Market Overview

| Study Period | 2021 - 2031 |

|---|---|

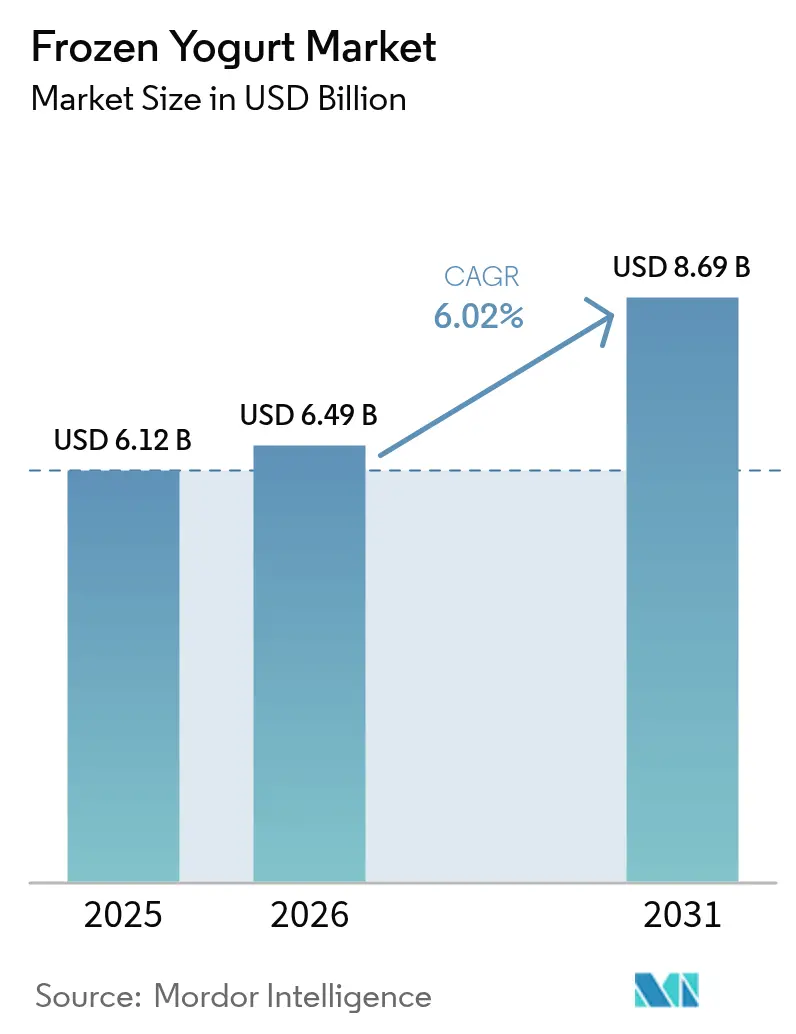

| Market Size (2026) | USD 6.49 Billion |

| Market Size (2031) | USD 8.69 Billion |

| Growth Rate (2026 - 2031) | 6.02% CAGR |

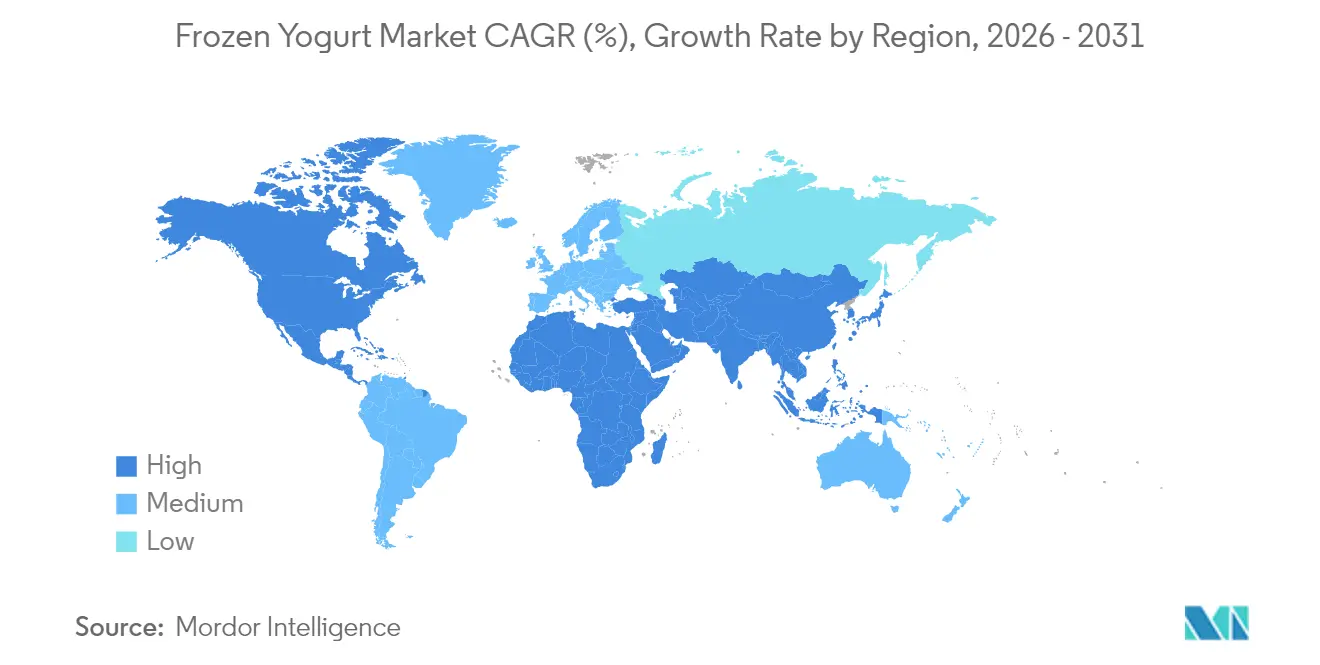

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Frozen Yogurt Market Analysis by Mordor Intelligence

The frozen yogurt market size in 2026 is estimated at USD 6.49 billion, growing from 2025 value of USD 6.12 billion with 2031 projections showing USD 8.69 billion, growing at 6.02% CAGR over 2026-2031. This growth is primarily driven by increasing consumer preference for desserts that combine indulgence with health benefits. Manufacturers are responding by incorporating probiotics, reducing sugar content, and focusing on clean-label ingredients to meet these demands. The introduction of plant-based alternatives is further expanding the market, while self-serve retail formats and easy-to-use digital ordering platforms are transforming the shopping experience. Additionally, regulatory support, such as the FDA's updated "healthy" definition set to take effect in February 2025, is encouraging the development of lower-sugar products, giving frozen yogurt a competitive advantage over traditional ice cream. The Asia-Pacific region is expected to witness the fastest growth, supported by rising urban incomes, while North America remains the leading market due to its well-established franchise networks and widespread smartphone usage, which facilitates loyalty app engagement.

Key Report Takeaways

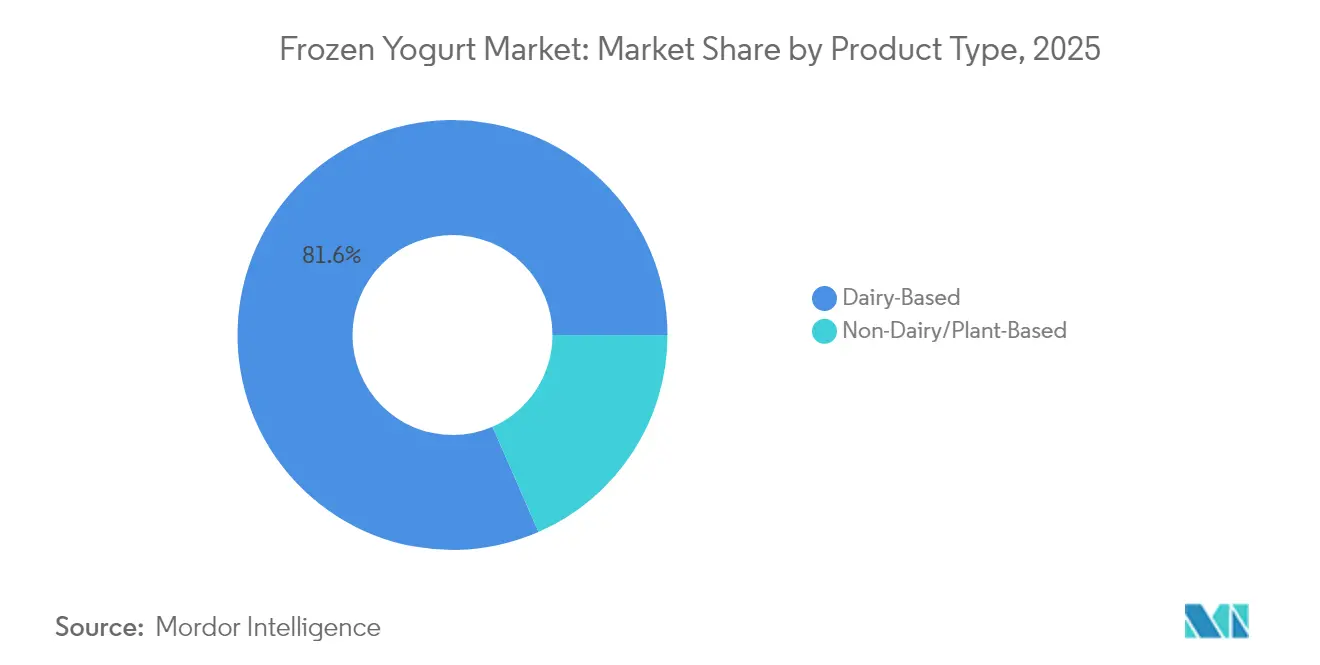

- By type, dairy-based products led with 81.55% revenue share in 2025; the non-dairy segment is forecast to expand at an 11.07% CAGR to 2031.

- By flavor, flavored variants captured 82.74% of the frozen yogurt market share in 2025; plain offerings are projected to post a 5.28% CAGR through 2031.

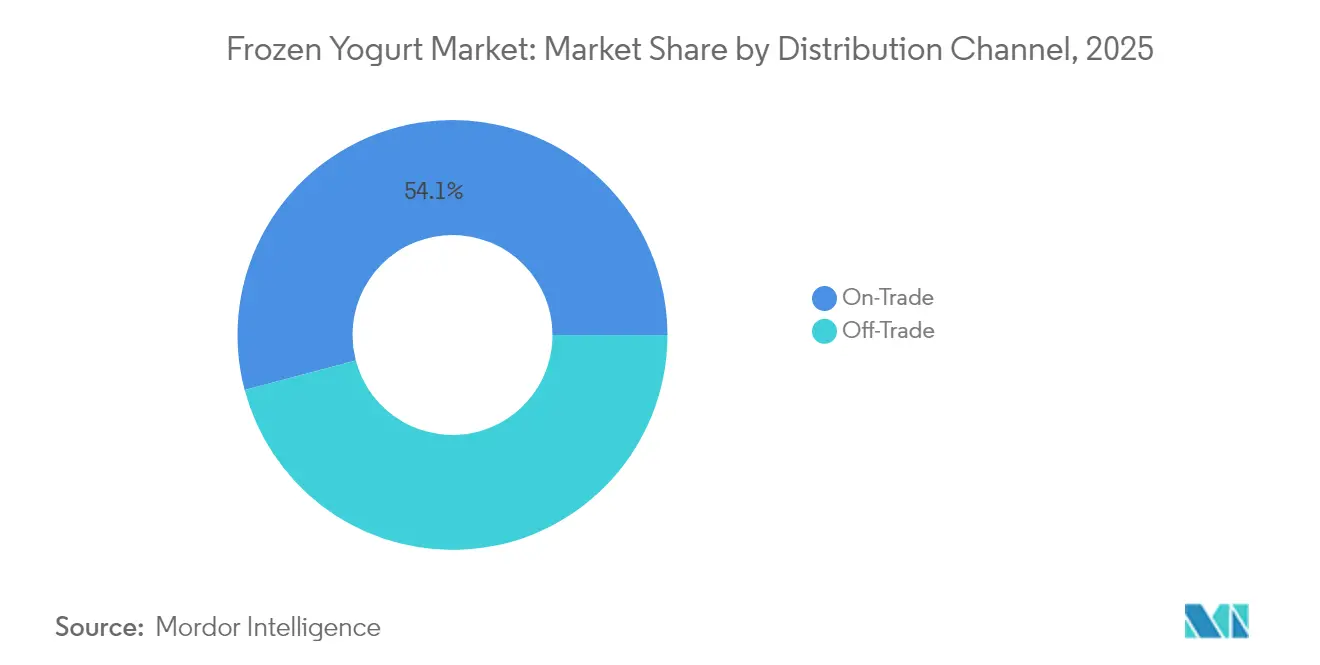

- By distribution channel, off-trade venues accounted for 45.88% of the frozen yogurt market size in 2025, while on-trade outlets are poised to advance at a 12.86% CAGR between 2026 and 2031.

- By packaging, cups and tubs commanded 66.78% revenue share in 2025; cones and sticks are expected to grow at a 8.74% CAGR during the same period.

- By geography, North America contributed 38.02% of global revenue in 2025; Asia-Pacific is the fastest-growing region with a projected 10.52% CAGR from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Frozen Yogurt Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising flexitarian demand for dairy-alternative desserts | +1.8% | North America, Europe, Australia | Medium term (3-4 years) |

| Proliferation of self-serve frozen yogurt retail formats | +1.2% | Global, with concentration in urban centers | Short term (≤ 2 years) |

| Product premiumization through probiotic fortification driving repeat purchases | +1.5% | North America, Europe, Japan, South Korea | Medium term (3-4 years) |

| E-commerce expansion increasing at-home consumption frequency | +1.0% | Global, with higher impact in developed markets | Short term (≤ 2 years) |

| Flavor innovation and customization | +0.8% | Global | Short term (≤ 2 years) |

| Government sugar-reduction initiatives favoring low-fat yogurt over ice-cream | +0.6% | Europe, North America | Long term (≥ 5 years) |

| Source: Mordor Intelligence | |||

Rising Flexitarian Demand for Dairy-Alternative Desserts

Flexitarian diets are transforming the frozen yogurt market, as consumers gravitate towards plant-based options while still enjoying some dairy. This shift has spurred advancements in non-dairy frozen yogurt, now boasting flavors and textures rivaling their dairy counterparts. Research from Food Chemistry in 2024 highlights that oat-based milk substitutes, specifically those with 20% oats and 0.5% xanthan gum, offer rheological and sensory qualities on par with traditional dairy. Additionally, the incorporation of other plant-based ingredients, such as almond and coconut milk, is further diversifying product offerings to cater to varying consumer preferences. While The Good Food Institute notes a minor dip in plant-based food sales in 2023, there has been a notable uptick in governmental backing for plant-based research. Canada has pledged CAD 150 million, joined by Germany and the United Kingdom, all bolstering alternative protein research and development. This collective support fosters a thriving environment for the evolution of non-dairy frozen yogurt, with manufacturers leveraging these investments to enhance production processes and expand distribution networks.

E-commerce Expansion Increasing At-Home Consumption Frequency

Digital platforms are reshaping how consumers relish frozen yogurt, shifting from in-store purchases to the convenience of home delivery. Yogurtland's three-year growth streak, driven by its digital push, underscores the power of savvy online strategies. But this digital shift isn't just about making sales; it's about engaging customers, paving the way for tailored marketing and loyalty initiatives. Highlighting the trend's importance, the U.S. Department of Agriculture points out the growing role of online grocery shopping in accessing nutritious foods. With programs like SNAP backing online purchases, healthier dessert choices, including frozen yogurt, stand to gain. Additionally, the integration of advanced technologies such as artificial intelligence and data analytics is enabling frozen yogurt brands to better understand consumer preferences, optimize supply chains, and enhance customer experiences. This evolution is especially crucial for frozen yogurt brands aiming to broaden their reach beyond conventional retail avenues.

Flavor Innovation and Customization

In the frozen yogurt market, flavor innovation and customization stand out as pivotal differentiators. Manufacturers are broadening their flavor portfolios, aiming to captivate consumers and encourage repeat purchases. A study in Frontiers in Food Science and Technology reveals that adding fruits or fruit pulp to yogurts not only boosts sensory appeal but also enriches nutritional value, owing to bioactive compounds like polyphenols and dietary fibers. The International Dairy Foods Association's Yogurt & Cultured Innovation Conference underscored flavor experimentation as a primary growth catalyst, dedicating sessions to engage claims-driven consumers and spur yogurt category innovations. Manufacturers, venturing beyond conventional fruit flavors, are delving into unique combinations and functional additives. Research indicates that ingredients such as coffee extracts and Spirulina not only elevate sensory qualities but also bolster health advantages. This trend of customization is most pronounced in self-serve venues, where patrons curate their unique blends of flavors and toppings, mirroring a wider consumer shift towards personalized culinary experiences.

Government Sugar-Reduction Initiatives Favoring Low-Fat Yogurt over Ice-Cream

Government-led initiatives to reduce sugar are favoring frozen yogurt over traditional ice cream, prompting reformulations and steering consumers towards healthier choices. Germany's Federal Ministry of Food and Agriculture has rolled out a National Reduction and Innovation Strategy, targeting a 15% sugar cut in sweetened dairy products by 2025 [1]Source: Federal Ministry of Agriculture, Food, and Regional Identity, "The National Reduction and Innovation Strategy for Sugar, Fats and Salt in Processed Foods,"bmel.de. This aligns with the broader European Union goals of promoting healthier diets and reducing obesity rates. Additionally, the USDA is reshaping school meal programs, capping added sugars in yogurts at 12 grams per 6 ounces starting July 1, 2025, and instituting a weekly added sugar limit by July 1, 2027. These measures are part of a larger strategy to combat childhood obesity and encourage healthier eating habits among students. These regulatory shifts are pushing manufacturers to rethink their formulations. Research into low-sugar dairy products is increasingly spotlighting alternative sweeteners like monkfruit and allulose, helping brands cut sugar without losing consumer appeal. Furthermore, advancements in food technology are enabling manufacturers to enhance the texture and taste of low-sugar frozen yogurt, ensuring it remains competitive in the market.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Seasonal demand fluctuations | -0.9% | Global, more pronounced in regions with distinct seasons | Short term (≤ 2 years) |

| Cold-chain energy costs undermining margin in developing regions | -1.2% | Asia-Pacific, Middle East and Africa, South America | Medium term (3-4 years) |

| Limited shelf-life restricts long-haul exports | -0.7% | Global, especially affecting cross-continental trade | Medium term (3-4 years) |

| Limited penetration in emerging markets | -0.5% | Africa, parts of Asia, rural areas globally | Long term (≥ 5 years) |

| Source: Mordor Intelligence | |||

Seasonal Demand Fluctuations

Frozen yogurt businesses grapple with operational hurdles due to seasonal consumption patterns. Demand surges in warmer months but plummets in colder ones. This cyclical trend compels companies to devise strategies to stabilize revenue throughout the year. To counteract off-peak lulls, businesses have turned to seasonal promotions and exclusive product launches. Additionally, some companies are leveraging loyalty programs and partnerships with delivery platforms to drive consistent sales regardless of the season. The challenge of seasonality hits self-serve outlets especially hard. With their high fixed costs, these establishments must deftly manage staffing and inventory to stay profitable during leaner times. Monthly operating costs for frozen yogurt shops, especially in urban locales, range from USD 2,500-7,500 for rent, with staffing consuming 30-40% of total revenue and utilities accounting for 8-15% of monthly expenses. This financial landscape intensifies the pressure during seasonal slumps, prompting some businesses to explore diversification into complementary products, such as smoothies or hot beverages, to mitigate revenue fluctuations.

Limited Shelf-Life Restricts Long-Haul Exports

Frozen yogurt's short shelf life poses a significant hurdle for cross-border and long-haul exports. Even in optimal refrigerated conditions (around 10°C), stirred-type yogurts and yogurt beverages have a shelf-life of just 17 to 19 days, which plummets to as little as 12 days at 25°C. These numbers underscore the product's fragility, being acutely sensitive to temperature changes during transit. Consequently, ensuring cold chain logistics over extended distances becomes a daunting technical challenge and a costly endeavor. The potential for spoilage, coupled with the threat of product recalls and diminished consumer trust, deters brands from exploring distant export markets, leading them to prioritize regional or domestic distribution. Guidance from regulatory bodies, such as Food Standards Scotland, underscores the challenge of ensuring product safety and quality throughout the shelf life, especially for perishable items like frozen yogurt. Factors like microbiological stability, pH levels, and water activity can quickly decline without stringent storage measures. While innovations like modified atmosphere packaging (MAP) and active antimicrobial films can extend shelf-life, they often fall short of making long-haul exports feasible or financially viable.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Plant-Based Alternatives Gain Momentum

In 2025, dairy-based frozen yogurt commands a dominant 81.55% market share, owing to established consumer familiarity and robust supply chains. Innovations in probiotic fortification bolster this segment's strength, with research highlighting dairy-based frozen yogurt's ability to sustain probiotic viability above 8.5 log CFU/mL even after 30 days of storage. Flavor experimentation remains a key driver of consumer interest in the dairy segment, as manufacturers delve into novel combinations and functional additives to elevate both taste and nutritional value.

Although the non-dairy/plant-based segment is boasting a projected CAGR of 11.07% from 2026 to 2031, this surge is fueled by advancements in formulation technology, enhancing taste and texture. With rising lactose intolerance globally, brands are rolling out diverse products to cater to these consumers. There's a notable uptick in demand for dairy-free flavored yogurts crafted from plant-based ingredients like soy, oats, coconuts, and rice. In response, market players are unveiling innovative products to capture a larger share. A case in point: In February 2024, Danone Canada launched a new line of plant-based yogurts, crafted from Canadian pea protein, in two flavors: Key Lime and Vanilla.

By Flavor: Customization Drives Consumer Engagement

In 2025, flavored frozen yogurt dominates the market, seizing a robust 82.74% share, fueled by consumers' desires for variety and indulgence. Both the ice cream and yogurt sectors are embracing a trend of flavor experimentation, with manufacturers exploring unique combinations to differentiate themselves in a saturated market. Flavored yogurts are on the rise, showcasing a diverse range of flavors and types. Offerings now include green yogurt, plant-based variants, and specialty selections like lactose-free and high-protein options, catering to a broad spectrum of consumer tastes. Industry giants like General Mills Inc., Drums Food International, and Chobani are spearheading innovations that have significantly propelled flavored yogurt consumption.

Plain frozen yogurt, while holding a modest 17.26% market share, is poised for growth, projected to expand at a CAGR of 5.28% from 2026 to 2031. This segment appeals mainly to health-conscious consumers and those seeking a customizable base for toppings. The growth is further supported by rising consumer awareness about added sugars, with 66% of US consumers actively steering clear of them, according to the International Food Information Council 2024 report . Moreover, plain varieties stand to benefit from regulatory changes, as the FDA's updated Nutrition Facts label and the new "healthy" definition lean towards lower-sugar options.

By Distribution Channel: On-Trade Venues Evolve Beyond Traditional Models

In 2025, off-trade channels dominate the frozen yogurt market, accounting for 45.88% of sales. Supermarkets, hypermarkets, convenience stores, and online platforms ensure consumers have easy access to take-home frozen yogurt. The importance of these channels is highlighted by institutional contracts, such as Brevard Public Schools' deal with Gord on Food Service. This agreement ensures frozen yogurt delivery to around 87 district facilities from 2024 through 2029. Additionally, programs by the U.S. Department of Agriculture bolster this segment by promoting access to nutritious foods, including frozen yogurt, via retail channels. Innovations in packaging further enhance this channel's appeal, as they protect products and extend shelf life, ensuring the quality of frozen yogurt is upheld throughout its journey.

On-trade channels are set to witness the most rapid expansion, with a projected CAGR of 12.86% from 2026 to 2031. This growth is fueled by the transformation of frozen yogurt outlets into vibrant social hubs, moving beyond their traditional role as dessert stops. A prime example is Australia's Yo-Chi, which has grown to 38 locations by extending hours and crafting inviting atmospheres, positioning itself as a nightlife alternative for younger patrons. Moreover, technological advancements are revolutionizing the on-trade scene. Automated vending solutions, for instance, are proving to be more cost-effective than traditional franchises like Bella's. The International Dairy Foods Association underscores the significance of innovation in on-trade formats, especially in customization and experiential offerings, as key drivers for consumer engagement and market expansion.

By Packaging Type: Sustainability Reshapes Container Choices

In 2025, cups and tubs dominate the frozen yogurt packaging market with a 66.78% share, offering versatility for both single servings and take-home options. Their widespread appeal stems from their adaptability, particularly in self-serve establishments where accommodating toppings and mix-ins is crucial. Recent advancements in cup and lid designs have improved functionality and enhanced brand differentiation, focusing on preserving product quality and ensuring consumer convenience. Additionally, the segment is experiencing a shift toward sustainability, with brands increasingly adopting bioplastics and other eco-friendly materials to align with the preferences of environmentally conscious consumers.

While cones and sticks currently represent a smaller portion of the market, they are experiencing rapid growth, with a projected CAGR of 8.74% from 2026 to 2031. This growth is driven by increasing consumer demand for convenient, on-the-go formats that offer portion control. Innovations in this segment include squeeze tubes and other portable packaging solutions designed for mobile consumption, catering to busy consumers seeking healthier snack alternatives. Furthermore, advancements in packaging materials are enhancing product protection, extending shelf life, and ensuring frozen yogurt quality throughout the supply chain.

Geography Analysis

In 2025, North America commands a 38.02% share of the frozen yogurt market, buoyed by its established self-serve retail framework and a pronounced consumer shift towards healthier dessert choices. Regulatory shifts, notably the FDA's revamped "healthy" definition set to take effect in February 2025, are tilting the competitive balance in favor of lower-sugar frozen yogurt variants. Complementing this, the U.S. Department of Agriculture champions programs that bolster access to nutritious foods, frozen yogurt included. Further underscoring the U.S. dairy sector's global prowess, the National Milk Producers Federation and U.S. Dairy Export Council revealed a robust USD 8.1 billion in dairy exports for 2023, accounting for 17% of the nation's total milk output .

Asia-Pacific is on a rapid ascent, eyeing a CAGR of 10.52% from 2026 to 2031, spurred by urbanization, rising incomes, and evolving dietary habits. Rapid urbanization, rising disposable incomes, and a shift toward healthier dessert alternatives are significantly driving this surge. The growing prevalence of lactose sensitivity and an increasing demand for probiotic-rich functional foods are further propelling consumption. Additionally, government-backed initiatives aimed at modernizing the dairy sector are playing a crucial role. The expansion of organized retail, particularly in India and Southeast Asia, as highlighted in the OECD-FAO Agricultural Outlook 2024–2033, is further accelerating market penetration.

In Europe, rising health consciousness and demand for low-fat, probiotic-rich desserts are fueling innovation, with premium players launching indulgent yet guilt-free options to attract urban millennials. South America shows steady expansion driven by growing middle-class incomes and increased availability of frozen yogurt in supermarkets, although price sensitivity limits premiumization. Meanwhile, in the Middle East and Africa, rising tourism and Western dining concepts are popularizing frozen yogurt, especially in affluent Gulf markets where mall culture drives foot traffic to frozen dessert kiosks.

Competitive Landscape

The frozen yogurt market is moderately fragmented, with both multinational corporations and regional players vying for market share. Major companies such as General Mills Inc., Danone S.A., Unilever PLC, and Nestle S.A. lead the market, leveraging their global presence and resources. Meanwhile, regional players are carving out niches by catering to local tastes and preferences. To address the growing demand for diverse flavors, key players are focusing on product and flavor innovation. They are also pursuing mergers and acquisitions to strengthen their market positions and expand their reach.

In response to rising demand, companies are broadening their reach. For instance, in April 2025, Lactalis Canada, a prominent player in the Canadian dairy sector, announced its foray into the frozen yogurt arena. This move comes via a licensing agreement with Nestlé Canada. Through this partnership, Lactalis Canada is rolling out an array of innovative frozen yogurt offerings. These will be marketed under its well-known iÖGO brand and will include eight distinct SKUs: four flavorful bars and four creamy tubs. Furthermore, the collaboration unveils three invigorating pops under the iÖGO nanö brand, presenting consumers with a delightful assortment of frozen treats.

Technology is playing an increasingly important role in shaping the competitive landscape. Innovations such as automated vending machines and digital engagement platforms are helping companies differentiate themselves. Yogurtland’s three consecutive years of growth, driven by its digital initiatives, highlight the value of adopting technology to enhance customer experience and streamline operations. Additionally, regulatory changes are influencing market dynamics. Companies are reformulating their products to comply with government sugar-reduction policies and to align with the evolving definition of "healthy" in food labeling.

Frozen Yogurt Industry Leaders

-

General Mills Inc.

-

Danone S.A.

-

Unilever PLC

-

Nestle S.A

-

Dairy Farmers of America Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Lactalis Canada entered the frozen yogurt segment through a licensing agreement with Nestlé Canada. The company introduced eight iÖGO-branded frozen yogurt products, consisting of four bars and four tubs, alongside three iÖGO nanö frozen yogurt pops.

- April 2025: MyFroyoland established its ninth retail location in Jogeshwari East, Mumbai, expanding its frozen yogurt operations. The company currently maintains more than 40 retail establishments across India, indicating its market penetration in the frozen dessert segment.

- April 2025: 16 Handles launched its Dubai Chocolate frozen yogurt flavor, tapping into the viral dessert trend inspired by the luxurious chocolate bar filled with crispy knafeh and rich pistachio. According to the brand, the frozen yogurt features a creamy pistachio-rich base blended with crushed milk chocolate bites and a hint of cocoa, recreating the original’s balance of crunch and smoothness, with optional toppings for added texture.

- April 2024: Yasso introduced three new fruit-based products to its frozen Greek yogurt bar product line: Strawberry Chocolate Crunch, Strawberries and Cream, and Creamy Mango. The products incorporate Greek yogurt with fruit ingredients, delivering a nutritional profile of 80-140 calories and 4 grams of protein per serving.

Global Frozen Yogurt Market Report Scope

Frozen yogurt is a frozen dessert made with yogurt and sometimes with other dairy and non-dairy products.

The global frozen yogurt market is segmented by type, flavor, distribution channel, packaging type, and geography. By type, the market is segmented into dairy-based and non-dairy-based frozen yogurt. The non-dairy-based frozen yogurt is further sub-segmented into soy, almond, coconut, oat, and others. By flavor, the market is segmented into plain and flavored. Based on distribution channels, the market is segmented into off-trade and on-trade channels. The off-trade channel is further sub-segmented into supermarkets/hypermarkets, convenience stores, online retailers, and others. By packaging type, the market is segmented into cups and tubs, cones and sticks, and others. Based on geography, the market is segmented into North America, Europe, Asia-Pacific, South America, the Middle East, and Africa. The market sizing has been done in value terms in USD for all the abovementioned segments.

By Type

| Dairy-Based | |

| Non-Dairy/Plant-Based | Soy |

| Almond | |

| Coconut | |

| Oat | |

| Others |

By Flavor

| Plain |

| Flavored |

By Distribution Channel

| Off-Trade | Supermarkets and Hypermarkets |

| Convenience Stores | |

| Online Retail | |

| Other Distribution Channels | |

| On-Trade |

By Packaging Type

| Cups and Tubs |

| Cones and Sticks |

| Others |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Type | Dairy-Based | |

| Non-Dairy/Plant-Based | Soy | |

| Almond | ||

| Coconut | ||

| Oat | ||

| Others | ||

| By Flavor | Plain | |

| Flavored | ||

| By Distribution Channel | Off-Trade | Supermarkets and Hypermarkets |

| Convenience Stores | ||

| Online Retail | ||

| Other Distribution Channels | ||

| On-Trade | ||

| By Packaging Type | Cups and Tubs | |

| Cones and Sticks | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the frozen yogurt market?

The frozen yogurt market size stands at USD 6.49 billion in 2026 and is forecast to reach USD 8.69 billion by 2031.

Which region is growing the fastest?

Asia-Pacific exhibits the highest growth, projected at a 10.52% CAGR between 2026 and 2031.

How important are plant-based frozen yogurts to future growth?

Plant-based alternatives represent 18.45% of sales today but are expanding at an 11.07% CAGR, making them the category’s most dynamic sub-segment.

Which distribution channel is seeing the quickest expansion?

On-trade venues—self-serve parlors, cafés and automated kiosks—are expected to grow at a 12.86% CAGR through 2031, outpacing off-trade retail.

Page last updated on: