Space Mining & Robots Market Size and Share

Market Overview

| Study Period | 2017 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2017 - 2023 |

| Market Size (2025) | USD 2.47 Billion |

| Market Size (2030) | USD 4.34 Billion |

| Growth Rate (2025 - 2030) | 11.89% CAGR |

| Market Concentration | High |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Space Mining & Robots Market Analysis by Mordor Intelligence

The Space Mining & Robots Market size is estimated at 2.47 billion USD in 2025, and is expected to reach 4.34 billion USD by 2030, growing at a CAGR of 11.89% during the forecast period (2025-2030).

The space mining and space robotics industry is experiencing unprecedented growth driven by increasing government investments and technological advancements in robotics and artificial intelligence. Government space agencies worldwide are demonstrating a strong commitment through substantial budget allocations, with Japan allocating over USD 1.4 billion in 2022 for space development programs, including the H3 rocket and Engineering Test Satellite-9. The European Space Agency (ESA) has requested EUR 18.5 billion for 2023-2025 from its 22 member nations, highlighting the growing emphasis on space exploration technology and resource utilization. This surge in government funding is complemented by private sector investments, as exemplified by GITAI's successful Series B Extension funding round of approximately USD 30 million in 2023, aimed at accelerating space robotics technology development.

The industry is witnessing significant technological breakthroughs in autonomous systems and robotic capabilities designed specifically for extreme space environments. Advanced robotics companies are developing sophisticated systems capable of performing complex tasks such as on-orbit assembly, satellite servicing, and resource extraction. These developments are particularly evident in the successful demonstration of ISAM activities by GITAI in a simulated space environment, showcasing the potential for autonomous robotic manufacturing and assembly platforms. The integration of artificial intelligence and machine learning algorithms has enhanced the ability of space robots to operate with greater precision and autonomy in harsh conditions.

International collaboration and regulatory frameworks are evolving to support the growing space mining and robotics sector. Japan's implementation of dedicated space resource exploration and exploitation laws in 2021 marked a significant milestone, joining the United States, Luxembourg, and the United Arab Emirates in creating supportive regulatory environments. The European Space Agency's development of the European Robotic Arm, involving a consortium of 22 European companies from seven countries, demonstrates the increasing emphasis on international cooperation in advancing space robotics capabilities. These collaborative efforts are essential for addressing technical challenges and establishing standardized protocols for space resource utilization.

The industry is witnessing a paradigm shift towards sustainable space exploration technology and resource utilization. NASA's DART mission successfully demonstrated asteroid deflection capabilities, highlighting the advancing technological readiness for asteroid mining and potential resource extraction. Private companies and space agencies are increasingly focusing on developing reusable robotic systems and sustainable mining practices to minimize space debris and ensure the long-term viability of space operations. This emphasis on sustainability is driving innovation in robotic design, with companies developing multi-purpose robots capable of performing various tasks from exploration and mining to maintenance and assembly, maximizing efficiency while minimizing environmental impact in space.

Global Space Mining & Robots Market Trends and Insights

Nano and mini-satellites are poised to create demand in the market

- The classification of spacecraft by mass is one of the main metrics for determining the launch vehicle size and cost of launching satellites into orbit. In North America, during 2017-2022, around 45+ large satellites launched were owned by North American organizations. North American organizations operated more than 80 medium-sized satellites launched, and around 2,900+ small satellites were manufactured and launched in this region.

- Europe has witnessed significant growth over recent years, primarily driven by the increasing demand for different satellite masses. Satellite mass is one of the most critical factors influencing the European satellite manufacturing market. This is because different types of satellites require different masses, which, in turn, affects the launch vehicle market. For instance, during 2017-2022, a total of 571 satellites were launched in the region. Of these 571 satellites, minisatellites accounted for most of the shares, with 452 satellites launched into orbit, followed by 45 nanosatellites, 37 large satellites, 30 medium size satellites, and seven microsatellites.

- Satellite manufacturing has become an increasingly important industry in the Asia-Pacific region over recent years, driven by the need to meet the growing demand for advanced satellite capabilities. The range of satellite mass being manufactured in the Asia-Pacific region varies significantly, and this has a significant impact on the market's growth. For instance, during 2017-2022, a total of 470 satellites were launched in the region. Of these 470 satellites, medium satellites accounted for most of the shares, with 152 satellites launched into orbit, followed by 132 microsatellites, 78 large satellites, 66 nanosatellites, and 42 minisatellites.

-by-region,-Number-of-Satellites-Launched,-Global,-2017---2022.svg)

Rising developments across all types of satellites and increased usage for several applications is driving the spending on space programs across the world

- Global government expenditure for space programs hit a record of approximately USD 103 billion in 2021. In the North American region, which is the epicenter of space innovation and research, with the presence of the world's biggest space agency, NASA. GITAI, the world's leading space robotics company, completed a Series B Extension round of funding totaling JPY 4 billion (approximately USD 30 million) to accelerate and expand its business and technology development in the United States.

- European countries are also recognizing the importance of various investments in the space domain. They are increasing their spending on space activities and innovation to stay competitive and innovative in the global space industry. The European Space Agency (ESA) is requesting its 22 nations to back a budget of EUR 18.5 billion during 2023-2025. Germany, France, and Italy are the major contributors. In June 2021, a consortium of 22 European companies from seven countries built a robot for ESA. The launch and installation of the European Robotic Arm was a first for Europe and Russia in space. This was the long-awaited premiere of this European-made robot that followed 14 years of perseverance.

- Considering the increase in space-related activities in the Asia-Pacific region, in 2022, according to the draft budget of Japan, the space budget of the country was over USD 1.4 billion, which included the development of the H3 rocket, Engineering Test Satellite-9, and the nation's Information Gathering Satellite (IGS) program. Similarly, the proposed budget for India's space programs for FY22 was USD 1.83 billion. In 2022, South Korea's Ministry of Science and ICT announced a space budget of USD 619 million for manufacturing satellites, rockets, and other key space equipment.

Space Mining & Robots Market Geography Segment Analysis

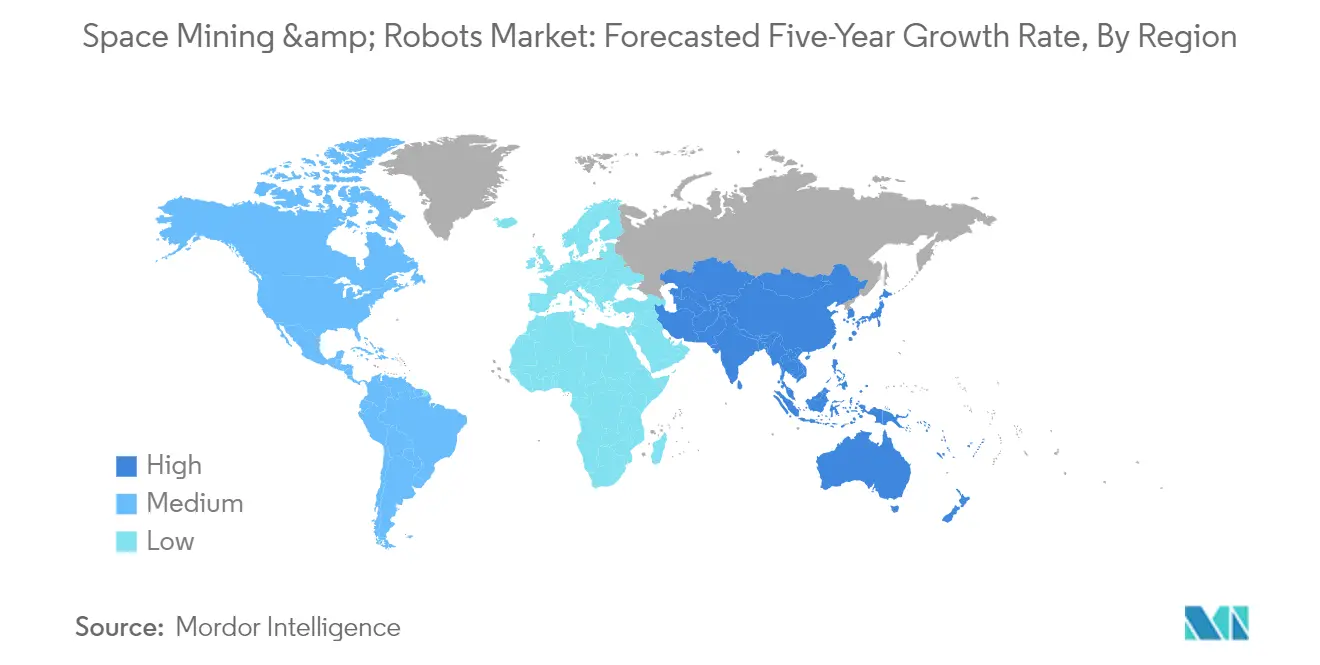

Space Mining & Robots Market in Asia-Pacific

The Asia-Pacific region has emerged as a significant player in the global space mining and space robotics market, commanding approximately 17% of the market share in 2024. The region's space industry is witnessing substantial transformation through increased investments in space exploration, mining activities, and robotic technologies. Countries across Asia-Pacific are emphasizing the development of new space robots and establishing robust infrastructure for space-related activities. The focus on exploiting space resources, particularly helium-3 from lunar surfaces, has become a key priority for major space agencies in the region. Government collaborations with private players have strengthened the ecosystem, fostering innovation and technological advancement in space robotics. The integration of artificial intelligence and advanced robotics in space missions has further accelerated market growth. Additionally, the region's commitment to developing autonomous space systems and establishing space mining capabilities has attracted significant investment from both public and private sectors.

Space Mining & Robots Market in Europe

Europe has demonstrated remarkable progress in the space mining market and robots sector, achieving an impressive growth rate of approximately 18% during the period 2019-2024. The region's advancement in space robotics technology has been driven by substantial investments in research and development, particularly in autonomous systems and artificial intelligence integration. European space agencies and private companies have been at the forefront of developing innovative robotic solutions for space exploration and mining operations. The region's strong focus on sustainable space activities and resource utilization has led to the development of sophisticated robotic systems capable of operating in extreme space environments. European countries have established comprehensive frameworks for space resource exploitation, supported by robust technological infrastructure and research facilities. The collaboration between academic institutions, research centers, and industry players has created a dynamic ecosystem for space robotics innovation. Furthermore, the region's emphasis on developing reusable space technologies and efficient mining solutions has positioned it as a global leader in the sector.

Competitive Landscape

Top Companies in Space Mining & Robots Market

Leading companies in this market are focusing heavily on technological advancement and innovation, particularly in developing autonomous robotic systems for space exploration robots and resource extraction. There is a clear trend toward establishing strategic partnerships with space agencies and other industry players to share expertise and resources. Companies are investing significantly in research and development to create more sophisticated robots capable of withstanding harsh space environments while performing complex tasks. Operational agility is demonstrated through the development of modular and adaptable robotic systems that can serve multiple purposes in space missions. Geographic expansion is primarily centered around establishing a presence in key space technology hubs, with many companies opening new facilities and research centers in strategic locations. Product innovation is largely driven by the need for more efficient and reliable space mining solutions, with emphasis on developing advanced robotic arms, autonomous rovers, and specialized space mining equipment.

Market Dominated by Established Space Players

The space mining and robots market exhibits a moderately consolidated structure, with major aerospace and defense conglomerates holding significant market share alongside specialized space robotics companies. Global players with extensive experience in space technology and substantial financial resources maintain dominant positions, while smaller specialized firms focus on developing niche technologies and solutions. The market is characterized by a mix of traditional space industry giants and innovative startups, creating a dynamic competitive environment that fosters both collaboration and competition. The presence of government space agencies as key customers has significant influence on market dynamics and competitive strategies.

Merger and acquisition activity in the market is primarily driven by larger companies seeking to acquire specialized robotics capabilities and innovative technologies. Strategic partnerships and joint ventures are common, particularly between established aerospace companies and emerging robotics specialists. Market entry barriers are substantial due to high technological requirements and significant capital investments needed for research and development. Regional players are increasingly gaining prominence through government support and specialized expertise in specific aspects of space robotics technology.

Innovation and Partnerships Drive Future Success

Success in this market increasingly depends on developing cutting-edge technologies while maintaining strong relationships with key stakeholders in the space industry. Incumbent companies must focus on continuous innovation in autonomous systems, artificial intelligence, and advanced materials to maintain their market position. Building strong partnerships with research institutions and government space agencies is crucial for accessing funding and securing contracts. Companies need to demonstrate capability in developing cost-effective solutions while maintaining high reliability standards. The ability to adapt to changing mission requirements and provide flexible, modular solutions will be crucial for maintaining competitive advantage.

For contenders looking to gain market share, focusing on specialized niches and developing unique technological capabilities offers the most promising path forward. Building expertise in specific areas such as lunar mining, debris removal, or in-orbit servicing can provide opportunities for market entry and growth. Regulatory compliance and safety standards will continue to play a crucial role in shaping competitive dynamics, particularly as space excavation activities increase. Companies must also consider the concentrated nature of end-users, primarily space agencies and large aerospace companies, while developing their market strategies. The risk of substitution remains relatively low due to the specialized nature of planetary rovers, but companies must continue to innovate to maintain their competitive edge.

Space Mining & Robots Industry Leaders

Astrobotic

iSpace Inc.

Maxar Technologies Inc.

MDA Ltd

Northrop Grumman Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2023: ispace inc announced that its HAKUTO-R Mission 1 lunar lander has successfully completed Success 5 of its Mission 1 Milestones by completing a month-long stable navigation and nominal cruise in deep space.

- January 2023: Motiv Space Systems announces it has been selected by the US Space Force’s innovation wing, SpaceWERX, for a Phase 1 STTR to develop robotically aided Active Debris Remediation services. Motiv is partnered with the U.S. Naval Research Laboratory (NRL), for the Orbital Prime contract.

- December 2022: Ispace's HAKUTO-R Mission 1 lander was successfully launched by a SpaceX Falcon 9 rocket. The lander carried 7 payloads and after the steady operational state of the lander was established, customer payloads were checked out individually.

Global Space Mining & Robots Market Report Scope

Asia-Pacific, Europe, North America are covered as segments by Region.| Asia-Pacific |

| Europe |

| North America |

| Rest of World |

| Region | Asia-Pacific |

| Europe | |

| North America | |

| Rest of World |

Market Definition

- Application - Various applications or purposes of the satellites are classified into communication, earth observation, space observation, navigation, and others. The purposes listed are those self-reported by the satellite’s operator.

- End User - The primary users or end users of the satellite is described as civil (academic, amateur), commercial, government (meteorological, scientific, etc.), military. Satellites can be multi-use, for both commercial and military applications.

- Launch Vehicle MTOW - The launch vehicle MTOW (maximum take-off weight) means the maximum weight of the launch vehicle during take-off, including the weight of payload, equipment and fuel.

- Orbit Class - The satellite orbits are divided into three broad classes namely GEO, LEO, and MEO. Satellites in elliptical orbits have apogees and perigees that differ significantly from each other and categorized satellite orbits with eccentricity 0.14 and higher as elliptical.

- Propulsion tech - Under this segment, different types of satellite propulsion systems have been classified as electric, liquid-fuel and gas-based propulsion systems.

- Satellite Mass - Under this segment, different types of satellite propulsion systems have been classified as electric, liquid-fuel and gas-based propulsion systems.

- Satellite Subsystem - All the components and subsystems which includes propellants, buses, solar panels, other hardware of satellites are included under this segment.

| Keyword | Definition |

|---|---|

| Attitude Control | The orientation of the satellite relative to the Earth and the sun. |

| INTELSAT | The International Telecommunications Satellite Organization operates a network of satellites for international transmission. |

| Geostationary Earth Orbit (GEO) | Geostationary satellites in Earth orbit 35,786 km (22,282 mi) above the equator in the same direction and at the same speed as the earth rotates on its axis, making them appear fixed in the sky. |

| Low Earth Orbit (LEO) | Low Earth Orbit satellites orbit from 160-2000km above the earth, take approximately 1.5 hours for a full orbit and only cover a portion of the earth’s surface. |

| Medium Earth Orbit (MEO) | MEO satellites are located above LEO and below GEO satellites and typically travel in an elliptical orbit over the North and South Pole or in an equatorial orbit. |

| Very Small Aperture Terminal (VSAT) | Very Small Aperture Terminal is an antenna that is typically less than 3 meters in diameter |

| CubeSat | CubeSat is a class of miniature satellites based on a form factor consisting of 10 cm cubes. CubeSats weigh no more than 2 kg per unit and typically use commercially available components for their construction and electronics. |

| Small Satellite Launch Vehicles (SSLVs) | Small Satellite Launch Vehicle (SSLV) is a three-stage Launch Vehicle configured with three Solid Propulsion Stages and a liquid propulsion-based Velocity Trimming Module (VTM) as a terminal stage |

| Space Mining | Asteroid mining is the hypothesis of extracting material from asteroids and other asteroids, including near-Earth objects. |

| Nano Satellites | Nanosatellites are loosely defined as any satellite weighing less than 10 kilograms. |

| Automatic Identification System (AIS) | Automatic identification system (AIS) is an automatic tracking system used to identify and locate ships by exchanging electronic data with other nearby ships, AIS base stations, and satellites. Satellite AIS (S-AIS) is the term used to describe when a satellite is used to detect AIS signatures. |

| Reusable launch vehicles (RLVs) | Reusable launch vehicle (RLV) means a launch vehicle that is designed to return to Earth substantially intact and therefore may be launched more than one time or that contains vehicle stages that may be recovered by a launch operator for future use in the operation of a substantially similar launch vehicle. |

| Apogee | The point in an elliptical satellite orbit which is farthest from the surface of the earth. Geosynchronous satellites which maintain circular orbits around the earth are first launched into highly elliptical orbits with apogees of 22,237 miles. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the historical and forecast years have been provided in revenue and volume terms. For sales conversion to volume, the average selling price (ASP) is kept constant throughout the forecast period for each country, and inflation is not a part of the pricing.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms.