Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 20.59 Billion |

| Market Size (2031) | USD 44.58 Billion |

| Growth Rate (2026 - 2031) | 16.71% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

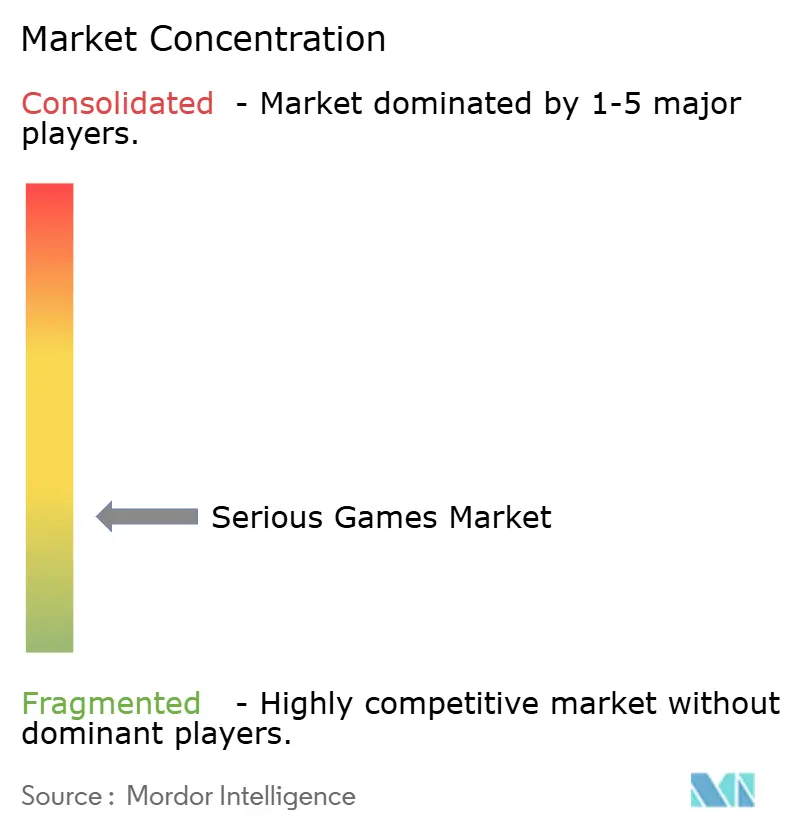

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Serious Games Market Analysis by Mordor Intelligence

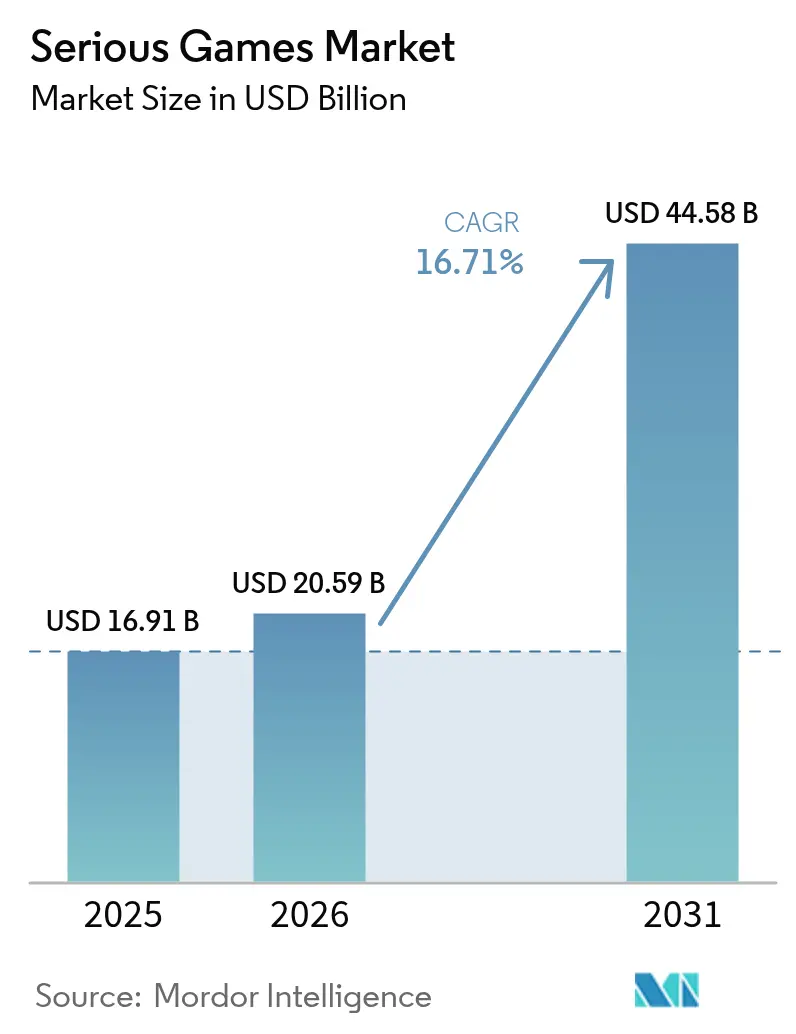

The serious games market size was valued at USD 16.91 billion in 2025 and estimated to grow from USD 20.59 billion in 2026 to reach USD 44.58 billion by 2031, at a CAGR of 16.7% during the forecast period (2026-2031). Demand is pivoting from passive slide-based instruction toward immersive, simulation-led experiences that compress training cycles, improve knowledge retention, and deliver quantifiable performance data. Corporate compliance mandates, defense readiness programs, and K-12 engagement concerns are converging to accelerate enterprise and public-sector spending. Mobile ubiquity, mainstream virtual reality (VR) hardware, and the rollout of 5G edge infrastructure make always-on, low-latency distribution commercially viable. Meanwhile, open-source engines reduce development barriers, although the absence of standardized outcome metrics and tightening data-privacy rules continue to temper growth momentum.

Key Report Takeaways

- By application, Simulation Training led with 37.54% revenue share in 2025, while Learning and Education is projected to advance at a 17.44% CAGR to 2031.

- By platform, Mobile and Tablet devices held 43.12% of 2025 revenue, whereas Cloud Gaming Platforms are forecast to climb at a 17.87% CAGR through 2031.

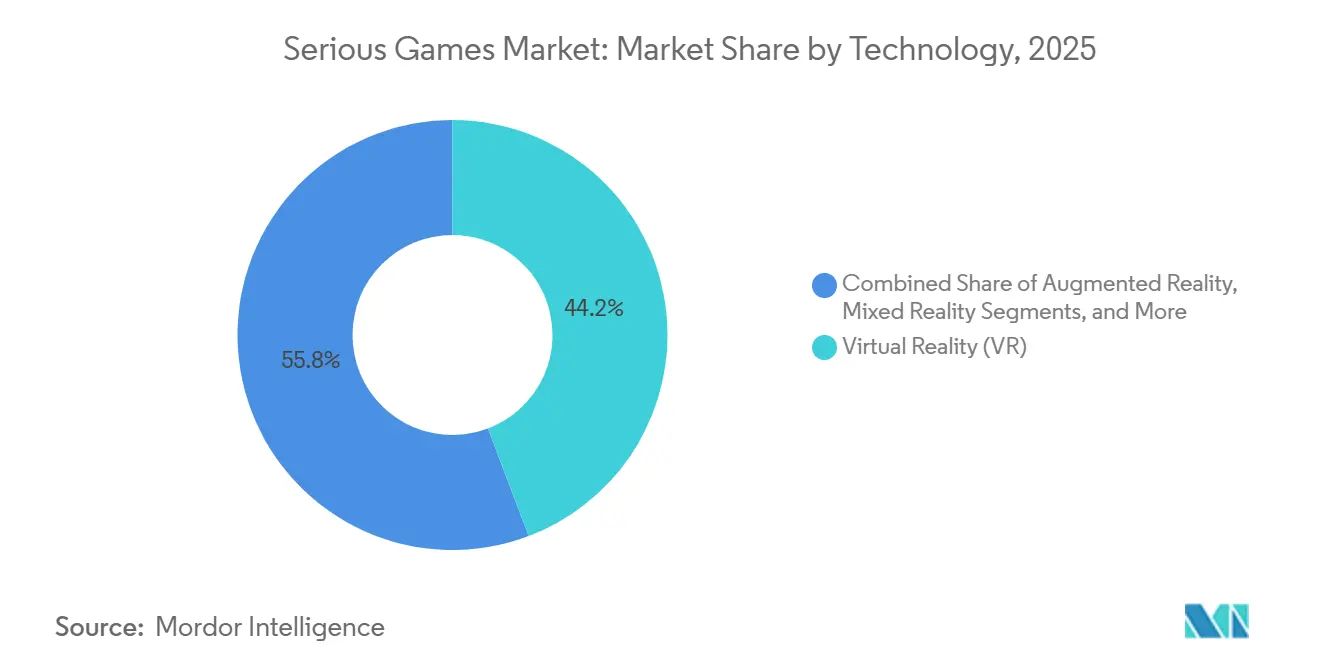

- By technology, VR accounted for 44.23% share in 2025 and Mixed Reality is poised for the fastest 17.83% CAGR to 2031.

- By end-user industry, Healthcare commanded 33.54% of 2025 revenue and Automotive is on track for an 18.07% CAGR through 2031.

- By geography, North America captured 34.92% share in 2025, while Asia-Pacific is predicted to register a 17.68% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Serious Games Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Widespread Adoption of Mobile-Based Micro-Learning Platforms | +3.2% | Global, strongest in North America and Asia-Pacific | Short term (≤ 2 years) |

| Corporate Demand for Simulation-Based Compliance Training | +3.5% | Global, led by North America and Europe | Short term (≤ 2 years) |

| Mainstream VR Headset Price Declines Fueling Classroom Deployments | +2.8% | North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| AI-Driven Adaptive Storylines Elevating Learner Retention | +2.9% | Global, early adoption in North America and Asia-Pacific | Medium term (2-4 years) |

| Government Incentives for Defense Readiness e-Exercises | +2.1% | North America, Europe, Middle East | Long term (≥ 4 years) |

| Open-Source Game Engines Lowering Entry Barriers for SMEs | +2.0% | Global, notable in Asia-Pacific and South America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Widespread Adoption of Mobile-Based Micro-Learning Platforms

Enterprise uptake of bite-sized mobile lessons reached 67% of organizations in 2025, driven by distributed workforces that prefer three-to-seven-minute scenarios over hour-long classes. Completion rates exceed 90% because sessions align with commute windows and break periods. High-churn sectors such as retail and hospitality gain particular value, trimming time-to-competency by nearly 40% as new hires play compliance, product, and service simulations on personal devices. Cloud dashboards let managers track progress in real time, and 5G coverage in dense Asia-Pacific metros now permits latency-free multiplayer drills that were once impossible. These factors collectively reinforce mobile’s position as the everyday channel for professional upskilling.[1]GSMA Intelligence, “The Mobile Economy 2025,” gsma.com

Corporate Demand for Simulation-Based Compliance Training

Escalating penalties—average OSHA fines topped USD 15,625 per serious violation in 2025 while GDPR levies reached EUR 4.5 billion (USD 4.9 billion)—are pushing firms to replace checkbox e-learning with interactive scenarios,[2]U.S. Occupational Safety and Health Administration, “Penalty Adjustments for Inflation,” osha.gov . Employees tackle virtual chemical spills, phishing threats, or harassment cases and witness immediate in-game consequences, cutting incident rates by up to 50%. Certification bodies in aviation, oil and gas, and healthcare now embed minimum simulation hours into license renewals, turning serious games into recurring budget lines rather than one-off pilots. Vendors respond by offering analytics suites that map player actions to policy clauses, enabling auditors to verify mastery with digital trails.

Mainstream VR Headset Price Declines Fueling Classroom Deployments

The USD 299 launch price of the Meta Quest 3S lowered hardware entry costs to public-school-friendly territory, resulting in more than 1,200 U.S. districts integrating VR by mid-2025. Untethered designs eliminate the need for gaming PCs, simplifying device management for thin IT teams. Although Meta signaled 2026 price increases, device-as-a-service bundles that roll hardware, content, and support into monthly fees are cushioning budget pressure. Competitive entries from Pico and Sony preserve alternatives, and bulk-purchase consortia let districts negotiate warranties and sanitize-kit add-ons. As library ecosystems mature, teachers increasingly swap static videos for immersive field trips, lab safety drills, and history reenactments, thereby boosting student engagement metrics without extra classroom hours.

AI-Driven Adaptive Storylines Elevating Learner Retention

Generative AI tools now cut branching-narrative design time by as much as 70%, spawning situational variants that respond to user choices and biometric cues. Adaptive difficulty curves maintain flow states, doubling engagement duration relative to linear modules. In healthcare, AI tutors monitor hand-controller tremors and gaze to determine if a medical intern requires extra scaffolding, then inject micro-lessons on anatomy or instrument orientation.[3]U.S. Food and Drug Administration, “FDA Clears VR Surgical Training Platforms,” fda.gov In data-science drills, algorithms diagnose conceptual gaps—such as misunderstanding correlation vs. causation—and pivot learners to targeted remediation. Oversight processes mandate human review of AI-authored scripts to avoid factual drift, but early pilots show assessment accuracy gains of 15-20% when adaptive engines rank skill proficiency.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited Pedagogical Standards for Outcome Measurement | -1.8% | Global, acute in Europe and North America | Medium term (2-4 years) |

| High Up-Front Development Costs for Custom 3D Assets | -2.3% | Global, heavier burden on SMEs in emerging markets | Short term (≤ 2 years) |

| Data-Privacy Concerns Around Biometric Feedback Loops | -1.2% | Europe, North America, rising scrutiny in Asia-Pacific | Long term (≥ 4 years) |

| Scarcity of Qualified Serious-Game Instructional Designers | -1.5% | Global, most severe in North America and Europe | Medium term (2-4 years |

| Source: Mordor Intelligence | |||

High Up-Front Development Costs for Custom 3D Assets

Realistic character models range from USD 1,800 to USD 30,000 apiece, while complex industrial scenes exceed USD 24,000, making asset creation the largest fixed cost for new entrants. A single simulation can demand 500-2,000 artist hours, and hourly rates near USD 150 in the United States squeeze small studios. Although AI texture pipelines and asset-marketplace reuse ease some pain, safety-critical verticals still require bespoke geometry with verified anatomical or mechanical accuracy. Investors hesitate to back studios lacking repeatable asset pipelines, subjecting founders to high bootstrapping risk. Consequently, many SMEs cap scope or resort to low-poly aesthetics that limit realism and narrow addressable sectors.

Limited Pedagogical Standards for Outcome Measurement

Fewer than 30% of commercial titles implement standardized xAPI statements or competency models, hindering cross-vendor efficacy comparisons,. Procurement teams often run 6-12-month pilots to secure board approval, elongating sales cycles and elevating customer-acquisition costs. Higher-education accreditors and medical boards question whether in-game assessments satisfy high-stakes test validity, impeding adoption in regulated programs. The shortage of long-term studies linking gameplay metrics to workplace KPIs leaves ROI narratives anecdotal. Until third-party benchmarking consortia establish reference datasets, vendors risk competing on graphics and gimmicks rather than demonstrable learning impact.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Compliance Pressures Sustain Simulation Leadership

Simulation Training represented 37.54% of 2025 revenue, confirming that regulated industries such as aviation, nuclear energy, and surgery rely on practice-or-perish frameworks. That share translates to a serious games market size advantage C-suite buyers rarely overlook. Recertification rules, coupled with insurance discounts for validated drills, institutionalize annual or quarterly refresh cycles. In contrast, Learning and Education is forecast to expand at a 17.44% CAGR to 2031 as districts combat 26% chronic absenteeism among U.S. students. Gamified math and history modules show double-digit boosts in test-score growth, convincing administrators to shift textbook funds into interactive content.

Advertising and Marketing titles turn entertainment loops into brand-awareness drivers, offering 2× dwell time and 70% higher recall than banner ads, yet they still represent a niche relative to mission-critical simulations. Recruitment assessments and therapeutic interventions, grouped under Other Applications, are quietly scaling as employers discover that game-based cognitive tests outperform résumé screens by 30% on job-performance predictability. Over the horizon, convergent lifelong-learning platforms may blur lines between compliance rehearsal and academic curricula, but near-term spending will continue to skew toward simulation’s proven liability-mitigation value.

By Platform: Mobile Convenience Meets Cloud Reach

Mobile and Tablet devices secured 43.12% of 2025 revenue, thanks to a world-wide installed base topping 6 billion smartphones. Employees train during commutes, and managers push bite-sized updates on regulation changes without reserving classroom slots. This ubiquity keeps the serious games market share for handheld form factors well ahead of stationary options. Cloud Gaming Platforms, however, are projected to climb at a 17.87% CAGR, streaming GPU-intensive physics models to under-powered devices with sub-20 millisecond latency. Firms eliminate hardware refresh cycles, and content updates propagate instantly, reducing IT overhead.

PC and Laptop setups remain irreplaceable for high-precision tasks, such as laparoscopy rehearsals that require low-latency haptic peripherals. Game Consoles are carving space in consumer upskilling, where individuals buy language-learning or financial-literacy titles directly. VR headsets supply immersion for confined-space rescue drills, while augmented-reality wearables broaden the field workforce’s ability to overlay schematics onto machinery. In remote oil platforms or rural clinics, offline-first designs still matter, showing that distribution models will coexist rather than converge entirely.

By Technology: VR Dominance Faces MR Growth Surge

VR delivered 44.23% of 2025 revenue, benefiting from mature authoring workflows and enterprise support partners that cut rollout time from quarters to weeks. Such traction secures a prominent serious games market presence despite motion-sickness concerns. Mixed Reality should outpace at a 17.83% CAGR to 2031 as industrial users exploit digital overlays to cut error rates by 40% on electrical panels and conveyor belts. Smartphone-anchored augmented-reality apps remain marketing-centric owing to limited spatial anchoring.

AI-infused engines inject procedural variation and conversational agents, reducing content-production cycles and enabling adaptive feedback loops. Meanwhile, 3D Graphics Engine-based games, chiefly on Unity and Unreal, dominate cross-platform codebases, ensuring backward compatibility amid rapid hardware churn. HTML5 and text-only simulations keep a foothold where bandwidth is scarce or compliance requires air-gapped execution, preserving low-fidelity but high-accessibility options across emerging economies.

By End User Industry: Healthcare Precision Versus Automotive Urgency

Healthcare’s 33.54% share in 2025 stems from FDA-cleared surgical rehearsal suites that shorten operating time by 20% and halve complication rates. That entrenched base guarantees a sizeable slice of the serious games market size for the foreseeable future. Hospitals now integrate VR into resident rotations, and payers reimburse for simulation hours that demonstrably lower malpractice claims. Automotive, forecast for an 18.07% CAGR, faces an electric-vehicle technician shortage expected to hit 75,000 by 2030; OEMs therefore fund hazard-free battery-disassembly modules to protect trainees from 800-volt packs.

Education institutions embed game-based progressions into STEM, recording 15-25% test-score lifts among middle-school cohorts. Retail chains leverage onboarding games to curb employee churn by 30%. Media and Entertainment firms pilot branded quests that translate fandom into e-commerce, while government agencies roll out scenario-based drills for public-health messaging and disaster response. Construction, logistics, and hospitality players—classified under Other End User Industries—adopt VR safety modules to mitigate workplace accidents and insurance premiums, signaling cross-sector momentum.

Geography Analysis

North America retained 34.92% of 2025 revenue, buoyed by USD 136 million in U.S. Army synthetic-training contracts and corporate budgets that average 1.5% of payroll for learning programs. Defense and healthcare customers demand domestic hosting and FedRAMP compliance, raising switching costs. Canadian bilingual mandates foster localized content, and Mexico’s near-shoring wave spurs Spanish-language industrial simulations. Yet vendor focus is shifting to mid-market accounts, where deal sizes are 60% lower but sales cycles close faster, diversifying revenue streams.

Asia-Pacific is set to record a 17.68% CAGR to 2031, propelled by China’s USD 70 billion EdTech spend, India’s National Education Policy 2020 digital-pedagogy targets, and Japan’s Society 5.0 vocational initiatives,. China’s tightened consumer-gaming rules pushed studios into enterprise segments, while India’s offline-first, vernacular design imperatives opened green-field opportunities for mobile-centric deployments. South Korea’s 5G density makes it a proving ground for cloud-delivered multiplayer drills. Australia and New Zealand offset labor shortages with VR upskilling, whereas Southeast Asia’s manufacturing boom drives logistics simulations amid pricing sensitivity and piracy risk.

Europe’s mature automotive, aerospace, and healthcare verticals adopt serious games to satisfy strict worker-safety mandates, even as GDPR Article 9 curtails eye-tracking and heart-rate analytics. Enterprises pay premiums for privacy-by-design software, creating a niche for vendors with certified data-handling pipelines. The Middle East channels smart-city and defense-modernization grants into urban-planning and wargaming platforms. Africa’s nascent uptake features mobile maternal-care simulations in Nigeria and Kenya, though bandwidth gaps impede VR rollouts. South America centers on Brazil and Argentina, where public-school digital-literacy drives and corporate retraining budgets grow despite currency volatility.

Competitive Landscape

The serious games market features high fragmentation; no vendor tops 8% share, and the top five combined hold roughly 28%, fostering a vigorously competitive environment. Infrastructure giants Unity Technologies and Epic Games supply engines that underpin 70% of published titles yet monetize mainly via license royalties, leaving direct customer relationships to content studios. Vertical specialists—such as Immersive VR Education for medical curricula and Triseum for business simulations—differentiate by accreditor alignment and domain authenticity, commanding premium pricing despite limited scale.

Strategic moves cluster around library acquisition, AI toolchain integration, and Asia-Pacific market entry. The USD 56.5 billion leveraged buyout of Electronic Arts in January 2026 underscores institutional confidence in subscription-led, utility-driven gaming trajectories, although the debt load may constrain experimental R&D. Mid-sized studios co-develop with enterprise-software providers, embedding gamified lessons into customer-relationship or enterprise-resource-planning platforms to tap embedded user bases. Open-source engine controversies—like Unity’s transient 2024 per-install fee proposal—have prompted some studios to evaluate in-house engines, but the cost-benefit equation still favors mainstream toolchains for cross-device reach.

Talent scarcity remains a structural bottleneck. Instructional designers who blend pedagogy with narrative and technical fluency command median U.S. salaries above USD 90,000 and positions stay open for up to nine months. Vendors therefore court university partnerships to create certificate pipelines, and some acquire boutique learning agencies outright. Content localization, particularly voice-over and cultural adaptation, grows in strategic importance as Asia-Pacific demand rises, rewarding firms with multi-lingual asset-libraries and on-shore support teams.

Serious Games Industry Leaders

Designing Digitally, Inc.

Diginext (CS Group)

CCS Digital Education Ltd

Applied Research Associate Inc.

Grendel Games BV

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: JetSynthesys acquired EverMerge to extend its casual-gaming catalog into cognitive-training niches aimed at aging populations.

- January 2026: A consortium led by Blackstone and Sixth Street Partners took Electronic Arts private in a USD 56.5 billion leveraged buyout, the largest deal in gaming history.

- January 2026: Atlas V raised USD 6 million Series A funding to scale museum-oriented VR serious-game experiences.

- January 2026: PlayVS acquired Vanta Esports, integrating competitive-gaming infrastructure with STEM curricula in high schools.

Global Serious Games Market Report Scope

Serious games are digital applications primarily prepared for training and education purposes, where the key function is to provide knowledge, training, memorize, inform, and teach the end-users. It is mainly utilized as a tool for knowledge transfer by methods that use gameplay (against self/others) and a penalty/reward system to assess learning in a game-based approach.

The Serious Games Market Report is Segmented by Application (Advertising and Marketing, Simulation Training, Learning and Education, Other Applications), Platform (PC and Laptop, Mobile and Tablet, Game Consoles, VR Head-Mounted Display, Cloud Gaming Platforms, Other Platforms), Technology (Virtual Reality, Augmented Reality, Mixed Reality, Artificial Intelligence Driven Games, 3D Graphics Engine Based Games, Other Technologies), End User Industry (Healthcare, Education, Retail, Media and Entertainment, Automotive, Government, Other End User Industries), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, Africa). The Market Forecasts are Provided in Terms of Value (USD).

By Application

| Advertising and Marketing |

| Simulation Training |

| Learning and Education |

| Other Applications |

By Platform

| PC and Laptop |

| Mobile and Tablet |

| Game Consoles |

| VR Head-Mounted Display |

| Cloud Gaming Platforms |

| Other Platforms |

By Technology

| Virtual Reality (VR) |

| Augmented Reality (AR) |

| Mixed Reality (MR) |

| Artificial Intelligence (AI) Driven Games |

| 3D Graphics Engine Based Games |

| Other Technologies |

By End User Industry

| Healthcare |

| Education |

| Retail |

| Media and Entertainment |

| Automotive |

| Government |

| Other End User Industries |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia and New Zealand | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Kenya | |

| Rest of Africa |

| By Application | Advertising and Marketing | |

| Simulation Training | ||

| Learning and Education | ||

| Other Applications | ||

| By Platform | PC and Laptop | |

| Mobile and Tablet | ||

| Game Consoles | ||

| VR Head-Mounted Display | ||

| Cloud Gaming Platforms | ||

| Other Platforms | ||

| By Technology | Virtual Reality (VR) | |

| Augmented Reality (AR) | ||

| Mixed Reality (MR) | ||

| Artificial Intelligence (AI) Driven Games | ||

| 3D Graphics Engine Based Games | ||

| Other Technologies | ||

| By End User Industry | Healthcare | |

| Education | ||

| Retail | ||

| Media and Entertainment | ||

| Automotive | ||

| Government | ||

| Other End User Industries | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Kenya | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current value of the serious games market?

The serious games market size stood at USD 20.59 billion in 2026 and is projected to nearly double by 2031.

How large will the serious games market be by 2031?

It is projected to reach USD 44.58 billion by 2031, expanding at a 16.7% CAGR from 2026.

Which application currently generates the most revenue?

Simulation Training leads, contributing 37.54% of global revenue in 2025.

Which region is forecast to grow the fastest?

Asia-Pacific is expected to post a 17.68% CAGR between 2026 and 2031 because of major education and industrial digital-learning programs.

What technology segment shows the highest future growth?

Mixed Reality is set to grow the quickest, with a projected 17.83% CAGR through 2031, driven by industrial overlay use cases.

Who are the leading engine providers behind serious games?

Unity Technologies and Epic Games supply engines powering about 70% of released titles, though they hold under 8% direct revenue share individually.

What is the biggest obstacle for smaller studios?

High up-front 3D-asset development costs and the shortage of instructional designers impose significant entry barriers.

Page last updated on: