Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 73.11 Billion |

| Market Size (2031) | USD 104.69 Billion |

| Growth Rate (2026 - 2031) | 7.47% CAGR |

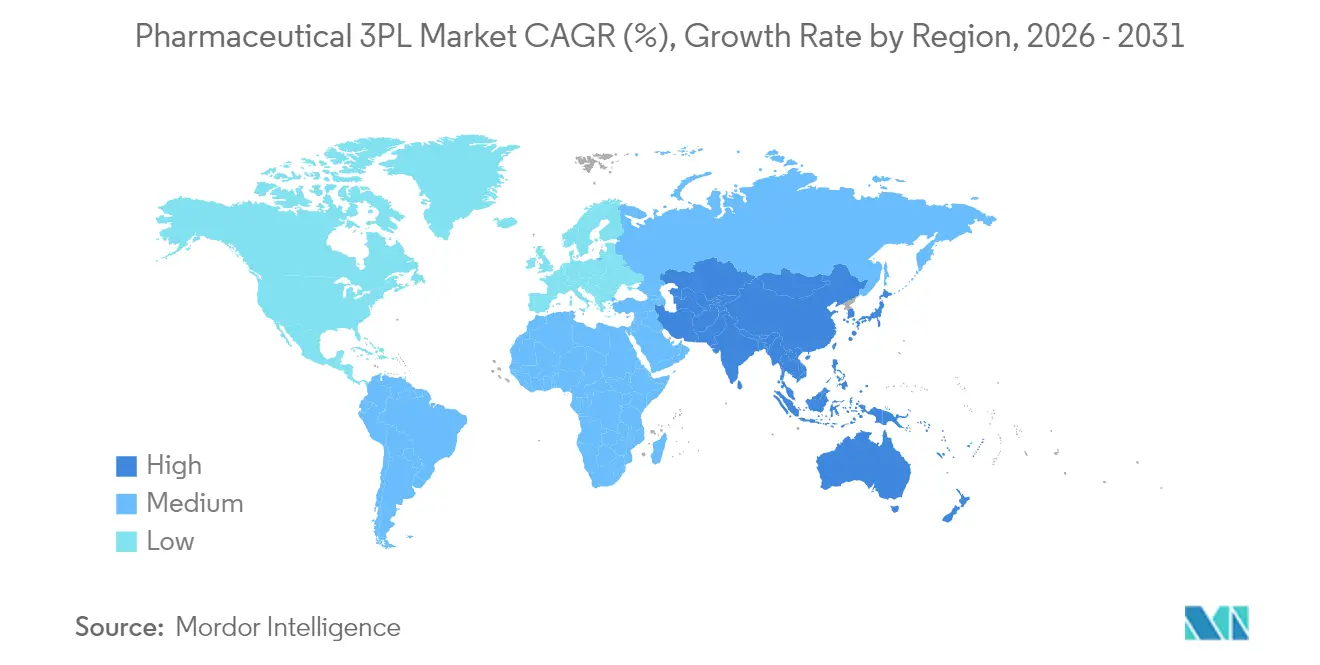

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

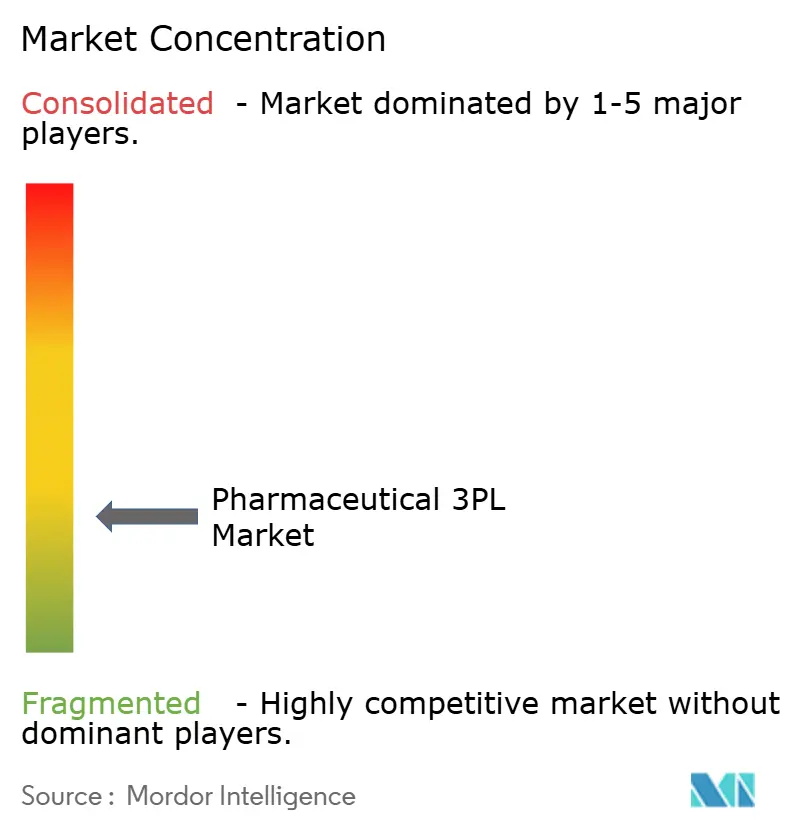

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Pharmaceutical 3PL Market Analysis by Mordor Intelligence

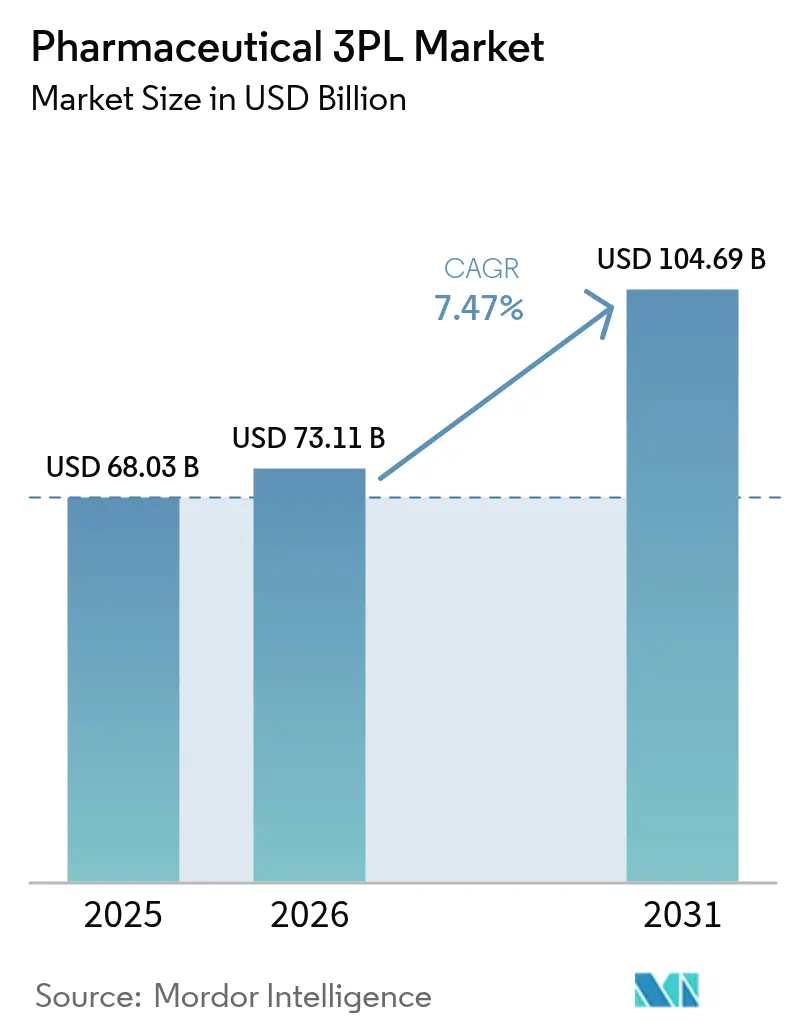

The Pharmaceutical 3PL Market size was valued at USD 68.03 billion in 2025 and estimated to grow from USD 73.11 billion in 2026 to reach USD 104.69 billion by 2031, at a CAGR of 7.47% during the forecast period (2026-2031). The growth reflects the widening range of temperature-sensitive products, tougher distribution regulations, and heightened outsourcing by small and mid-sized drug makers. Competitive intensity is rising as integrators expand dedicated healthcare networks, and investments in digital monitoring technologies deliver end-to-end shipment visibility. Demand for ultra-cold capabilities, driven by cell and gene therapies, is pulling 3PL capital toward cryogenic freezers, liquid-nitrogen shippers, and real-time IoT tracking. In parallel, the surge in e-pharmacies is parceling supply chains and pushing last-mile operators to guarantee product integrity down to the patient's doorstep. Asia-Pacific’s manufacturing build-out and government healthcare spending amplify these trends, making the region the fastest-growing arena for specialized logistics contracts.

Key Report Takeaways

- By service type, Domestic Transportation Management held 45.65% of the Pharmaceutical 3PL Market share in 2025. The Pharmaceutical 3PL Market for Value-Added Warehousing & Distribution is forecast to grow at an 8.31% CAGR between 2026-2031.

- By temperature type, non-cold chain services accounted for 63.25% of the Pharmaceutical 3PL market size in 2025. The Pharmaceutical 3PL Market for cold-chain offerings is expanding at a 10.14% CAGR between 2026-2031.

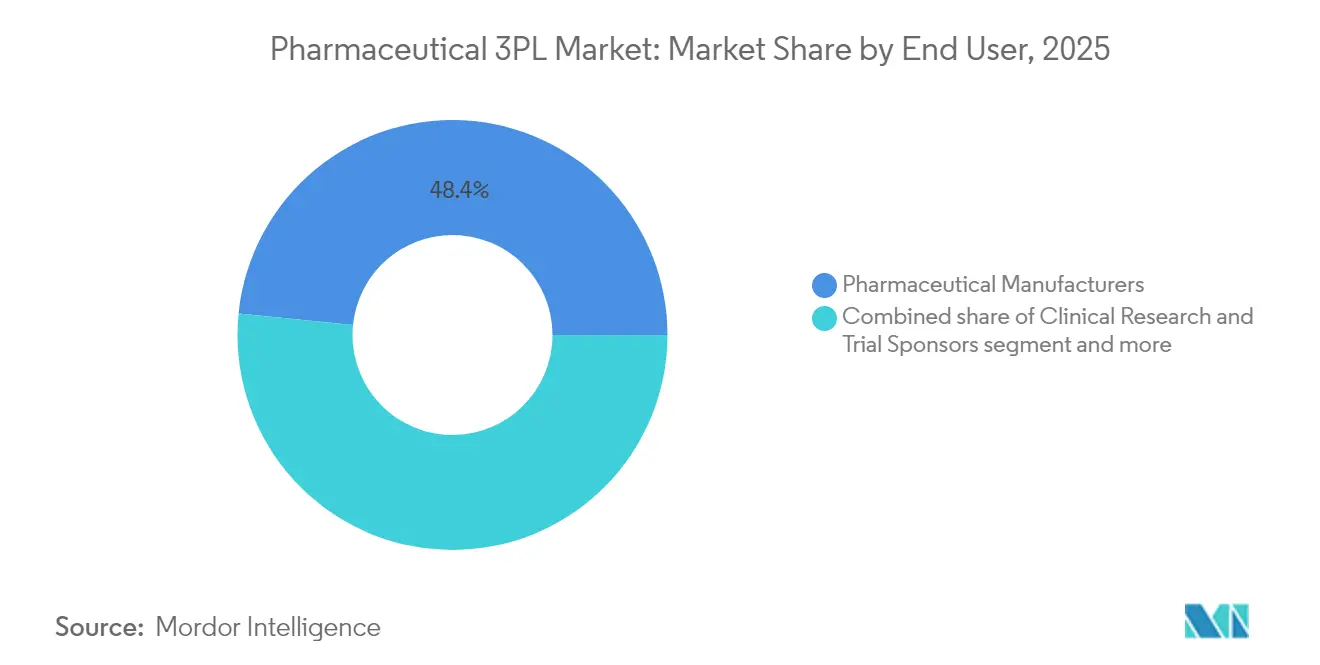

- By end user, pharmaceutical manufacturers commanded 48.40% of the Pharmaceutical 3PL market size in 2025. The Pharmaceutical 3PL Market for the e-pharmacy channel is advancing at an 11.22% CAGR between 2026-2031.

- Prescription drugs accounted for 54.20% of the pharmaceutical 3PL market in 2025, while cell and gene therapies are projected to grow at a 12.32% CAGR from 2026 to 2031.

- By region, North America led with 33.40% of the Pharmaceutical 3PL market revenue share in 2025. The Pharmaceutical 3PL Market for Asia-Pacific is projected to post the fastest 10.65% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Pharmaceutical 3PL Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Specialty biologics need cold-chain rigor | +2.1% | North America, Europe, global deployments | Medium term (2-4 years) |

| SME pharma outsourcing in emerging regions | +1.3% | Asia-Pacific, South America, Middle East | Medium term (2-4 years) |

| GDP-driven real-time monitoring | +1.0% | Europe, North America, global | Short term (≤ 2 years) |

| E-pharmacy parcelization | +1.8% | North America, Europe, developed Asia-Pacific | Short term (≤ 2 years) |

| Post-COVID vaccine pipeline | +0.9% | Global | Medium term (2-4 years) |

| IoT & blockchain visibility | +1.2% | North America, Europe, global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rise of Specialty Biologics Requiring Strict Cold-Chain Compliance

Half of all vaccine doses are still lost each year because temperature excursions ruin potency, wasting USD 35 billion and exposing compliance gaps in many distribution networks[1]Patheon, “Cold Chain Challenges in Vaccine Distribution,” patheon.com. Biologics now span refrigerated, frozen, and cryogenic regimes, driving carriers to invest in GDP-certified hubs, active containers, and continuous-monitor data loggers. DHL, for example, is enlarging its Specialized Pharma Network and GDP-approved sites to double life-science revenue above EUR 10 billion (USD 11.43 billion) by 2030. These facilities combine redundant refrigeration, qualified packaging, and in-transit telemetry, allowing manufacturers to shorten inventory buffers and accelerate launch cycles.

SME Pharma Outsourcing to 3PLs in Emerging Countries

Mid-tier drug firms in India, Vietnam, and Brazil often lack the capital to install validated freezers, serialization scanners, or GDP-qualified staff. Outsourcing to regional specialists gives them compliant infrastructure on demand, improving release timelines and freeing working capital. In China, alliances between China Resources Pharmaceutical and more than 60 multinational suppliers signal robust demand for integrated storage and distribution services tailored to smaller product volumes. Vendors offering multi-tenant warehouses, batch-level traceability, and customs-brokerage support enjoy a clear advantage when courting these clients.

Stringent GDP Regulations Driving Real-Time Monitoring Investments

The European Medicines Agency resumed on-site GDP inspections during 2024 and now targets high-risk distributors first, pushing logistics operators to maintain validated temperature records at the lane level[2]European Medicines Agency, “GDP Inspections Resume Post-COVID,” ema.europa.eu. In the United States, FDA inspectors carried out 776 GDP audits in 2023, the highest tally since the pandemic. Providers are installing IoT sensors that feed control-tower dashboards, enabling proactive diversion when thresholds drift. Blockchain pilots further ensure immutable audit trails, satisfying both DSCSA mandates and rising customer expectations for verifiable provenance.

E-pharmacy Parcelization Boosting Last-Mile Temperature-Control Needs

Direct-to-patient platforms dispatch smaller, more frequent shipments that must stay within label-specific ranges across suburban and rural addresses. CoverMyMeds notes U.S. virtual pharmacies increasingly tap UPS and FedEx clinical solutions to meet next-day delivery targets while preserving cold-chain integrity[3]. The model pushes 3PLs to blend insulated shippers, reusable gel packs, and real-time routing algorithms to manage cost without sacrificing compliance. Hub-and-spoke micro-fulfilment centers near demand clusters reduce transit time and risk as prescription volumes migrate online.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cold-chain infrastructure deficit | –1.5% | Africa, parts of Asia-Pacific, South America | Long term (≥ 4 years) |

| Cost pressure from tendering models | –0.8% | Europe, emerging markets | Medium term (2-4 years) |

| Cross-border regulatory divergence | –1.2% | Major trade lanes | Medium term (2-4 years) |

| GDP-trained labor shortage | –0.7% | North America, Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Cold-Chain Infrastructure Deficit in Developing Regions

Limited GDP-compliant storage and inconsistent power grids constrain vaccine outreach across sub-Saharan Africa and parts of Southeast Asia. Portable solar freezers and community distribution hubs are emerging stopgaps, yet capacity lags behind the booming pipeline of temperature-sensitive medicines. Multinational 3PLs face higher set-up costs and longer payback horizons, dampening expansion pace despite compelling public-health needs.

Cross-Border Regulatory Divergence Complicating Trade Flows

Rules such as the Windsor Framework oblige distributors serving Northern Ireland to comply with both UK and EU GDP statutes, triggering duplicate audits and documentation. Similar dual standards arise in GCC states and Mercosur countries, extending transit times and raising inventory buffers. Firms with strong regulatory affairs benches and multilingual control tower staff can mitigate these bottlenecks, but smaller brokers risk fines or shipment delays.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Value-Added Warehousing & Distribution Accelerates

The service-mix within the pharmaceutical 3PL market remains skewed toward Domestic Transportation Management, which accounted for 45.65% revenue in 2025. Yet the Value-Added Warehousing & Distribution sub-category is set to expand at an 8.31% CAGR, reflecting drug makers’ appetite for single-window partners able to store, kit, relabel, and comply with stringent sampling requirements. Providers differentiate by offering modular clean-rooms, serialization lines, and GDP-audited custody processes. The pharmaceutical 3PL market size for warehousing services should therefore outpace line-haul revenues as manufacturers incorporate postponement strategies and later-stage customization closer to end markets. Advanced warehouse-management systems, vertical racking, and energy-efficient refrigeration improve both cost and carbon metrics, reinforcing customer loyalty.

Domestic Transportation Management retains the scale advantage thanks to its embedded role in the daily replenishment of hospitals and pharmacies. However, pricing remains competitive and heavily dependent on fuel surcharges. International Transportation Management grows more slowly as cross-border regulatory divergence and modal congestion lengthen cycle times. Market leaders funnel capital into freight-forwarding control towers and customs-broker platforms, but smaller operators seek niche differentiation by specializing in clinical trials or named-patient imports, cushioning margin compression within the broader pharmaceutical 3PL market.

By Temperature Type: Cold Chain Outpaces Ambient

Non-cold services dominated 63.25% of 2025 revenue but are projected to lose mix as temperature-controlled lanes post a robust 10.14% CAGR. Ambient lanes nonetheless remain critical for over-the-counter analgesics, generics, and bulk excipients, constraining price hikes due to abundant carrier capacity. Conversely, cryogenic moves for cell & gene therapies command premium yields, often five to seven times higher than refrigerated tariffs. Such disparities compel operators to segment fleets and warehouses by lane-specific margin profiles, sharpening the strategic focus across the pharmaceutical 3PL market.

Infrastructural investment concentrates on hybrid cold rooms that flex between 2 °C and –20 °C, backed by dual-redundant compressors and real-time validation. Where the pharmaceutical 3PL market share for frozen lanes approaches regulatory thresholds, carriers trial passive containers with phase-change materials to shrink dry-ice carbon footprints. Digital twin simulations flag potential bottlenecks, helping planners reroute around weather disruptions while maintaining validated temperature brackets.

By End User: E-Pharmacies Transform Fulfilment

Manufacturers still supplied 48.40% of the 2025 revenue pool, leveraging the pharmaceutical 3PL market for compliant storage and bulk distribution to wholesalers and hospital networks. Yet the direct-to-consumer subsector of e-pharmacies will climb at an 11.22% CAGR, fueled by prescription digitization and insurer incentives for home delivery. This shift multiplies stock-keeping units and accelerates pick-cycles, prompting 3PLs to retrofit facilities with automated dispensers, vision-based QA checks, and secure locker loading bays.

Traceability legislation obliges serial-level scanning for each outbound parcel, raising the data burden. Providers that pair IoT beacons with AI route optimization can curtail spoilage risk and improve on-time performance, winning repeat business from tele-health platforms. The pharmaceutical 3PL industry, therefore, pivots from pallet-centric operations to parcelled networks, increasing demand for small-format insulated shippers and reusable packaging pools that trim waste and align with ESG goals.

By Product Type: Cell & Gene Therapies Stretch Logistics

Prescription medicines delivered 54.20% of 2025 revenue, underpinned by long-established supply chains and predictable order patterns. The cold-chain subset within this segment nevertheless expands as biologics gain label share. Meanwhile, cell and gene therapies post a 12.32% CAGR and trigger unprecedented handling complexity across the pharmaceutical 3PL market size. Each personalized batch travels under chain-of-identity controls at cryogenic temperatures below –150 °C, leaving no room for replacement in case of excursion.

3PLs invest in vapour-phase LN2 shippers, redundant temperature probes, and 24/7 command centers staffed by life-science engineers. World Courier reports that nearly 60% of CGT developers expect cryogenic-transport demand to surge, validating this CapEx trajectory. The pharmaceutical 3PL market share for CGT lanes thus rises disproportionately to shipment volume, contributing outsized profitability but requiring rigorous SOP governance to pass sponsor audits and regulatory inspections.

Geography Analysis

North America accounted for 33.40% of global revenue in 2025, buoyed by robust biologics pipelines, advanced cold-chain capacity, and integrated regulatory frameworks. UPS alone targets USD 20 billion in healthcare logistics turnover by 2026, a goal underwritten by acquisitions such as Frigo-Trans, which bolsters multi-temperature offerings across continental corridors. The United States’ DSCSA rollout and Canada’s tightened Health Canada guidelines sustain demand for serialization, track-and-trace, and GDP-qualified personnel. As a result, the region’s pharmaceutical 3PL market cultivates premium-priced lanes and remains a bellwether for service innovation.

Asia-Pacific will post the strongest 10.65% CAGR through 2031, propelled by manufacturing scale-ups in China and India and widened insurance coverage in Indonesia, Thailand, and Vietnam. China Resources Pharmaceutical’s partnerships with Pfizer and AstraZeneca illustrate the shift toward integrated warehousing and distribution platforms that span B2B and direct-to-patient channels. Japanese incumbents such as ALPS LOGISTICS and MITSUI-SOKO broaden cryogenic networks, while Singapore’s GDP-certified free-trade zone warehousing reinforces the city-state’s hub status. Infrastructure gaps persist in secondary cities, but national logistics corridors, highway upgrades, and customs digitalization narrow the service-level divide.

Europe maintains a sizeable share underpinned by strict GDP oversight and resilient life-science clusters in Germany, Switzerland, and Ireland. The European Medicines Agency’s resumed inspections stress continuous temperature documentation, spurring carriers to retrofit fleets with calibrated IoT sensors. Cross-border complexity after Brexit and the Windsor Framework forces distributors serving Northern Ireland to dual-qualify processes under both EU and UK statutes, elevating compliance overhead. Operational resilience remains high as trans-European rail and road corridors integrate with well-established air-cargo gateways at Frankfurt, Amsterdam-Schiphol, and Liege.

Competitive Landscape

Competition in the pharmaceutical 3PL market balances scale economics against niche specialization. DHL Supply Chain, UPS Healthcare, and FedEx Custom Critical anchor the top tier, leveraging multi-continent networks, GDP-compliant facilities, and aggressive acquisition pipelines. DHL’s USD 2.2 billion five-year investment plan targets network densification and doubled life-science revenue by 2030, aided by its 2025 takeover of Cryopdp, a clinical-trial courier. UPS mirrors that strategy with purchases of temperature-controlled specialists Frigo-Trans and BPL, consolidating capabilities across Europe and North America.

Mid-cap players such as World Courier, Marken, and GEODIS carve defensible niches by excelling in time-critical therapeutic areas, clinical-trial supply, and value-added analytics. Their agility and therapy-specific know-how often attract biotech sponsors seeking bespoke solutions outside global integrators’ standardized playbooks. Technology differentiators include blockchain-enabled provenance, digital twins for route simulation, and AI-assisted demand forecasting. Barriers to entry rise as certification costs, cryogenic infrastructure, and cybersecurity mandates escalate, yet regional champions still emerge by mastering local regulatory requirements and building pharmacist-level competence among frontline staff.

Long-run competitive advantage hinges on continuous innovation in packaging sustainability, carbon-neutral lane design, and integrated billing-plus-compliance dashboards. Partnerships with packaging manufacturers, sensor providers, and cloud analytics firms will dictate future winners as the pharmaceutical 3PL market shifts from transactional freight transactions to data-rich, risk-managed supply chain orchestration.

Pharmaceutical 3PL Industry Leaders

DHL Supply Chain & Global Forwarding

Kuehne + Nagel International AG

UPS Healthcare

FedEx Logistics

DB Schenker

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: DHL Group acquired Cryopdp, strengthening specialized pharma logistics for clinical trials and biopharma products.

- March 2025: DHL Group announced plans to double Life Science and Healthcare revenue to EUR 10 billion (USD 11.43 billion) by 2030 through expanded GDP-compliant facilities.

- January 2025: UPS finalized purchases of Frigo-Trans and BPL, enhancing temperature-controlled capacity in Europe.

- January 2025: DHL Supply Chain agreed to acquire Inmar Supply Chain Solutions, enlarging its pharmaceutical 3PL presence in North America.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study counts the pharmaceutical third-party logistics (3PL) market as the total annual revenue earned by independent service providers that store, handle, and move finished human medicines, prescription, over-the-counter, biologics, cell-and-gene therapies, and clinical-trial materials under Good Distribution Practice compliant conditions, across domestic and international lanes. The scope follows the three classical service buckets: domestic transportation management, international transportation management, and value-added warehousing and distribution.

Scope exclusion: bulk active-ingredient freight, primary drug packaging lines, and captive in-house logistics arms are kept outside the boundary.

Segmentation Overview

- By Service Type

- Domestic Transportation Management (DTM)

- Roadways

- Railways

- Airways

- Waterways

- International Transportation Management (ITM)

- Roadways

- Railways

- Airways

- Waterways

- Value-Added Warehousing and Distribution (VAWD)

- Domestic Transportation Management (DTM)

- By Temperature Type

- Cold Chain

- Non-cold Chain

- By End User

- Pharmaceutical Manufacturers

- Biotech and Biosimilar Manufacturers

- Clinical Research and Trial Sponsors

- Hospitals and Retail Pharmacies

- Healthcare Distributors and Wholesalers

- E-pharmacies and Direct-to-Patient Services

- By Product Type

- Prescription Drugs

- OTC and Consumer Health Products

- Biopharmaceuticals and Biosimilars (ex-CGT)

- Cell and Gene Therapies

- Vaccines and Blood-derived Products

- Veterinary Pharmaceuticals and Animal Health Products

- Medical Devices, Diagnostics and Combination Products

- Clinical-trial Materials (Investigational Medicinal Products)

- Others

- By Region

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Chile

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Spain

- Italy

- Netherlands

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Singapore

- Vietnam

- Indonesia

- Australia

- Rest of Asia-Pacific

- Middle East

- United Arab Emirates

- Saudi Arabia

- Turkey

- Israel

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Nigeria

- Kenya

- Rest of Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts held in-depth calls with logistics directors at global integrators, specialty cold-chain operators, and procurement heads of mid-sized pharma companies across North America, Europe, and Asia-Pacific. These conversations illuminated lane-level rate shifts, warehousing conversion costs, and upcoming regulatory triggers, letting us refine desk assumptions and reconcile gray areas.

Desk Research

We started with public datasets that trace drug output and trade, such as UN Comtrade HS-30 shipment values, Eurostat Prodcom pharmaceutical codes, and US Census NAICS 3254 shipment surveys. Regulations from the US FDA (DSCSA serialization progress), the European Medicines Agency GDP guidelines, and IATA Perishable Cargo Regulations helped size compliant capacity needs. Trade-body white papers from the International Federation of Pharmaceutical Wholesalers and the Healthcare Distribution Alliance clarified channel splits, while company 10-Ks and investor decks revealed outsourcing ratios. Commercial insight was supplemented, where relevant, with D&B Hoovers financial snapshots and Dow Jones Factiva news archives. This list illustrates our evidence base; many additional reputable sources were tapped during validation.

Market-Sizing and Forecasting

A top-down construct converts pharmaceutical production value into outsourceable logistics spend by applying service-specific penetration ratios, GDP-mandated cold-chain prevalence, and average freight-plus-warehousing tariffs, which are then cross-checked against sampled supplier roll-ups from key 3PL annual reports. Critical variables include biologic shipment tonnage, e-pharmacy parcel volumes, branded Rx sales growth, temperature-controlled pallet counts, average domestic line-haul rates, and warehouse GDP-certification additions. Multivariate regression, anchored on those drivers, projects demand through 2030; missing sub-segment data points are bridged using regional analogs vetted in expert interviews.

Data Validation and Update Cycle

Before sign-off, our model passes anomaly checks against independent cold-chain capacity audits and national freight price indices. Senior reviewers challenge outliers, and we re-contact experts when deviations exceed preset bands. Reports refresh annually, with mid-cycle tweaks when material events, regulatory or macroeconomic, occur.

Why Mordor's Pharmaceutical Third Party Logistics Baseline Earns Confidence

Published estimates often diverge because firms choose different service mixes, include captive transport, or freeze exchange rates at distinct points. Such choices can double count value or inflate totals.

Key gap drivers are that several publishers fold primary packaging, medical device freight, or hospital inventory services into 'logistics,' adopt aggressive blended price inflation, and project uniform cold-chain penetration across all regions; assumptions our team rejects after granular channel checks and annual refresh cadence.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 68.03 B (2025) | Mordor Intelligence | |

| USD 137.25 B (2024) | Global Consultancy A | Adds packaging and contract manufacturing flows; single global ASP uplift |

| USD 146.20 B (2024) | Data Publisher B | Bundles all healthcare logistics; static currency conversion; limited cold-chain break-out |

These comparisons show that our disciplined scope selection, variable-level transparency, and yearly recalibration give decision-makers a balanced, reproducible baseline they can trust over more expansive but less validated figures.

Key Questions Answered in the Report

What is the projected growth rate of the pharmaceutical 3PL market between 2026 and 2031?

The pharmaceutical 3PL market is forecast to expand at a 7.47% CAGR, rising from USD 73.11 billion in 2026 to USD 104.69 billion by 2031.

Which service segment is expected to grow the fastest?

Value-Added Warehousing & Distribution leads with an 8.31% CAGR, reflecting demand for integrated storage, inventory and packaging services.

Why is Asia-Pacific the fastest-growing region for pharmaceutical 3PL services?

Manufacturing scale-ups in China and India, rising healthcare spending and ongoing infrastructure upgrades lift the region toward a 10.65% CAGR.

How are e-pharmacies changing pharmaceutical logistics?

E-pharmacies increase parcel-level, temperature-controlled deliveries directly to patients, boosting last-mile complexity and driving 11.22% CAGR for this end-user segment.

What technologies are most critical for ensuring compliance in pharmaceutical logistics?

IoT sensors for real-time monitoring, blockchain for immutable traceability and digital-twin analytics for proactive lane management are now central to GDP compliance.

What makes cell & gene therapy logistics uniquely challenging for 3PLs?

These therapies require cryogenic conditions below –150 °C, strict chain-of-identity processes and rapid, individualized delivery windows, demanding specialized infrastructure and 24/7 oversight.

Page last updated on: