Application

- Radiology

- Interventional Cardiology

- Other Applications

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work started with mapping demand-side signals that explain injector utilization, and then matching them to the device and consumables revenue pool. Public sources such as the US FDA device databases, the US Centers for Medicare and Medicaid Services (for procedure and payment references), the OECD health statistics, and the World Bank health expenditure indicators helped anchor the care-setting mix and the direction of imaging activity.

To support the supply view, we reviewed sources such as SEC filings and annual reports, investor presentations, reputable medical-imaging association materials, and peer-reviewed radiology and cardiology journals discussing injection protocols and contrast safety practices. Where needed, paid subscriptions that track company financials and intelligence, global contracts and tenders, shipment-level trade flows, and patent filings were used to spot product refresh cycles and cross-check commercialization timing. These desk sources are illustrative, and we used additional public documents for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work was used to validate what portion of imaging volumes typically uses powered injection, how sites choose between single-head, dual-head, and syringeless platforms, and how disposable usage scales per procedure. We spoke with stakeholders across manufacturers, distributors, hospital imaging departments, and outpatient diagnostic centers, and balanced input across APAC, EMEA, and the Americas so regional practice patterns were not overstated.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 29% | CXOs: 14% | APAC: 51% |

| Mid tier: 52% | Functional/Unit leaders: 40% | EMEA: 31% |

| Smaller Players: 19% | Managers: 46% | Americas: 18% |

Market-Sizing & Forecasting

Sizing was built from a top-down demand pool that reconstructs injector-related spend from imaging and interventional procedure activity, and then filters it through injector usage rates and disposable consumption patterns. In practice, we modeled how CT and MRI exam growth, interventional cardiology case mix, and installed base replacement cycles translate into injector system demand, and then linked that to recurring consumables pull-through.

To keep the model grounded, we tracked market fingerprints as inputs, such as the split of procedures performed in hospitals versus outpatient diagnostic centers, the adoption share of dual-head and syringeless injectors for CT workflows, typical syringes and tubing sets consumed per eligible procedure, and average selling price movement tied to software integration and dose tracking features. Results were corroborated with selective bottom-up checks, such as sampled ASP times that estimated unit shipments for injector systems, and a separate roll-up for consumables using per-procedure usage and channel feedback. Where gaps existed for smaller countries or low-disclosure product lines, assumptions were bridged using regional analogs and then adjusted after interviews.

Forecasting used scenario analysis supported by simple multivariate regression, with imaging volume growth and installed base aging as the main drivers, and pricing stress-tested under stable, conservative, and faster upgrade scenarios. Final growth paths were accepted only after variable trends matched what practitioners described as plausible for budget cycles and protocol changes.

Data Validation & Update Cycle

Outputs were validated through triangulation across procedure signals, device adoption indicators, and supplier-side checks, and then reviewed for variance by modality and region before sign-off. When unusually high growth or pricing jumps appeared, we rechecked the underlying driver, and triggered follow-up outreach to confirm whether the shift was real or a modeling artifact.

The report is refreshed annually, and interim updates are made when material events occur, such as regulatory actions, large hospital procurement changes, or notable technology launches that affect adoption. Before delivery, an analyst performs a fresh pass on key inputs so clients receive an updated view aligned with the latest publicly available information.

Mordor Intelligence's Contrast Media Injectors Market Size Compared With Other Published Estimates

Published market sizes for contrast media injectors can differ even when the topic label looks identical, because authors may treat consumables, software, and service revenue differently, and they may anchor demand to different procedure pools. Timing also matters, since some studies quote a base year while others quote a forecast year, and currency conversion choices can shift the final number.

By tracking injector system shipments and consumables pull-through separately, and then refreshing the procedure-to-injection utilization ratios through interviews, Mordor Intelligence keeps the estimate aligned to CT, MRI, and angiography use cases rather than broad imaging equipment spend that can inflate totals.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 1.96 B (2025) | |

| Global Consultancy A | USD 1.68 B (2024) | Uses a factory-gate framing and a nearer-term historic year, and the scope write-up places more emphasis on manufacturer-side revenue capture, which can understate distributor-marked value in some geographies. |

| Industry Research Group B | USD 2.24 B (2025) | Often groups broader injector-related revenue and applies faster price progression assumptions, and the definition around included accessories and software is less consistently separated from core injector and disposable demand. |

The spread in values is mainly explained by what gets counted with the injector platform (systems-only versus systems plus disposable sets plus add-ons) and which year is treated as the current reference. A clean split between systems and recurring consumables, checked against procedure-linked utilization, produces a number that decision-makers can trace back to clear drivers and use for repeatable updates.

Key Questions Answered in the Report

How large is the contrast media injectors market in 2026 and how fast is it growing?

The contrast media injectors market size is USD 2.11 billion in 2026 and is forecast to register a 7.54% CAGR to reach USD 3.03 billion by 2031.

Which injector type is expanding the fastest?

Syringeless platforms are projected to record a 10.85% CAGR through 2031 because they streamline workflow and eliminate disposable syringes.

Which application area is set to lead future growth?

Interventional cardiology is expected to post a 9.87% CAGR as percutaneous coronary interventions and transcatheter valve procedures rise across major health systems.

What is the leading regional market today?

North America held 36.13% of global revenue in 2025 thanks to a large installed imaging base and rapid adoption of AI-enabled injectors.

Why are AI protocols important for injector purchases?

AI software such as Bracco's AiMIFY halves iodine dose while maintaining image quality, helping hospitals cut consumable costs and meet dose-tracking mandates.

Page last updated on: