Electric Vehicle Battery Materials Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 55.52 Billion |

| Market Size (2031) | USD 105.74 Billion |

| Growth Rate (2026 - 2031) | 13.74% CAGR |

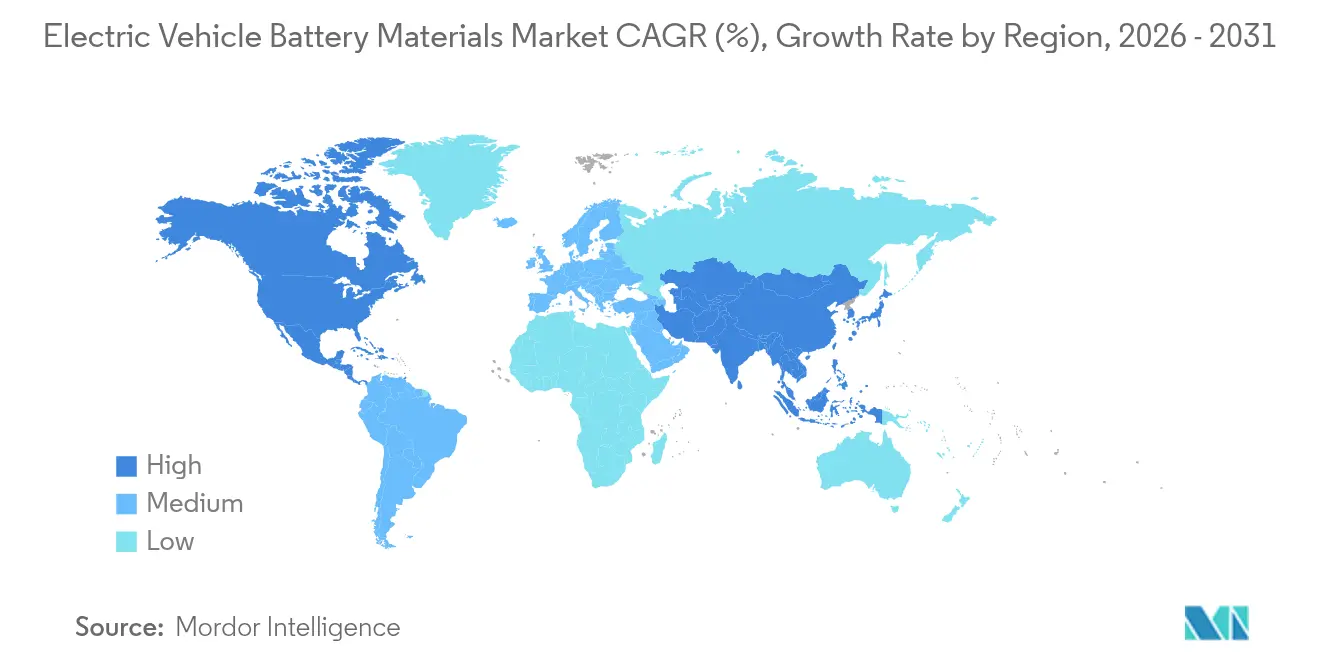

| Fastest Growing Market | North America |

| Largest Market | Asia Pacific |

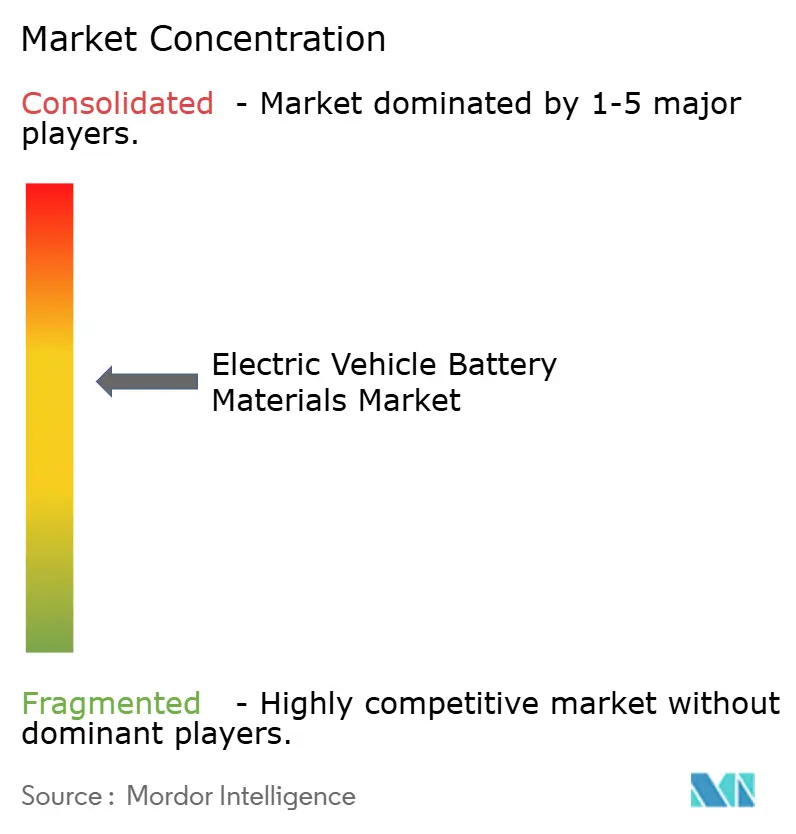

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Electric Vehicle Battery Materials Market Analysis by Mordor Intelligence

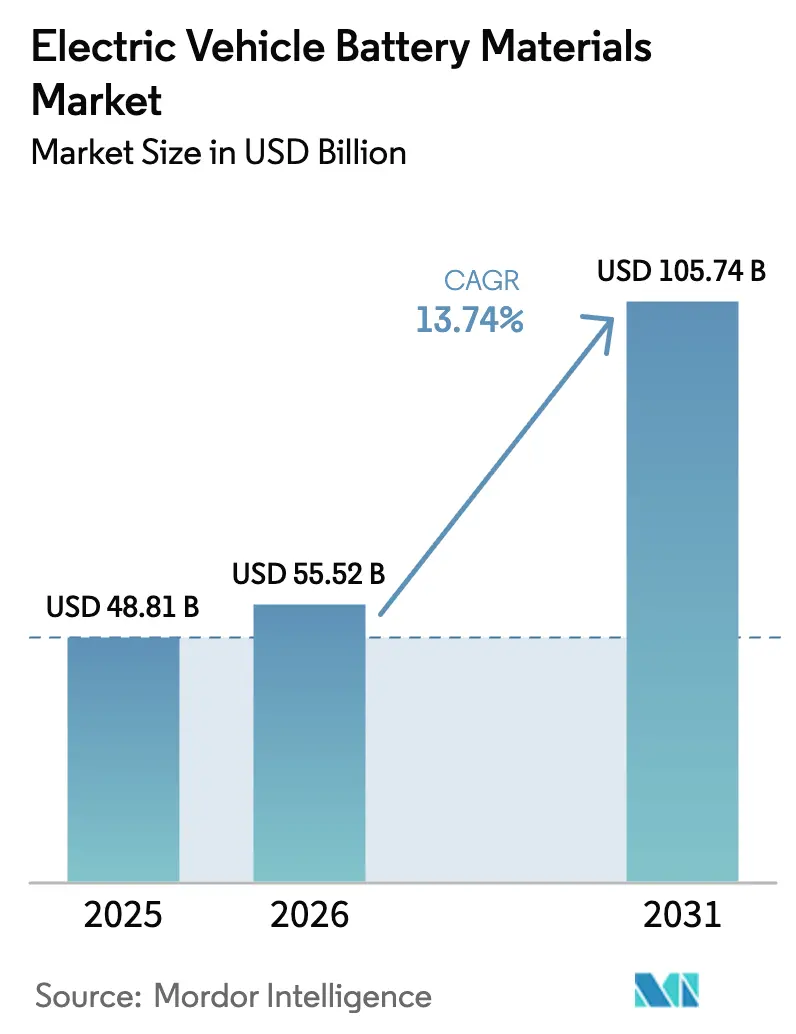

The Electric Vehicle Battery Materials market size is expected to grow from USD 48.81 billion in 2025 to USD 55.52 billion in 2026 and is forecast to reach USD 105.74 billion by 2031 at 13.74% CAGR over 2026-2031.

Cathode materials continue to dominate value creation because energy density and safety still hinge on cathode chemistry, whereas binders, conductive additives, and foils are gaining traction as cell makers chase incremental fast-charge gains and tighter thermal windows. Accelerated local-content mandates in North America and Europe, coupled with mounting investor pressure to derisk supply chains, are fragmenting what was once a linear China-centric sourcing map. The surge in Southeast Asia’s two-wheeler electrification, rapid progress in high-manganese cathodes, and AI-enabled R&D cycles that validate new chemistries in months instead of years are compressing product-launch timelines. At the same time, raw-material price volatility and concentrated lithium, cobalt, and nickel refining capacity remain structural headwinds likely to shape supplier strategies through the decade.

Key Report Takeaways

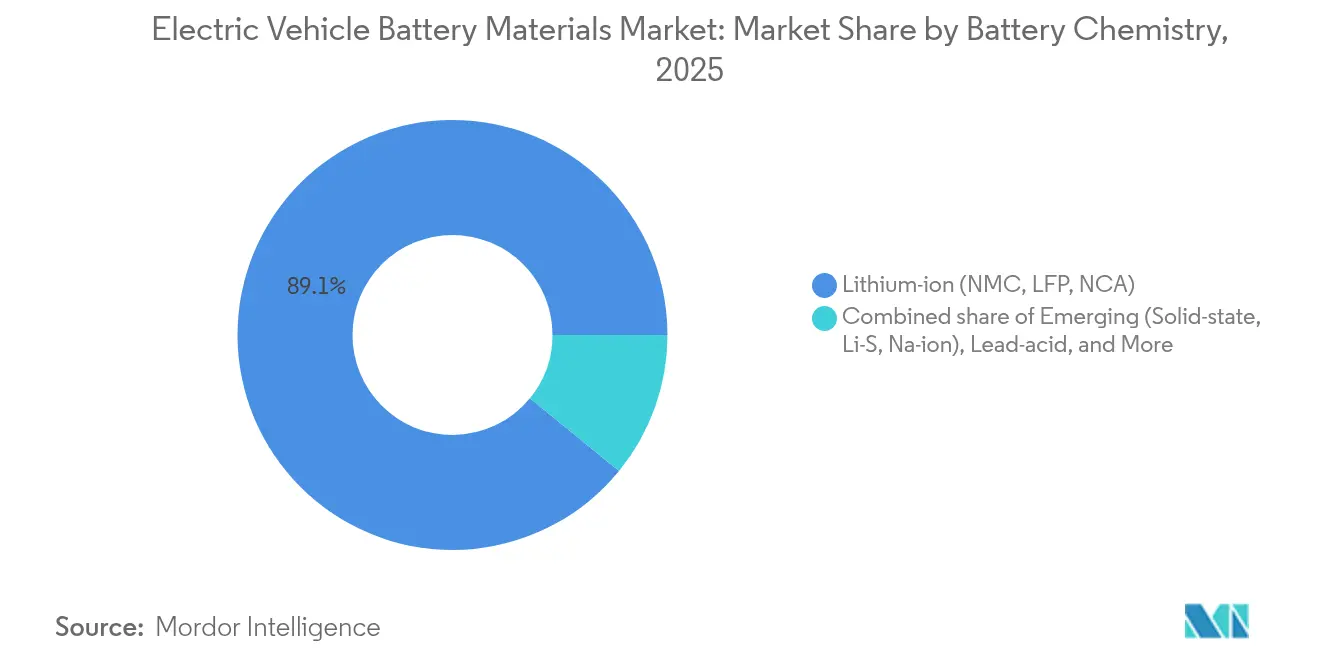

- By battery chemistry, lithium-ion held 89.10% of the electric vehicle battery materials market share in 2025, whereas solid-state, lithium-sulfur, and sodium-ion are forecast to expand at a 36.4% CAGR to 2031.

- By material, cathodes led with 59.30% revenue share in 2025, while the “Others” segment is projected to post a 26.2% CAGR through 2031.

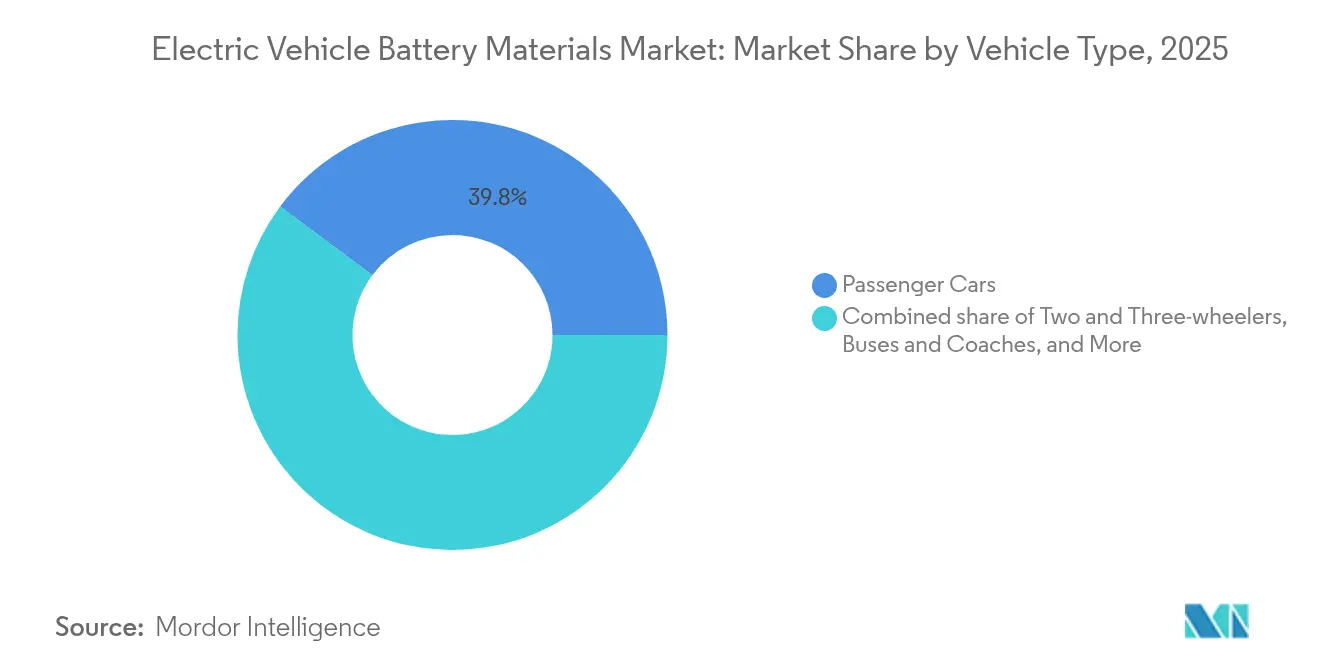

- By vehicle type, passenger cars accounted for 39.80% demand in 2025; two- and three-wheelers represent the fastest trajectory at a 20.1% CAGR to 2031.

- By geography, Asia-Pacific captured 50.20% of 2025 volume, yet North America is on course for a 20.6% CAGR through 2031 as IRA incentives accelerate local precursor and graphite projects.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Electric Vehicle Battery Materials Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in global EV sales | +4.20% | Global, with concentration in China, Europe, North America | Medium term (2-4 years) |

| Falling $/kWh for Li-ion packs | +3.10% | Global, particularly Asia-Pacific manufacturing hubs | Short term (≤ 2 years) |

| National subsidies for on-shore critical-mineral refining | +2.80% | North America, Europe, Australia | Long term (≥ 4 years) |

| Breakthrough high-Mn cathodes cutting cobalt use | +1.90% | Global, led by South Korea, Japan, China | Medium term (2-4 years) |

| Commercialisation of silicon-carbon composite anodes | +1.20% | Asia-Pacific, North America | Long term (≥ 4 years) |

| AI-driven discovery platforms speeding material R&D | +0.80% | Global, concentrated in advanced R&D centers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in Global EV Sales

Global EV registrations climbed to roughly 14 million units in 2024, widening demand beyond passenger cars to medium-duty fleets as regulatory deadlines lock in zero-emission targets. Automakers now demand chemistries that balance energy density, rapid charging, and extended warranties, a mix that pushes material suppliers to qualify high-nickel NMC or silicon-doped anodes. China’s 35% domestic penetration and rising exports diffuse battery material pull across emerging hubs in Southeast Asia, Latin America, and the Middle East. Fleet managers in Europe and North America are moving to three-to-five-year payback horizons, shifting procurement from experimental pilots to multi-year offtake contracts. As EV lifecycles shrink, second-generation pack replacements promise a recurring aftermarket for refined cathode and anode feedstocks.

Falling $/kWh for Li-ion Packs

Average pack prices slid to USD 115 per kWh in 2024, enabling sub-USD 30,000 electric sedans in North America without subsidies. Higher cell-to-pack integration and temporary lithium oversupply drove the decline, but the price drop compresses margins for independent separator and electrolyte makers. In response, suppliers are introducing ceramic-coated films that command premium ASPs, and cathode designers are pushing nickel content past 90% in NCA blends to lift volumetric energy density. Forecasts place pack costs at USD 80 per kWh by 2028, a tipping point that brings sticker-price parity with gasoline vehicles across most segments. That outlook is intensifying long-term hedging, with automakers negotiating floor-and-ceiling contracts rather than floating spot exposure.

National Subsidies for On-Shore Critical-Mineral Refining

Section 45X of the U.S. Inflation Reduction Act grants up to USD 35 per kWh for domestic battery cells, pulling cathode precursor, graphite, and separator projects into Tennessee, Ohio, Michigan, and Quebec. Europe’s Critical Raw Materials Act echoes these ambitions by requiring 40% of strategic minerals to be processed inside the bloc by 2030, catalyzing nickel sulfate and lithium hydroxide investments in Finland, Germany, and France. Australia’s 10% production tax credit on processed lithium and cobalt aims to export refined chemicals instead of raw concentrates. While these incentives diversify supply chains, permitting timelines remain a bottleneck: U.S. refineries average 4-6 years from proposal to commissioning, double China’s typical lead time. Developers face a race against the 2028-2030 demand spike to bring capacity online.(1) U.S. Geological Survey, “2024 Critical Minerals Review,” usgs.gov

Breakthrough High-Mn Cathodes Cutting Cobalt Use

High-manganese cathodes reduce cobalt content below 5 wt% while delivering 200 Wh/kg at the cell level, a compromise automakers accept for lower cost and simplified compliance with ethical-sourcing rules. BASF’s Schwarzheide line shipped lithium manganese iron phosphate (LMFP) samples to European OEMs in early 2024; POSCO Future M followed with high-Mn NMC achieving 2,000+ cycles suited for commercial vans. Demand for manganese sulfate is projected to triple by 2030, yet refining capacity sits mostly in China and South Africa, prompting new projects in Gabon and Australia. EU battery regulations that mandate carbon-footprint reports from 2025 accelerate adoption because low-cobalt chemistries reduce audit complexity. Energy-density trade-offs of 10-15% versus high-Ni NMC restrict high-Mn cells to mid-range vehicles, but volume potential remains sizable.

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Concentrated supply of Li, Co & Ni | -2.30% | Global, with critical nodes in China, DRC, Indonesia | Medium term (2-4 years) |

| Raw-material price volatility | -1.80% | Global, affecting all regions | Short term (≤ 2 years) |

| Processing-skills talent gap | -0.90% | North America, Europe | Medium term (2-4 years) |

| Water-stress opposition to brine extraction | -0.70% | South America (Chile, Argentina), North America (Nevada) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Concentrated Supply of Li, Co & Ni

China refined around 70% of global lithium, 65% of cobalt, and 60% of nickel sulfate in 2024, creating a single-point failure risk for automakers. The Democratic Republic of Congo provided roughly 70% of mined cobalt but refined only 10% domestically, with most feedstock routed to Chinese converters, exposing OEMs to both political unrest and ethical-sourcing scrutiny. Indonesia’s ore-export ban forces nickel value-addition onsite in Chinese-funded smelters, deepening reliance on one geopolitical sphere. Although new lithium brine projects in Argentina and hard-rock expansions in Australia promise diversification, mine lead times of 5-10 years limit near-term relief. The U.S. Geological Survey ranks cobalt and natural graphite among the highest supply-risk minerals, prompting federal grants for recycling pilot plants.

Raw-Material Price Volatility

Chinese lithium carbonate spot prices whipsawed from USD 80,000/t in late 2022 to under USD 12,000/t in mid-2024 before rebounding, forcing OEMs to shift from spot to long-term indexed contracts. Cobalt vacillated between USD 30,000 and USD 50,000/t in 2024, driven by Indonesian co-production and intermittent mine closures in higher-cost regions. Nickel sulfate premiums over LME nickel widened even as bulk inventories rose, underscoring mismatches between commodity and battery-grade supply. Lacking transparent exchanges for battery-grade lithium hydroxide, price discovery remains opaque and bilateral, complicating hedge strategies. Suppliers now peg cathode quotes to quarterly metal averages, shifting risk further downstream.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Battery Chemistry: Lithium-Ion Dominance Faces Niche Challengers

Lithium-ion chemistries secured 89.10% of demand in 2025, underscoring their fit for mainstream EV range, cycle life, and established manufacturing lines, while the segment is expected to grow in tandem with overall electric vehicle battery materials market volumes. Emerging platforms such as solid-state, lithium-sulfur, and sodium-ion are forecast to register a 36.4% CAGR through 2031, expanding the electric vehicle battery materials market footprint into applications that prioritize safety or raw-material diversity. Solid-state pilot lines from Toyota and QuantumScape aim for premium models that can absorb the present 3-5 fold cost premium. Sodium-ion eliminates lithium and cobalt, facilitating cost-efficient supply for urban mobility fleets in India and Southeast Asia. Lead-acid’s residual foothold in micro-hybrids continues to erode, while nickel-metal-hydride persists mainly in legacy hybrid platforms.

Parallel R&D budgets now support two divergent pathways. High-nickel NMC or NCA push energy density for SUVs and light trucks in North America, whereas LMFP and sodium-ion cater to cost-sensitive scooters and compact cars. Regulatory thermal-propagation tests under UN Global Technical Regulation frameworks raise barriers for new chemistries, delaying commercial timelines even when lab metrics look favorable. Consequently, the electric vehicle battery materials industry is investing in modular pilot facilities that can pivot between chemistries with minimal downtime, a hedge against uncertain adoption curves.

By Material: Cathode Economics Drive Value-Chain Margins

Cathodes accounted for 59.30% of revenue in 2025 and remain the profit anchor because energy density, charge rate, and safety converge on cathode designs. LFP captured roughly 40% of cathode volume, with market momentum building in North America, where OEMs value cobalt-free supply chains. High-nickel NMC and NCA, representing 45% of tonnage, cater to range-critical segments despite stringent dry-room and coating requirements that inflate capex. Anode demand is pivoting toward silicon-carbon composites, a shift that necessitates high-performance binders and SEI-stabilizing electrolyte additives, thereby lifting the “Others” category.

The “Others” segment is projected to clock a 26.2% CAGR through 2031 as cell designs adopt thinner current-collector foils and ceramic-coated separators to enable ultra-fast charging. Electrolyte formulations rich in fluoroethylene carbonate are standardizing, extending cycle life in high-voltage cells. Collectively, these upgrades maintain the electric vehicle battery materials market value even as $/kWh declines, because advanced supplies command unit price premiums. Suppliers with vertical integration, from precursor synthesis to finished cathode powder, enjoy margin insulation, whereas standalone additive firms face consolidation pressures.

By Vehicle Type: Passenger Cars Lead, Two-Wheelers Accelerate

Passenger cars represented 39.80% of 2025 demand, reflecting the weight-intensive nature of 60-80 kWh packs in sedans and SUVs, and continue to anchor gross tonnage within the electric vehicle battery materials market size. Two- and three-wheelers, while using smaller 2-5 kWh packs, are forecast to expand at 20.1% CAGR, adding high-volume cell orders that favor standardized cylindrical formats and LFP or sodium-ion chemistries. Light commercial vehicles are electrifying rapidly in Europe and North America, driven by urban fleet mandates and TCO economics that now break even within four years.

Medium- and heavy-duty trucks adopt LFP for deep-cycle durability, yet require 200-600 kWh packs that generate lumpy cathode orders. Off-highway EVs in construction and agriculture form a niche but high-margin segment given their ruggedization needs and long-duty cycles. Regionally, North America’s penchant for large SUVs pushes high-nickel cathodes, whereas Asia’s micro-mobility boom pulls LFP and sodium-ion. The vehicle-type mix thus shapes localized procurement, compelling suppliers to maintain flexible product portfolios to capture a stable electric vehicle battery materials market share across classes.

Geography Analysis

Asia-Pacific captured 50.20% of 2025 volume thanks to China’s cradle-to-grave ecosystem that spans lithium refining, cathode synthesis, cell manufacturing, and pack assembly, embedding scale-economy advantages that compress costs and accelerate product iteration. Japan and South Korea remain technology front-runners in high-nickel cathodes and ceramic-coated separators, exporting premium materials under long-term agreements into Europe and North America.

North America is slated for a 20.6% CAGR through 2031, propelled by the Inflation Reduction Act credits that reward domestic content, energizing precursor and graphite projects in Tennessee, Ohio, Quebec, and Michigan. Canada’s hydropower advantage and proximity to nickel sulfide deposits further anchor investment. Still, the electric vehicle battery materials market size for North America hinges on resolving permitting backlogs that slow refinery construction. Europe remains hampered by elevated energy costs and lengthy environmental reviews, constraining market share gains despite the European Battery Alliance’s aim for 30 gigafactories by 2030. Southeast Asia’s Indonesia, Thailand, and Vietnam emerge as processing hubs supplying both local demand and export markets, supported by abundant nickel laterite reserves and favorable investment policies. Australia is transitioning from spodumene exporter to value-added lithium hydroxide refiner via a 10% production tax credit, while South America’s lithium triangle wrestles with water-use conflicts that may delay additional brine capacity.

Mordor Intelligence provides coverage of the electric vehicle battery materials market across other key regional markets, including North America, South America, Europe, Asia, and Middle East and Africa, each with their regulatory frameworks and demand patterns. Detailed country-level analysis extends to United States, United Kingdom, China, India, and Germany incorporating local coverage and market participation, as required.

Competitive Landscape

Global supply remains moderately concentrated: the top 10 cathode and anode suppliers controlled roughly 55-60% capacity in 2024, yet automation and policy incentives are enabling fresh entrants, diluting legacy market power. Vertically integrated cell makers, CATL, LG Energy Solution, Samsung SDI, and BYD, are backward-integrating into precursor synthesis, pressuring independent material firms to specialize or merge. Strategic moves in 2024 included POSCO Future M’s USD 400 million cathode JV in Quebec, Albemarle’s USD 6.6 billion lithium acquisition in Australia, and LG Chem’s decade-long nickel sulfate pact with Huayou Cobalt.

Technology leadership is shifting toward AI-assisted discovery platforms that shorten formulation cycles and adapt rapidly to regulatory changes. Patent landscapes show Toyota, Samsung, and QuantumScape leading solid-state electrolyte IP, while CATL dominates sodium-ion and LFP claims. Recycling startups such as Ascend Elements and Redwood Materials promote cathode-to-cathode regeneration, aligning with EU mandates for recycled content and offering OEMs circular-economy assurances.

Compliance with ISO 14001 and Responsible Minerals Initiative protocols is becoming table stakes, yet enforcement gaps present arbitrage opportunities for agile suppliers. The electric vehicle battery materials industry thus balances scale economics, innovation velocity, and ESG credentials, all under intensifying governmental scrutiny.(4)US Department of Energy, “AI for Materials Discovery Initiative,” energy.gov

Electric Vehicle Battery Materials Industry Leaders

Targray Technology International Inc.

BASF SE

Mitsubishi Chemical Group Corporation

UBE Corporation

Umicore SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: POSCO Future M committed USD 1.2 billion to expand high-nickel NMC cathode capacity in South Korea by 100,000 tpa, integrating AI-driven quality control and closed-loop scrap recycling.

- December 2024: Albemarle acquired Liontown Resources’ Kathleen Valley lithium project for USD 6.6 billion, locking in 500,000 tpa of spodumene concentrate for U.S. gigafactory supply.

- November 2024: LG Chem and Huayou Cobalt signed a 10-year, 150,000 tpa nickel sulfate agreement tied to LME pricing with floor protection.

- October 2024: BASF opened a EUR 500 million cathode precursor plant in Germany with 40,000 tpa capacity for LMFP and high-Mn NMC lines.

Global Electric Vehicle Battery Materials Market Report Scope

Electric vehicle (EV) battery materials are the specific substances and components used in the construction of batteries for powering electric vehicles. These materials determine electric vehicles' efficiency, range, longevity, and safety. The report offers the market size in value terms (USD) for all the above-mentioned segments. The global electric vehicle battery materials market report includes:

| Lithium-ion (NMC, LFP, NCA) |

| Emerging (Solid-state, Li-S, Na-ion) |

| Lead-acid |

| Nickel-metal-hydride |

| Anode |

| Cathode |

| Separator |

| Electrolyte |

| Others |

| Passenger Cars |

| Light Commercial Vehicles |

| Medium and Heavy Trucks |

| Buses and Coaches |

| Two and Three-wheelers |

| Off-Highway and Specialty EVs |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| NORDIC Countries | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Australia and New Zealand | |

| Rest of Asia Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Battery Chemistry | Lithium-ion (NMC, LFP, NCA) | |

| Emerging (Solid-state, Li-S, Na-ion) | ||

| Lead-acid | ||

| Nickel-metal-hydride | ||

| By Material | Anode | |

| Cathode | ||

| Separator | ||

| Electrolyte | ||

| Others | ||

| By Vehicle Type | Passenger Cars | |

| Light Commercial Vehicles | ||

| Medium and Heavy Trucks | ||

| Buses and Coaches | ||

| Two and Three-wheelers | ||

| Off-Highway and Specialty EVs | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| NORDIC Countries | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Australia and New Zealand | ||

| Rest of Asia Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How fast is the electric vehicle battery materials market projected to grow?

It is forecast to expand at a 13.74% CAGR between 2026-2031, reaching USD 105.74 billion by 2031.

Which chemistry currently dominates demand?

Lithium-ion chemistries, including NMC, LFP, and NCA, represented 89.10% of 2025 demand.

What drives North America’s rapid growth?

Inflation Reduction Act tax credits and local-content rules are drawing cathode precursor and synthetic graphite projects into the United States and Canada.

Why are high-manganese cathodes gaining traction?

They cut cobalt content below 5% and lower cost while meeting durability requirements for mid-range vehicles.

How do raw-material price swings affect suppliers?

Volatility forces a shift from spot purchases to long-term indexed contracts, and suppliers increasingly peg cathode prices to quarterly metal averages.

Which segment is growing quickest by vehicle type?

Two- and three-wheelers are projected to post a 20.1% CAGR through 2031 due to Southeast Asia’s micro-mobility boom and India’s subsidy extensions.

Page last updated on: