Digital Fault Recorder Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

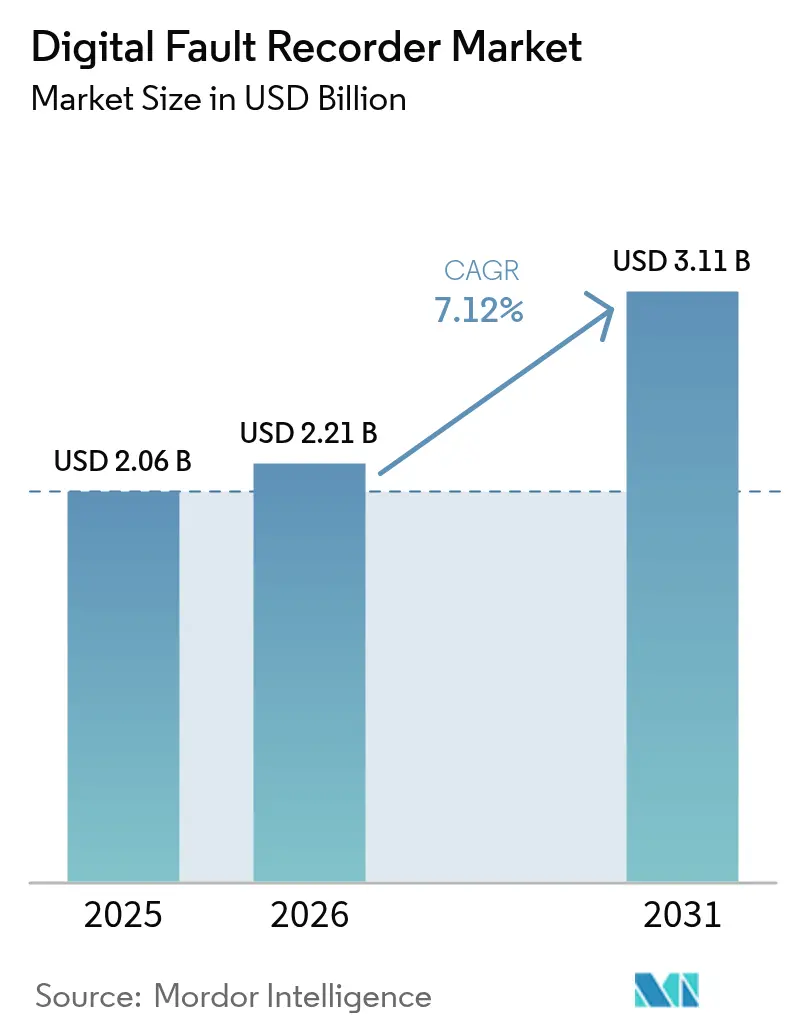

| Market Size (2026) | USD 2.21 Billion |

| Market Size (2031) | USD 3.11 Billion |

| Growth Rate (2026 - 2031) | 7.12% CAGR |

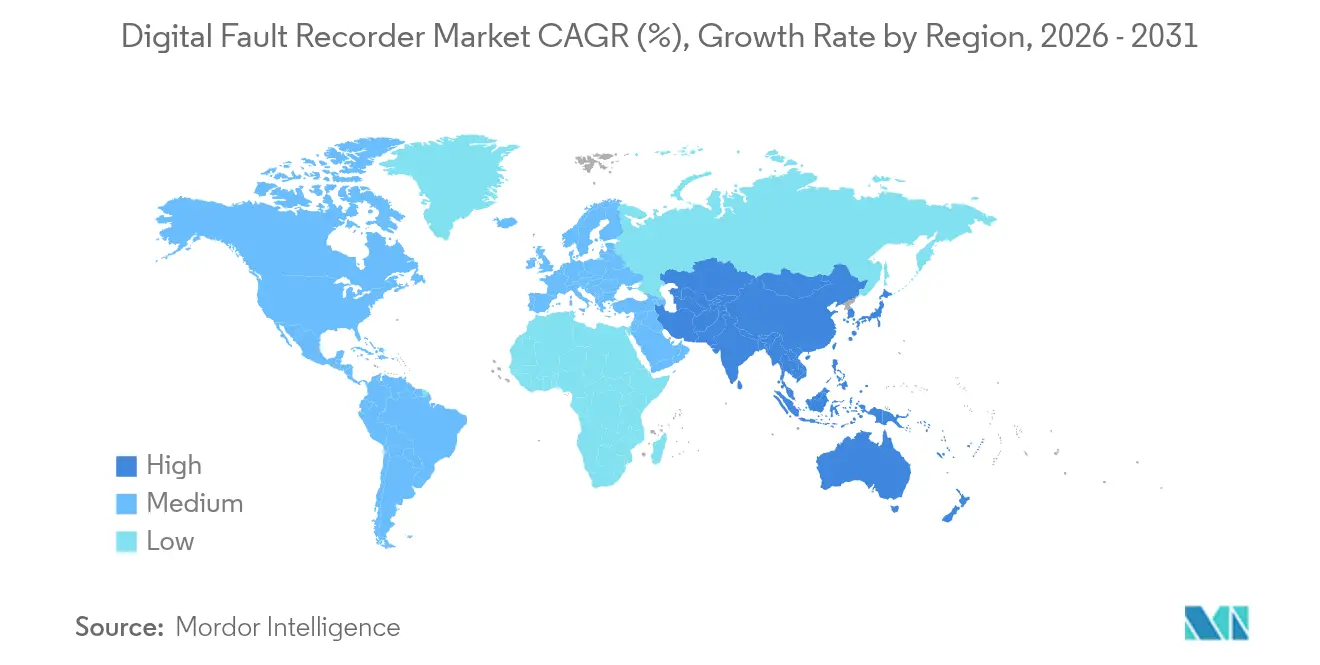

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

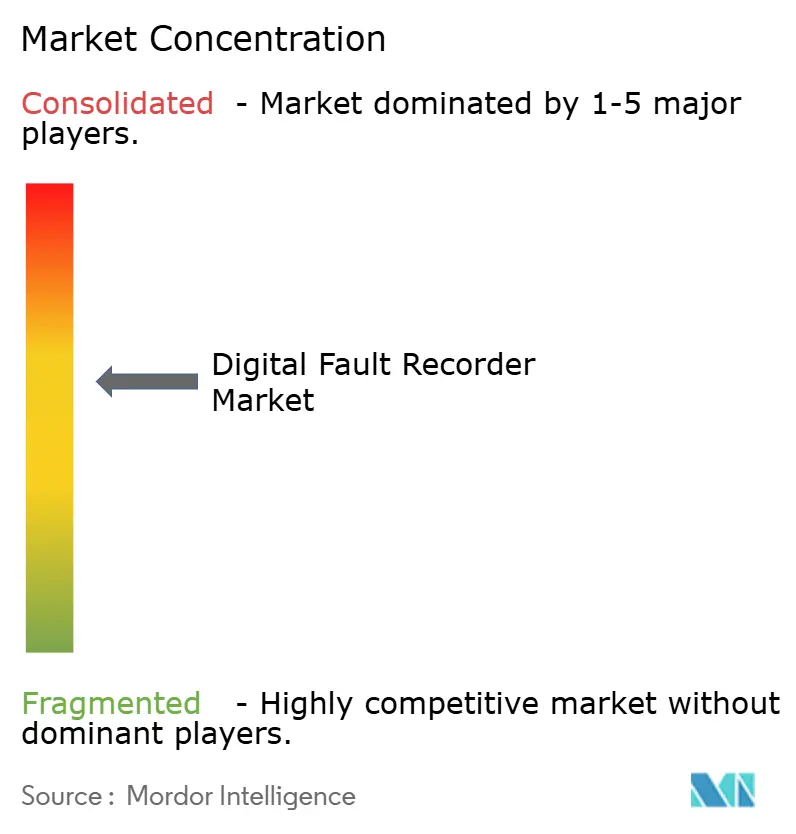

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Digital Fault Recorder Market Analysis by Mordor Intelligence

The Digital Fault Recorder Market size is expected to grow from USD 2.06 billion in 2025 to USD 2.21 billion in 2026 and is forecast to reach USD 3.11 billion by 2031 at 7.12% CAGR over 2026-2031. Growth momentum is tied to record-high grid-modernization budgets, expanding renewable penetration, and strict compliance mandates that push utilities toward real-time disturbance monitoring capabilities that traditional electromechanical devices cannot deliver. Utilities across North America and Europe are drawing on multi-billion-dollar public funding programs to replace aging assets, while Asian network operators accelerate ultra-high-voltage roll-outs to move renewable power over long distances. Heightened power-quality expectations from hyperscale data centers add a new demand stream, and the move to IEC 61850 process-bus architectures cements interoperability as a core purchase criterion. Cost pressures from semiconductor shortages and copper inflation persist, but buyers are prioritizing life-cycle value and analytics readiness over lowest first cost, maintaining steady order pipelines for both dedicated and multifunction platforms.

Key Report Takeaways

- By type, dedicated recorders led with 57.90% revenue share in 2025; multifunction devices are projected to grow at a 8.90% CAGR through 2031.

- By installation, the transmission segment held 47.90% of the digital fault recorder market share in 2025, while distribution networks are advancing at a 8.65% CAGR to 2031.

- By voltage class, 110-220 kV captured 43.05% share of the digital fault recorder market size in 2025; the 220-500 kV segment is anticipated to expand at an 8.05% CAGR between 2026 and 2031.

- By communication protocol, IEC 61850-compliant devices accounted for 60.75% of the digital fault recorder market size in 2025 and are growing at an 7.75% CAGR to 2031.

- By end-user, utilities represented 38.35% share in 2025; data centers are advancing at an 8.10% CAGR through 2031.

- By geography, North America commanded a 35.35% share in 2025, whereas Asia-Pacific is poised for an 8.45% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Digital Fault Recorder Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Grid-modernization capex surge | +2.1% | Global, concentrated in North America and EU | Medium term (2-4 years) |

| Mandatory NERC PRC-002-2 compliance | +1.8% | North America, expanding globally | Short term (≤ 2 years) |

| Renewable and inverter-based generation penetration | +1.5% | Global, led by APAC and Europe | Long term (≥ 4 years) |

| IEC 61850 process-bus roll-out | +1.2% | Global, early adoption in mature markets | Medium term (2-4 years) |

| AI-driven predictive maintenance demand | +0.9% | North America and EU, moving to APAC | Long term (≥ 4 years) |

| Data-center substation reliability push | +0.7% | Global, data-center hubs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Grid-Modernization Capex Surge

Record utility capital programs underpin sustained ordering cycles for the digital fault recorder market. The European Union has earmarked EUR 584 billion for network upgrades by 2030, while North America channels USD 10.5 billion in federal funds toward grid resilience. Suppliers such as Hitachi Energy are investing heavily—USD 4.5 billion through 2027—to scale production and digital capabilities, signalling confidence that modernization spending will survive macroeconomic slowdowns. Utilities increasingly bundle fault recorders with power-quality meters and disturbance analytics, treating them as foundational elements of next-generation grid control architectures. National security framing around grid reliability further shields budgets from cyclical cuts. [1]European Commission, “Grids, the Missing Link – An EU Action Plan for Grids,” European Commission

Mandatory NERC PRC-002-2 Disturbance-Monitoring Compliance

North American utilities face immovable timelines to demonstrate disturbance-recording coverage across bulk power assets. Penalties for non-compliance can reach multimillion-dollar levels, driving an accelerated procurement cycle for IEC 61850-ready digital fault recorders that satisfy PRC-002-2 event-capture windows while also delivering power-quality insights. The compliance model is resonating abroad: European and Asian regulators reference NERC’s framework as they craft equivalent monitoring rules, laying the groundwork for export growth. Utilities favor multifunction units to meet multiple standards in one footprint, supporting the consolidation of relay and recorder hardware.

Renewable and Inverter-Based Generation Penetration

Wind and solar assets introduce high-frequency harmonics, sub-synchronous oscillations, and rapid voltage swings that overwhelm legacy electromechanical recorders. Utilities such as Dominion Energy deploy high-resolution digital fault recorders to validate inverter models and fine-tune protection settings, reducing false trips during variable generation ramps. As renewable shares rise past 40% in several grids, event data from fault recorders feed into stability studies and adaptive protection schemes that maintain reliability. The need for millisecond-level event correlation favours devices with multi-gigabyte buffers and advanced signal-processing algorithms. [3]PAC World, “Inverter-Based Generation Monitoring and Fault Analysis,” pacw.org

IEC 61850 Process-Bus Roll-Out

Utilities migrating toward process-bus topologies view digital fault recorders as core nodes within an IEC 61850-native substation. Process-bus architectures digitize measurements at source transformers, cutting copper runs in half and boosting data fidelity. Vendors offer modular recorders that ingest sampled values under IEC 61850-9-2, enabling station-wide event correlation on a single platform. Early adopters report engineering time savings and smoother device interoperability, though skilled configuration resources remain scarce. Cyber-secure editions of IEC 61850 strengthen adoption momentum as utilities weigh long-term asset life-cycle costs over initial spend.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront cost of multifunction DFRs | -1.4% | Global, acute for smaller utilities | Short term (≤ 2 years) |

| OT-network cyber-security concerns | -1.1% | Global, heightened in critical infrastructure | Medium term (2-4 years) |

| Shortage of waveform-analysis expertise | -0.8% | Global, sharp in emerging markets | Long term (≥ 4 years) |

| Memory-chip thermal-cycle reliability | -0.6% | Global, harsh environments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Upfront Cost of Multifunction DFRs

Advanced multifunction units priced between USD 50,000 and USD 200,000 test smaller utilities’ budgets at a time when they must also fund cybersecurity hardening and distribution automation. Integration, training, and licensing expenses can double the life-cycle cost, prompting tiered deployment strategies that limit installations to critical nodes. Suppliers counter by offering subscription pricing and modular firmware unlocks, yet capital constraints remain the chief adoption brake in price-sensitive regions. [4]U.S. Department of Energy, “Workforce Trends in the Electric Utility Industry,” energy.gov

OT-Network Cyber-Security Concerns

Recorder connectivity to SCADA backbones raises fears of new attack vectors. Utilities deploy deep-packet-inspection appliances and micro-segmentation firewalls, but many smaller operators lack the talent to sustain 24/7 monitoring. Cyber incidences involving operational technology reinforce caution, delaying recorder upgrades where legacy air-gapped designs still operate reliably. Vendors embed secure boot and role-based access controls, but risk aversion persists until utilities standardize zero-trust architectures across substations. [2]Sahu et al., “A Firewall Optimization for Threat-Resilient Micro-Segmentation in Power System Networks,” arxiv.org

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Multifunction Platforms Accelerate Consolidation

Dedicated units dominated the digital fault recorder market with a 57.90% revenue share in 2025. Transmission operators value their proven reliability, deterministic response, and straightforward relay-scheme integration. However, multifunction devices record a 8.90% CAGR to 2031 as buyers seek to collapse disturbance recording, power-quality metering, and analytics gateways into a single enclosure. Multifunction adoption is strongest in greenfield substations where space and wiring reduction justify premium pricing. Utilities running pilot projects report engineering-hour savings of up to 20% when relying on virtualized protection software. The digital fault recorder market size captured by multifunction devices is forecast to reach USD 1.42 billion by 2031, underpinned by declining per-channel costs and firmware-driven feature expansion. Vendor roadmaps converge toward cloud-update capability, enabling remote addition of synchrophasor streaming and IEC 61850 Edition 2 features without hardware swaps. The competitive narrative shifts as relay incumbents integrate high-resolution capture cards, while traditional recorder specialists develop modular I/O options to protect their share.

By Installation: Distribution Builds Momentum

Transmission grids held 47.90% of the digital fault recorder market share in 2025 because bulk-power nodes remain mandatory monitoring points across most reliability regimes. Yet distribution networks, historically under-instrumented, post the fastest 8.65% CAGR through 2031. Distributed energy resource connections, voltage-regulating inverters, and vehicle-to-grid pilots create complex fault signatures at medium-voltage levels. Utilities now specify recorders for feeder head-ends and critical distribution transformers to resolve power-quality complaints and minimize outage investigation times. The digital fault recorder market size attributable to distribution is projected to pass USD 980 million in 2031 as unit costs fall and compact form factors become mainstream. Meanwhile, generation-site deployments concentrate on renewable plants where grid-code compliance requires oscillography for every fault trip; these projects favour devices with embedded disturbance analysis that ease certification.

By Voltage Class: Ultra-High-Voltage Drives Upside

The 110-220 kV band retained 43.05% revenue in 2025, reflecting its status as backbone voltage across most regional grids. Rapid rollout of 220-500 kV corridors, especially in China and India, pushes that segment to an 8.05% CAGR. Ultra-high-voltage alternating-current and direct-current lines transfer wind and solar power over 1,000 km distances, demanding recorders that support high sampling rates and fibre-optic time-sync. Vendors introduce temperature-hardened designs rated to −40 °C for remote converter stations. The >500 kV niche commands premium prices and advanced fault-location algorithms that integrate traveling-wave methods, but volume remains comparatively low. Nevertheless, the digital fault recorder market finds outsized value creation in these mega-projects, often bundling recorders with STATCOMs and series-compensation upgrades. Device interoperability at such voltage levels becomes critical due to multi-vendor consortia tasked with grid interconnection.

By Communication Protocol: IEC 61850 Sets the Benchmark

IEC 61850-compliant equipment accounted for 60.75% of total 2025 revenue and expanded at an 7.75% CAGR as operators standardize on open, vendor-agnostic architectures. The digital fault recorder industry benefits from universal adoption of GOOSE messaging and Sampled Values streams, which simplify protection coordination and reduce wiring. Recorders now ship with integrated engineering tools that auto-generate Intelligent Electronic Device descriptions, cutting project commissioning days by up to 30%. Legacy DNP3 and Modbus variants persist in retrofit contexts where replacement budgets are limited or cyber-risk reviews remain incomplete. Nonetheless, most utilities set IEC 61850 interoperability as a prerequisite for tender qualification. The digital fault recorder market size attributable to IEC 61850 solutions is forecast to reach USD 1.95 billion by 2031 as Edition 3 security extensions gain traction.

By End-user: Data Centers Surge Ahead

Utilities remained the prime buyers with 38.35% 2025 revenue, but hyperscale data-center operators drive the strongest 8.10% CAGR to 2031. These facilities exceed 100 MW demand and stipulate fault-recorder installation at upstream substations and on-site generator buses to ensure compliance with strict service-level agreements. Real-time waveform analytics integrate into data-center infrastructure management dashboards, providing operators with early-warning alarms for sags, swells, or transient over-voltages. Industrial plants retain steady adoption rhythms, focusing recorders on production lines where unplanned outages incur significant downtime penalties. Rail and metro projects constitute a growing niche as electrification targets broaden, with recorders aiding traction power protection studies. Oil and gas rigs install ruggedized units rated for offshore vibration and humidity, underscoring the breadth of operational contexts captured within the digital fault recorder market.

Geography Analysis

North America, holding 35.35% revenue share in 2025, benefits from robust federal funding and stringent NERC standards that oblige disturbance monitoring on all bulk-electric-system elements. Programs under the Bipartisan Infrastructure Law drive rapid retrofit cycles that favour multifunction recorders packaged with power-quality features. United States utilities expand disturbance-monitoring scope to inverter-based resources, while Canada aligns standards to smooth cross-border power flows. Mexico presents emerging opportunities as interconnection upgrades and renewable integration mandates demand improved event visibility.

Asia-Pacific posts the fastest 8.45% CAGR, powered by China’s State Grid investment of more than CNY 600 billion (USD 84.5 billion) in ultra-high-voltage construction and comprehensive digital upgrades. India’s grid modernization surges on strong demand growth, with recent HVDC awards lifting record installations in renewable corridors. Japan, South Korea, and Australia roll out smart-grid pilots that require IEC 61850 process-bus compatibility, creating openings for multinational suppliers. Southeast Asian distribution utilities embrace compact recorders for feeder automation as electrification rates climb.

Europe sustains steady growth under the European Commission’s EUR 584 billion network plan, focusing on offshore wind integration and cross-border trading. Germany and the Netherlands adopt innovative grid-technology packages that expand capacity without new lines, relying on high-resolution data for dynamic rating algorithms. Nordic operators invest in synchronous condensers and STATCOM upgrades, bundling recorders to validate performance. Eastern European networks catch up on substation digitalization, supported by cohesion funds that lower capital hurdles. The Middle East and Africa, while smaller in volume, display rising interest as industrialization and renewable build-outs advance, prompting the adoption of scalable monitoring solutions.

Competitive Landscape

The digital fault recorder market remains moderately fragmented. Global majors—Qualitrol, GE Vernova, Siemens, and ABB/Hitachi Energy—leverage deep utility relationships and end-to-end portfolios covering recorders, relays, and analytics platforms. Mid-tier specialists such as Schweitzer Engineering Laboratories and ERLPhase differentiate through ultra-high-speed capture and niche applications in research labs or HVDC converter stations. Competitive pressure intensifies as buyers prioritize integrated solutions: vendors bundle cyber-secure gateways, power-quality modules, and AI-based diagnostics to command premium margins.

Technology leadership now revolves around edge compute and cloud connectivity. Hitachi Energy’s collaboration with Amazon Web Services demonstrates the pivot toward X-as-a-Service models that extend revenue streams beyond hardware. GE Vernova scales manufacturing footprints in the United States, Germany, and India to mitigate component shortages and serve localized demand. Patent filings escalate around digital twin simulation and traveling-wave location methods, signaling a race for intellectual-property defensibility. Strategic acquisitions—such as Schneider Electric’s Motivair purchase—expand adjacent capabilities in data-center liquid cooling, underscoring convergence between monitoring, thermal management, and energy optimization in mission-critical facilities.

Component supply constraints pose an industry-wide challenge. Memory-chip thermal-cycle reliability issues require redesign of high-frequency storage modules, while copper price volatility squeezes margins. Vendors shift to alternative alloys and explore vertical integration to secure semiconductor supply. Workforce shortages in waveform-analysis expertise further complicate project execution, prompting suppliers to embed guided analytics in firmware to shorten learning curves for substation engineers. Overall, differentiation hinges on delivering cyber-secure, interoperable, and analytics-ready platforms that de-risk utility capital programs.

Digital Fault Recorder Industry Leaders

-

Qualitrol Company LLC

-

GE Grid Solutions (GE Vernova)

-

Siemens AG

-

AMETEK Power Instruments

-

ABB Ltd. (Hitachi Energy DFR line)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Hitachi Energy delivered the world’s first SF₆-free 550 kV gas-insulated switchgear to China’s State Grid Corporation, integrating advanced monitoring for environmental compliance and reliability.

- April 2025: Hitachi Energy announced more than USD 70 million investment in Pennsylvania to scale EconiQ® SF₆-free switchgear production and open a new R&D lab.

- March 2025: Hitachi Energy committed an additional USD 250 million to expand transformer factories worldwide to meet data-center and AI-driven electricity demand.

- March 2025: Hitachi Energy and Amazon Web Services formed a strategic collaboration to develop cloud-based AI solutions for utility operations.

- February 2025: GE Vernova invested more than USD 10 million to expand its Pittsburgh facility for FLEX INVERTER systems, creating 270 jobs.

- January 2025: Hitachi Energy India secured record quarterly orders worth INR 11,594.3 crore (USD 1.4 billion) driven by major HVDC projects.

- December 2024: Hitachi Energy contracted by Ørsted to supply Enhanced STATCOM for the 2.4 GW Hornsea 4 offshore wind project.

- November 2024: GE Vernova launched an HVDC Competence Center in Berlin, adding 500 skilled jobs to support the European energy transition.

- November 2024: Hitachi Energy won a USD 300 million order from Svenska kraftnät for series-compensation systems to lift Swedish transmission capacity by up to 50%.

- September 2024: Hitachi Energy announced USD 155 million to expand North American manufacturing, including a new transformer plant in Mexico.

Global Digital Fault Recorder Market Report Scope

The digital fault recorder market report includes:

| Dedicated |

| Multifunctional |

| Generation |

| Transmission |

| Distribution |

| <110 kV |

| 110-220 kV |

| 220-500 kV |

| >500 kV |

| IEC 61850-compliant |

| Legacy/Proprietary |

| Utilities |

| Industrial and Manufacturing |

| Railways and Metros |

| Data Centers |

| Oil and Gas |

| Other End-users |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Singapore | ||

| Malaysia | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Type | Dedicated | ||

| Multifunctional | |||

| By Installation | Generation | ||

| Transmission | |||

| Distribution | |||

| By Voltage Class | <110 kV | ||

| 110-220 kV | |||

| 220-500 kV | |||

| >500 kV | |||

| By Communication Protocol | IEC 61850-compliant | ||

| Legacy/Proprietary | |||

| By End-user | Utilities | ||

| Industrial and Manufacturing | |||

| Railways and Metros | |||

| Data Centers | |||

| Oil and Gas | |||

| Other End-users | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Chile | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Singapore | |||

| Malaysia | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size of the digital fault recorder market?

The market stands at USD 2.21 billion in 2026 and is forecast to reach USD 3.11 billion by 2031 at a 7.12% CAGR over 2026-2031.

Which region leads the digital fault recorder market?

North America leads with 35.35% revenue in 2025, driven by strict NERC compliance and federal modernization funding.

Why are data centers important for future digital fault recorder demand?

Hyperscale data centers require micro-second disturbance visibility, propelling an 8.10% CAGR for recorder installations in this segment through 2031.

How does IEC 61850 influence recorder selection?

IEC 61850-compliant devices hold 60.75% market share thanks to their interoperability and process-bus capabilities, making the standard a default tender requirement.

What is the biggest restraint on digital fault recorder adoption?

High upfront costs of multifunction units, ranging from USD 50,000 to USD 200,000, limit uptake among smaller utilities.

Which segment is growing fastest within the digital fault recorder market?

The distribution-network installation segment is advancing at a 8.65% CAGR as utilities seek deeper visibility into medium-voltage grids.

Page last updated on: