Polymer Electrolyte Membrane Fuel Cells (PEMFC) Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

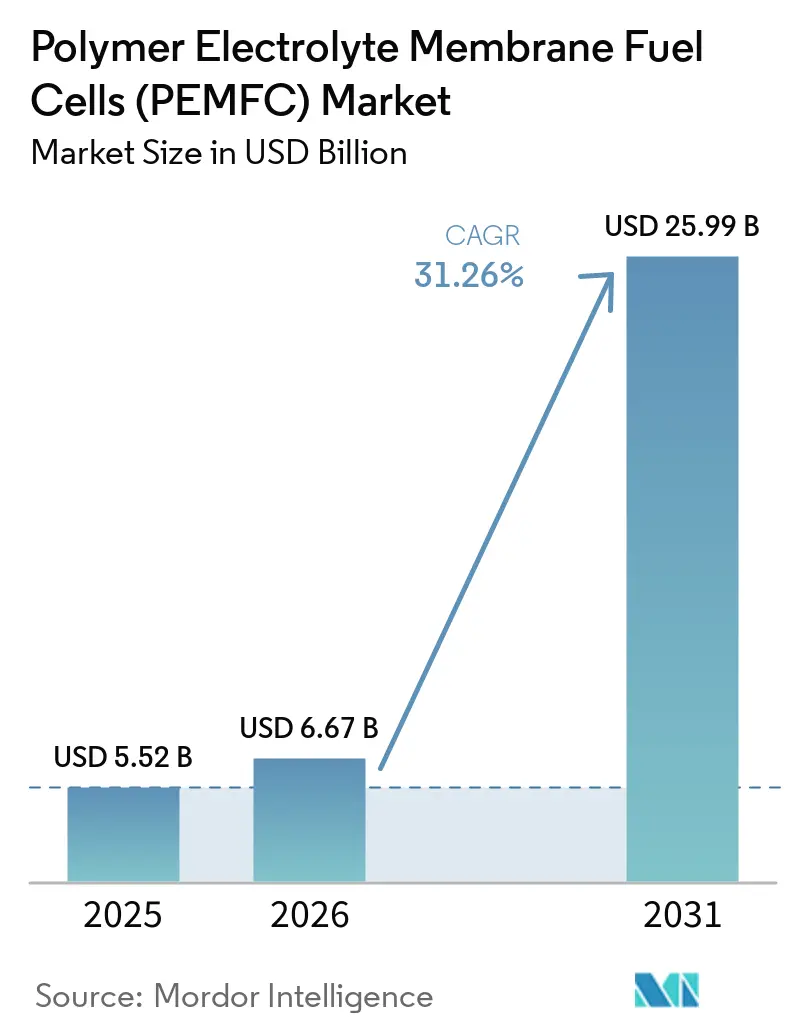

| Market Size (2026) | USD 6.67 Billion |

| Market Size (2031) | USD 25.99 Billion |

| Growth Rate (2026 - 2031) | 31.26% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Polymer Electrolyte Membrane Fuel Cells (PEMFC) Market Analysis by Mordor Intelligence

The Polymer Electrolyte Membrane Fuel Cells (PEMFC) Market size is estimated at USD 6.67 billion in 2026, and is expected to reach USD 25.99 billion by 2031, at a CAGR of 31.26% during the forecast period (2026-2031).

Manufacturing scale-up, supportive zero-emission mandates, and expanding hydrogen corridors now align to push stack costs below USD 60 per kW, tipping total cost of ownership in favor of fuel cell electric trucks and resilient stationary systems. California’s Advanced Clean Fleets rule, the European Union’s Fit for 55 package, and China’s dual-credit regime collectively guarantee long-term demand visibility for vehicle makers, while gigafactory-class assembly lines compress per-unit overheads. In parallel, second-life automotive modules repurposed into containerized generators extend asset life cycles and reduce end-of-life disposal liabilities, reinforcing a circular supply chain. Increasing grid outages in North America and Europe further heighten interest in on-site fuel cell backup, especially across data centers and telecom nodes.

Key Report Takeaways

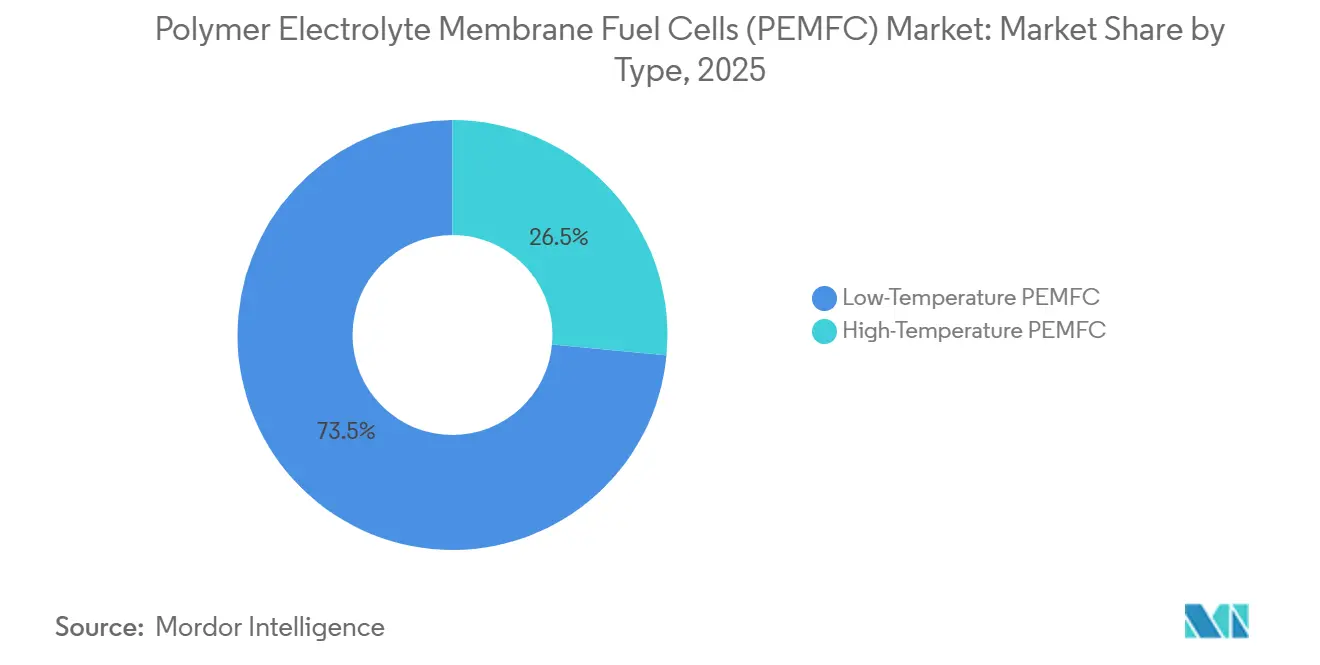

- By type, low-temperature PEM stacks held 73.5% of 2025 revenue; high-temperature variants are set to expand at a 35.8% CAGR through 2031.

- By cooling method, liquid architectures captured 70.1% of the 2025 share; air-cooled solutions are forecast to grow at a 28.9% CAGR on cost-sensitive portable duties.

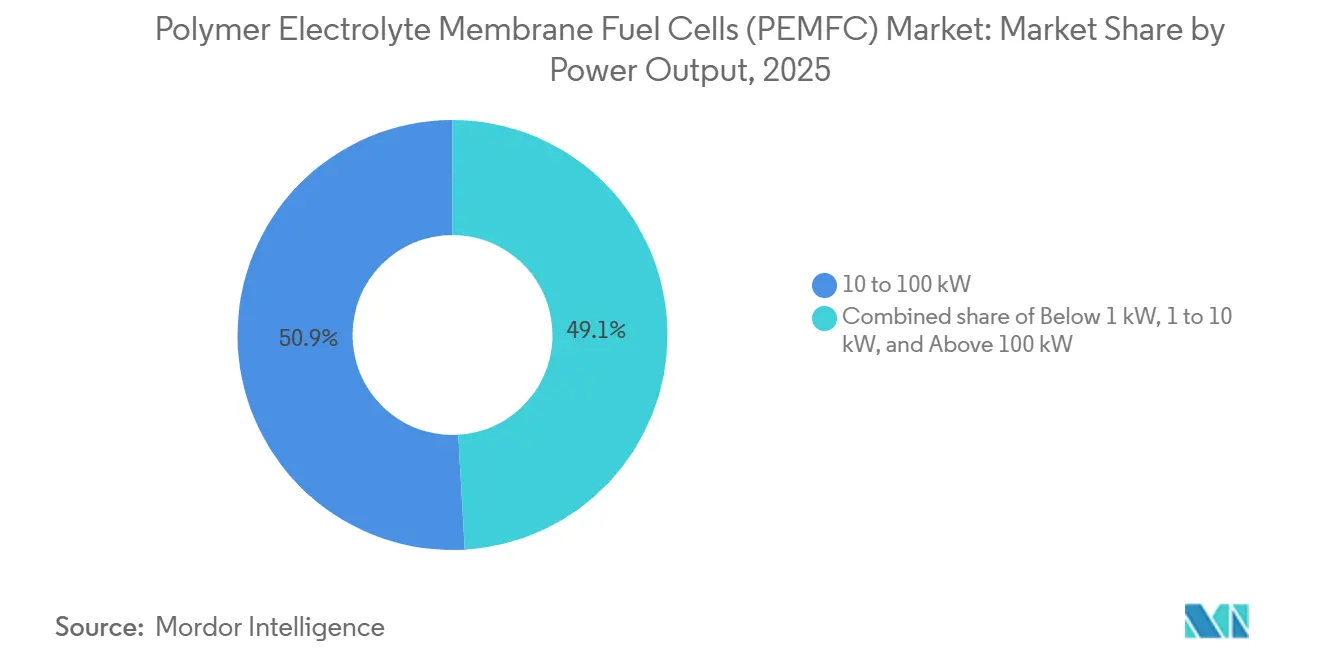

- By power output, the 10 kW–100 kW band commanded 50.9% of the polymer electrolyte membrane fuel cell market share in 2025; stacks above 100 kW will rise at 37.2% through 2031.

- By component, membrane electrode assemblies accounted for 58.3% of the 2025 value; catalysts posted the quickest climb at a 36.4% CAGR as PFAS-free formulations unlock new entrants.

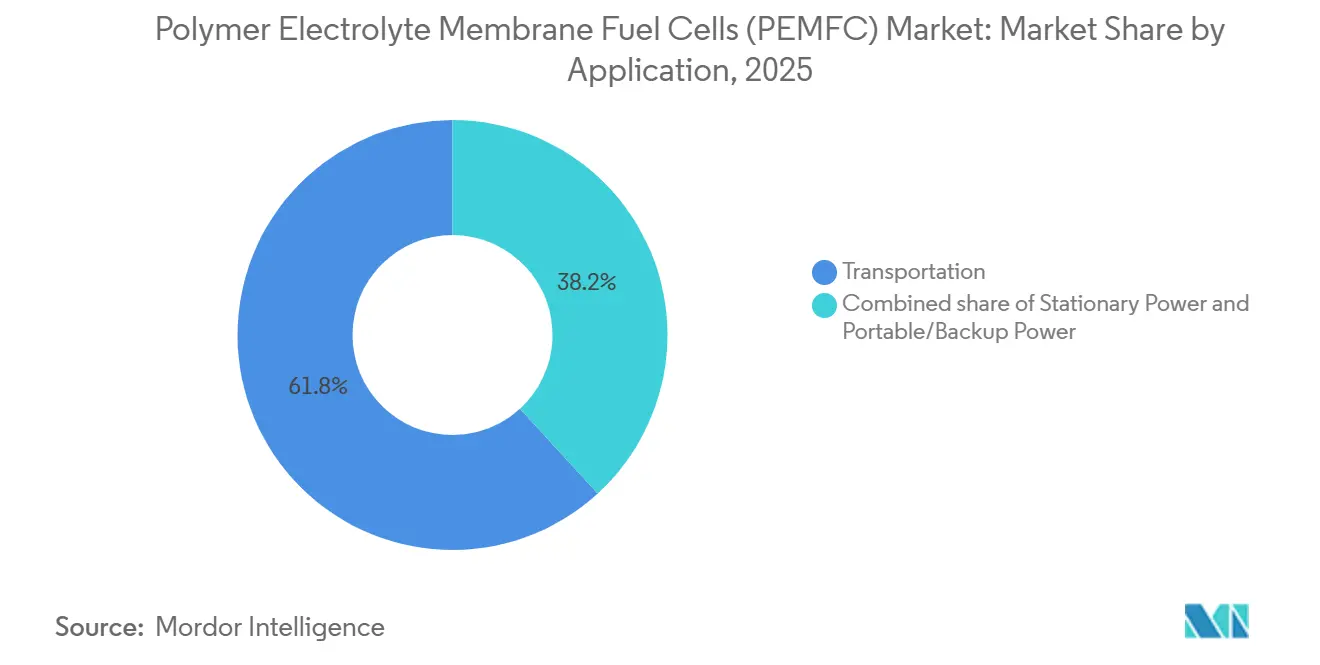

- By application, transportation dominated with 61.8% of demand in 2025; stationary power leads growth at 38.9% CAGR as data center resilience gains priority.

- By end-user industry, transportation dominated with 61.8% of demand in 2025; utilities led growth at 39.3% CAGR.

- By geography, Asia–Pacific controlled 47.6% of the global share in 2025 and is projected to rise at 33.1% through 2031 on aggressive corridor build-outs and vehicle subsidies.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Polymer Electrolyte Membrane Fuel Cells (PEMFC) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government zero-emission mandates & subsidies | +8.2% | Global, with concentration in EU, China, California, South Korea | Medium term (2-4 years) |

| Rapid decline in PEM stack $/kW due to gigafactory-scale production | +7.5% | APAC core, spill-over to North America & EU | Short term (≤ 2 years) |

| Expansion of hydrogen refueling infrastructure in Asia, EU & US | +6.8% | Asia-Pacific, Europe, North America | Medium term (2-4 years) |

| Automaker FCEV production commitments beyond 2025 | +5.4% | Global, led by Japan, South Korea, Germany | Medium term (2-4 years) |

| Second-life automotive PEM modules repurposed for containerized gensets | +2.1% | North America & EU, early adoption in APAC | Long term (≥ 4 years) |

| PFAS-free membrane breakthroughs enabling new suppliers | +1.6% | Global, regulatory push in EU & North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Government Zero-Emission Mandates & Subsidies

Mandates now oblige fleet owners to phase out diesel across ports, logistics corridors, and municipal fleets. California’s rule, effective 2024, compels all new drayage trucks to be zero-emission, while the EU’s revised heavy-duty CO₂ standards target a 90% cut by 2040, spurring fuel cell or battery adoption for long-haul.[1]California Air Resources Board, “Advanced Clean Fleets Regulation,” arb.ca.gov China extended its New Energy Vehicle subsidy through 2025, earmarking CNY 3.7 billion for commercial FCEVs and matching support at provincial levels. South Korea’s roadmap funds 850,000 FCEVs and 1,200 hydrogen stations by 2030. These synchronized policies underpin offtake security that justifies private investment in large-scale stack production and dispensing networks.[2]European Union, “Fit for 55: Heavy-Duty CO₂ Standards,” ec.europa.eu

Rapid Decline in PEM Stack Cost Due to Gigafactory Scale

Rochester’s 1 GW gigafactory, commissioned by Plug Power in late 2025, demonstrated a 35% cost drop by unifying MEA coating, plate stamping, and end-of-line testing under one roof. Hyundai’s Guangzhou plant already targets USD 50 per kW stacks by 2027 through automated cell placement, while Bosch leverages automotive tolerances to drive scrap below 2%. U.S. DOE roadmaps confirm traction, reporting 2024 stack costs at USD 60 per kW, one year ahead of plan. Such economies open price-sensitive niches like material handling and telecom backup that previously favored diesel engines.

Expansion of Hydrogen Refueling Infrastructure

Global station counts rose to 428 in China, 254 across Europe, and 59 in the United States by the end of 2025. China’s build-out clusters along the Beijing–Tianjin–Hebei and Yangtze corridors; Japan allotted JPY 37 billion in 2025 to co-fund 80 additional stations toward a 1,000-station goal. Europe concentrates on TEN-T routes, while U.S. federal hydrogen hubs will triple current sites by 2028. Capacity is intentionally running ahead of vehicle deployment, giving fleets confidence that full operational cycles can be supported.

Automaker FCEV Production Commitments Beyond 2025

Hyundai plans 30,000 Xcient fuel cell trucks yearly by 2028, targeting North America and Europe, where early fleet pilots logged 400,000 km per vehicle. Toyota is scaling module capacity tenfold to 200,000 units by 2027 and branching into marine and stationary sectors. Daimler–Volvo’s cellcentric venture began series output of 150 kW systems in 2025, while GM–Honda stacks underpin Navistar’s eMV truck with 1,200 km range. Aggregated announcements exceed 100,000 vehicles for 2026–2028 deliveries, creating the volume surge required for supply-chain learning curves.[3]Hyundai Motor Company, “Fuel Cell Business Update,” hyundai.com

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High platinum-group metal cost exposure | -4.2% | Global, acute in regions without recycling infrastructure | Short term (≤ 2 years) |

| Limited hydrogen distribution outside early-adopter regions | -3.8% | North America (ex-California), South America, MEA, rural APAC | Medium term (2-4 years) |

| Looming iridium & platinum supply bottlenecks | -2.6% | Global, supply concentrated in South Africa & Russia | Medium term (2-4 years) |

| SOFC competition for ≥100 kW stationary projects | -1.9% | North America & EU utility-scale projects | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Platinum-Group Metal Cost Exposure

Platinum averaged USD 1,050 per troy oz in 2025, inflating catalyst bills to roughly USD 1,000 for an 80 kW automotive stack. Recycling helps: Toyota’s closed-loop program recovers 95% of platinum from retired modules, trimming virgin demand by 12,000 oz annually. Yet Ballard reports every 10% uptick in platinum price erodes gross margin by 2.5 points unless passed to customers. Research into iron–nitrogen–carbon catalysts hits 60% of platinum activity but falls short of durable service life, meaning exposure persists at least through mid-forecast.[4]London Metal Exchange, “Platinum Pricing Dashboard 2025,” lme.com

Looming Iridium & Platinum Supply Bottlenecks

Iridium output was only 7.2 t in 2025, with 85% a by-product of platinum mining, capping electrolyzer build-out potential. Prices spiked to USD 5,200 per oz, and platinum remained in its fourth consecutive deficit year. Electrolyzer suppliers such as ITM Power sliced iridium loading from 2 g kW⁻¹ to 0.5 g kW⁻¹ via nanostructured coatings, while Plug Power targets 0.1 mg cm⁻² platinum in stacks by 2027. Until such thrifting reaches full commercial roll-out, material supply remains a hard ceiling on expansion.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: High-Temperature Variants Pick Up Industrial Heat Integration

High-temperature stacks will grow at 35.8% through 2031, even though low-temperature units owned 73.5% of 2025 sales. Industrial operators value 120 °C–180 °C operation because the waste heat can be recuperated for process loads, cutting balance-of-plant spending by 25%. Serenergy’s 5 kW installs in Danish apartment blocks in 2025 delivered 90% combined efficiency by channeling exhaust heat into radiators. Low-temperature designs remain standard for vehicles owing to quick cold starts and 4 kW L⁻¹ power density. However, phosphoric-acid-doped polybenzimidazole membranes now show 10,000-hour durability, shrinking the density gap and suggesting high-temperature adoption may broaden where refined hydrogen is scarce.

By Cooling Method: Liquid Systems Retain the High-Power Edge

Liquid-cooled stacks covered 70.1% of 2025 volume and will expand at a 32.5% CAGR, essential once outputs exceed 30 kW. Deionized water or glycol circuits keep cells within the 65 °C–75 °C sweet spot, allowing 4 kW L⁻¹ density even if radiators add 15% weight. Horizon’s hybrid cooling launched in 2025 toggles between air and liquid, trimming parasitic draw by 8%. Maritime uses underline liquid’s relevance: Wärtsilä’s 1.2 MW ship module dissipates 600 kW of heat to seawater, an impossible feat with air-only cooling. Air-cooled units stay relevant for telecom and forklifts where simplicity overrides peak power.

By Power Output: Heavy-Duty and Utility Systems Race Ahead

The segment above 100 kW will post the fastest 37.2% CAGR because it underpins Class 8 freight and multi-megawatt backup. Nikola’s Tre truck proves a 1,000 km reach on 80 kg of hydrogen, refueled in 15 minutes, neutralizing battery-electric downtime. Microsoft replaced diesel standby with 3 MW of PEM fuel cells in Dublin, a template telecoms now assess. The long-tail 10 kW–100 kW band still held 50.9% slice of 2025 demand by serving delivery vans and forklifts that run >6 hours daily. Below 1 kW remains niche, constrained by lithium-ion’s convenience.

By Component: Catalyst Revenues Accelerate on Loading Reduction

Membrane electrode assemblies controlled 58.3% of the value in 2025, yet catalyst sales will climb faster at 36.4% CAGR. Johnson Matthey’s Pt-Co alloy boosts mass activity 20%, letting producers shave loading to 0.25 mg cm⁻². Umicore’s carbon nanotube supports reached 0.18 mg cm⁻² while keeping 8,000-hour life. Gore commercialized a PFAS-free reinforced membrane in 2025 to meet EU and California directives, enabling suppliers without legacy licensing to enter. Bipolar plates trend toward stamped stainless at volume, trimming graphite share and lowering per-stack cost by 15%.

By Application: Stationary Power Shifts Into High Gear

Transportation accounted for 61.8% of 2025 uptake, but stationary power will deliver a 38.9% CAGR to 2031, propelled by data-center and utility resilience needs. Amazon Web Services is committed to 50 MW of fuel cell backup by 2027, while Japan’s Ene-Farm has surpassed 450,000 cumulative home systems. Grid unrest drives Southern California Edison’s 2.8 MW array, providing spinning reserve. The pivot depends on hydrogen prices sliding below USD 4 kg⁻¹, a level that multiple renewable corridors project by 2028. Portable and telecom backup stay secondary until distribution widens.

By End-User Industry: Utilities Pace Future Demand

Utilities are primed for a 39.3% CAGR, chasing dispatchable zero-carbon capacity that complements solar and wind. Southern California Edison and Tokyo Electric Power already pilot multi-MW arrays for black-start and frequency regulation duties. Logistics fleets retain 61.8% presence owing to hydrogen’s parity with diesel beyond 300 km daily routes. Material-handling surpassed 60,000 fuel-cell forklifts in North America. Defense adoption inches forward via submarine auxiliary power and mobile generators in NATO exercises, but remains minor volume.

Geography Analysis

Asia–Pacific commanded 47.6% of the polymer electrolyte membrane fuel cell (PEMFC) market share in 2025 and should grow at 33.1% through 2031. China deployed 428 hydrogen stations, with Guangdong, Shandong, and Hebei subsidizing 40% of truck purchase costs. Japan extended its Ene-Farm rebate to 2027 and targets 5.3 million home installs by 2030. South Korea funds 850,000 FCEVs and 1,200 stations, while India’s National Hydrogen Mission mandates 10% refinery hydrogen be green by 2027. Australia concentrates on export ammonia, with limited domestic uptake outside mining equipment.

Europe’s hydrogen backbone will repurpose 28,000 km of pipelines by 2027, lowering delivered hydrogen 30% below trucking costs. Germany assigned EUR 9 billion to electrolyzers and heavy-duty truck incentives, France targets 6.5 GW electrolysis by 2030, and the U.K. clusters on HyNet. Nordic hydropower underwrites low-carbon hydrogen export deals. Policy alignment under RED III mandates 42% renewable hydrogen in industry by 2030, anchoring future demand.

North America benefits from the USD 8 billion federal hub program. The Gulf Coast hub aims at 1.2 GW of blue hydrogen for refineries, whereas California drayage rules push trucking demand. Canada’s Bécancour plant will export 88,000 t of green hydrogen to Europe. Mexico, South America, and the Middle East remain nascent, skewing current deployments toward export ammonia rather than domestic fuel cells.

Competitive Landscape

The polymer electrolyte membrane fuel cell market remains moderately fragmented; the top five suppliers control roughly 40% combined share, leaving room for >50 niche players. Ballard partners with Weichai and Solaris to dominate heavy-duty buses, while Plug Power’s integrated hydrogen supply model secures Amazon and Walmart fleets but demands high capital. Cummins leverages its 600-shop service footprint to cross-sell range extenders, and Toyota plus Hyundai vertically integrate stacks to shield margins.

Weichai’s 200 MW capacity ramp in Shandong undercuts Western pricing by 30%, challenging incumbents in cost-sensitive sectors. Technology focus has shifted toward catalyst loading cuts and PFAS-free membranes; Gore’s 10,000-hour PFAS-free sheet opened the field to newcomers lacking legacy licensing. Marine and aviation ground support are emerging whitespaces, evidenced by Wärtsilä’s 1.2 MW ship module and airport baggage tractor pilots. Standards such as SAE J2601 increasingly dictate refueling and influence stack thermal design.

Polymer Electrolyte Membrane Fuel Cells (PEMFC) Industry Leaders

Ballard Power Systems

Plug Power Inc.

Toyota Motor Corporation (FCEV stacks)

Hyundai Motor Company

Cummins Inc. (Hydrogenics)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Plug Power announced that the 30 MW Barrow Green Hydrogen Project in the UK had reached its Final Investment Decision (FID). The project will utilize six 5 MW GenEco PEM electrolyzers to facilitate industrial hydrogen production and support decarbonization efforts.

- May 2026: Ballard Power Systems and Wrightbus revealed that Wrightbus' upcoming StreetDeck Hydroliner Gen 3.0 hydrogen buses will be powered by Ballard's FCmove®-SC PEM fuel cell engine, with an eye on production in 2027.

- March 2026: Ballard Power Systems entered into a commercial agreement with New Flyer for the supply of 500 FCmove®-HD+ PEM fuel cell bus engines, totaling 50 MW. Deliveries are expected to commence in 2026 for hydrogen fuel-cell transit buses across North America.

- January 2026: Plug Power announced the completion of the installation of 100 MW GenEco™ PEM electrolyzer units at Galp’s Sines Refinery in Portugal. The project is projected to produce up to 15,000 tons of renewable hydrogen annually, significantly reducing CO₂ emissions from the refinery.

Global Polymer Electrolyte Membrane Fuel Cells (PEMFC) Market Report Scope

Polymer electrolyte membrane fuel cells (PEMFC) are developed for portable, stationary, and transportation applications. These fuel cells generate electricity and operate on the opposite principle of polymer electrolyte membrane electrolysis, which consumes electricity. Furthermore, PEM fuel cells are expected to replace the aging alkaline fuel cell technology in the space shuttle.

The Polymer electrolyte membrane fuel cell (PEMFC) market is segmented by type, cooling method, power output, component, application, end-user, and geography. By type, the market is segmented into low-temperature PEMFC and high-temperature PEMFC. By cooling method, the market is segmented into air-cooled and liquid-cooled. By power output, the market is segmented into below 1 kW, 1-10 kW, 10-100 kW, and above 100 kW. By component, the market is segmented into stack, MEA, bipolar plates, GDL, catalysts, and BoP. By application, the market is segmented into transportation, stationary, and portable. By end-user industry, the market is segmented into transport, utilities, commercial, and others. The report offers the market size and forecasts in terms of revenue in USD billion for all the above segments.

| Low-Temperature PEMFC |

| High-Temperature PEMFC |

| Air-Cooled |

| Liquid-Cooled |

| Below 1 kW |

| 1 to 10 kW |

| 10 to 100 kW |

| Above 100 kW |

| Fuel Cell Stack |

| Membrane Electrode Assembly |

| Bipolar Plates |

| Gas Diffusion Layers |

| Catalysts |

| Balance-of-Plant Components |

| Transportation |

| Stationary Power |

| Portable/Backup Power |

| Transportation |

| Utilities |

| Commercial and Industrial |

| Others (Defense, Residential) |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Nordic Countries | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Malaysia | |

| Thailand | |

| Indonesia | |

| Vietnam | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Rest of Middle East and Africa |

| By Type | Low-Temperature PEMFC | |

| High-Temperature PEMFC | ||

| By Cooling Method | Air-Cooled | |

| Liquid-Cooled | ||

| By Power Output | Below 1 kW | |

| 1 to 10 kW | ||

| 10 to 100 kW | ||

| Above 100 kW | ||

| By Component | Fuel Cell Stack | |

| Membrane Electrode Assembly | ||

| Bipolar Plates | ||

| Gas Diffusion Layers | ||

| Catalysts | ||

| Balance-of-Plant Components | ||

| By Application | Transportation | |

| Stationary Power | ||

| Portable/Backup Power | ||

| By End-User Industry | Transportation | |

| Utilities | ||

| Commercial and Industrial | ||

| Others (Defense, Residential) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Nordic Countries | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Malaysia | ||

| Thailand | ||

| Indonesia | ||

| Vietnam | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the polymer electrolyte membrane fuel cell market?

The polymer electrolyte membrane fuel cell (PEMFC) market size stood at USD 6.67 billion in 2026 and is forecast to rise sharply through 2031, reaching USD 25.99 billion.

How fast is the polymer electrolyte membrane fuel cell market expected to grow?

The market is projected to post a 31.26% CAGR from 2026 to 2031, riding supportive regulations and falling stack costs.

Which region leads fuel cell adoption today?

Asia-Pacific held 47.6% of global share in 2025 thanks to aggressive infrastructure build-outs and vehicle subsidies in China, Japan, and South Korea.

Why are high-temperature PEM fuel cells attracting interest?

They tolerate lower-purity hydrogen and deliver usable waste heat for industrial integration, driving a 35.8% forecast CAGR.

What is the biggest barrier to widespread PEM fuel cell deployment?

Exposure to platinum-group metal pricing and constrained iridium supply remain the chief headwinds until loading-reduction technologies fully mature.

Page last updated on: