Online Strategy Games Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

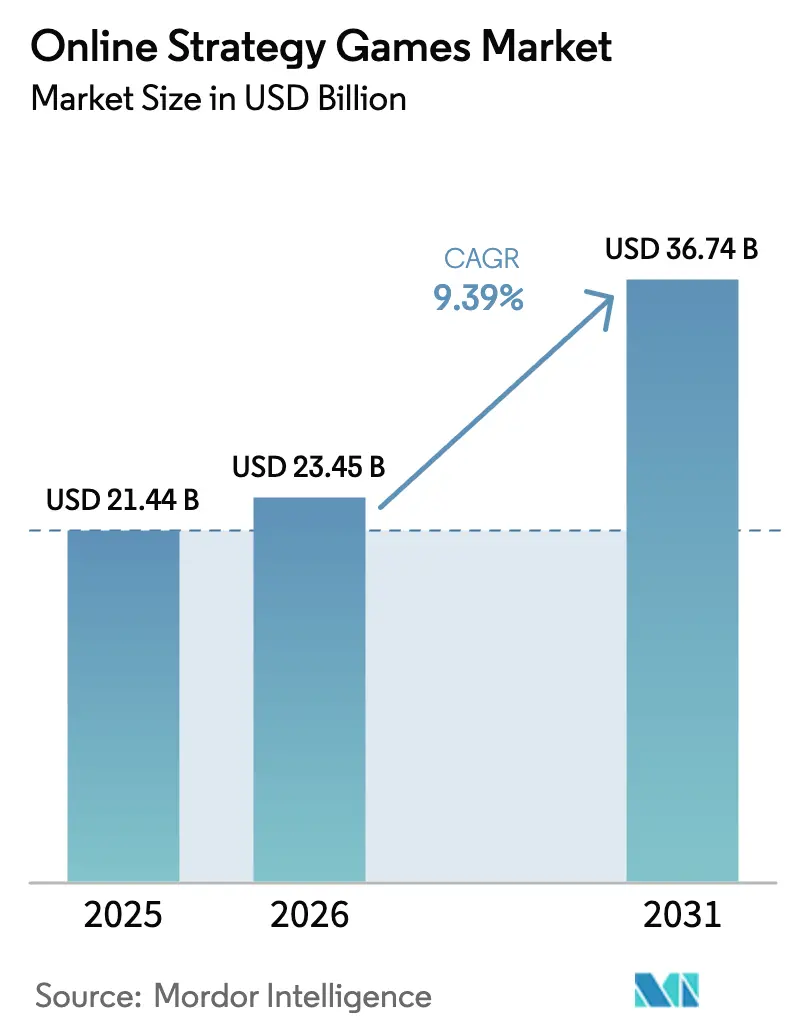

| Market Size (2026) | USD 23.45 Billion |

| Market Size (2031) | USD 36.74 Billion |

| Growth Rate (2026 - 2031) | 9.39% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Online Strategy Games Market Analysis by Mordor Intelligence

The online strategy games market size was valued at USD 21.44 billion in 2025 and estimated to grow from USD 23.45 billion in 2026 to reach USD 36.74 billion by 2031, at a CAGR of 9.39% during the forecast period (2026-2031). This growth reflects the shift from PC-centric releases toward cloud-native, AI-enhanced titles that exploit 5G connectivity, edge computing, and cross-platform engines. Strategic consolidation, exemplified by Microsoft’s USD 69 billion purchase of Activision Blizzard, has reshaped competitive dynamics even as entertainment conglomerates such as Disney inject new capital into game platforms. Cloud distribution lowers upfront infrastructure costs for developers, while 5G rollouts support low-latency real-time strategy play that expands mobile engagement.[1]Huawei Research Dept., “AI in the 5G-A Era: Scenarios, Key Technologies, and Evolution Trends,” Huawei, huawei.com Generative-AI tools reduce content-update costs, supporting faster iteration cycles and personalized experiences that boost retention. These forces collectively position the online strategy games market for sustained, technology-led expansion despite margin pressure from rising user-acquisition costs and platform fees.

Key Report Takeaways

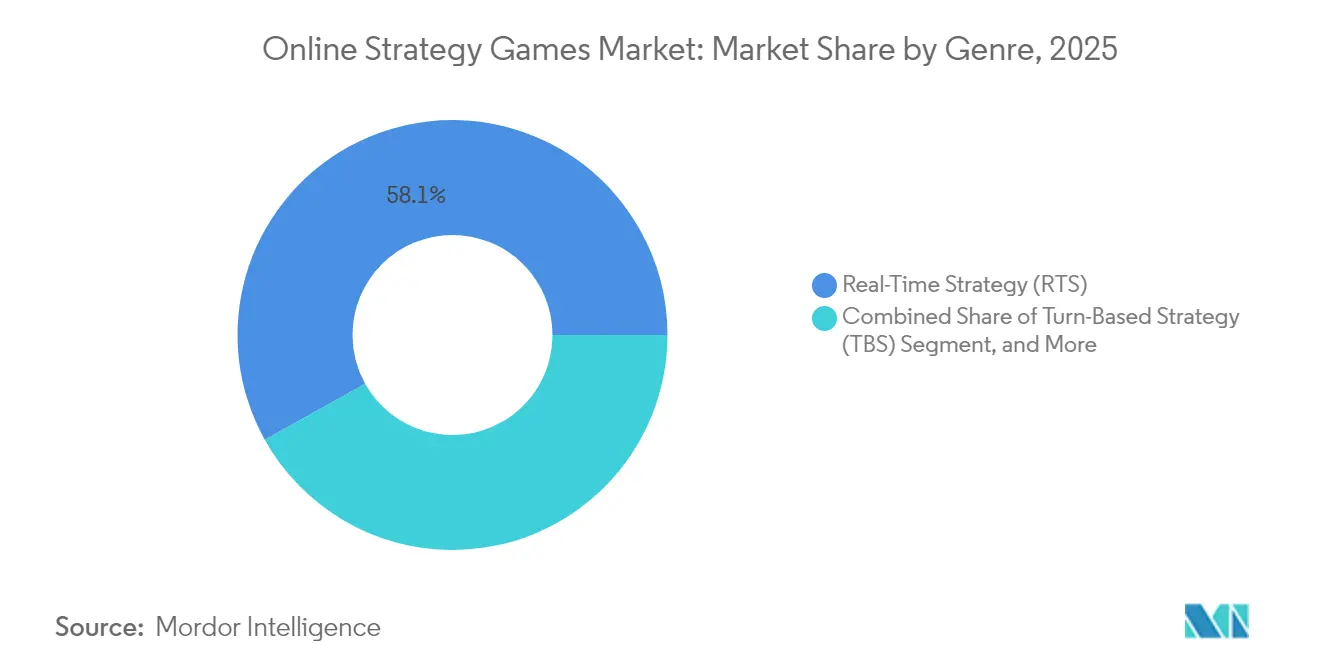

- By genre, real-time strategy led with a 58.10% revenue share in 2025 in the online strategy games market, whereas auto-battler is forecast to compound at 10.36% CAGR through 2031.

- By platform, mobile accounted for 47.10% of the 2025 total in the online strategy games market, while cloud gaming is set to grow fastest at 10.21% CAGR as infrastructure matures.

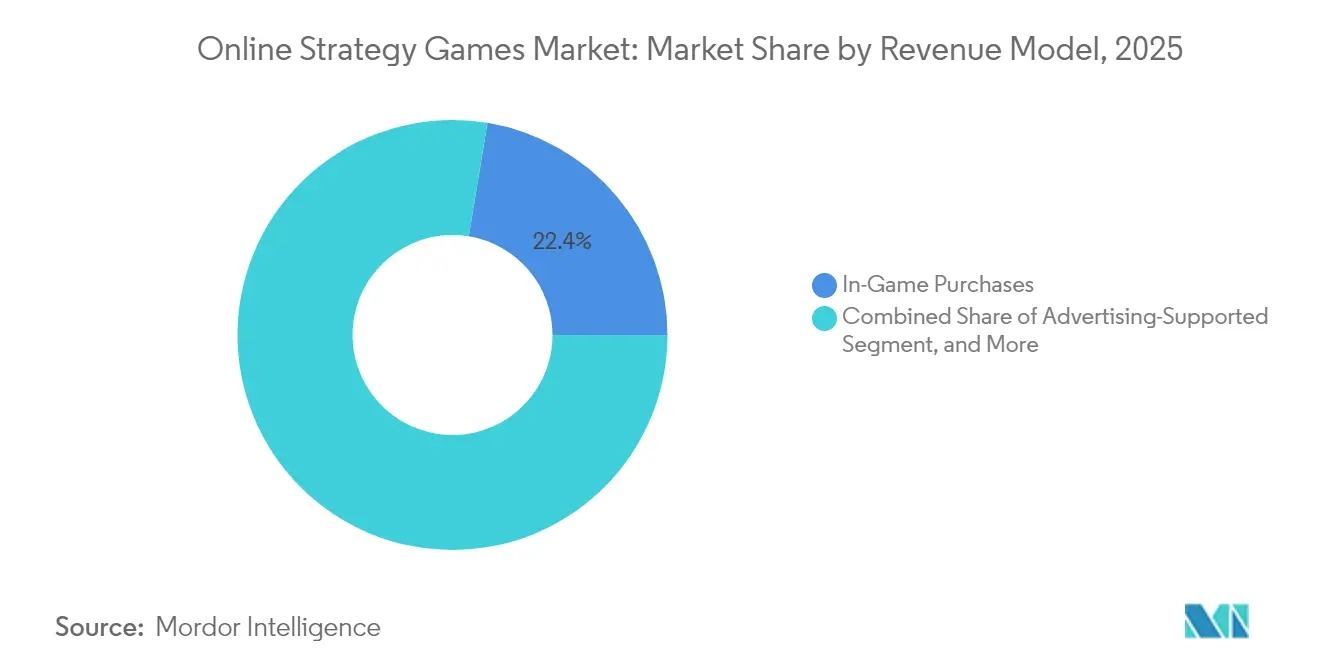

- By revenue model, in-game purchases captured 22.40% in 2025 in the online strategy games market; subscriptions are expected to advance at a 9.82% CAGR to 2031.

- By player mode, MMO/4X titles held 40.20% in 2025 in the online strategy games market, whereas esports-focused releases are projected to escalate at 10.11% CAGR through 2031.

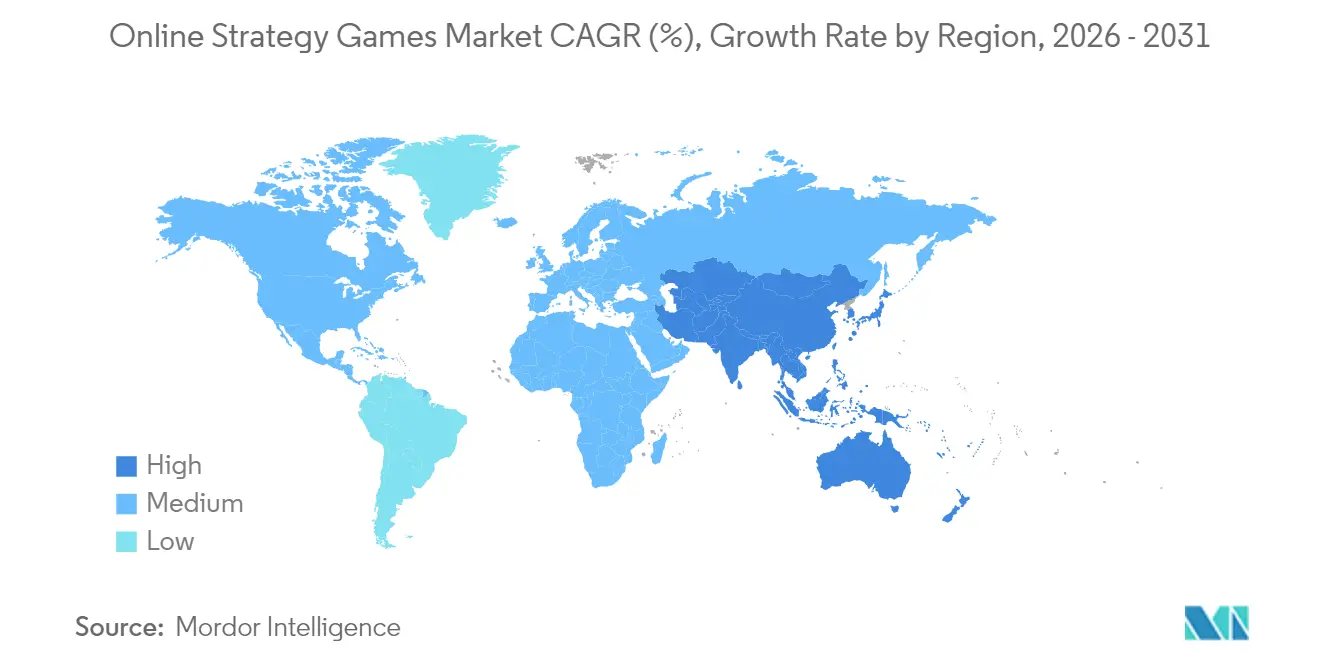

- By geography, North America retained 39.30% of 2025 sales in the online strategy games market, but Asia-Pacific is poised for a 9.95% CAGR, outpacing all other regions.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Online Strategy Games Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cloud-native distribution lowering entry barriers | +1.8% | Global, with stronger impact in North America and Europe | Medium term (2-4 years) |

| 5G rollouts enabling low-latency mobile RTS | +2.1% | APAC core, spill-over to North America and Europe | Long term (≥ 4 years) |

| Esports monetization expanding real-time strategy viewership | +1.4% | Global, concentrated in North America, Europe, APAC | Medium term (2-4 years) |

| Generative-AI tools cutting content-update costs | +1.9% | Global, early adoption in North America and Europe | Short term (≤ 2 years) |

| Cross-play engines broadening addressable base | +1.3% | Global, with emphasis on mobile-PC integration | Medium term (2-4 years) |

| Rising VC funding for mid-core mobile strategy titles | +1.1% | North America and Europe primarily, expanding to APAC | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Cloud-Native Distribution Lowering Entry Barriers

Cloud delivery removes hardware and retail constraints, enabling a flood of new titles and allowing smaller studios to reach global audiences without a physical footprint.[2]Gcore, “How AI Is Transforming Gaming Experiences,” Gcore, gcore.com Over 15,000 browser-based strategy games launched in H1 2025, a 4.9-fold increase versus H1 2023, demonstrating how low entry costs energize creative competition. Unity’s 55% share of browser development underscores middleware’s role in accelerating launch cycles. Platform providers such as Amazon GameLift Streams extend scalable back-end services, letting developers prioritize gameplay innovation over server maintenance. Regulatory fragmentation, however, means compliance requirements vary widely, demanding legal vigilance across jurisdictions.

5G Rollouts Enabling Low-Latency Mobile RTS

Commercial 5G deployments have cut end-to-end lag to 70–100 ms, while 5G-A test networks show 5–10 ms radio latency and 100 Mbps downlink potential. These parameters allow console-grade real-time strategy experiences on smartphones and tablets, especially in Asia-Pacific where mobile-first adoption dominates. Edge facilities shorten data paths, preserving frame-sync integrity for competitive play. The performance leap expands addressable demographics among users lacking high-end PCs, although operators must still manage variable indoor coverage and data tariffs that influence session length.

Esports Monetization Expanding Real-Time Strategy Viewership

Esports revenue streams now span ticketing, sponsorships, in-client item sales, and media rights, shifting reliance away from publisher-run leagues. Brands such as Mercedes-Benz and Mastercard sponsor tournaments, widening exposure for strategy titles. Fnatic’s EUR 5.91 million 2023 digital-item takings, up 121% year-on-year, showcase scalable, high-margin income channels. Tournament APIs enable developers to automate bracket management, while Web3 assets promise future pathways for fan engagement subject to regulatory clarity.

Generative-AI Tools Cutting Content-Update Costs

Microsoft’s Muse model illustrates AI’s capacity to generate contextual map layouts and mission scripts on demand. Industry surveys indicate 49% of studios adopt generative AI, citing shorter art-pipeline loops and personalized narratives that sustain daily active users. Edge inference solutions from providers like Gcore achieve sub-50 ms response, enabling real-time AI adaptation during competitive matches. Intellectual-property protection remains critical; studios therefore implement process controls to avoid dataset contamination and mitigate legal exposure under emerging global AI policy regimes.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising user-acquisition (UA) CPMs post-IDFA privacy changes | -1.6% | Global, concentrated impact in North America and Europe | Short term (≤ 2 years) |

| App-store policy fees squeezing developer margins | -1.2% | Global, particularly affecting mobile-first developers | Medium term (2-4 years) |

| Cloud-gaming bandwidth throttling in emerging markets | -0.8% | Emerging markets in South America, MEA, and rural APAC regions | Long term (≥ 4 years) |

| Deep-fake and botting risks eroding competitive integrity | -0.7% | Global, with heightened impact in esports-focused markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising User-Acquisition CPMs Post-IDFA Privacy Changes

Apple’s identifier-for-advertisers deprecation raised CPMs and diluted targeting precision, complicating recoupment of long-tail lifetime values prevalent in strategy genres. Studios respond by reinforcing first-party data collection, via opt-in gameplay telemetry, and by adopting contextual ad placements anchored to genre affinity. Scale remains vital; without large user cohorts the statistical power of these alternative approaches diminishes, keeping acquisition costs elevated in the near term.

App-Store Policy Fees Squeezing Developer Margins

Standard 30% commissions on in-app payments erode profitability, particularly for free-to-play titles reliant on high-frequency micro-transactions. Legislative scrutiny under the EU Digital Markets Act has initiated fee-reduction debates, yet practical relief could lag until 2026 or later. To mitigate exposure, publishers test progressive-web-app distribution and cloud gaming gateways, but user-onboarding friction outside centralized stores still restricts near-term reach.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Genre: RTS Leadership Confronts Auto-Battler Momentum

Real-time strategy titles represented 58.10% of 2025 revenue, an outperformance anchored by evergreen franchises and spectator-friendly esports ecosystems. Auto-battler innovation, however, is pulling new demographics through accessible mechanics and shorter match loops, giving the sub-category a forecast 10.36% CAGR. Players migrate fluidly across genres, prompting developers to blend real-time decision loops with auto-resolved combat modules that conserve session time without sacrificing depth. Successful hybrids can tap both hardcore and casual cohorts, broadening lifetime value and diversifying competitive metas. The online strategy games market therefore witnesses experimental genre convergence as studios apply AI-driven procedural systems to prototype new archetypes rapidly, reinforcing pipeline agility while mitigating budget risk.

Second-order effects include a rising e-commerce aftermarket for cosmetic assets that transcend individual genres, reinforcing monetization through interoperable skins and avatars. RTS publishers, meanwhile, leverage cross-progression between PC and cloud platforms to anchor their installed bases. Auto-battler startups exploit lightweight mobile builds to reach emerging economies, using low-bandwidth footprints and regional language packs to accelerate adoption. Provided regulatory guardrails on loot boxes remain stable, both segments expect incremental spend-per-paying-user to hold above mid-single-digit USD levels through 2030.

By Platform: Mobile Scale Faces Cloud Gaming Acceleration

Mobile captured 47.10% in 2025 on the back of high smartphone penetration and intuitive touch controls, confirming the device’s position as the primary on-ramp to the online strategy games market. Yet cloud gaming’s 10.21% projected CAGR indicates shifting infrastructure economics: low-powered devices gain access to high-fidelity titles without discrete GPUs. Operators combine adaptive bitrate streaming with instant-resume state management to remove patch downloads, shrinking churn associated with friction at first launch. Developers build control-scheme abstraction layers to support controller, keyboard-mouse, and gesture input concurrently, reinforcing cross-play viability.

Browser games, fueled by WebAssembly and WebGPU, collected more than 15,000 launches in H1 2025; they illustrate how zero-install access counters app-store fees while aiding global reach. PC and console remain staples for competitive ladders that mandate precision inputs, with multi-monitor data overlays giving high-skill players marginal advantages. The platform mix is therefore fluid: consumer loyalty fragments across devices, challenging publishers to optimize social graphs, leaderboards, and virtual-economy sync in near real-time.

By Revenue Model: Subscriptions Rise Amid In-Game Purchase Dominance

In-game purchases held 22.40% in 2025, cementing their status as the economic backbone for free-to-play design. Subscriptions, expected to rise at 9.82% CAGR, appeal to cost-conscious players who value predictable spending and bundled content libraries. Xbox Game Pass’s target of USD 5.5 billion 2025 revenue exemplifies how tiered membership tiers can fund AAA development while spreading risk across multiple releases. Hybrid monetization prevails; operators weave battle-passes and item shops into subscription frameworks, capturing both whales and mid-tail spenders.

Advertising support intensifies within mid-core mobile strategy games through rewarded videos and playable ads that preserve immersion. Premium pay-once models persist mainly among niche 4X and grand-strategy audiences who emphasize mod support and offline play. Regulatory inquiry into randomized loot tables continues to encourage transparent, direct-sale mechanics, pushing studios to disclose rarity odds and cap spending to retain compliance.

By Player Mode: MMO Stability Meets Esports Upswing

MMO/4X modes maintained a 40.20% slice in 2025, leveraging persistent worlds that foster long-run retention via guild structures and territorial competition. Esports-oriented formats look to a 10.11% CAGR, buoyed by infrastructure improvements such as automated anti-cheat and global spectator servers. Developers are embedding tournament APIs at launch, enabling community organizers to host seasonal circuits without publisher intervention.

Cross-play is widening player pools, lowering queue times, and boosting matchmaking accuracy, yet it requires identical balance patches across all clients, raising coordination overhead. Meanwhile, single-player campaigns exploit AI companions to deliver dynamic narrative arcs, enhancing perceived value for time-scarce users. Asynchronous multiplayer remains attractive in bandwidth-limited markets, offering strategic depth without concurrency requirements.

Geography Analysis

North America’s leadership in the online strategy games market stems from sophisticated payment rails that support diverse monetization, from premium purchases to recurring passes, while esports arenas in Los Angeles and Dallas act as broadcast hubs for global tournaments. Cloud-infrastructure ownership by U.S. hyperscalers grants developers direct access to scalable GPU clusters, accelerating iterative live-ops cycles. Regulatory focus on antitrust within digital storefronts signals possible commission relief but introduces legal uncertainty that may delay investment decisions.

Asia-Pacific’s acceleration reflects a convergence of factors: China’s regulatory stabilization after prior licensing freezes, the popularity of mobile-first strategy titles, and state-backed esports infrastructure expansion. Domestic studios refine cultural localization, enabling titles to resonate in Southeast Asia while preserving monetization hooks optimized for WeChat Pay and Alipay. Japanese publishers leverage strong character IP and cross-media partnerships to differentiate amidst rising domestic competition, whereas South Korean firms pioneer 5G-native cloud releases with integrated broadcast overlays.

European developers navigate GDPR restrictions by deploying on-device analytics and explicit consent flows. Established PC modding communities in Germany and Poland cultivate long-tail engagement for grand-strategy titles. Middle Eastern sovereign-wealth funds invest in esports venues, eyeing tourism spill-overs, while African telecom operators bundle low-cost data passes for mobile games. South America’s dominant markets such as Brazil observe growing export potential for locally themed strategy content, although high import tariffs on gaming hardware constrain console adoption.

Competitive Landscape

The online strategy games market exhibits moderate concentration as tech conglomerates pursue vertical integration while independent studios gain traction through cloud distribution. Microsoft’s post-merger portfolio now spans server infrastructure, subscription distribution, and marquee franchises; its USD 5.5 billion Game Pass revenue target for 2025 illustrates diversified monetization. Disney’s USD 1.5 billion stake in Epic Games underscores entertainment-gaming convergence that threatens traditional publisher gatekeepers.

AI adoption differentiates competitors by cutting dev-cycle times; studios that integrate model-as-a-service pipelines accelerate content drops and maintain retention peaks. Cloud-native newcomers sidestep legacy engine constraints, releasing iterative season updates without client downloads. Conversely, established publishers wield large compliance teams that tackle global age-rating, privacy, and loot-box laws, sustaining advantage in regulated regions.

Browser-based entrants capitalize on low acquisition costs, leveraging social-media virality rather than paid installs. Still, network effects favor incumbents that operate cross-IP meta-platforms offering unified identity and wallet services. The competitive landscape will therefore reward firms capable of synchronizing content, infrastructure, and community ecosystems while managing multicultural regulatory demands.

Online Strategy Games Industry Leaders

Mircosoft Coroporation

Paradox Interactive AB (publ)

Take-Two Interactive Software, Inc.

Relic Entertainment Inc.

Amplitude Studios SAS

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Disney invested USD 1.5 billion in Epic Games to co-create interconnected entertainment and gaming experiences.

- December 2024: Tencent acquired Kuro Games, augmenting its competitive mobile portfolio.

- November 2024: Microsoft integrated Activision Blizzard IP into Xbox Game Pass, adding Call of Duty to the subscription catalog.

- October 2024: Playtika purchased SuperPlay for USD 700 million, expanding into casual strategy.

Global Online Strategy Games Market Report Scope

Strategy games focus on gameplay that requires clever long-term planning. Most strategy games provide a top-down view of the world where players can control buildings and units. The classic civilization game by Sid Meier, where players start in a small primitive village and move on to a more technologically advanced society, is a perfect example of this category. The Clash of Clans, where players can build towns online and attack other players' towns, is also a big hit on mobile devices.

The online strategy games market is segmented by type (advertising, in-app purchase, paid app), by geography (North America [United States, Canada], Europe [Germany, United Kingdom, France, Russia, Spain, Italy, Rest Of Europe], Asia-Pacific [China, Japan, South Korea, Rest Of Asia-Pacific], Latin America [Brazil, Argentina, Mexico, Rest Of Latin America], Middle East And Africa [United Arab Emirates, Saudi Arabia, Iran, Egypt, Rest of the Middle East and Africa]). The market sizes and forecasts are provided in terms of value in (USD) for all the above segments.

| Real-Time Strategy (RTS) |

| Turn-Based Strategy (TBS) |

| 4X / Grand Strategy |

| Tower-Defense and Auto-Battler |

| PC |

| Mobile |

| Console |

| Browser-based |

| Cloud Gaming |

| In-Game Purchases |

| Advertising-Supported |

| Subscription / Battle-Pass |

| Premium (Paid Download) |

| Hybrid |

| Single-Player |

| Asynchronous Multiplayer |

| Real-Time Multiplayer |

| Massively Multiplayer Online (MMO/4X) |

| Esports-Focused |

| North America | United States | |

| Canada | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Netherlands | ||

| Spain | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Mexico | ||

| Rest of South America | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Genre | Real-Time Strategy (RTS) | ||

| Turn-Based Strategy (TBS) | |||

| 4X / Grand Strategy | |||

| Tower-Defense and Auto-Battler | |||

| By Platform | PC | ||

| Mobile | |||

| Console | |||

| Browser-based | |||

| Cloud Gaming | |||

| By Revenue Model | In-Game Purchases | ||

| Advertising-Supported | |||

| Subscription / Battle-Pass | |||

| Premium (Paid Download) | |||

| Hybrid | |||

| By Player Mode | Single-Player | ||

| Asynchronous Multiplayer | |||

| Real-Time Multiplayer | |||

| Massively Multiplayer Online (MMO/4X) | |||

| Esports-Focused | |||

| By Geography | North America | United States | |

| Canada | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Netherlands | |||

| Spain | |||

| Italy | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| South Korea | |||

| India | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Argentina | |||

| Mexico | |||

| Rest of South America | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How large is the online strategy games market in 2026?

The online strategy games market size reached USD 23.45 billion in 2026 and is forecast to USD 36.74 billion by 2031 at a 9.39% CAGR.

Which genre leads revenues within online strategy titles?

Real-time strategy maintained a 58.10% share in 2025, remaining the largest genre.

What platform is growing fastest for strategy games?

Cloud gaming is projected to expand at 10.21% CAGR through 2031, outpacing all other platforms.

Which revenue model is gaining traction?

Subscriptions are the fastest-growing monetization model, expected to rise at 9.82% CAGR.

Which region will add the most new spending by 2031?

Asia Pacific is forecast for a 9.95% CAGR, placing it as the leading contributor to incremental revenue.

Page last updated on: