Market Overview

| Study Period | 2020 - 2031 |

|---|---|

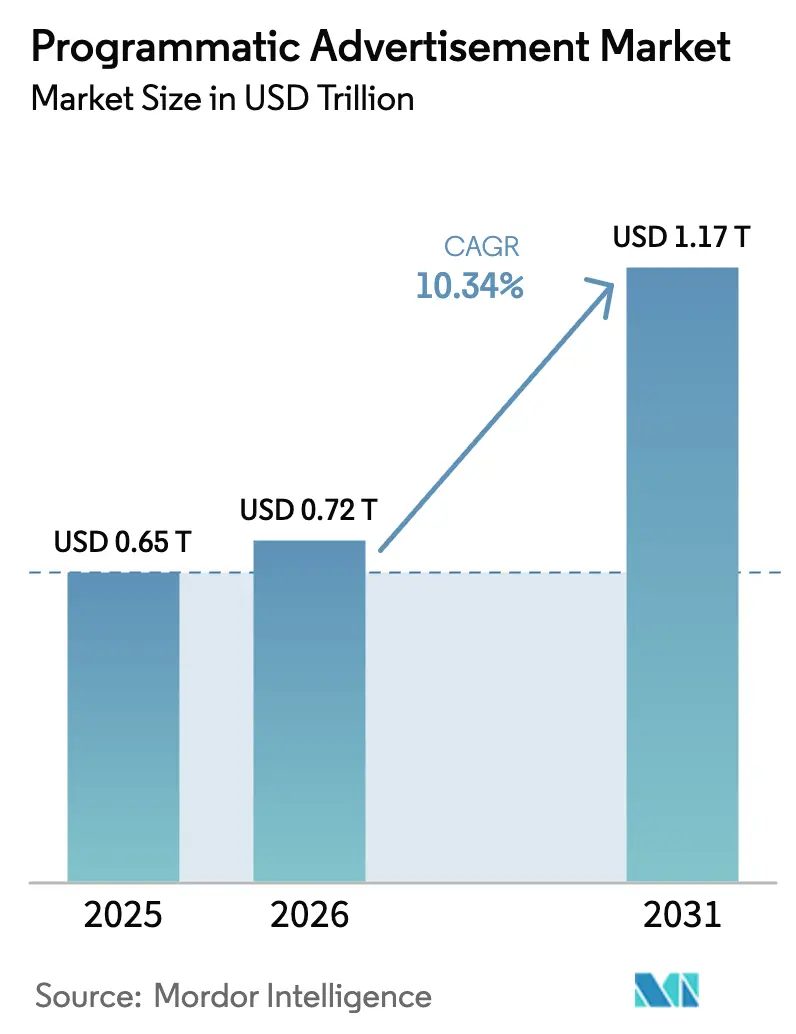

| Market Size (2026) | USD 0.72 Trillion |

| Market Size (2031) | USD 1.17 Trillion |

| Growth Rate (2026 - 2031) | 10.34% CAGR |

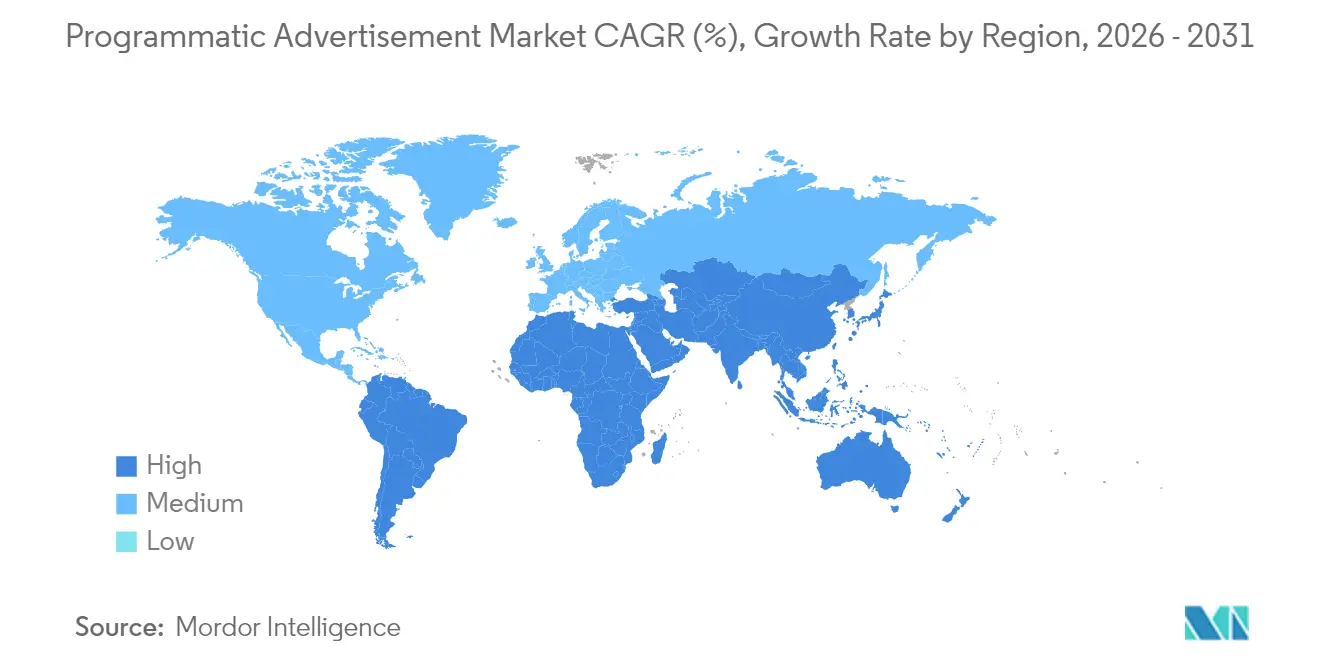

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Programmatic Advertisement Market Analysis by Mordor Intelligence

Programmatic advertising market size in 2026 is estimated at USD 0.72 trillion, growing from 2025 value of USD 0.65 trillion with 2031 projections showing USD 1.17 trillion, growing at 10.34% CAGR over 2026-2031. Automated buying now serves as the core operating system for digital media, expanding beyond open-exchange display into streaming television, retail media, and digital out-of-home environments. Buyers that lean on real-time optimisation report higher return on ad spend, prompting even conservative brand teams to shift budgets from manual insertion orders. Liquidity created by this migration lifts fill rates and average clearing prices, which in turn encourages fresh investments in optimisation technology and reduces the minimum viable scale for smaller advertisers to compete. Over the forecast horizon, the programmatic advertising market will converge formats and devices into single-workflow buying, with privacy regulation accelerating contextual intelligence and clean-room adoption to offset third-party-cookie loss. Emerging economies, unburdened by legacy ad-tech, are moving directly to cloud-native stacks, helping to sustain double-digit revenue growth, while transparent, auditable supply chains are expected to capture a disproportionate share as buyers reward measurable accountability.

Key Report Takeaways

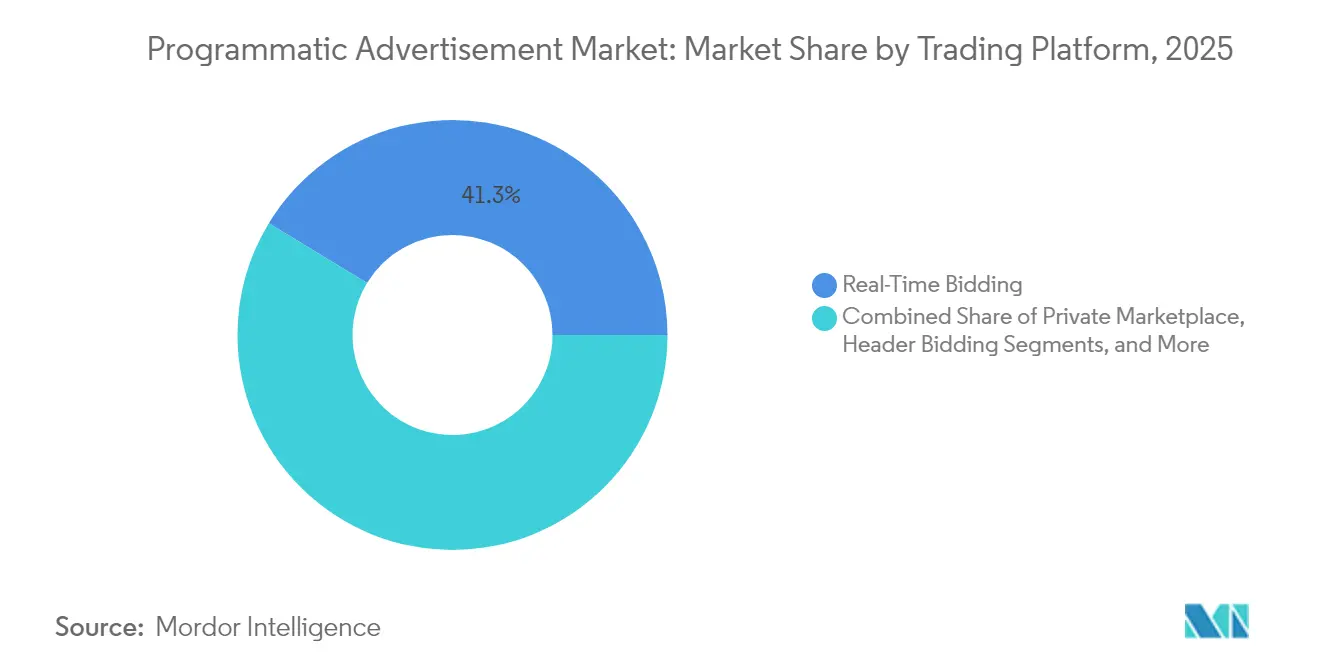

- By trading platform, Real-Time Bidding led with 41.30% of programmatic advertising market share in 2025, while Programmatic Guaranteed is projected to expand at a 24.15% CAGR between 2026-2031.

- By advertising channel, display banners accounted for 34.25% share of the programmatic advertising market size in 2025, whereas programmatic video is forecast to climb at a 25.1% CAGR to 2031.

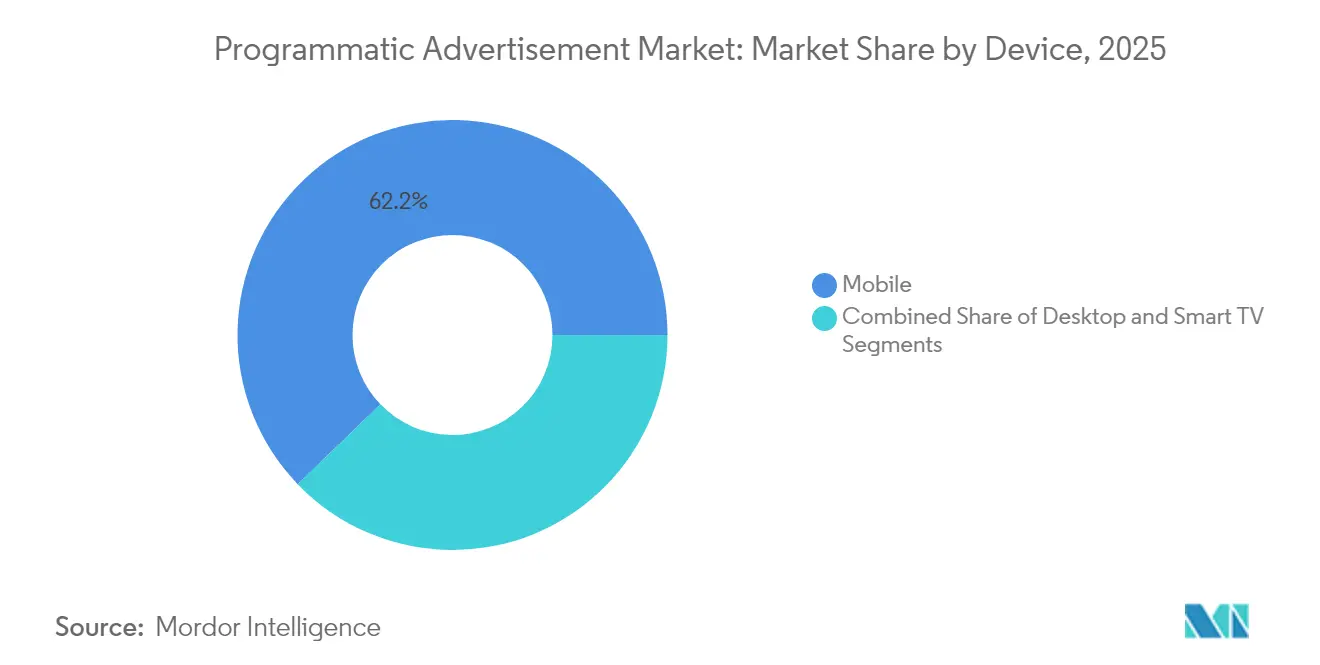

- By device, mobile commanded 62.20% of programmatic advertising market share in 2025; smart-TV impressions are expected to rise at an 17.95% CAGR through 2031.

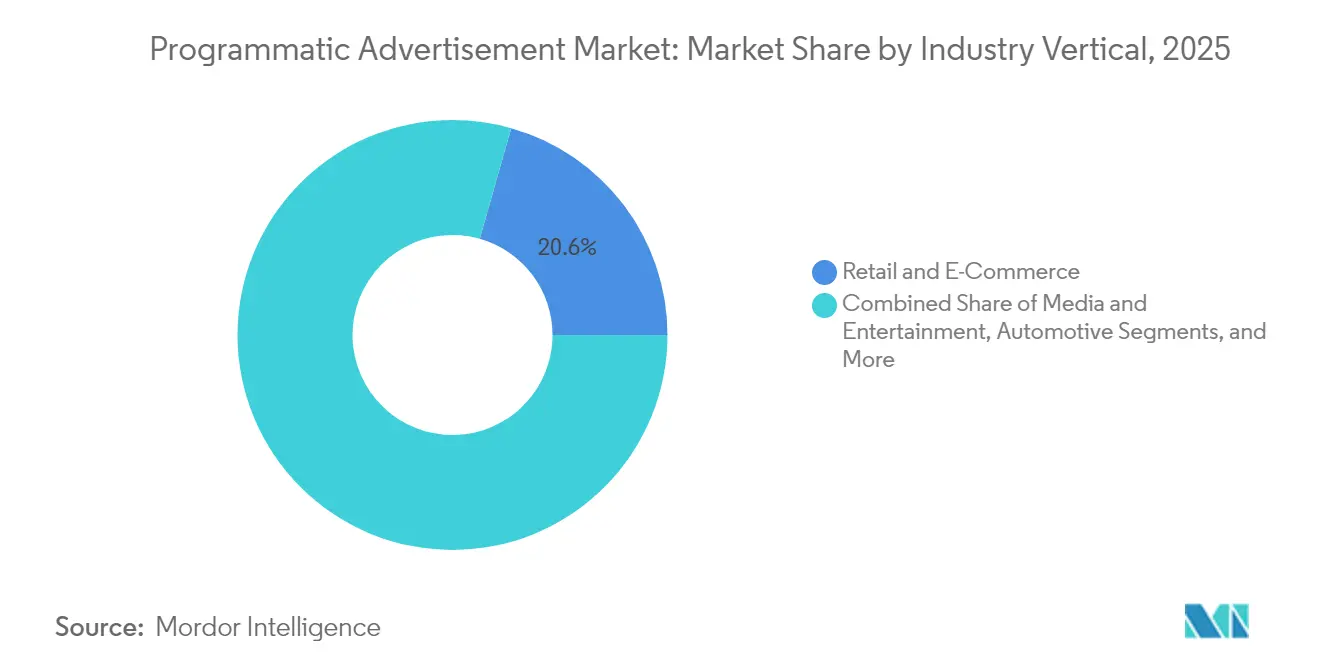

- By industry vertical, Retail & E-Commerce held 20.60% share of the programmatic advertising market size in 2025, while Media & Entertainment is advancing at a 13.74% CAGR to 2031.

- By enterprise size, large enterprises contributed 67.30% of spend in 2025, whereas SMB outlays are set to increase at a 14.66% CAGR through 2031.

- By geography, North America maintained 37.50% programmatic advertising market share in 2025; Asia-Pacific is the fastest-growing region at a 12.3% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Programmatic Advertisement Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Premium Inventory Migration to Private Marketplaces Fuelling CPMs | +2.1% | Global, with higher impact in North America and Europe | Medium term (3-4 yrs) |

| AI-Driven Bid Optimisation Elevating ROAS in Europe | +1.8% | Europe, North America, with spillover to APAC | Medium term (3-4 yrs) |

| Connected-TV Programmatic Surge in the US and Japan | +2.4% | US, Japan, with growing impact in Europe | Short term (≤2 yrs) |

| Retail-Media First-Party Data Unlocking Budgets | +1.5% | Global, with highest impact in North America | Medium term (3-4 yrs) |

| Contextual Targeting Renaissance Post-Cookie | +1.2% | Global | Medium term (3-4 yrs) |

| 5G-Enabled Real-Time Mobile RTB Growth in Asia | +0.9% | APAC core, with spillover to emerging markets | Long term (≥5 yrs) |

| Source: Mordor Intelligence | |||

Premium Inventory Migration to Private Marketplaces

Premium publishers continued to shift flagship inventory into invitation-only environments throughout 2024, lifting average clearing prices as brand-safety assurances Magnite. Buyers and sellers alike increasingly default to private deals because closed auctions combine higher revenue certainty with reduced fraud exposure. One global news outlet bundled live-event slots with lifestyle content in early 2025 and secured CPMs more than one-third above its open-exchange rate. The structural outcome is that remnant impressions will remain in open exchanges while high-value supply gravitates to curated marketplaces, effectively redrawing liquidity maps. As this migration gains momentum, transparent supply paths and auditable reporting standards become table stakes for premium demand.

AI-Driven Bid Optimisation

Machine-learning models that predict post-click value moved from pilot to mainstream in 2024 and were embedded across leading demand-side platforms by Q1 2025 [1]Basis Technologies, “BasisAI Drives 5x Advertising Performance Increase for Agencies,” basis.com. A European subscription service recorded a 35% uplift in six-month revenue per advertising dollar after applying lifetime-value-weighted bidding, and retailers now adjust bids based on SKU-level margin contribution. These examples show management focus pivoting from cost control to growth acceleration as algorithms refine bid prices in real time. The net effect is a redefinition of success metrics around incremental profit rather than impressions served, deepening the reliance on data-science talent within in-house media teams. Competitive advantage increasingly hinges on proprietary predictive datasets coupled with fast feedback loops.

Connected-TV Programmatic Surge

CTV inventory expanded rapidly in 2024, with programmatic transactions reaching three-quarters of all impression-level buys within the channel [2]The Trade Desk, “Vizio Boosts Programmatic Connected-TV Revenue with OpenPath,” thetradedesk.com. A major smart-TV operating-system owner documented a 40% revenue gain after implementing a direct supply-path model that links buyers straight to device-level inventory. In Japan, average daily streamed content minutes overtook broadcast TV for the first time in January 2025, underscoring the shift in living-room behaviour. Advertisers increasingly treat CTV as a performance channel, marrying household exposure data with commerce signals to close measurement loops. As more broadcasters enable programmatic guaranteed in long-form content, CTV pricing power is likely to rise, reinforcing its centrality in omnichannel strategies.

Retail-Media First-Party Data Unlocking Budgets

Supermarkets, marketplaces, and specialty retailers commercialised rich shopper graphs via self-serve portals throughout 2024, making SKU-level targeting mainstream. A consumer-electronics brand that blended a retailer’s purchase data with programmatic CTV doubled attributable sales during a 2025 back-to-school campaign. Closed-loop reporting shortens learning cycles, drives repeat budgets, and positions retailers as full-funnel media owners. As more chains embed clean-room integrations, deterministic purchase data will flow into cross-channel bidding, tightening the feedback loop between exposure and transaction. This data privilege is poised to shift budget share from open web display to retailer-owned ecosystems

Restraints Impact Analysis of Programmatic Advertisement Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Third-Party-Cookie Loss Shrinking ID Pools in Europe | -1.7% | Europe, with spillover to North America | Short term (≤2 yrs) |

| Ad-Fraud and Supply-Chain Opacity in Emerging Markets | -1.1% | Emerging Markets, particularly APAC and Latin America | Long term (≥5 yrs) |

| Programmatic Talent Scarcity Among SMB Advertisers | -0.8% | Global, with higher impact in emerging markets | Medium term (3-4 yrs) |

| Divergent Privacy Laws Stalling Cross-Border Buys | -0.6% | Global, with highest impact in cross-border campaigns | Long term (≥5 yrs) |

| Source: Mordor Intelligence | |||

Third-Party-Cookie Loss Shrinking ID Pools in Europe

Europe’s stringent privacy regime accelerated identifier contraction in 2024 when a multi-market publisher group reported a 20% drop in third-party IDs immediately after new policy enforcement. Half of that loss was recovered through first-party sign-ins and encrypted email hashes, leading to higher win rates and lower impression waste for participating advertisers. Smaller yet consented audiences demonstrate scalable outcomes, indicating that addressability anchored in publisher relationships will shape future targeting frameworks. Nonetheless, transition costs and measurement disruptions constrain short-term growth, shaving an estimated 1.7 percentage points from the projected CAGR across the programmatic advertising market.

Ad-Fraud and Supply-Chain Opacity in Emerging Markets

Invalid traffic remains elevated where verification layers are thin. A 2024 benchmark showed effective reach on loosely curated supply paths improving from 36% to 44% year on year, but still leaving more than half of the impressions of dubious value MediaPost. In early 2025 a South-East-Asian buyer consortium employed inclusion lists across mobile web and achieved a 40% viewability lift while cutting fraud flags by one-third. Although curated buying mitigates risk, it raises operational complexity for smaller advertisers. Persistently opaque inventory could subtract 1.1 percentage points from the global growth rate until verification standards converge with mature-market norms.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Programmatic Advertisement Market Segment Analysis

By Trading Platform:

Hybrid Paths Redefine Deal MixReal-Time Bidding accounted for 41.30% of programmatic advertising market share in 2025, underscoring its prominence for incremental reach. Yet the segment’s proportion is gradually declining as Programmatic Guaranteed accelerates at a 24.15% CAGR to 2031, reflecting advertiser demand for fixed-price certainty in premium slots. Publishers that bundled episodic content and live news into guaranteed portfolios sold out weeks ahead of schedule, demonstrating latent demand for assured delivery. A hybrid future is emerging in which buyers maintain open auctions for scale while reserving strategic moments through guaranteed pipes, increasing platform diversification. Supply-side partners are therefore expanding APIs to accommodate multi-deal-type execution in a single workflow.

Programmatic advertising market participants recognise that guaranteed deals improve forecast accuracy and yield stability, attracting brand dollars once confined to linear television. Meanwhile, real-time auctions continue to innovate with bid-shading and floor-price automation. The coexistence of these paths encourages technology vendors to develop consolidated dashboards that visualise performance across deal types, reducing operational friction. Over the forecast period, trading partners that deliver cross-channel, multi-deal governance will capture outsized wallet share, particularly from brands centralising omnichannel budgets.

By Advertising Channel / Format:

Video Overtakes Display in Growth ContributionDisplay banners still represented 34.25% of impressions and remain indispensable for retargeting and frequency balancing. Nevertheless, programmatic video is set to capture the dominant share of incremental spend as its market size grows at a 25.1% CAGR through 2031. Short-form content on social feeds complements long-form streaming on living-room screens, forming contiguous video journeys that multiply touchpoints throughout the day. A European automotive brand combined vertical video with adaptive six-second bumpers and saw visit intent rise 28%, illustrating creative synergies.

As buyers integrate rich-media, audio, and emerging immersive units into unified video budgets, the programmatic advertising market size attached to video formats is poised to widen further. Measurement vendors are responding with unified reach curves that aggregate connected-TV, mobile, and out-of-home exposures into a single, deduplicated metric set. The cross-format orchestration of creative assets now differentiates leading campaigns from median performers, spurring agencies to invest in cloud-based asset-versioning and AI-driven editing suites.

By Device:

Mobile Dominates, Smart-TV AcceleratesMobile devices delivered 62.20% of global impression volume in 2025, reflecting smartphone ubiquity and durable app engagement. Smart-TV sets, however, represent the fastest-growing endpoint, projected to expand at an 17.95% CAGR to 2031. A sporting-goods retailer’s January 2025 initiative used smart-TV prospecting followed by mobile retargeting within two hours, producing a 23% lift in in-app conversions. Cross-device identity resolution, therefore, becomes indispensable for sequential storytelling.

Programmatic advertising market size attributed to desktop remains meaningful for high-consideration purchases in finance and travel, where larger screens aid form completion. Yet as privacy frameworks restrict user-level identifiers, deterministic device graphs anchored in opt-in environments gain prominence. Vendors able to string together household-level smart-TV exposures with individual mobile signal trails will command premium CPMs, elevating the strategic value of proprietary device graphs.

By Industry Vertical:

Retail Retains Scale, Media Leads GrowthRetail & E-Commerce controlled 20.60% of the programmatic advertising market size in 2025 by leveraging shopper-level data to inform bidding and creative sequences. A 2025 flash sale from a fashion marketplace, powered by live-countdown banners and purchase-probability algorithms, doubled daily revenue against control, reaffirming commerce-media momentum. Media & Entertainment, while smaller in absolute spend, is the fastest-growing vertical at a 13.74% CAGR as streaming services unlock tier-one inventory.

Financial services, automotive, and healthcare verticals are accelerating programmatic adoption yet face complex compliance constraints. Financial advertisers increasingly collaborate with publishers in encrypted environments to match first-party data without leaking personal identifiers. As deterministic data becomes ubiquitous, vertical-specific creative frameworks and measurement currencies will expand, creating bespoke demand for specialist agencies.

By Enterprise Size:

SMBs Close Capability GapLarge enterprises generated 67.30% of programmatic spend in 2025, enabled by in-house trading desks and clean-room platforms that connect loyalty data to publisher signals. Still, SMB spending is forecast to grow at a 14.66% CAGR through 2031. A midwestern home-improvement chain that tested an AI budget-allocation tool in early 2025 cut cost-per-lead by 30% within three weeks, showcasing the democratisation of sophisticated optimisation.

Cloud-native self-serve interfaces launched during the 2024 holiday campaigns lowered entry barriers, letting SMBs tap the programmatic advertising market infrastructure once reserved for global conglomerates. Payment-on-delivery models and templated creative further reduce barriers, fostering a more diverse auction landscape. Vendors that facilitate low-friction onboarding and automated brand-safety controls will be best positioned to capture the long tail of advertisers.

Geography Analysis

North America Programmatic Advertisement Market

North America sustained a 37.50% programmatic advertising market share in 2025, cementing its status as the largest regional hub. Political election cycles injected fresh funds that remained in automated workflows after proving efficient. Supply-path optimisation continues to shorten the distance between publisher and buyer, lifting publisher yield and lowering demand-side fees. Transparent routes are expected to lock in buyer loyalty, reinforcing the region’s role as the test bed for new measurement standards such as clean-room-based reach verification and outcome reporting.

APAC Programmatic Advertisement Market

Asia-Pacific is forecast to expand at a 12.3% CAGR to 2031, making it the fastest-growing region by a clear margin. Mobile-first consumer behavior and rapid e-commerce adoption fuel impression liquidity, especially in India and Indonesia, where app-centric ecosystems bypass desktop legacies. A Southeast-Asian streaming app’s real-time ad insertion during 2025 sporting events achieved record view-through rates, highlighting regional readiness for advanced server-side ad insertion. Governments are drafting privacy statutes modelled on European precedents, prompting vendors to embed consent frameworks from inception. This proactive compliance stance could yield a structurally cleaner supply pool than mature markets faced in earlier growth waves.

EMEA and LATAM Programmatic Advertisement Market

Europe remains pivotal despite stricter regulations that trimmed third-party-cookie pools. Publishers double down on authenticated traffic, and early encrypted-email-hash collaborations delivered a 17% boost in qualified banking applications versus cookie-based retargeting. Although compliance raises operational overhead, deterministic addressability is stabilising performance, keeping the programmatic advertising market size in the region on a mid-single-digit growth path. Latin America and the Middle East and Africa trail in absolute spend but register rapid relative growth, driven by smartphone penetration and urban out-of-home digitisation. Investors are funnelling capital into regional verification start-ups, signalling advertiser confidence in medium-term scalability.

Competitive Landscape

Integrated platform ecosystems and independent point solutions coexist, shaping a competitive field defined by data-scale and transparency trade-offs. In February 2025, a content-recommendation network closed a USD 900 million acquisition of a global video technology firm, creating an omnichannel marketplace that touches more than 2 billion monthly users [3]Outbrain, “Outbrain Completes Acquisition of Teads,” investors.outbrain.com. The deal demonstrates how horizontal scale across formats becomes a defensive moat as buyers demand consolidated reach.

Identity and measurement infrastructure form the second pillar of consolidation. In January 2025, a global data-services firm acquired an identity-activation company to merge publisher first-party data with credit-file precision. The integration underscores market preference for privacy-compliant addressability built on durable identifiers. Supply-side optimisation also saw activity: a telecommunications company bought a digital-out-of-home technology provider for USD 600 million, planning to mesh subscriber insights with roadside screen inventory[4]T-Mobile, “T-Mobile to Acquire Vistar Media DOOH Advertising,” t-mobile.com. Such moves aim to simplify ad delivery logistics and secure incremental publisher share in high-growth sub-channels.

Cross-industry partnerships that blend proprietary datasets with bidding technology have intensified. A self-serve supply-side vendor joined forces with a small-business accounting-software provider to feed anonymised transactional insights into biddable segments, improving B2B conversion propensity PubMatic. With high-fidelity consented signals emerging as the defining competitive asset, firms that control premium first-party data—and the pipes that activate it—are positioned to set trading terms. Independent demand-side technology platforms continue to differentiate through transparency, offering buyer-controlled algorithms and log-level data access that large walled gardens restrict.

Programmatic Advertisement Industry Leaders

War Room Holdings, Inc

MediaMath

Digilant

Fyber N.V.

SmartyAds

- *Disclaimer: Major Players sorted in no particular order

Programmatic Advertisement Market Companies Covered in this Report

- Alphabet Inc. (Google Ads)

- Meta Platforms, Inc.

- Amazon.com, Inc.

- The Trade Desk, Inc.

- Magnite, Inc.

- PubMatic, Inc.

- Index Exchange, Inc.

- Verizon Communications Inc. (Yahoo)

- Adobe Inc.

- Microsoft Corp. (Xandr)

- MediaMath Inc.

- War Room Holdings, Inc.

- Digilant

- Fyber N.V.

- SmartyAds

- Choozle, Inc.

- Zeta Global Holdings Corp.

- Criteo S.A.

- Roku, Inc.

- AppLovin Corp.

- OpenX Technologies, Inc.

- TripleLift, Inc.

- Adform A/S

Recent Industry Developments in Programmatic Advertisement Market

- February 2025: A content-recommendation network completed the acquisition of a global video technology firm for USD 900 million, forming an omnichannel outcome-driven platform with USD 1.7 billion annual ad spend.

- January 2025: A telecommunications company announced the purchase of a digital-out-of-home technology provider for approximately USD 600 million to merge subscriber insights with roadside screen inventory.

- January 2025: An independent demand-side platform acquired a metadata analytics start-up to bolster impression-level valuation models across open internet supply.

- January 2025: A commerce-media specialist bought a customer-data infrastructure company for USD 300 million, strengthening real-time decisioning in e-commerce environments.

Programmatic Advertisement Market Report Scope and Research Methodology

Market Definition and Coverage

Our study defines the programmatic advertising market as all digital ad impressions traded through automated platforms, including real-time bidding exchanges, private marketplaces, and programmatic guaranteed pipes, irrespective of format, device, or vertical.

Scope exclusion: Spend routed through fully manual insertion-order buying for print, linear broadcast, or terrestrial radio sits outside this assessment.

Segments Covered in This Report

- By Trading Platform

- Real-Time Bidding (Open Auction)

- Private Marketplace

- Programmatic Guaranteed

- Preferred Deals (Unreserved Fixed-Rate)

- Header Bidding

- By Advertising Channel / Format

- Display Banner

- Video

- Mobile Display

- Connected TV (CTV)

- Digital Out-of-Home (DOOH)

- Others

- By Device

- Desktop

- Mobile

- Smart TV

- By Industry Vertical

- Retail and E-Commerce

- Media and Entertainment

- Automotive

- BFSI

- Healthcare and Pharma

- Others

- By Enterprise Size

- SMBs

- Large Enterprises

- By Geography

- North America

- United States

- Canada

- Latin America

- Brazil

- Argentina

- Mexico

- Rest of Latin America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- South Korea

- India

- Australia

- New Zealand

- Rest of Asia-Pacific

- Middle East and Africa

- United Arab Emirates

- Saudi Arabia

- South Africa

- Rest of Middle East and Africa

- North America

Data Sources, Market Sizing, and Validation

Primary Research

We spoke with demand-side platform product heads, premium publishers, media-agency buyers, and brand marketers across North America, Europe, Asia-Pacific, and the Gulf. Their inputs sharpened adoption ratios for connected-TV, retail-media, and pDOOH, and validated auction win-rate assumptions that secondary data could not fully surface.

Desk Research

Our analysts first mapped global digital ad outlays using freely accessible sources such as the Interactive Advertising Bureau revenue survey, the United Nations ITU connectivity database, Ofcom communications reports, and select national statistics portals. These feeds clarified inventory volumes, CPM inflation, and screen-time trends. We then tapped D&B Hoovers for platform financials, Dow Jones Factiva for deal flow, and Questel for ad-tech patent filings that signal upcoming supply shifts. A running news sweep on major privacy regulations rounded out the context. The sources listed are illustrative, and many additional publications supported data gathering and cross-checks.

Market-Sizing & Forecasting

We begin with a top-down reconstruction anchored on certified digital ad spend, which is then filtered through historic programmatic penetration benchmarks and adjusted for device mix shifts. Select bottom-up approximations, DSP revenue disclosures, sampled average CPM × impression counts, and channel checks serve as reasonability gates. Key variables in the model include smartphone penetration, average data consumption per user, incremental connected-TV households, cookie-less inventory share, and global GDP outlook. A multivariate regression, stress-tested through scenario analysis, projects each driver forward and produces the 2025-2030 trajectory. Data gaps in bottom-up rolls are bridged with region-specific interpolation guided by primary interview ranges.

Data Validation & Update Cycle

Model outputs pass three layers of variance screening, peer review, and senior analyst sign-off. We refresh every twelve months, with interim updates triggered by material events such as privacy rule enforcement or major M&A, and perform a last-mile sense check immediately before release.

How Mordor Intelligence's Programmatic Advertisement Market Size Compares to Other Published Estimates

Published values for this market often differ because firms start from unlike scopes, apply divergent penetration ratios, and refresh data on separate cadences.

Key gap drivers include whether estimates net publisher rebates, how wide the definition stretches beyond RTB, the aggressiveness of long-range CPM escalation, and the frequency of regulatory resets. Mordor's disciplined use of transparent variables, annual refresh, and dual-lens validation reduces those variances.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 650 B (2025) | Mordor Intelligence | |

| USD 802 B (2024) | Regional Consultancy A | Includes all digital display and video spend without isolating automated transactions, inflating base |

| USD 64 B (2024) | Trade Journal B | Counts only RTB deals, omits private marketplace and guaranteed flows, yielding a narrow view |

| USD 12 B (2024) | Global Consultancy C | Tracks managed-service billings in twenty nations and excludes self-serve platforms, leading to understatement |

The comparison shows that estimates swing widely when scope and variable choices diverge, which is why Mordor's balanced, transparent build remains the dependable starting point for strategic decisions.

Key Questions Answered in the Report

What is the current market size of programmatic advertising?

The market stands at USD 0.72 Trillion in 2026.

How fast will the market grow?

A CAGR of 10.34 % is forecast, propelling revenue to USD 1.17 Trillion by 2031

Which region leads in market share?

North America holds the largest share at 37.50 %, supported by widespread connected-TV adoption

Why is Programmatic Guaranteed expanding rapidly?

Advertisers gain inventory certainty and publishers secure predictable yield, prompting projected 24.15 % CAGR in this sub-segment.

What years does this Global Programmatic Advertisement Market cover?

The report covers the Global Programmatic Advertisement Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Global Programmatic Advertisement Market size for years: 2026, 2027, 2028, 2029, 2030 and 2031.

How are brands adapting to cookie deprecation?

They are increasing investment in contextual intelligence and first-party clean-room collaborations, which maintain reach without third-party IDs

What role do retail media networks play?

They monetise shopper data, enabling deterministic targeting that delivers measurable sales lifts for participating brands.

Page last updated on: