Personal Care Contract Manufacturing Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

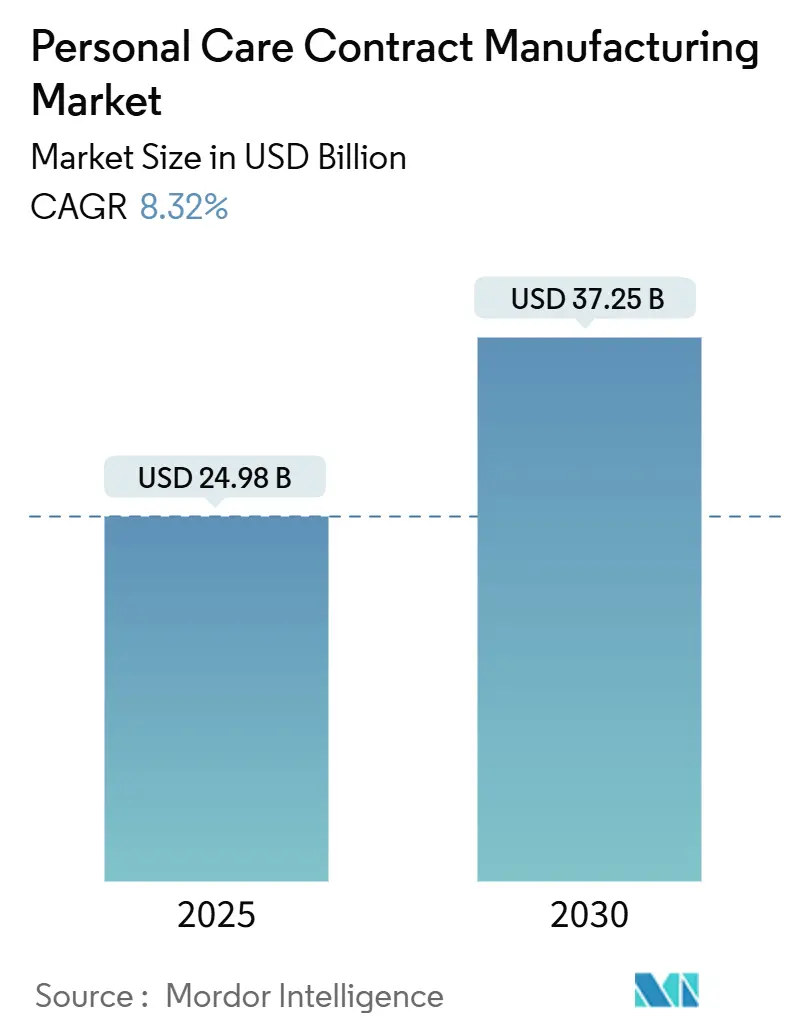

| Market Size (2025) | USD 24.98 Billion |

| Market Size (2030) | USD 37.25 Billion |

| Growth Rate (2025 - 2030) | 8.32% CAGR |

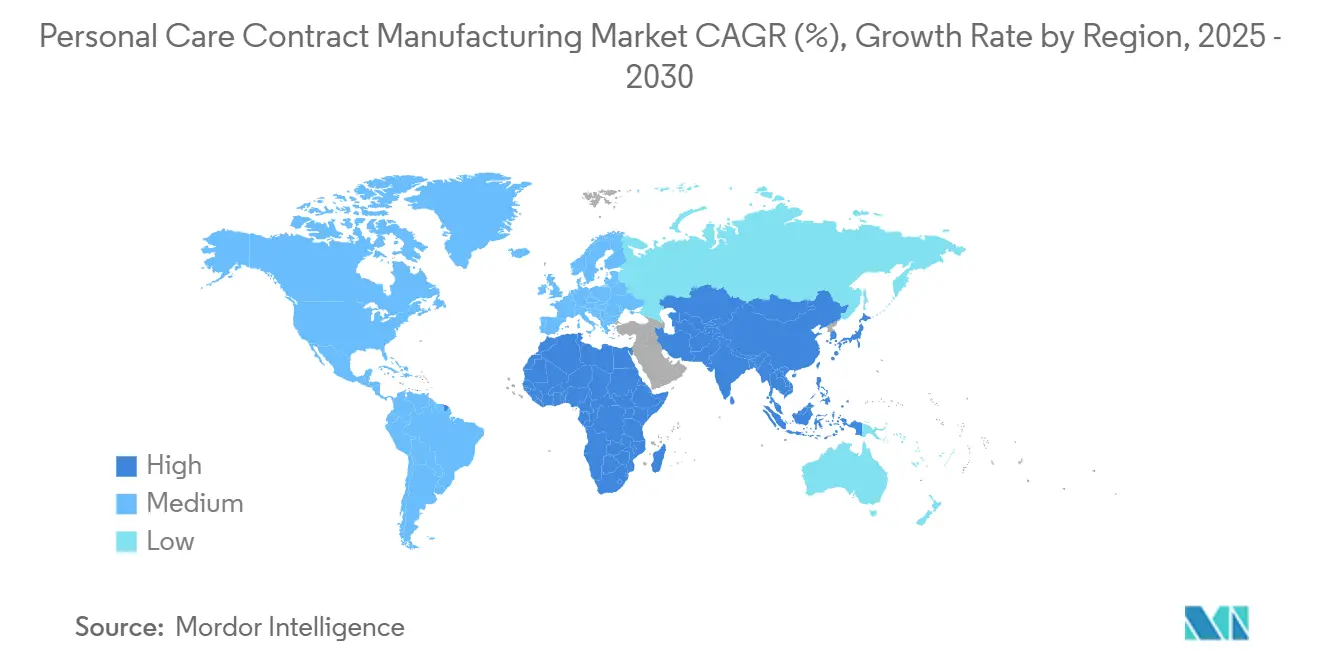

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Personal Care Contract Manufacturing Market Analysis by Mordor Intelligence

The personal care contract manufacturing market size stands at USD 24.98 billion in 2025 and is predicted to reach USD 37.25 billion by 2030, reflecting an 8.32% CAGR that signals durable momentum for outsourced production partnerships. A combination of tightening regulatory frameworks, brand-side focus on speed-to-market, and mounting sustainability pressures is steering both global majors and emerging indie labels toward external manufacturing alliances. Outsourcing also mitigates capital risk at a time when inflation and raw-material volatility have elevated the cost of plant upgrades and compliance programs. In parallel, digital formulation tools and modular production systems reduce minimum order quantities, opening the door for niche entrants and private-label retailers. Asia-Pacific’s scalable factory base gives the region a cost lead, but reshoring activity in North America and Western Europe is accelerating as brands seek greater supply resilience.

Key Report Takeaways

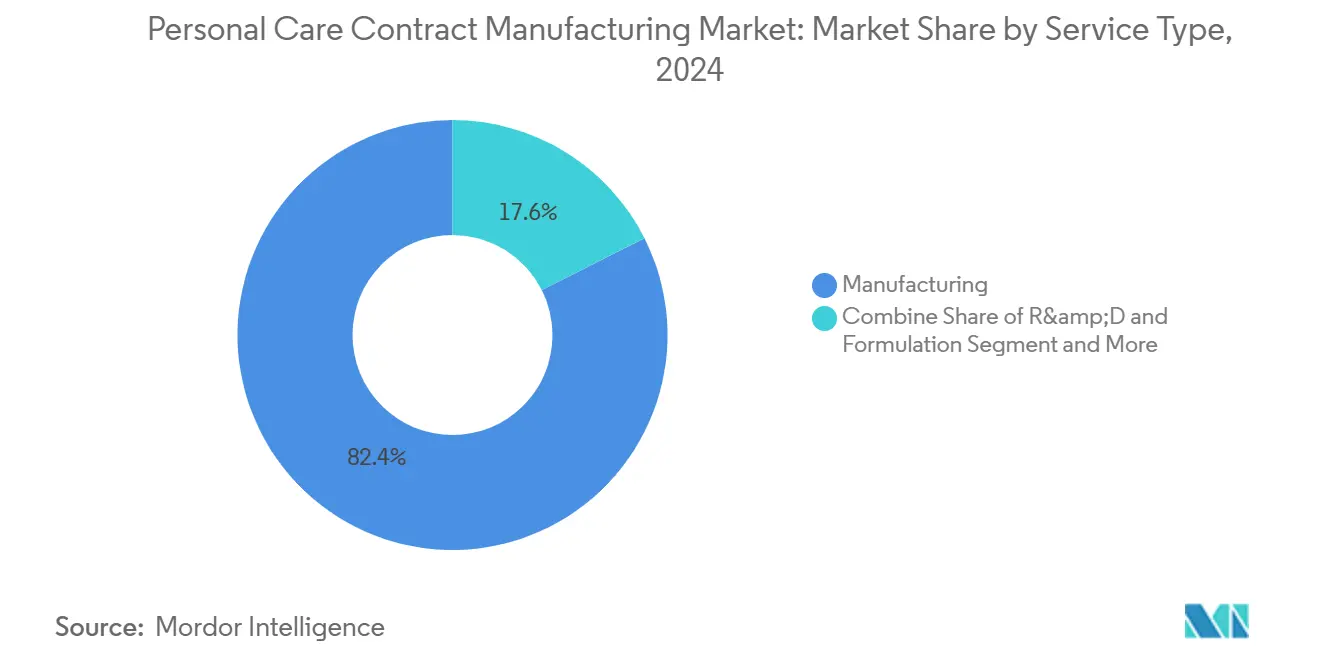

- By service type, manufacturing services held 82.42% of personal care contract manufacturing market share in 2024, while turnkey R&D and formulation posted the fastest 12.33% CAGR outlook through 2030.

- By product type, skin care captured 35.32% revenue in 2024; hair care is projected to expand at a 14.42% CAGR to 2030.

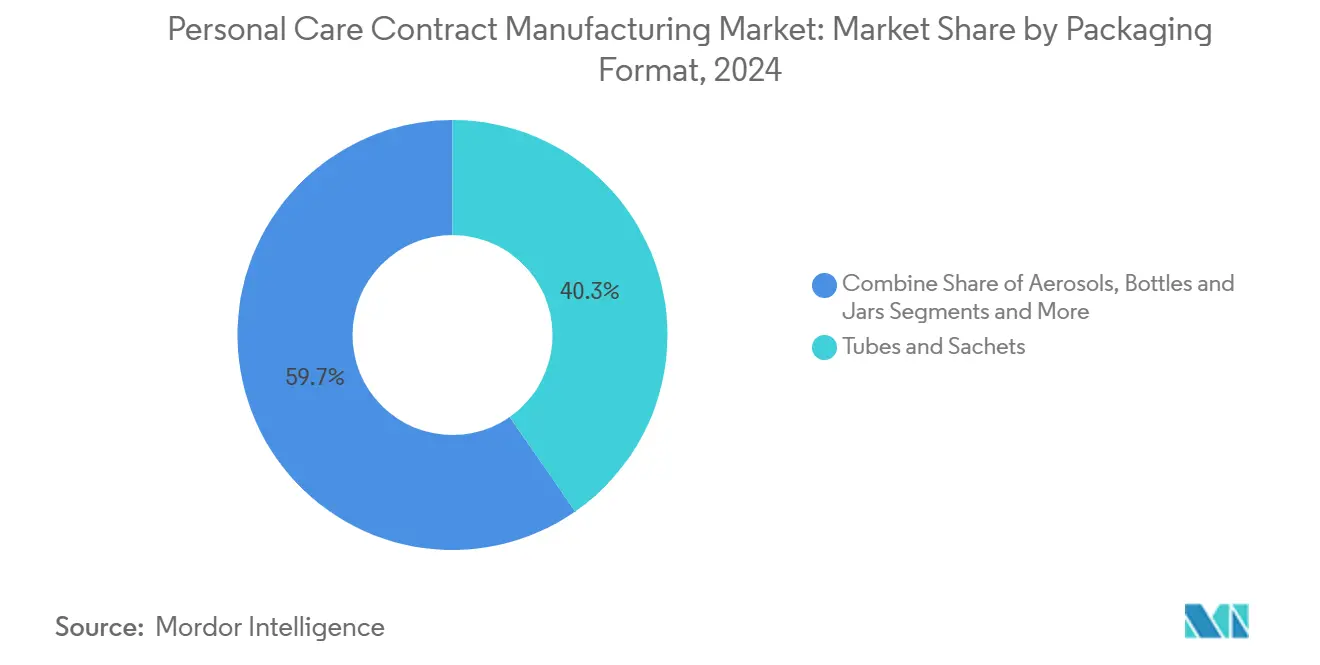

- By packaging format, tubes and sachets led with 40.32% share in 2024; aerosols record the strongest 12.97% CAGR forecast.

- By contract manufacturing model, OBM/private label accounted for 50.32% share of the personal care contract manufacturing market size in 2024, whereas ODM is set to grow 12.63% annually to 2030.

- By region, Asia-Pacific dominated with 38.23% share in 2024, and the same region is advancing at a 14.01% CAGR over the period.

Global Personal Care Contract Manufacturing Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Evolution of service offerings enables outsourcing focus | +1.8% | Global, with concentration in North America & EU | Medium term (2-4 years) |

| Localization of manufacturing for lead-time and cost advantage | +1.5% | North America & EU, spill-over to APAC | Short term (≤ 2 years) |

| Surge of indie/DTC brands outsourcing production | +2.1% | Global, early gains in North America, Europe, Asia-Pacific | Short term (≤ 2 years) |

| Demand for organic and natural formulations | +1.2% | Global, with premium markets leading adoption | Medium term (2-4 years) |

| AI-driven rapid formulation platforms | +0.9% | APAC core, spill-over to North America & EU | Long term (≥ 4 years) |

| Refillable-packaging mandates requiring specialized CM | +0.7% | EU leading, North America following | Long term (≥ 4 years) |

Source: Mordor Intelligence

Evolution of Service Offerings Enables Outsourcing Focus

Contract manufacturers are evolving into end-to-end solution partners that blend GMP production, regulatory filing, digital batch tracking, and sustainability consulting within a single contract. Enhanced capabilities create a one-stop ecosystem that allows beauty houses to concentrate resources on brand building and channel strategy. The forthcoming December 2025 GMP deadline under the U.S. MoCRA law has intensified demand for partners already operating FDA-ready lines. [1]U.S. Food and Drug Administration, “Guidance for Industry – Registration and Listing of Cosmetic Product Facilities and Products,” fda.gov Full-service providers report rising inquiries from medium-sized North American brands eager to outsource compliance paperwork, stability testing, and safety substantiation. Larger manufacturers have responded by expanding peptide, biotech, and fermentation expertise through technology licensing from ingredient innovators. The convergence of compliance depth and formulation breadth is shifting the value proposition away from unit-cost calculation toward holistic risk sharing within the personal care contract manufacturing market.

Localization of Manufacturing for Lead-Time and Cost Advantage

Geopolitical friction, container shortages, and elevated freight costs have shortened acceptable lead times, driving procurement teams to re-map supply chains toward regional hubs. New investments in the United States, Poland, and Mexico emphasize modular clean-room design, allowing quick format changeovers for color-cosmetics or peel-off masks. Brands cite inventory holding reductions of up to 25 days when production sits inside the target customs zone. Localization also circumvents divergent rules on organic certification, allergen disclosure, and extended producer responsibility for packaging. Firms that operate dual-continent footprints now capture multi-year commitments from prestige clients seeking geographic diversification inside the personal care contract manufacturing market.

Surge of Indie/DTC Brands Outsourcing Production

Lower barriers to digital retail have propelled thousands of direct-to-consumer labels that possess marketing flair yet lack manufacturing muscle. Contract manufacturers with low-minimum-order-quantity lines fill this gap, offering pilot runs below 5,000 units alongside micro-batch sampling. The indie wave produces shorter trend cycles, raising demand for agile partners capable of formula tweaks in under four weeks. Flexible outsourcing also helps founders comply with MoCRA’s facility-registration rule, as a single FDA-registered site can cover multiple SKUs. This structural dependence reinforces service pipelines for small-run emulsions, balms, and clean-beauty toners across the personal care contract manufacturing market.

Demand for Organic and Natural Formulations

The USDA’s Strengthening Organic Enforcement rule, live since March 2024, mandates certification for every handler in the organic chain and defines two formal claims: “100% organic” and “organic” at 95% minimum content. [2]U.S. Department of Agriculture, “Strengthening Organic Enforcement Frequently Asked Questions,” ams.usda.gov Contract manufacturers that operate audited supply networks and segregated storage now attract prestige skin-care launches that stress traceability back to farm level. Growth is pronounced in Europe, where eco-label awareness is high, and in Japan, where fermentation-based naturals resonate with consumers. Market players report double-digit project growth for preservative-free gels, waterless bars, and COSMOS-certified treatment oils, reinforcing the premium segment of the personal care contract manufacturing market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent regulatory and counterfeit concerns | -1.1% | Global, with varying intensity by region | Short term (≤ 2 years) |

| Raw-material price and supply-chain volatility | -1.4% | Global, with acute impact in Asia-Pacific | Short term (≤ 2 years) |

| In-house capacity expansion by mega beauty brands | -0.8% | Global, concentrated in North America & EU | Medium term (2-4 years) |

Source: Mordor Intelligence

Stringent Regulatory and Counterfeit Concerns

Full enforcement of MoCRA begins December 2025, obliging every cosmetics facility that ships into the United States to register, list products, and maintain adverse-event files. Non-compliance triggers refusal of entry, civil penalties, or product seizure.[3]Federal Register, “Registration and Listing of Cosmetic Product Facilities and Products; Guidance for Industry; Availability,” federalregister.govParallel rules in the EU boost traceability through digital product passports. Contract manufacturers shoulder significant audit, documentation, and serialization costs, especially when serving cross-border brand portfolios. Adding to the compliance load, counterfeit proliferation drives brands to demand tamper-evident seals and blockchain-based batch verification. Smaller factories lacking capital for such systems face exit risks, tightening capacity but curbing supplier diversity in the personal care contract manufacturing market.

Raw-Material Price and Supply-Chain Volatility

Feedstock swings—exemplified by Dow’s USD 0.05 per pound glycol-ether increase effective January 2025—compress margins and complicate quotation validity. Contract manufacturers must hedge solvent and surfactant exposure or accept periodic re-pricing clauses, a shift that strains downstream relationships. Port congestion and political tensions create spot shortages in fragrance oils, palm-derived fatty acids, and glass droppers. Factories without multiple approved vendors risk line stoppages, prompting a strategic pivot toward dual sourcing, buffer inventories, and vendor-managed stocking agreements across the personal care contract manufacturing market.

Segment Analysis

By Service Type: Manufacturing Dominance Drives Market Growth

Manufacturing services captured 82.42% of the personal care contract manufacturing market in 2024, reflecting brands’ core need for scalable, GMP-compliant production lines. The segment benefits from multi-shift utilization, automated filling, and economies of raw-material scale that individual labels cannot afford. Forecast expansion at 12.33% annually shows that even as digital formulating gains traction, physical output remains the capacity bottleneck. Turnkey providers bundle formulation, microbiological testing, and secondary packaging, enabling a single purchase order from ideation to warehouse gate. This integration locks in longer contracts and elevates switching costs for brand owners.

R&D and formulation services, although a smaller revenue slice, serve as a pipeline magnet. Early-stage engagements secure later manufacturing awards once pilots move to commercial scale, capturing lifetime value. Contract development arms now run solvent-less emulsification, green chemistry screening, and accelerated stability protocols, improving hit rates. Fee-for-service models convert to margin-rich unit production, reinforcing the service-led moat inside the personal care contract manufacturing market.

Note: Segment shares of all individual segments available upon report purchase

By Product Type: Skin Care Leadership Meets Hair Care Innovation

Skin care dominated with 35.32% personal care contract manufacturing market share in 2024, anchored by multi-step routines that spur cleanser, serum, and sunscreen rotations. The category’s appetite for actives such as retinoids, ceramides, and probiotics commands fermentation tanks and clean-room environments, aligning with contract manufacturers that already hold relevant certifications. Bags-on-valve and airless pumps extend shelf stability, adding engineering complexity that favors specialized fillers.

Hair care races ahead at a 14.42% CAGR, propelled by scalp-health awareness, textured-hair inclusivity, and biotech-based bond-repair claims. Brands require emulsifiers that keep viscosity stable across climates, pushing contract partners to validate rheology at multiple humidity points. Professional salon crossover SKUs add high-margin volumes, intensifying demand for precise batch reproducibility within the personal care contract manufacturing market size at segment level. Down the stack, color cosmetics, fragrance, and deodorants preserve steady demand, absorbing filler capacity during off-peak skin-care cycles.

By Packaging Format: Tubes and Sachets Lead Sustainability Transition

Tubes and sachets held 40.32% share as of 2024 because their single-dose convenience aligns with travel retail, e-commerce sampling, and hygienic dispensing. Recyclable mono-material laminate upgrades allow easy separation of barrier layers, easing EU recyclability compliance. Contract fillers adjust crimping pressure and sealing temperatures to cut wastage, thus lifting throughput yields.

Aerosols show a 12.97% CAGR outlook thanks to dry shampoos, self-tan mists, and SPF sprays. Manufacturers are converting lines to next-generation propellants with lower global-warming potential, investments that heighten technological barriers. Bottle and jar formats remain staples for prestige creams, while pumps gain ground in sanitary batch-viscous products. Flexibility across filling heads safeguards utilization rates in the personal care contract manufacturing market.

Note: Segment shares of all individual segments available upon report purchase

By Contract Manufacturing Model: Private Label Growth Accelerates

Private-label/OBM activity represents 50.32% of market revenue, reflecting retailer power and consumers’ growing trust in store brands. Scale retailers engage turnkey partners to launch clean-formula ranges priced 20% below national brands yet with near-identical performance. For contract manufacturers, OBM lines guarantee forecastable runs and lower artwork changeovers.

ODM, advancing 12.63% per year, lets brands adopt a base formula library, select scent or color variants, and enter market within 90 days. This speed appeals to social-media-driven businesses that capitalize on trending ingredients before buzz fades. OEM engagements persist for blockbuster products when originators require surge capacity, while toll manufacturing fills specialist gaps such as cold-process soap or fluoride tooth tabs, diversifying revenue inside the personal care contract manufacturing industry.

Geography Analysis

Asia-Pacific commanded 38.23% of the personal care contract manufacturing market in 2024 and is projected to grow 14.01% annually through 2030. China, South Korea, and Thailand host dense supplier ecosystems ranging from surfactant plants to pump-molder clusters. Shanghai’s new 2,500-square-meter consumer-brand R&D center enables rapid prototype-to-production handoff, strengthening local supply resilience. Regional governments grant tax credits for advanced automation and export promotion, further lowering per-unit costs. Vietnam’s domestic cosmetics turnover topping VND 45,000 billion in 2024 underscores rising intra-Asia demand that backfills any Western order softness.

North America is a mature yet strategically vital pocket for the personal care contract manufacturing market. MoCRA compliance deadlines create a compliance moat for FDA-registered factories, driving volume toward established operators. Brands appreciate domestic lead-time savings and ESG transparency when using U.S. or Canadian fillers. Incentives at state level—such as workforce grants and property-tax abatements—offset higher wage costs. New production wings in North Carolina illustrate the re-shoring play, targeting indie labels that value proximity for shorter concept reviews.

Europe balances tight regulation with premium positioning. The bloc’s recyclable-packaging mandate spurs investment in refill pod assembly and mono-material componentry. A EUR 11 million Spanish facility featuring photovoltaic power showcases how energy-positive plants can still deliver unit-cost competitiveness. German and French labs focus on blue-biotech actives and microbiome-safe preservatives, cementing the region’s technical reputation. Elsewhere, Latin America and the Middle East post mid-single-digit gains off small bases, leveraging growing middle-class demand and government import-substitution policies to attract capacity, though supply-chain maturity still lags leading regions.

Competitive Landscape

Innovation and Adaptability Drive Future Success

Success in the personal care contract manufacturing market increasingly depends on companies' ability to adapt to evolving consumer preferences and regulatory requirements while maintaining operational efficiency. Incumbent players must focus on developing sustainable manufacturing practices, investing in advanced technologies, and expanding their service offerings to maintain their market position. Companies need to strengthen their research and development capabilities to address the growing demand for natural and organic products while ensuring compliance with increasingly stringent regulatory requirements. Building strong relationships with both established brands and emerging players remains crucial for long-term success.

For contenders seeking to gain market share, specialization in niche segments and a focus on innovative formulations present significant opportunities. Companies must develop robust quality management systems and maintain flexibility in production capabilities to address varying customer demands. The ability to offer comprehensive solutions, from product development to packaging and distribution, will become increasingly important for market success. Regulatory compliance, particularly regarding sustainable practices and ingredient transparency, will continue to shape competitive dynamics. Companies must also invest in digital capabilities to enhance operational efficiency and improve customer service while maintaining strong supply chain relationships to ensure reliable product delivery. The role of cosmetic contract manufacturers and personal care manufacturers in this evolving landscape cannot be overstated, as they are pivotal in driving innovation and meeting consumer demands.

Personal Care Contract Manufacturing Industry Leaders

-

McBride PLC

-

Colep Consumer Products

-

PLZ Corp

-

Voyant Beauty

-

Albea Services S.A.S.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Fagron acquired CareFirst Specialty Pharmacy (USA) and Injeplast (Brazil) for €30 million to expand wellness offerings and Latin American reach.

- January 2025: Kolmar Korea announced a second U.S. plant aimed at USD 100 million sales in five years and wider Americas distribution.

- November 2024: Cosmewax opened a EURO 11 million Spanish skin-care factory equipped with photovoltaic energy systems, boosting capacity 50%.

- August 2024: Cosmetics & Cleaners International invested USD 8.4 million in a 108,000-square-foot North Carolina plant for manufacturing and distribution.

Global Personal Care Contract Manufacturing Market Report Scope

Contract manufacturing in the personal care industry involves companies outsourcing design, formulation, manufacturing, packaging, and related services. This approach allows small business owners to market their personal care products without the hefty investment of building and operating a manufacturing plant. The report tracks and analyzes the demand for outsourced services ranging from manufacturing and formulation to research and packaging within the personal care industry, all while considering current market trends and dynamics. Additionally, the study assesses the impact of geopolitical factors on the market, considering prevailing scenarios, key themes, and demand cycles tied to specific product types.

The personal care contract manufacturing market is segmented by service type (R&D and formulation, manufacturing, and packaging and allied services), product type (skincare, haircare, make-up and cosmetics, and other product types), and geography (North America [United States, Canada], Europe [United Kingdom, France, Italy, and Rest of Europe], Asia-Pacific [China, Japan, India, South Korea, and Rest of Asia-Pacific], and Rest of the World). The report offers market sizes and forecasts in value (USD) for all the above segments.

| By Service Type | R&D and Formulation | |||

| Manufacturing | ||||

| Packaging and Allied Services | ||||

| Turnkey / Full-Service Manufacturing | ||||

| By Product Type | Skin Care | |||

| Hair Care | ||||

| Color Cosmetics | ||||

| Fragrance and Deodorants | ||||

| Oral Care | ||||

| Other Product Type | ||||

| By Packaging Format | Aerosols | |||

| Bottles and Jars | ||||

| Tubes and Sachets | ||||

| Pumps and Dispensers | ||||

| Sticks and Roll-ons | ||||

| Other Packaging Format | ||||

| By Contract Manufacturing Model | OEM | |||

| ODM | ||||

| OBM / Private Label | ||||

| Toll Manufacturing | ||||

| By Geography | North America | United States | ||

| Canada | ||||

| Mexico | ||||

| Europe | Germany | |||

| United Kingdom | ||||

| France | ||||

| Italy | ||||

| Spain | ||||

| Russia | ||||

| Rest of Europe | ||||

| Asia-Pacific | China | |||

| India | ||||

| Japan | ||||

| South Korea | ||||

| Australia and New Zealand | ||||

| Rest of Asia-Pacific | ||||

| Middle East and Africa | Middle East | United Arab Emirates | ||

| Saudi Arabia | ||||

| Turkey | ||||

| Rest of Middle East | ||||

| Africa | South Africa | |||

| Nigeria | ||||

| Egypt | ||||

| Rest of Africa | ||||

| South America | Brazil | |||

| Argentina | ||||

| Rest of South America | ||||

| R&D and Formulation |

| Manufacturing |

| Packaging and Allied Services |

| Turnkey / Full-Service Manufacturing |

| Skin Care |

| Hair Care |

| Color Cosmetics |

| Fragrance and Deodorants |

| Oral Care |

| Other Product Type |

| Aerosols |

| Bottles and Jars |

| Tubes and Sachets |

| Pumps and Dispensers |

| Sticks and Roll-ons |

| Other Packaging Format |

| OEM |

| ODM |

| OBM / Private Label |

| Toll Manufacturing |

| North America | United States | ||

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia and New Zealand | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

What is the current size of the personal care contract manufacturing market?

The personal care contract manufacturing market size is USD 24.98 billion in 2025 and is forecast to reach USD 37.25 billion by 2030 at an 8.32% CAGR.

Which service segment is most dominant in outsourced personal care production?

Pure manufacturing services dominate, accounting for 82.42% of market revenue in 2024 due to brands’ reliance on scalable GMP-compliant output.

Why is Asia-Pacific critical to future growth?

The region supplies 38.23% of global contract manufacturing value, benefits from dense supplier networks, and is projected to grow 14.01% annually through 2030.

How do new U.S. MoCRA regulations affect contract manufacturers?

All facilities must register, list products, and meet GMP standards by December 2025, elevating compliance costs but favoring well-capitalized operators.

What packaging format is gaining the fastest traction?

Aerosol applications show the fastest growth at a 12.97% CAGR, driven by dry shampoo, sun-care sprays, and advances in low-impact propellant systems.

How are indie and direct-to-consumer brands shaping demand?

These brands rely on low-minimum-order and quick-turnaround partners, accelerating project pipelines and reinforcing agile production models across the market.

Page last updated on: July 7, 2025