Online Action Games Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

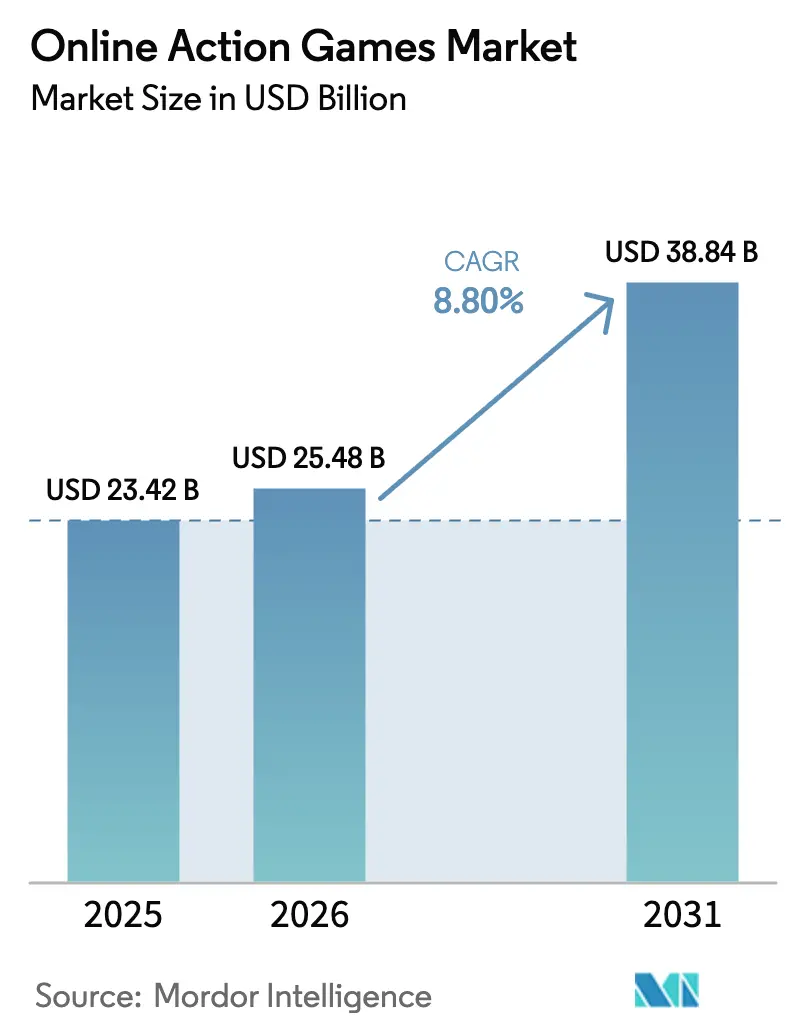

| Market Size (2026) | USD 25.48 Billion |

| Market Size (2031) | USD 38.84 Billion |

| Growth Rate (2026 - 2031) | 8.80% CAGR |

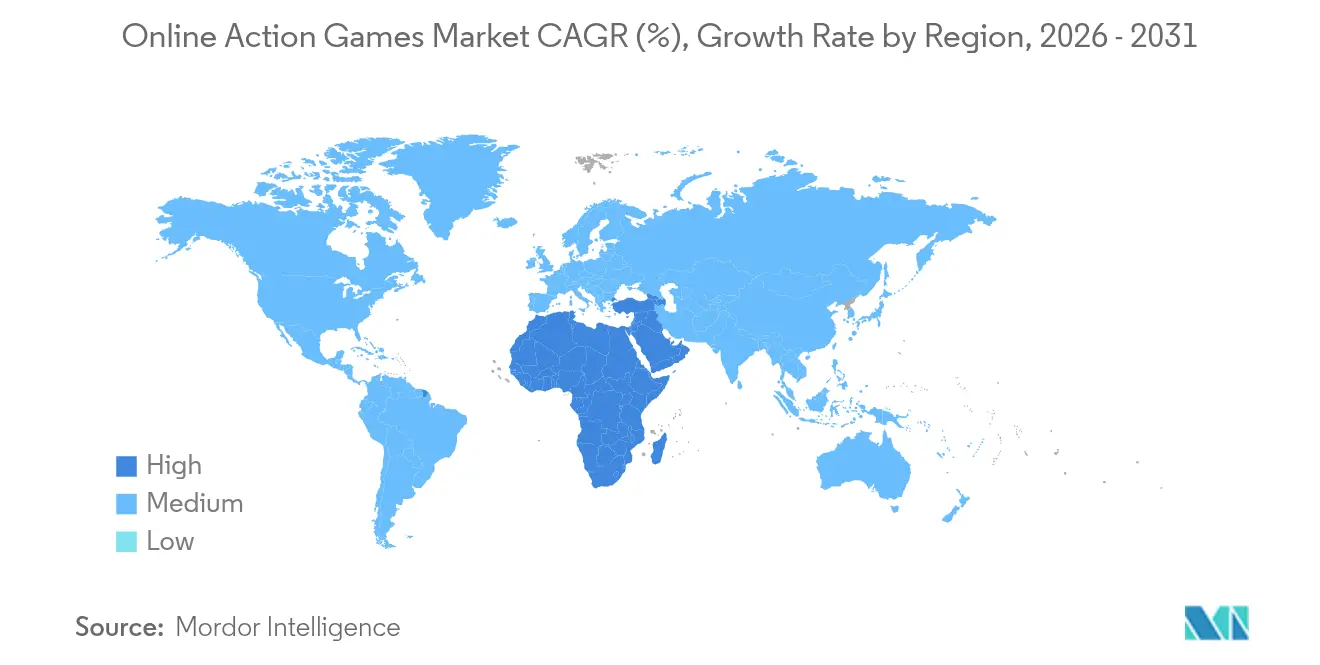

| Fastest Growing Market | Middle East |

| Largest Market | Asia |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Online Action Games Market Analysis by Mordor Intelligence

Online Action Games Market size in 2026 is estimated at USD 25.48 billion, growing from 2025 value of USD 23.42 billion with 2031 projections showing USD 38.84 billion, growing at 8.80% CAGR over 2026-2031.

The Online Action Games Market size is estimated at USD 23.42 billion in 2025, and is expected to reach USD 38.60 billion by 2030, at a CAGR of 8.95% during the forecast period (2025-2030). Uptake of 5G handsets in Asia-Pacific (APAC) and the Middle East and North Africa (MENA) is lowering median multiplayer latency below 40 ms, driving longer play sessions and higher conversion to in-game purchases.[1]Ericsson, “Elevating 5G with differentiated connectivity,” ericsson.com Cross-platform engines such as Unreal and Unity are compressing porting schedules, enabling publishers to ship day-one builds for console, PC, and mobile with a single art pipeline.[2]Epic Games, “Building Multi-Platform Games in Unreal Engine,” unrealengine.com Cloud-streaming alliances with telcos and smart-TV makers are widening access in bandwidth-constrained markets, a shift that is already visible in Brazil, India, and Nigeria.[3]Xbox Wire, “Xbox Gaming Coming to Amazon Fire TV: Play More Games, No Console Needed,” news.xbox.com Meanwhile, escalating esports prize pools in the shooter sub-genre are amplifying spectator interest and funneling fresh advertising spend into first-person and hero-shooter ecosystems. On the monetization front, generative-AI-powered operations are supporting tailored events and dynamic storefronts, lifting average revenue per user (ARPU) in tier-1 markets

Key Report Takeaways

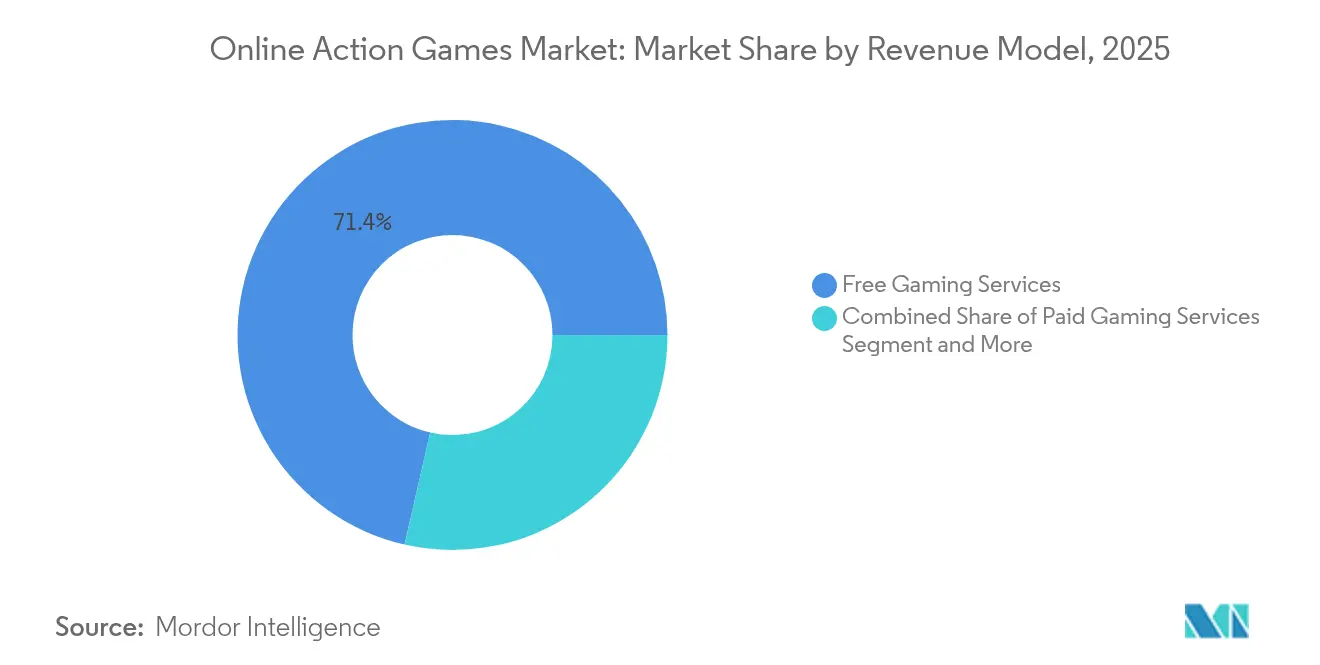

- By revenue model, free gaming services led with 71.42% share in 2025; subscription-based gaming services show the highest projected CAGR at 12.35% through 2031.

- By platform, mobile phones commanded 55.23% of 2025 revenue; cloud gaming platforms are forecast to expand at an 17.62% CAGR to 2031.

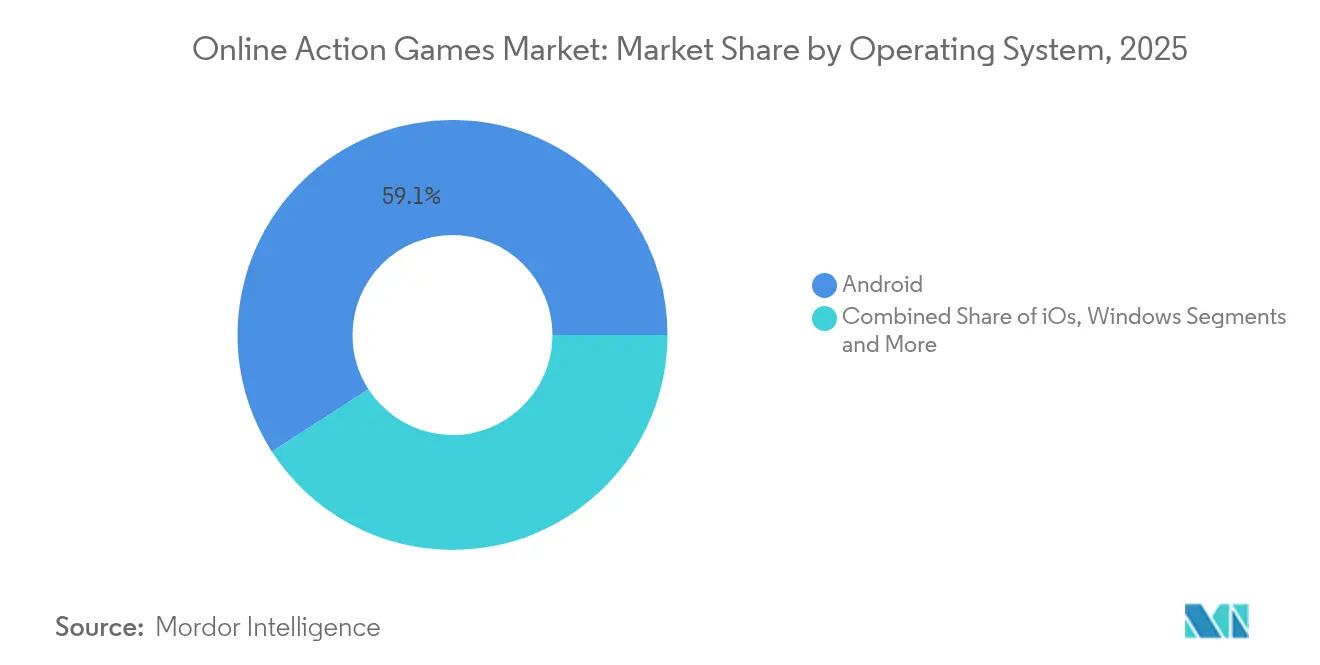

- By operating system, Android captured 59.12% share in 2025 while iOS is poised for the fastest 2026-2031 growth at 9.88% CAGR.

- By geography, Asia-Pacific generated 51.35% of 2025 sales; the Middle East and Africa is projected to grow the quickest at a 13.58% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Online Action Games Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| 5G-enabled low-latency mobile play | +1.10% | APAC, MENA | Medium term (2-4 years) |

| Cross-platform engines reducing porting costs | +0.80% | Global | Short term (≤ 2 years) |

| Cloud-streaming partnerships in emerging markets | +0.90% | Latin America, Africa | Medium term (2-4 years) |

| Esports prize-pool escalation in shooter titles | +0.60% | North America, Europe, Korea | Long term (≥ 4 years) |

| GenAI-driven live-ops personalization boosting ARPU | +0.70% | North America, Europe, Japan | Short term (≤ 2 years) |

| European tax incentives stimulating AAA pipelines | +0.40% | France, United Kingdom, Italy, Spain | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

5G-Enabled Low-Latency Mobile Action Gaming Adoption across APAC and MENA

Commercial 5G rollouts across India, Saudi Arabia and the United Arab Emirates have slashed median round-trip latency for multiplayer titles, enabling real-time hit detection and smoother competitive play. Network-slicing pilots in Riyadh and Mumbai allocate assured throughput tiers for game packets, translating into 20% higher session lengths compared with 4G cohorts. Publishers are responding by staging timed live-ops events optimized for sub-50 ms latency, accelerating regional revenue pick-up.

Cross-Platform Game Engines Reducing Porting Costs

Unreal Engine and Unity now ship multi-target build tools that reuse shaders and asset bundles across PC, console and mobile SKUs, trimming porting cycles by up to 30 days per platform. Independent studios can therefore reach addressable install bases exceeding 2 billion devices while maintaining a single QA pipeline. The move also improves time-to-market for downloadable content, reinforcing player retention.

Cloud-Streaming Partnerships Expanding Access in Emerging Markets

Microsoft’s Boosteroid and Amazon Fire TV tie-ups provide console-grade action titles on sub-USD 50 streaming sticks, eliminating hardware barriers in mass-market households. Telcos bundle zero-rated data tiers with premium game passes, converting prepaid subscribers who exhibit low willingness to pay for consoles. The model broadens funnel reach for AAA shooters and brawlers in Brazil, South Africa and Indonesia.

Esports Prize-Pool Escalation in Shooter Sub-genre

The 2024 VALORANT Champions purse of USD 2.25 million outranked 2023’s pot by 29%, catalyzing record peak concurrent viewership of 1.3 million across Twitch and Huya. Higher visibility translates into brand-sponsored in-game cosmetic bundles and battle-pass uplifts, channeling incremental funding back to tournament circuits and sustaining a virtuous monetization loop.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Post-ATT mobile user-acquisition cost spike | −0.7% | North America, Europe | Short term (≤ 2 years) |

| Violence-content regulations in China and South Korea | −0.6% | East Asia | Medium term (2-4 years) |

| High real-time multiplayer infrastructure costs for indies | −0.5% | Global | Short term (≤ 2 years) |

| Escalating cybersecurity threats in competitive play | −0.4% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising User-Acquisition Costs post-ATT on Mobile Ad Networks

Apple’s App Tracking Transparency (ATT) framework has suppressed ID-level targeting, inflating average CPI (cost per install) for action genres by 25% year on year. Publishers divert spend toward influencer-led discovery channels, but conversion efficiency remains below pre-ATT baselines, compressing margins on free-to-play launches.

Violence-Related Content Regulations in China and South Korea

Stringent content grading standards in China’s National Press and Publication Administration and South Korea’s Game Rating and Administration Committee impose capricious approval timelines for blood and gunfire depictions. Studios often reshoot entire cinematics or recolor particle effects, inflating localization budgets and delaying monetization windows in two of the world’s most lucrative markets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Revenue Model: Subscription momentum complements dominant free-to-play economics

Subscription offerings contribute 13.25% of 2025 spend, yet their growth trajectory at 12.35% CAGR exceeds that of ad-funded free services. Competitive publishers differentiate by bundling a rotating catalog of premium shooters, early access to DLC and platform-agnostic cloud saves. In turn, the online action games market size for subscription tiers is projected to reach USD 6.23 billion by 2031, capturing players averse to micro-transactions.

Diversified hybrids such as battle-pass models combine predictable recurring revenue with aspirational cosmetic unlocks. Premium passes priced at USD 9.99 per season achieve an attach rate above 35% in tier-1 countries, feeding into higher monthly active user retention. Conversely, advertising-supported experiences remain critical for emerging markets where average spend per paying user trails the global mean by over 45%.

By Platform: Mobile leads, cloud accelerates

Mobile phones held 55.23% revenue share in 2025, anchored by extensive Android device penetration in India, Indonesia and Nigeria. Edge-rendering and low-memory texture packs now secure console-like fidelity on mid-tier SOCs, narrowing the experiential gap with dedicated hardware. Cloud gaming platforms, although only 5.6% of revenue in 2025, enjoy the fastest climb at an 17.62% CAGR, aided by bundled 5G fixed-wireless plans. The online action games market share for cloud services could breach 11.75% by 2031 if 5G SA networks achieve 65% nationwide coverage across APAC.

Interoperability gains traction as Xbox Cloud Gaming broadens to Amazon Fire TV, and Boosteroid introduces day-one AAA releases. This mitigates hardware cycle risk for publishers and enables asset amortization across a larger paying audience. Parallel improvements in Wi-Fi 6E routers further reduce input lag, strengthening living-room cloud adoption.

By Operating System: Android breadth confronts iOS monetization edge

Android captured 59.12% of gross spending as of 2025, largely due to handset affordability in Asia and Africa. Yet iOS devices deliver lifetime value per payer that is 1.7 times higher, influenced by higher disposable income segments in North America and Western Europe. Cross-save ecosystems encourage dual-device play, with one-third of Korean shooter users alternating between iPhone and Windows PC during a single 24-hour period.

Platform holders intensify efforts to keep developers loyal: Apple elevates Metal performance layers for Unreal Engine, while Google Play Games for PC exits beta with full keyboard and mouse remapping. Such moves narrow feature disparities and incentivize simultaneous update cadences across operating systems.

Geography Analysis

Asia-Pacific generated 51.35% of global revenue in 2025, underpinned by mobile-first markets such as China, South Korea and India. Government-led fiber-to-home investment in South Korea pushes average downstream speeds beyond 200 Mbps, sustaining 240 Hz shooters and 4K streaming campaigns. However, the introduction of play-time caps in China tempers under-18 monetization velocity, shifting publisher focus toward adult whales and cross-border Southeast Asian growth.

North America follows as the second-largest territory, benefitting from console install-base density and robust esports infrastructure. Franchise tie-ins with Hollywood IP accelerate brand recognition, while league-based monetization—echoing traditional sports media rights—strengthens recurring revenue streams. Yet rising labor costs in California and Texas AAA studios encourage outsourcing to Montreal, Vancouver and Guadalajara to preserve project margins.

Europe’s regulatory climate remains fragmented; tax incentives in France, the United Kingdom and Italy underpin the resurgence of AAA single-player action titles, enriching the wider ecosystem through asset reuse in multiplayer expansions. Eastern Europe, spearheaded by Poland and Romania, emerges as a cost-competitive hub for Unreal Engine programmers, attracting outsourcing contracts from Western publishers seeking to expedite concurrent PC-console releases.

Competitive Landscape

The market features a blend of platform holders and content specialists. Tencent, Sony Interactive Entertainment (SIE) and Activision Blizzard jointly accounted for an estimated top-five combined share of around 45% in 2024. Tencent leverages its multi-tenant cloud infrastructure to run battle-royale instances hosting 120-player lobbies, enhancing retention rates among Gen Z users. SIE’s minority stake in African publisher Carry1st signals a sustained effort to seed PlayStation Network presence across sub-Saharan Africa.

Activision Blizzard continues to refine seasonal cadence for its flagship first-person shooter, integrating AI-assisted anti-cheat modules to curb competitive integrity threats. Ubisoft doubles down on its proprietary Anvil engine for open-world brawlers, while simultaneously trialing Unreal Engine 5 for vertical-slice prototypes to fast-track next-gen console scalability. Independent darlings such as FromSoftware and PlatinumGames cultivate niche yet loyal fan bases via distinctive combat mechanics and punishing difficulty loops.

Consolidation remains a salient feature: Embracer Group’s divestitures open acquisition windows for cash-rich platform holders pursuing exclusive cloud-streaming rights. Meanwhile, NetEase and NEXON scale Western satellite studios to secure fresh IP that resonates beyond their domestic markets.

Online Action Games Industry Leaders

Tencent

Sony Interactive Entertainment

Konami

Capcom

Ubisoft

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Scopely acquired Niantic's games business for USD 3.5 billion, significantly expanding its portfolio in the location-based gaming segment

- April 2025: Vector Solutions acquired ArdentSky, enhancing compliance solutions for the rapidly growing gaming industry

- April 2025: The Esports World Cup announced a record-breaking USD 70 million prize pool, setting a new benchmark for competitive gaming

- March 2025: Xsolla launched updated Cloud Gaming solutions, expanding developer access to players through cloud technology valued at USD 6.91 billion in 2024

Global Online Action Games Market Report Scope

An online action game refers to a video game genre that strongly emphasizes physical challenges, including hand-eye coordination and reaction time, primarily played through the Internet or other computer networks. The genre includes a large variety of sub-genres, such as fighting games, beat them ups, shooter games, and platform games. Some real-time strategy games and multiplayer online battle arenas are also considered action games.

The online action games market is segmented by revenue model (free gaming services, paid gaming services), by platform (PCs, consoles, mobile phones), by operating system (iOS, Android, Windows, other operating systems), and by geography.

| Free Gaming Services |

| Paid Gaming Services |

| Subscription-Based Gaming Services |

| Hybrid Battle-Pass Models |

| In-Game Advertising-Supported Free Services |

| PCs |

| Consoles |

| Mobile Phones |

| Cloud Gaming Platforms |

| XR/VR Devices |

| iOS |

| Android |

| Windows |

| Other Operating Systems (macOS, Linux, ChromeOS) |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of SouthAmerica | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| India | |

| Australia | |

| New Zealand | |

| Rest of Asia-Pacific | |

| Middle East and | United Arab Emirates |

| Saudi Arabia | |

| Rest of Middle East | |

| Africa | South Africa |

| Rest of Africa |

| By Revenue Model | Free Gaming Services | |

| Paid Gaming Services | ||

| Subscription-Based Gaming Services | ||

| Hybrid Battle-Pass Models | ||

| In-Game Advertising-Supported Free Services | ||

| By Platform | PCs | |

| Consoles | ||

| Mobile Phones | ||

| Cloud Gaming Platforms | ||

| XR/VR Devices | ||

| By Operating System | iOS | |

| Android | ||

| Windows | ||

| Other Operating Systems (macOS, Linux, ChromeOS) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of SouthAmerica | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Australia | ||

| New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and | United Arab Emirates | |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current size of the online action games market?

The online action games market stood at USD 25.48 billion in 2026 and is forecast to reach USD 38.84 billion by 2031.

Which platform contributes most to online action game revenue?

Mobile phones lead with 55.23% of 2025 revenue, thanks to widespread Android handset adoption in Asia and Africa.

How fast is cloud gaming growing within the online action games market?

Cloud gaming platforms are expanding at an 17.62% CAGR from 2026 to 2031, the fastest among all delivery platforms.

Why is 5G important for online action games?

5G reduces multiplayer latency below 40 ms, enabling smoother competitive play and encouraging longer in-game sessions, particularly in APAC and MENA.

Which revenue model is accelerating the quickest?

Subscription-based gaming services are projected to grow at a 12.35% CAGR through 2031, as bundled catalogs and cross-save features gain traction.

What are the main restraints on market growth?

Higher user-acquisition costs after Apple’s privacy changes and content restrictions in China and South Korea weigh on short-term revenue expansion.

Page last updated on: