Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 33.58 Billion |

| Market Size (2026) | USD 34.97 Billion |

| Market Size (2031) | USD 43.56 Billion |

| Growth Rate (2026 - 2031) | 5.14% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Yogurt Market Analysis by Mordor Intelligence

The Europe yogurt market size was valued at USD 33.58 billion in 2025 and is estimated to grow from USD 34.97 billion in 2026 to reach USD 43.56 billion by 2031, at a CAGR of 5.14% during the forecast period (2026-2031). The demand for healthier and more sustainable food options is increasingly shifting toward recipes fortified with protein and those based on plant ingredients. At the same time, regulatory authorities are implementing mandates to reduce sugar content, which is compelling manufacturers to rethink and reshape their formulation strategies. Drinkable formats, such as ready-to-drink beverages, are gaining significant traction due to longer commute times and the growing popularity of on-the-go breakfasts. This trend is driving a notable increase in single-serve sales, particularly in urban areas where convenience is a priority. Plain yogurt is also experiencing a resurgence in demand as retailers adopt stricter front-of-pack nutrition labeling practices that discourage high-sugar stock-keeping units (SKUs). Additionally, the rising cost pressures associated with cold-chain logistics, which involve the transportation and storage of temperature-sensitive products, are encouraging manufacturers to explore aseptic cartons and pouches. These packaging solutions offer the advantage of being transported without refrigeration, providing a more cost-effective and efficient alternative for distribution.

Key Report Takeaways

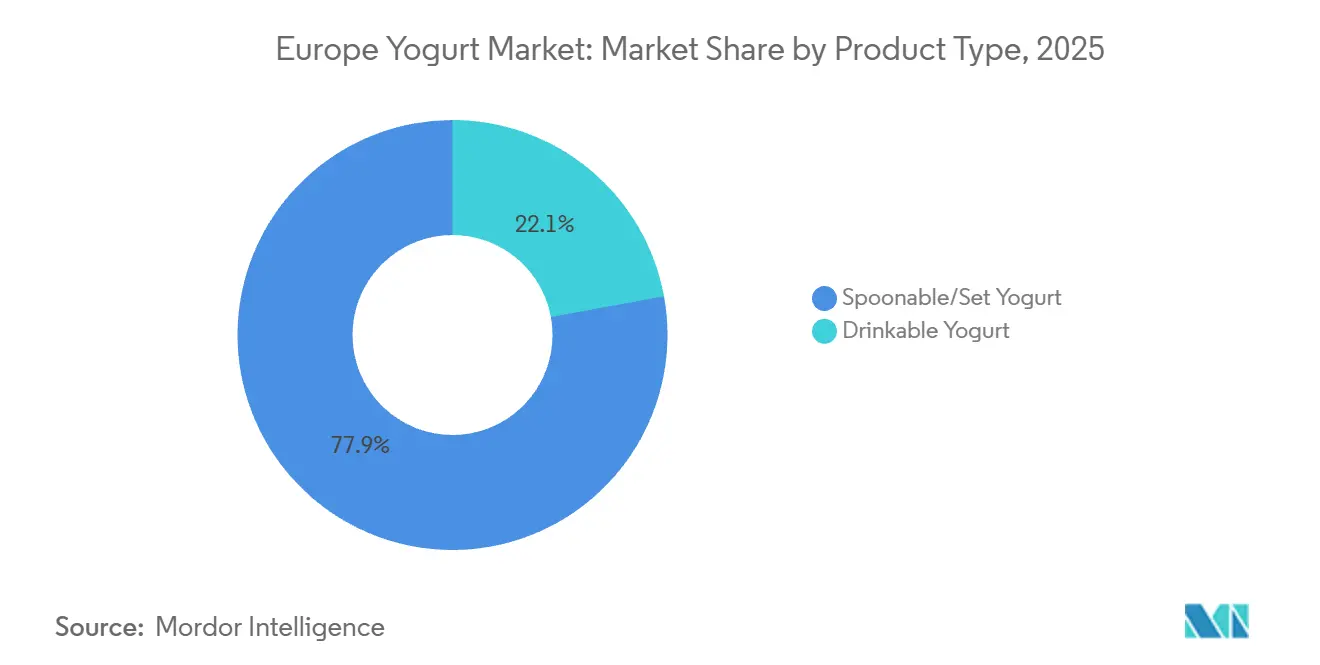

- By product form, spoonable styles led with 77.88% revenue share in 2025, whereas drinkable yogurts are projected to grow at 6.04% CAGR through 2031.

- By flavor profile, flavored yogurts held 70.43% of the share in 2025; plain/natural gained traction with a 6.05% CAGR through 2031.

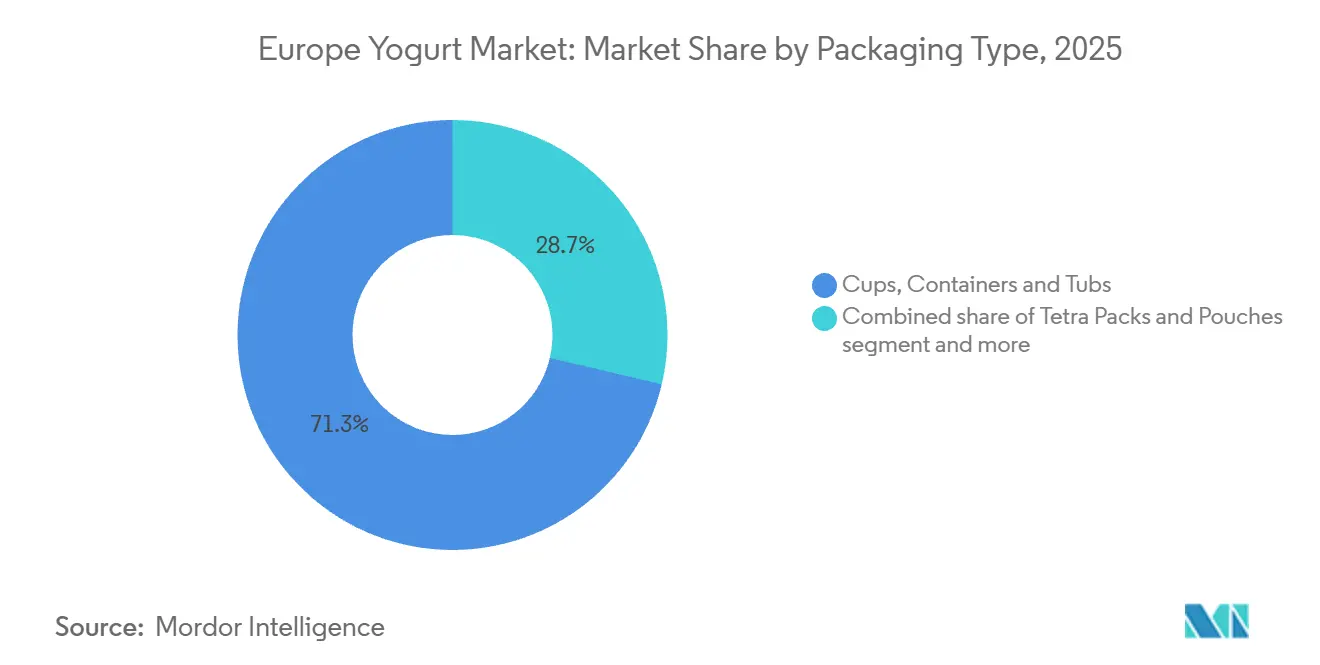

- By packaging, cups and tubs held 71.32% share in 2025; tetra packs and pouches are poised for a 6.19% CAGR, supported by EU single-use plastic restrictions.

- By distribution channel, off-trade dominated with 94.54% share in 2025, whereas on-trade outlets are projected to grow at a 5.43% CAGR through 2031.

- By geography, Germany contributed 18.73% of 2025 sales, while the United Kingdom market is forecast to expand at a 5.61% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Yogurt Market Trends and Insights

Drivers Impact Table*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rising demand for high-protein Greek yogurt among millennials | +0.8% | Western Europe (Germany, United Kingdom, France), Nordic markets | Medium term (2-4 years) |

| Flavor innovation using local fruits accelerating yogurt uptake | +0.6% | Southern Europe (Italy, Spain), France, Benelux | Short term (≤ 2 years) |

| Growth of on-the-go breakfast occasions boosting drinkable yogurt formats | +0.9% | Urban centers across Germany, United Kingdom, France, Netherlands | Short term (≤ 2 years) |

| Surge in lactose-free and digestive health claims accelerating non-dairy alternatives | +1.1% | Southern Europe (Italy, Spain), Central Europe (Poland, Czech Republic) | Long term (≥ 4 years) |

| Clean label and locally sourced ingredients aligned with sustainability preferences | +0.7% | Nordic markets (Sweden, Denmark), Germany, Netherlands | Medium term (2-4 years) |

| Health benefits including probiotics for gut health and immunity | +0.9% | Pan-European with concentration in Germany, France, United Kingdom | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising demand for high-protein Greek yogurt among millennials

Greek yogurt's high protein content, which typically ranges from 15 to 20 grams per 200-gram serving compared to 8 to 10 grams in conventional yogurt, makes it a functional food that resonates with millennials. This group, aged between twenty-eight and forty-two in 2026, values satiety and muscle recovery after exercise, making Greek yogurt a preferred choice. Millennials are contributing to steady volume growth in Western European markets, where gym memberships have been rising annually in recent years, according to fitness industry data. The strained production process of Greek yogurt removes whey, concentrating protein but also generating significant amounts of acid whey per liter of finished product. This creates a disposal challenge that manufacturers address through methods such as whey protein isolate extraction or anaerobic digestion for biogas. For example, FAGE's investment in whey-processing facilities in Greece and Danone's introduction of high-protein Oikos variants in Germany and the United Kingdom highlight strategic efforts to meet sustained millennial demand. However, price premiums over standard yogurt limit adoption among price-sensitive consumers. Projections indicate that Greek yogurt will stabilize at a significant category share by 2030, as its satiety benefits become standard and innovation shifts toward hybrid formats that combine Greek-style thickness with probiotic strains or plant-based proteins.

Flavor innovation using local fruits accelerating yogurt uptake

Regional fruit varieties, such as Sicilian blood orange, Asturian apple, and Polish black currant, play a significant role in differentiating premium yogurt lines. These varieties appeal to consumers who are increasingly seeking authentic and place-based food experiences. For example, Arla Foods introduced a Nordic berry collection in Sweden and Denmark in 2025. This collection features cloudberry and lingonberry sourced from cooperatives located within 200 kilometers of the production sites. By leveraging short supply chains that reduce the carbon footprint and support rural economies, this initiative achieved an 8% market share within six months. Additionally, flavor innovation in yogurt is not limited to fruit inclusions but also extends to savory profiles such as beetroot, carrot, and turmeric. These savory flavors position yogurt as a versatile ingredient suitable for dips and dressings, thereby broadening its consumption occasions beyond traditional breakfast and snack times. However, a key challenge lies in maintaining flavor stability and color retention throughout the product's shelf life, especially without relying on synthetic additives. Natural colorants, such as anthocyanins derived from elderberry or beta-carotene extracted from carrots, offer a partial solution to this issue but come with higher input costs. To address these challenges, companies like Lactalis and Nestlé are exploring encapsulation technologies. These technologies are designed to protect volatile flavor compounds and delay their release until the point of consumption. This approach enhances the sensory impact of the product while meeting clean-label requirements, which exclude artificial flavors and preservatives.

Growth of on-the-go breakfast occasions boosting drinkable yogurt formats

Drinkable yogurt's annual growth reflects a structural shift in European breakfast habits, driven by longer commute times and compressed morning routines. Single-serve bottles and pouches with integrated straws facilitate on-the-go consumption, gaining market share from cereal bars and pastries that require two-handed eating. Danone's Actimel and Müller's Froop To Go formats lead in impulse purchase channels such as convenience stores, fuel stations, and transit hubs, where chilled display cases and strategic point-of-sale placement encourage unplanned purchases. The format's appeal also extends to workplace wellness programs. Employers in countries like Germany and the Netherlands subsidize drinkable yogurt in vending machines as part of health initiatives aimed at reducing absenteeism and improving productivity, as supported by occupational health studies. Packaging innovation plays a critical role, with features such as resealable caps and ergonomic bottle designs that fit vehicle cup holders enhancing usability. Additionally, aseptic processing enables ambient-stable variants that do not require refrigeration, allowing penetration into vending and e-commerce channels while reducing logistics costs. The segment's growth potential depends on manufacturers' ability to maintain mouthfeel and probiotic viability in liquid formats. Emerging technologies such as high-pressure processing and microencapsulation are beginning to address these challenges.

Surge in lactose-free and digestive health claims accelerating non-dairy alternatives

The prevalence of lactose intolerance, which ranges from 15% in Northern Europe to 70% in Southern Italy, has driven consistent demand for lactose-free dairy products and plant-based alternatives [1]Source: National Institutes of Health, “Lactose Intolerance Prevalence,” nih.gov. These options address digestive discomfort while offering comparable nutritional profiles. Valio's lactose-free yogurt line, developed using lactase enzyme treatment to hydrolyze lactose into glucose and galactose, captured 12% of the Finnish market in 2025. The product successfully retains the taste and texture of dairy while eliminating gastrointestinal symptoms. Plant-based yogurts, made from oat, almond, and coconut bases, are gaining traction more rapidly in Western Europe. This growth is fueled by the rise of flexitarian diets and environmental concerns. However, these products face challenges related to protein content, mouthfeel, and the survival of probiotics in non-dairy formulations. Oatly's fermented oat-based yogurt, fortified with pea protein to provide 10 grams per serving, achieved distribution in 8,000 European retail outlets by late 2025. This success was supported by partnerships with coffee chains, which incorporated the product into breakfast bowls and smoothies. The regulatory environment remains fragmented. The European Court of Justice's 2017 ruling prohibits the use of terms like "yogurt" for plant-based products unless explicitly labeled as alternatives. This restriction complicates shelf placement and consumer education efforts.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Health concerns over lactose intolerance limiting dairy yogurt | -0.6% | Southern Europe (Italy, Spain, Greece), Eastern Europe | Long term (≥ 4 years) |

| High sugar content scrutiny in flavored varieties | -0.5% | Western Europe (United Kingdom, Germany, Netherlands), Nordic markets | Short term (≤ 2 years) |

| Strict regulations on sugar levels and additives | -0.4% | Pan-European with emphasis on United Kingdom, France, Germany | Medium term (2-4 years) |

| High cold-chain logistics costs for perishable distribution | -0.7% | Eastern Europe (Poland, Romania), peripheral regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Health concerns over lactose intolerance limiting dairy yogurt

Lactose intolerance affects an estimated 30% to 40% of Southern European populations, with prevalence reaching up to 70% in regions of Italy and Greece where lactase persistence, which is the genetic trait enabling adult lactose digestion, is less common compared to Northern Europe. This physiological limitation reduces dairy yogurt consumption and increases demand for lactose-free options and plant-based alternatives, leading to market fragmentation and complicating production planning for manufacturers with pan-European portfolios. The use of lactase enzyme treatment, which hydrolyzes lactose into glucose and galactose, increases production costs by 5% to 8% and necessitates dedicated processing lines to prevent cross-contamination. This requirement poses a significant challenge for smaller dairies, which may find the capital investment difficult to justify. Consumer education remains a key challenge, as many lactose-intolerant individuals avoid all dairy products despite yogurt's naturally lower lactose content due to bacterial fermentation, which partially breaks down lactose during production. The impact of this restraint is most significant in Southern and Eastern Europe, where lactose intolerance prevalence is highest, but awareness of lactose-free options and plant-based alternatives lags behind that of Western markets. In response, manufacturers are adopting hybrid strategies by expanding lactose-free dairy product lines while investing in plant-based research and development to address both segments. However, these efforts are complicated by risks of cannibalization and margin dilution, making portfolio management more challenging.

High sugar content scrutiny in flavored varieties

Flavored yogurt, with a sugar content often ranging from 12% to 18% per 150-gram serving, comparable to that of soft drinks, has come under increasing scrutiny from public health authorities and consumer advocacy groups due to concerns about obesity and metabolic diseases. In the United Kingdom, a voluntary sugar-reduction program aims to achieve a 20% reduction in yogurt sugar content by 2025. This initiative has led major brands to reformulate their products, with some manufacturers replacing sucrose with alternatives such as stevia, monk fruit extract, or erythritol to maintain sweetness while lowering caloric content [2]Source: UK Government, “Sugar Reduction Programme,” gov.uk. However, these natural sweeteners come with higher input costs as stevia, for instance, is 3 to 5 times more expensive than sugar per kilogram and present aftertaste challenges that consumer testing identifies as a barrier to repeat purchases, particularly among children, a key consumer group. Front-of-pack nutrition labeling schemes, such as Nutri-Score in France and traffic-light labels in the United Kingdom, penalize high-sugar products with lower ratings. These ratings influence consumer purchase decisions and encourage manufacturers to reformulate products to achieve more favorable scores. The impact of these measures is most pronounced in Western Europe, where health consciousness and regulatory pressures are strongest, but the effects are also extending to Southern and Eastern European markets as European Union (EU)-wide nutrition policies work to harmonize standards. Manufacturers face a strategic challenge as aggressively reducing sugar content risks alienating taste-driven consumers, while maintaining current formulations could lead to regulatory action and reputational harm as public health campaigns gain momentum.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Form: Drinkable Formats Gain Traction

Spoonable or set yogurt accounted for 77.88% of the market share in 2025, reflecting its established role in European breakfast habits and snacking occasions. However, drinkable yogurt is projected to grow at an annual rate of 6.04% through 2031, driven by urbanization and the increasing preference for portable, single-handed consumption among time-constrained consumers. The growth of the drinkable yogurt segment is primarily concentrated in Western Europe, where average commute times range from 45 to 60 minutes in major metropolitan areas, and convenience stores have expanded along transit routes. Products like Danone's Actimel, which highlights immune-support claims linked to Lactobacillus casei DN-114001, and Müller's Froop To Go, which emphasizes fruit content and resealable packaging, illustrate the segment's evolution from functional health shots to mainstream breakfast alternatives.

Spoonable yogurt maintains its dominance due to its versatility, serving as a base for granola, fruit, and honey, and its superior mouthfeel which liquid formats struggle to replicate without the use of stabilizers such as pectin or modified starch. However, the drinkable yogurt format faces challenges in preserving probiotic viability. In liquid matrices, shear forces during processing and lower viscosity expose probiotics to oxygen and pH fluctuations, reducing colony-forming units by 30% to 50% over the product's shelf life. Aseptic processing and high-pressure treatment provide partial solutions, enabling ambient-stable drinkable yogurts that can be distributed through electronic commerce (e-commerce) and vending channels without cold-chain requirements. However, these methods often result in reduced probiotic counts, which can weaken the health-related positioning of these products.

By Flavor Profile: Plain Yogurt's Comeback

Flavored yogurt accounted for 70.43% of sales in 2025, driven by consumer preferences for sweetness and variety. However, plain or natural yogurt is projected to grow at an annual rate of 6.05% through 2031, supported by clean-label trends and sugar-reduction mandates. These factors are repositioning unsweetened yogurt as a versatile ingredient rather than solely a standalone snack. The growth of plain yogurt is particularly notable in Nordic markets and Germany, where culinary traditions incorporate yogurt into savory dishes such as tzatziki, marinades, and salad dressings. Additionally, health-conscious consumers often customize sweetness levels by adding honey, fruit, or granola. The plain yogurt segment also benefits from lower production costs, as the absence of flavoring, fruit preparation, and sweeteners reduces manufacturing expenses by 15% to 20%. This cost advantage allows plain yogurt to compete effectively on price, particularly in discount channels, which now represent over 40% of yogurt sales in Germany and the Netherlands.

Flavored yogurt remains dominant among children and adolescents, whose taste preferences lean toward sweetness and novelty flavors such as cookies and cream or salted caramel. These flavors drive both trial and repeat purchases. However, the segment faces challenges in reformulating products to reduce sugar content without compromising taste. While natural sweeteners and flavor-masking technologies offer partial solutions, they come with higher input costs, which place pressure on profit margins.

By Packaging Type: Sustainable Formats Accelerate

Cups, containers, and tubs accounted for 71.32% of packaging in 2025, highlighting their prominence in household consumption and bulk-purchase formats, which provide cost advantages for families and frequent users. Tetra Packs and pouches are projected to grow at an annual rate of 6.19% through 2031, driven by factors such as sustainability preferences, extended shelf life, and suitability for on-the-go consumption, which aligns with the growth of drinkable yogurt. Aseptic carton packaging eliminates the need for refrigeration for ambient-stable yogurts, reducing cold-chain costs by 15% to 20% and facilitating entry into vending, e-commerce, and export channels where temperature control is challenging.

Pouches with integrated spouts appeal to children and active consumers by offering portability and portion control. However, they face recycling challenges due to the difficulty of separating and reprocessing multi-layer laminates, which include polyethylene, aluminum, and polyester, in municipal waste streams. Bottles, a smaller segment of the packaging mix, cater to drinkable formats and command premium pricing in convenience channels but contribute to plastic waste concerns, attracting regulatory scrutiny and consumer criticism in environmentally conscious markets. Cups and containers maintain their dominance due to their versatility, accommodating spoonable and Greek-style yogurts, and their recyclability, as polypropylene and polystyrene materials are widely accepted in European recycling systems. However, contamination from residual yogurt reduces actual recycling rates to 30% to 40%.

By Distribution Channel: Off-Trade Dominance Persists

In 2025, off-trade channels accounted for 94.54% of yogurt sales, encompassing supermarkets, hypermarkets, convenience stores, and online retail, which primarily serve household consumption and bulk purchases. In contrast, on-trade venues, including cafés, quick-service restaurants, and workplace canteens, are projected to grow at an annual rate of 5.43% through 2031. This growth is attributed to foodservice operators incorporating yogurt into breakfast menus, smoothie bowls, and snack offerings, highlighting health benefits and customization options. Supermarkets and hypermarkets dominate the off-trade segment due to their extensive chilled display cases and promotional activities that drive higher sales volumes. However, these outlets face margin pressures from discount chains such as Aldi and Lidl, which captured 28% of German yogurt sales in 2025 through private-label products priced 20% to 30% lower than branded alternatives. Convenience stores and fuel stations cater to impulse purchases and on-the-go consumption, commanding price premiums of 15% to 25%, which help offset lower transaction volumes. Meanwhile, online retail, though still in its early stages for yogurt sales, is experiencing double-digit growth. This growth is supported by subscription services and same-day delivery options, which simplify the purchase of perishable goods. According to the International Trade Administration, Europe is the third-largest retail e-commerce market globally, with an annual growth rate exceeding 9% [3]Source: International Trade Administration, “European Retail eCommerce,” trade.gov.

On-trade growth is primarily concentrated in urban areas, where café culture and workplace wellness programs create new consumption occasions beyond traditional meal times. Yogurt is increasingly positioned as a healthier alternative to pastries and energy drinks. However, the segment faces challenges in maintaining cold-chain integrity and managing spoilage in venues with limited refrigeration capacity. These issues are partially mitigated by ambient-stable formats and single-serve packaging solutions.

Geography Analysis

Germany is projected to account for 18.73% of regional revenue in 2025. This is attributed to its large population, high per-capita dairy consumption, and a well-established retail infrastructure that supports extensive chilled distribution networks. France, Italy, and Spain collectively represent 28% to 30% of the market. France's strong yogurt culture, highlighted by Danone's origins and the popularity of fromage blanc, sustains high per-capita consumption. Meanwhile, Italy and Spain face challenges due to the prevalence of lactose intolerance and a preference for alternative dairy products such as cheese and milk. These factors make Germany and France key contributors to the regional market, while Italy and Spain encounter specific hurdles in maintaining growth.

The United Kingdom is expected to grow at the fastest annual rate of 5.61% through 2031. This growth is driven by the introduction of probiotic-enriched products, strong private-label competition, and health campaigns promoting yogurt consumption for digestive health and immune support. The increasing focus on health and wellness among consumers in the United Kingdom has created a favorable environment for innovation in yogurt products. These factors, combined with aggressive marketing strategies, position the United Kingdom as the fastest-growing market in the region over the forecast period.

Poland, Sweden, and the Rest of Europe, including the Czech Republic, Romania, and Hungary, present growth opportunities due to rising incomes, westernizing diets, and underdeveloped retail channels. Multinational brands are targeting these markets through local partnerships and tailored product formulations. Poland's yogurt market is expanding as modern trade formats replace traditional shops and health awareness increases among urban middle-class consumers, although price sensitivity limits the development of the premium segment. In Sweden, high organic product penetration and environmental awareness drive demand for sustainably produced yogurt with carbon-neutral certifications. These products command a 15% to 20% price premium and attract environmentally conscious consumers willing to pay more for ecological benefits. The geographic landscape through 2031 will also be shaped by income convergence in Eastern Europe, aging populations in Western markets prioritizing functional nutrition, and regulatory harmonization under European Union (EU) frameworks that standardize labeling and health-claim requirements. Competitive advantages will favor brands that localize flavor profiles, adjust pricing to income levels, and effectively navigate fragmented retail landscapes where regional cooperatives and local brands maintain strong market positions.

Competitive Landscape

The Europe yogurt market demonstrates moderate concentration, with multinational dairy companies such as Danone, Lactalis, Arla, and Nestlé holding significant market shares. These players are complemented by regional cooperatives and emerging plant-based specialists that leverage niche positioning and local authenticity. Strategic trends in the market highlight portfolio diversification across both dairy and non-dairy categories. For example, Danone's acquisition of plant-based brands and Nestlé's investment in precision fermentation reflect strategies to mitigate risks associated with fluctuating milk prices and regulatory uncertainties concerning dairy's environmental impact.

White-space opportunities in the market include hybrid product formats, such as yogurt-smoothie blends and savory yogurt dips, as well as functional enhancements like adaptogens, collagen, and omega-3 fatty acids. These innovations cater to specific health outcomes and support premium pricing strategies. Emerging disruptors, such as The Coconut Collaborative and smaller oat-based brands, are capitalizing on direct-to-consumer channels and sustainability-focused narratives to attract environmentally conscious consumers. However, these smaller players face challenges related to scaling operations, national distribution, and maintaining competitive margins due to capital constraints.

Technological advancements in the market are centered on cold-chain optimization. The use of Internet of Things (IoT) sensors and predictive analytics has reduced spoilage rates by 10% to 15% through real-time temperature monitoring and dynamic routing that adjusts to traffic and weather conditions. Danone's collaboration with logistics providers to implement blockchain-based traceability systems has improved supply chain transparency and bolstered sustainability claims. Similarly, Arla's investment in renewable-energy-powered refrigeration at distribution centers has reduced carbon intensity, aligning with corporate net-zero goals. Patent activity in encapsulation technologies, which protect probiotics and flavor compounds, and innovations in aseptic processing that extend shelf life without preservatives, highlight key research and development (R&D) priorities. These advancements aim to enhance product performance while reducing distribution costs. The competitive landscape through 2031 is expected to favor established players with scale advantages in procurement, production, and distribution. However, opportunities remain for agile entrants to address regulatory gaps, underserved market segments, and shifting consumer preferences more rapidly than legacy companies can adapt their portfolios and go-to-market strategies.

Europe Yogurt Industry Leaders

Danone SA

Groupe Lactalis S.A.

Arla Foods amba

Theo Müller Group

Nestlé SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Lactalis acquired General Mills’ yogurt businesses for USD 2.1 billion, incorporating Yoplait and Go-Gurt into its global portfolio, further expanding its presence in the international dairy market.

- May 2025: Valio and Borealis introduced recycled-polypropylene yogurt cups, aligning with the European Union's circular economy objectives, demonstrating their commitment to sustainability and innovation in packaging solutions within the food industry.

- April 2025: Atlante launched new products developed by its Research and Development team, incorporating innovation and traditional Greek elements. The Indulgent Yogurt Range featured a 5% fat base balancing taste and nutrition.

Europe Yogurt Market Report Scope

Yogurt is a food produced by the bacterial fermentation of milk. The Europe yogurt market is segmented by product form, flavor profile, packaging type, distribution channel, and geography. Based on product form, the market is segmented into spoonable/set yogurt and drinkable yogurt. Based on flavor profile, the market is segmented into plain/natural and flavored. By packaging type, the market is divided into cups, containers and tubs, bottles, tetra paks and pouches and others. Based on distribution channels, the market is segmented into off-trade (hypermarkets/supermarkets, convenience stores, online retail channels, and other distribution channels) and on-trade. Based on geography, the market is segmented into United Kingdom, Germany, France, Italy, Spain, Russia, and the Rest of Europe. The market sizing has been done in value terms in USD and volume in tonnes for all the abovementioned segments.

By Product Form

| Spoonable/Set Yogurt |

| Drinkable Yogurt |

By Flavor Profile

| Plain/Natural |

| Flavored |

By Packaging Type

| Cups, Containers and Tubs |

| Bottles |

| Tetra Packs and Pouches |

| Others |

By Distribution Channel

| On-trade | |

| Off-trade | Supermarkets and Hypermarkets |

| Convenience Stores | |

| Online Retail | |

| Others |

By Geography

| Germany |

| United Kingdom |

| Italy |

| France |

| Spain |

| Netherlands |

| Poland |

| Belgium |

| Sweden |

| Rest of Europe |

| By Product Form | Spoonable/Set Yogurt | |

| Drinkable Yogurt | ||

| By Flavor Profile | Plain/Natural | |

| Flavored | ||

| By Packaging Type | Cups, Containers and Tubs | |

| Bottles | ||

| Tetra Packs and Pouches | ||

| Others | ||

| By Distribution Channel | On-trade | |

| Off-trade | Supermarkets and Hypermarkets | |

| Convenience Stores | ||

| Online Retail | ||

| Others | ||

| By Geography | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

Key Questions Answered in the Report

How large will European demand for yogurt be by 2031?

The Europe yogurt market is forecast to reach USD 43.56 billion by 2031, reflecting a 4.49% CAGR from 2026.

Which product form is rising fastest?

Drinkable yogurt leads growth at a 6.04% CAGR thanks to commuter-driven, on-the-go breakfast needs.

Why is plain yogurt gaining share?

Clean-label trends and sugar-reduction policies push shoppers toward unsweetened bases they can flavor themselves.

Which packaging innovation matters most now?

Aseptic cartons and pouches that avoid refrigeration are expanding at 6.19% per year while trimming cold-chain costs.

Where is geographic growth strongest?

The United Kingdom shows the quickest rise, expected at a 5.61% CAGR through 2031 on probiotic launches and private-label momentum.

Page last updated on: